Plasma Protease C1-inhibitor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.38 Billion |

| Market Size (2031) | USD 6.77 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

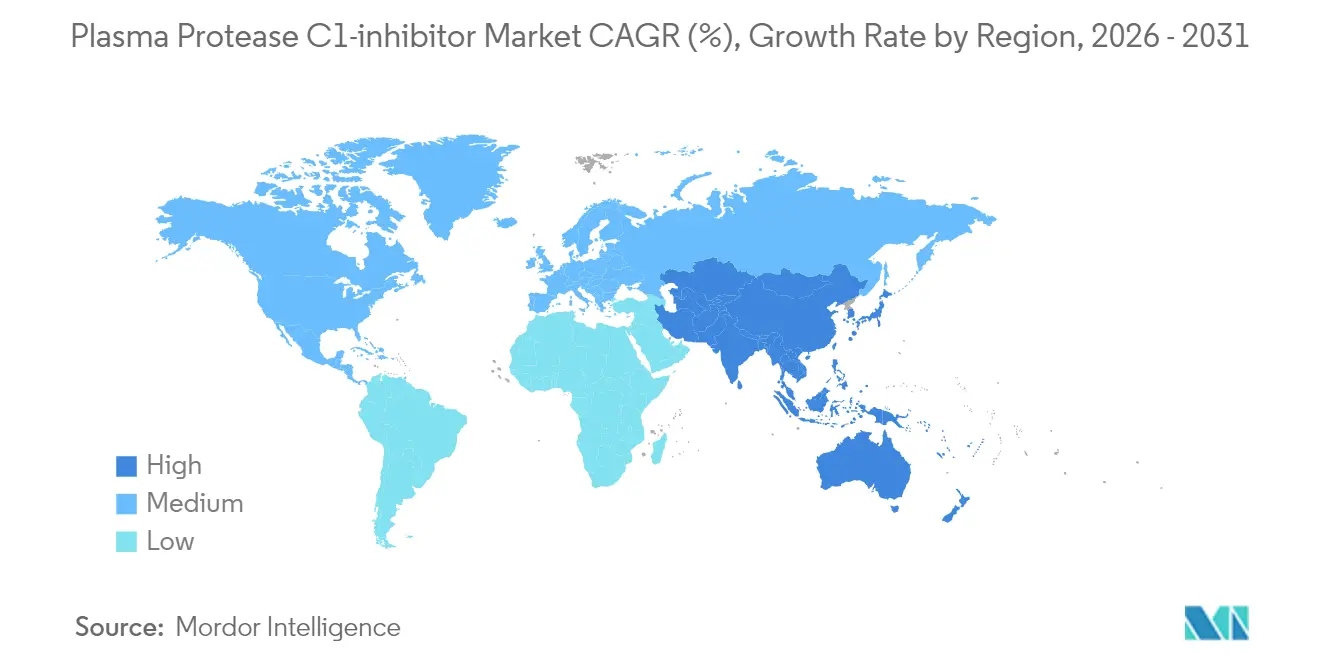

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

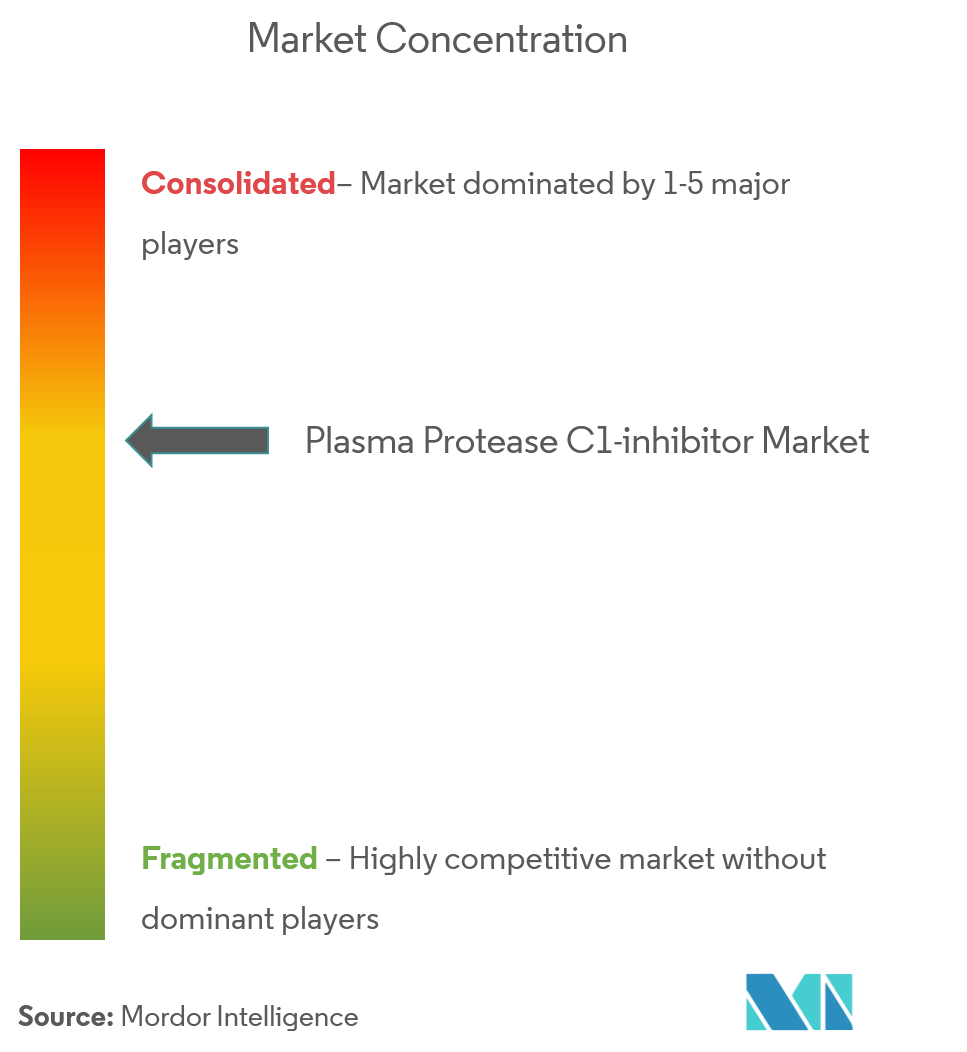

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plasma Protease C1-inhibitor Market Analysis by Mordor Intelligence

The plasma protease C1-inhibitor market size is expected to grow from USD 4.01 billion in 2025 to USD 4.38 billion in 2026 and is forecast to reach USD 6.77 billion by 2031 at 9.12% CAGR over 2026-2031. Strong demand comes from the rapid shift toward preventive care for hereditary angioedema (HAE), expanding clinical evidence that early prophylaxis curbs emergency costs, and the arrival of oral and subcutaneous products that simplify self-management. Robust orphan-drug incentives in North America and Europe, ongoing plasma fractionation investments in Asia, and improving diagnosis rates add momentum. At the same time, the plasma protease C1-inhibitor market contends with plasma-supply bottlenecks and reimbursement scrutiny, factors that are prompting manufacturers to diversify supply chains, explore recombinant routes, and deliver clearer health-economic dossiers. Moderate competitive intensity prevails because heavy regulatory compliance, donor-recruitment logistics, and biologics manufacturing expertise limit new entry, yet innovation cycles are accelerating as developers race to introduce patient-centric formulations and novel mechanisms of action.

Key Report Takeaways

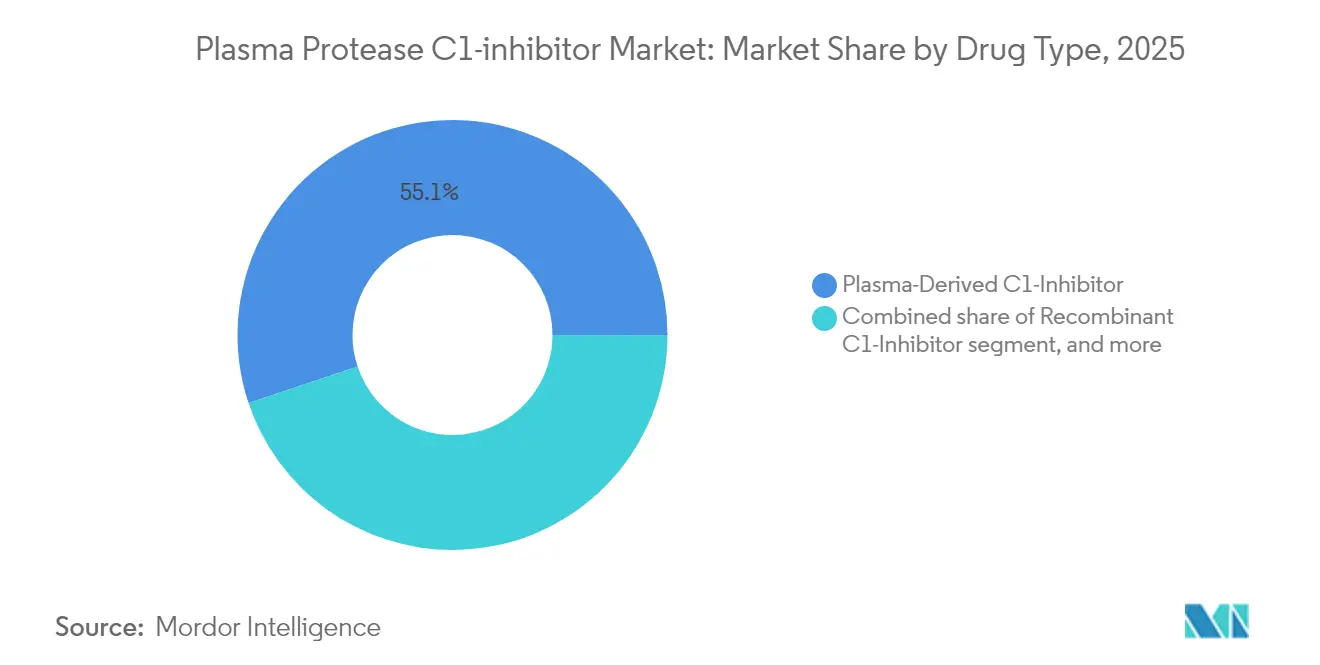

- By drug type, plasma-derived products led with 55.12% of the plasma protease C1-inhibitor market share in 2025, while oral plasma-kallikrein inhibitors are on track for the fastest 11.02% CAGR through 2031.

- By dosage form, lyophilized powder held 53.70% of the plasma protease C1-inhibitor market size in 2025; liquid injectables are set for the highest growth at 9.86% CAGR to 2031.

- By route of administration, intravenous therapy retained 56.92% share of the plasma protease C1-inhibitor market size in 2025, whereas oral administration is the quickest riser at 12.14% CAGR to 2031.

- By indication, acute on-demand treatment captured 50.88% revenue share in 2025; long-term prophylaxis is projected to expand at an 11.19% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 46.05% of 2025 revenues; online pharmacies will post the strongest 11.98% CAGR to 2031.

- By geography, North America commanded 44.21% share in 2025, while Asia-Pacific is the fastest-growing region at 10.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plasma Protease C1-inhibitor Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Burden of Rare Genetic Disorders | +2.1% | Global, concentrated in North America & EU | Long term (≥ 4 years) |

| Increasing Orphan Drug Designations and Incentives | +1.8% | North America & EU primary, APAC emerging | Medium term (2-4 years) |

| Rising Healthcare Expenditure in Emerging Economies | +1.5% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expansion of Plasma Fractionation Infrastructure in Asia | +1.2% | APAC focused, especially China & India | Long term (≥ 4 years) |

| Technological Advancements in Biologic Drug Delivery | +1.0% | Global, led by North America innovation hubs | Short term (≤ 2 years) |

| Strategic Collaborations and M&A Activities Among Biopharma Companies | +0.8% | Global, clustered in major pharma centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Global Burden of Rare Genetic Disorders

Better epidemiological surveillance indicates HAE prevalence of 2.67 per 100,000 in the United States, translating to 9,559 diagnosed cases by 2024 and narrowing historic under-diagnosis gaps[1]C. Bork et al., “Updated HAE Epidemiology,” Annals of Allergy, Asthma & Immunology, aacipjournals.org. Each patient faces combined direct and indirect annual costs nearing USD 42,000, a figure that health systems aim to cut through preventive therapies. System-wide acceptance that early prophylaxis lowers emergency interventions is propelling systematic adoption programs. Alongside medical cost containment, improved physician education and patient advocacy are raising screening uptake in family members, expanding the treatable population for the plasma protease C1-inhibitor market. Insurers consequently view prophylactics as budget-neutral over time, reinforcing demand for high-value products.

Increasing Orphan Drug Designations and Incentives

In 2024 the US FDA cleared multiple complement-mediated disorder biologics and launched a Rare Disease Innovation Hub that unifies real-world evidence with patient-reported outcomes, shortening review cycles[2]FDA, “Rare Disease Innovation Hub Announcement,” fda.gov. Europe’s positive scientific opinion for garadacimab reflects similar alignment on expedited access when an unmet need is addressed. Priority review vouchers, tax credits, and extended market exclusivity draw mid-cap developers and large pharma alike, sustaining a thick pipeline that will shape the plasma protease C1-inhibitor market through 2030. Payers, seeing clearer outcomes data, show greater tolerance for premium pricing that keeps emergency-department visits low, particularly when treatments can be self-administered.

Rising Healthcare Expenditure in Emerging Economies

China’s National Medical Products Administration enlarged its Rare Diseases List from 121 to 207 conditions and unveiled the CARE program to guide orphan-drug development, spurring multinational and domestic sponsors to file new dossiers. Southeast Asian spending on biologics is accelerating, illustrated by Indonesia’s first plasma fractionation site with 600,000-liter annual capacity. Public budgets, insurance expansion, and philanthropic support are converging, raising affordability for advanced HAE therapy. These dynamics amplify the addressable base for the plasma protease C1-inhibitor market in large populations previously served only sporadically.

Expansion of Plasma Fractionation Infrastructure in Asia

Kamada’s new Houston collection hub and CSL’s roll-out of RIKA devices that cut donation times by 15 minutes exemplify sector-wide moves to relieve supply tension. Asia is following suit, with governments encouraging local fractionation to hedge against import delays. Europe’s call for 2 million additional donors underlines the systemic urgency[3]Vox Sanguinis, “Plasma Supply in Europe,” vox-sang.org. Capacity upgrades stabilize input availability and reassure regulators that production can meet forecast demand for the plasma protease C1-inhibitor market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs and Reimbursement Challenges | −1.4% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Limited Plasma Supply and Collection Bottlenecks | −1.1% | Global, Europe most affected | Long term (≥ 4 years) |

| Stringent Regulatory Requirements for Plasma-Derived Products | −0.9% | Global, with heightened scrutiny in EU & North America | Medium term (2-4 years) |

| Low Disease Awareness and Diagnostic Delays | −0.7% | Emerging markets and underserved rural areas worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Reimbursement Challenges

Median fair pricing for chronic orphan drugs runs at USD 256,000 annually according to recent payer surveys. Prior authorization hurdles at insurers such as UnitedHealthcare often slow therapy initiation because physicians must document HAE frequency and prior therapy failure. In markets still building rare-disease frameworks, co-pays remain daunting, limiting uptake despite clinical guidelines. The US Inflation Reduction Act adds an extra layer of pricing negotiations that could dampen longer-term R&D appetite. These friction points collectively weigh on the growth trajectory of the plasma protease C1-inhibitor market.

Limited Plasma Supply and Collection Bottlenecks

The United States supplies around 70% of global plasma, leaving other geographies exposed to export restrictions or transport disruptions. Fragmented state regulations—for instance, Connecticut’s stringent rules leaving it with a single donation center—further thin collection capacity. As new indications emerge and patient volumes rise, collection growth is not keeping pace, risking shortages. Persistent imbalance may steer prices upward and encourage accelerated moves toward recombinant or transgenic platforms within the plasma protease C1-inhibitor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Plasma-Derived Dominance Faces Oral Innovation

Plasma-derived C1-inhibitor therapies held 55.12% of 2025 revenues in the plasma protease C1-inhibitor market thanks to long clinical track records and familiar dosing algorithms. Brands such as Berinert and Cinryze remain the default choice for acute and prophylactic care in most hospital formularies. Their robust safety archives reassure prescribers when treating children or pregnant women, two cohorts under close watch. Despite this incumbency, pipeline visibility shows that oral kallikrein inhibitors will expand at an 11.02% CAGR through 2031 as they remove injection anxiety and fit telehealth models. BioCryst’s ORLADEYO posted USD 134.2 million in Q1 2025 sales, a rise of 51% year-over-year that validates consumer appetite for swallowable options. Should sebetralstat secure FDA clearance in mid-2025, a second oral product will further normalize non-invasive treatment, likely capturing adolescents who resist needles. As competition widens, plasma protease C1-inhibitor market size for oral drugs could exceed USD 1.33 billion in 2031, reshaping revenue splits without fully displacing plasma-derived incumbents that still cover special populations.

Pipeline diversification extends beyond kallikrein inhibition. Recombinant C1-inhibitors now reach scale sufficient for commercial pricing, offering virus-inactivation advantages and sidestepping donor reliance. Developers also test gene-silencing modalities that curb bradykinin release upstream, though commercial timing sits beyond 2030. Collectively, these approaches temper long-term plasma demand growth, but manufacturing cost structures will determine competitive margins. Between 2025 and 2030, product positioning will hinge on dosing frequency, device convenience, and payer contracts that favor predictable monthly outlays over per-attack spending.

By Dosage Form: Lyophilized Powder Leadership Challenged by Innovation

Lyophilized powder secured 53.70% of 2025 revenues in the plasma protease C1-inhibitor market because freeze-drying extends shelf life and assures stability during shipping to remote clinics. Hospitals value the lower cold-chain burden and the option to stock strategic reserves for emergency departments. However, reconstitution steps lengthen administration time, especially during laryngeal attacks that demand speed. CSL’s liquid-stable HAEGARDA answered that gap by offering prefilled syringes for at-home subcutaneous use, trimming preparation to minutes. As autoinjectors and room-temperature vials proliferate, liquid forms are forecast to record a 9.86% CAGR, chipping at powder share.

Manufacturers of lyophilized presentations respond by integrating on-needle mixing devices and single-vial packaging to streamline workflows. Parallel advances in spray-drying and vacuum-induced nano-porous matrices may shorten reconstitution to under 15 seconds and restore competitive footing. Nonetheless, patient convenience remains the decisive adoption criterion in prophylaxis, nudging formulators to liquid solutions where possible. Over the forecast horizon the plasma protease C1-inhibitor market size gain from liquid products could add USD 580 million, while powders maintain relevance in humanitarian stockpiles and low-resource settings.

By Route of Administration: IV Dominance Yields to Patient-Centric Alternatives

Intravenous delivery retained 56.92% share in 2025 because acute intervention still relies on rapid systemic exposure that peripheral veins deliver reliably. Emergency physicians prefer IV Berinert when airway compromise looms, given its near-instant bioavailability. Yet patient surveys show growing frustration with venous access challenges, infusion site pain, and time lost traveling to infusion centers. Subcutaneous C1-inhibitor regimens answer convenience without sacrificing efficacy, boosting adherence in adults who face frequent attacks. Market research suggests that two-thirds of new prophylaxis prescriptions in North America now specify subcutaneous or oral formulations, underscoring a meaningful shift.

Oral administration, though only a single marketed product today, shows the steepest adoption curve. KalVista projects peak US sebetralstat sales of USD 750 million, reflecting strong physician interest in on-demand tablets that patients can carry anywhere. Should real-world experience reconfirm rapid symptom relief, guidelines will likely advise keeping an oral rescue option alongside prophylaxis, implying dual prescriptions per patient and enlarging the plasma protease C1-inhibitor market. Device-free dosing also unlocks e-pharmacy channels and subscription-based supply models, creating incremental convenience advantages.

By Indication: Acute Treatment Leads as Prophylaxis Gains Momentum

Emergency attacks remained responsible for 50.88% of 2025 revenues within the plasma protease C1-inhibitor market because laryngeal edema demands immediate pharmacologic blockade to avert asphyxiation. Hospitals stock IV vials under sepsis-code protocols to secure 24/7 access. Nonetheless, HAE management guidelines now recommend prophylaxis for patients experiencing more than one attack monthly or any laryngeal episode, expanding the eligible cohort dramatically. Real-world data show ORLADEYO cut average attack rates to 0.50 per month by day 90, sustaining gains over 18 months.

As insurers embrace the economic logic of prophylaxis preventing costly admissions, long-term therapy uptake accelerates. The prophylaxis CAGR of 11.19% suggests that by 2031 preventive regimens could outspend acute products for the first time, raising questions about inventory management in emergency departments. Still, acute formulations remain non-optional because breakthrough attacks occur even under prophylaxis and because some patients decline daily tablets or injections. Forward-looking manufacturers, therefore, design dual-indication portfolios to keep coverage across the full patient journey.

By Distribution Channel: Hospital Pharmacies Lead Amid Digital Transformation

Hospital pharmacies held 46.05% of 2025 plasma protease C1-inhibitor market revenue because acute products move through inpatient formularies and require cold-chain stewardship. In addition, in-hospital dispensing ensures immediate reimbursement capture and supports supplier consignment strategies that mitigate stock-out risk. Specialty clinics function as secondary hubs, coordinating infusion suites and patient-training programs for subcutaneous products. Yet telehealth expansion and e-prescribing have paved the way for mail-order fulfillment. Online pharmacies are expected to reach a 11.98% CAGR as insurers partner with digital specialty platforms to lower distribution costs and monitor adherence electronically.

Manufacturers enhance these channels via integrated care programs. CSL’s HAEGARDA Connect pairs nurse educators, pharmacy dispatch, and co-pay support, improving refill continuity. As value-based contracts spread, payers will likely steer stable prophylaxis patients toward home delivery, freeing hospital capacity for critical care. Over time, direct-to-patient logistics may reshape demand forecasting, with real-time data informing production runs and reducing wastage.

Geography Analysis

North America led the plasma protease C1-inhibitor market with a 44.21% share in 2025. The United States drives volume due to orphan-drug exclusivity incentives, broad insurance coverage, and unmatched plasma collection capacity supplying 70% of the world’s source plasma. Medicare covers 89% of eligible patients for ORLADEYO, and private payers reimburse both prophylactic and rescue regimens when diagnostic criteria are met. Canada leverages pan-Canadian buying alliances to negotiate province-wide access, while Mexico’s Seguro Popular pilots reimbursement for high-cost biologics through state co-funding schemes.

Europe remains the second-largest region but contends with plasma self-sufficiency shortfalls estimated at two million donors, pushing governments to incentivize domestic collection. EMA’s rolling review of garadacimab exemplifies the bloc’s openness to non-replacement modalities that could lighten plasma demand. Germany and the United Kingdom top per-capita usage thanks to specialized HAE reference centers and active patient networks. Reimbursement is increasingly tied to health-technology-assessment outcomes that weigh emergency-department avoidance and quality-of-life gains, favoring prophylactic strategies.

Asia-Pacific is the fastest-growing territory at 10.11% CAGR, and its share of the plasma protease C1-inhibitor market is expected to reach double digits by 2030. China’s revised rare-disease framework, the CARE program, and expanding Essential Drugs List accelerate approvals, while local manufacturers invest in fractionation to secure supply fortrea.com. Japan maintains premium pricing through stringent clinical evidence requirements, yet fast-track schemes for pediatric orphanindications speed uptake. Australia’s Pharmaceutical Benefits Scheme widened its reimbursement criteria for prophylactic C1-inhibitors in 2025, lowering co-payments and lifting adherence. India, aided by its National Policy for Rare Diseases, is financing named-patient imports while state governments co-invest in fractionation plants aimed at reducing import dependency. Across Southeast Asia, advocacy groups cooperate with telemedicine platforms so rural patients can secure specialist consultations, expanding diagnosis pipelines that feed regional demand in the plasma protease C1-inhibitor market.

South America shows heterogeneous growth. Brazil’s Unified Health System funds acute therapies through judicial mandates, but prophylaxis remains limited to private insurance. Argentina’s ANMAT fast-tracked two subcutaneous products in late 2024, and Chile’s Ricarte Soto Law now reimburses up to 100% of treatment costs for catastrophic diseases, opening incremental volumes. The Middle East and Africa contribute small but rising revenues as Gulf Cooperation Council states integrate orphan drugs into centralized tender systems and South Africa revises its National Health Insurance bill to earmark funds for rare conditions.

Competitive Landscape

Established plasma specialists, integrated biologics firms, and nimble mid-caps coexist in a moderately concentrated environment. CSL Behring leverages more than 300 North American donation centers, vertical integration from collection to final fill-finish, and a broad rare-disease portfolio, anchoring leadership in plasma-derived C1-inhibitors. Takeda retains a formidable footprint through Cinryze and Takhzyro, posting 29.7% year-over-year growth in its plasma-derived therapies segment to JPY 271.4 billion in 2025. BioCryst’s ORLADEYO illustrates how a single oral agent can disrupt incumbency, generating USD 580-600 million expected 2025 revenues and projecting corporate profitability a year ahead of plan.

KalVista’s sebetralstat is the most advanced oral on-demand candidate under FDA review, and positive pediatric data could unlock lifetime-value advantages starting at age two. ADMA Biologics exemplifies growth via differentiated fractionation technology and long-term supply contracts, with USD 417-425 million 2024 sales forecast. Emerging players pursue recombinant or transgenic platforms to bypass plasma constraints, while device companies such as Ypsomed and West Pharma integrate autoinjectors into co-development deals to strengthen switching incentives. Strategic alliances proliferate: manufacturing tie-ups ensure fill-finish redundancy, and co-promotion deals accelerate global reach without duplicating salesforces.

Competitive strategy is shifting from efficacy claims to convenience, supply reliability, and service layers. Companies bundle nurse hotlines, remote monitoring apps, and financial-assistance portals to cement brand loyalty. Portfolio breadth also matters as payers seek contracting efficiencies; firms able to negotiate across immunology, hematology, and pulmonology can trade rebates for broader formulary placement. Late-stage M&A remains plausible, especially if oral market penetration erodes plasma volumes faster than collection capacity adjustments, driving incumbents to acquire pipeline assets for diversification within the plasma protease C1-inhibitor market.

Plasma Protease C1-inhibitor Industry Leaders

CSL Behring LLC

Takeda Pharmaceutical Company Limited (Shire Pharmaceutical Holdings)

Pharming Technologies B.V.

KalVista Pharmaceuticals, Inc.

BioCryst Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: KalVista Pharmaceuticals awaited an FDA decision on sebetralstat, with a PDUFA goal date of 17 June 2025 and potential peak sales projected at USD 750 million.

- June 2025: CSL Behring secured FDA approval for garadacimab (Andembry), the first once-monthly subcutaneous prophylactic targeting activated Factor XII for HAE prevention in patients ≥12 years.

- May 2025: BioCryst Pharmaceuticals posted Q1 2025 ORLADEYO sales of USD 134.2 million, up 51% from Q1 2024, and raised its full-year outlook to USD 580-600 million.

- March 2025: KalVista Pharmaceuticals completed enrollment early in the KONFIDENT-KID pediatric sebetralstat trial after expanding the cohort from 24 to 36 participants. Initial data are expected by year-end 2025.

- January 2025: ADMA Biologics announced preliminary 2024 revenue of USD 417-425 million, exceeding its earlier guidance while finalizing long-term plasma supply contracts expected to back ASCENIV growth into the late 2030s.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the plasma protease C1-inhibitor market as the worldwide ex-factory revenue earned from plasma-derived or recombinant C1-esterase inhibitors and approved kallikrein or bradykinin B2 receptor antagonists used for hereditary or acquired angioedema, covering both on-demand and long-term prophylaxis.

Scope exclusion: investigational gene therapies, pharmacy-compounded preparations, and non-drug supportive care remain outside this study.

Segmentation Overview

- By Drug Type

- Plasma-Derived C1-Inhibitor

- Recombinant C1-Inhibitor

- Kallikrein Inhibitors

- Bradykinin B2 Receptor Antagonists

- Emerging Oral Plasma-Kallikrein Inhibitors

- By Dosage Form

- Lyophilised Powder

- Liquid Injectable

- By Route Of Administration

- Intravenous

- Subcutaneous

- Oral

- By Indication

- Long-Term Prophylaxis

- On-Demand (Acute) Treatment

- By Distribution Channel

- Hospital Pharmacies

- Specialty Clinics

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed hematologists, rare-disease pharmacists, patient-advocacy leaders, and hospital procurement heads across North America, Europe, and Asia. These discussions refined dose frequency, therapy-switch patterns, and average selling prices that desk work alone could not surface.

Desk Research

We first mapped the treated patient pool through Orphanet prevalence sheets, NIH GARD records, and the WHO Global Health Observatory. We then linked supply volumes to FDA and EMA biologic-license dossiers, UN Comtrade plasma-fraction codes, and regional plasma-collection reports. Company 10-Ks, investor decks, and specialist press clarified revenue splits, while paid databases such as D&B Hoovers and Dow Jones Factiva sharpened firm-level inputs.

A follow-up sweep logged reimbursement updates, pipeline milestones from Questel patents, and trade-association data, giving comparable country sheets before any numbers reached our model. These listed sources are illustrative; many additional references supported validation.

Market-Sizing & Forecasting

We start with a top-down prevalence-to-treated cohort build for every country, multiply the cohort by region-specific dosing intensity and blended average selling prices, and then cross-check totals with selective bottom-up shipment roll-ups. Key inputs include diagnosed prevalence, diagnostic-delay trends, prophylaxis uptake curve, plasma-collection growth, and payer policy shifts. Multivariate regression plus scenario analysis carries these drivers through 2030, and residual gaps are spread in line with verified epidemiology.

Data Validation & Update Cycle

Outputs pass analyst, senior peer, and domain lead reviews; variance triggers tied to price swings, approvals, or supply shocks force recalibration. Reports refresh yearly, and a final pre-delivery sweep ensures clients receive the latest view.

Why Mordor's Plasma Protease C1-inhibitor Market Baseline Earns Trust

Published estimates often diverge because firms choose different drug baskets, geography mixes, and currency conventions.

By rooting our baseline in real epidemiology and audited manufacturer revenue, we deliver a balanced middle ground. Key gap drivers elsewhere include frozen 2024 exchange rates, omission of oral kallikrein launches, narrow region lists, and reliance on historic prices without inflation indexing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.01 B (2025) | Mordor Intelligence | None |

| USD 3.54 B (2024) | Global Consultancy A | Excludes oral blockers; pre-launch prevalence |

| USD 1.80 B (2024) | Trade Journal B | Limited regions; old price assumptions |

| USD 0.91 B (2024) | Industry Association C | Counts only plasma-derived hospital sales |

These side-by-side numbers show that our disciplined scope choices, transparent variables, and annual refresh give decision-makers a dependable, reproducible baseline.

Key Questions Answered in the Report

What is the current size of the plasma protease C1-inhibitor market?

The plasma protease C1-inhibitor market reached USD 4.38 billion in 2026 and is on course for USD 6.77 billion by 2031 on a 9.12% CAGR trajectory (2026-2031).

Which drug class is growing fastest within this market?

Oral plasma-kallikrein inhibitors, led by BioCryst’s ORLADEYO and pending entrants such as sebetralstat, are projected to grow at an 11.02% CAGR through 2031.

Why are plasma supply constraints a concern?

The United States collects roughly 70% of global plasma, and European health systems estimate a shortfall of two million donors, leaving many regions vulnerable to supply disruptions that could restrain therapy availability.

How is patient preference shaping product development?

Demand for needle-free, home-based treatment is steering R&D toward oral tablets and autoinjectors, evidenced by rapid sales growth for subcutaneous and oral formulations over traditional intravenous infusions.

Which region is expected to offer the highest growth opportunity?

Asia-Pacific leads with a 10.11% CAGR, powered by China’s expanded rare-disease policies, rising healthcare budgets, and new local plasma fractionation facilities that secure supply.

What impact will new FDA approvals have on the competitive landscape?

The 2025 approval of garadacimab introduces the first Factor XII inhibitor, while a positive decision on sebetralstat would establish the first oral on-demand therapy, intensifying competition and accelerating the shift to patient-centric regimens.

Page last updated on: