Public Safety Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

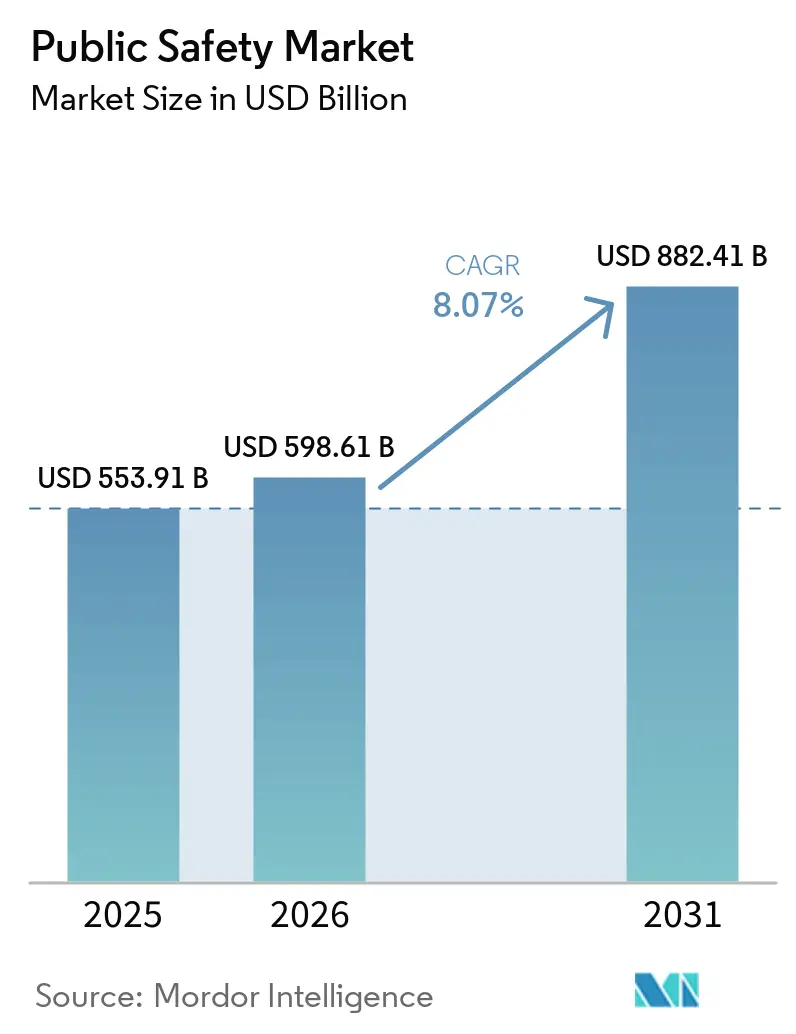

| Market Size (2026) | USD 598.61 Billion |

| Market Size (2031) | USD 882.41 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

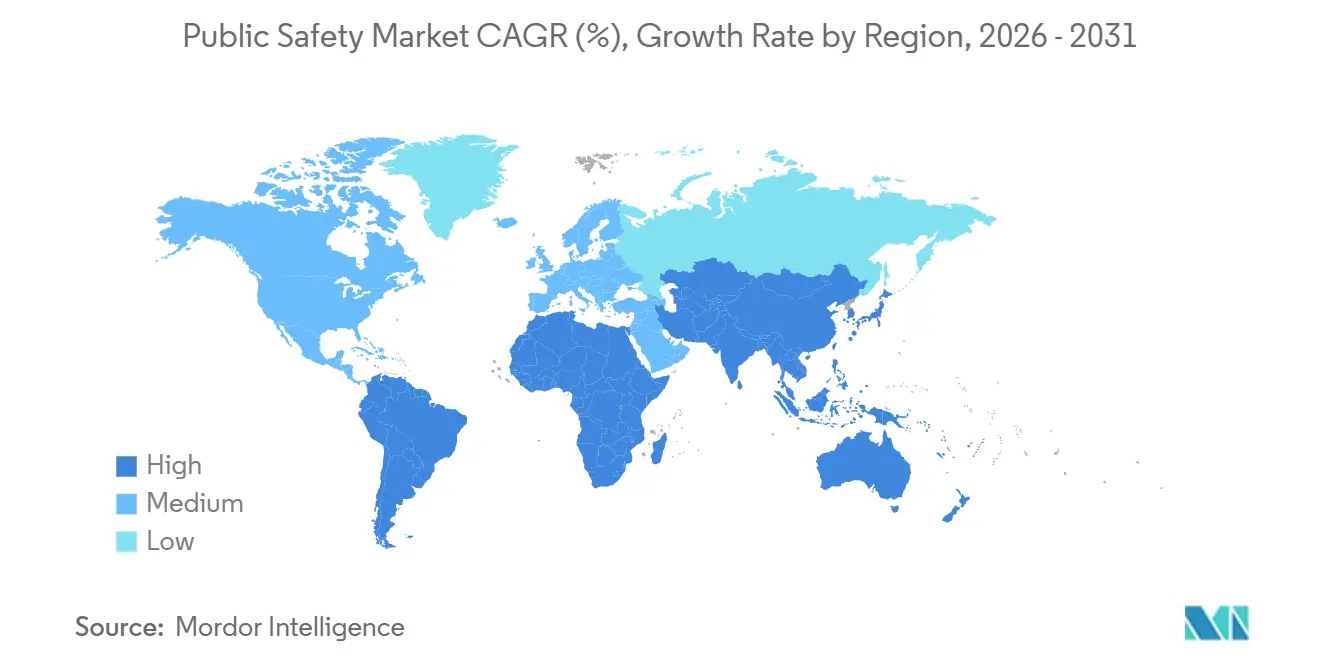

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

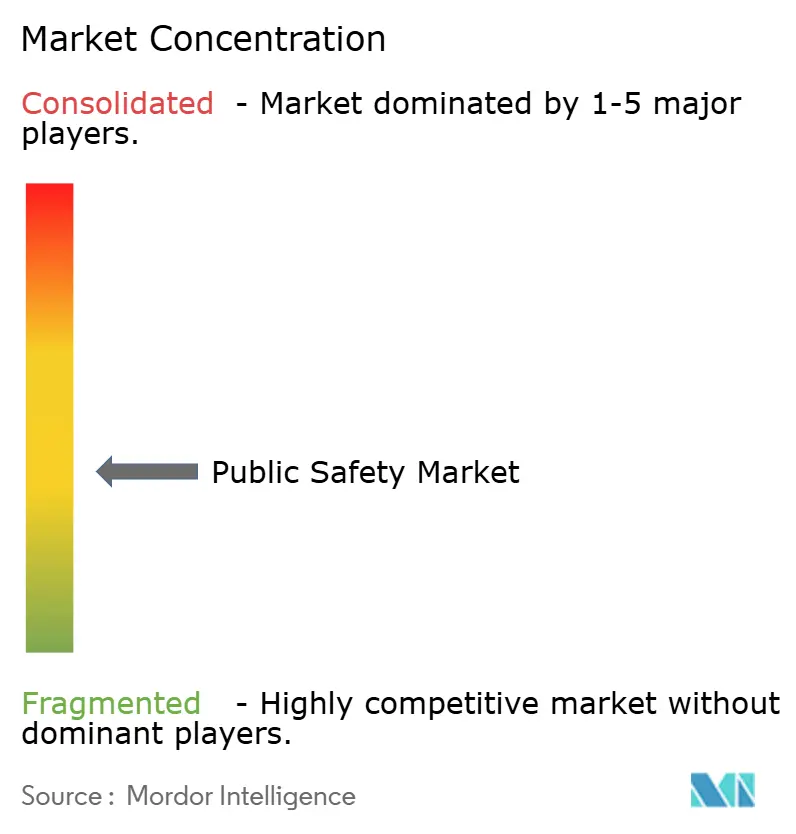

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Public Safety Market Analysis by Mordor Intelligence

The public safety market size is projected to expand from USD 553.91 billion in 2025 and USD 598.61 billion in 2026 to USD 882.41 billion by 2031, registering a CAGR of 8.07% between 2026 to 2031. Momentum is accelerating as agencies shift budget away from stand-alone land-mobile radio toward cloud-centric command platforms that blend broadband connectivity, edge analytics, and artificial intelligence. Smart-city programs, disaster-resilience mandates, and new mid-band spectrum allocations are widening the addressable base for integrated voice, video, and data solutions. Vendors that combine broadband network assets with software and managed services are moving fastest, compressing refresh cycles for legacy narrowband systems. Capital expenditure is strongest in the United States, China, India, and Japan, yet price-performance improvements in satellite and 5G radios expand coverage for rural and maritime responders, broadening the total number of reachable users across the public safety market.

Key Report Takeaways

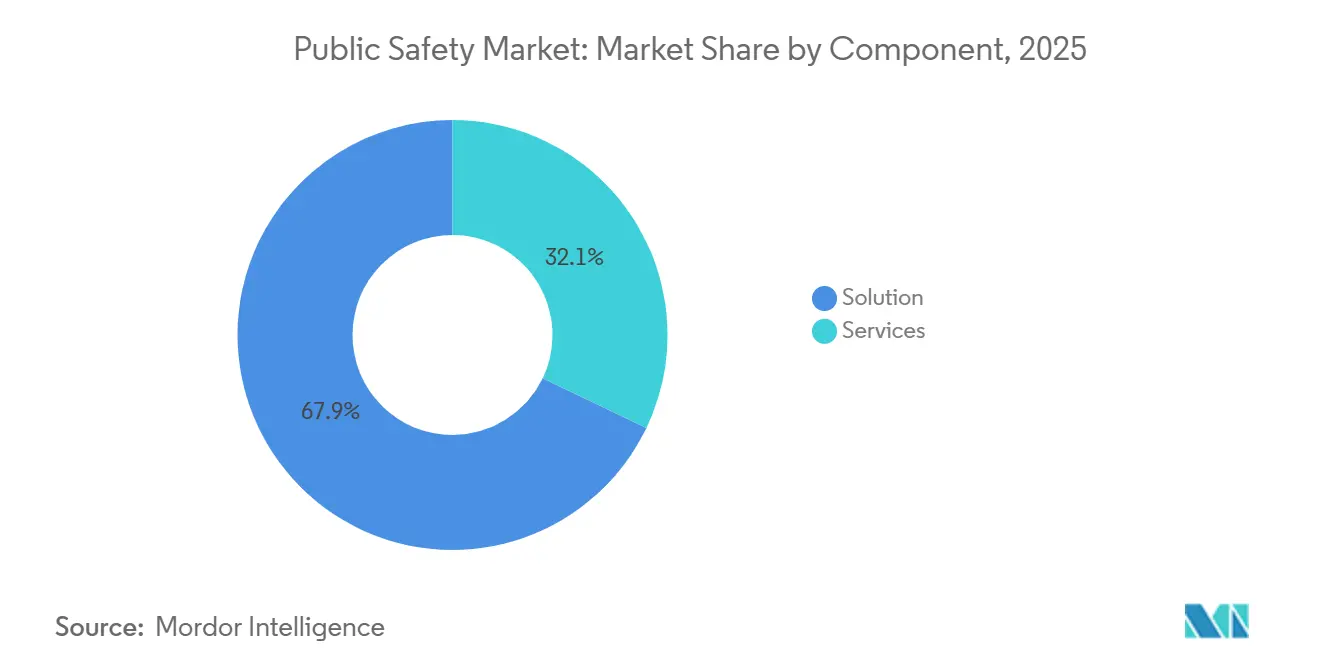

- By component, solutions led with 67.89% of public safety market share in 2025, while services are forecast to expand at an 8.22% CAGR through 2031.

- By deployment type, on-premises installations accounted for 71.33% of the public safety market in 2025, and cloud-enabled architectures are projected to grow at an 8.29% CAGR between 2026-2031.

- By end-user vertical, law enforcement agencies commanded 47.56% of public safety market revenue in 2025; disaster and rescue management authorities have the fastest outlook, with a 9.23% CAGR to 2031.

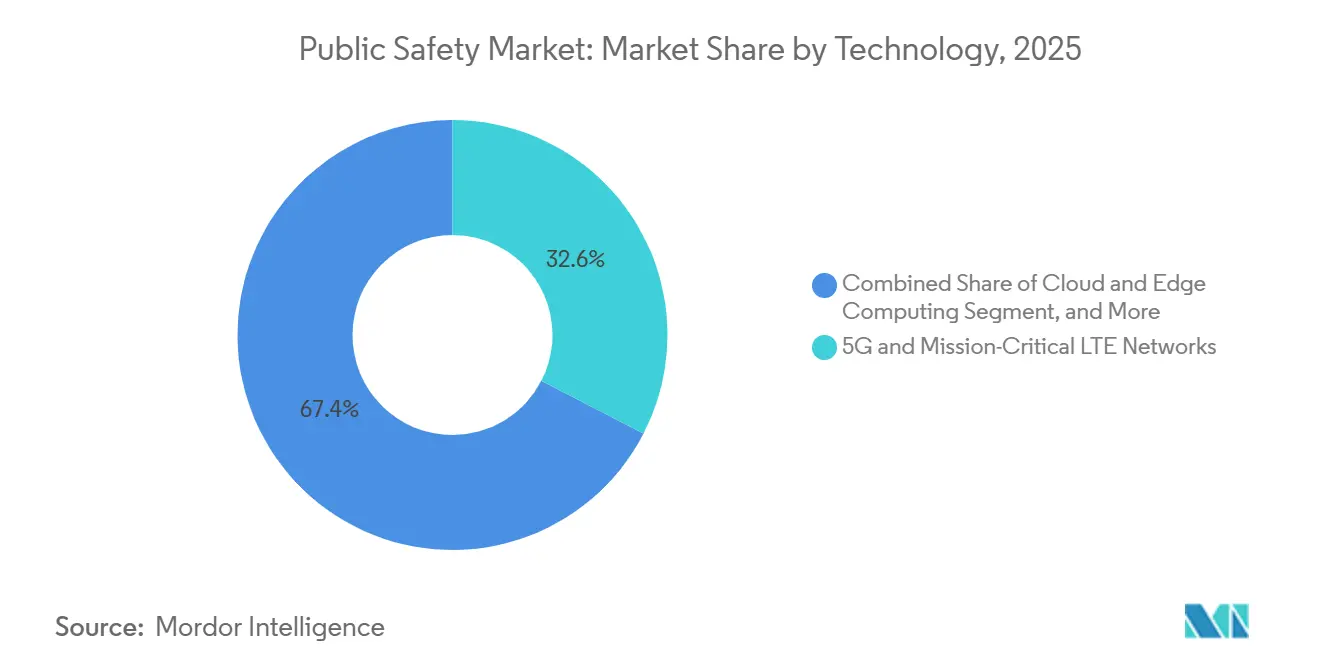

- By 2025, 5G and mission-critical LTE networks captured 32.58% of the public safety market share, whereas artificial intelligence and predictive analytics are poised for a 9.11% CAGR over 2026-2031.

- By agency type, state and provincial bodies represented 42.39% of public safety market spending in 2025, and municipal and local agencies are expected to register an 8.63% CAGR during 2026-2031.

- By geography, North America generated 38.44% of global public safety market revenue in 2025, while Asia-Pacific is projected to expand at a 9.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Public Safety Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated Transition from Legacy LMR to 4G/5G Mission-Critical Broadband Networks Across Public Safety Agencies | +2.1% | Global, with concentrated deployment in North America, Western Europe, and Asia-Pacific urban corridors | Medium term (2-4 years) |

| Smart City Programs Scaling Real-Time Video Surveillance and Situational Awareness Platforms | +1.8% | Asia-Pacific core (China, India, Singapore), spillover to Middle East (UAE, Saudi Arabia) and select South American metros | Medium term (2-4 years) |

| Heightened Frequency and Severity of Climate-Related Disasters Increasing Emergency Response Spending | +1.5% | North America (wildfire, hurricane zones), Europe (flood-prone basins), Asia-Pacific (typhoon corridors), Australia | Long term (≥ 4 years) |

| Rising Geopolitical Tensions Pushing Defense and Homeland Security Budgets for Integrated Command-and-Control Centers | +1.3% | North America, Europe (NATO members), Middle East, East Asia (South Korea, Japan) | Short term (≤ 2 years) |

| Real-Time Satellite IoT Connectivity Unlocking Coverage in Rural and Maritime Emergency Zones | +0.9% | Global, with early gains in North America rural counties, Nordic regions, maritime Southeast Asia, Latin America remote areas | Long term (≥ 4 years) |

| Energy-Resilient Microgrid Deployment for Disaster-Proof Public Safety Facilities | +0.5% | North America (California, Texas, Puerto Rico), Asia-Pacific island nations, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandated Transition from Legacy LMR to 4G-5G Broadband Networks

FirstNet’s USD 6.3 billion nationwide 5G overlay, completed in 2024, enabled full-motion video, biometric uploads, and mission-critical push-to-talk that narrowband Project 25 channels cannot handle. The United Kingdom’s Emergency Services Network, although delayed, reinforces the inevitability of broadband migration as 300,000 responders prepare to leave TETRA handsets for 4G service once rural coverage gaps close. With 3GPP Release 17, devices from multiple vendors can share quality-of-service slices that guarantee sub-100-millisecond latency during congestion, reducing vendor lock-in risk for agencies. Complementary spectrum awards, such as the FCC’s mid-band allocation in July 2025, further expedite rollouts by ensuring contiguous blocks for Band 14 upgrades.[1]Federal Communications Commission, “FCC Allocates Additional Mid-Band Spectrum for Public Safety,” fcc.gov Collectively, these measures accelerate refresh cycles, making broadband conversion the largest single uplift to spending in the public safety market.

Smart-City Programs Scaling Real-Time Video Surveillance and Situational Awareness

China’s Safe City initiative now exceeds 600 million networked cameras that stream high-definition video to AI hubs for license-plate matching, crowd counting, and anomaly alerts. India’s Smart Cities Mission earmarked INR 48,000 crore (USD 5.8 billion) for 100 command centers that fuse traffic sensors, 911-style calls, and municipal CCTV on shared dashboards.[2]Ministry of Housing and Urban Affairs, “Smart Cities Mission,” smartcities.gov.in Saudi Arabia’s USD 500 billion NEOM project embeds 5G coverage and predictive policing into its basic infrastructure, signaling that greenfield cities bake public-safety analytics into their design rather than retrofit. Municipalities contract with managed service providers to operate these massive data estates, pushing recurring software revenue ahead of hardware revenue. Privacy regimes such as the California Consumer Privacy Act lengthen procurement timelines but also steer vendors toward consent logs and on-device redaction, adding defensible differentiation.

Heightened Frequency and Severity of Climate-Related Disasters Increasing Emergency Response Spending

FEMA disaster declarations climbed 23% year over year in 2025, unlocking USD 2.2 billion for microgrids, satellite backhaul, and sensor-rich early-warning networks that strengthen communications resilience.[3]Federal Emergency Management Agency, “Disaster Relief Grants and Funding 2025,” fema.gov ALERTCalifornia’s 1,800 high-definition wildfire cameras, coupled with AI smoke recognition, cut detection time from hours to minutes, saving an estimated 200 lives during the 2025 season. NOAA disbursed USD 575 million in coastal-resilience grants that funded surge sensors and redundant fiber links across the Gulf and Mid-Atlantic regions. Japan’s earthquake early-warning broadcast, proven during the March 2025 Fukushima tremor, triggered train shutdowns seconds before ground shaking, underscoring the life-saving value of ultra-low-latency alerts. As extreme weather becomes more common, multiyear capital plans now bundle predictive analytics, hardened power, and multi-bearer connectivity, deepening the public safety market’s addressable spend.

Rising Geopolitical Tensions Pushing Defense and Homeland Security Budgets for Integrated Command Centers

Canada’s CAD 38.6 billion (USD 28.5 billion) NORAD modernization funds will fund next-generation radar and satellite early-warning systems that also feed provincial emergency dashboards. South Korea’s Army Tactical Command Information System upgrade integrates battlefield telemetry with civilian 119 dispatch platforms, enabling responders to share a common operating picture during border incidents. The United Arab Emirates opened a national operations center in 2025 that aggregates cyber, border, and infrastructure sensors into a single AI-driven console, shortening threat-identification cycles. NATO members are accelerating similar fusions of civilian and defense feeds to address hybrid threats, raising demand for hardened networks and multi-classification data fabrics. As regional flashpoints persist, homeland security agencies allocate a higher percentage of defense budgets to interoperable public-safety technology, sustaining above-trend growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front CAPEX and Long Procurement Cycles Limiting Adoption in Cash-Strapped Municipalities | -1.2% | Global, with acute pressure in South America, Africa, and rural North America counties | Short term (≤ 2 years) |

| Fragmented Radio Spectrum Governance Hindering Interoperability Between Agency Networks | -0.9% | Europe (27 EU member states), Asia-Pacific (varied national allocations), Africa | Medium term (2-4 years) |

| Rising Public Scrutiny and Data-Privacy Regulations Slowing Deployment of Facial-Recognition Surveillance | -0.7% | North America (CCPA jurisdictions), Europe (GDPR enforcement), select Asia-Pacific markets | Short term (≤ 2 years) |

| Shortage of Certified Mission-Critical Network Installers Delaying Rural Deployments | -0.4% | North America rural counties, Europe periphery, Asia-Pacific tier-2 and tier-3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front CAPEX and Long Procurement Cycles Limiting Adoption in Cash-Strapped Municipalities

A 2024 Government Accountability Office study shows that the average radio-system replacement takes 7 to 10 years, with cost overruns averaging 18% due to scope creep and vendor change orders. The Congressional Budget Office estimates coastal counties need USD 400 billion through 2040 just to climate-harden emergency infrastructure, a figure far beyond typical discretionary budgets. While U.S. federal grants, such as the COPS and Homeland Security Program channels, provide USD 1.2 billion annually, complex applications and matching-fund requirements exclude many rural jurisdictions. Subscription software partially eases upfront costs, yet strict data-residency mandates can force agencies back to capital-intensive on-premises builds. Consequently, cash-constrained municipalities often defer upgrades, damping near-term unit sales even when the long-run total cost of ownership favors modernization.

Fragmented Radio Spectrum Governance Hindering Interoperability Between Agency Networks

Europe’s 27 member states split public-safety broadband across 380-390 MHz, 700 MHz, and other local bands, forcing responders to carry multi-band radios or deploy gateways, which raise costs and complexity. The FCC’s Band 14 assignment demonstrates the benefit of national harmonization, yet tribal lands and certain U.S. federal enclaves still occupy incompatible blocks, leaving gaps in mutual-aid coverage. 3GPP Release 17 ratifies mission-critical services over 5G, but agencies delay orders until field-proven handsets and slice orchestration are available in volume. Industry guidelines from APCO International call for standardized APIs and encryption, though adoption remains voluntary and is expected to extend into the 2030s. Until regulators align and vendors converge on common profiles, interoperability challenges will continue to subtract from growth in the public safety market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Scale While Solutions Retain The Majority Share

Solutions accounted for 67.89% of the public safety market share in 2025, reflecting the capital-intensive nature of critical communication networks, surveillance cameras, and biometric readers. Within that slice, broadband base stations represented the largest ticket item because nationwide overlays, such as FirstNet’s USD 6.3 billion 5G build in the United States, required dense site deployments. Surveillance and video-analytics suites followed close behind, buoyed by China’s 600 million-camera Safe City footprint. Biometric authentication, exemplified by India’s Aadhaar platform, is growing as border and access-control agencies converge on multi-factor identity checks. These hardware-anchored orders anchor the current revenue mix but carry multiyear refresh intervals that vendors seek to shorten with embedded software upgrades.

The services category, which accounted for the remaining 32.11% of the public safety market in 2025, is projected to post an 8.22% CAGR through 2031 as agencies outsource network maintenance and software patching. Managed-service bundles that include monitoring, cybersecurity, and analytics tuning now accompany most broadband radio awards, smoothing agency staffing gaps and shifting spend from capital to operating lines. Evidence-management subscriptions, such as Axon’s Draft One report-automation engine, add recurring revenue on top of body-camera hardware. System-integration consultancies also gain ground because multi-vendor ecosystems demand project coordination. As municipalities adopt outcome-based contracts that link payments to uptime and response metrics, the services slice will account for an increasingly larger share of incremental growth in the public safety market.

By Deployment Type: On-Premise Dominance Persists, But Hybrid Cloud Advances

On-prem implementations accounted for 71.33% of the public safety market share in 2025, driven by data-residency statutes and the sub-200-millisecond response times required for computer-aided dispatch. European Union General Data Protection Regulation clauses oblige agencies to keep personal data inside national borders, which steers many computer-aided dispatch and records systems toward local data centers. Similar constraints in California and other U.S. states reinforce the preference. Latency also matters because emergency call takers cannot tolerate jitter when querying warrants or medical records. As a result, agencies often refresh on-site servers alongside radio upgrades, elongating replacement cycles but assuring deterministic performance.

Cloud and hybrid models are gaining traction for less latency-sensitive workloads, fueling an 8.29% CAGR for cloud deployments between 2026-2031. Vendors now deliver edge appliances that cache active incidents locally while archiving video and analytics to public cloud object stores, bridging compliance with scalability. CentralSquare’s hybrid dispatch platform and Everbridge’s cloud-native mass-notification suite illustrate the blended architecture many cities now favor. Subscription pricing lightens upfront budgets and automatically rolls in security patches, helping smaller counties leapfrog older hardware. As more states publish zero-trust blueprints and FedRAMP-equivalent frameworks, hybrid cloud is poised to expand its share of the public safety market without displacing mission-critical on-premises cores.

By End-User Vertical: Disaster Management Authorities Accelerate Amid Climate Stress

Law enforcement agencies accounted for 47.56% of public safety market revenue in 2025, driven by body-worn camera mandates and real-time crime centers that require constant refresh. Spending includes broadband modems embedded in patrol vehicles, AI video analytics, and upgraded evidence lockers. Fire departments, the second-largest consumer, are expanding thermal-imaging drone fleets and mesh radios to maintain signal in urban canyons and underground tunnels. Emergency medical services use telemedicine consoles that transmit patient vitals over 5G, reducing door-to-balloon time for cardiac cases. Transportation and critical infrastructure operators deploy analytics that flag track intrusions and substation breaches, thereby widening the addressable base.

Disaster and rescue management authorities are expected to post the fastest growth, at a 9.23% CAGR through 2031, driven by longer wildfire seasons, heavier floods, and more frequent hurricanes. ALERTCalifornia’s smoke-detection cameras, NOAA surge sensors, and Japanese earthquake early-warning feeds demonstrate the life-saving value of sensor fusion. These agencies buy rugged satellite radios, microgrid power backups, and cloud dashboards that handle high event surges. Grant programs earmarked for climate resilience guarantee multiyear capital flows, cushioning economic downturns. As natural hazards intensify, the disaster vertical is set to capture a growing share of the public safety market while catalyzing cross-agency data-sharing standards.

By Technology: Broadband Radio Leads Revenue, AI Leads Growth

5G and mission-critical LTE infrastructure represented 32.58% of public safety market share in 2025, buoyed by national broadband overlays that bundle base stations, ruggedized user equipment, and evolved packet cores. These investments lay the transport foundation for advanced applications yet entail heavy capital that peaks early in rollout cycles. Satellite IoT gateways and mesh extensions complement terrestrial cells, expanding coverage in rural and maritime areas. Internet-connected sensors for air quality, bridge stress, and flood waters channel vast amounts of telemetry into command centers, increasing data analytics workloads.

Artificial intelligence and predictive analytics are on a strong trajectory, with a 9.11% CAGR from 2026-2031, as agencies look beyond connectivity toward operational efficiency. Body-camera streams now auto-generate incident transcripts, and AI smoke recognition trims wildfire detection from hours to minutes. Predictive resource-allocation engines cut ambulance idle time and guide patrol placement. Cloud and edge computing converge as vendors push processing close to cameras to minimize bandwidth. Privacy concerns prompt suppliers to ship explainability kits and on-device redaction, features that further differentiate AI offerings. Together, broadband transport and intelligent analytics form a virtuous loop that underpins the expansion of the public safety market.

By Agency Type: Municipal Buyers Outpace State Programs As Grants Devolve

State and provincial bodies accounted for 42.39% of public safety market spending in 2025, as they operate statewide radio systems and coordinate multi-county incident response. Their budgets fund core radio towers, master sites, and next-generation 911 routing, all of which carry high per-site costs. These agencies typically negotiate decade-long service contracts, giving incumbents a predictable revenue stream but slowing competitive churn. Federal and national entities, though smaller in share, procure specialized gear with hardened security profiles to support intelligence and classified communications.

Historically constrained municipal and local departments are now the fastest movers, with an expected 8.63% CAGR through 2031. Federal and state grants encourage county clusters to pursue interoperable systems together, stretching dollars and boosting procurement clout. Cities embed cameras in streetlights, place FirstNet small cells on water towers, and adopt cloud records systems that bill monthly rather than all at once. The shift pulls software-centric entrants into bids once dominated by radio stalwarts. As community oversight boards demand transparency and data-driven policing, municipal users pilot analytics dashboards that elevate vendor diversity. This grassroots expansion promises to expand the overall public safety market while pressuring suppliers to tailor their offers for smaller but more numerous contracts.

Geography Analysis

North America contributed 38.44% of global revenue in 2025, anchored by FirstNet’s nationwide 5G build, USD 2.2 billion in FEMA disaster-relief grants, and state-level Next-Generation 911 upgrades. The United States accounts for most of the region’s public safety market, with contracts such as Motorola Solutions’ USD 1.1 billion FirstNet extension and L3Harris’ USD 1.4 billion Air Force award, sustaining near-term equipment demand. Canada’s CAD 38.6 billion (USD 28.5 billion) NORAD modernization and Mexico’s USD 700 million hurricane-resilience network round out capital flows, though overall regional growth moderates as broadband overlay milestones wind down.

Europe held the second-largest slice in 2025, yet fragmented spectrum rules and stringent privacy laws temper expansion. The United Kingdom’s protracted Emergency Services Network migration, France’s biometric-compliance fines, and Italy’s EUR 800 million command-and-control refresh illustrate a patchwork of national timelines that elongate revenue recognition. Despite these hurdles, Germany’s EUR 2.5 billion radio upgrade and cross-border 5G trials indicate untapped scale once harmonized roaming and encryption profiles mature.

Asia-Pacific is projected to expand at a 9.17% CAGR through 2031, the fastest of all regions, driven by China’s 600 million-camera Safe City build and India’s USD 5.8 billion Smart Cities Mission. Japan’s earthquake early-warning backbone, South Korea’s battlefield-to-civilian data fusion, and Singapore’s 100,000-node IoT grid further diversify spending beyond surveillance. Together, these initiatives elevate the region’s public safety market share as urbanization, disaster resilience, and defense imperatives converge, positioning Asia-Pacific to overtake slower-growing mature markets by the end of the forecast window.

Mordor Intelligence provides coverage of the public safety market across other key regional markets, including Europe, Asia, and Latin America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The top five suppliers, Motorola Solutions, Cisco Systems, L3Harris Technologies, Hexagon, and IBM, controlled roughly 35%-40% of 2025 revenue, indicating moderate concentration but ample headroom for challengers. Incumbent radio vendors pivot to software and managed services to offset single-digit growth in hardware, exemplified by Motorola’s 12% video-analytics expansion versus 3% in land-mobile radio. Cisco leverages its enterprise footprint to bundle Meraki cameras and collaboration tools, winning citywide contracts that value single-vendor simplicity.

Cloud-native specialists accelerate disruption by monetizing recurring subscriptions. Axon’s Draft One report-automation suite trims officer paperwork by 30 minutes per shift, while Everbridge’s Critical Event Management platform drives double-digit growth through public cloud mass-notification deals. Tyler Technologies’ USD 2.3 billion acquisition of CentralSquare brought together two municipal software stalwarts, instantly lifting the combined entity’s public safety market share to an estimated 22% in the North American software market.

Telecom equipment makers and satellite operators widen the field as 3GPP Release 17 validates network slicing and multi-bearer continuity. Ericsson and Nokia now court mission-critical broadband tenders once reserved for specialized radio firms, and Iridium Certus’ 1.4 Mbps uplink provides border agents with a fallback coverage. Privacy-by-design features such as Axon Body 4’s on-device redaction and Splunk-infused threat analytics in Cisco’s portfolio serve as competitive tiebreakers, underscoring how regulatory compliance increasingly shapes win rates in the evolving public safety market.

Public Safety Industry Leaders

Cisco Systems Inc.

L3Harris Technologies Inc.

IBM Corporation

General Dynamics Corporation

BlackBerry Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Motorola Solutions signed a USD 450 million agreement with the New York City Police Department to build an AI-enabled real-time crime center that integrates body-camera feeds, license-plate readers, and gunshot sensors.

- January 2026: L3Harris Technologies won a USD 320 million Customs and Border Protection radio contract that includes 50,000 handhelds with satellite fail-over for coverage gaps.

- December 2025: Cisco Systems completed its USD 28 billion acquisition of Splunk to fuse network telemetry with physical-security alerts for faster incident correlation.

- November 2025: Axon launched Body 4 cameras that perform on-device face and plate redaction, trimming post-production time and boosting patrol availability.

Global Public Safety Market Report Scope

The Public Safety Market Report is Segmented by Component (Solution, and Services), Deployment Type (On-Premise, and Cloud), End-User Vertical (Law Enforcement Agencies, Firefighting Departments, Emergency Medical Services, Transportation and Critical Infrastructure Operators, Disaster and Rescue Management Authorities, Other End-User Verticals), Technology (Artificial Intelligence and Predictive Analytics, Internet of Things Sensors and Gateways, Cloud and Edge Computing, Big-Data and GIS Analytics, 5G and Mission-Critical LTE Networks), Agency Type (Federal/National, State and Provincial, Municipal/Local), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solution | Critical Communication Network |

| Surveillance and Analytics Systems | |

| Biometric Security and Authentication Systems | |

| Emergency and Disaster Management Platforms | |

| Incident and Evidence Management Software | |

| Services | Professional Services |

| Managed Services |

| On-Premise |

| Cloud |

| Law Enforcement Agencies |

| Firefighting Departments |

| Emergency Medical Services |

| Transportation and Critical Infrastructure Operators |

| Disaster and Rescue Management Authorities |

| Other End-User Verticals |

| Artificial Intelligence and Predictive Analytics |

| Internet of Things Sensors and Gateways |

| Cloud and Edge Computing |

| Big-Data and GIS Analytics |

| 5G and Mission-Critical LTE Networks |

| Federal / National |

| State and Provincial |

| Municipal / Local |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Solution | Critical Communication Network | |

| Surveillance and Analytics Systems | |||

| Biometric Security and Authentication Systems | |||

| Emergency and Disaster Management Platforms | |||

| Incident and Evidence Management Software | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Type | On-Premise | ||

| Cloud | |||

| By End-User Vertical | Law Enforcement Agencies | ||

| Firefighting Departments | |||

| Emergency Medical Services | |||

| Transportation and Critical Infrastructure Operators | |||

| Disaster and Rescue Management Authorities | |||

| Other End-User Verticals | |||

| By Technology | Artificial Intelligence and Predictive Analytics | ||

| Internet of Things Sensors and Gateways | |||

| Cloud and Edge Computing | |||

| Big-Data and GIS Analytics | |||

| 5G and Mission-Critical LTE Networks | |||

| By Agency Type | Federal / National | ||

| State and Provincial | |||

| Municipal / Local | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the public safety market in 2026?

The public safety market size is expected to reach USD 598.61 billion in 2026, on its way toward a USD 882.41 billion total by 2031.

Which region is growing fastest?

Asia-Pacific leads with a projected 9.17% CAGR through 2031, propelled by China’s Safe City systems and India’s Smart Cities Mission.

What technology segment shows the highest growth?

Artificial intelligence and predictive analytics segment is forecast to grow at 9.11%, the fastest within the technology mix.

Why do agencies still favor on-premise deployments?

Data-sovereignty laws and sub-200-millisecond latency requirements for dispatch keep 71.33% of solutions on local servers despite rising cloud adoption.

Which end-user vertical is expanding most quickly?

Disaster and rescue management authorities are set for a 9.23% CAGR as climate-driven emergencies increase grant funding.

How concentrated is vendor competition?

The top five suppliers control about 35%-40% of revenue, yielding a moderate concentration that allows new entrants to gain share in specialized niches.

Page last updated on: