Public Key Infrastructure (PKI) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.96 Billion |

| Market Size (2031) | USD 22.99 Billion |

| Growth Rate (2026 - 2031) | 20.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Public Key Infrastructure (PKI) Market Analysis by Mordor Intelligence

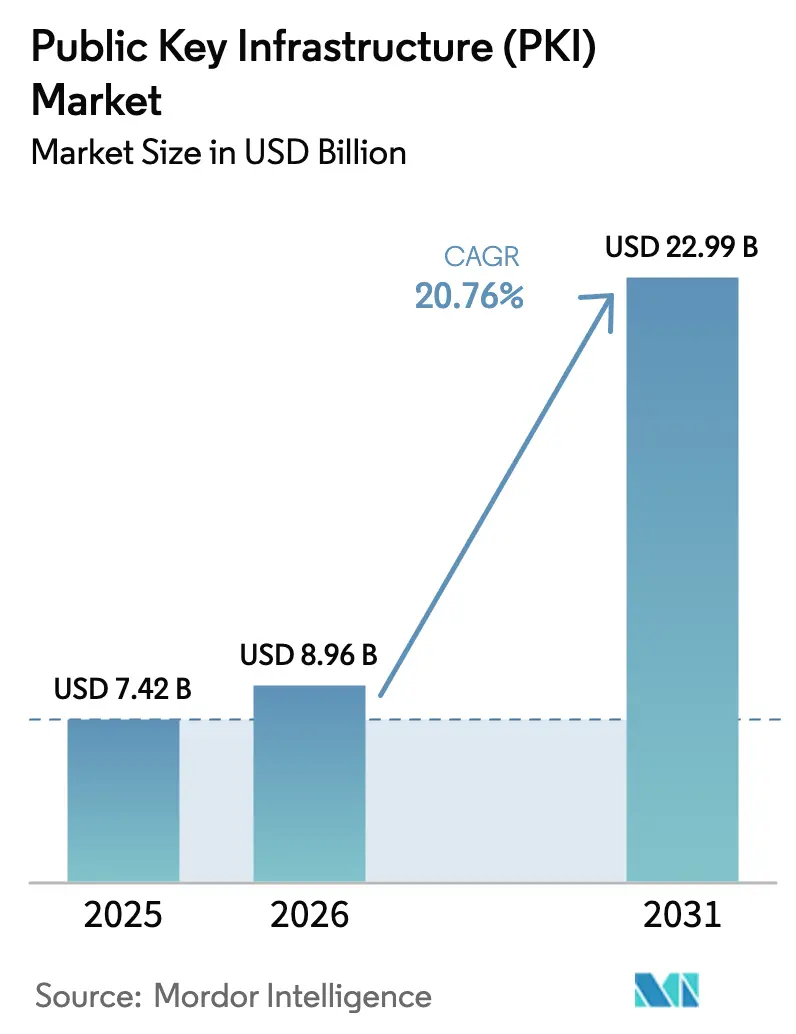

The Public Key Infrastructure Market size was valued at USD 7.42 billion in 2025 and estimated to grow from USD 8.96 billion in 2026 to reach USD 22.99 billion by 2031, at a CAGR of 20.76% during the forecast period (2026-2031).

Uptake accelerates as enterprises shift from legacy authentication toward quantum-resistant frameworks aligned with NIST’s August 2024 post-quantum standards [1]National Institute of Standards and Technology, “NISTIR 8547 Draft: Transition to Post-Quantum Cryptography Standards,” nist.gov. Rapid IoT endpoint growth, zero-trust mandates in financial services, and Asia-Pacific data-residency rules requiring localized certificate authorities collectively reinforce demand. Vendor consolidation, heightened automation needs created by shorter certificate lifespans, and expanding managed-service offerings further shape competitive dynamics. Simultaneously, the acute cryptographic-skills gap and high capital costs of FIPS-140-compliant hardware security modules temper adoption, keeping the Public Key Infrastructure market in a moderately concentrated yet fast-evolving state.

Key Report Takeaways

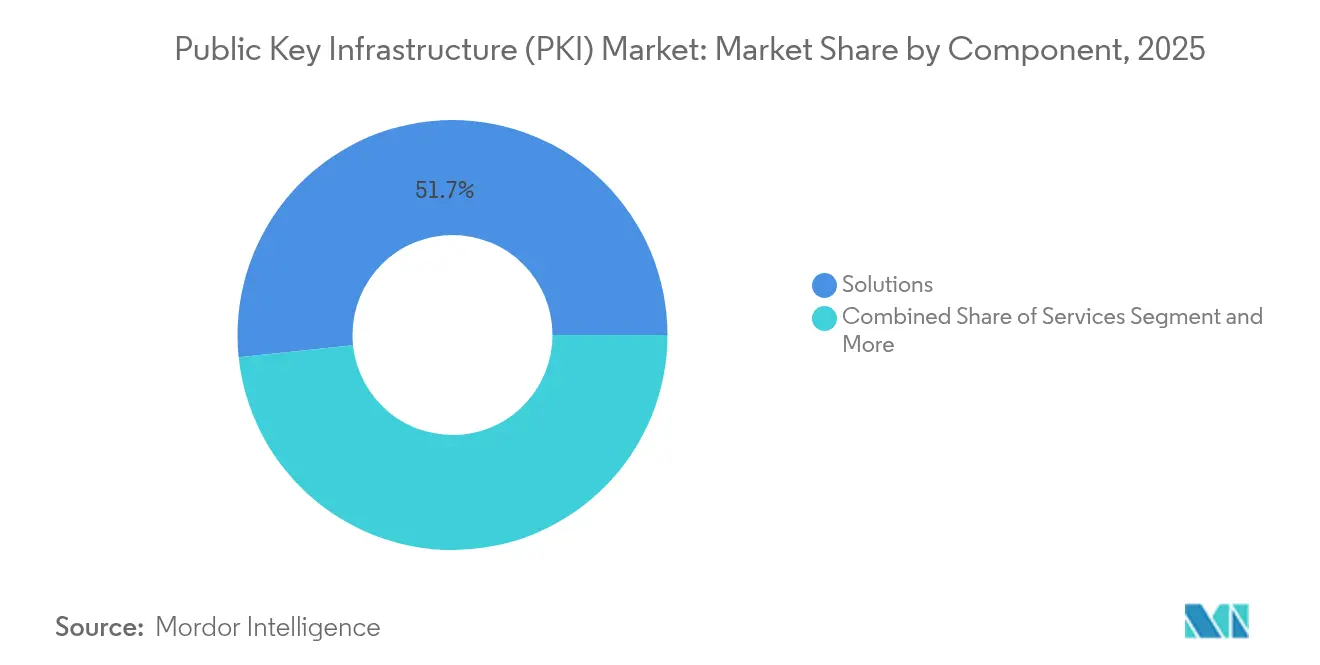

- By component, Solutions held 51.65% of the Public Key Infrastructure market share in 2025, while Services are poised to expand at a 22.85% CAGR to 2031.

- By deployment, on-premises models retained 53.55% of the Public Key Infrastructure market size in 2025, whereas cloud PKI is projected to advance at 21.45% CAGR through 2031.

- By enterprise size, large organizations commanded 59.35% share of the Public Key Infrastructure market size in 2025; small and medium enterprises record the fastest growth at 22.4% CAGR.

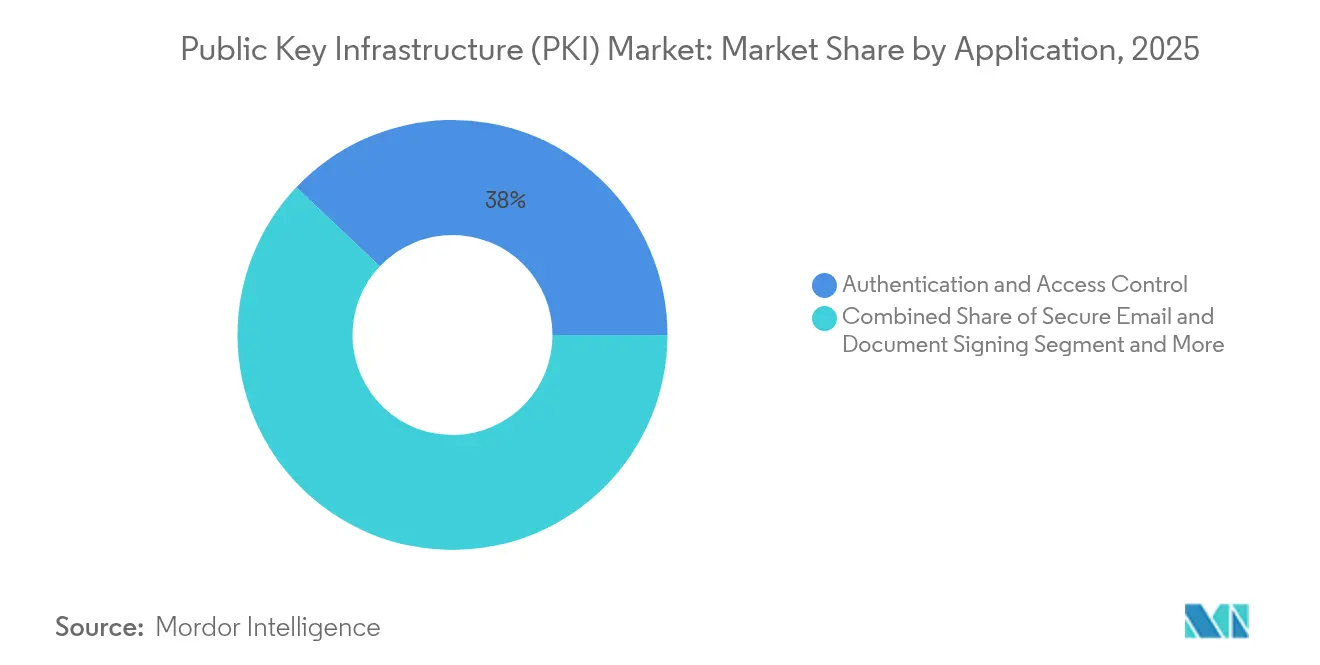

- By application, authentication and access control dominated with 37.95% revenue share in 2025; IoT identity management is set to grow at 23.05% CAGR between 2026-2031.

- By end-user industry, BFSI led with 25.85% of the Public Key Infrastructure market size in 2025, whereas healthcare and life sciences will post a 21.8% CAGR to 2031.

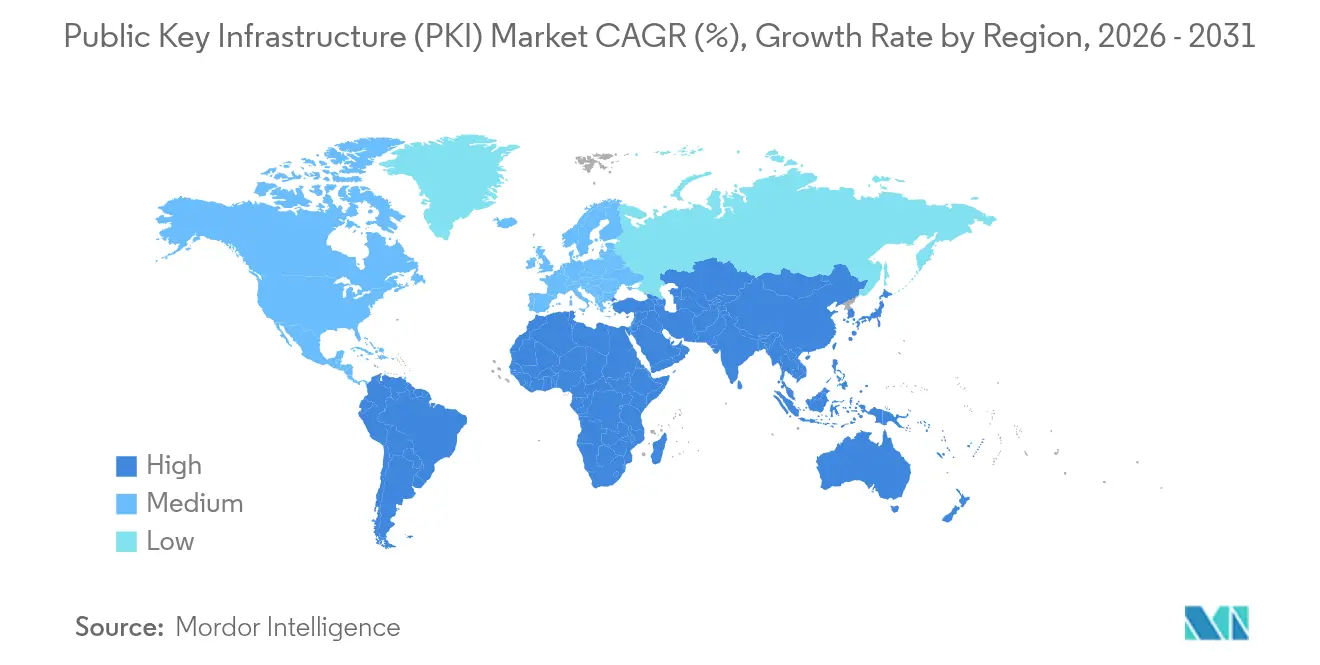

- By geography, North America captured 34.95% revenue share in 2025; Asia Pacific is projected to be the fastest-growing region at 22.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Public Key Infrastructure (PKI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT endpoints necessitating device-level trust | +4.2% | Global; focus on North America & APAC | Medium term (2-4 years) |

| Zero-trust roll-outs in North-American BFSI | +3.8% | North America, expanding to Europe | Short term (≤ 2 years) |

| Data-residency mandates fueling national CAs across Asia | +3.5% | Asia Pacific; spillover to MEA | Medium term (2-4 years) |

| Quantum-readiness programs accelerating modernization in Europe | +2.9% | Europe; early adoption in Germany & UK | Long term (≥ 4 years) |

| Managed-PKI demand from SMEs in GCC countries | +2.1% | Middle East (GCC); broader MEA | Short term (≤ 2 years) |

| Migration of national e-ID schemes to PKI platforms in Africa | +1.8% | Africa; focus on South Africa & Nigeria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT Endpoints Necessitating Device-Level Trust

Smart-grid deployments and connected-vehicle programs create a flood of devices that all require unique cryptographic identities, forcing organizations to automate certificate enrollment at unprecedented scale. Siemens operates dual PKI environments and manages lifecycles for internal users and IoT assets through Red Hat Ansible, illustrating the operational scale now demanded. IEEE 2030.5 further cements PKI as mandatory for distributed energy resources, pushing utilities toward automated lifecycle management. Because IoT devices often remain in service 10-15 years, quantum-resistant algorithms such as those inside SEALSQ’s INeS PKI are already shipping to guarantee future safety. These factors collectively expand the Public Key Infrastructure market through sustained hardware, software, and services outlays.

Zero-Trust Architecture Roll-outs in North-American BFSI

U.S. financial institutions now embed PKI as the trust core of zero-trust blueprints, a stance formalized in NIST SP 800-207 guidance [2]National Institute of Standards and Technology, “Zero Trust Architecture,” nist.gov . Payment Card Industry regulations have incorporated zero-trust concepts, driving widespread deployment of certificate-based machine and user identities. DigiCert research reports that 96% of security leaders see PKI as the only scalable means to implement continuous verification at line-of-business speed. Intense compliance demands, paired with growing cyber-attack frequency, accelerate PKI spending and underpin near-term growth in the Public Key Infrastructure market.

Data-Residency Mandates Fueling National CAs across Asia

Governments across Asia Pacific are instituting local certificate authorities to keep keys within borders. Japan’s My Number Card PKI now supports 736 firms, while the Philippines’ PNPKI distributes free digital certificates to streamline e-government transactions [3]Philippine News Agency, “PNPKI Ensures Cybersecurity in the Digital Future,” pna.gov.ph. India’s Aadhaar and UPI systems, both PKI-anchored, illustrate how digital public infrastructure reforms translate into volume license demand [4]Economic Research Institute for ASEAN and East Asia, “India-ASEAN Digital Public Infrastructure Collaboration,” eria.org. Regional initiatives, such as the Asia Pacific Digital Identity Consortium, promise cross-border interoperability while retaining national control, bolstering the Public Key Infrastructure market outlook.

Quantum-Readiness Programs Accelerating PKI Modernization in Europe

With quantum computing threats on the horizon, European organizations are modernizing PKI stacks well before the end-of-decade deadline. eIDAS now references quantum-safe digital signatures, compelling certificate authorities to integrate CRYSTALS-Dilithium and SPHINCS+ schemes. Yet only 3% of Finnish firms rate themselves ready for the transition, driving significant consulting and hardware refresh spending. Hybrid solutions permitting co-existence of current and post-quantum algorithms have become a standard feature set, feeding another wave of Public Key Infrastructure market demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute cryptographic-skills gap hindering PKI operations | −2.8% | Global; most severe in emerging markets | Medium term (2-4 years) |

| High initial cost of FIPS-140-compliant HSMs | −2.3% | North America & Europe; expanding globally | Short term (≤ 2 years) |

| Fragmented certificate standards across Latin-American regulators | −1.9% | Latin America; spillover to regional trade | Long term (≥ 4 years) |

| Latency-sensitive 5G/edge use-cases reluctant toward cloud PKI | −1.5% | Global; concentrated in telecom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Cryptographic-Skills Gap Hindering PKI Operations

Entrust’s 2024 survey shows 64% of enterprises lack skilled staff to operate PKI, while 33% see new IoT use cases adding uncertainty. As post-quantum algorithms arrive, the knowledge deficit widens, prompting heavier reliance on managed services and automation. This restraint tempers the Public Key Infrastructure market expansion, particularly in regions with limited STEM education capacity.

High Initial Cost of FIPS-140-Compliant HSMs

Up-front expenditure for certified hardware security modules remains a hurdle, particularly for SMEs. Although cloud HSM services from IBM and Futurex reduce capex, the pivot converts fixed assets into recurring opex, prolonging return-on-security-investment evaluations. Budget pressure can delay new PKI programs and slows part of the Public Key Infrastructure market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge Despite Solutions Dominance

Solutions captured USD 3.83 billion in 2025, equal to 51.65% of the Public Key Infrastructure market. Revenue spans certificate-lifecycle platforms, hardware security modules, and cryptographic toolkits anchoring enterprise trust fabrics. Services, encompassing managed PKI and consulting, will compound at 22.85% through 2031 as firms lacking skilled personnel offload operational complexity. ACME-driven automation, shorter certificate validity proposals, and quantum-migration roadmaps intensify the need for external expertise, cementing services’ long-term momentum within the broader Public Key Infrastructure market.

As post-quantum standards mature, organizations purchase advisory projects to integrate CRYSTALS-Dilithium and SPHINCS+ algorithms without downtime. This consulting wave dovetails with managed-service contracts that convert capex into predictable opex. The result is a secular inversion: services growth surpasses infrastructure growth even though hardware security modules remain non-discretionary for root-of-trust integrity. Vendors differentiate by bundling lifecycle automation and compliance dashboards, raising switching costs and reinforcing recurring revenue streams in the Public Key Infrastructure industry.

By Deployment: Cloud PKI Challenges On-Premises Dominance

On-premises architectures held 53.55% of the Public Key Infrastructure market in 2025, reflecting enterprise control preferences for root CAs. Yet cloud PKI is rising at 21.45% CAGR as scalability, rapid provisioning, and consumption-based pricing outweigh sovereignty concerns for many workloads. DigiCert ONE’s listing on Microsoft Azure typifies frictionless procurement, accelerating adoption among DevOps teams. Hybrid models keeping root keys on-site while issuing leaf certificates from the cloud are becoming standard, underpinning transition journeys without jeopardizing compliance.

Latency-sensitive edge deployments in 5G and autonomous-vehicle environments, however, still shy away from remote validation to avoid performance hits. Consequently, the Public Key Infrastructure market exhibits a bifurcated deployment profile: mission-critical low-latency use cases remain on-premises, whereas web-scale or public-facing applications migrate to SaaS PKI. Vendors that offer consistent policy control across the two realms increase stickiness and reduce migration risk.

By Enterprise Size: SMEs Drive Growth Through Managed Services

Large enterprises accounted for 59.35% of the Public Key Infrastructure market in 2025, backed by their deep resources and compliance mandates. Small and medium enterprises now form the fastest-growing cohort at 22.4% CAGR, leveraging managed PKI subscriptions to bypass skill shortages and hardware purchases. In the Gulf Cooperation Council, government e-services require certificate-based authentication, pushing SMEs onto external PKI platforms.

Automation, pay-as-you-go pricing, and bundled HSM-as-a-Service deliver enterprise-grade security without the associated overhead. Asian Development Bank data underscores the scale: SMEs constitute 97% of firms across developing Asia, representing a vast unpenetrated addressable base. Vendors tailor simplified dashboards, guided onboarding, and compliance templates to accelerate adoption, further expanding the Public Key Infrastructure market footprint.

By Application: IoT Identity Management Accelerates Beyond Authentication

Authentication and access control delivered 37.95% of 2025 revenue, reaffirming PKI’s foundational role in safeguarding users and systems. IoT identity management is set to outpace all other segments with 23.05% CAGR, fueled by smart-grid programs and connected-vehicle rollouts that each demand low-touch certificate provisioning at planetary scale. Code signing and software integrity uses have also risen sharply following high-profile supply-chain attacks, inducing enterprises to embed PKI into DevSecOps pipelines.

Payment ecosystems, including emerging CBDC pilots, lean on high-performance certificate validation, extending market relevance into fintech micro-services. Hence, even as the Public Key Infrastructure market sustains its legacy stronghold in enterprise authentication, new edge-device and software-supply-chain demands catapult fresh spending categories.

By End-user Industry: Healthcare Accelerates While BFSI Leads

BFSI retained 25.85% of global demand in 2025, guided by stringent data-protection statutes and zero-trust adoption. Healthcare and life sciences will register the fastest CAGR at 21.8% through 2031 as electronic health records, telemedicine, and connected medical devices require tamper-proof identities for clinicians and patients. Government and defense remain consistent adopters via e-ID programs, while manufacturing leans on PKI for secure industrial IoT.

Media, retail, and utilities sectors likewise integrate certificate-based controls for content protection, payment security, and distributed energy resource authentication. These cross-industry expansions reinforce the Public Key Infrastructure market’s centrality to digital-trust architectures.

Geography Analysis

North America retained 34.95% of 2025 revenue, anchored by early enterprise adoption and federal post-quantum directives. U.S. agencies and banks dominate procurement, while Canada’s healthcare digitization fuels steady growth. Asia Pacific is the clear high-velocity engine at 22.35% CAGR, with Japan’s My Number ecosystem, India’s Aadhaar and UPI rails, and China’s smart-city initiatives all delivering large-scale certificate volumes.Europe follows with strong albeit steadier expansion as eIDAS and GDPR drive privacy-centric CAs alongside quantum-upgrade projects. Latin America grows more slowly due to fragmented standards, though Brazil’s digital-government program offers upside. The Middle East and Africa lure managed-service vendors to compensate for local skills shortages, especially where national e-ID schemes are underway. Overall, geography-specific drivers ensure the Public Key Infrastructure market grows in every region albeit at varied speeds.

Competitive Landscape

The Public Key Infrastructure market remains moderately concentrated. DigiCert, Entrust, and Thales leverage decades-old roots of trust, entrenched audit credentials, and extensive partner ecosystems. Cloud hyperscalers—Amazon Web Services, Microsoft, and Google—pressure incumbents by embedding PKI into broader cloud security suites, lowering adoption barriers for DevOps-centric clients. Post-quantum readiness is the emerging battleground; vendors that offer crypto-agile stacks and automated migration tooling differentiate strongly.

2024 consolidation re-shaped the field: CyberArk paid USD 1.54 billion for Venafi to unify machine-identity management with secrets governance.Sectigo’s acquisition of Entrust’s public certificate business doubled its enterprise footprint and accelerated roadmap execution toward shorter-lived certificates.Patent filings surged, with DigiCert registering 81 new applications around AI-driven lifecycle orchestration and quantum-safe issuance.These moves reflect a strategic stretch toward platform convergence, recurring revenue, and future-proof cryptography all central themes sustaining competition in the Public Key Infrastructure market.

Public Key Infrastructure (PKI) Industry Leaders

Microsoft Corporation

HID Global Corporation

Amazon Web Services, Inc.

Google LLC

Entrust Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: DigiCert introduced DigiCert ONE, converging PKI and DNS management to automate renewals and mitigate DDoS exposure.

- February 2025: Sectigo completed the acquisition of Entrust’s public certificate business, broadening lifecycle-management capabilities and advancing post-quantum readiness.

- January 2025: DigiCert reported record FY2025 growth, citing a 67% rise in customers adopting the integrated digital-trust platform .

- December 2024: SEALSQ launched INeS PKI featuring CRYSTALS-Kyber and CRYSTALS-Dilithium to secure smart-city and healthcare IoT environments.

Global Public Key Infrastructure (PKI) Market Report Scope

Public Key Infrastructure (PKI) serves as a framework for managing digital keys and certificates, facilitating secure communication and authentication across networks. By leveraging public-key cryptography, PKI safeguards data confidentiality, integrity, and authenticity.

The study tracks the revenue accrued through the sale of public key infrastructure (PKI) by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The public key infrastructure (PKI) Market is segmented by component (hardware security modules (HSM), solutions, services), deployment (on-premises and cloud), enterprise size (small & medium enterprises (SMEs) and large enterprises), end-user (BFSI, it & telecom, government & defense, media and entertainment, retail, healthcare, manufacturing, education, automotive, and others), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Hardware Security Modules (HSM) |

| Certificate Lifecycle-Management Platforms / Solutions |

| Services |

| On-premises |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Authentication and Access Control |

| Secure Email and Document Signing |

| Web and e-Commerce Security (SSL/TLS) |

| IoT Device Identity Management |

| Code Signing and Software Integrity |

| Payment Processing and Mobile Wallets |

| BFSI |

| Government and Defense |

| IT and Telecom |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Retail and E-Commerce |

| Media and Entertainment |

| Energy and Utilities |

| Education |

| Automotive and Transportation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware Security Modules (HSM) | ||

| Certificate Lifecycle-Management Platforms / Solutions | |||

| Services | |||

| By Deployment | On-premises | ||

| Cloud | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Application | Authentication and Access Control | ||

| Secure Email and Document Signing | |||

| Web and e-Commerce Security (SSL/TLS) | |||

| IoT Device Identity Management | |||

| Code Signing and Software Integrity | |||

| Payment Processing and Mobile Wallets | |||

| By End-user Industry | BFSI | ||

| Government and Defense | |||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Manufacturing and Industrial | |||

| Retail and E-Commerce | |||

| Media and Entertainment | |||

| Energy and Utilities | |||

| Education | |||

| Automotive and Transportation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Public Key Infrastructure market?

The Public Key Infrastructure market is valued at USD 8.96 billion in 2026 and is projected to reach USD 22.99 billion by 2031 at a 20.76% CAGR.

Which region is growing fastest in the Public Key Infrastructure market?

Asia Pacific posts the highest growth rate, projected at 22.35% CAGR through 2031 due to national digital-identity initiatives and data-residency mandates.

Why are services outpacing solutions in PKI spending?

Acute shortages of cryptographic expertise and the complexity of post-quantum migration push enterprises to outsource certificate lifecycle management, driving a 22.85% CAGR in services.

How does post-quantum cryptography affect PKI roadmaps?

NIST-approved algorithms such as CRYSTALS-Dilithium require hardware upgrades and crypto-agile software, prompting global PKI modernization programs, particularly in Europe and North America.

Page last updated on: