Size and Share of Protective Clothing Market for Life Sciences Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

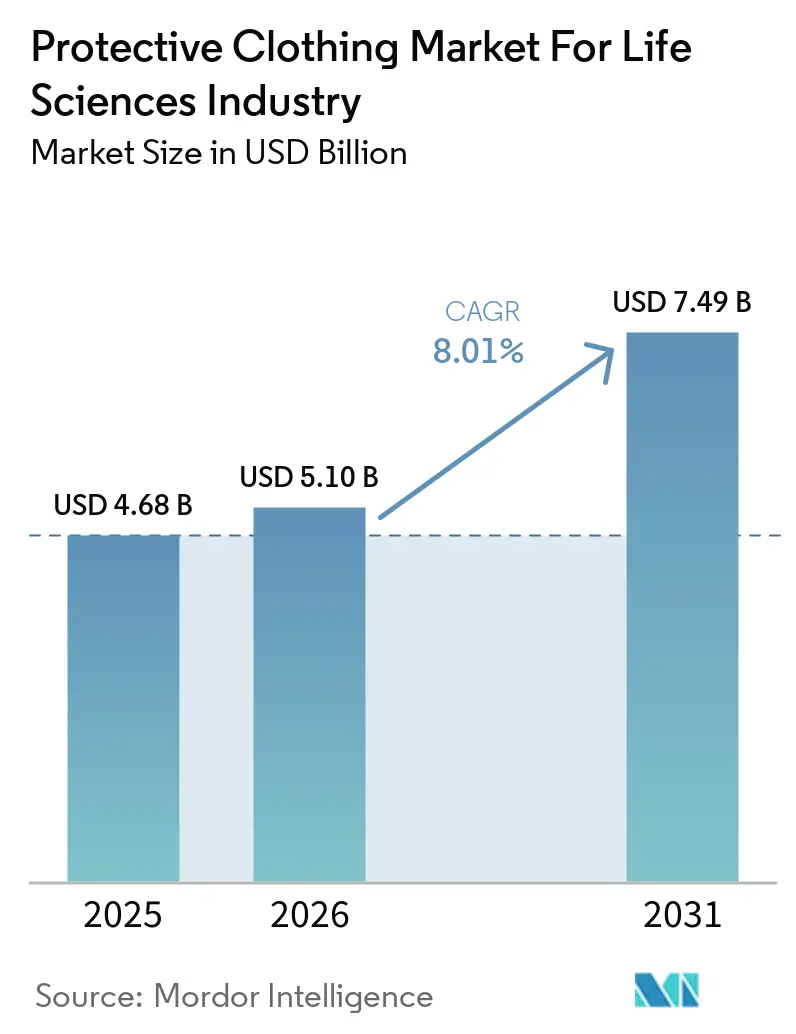

| Market Size (2026) | USD 5.10 Billion |

| Market Size (2031) | USD 7.49 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

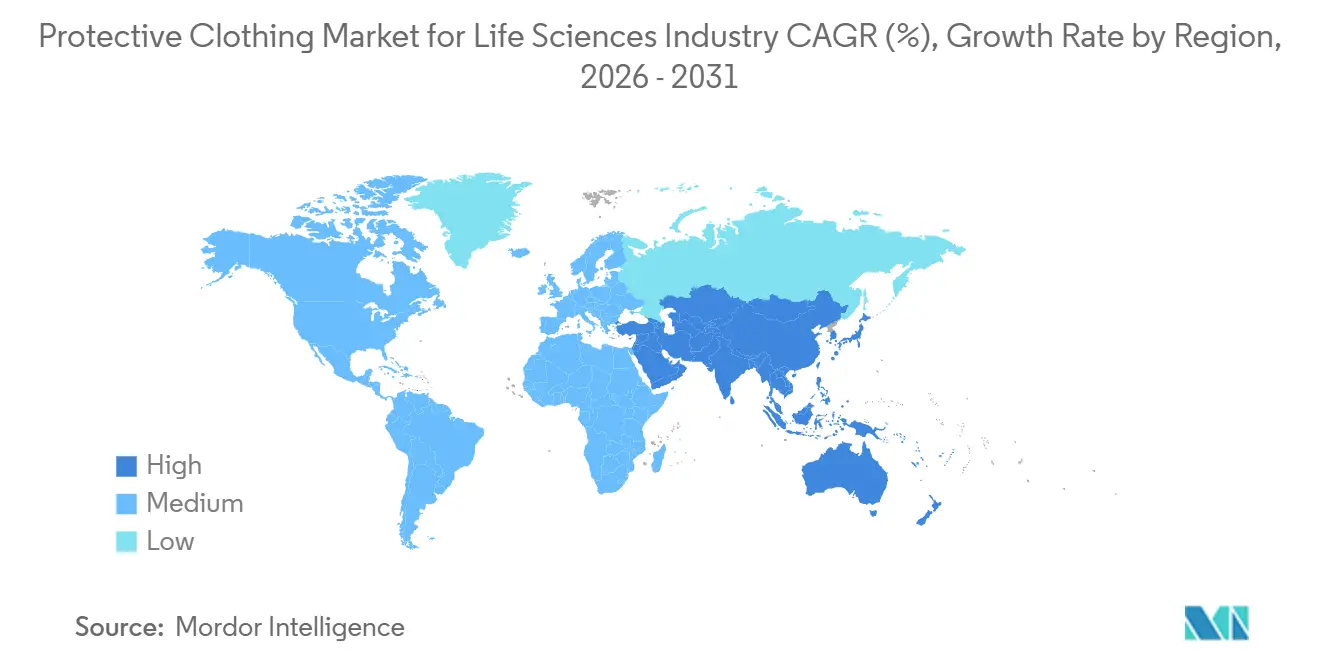

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

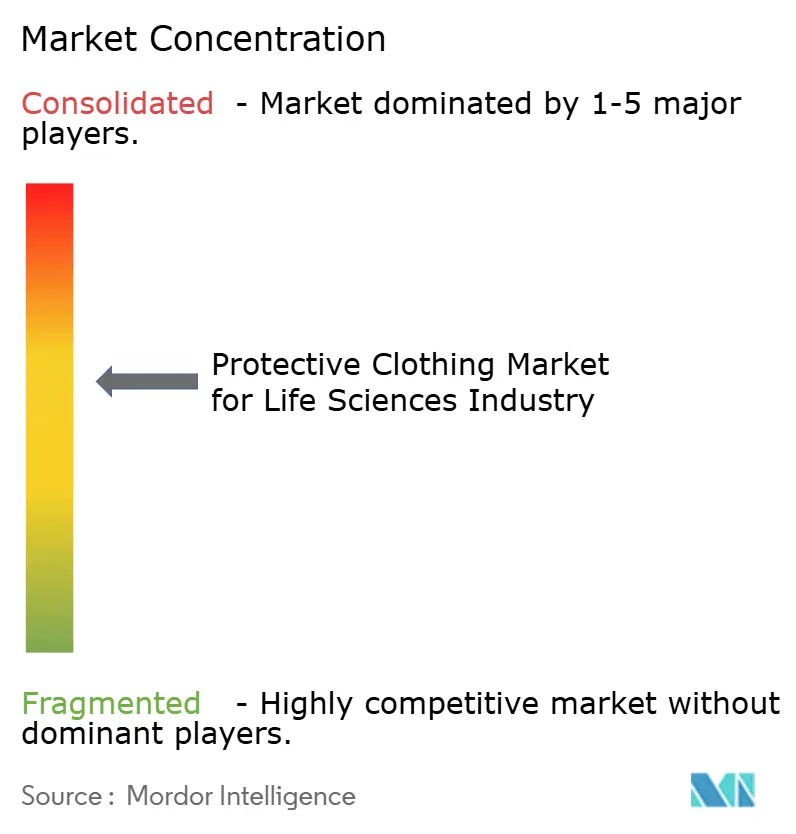

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Protective Clothing Market for Life Sciences Industry by Mordor Intelligence

The protective clothing market size is projected to expand from USD 4.68 billion in 2025 and USD 5.10 billion in 2026 to USD 7.49 billion by 2031, registering a CAGR of 8.01% between 2026 to 2031. Rising demand is now anchored in cell and gene therapy manufacturing, tighter EU and ISO gowning rules, and faster change-outs enabled by single-use garments. Vendors are adjusting product lines toward bio-circular feedstocks as large pharmaceutical buyers embed climate metrics in sourcing scorecards. Regulatory convergence, especially ISO 14644-5:2025, is driving standardized competency assessments that raise switching costs for non-compliant apparel. Moderate market concentration leaves room for regional specialists, yet recent mergers show global players consolidating route-to-market efficiencies.

Key Report Takeaways

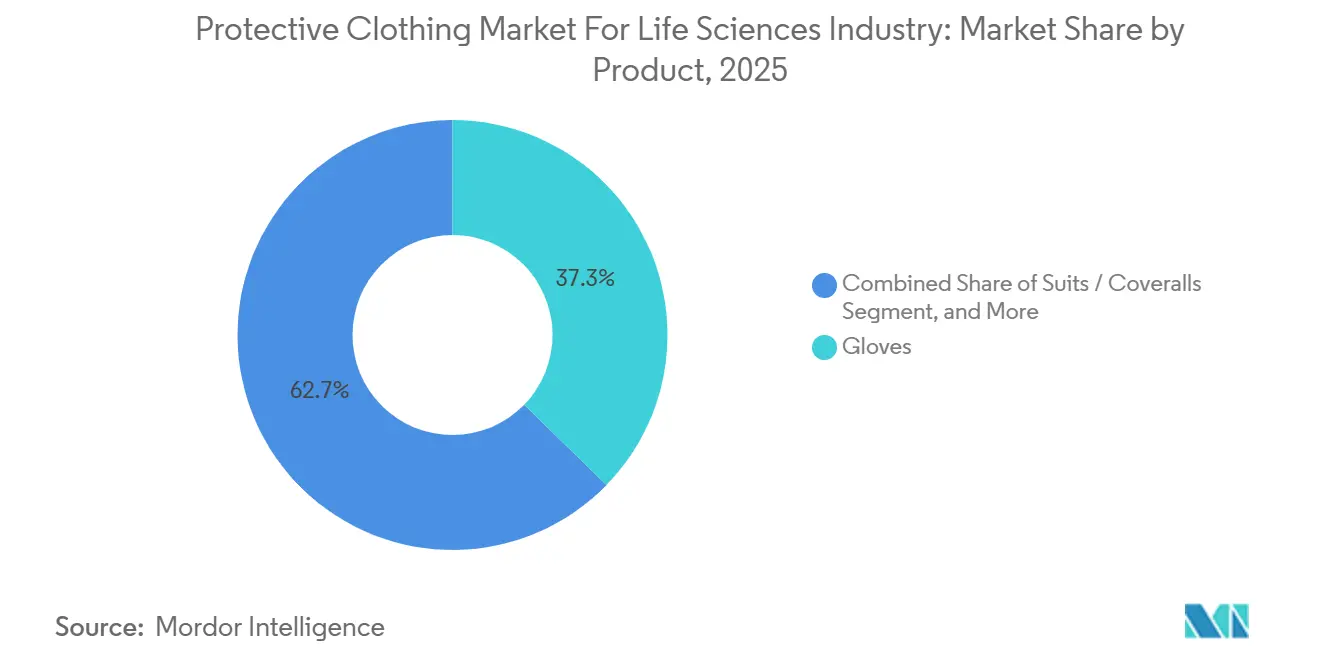

- By product, gloves captured 37.29% revenue in 2025, while suits and coveralls will post the highest 8.99% CAGR through 2031.

- By material, Tyvek commanded 28.41% of 2025 share, yet microporous film laminates are expanding at an 8.91% rate to 2031.

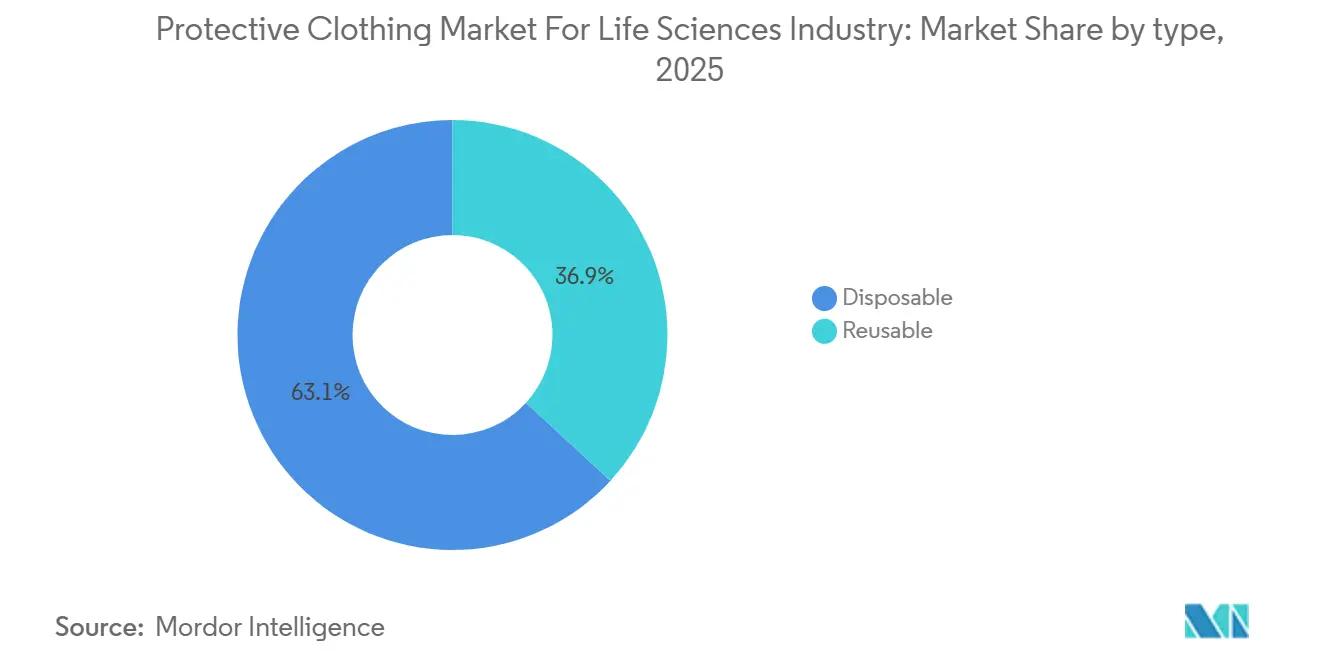

- By type, disposable formats held 63.15% of 2025 value, but reusable garments are advancing at a 9.01% CAGR on forthcoming textile stewardship laws.

- By application, cleanroom clothing represented 46.74% demand in 2025, and cell and gene therapy cleanrooms are growing fastest at 9.06%.

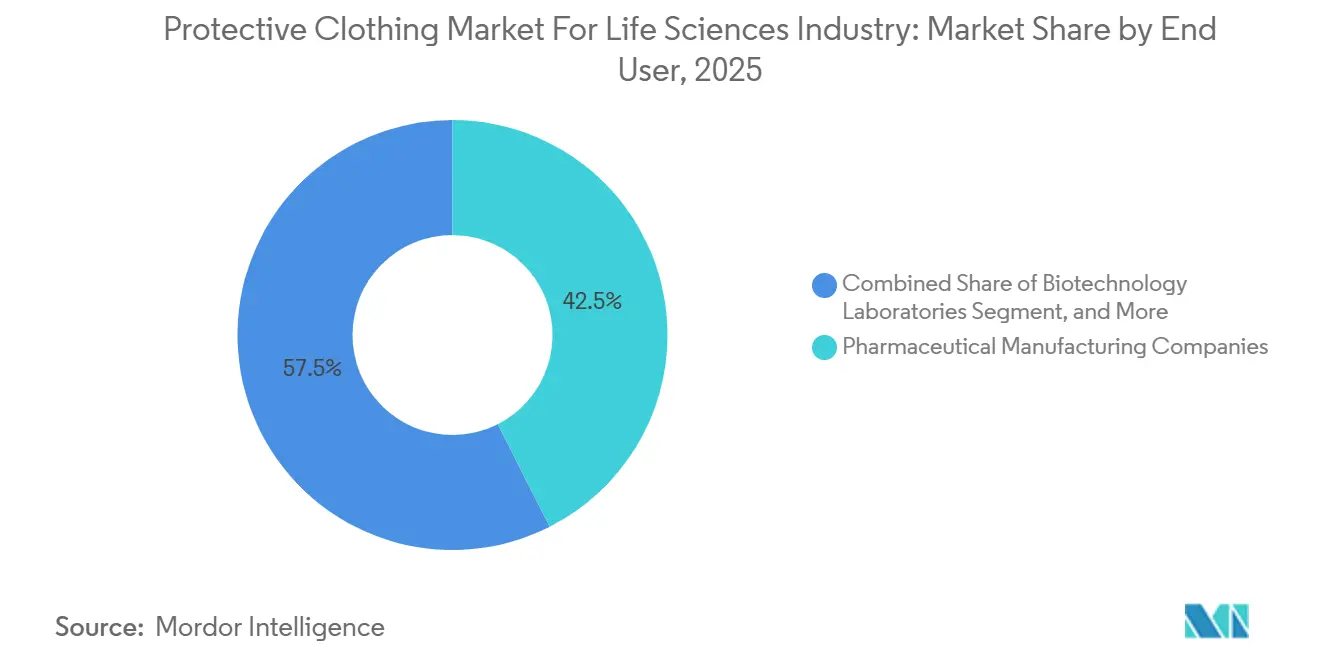

- By end user, pharmaceutical manufacturers spent 42.53% of 2025 outlays, whereas contract manufacturing and research organizations are rising at an 8.84% CAGR.

- By geography, North America led with 39.84% share in 2025, and Asia-Pacific is forecast to climb at a 9.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Protective Clothing Market for Life Sciences Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Regulatory Standards on Patient Safety | +1.80% | Global, with heightened enforcement in North America and EU | Medium term (2-4 years) |

| Growth in Biotechnology and Healthcare Spending | +1.50% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Rising Adoption of Single-Use Cleanroom Apparel | +1.30% | North America and EU, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Enforcement of Occupational Safety Norms in Emerging Markets | +1.10% | Asia-Pacific core, Middle East and Africa secondary | Medium term (2-4 years) |

| Integration of Smart Protective Textiles for Contamination Monitoring | +0.70% | North America and EU pilot sites, Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Expansion of Cell and Gene Therapy Manufacturing Facilities | +1.40% | North America primary, Europe and Asia-Pacific secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Regulatory Standards on Patient Safety

Revisions to EU Regulation 2016/425 have harmonized four barrier-performance standards, compelling suppliers to validate microbial and liquid penetration resistance under uniform laboratory methods. ISO 14644-5:2025 now prescribes recorded competency checks, meaning procurement contracts increasingly bundle garments with annual requalification services.[1]European Commission, “Commission Implementing Decision 2025/2078,” European Commission, europa.eu U.S. FDA warning letters doubled year-on-year in early 2026, with 40% citing contamination control gaps, a signal that domestic plants must tighten gowning discipline. Draft ISO/DIS 22615 will introduce risk classes for apparel against infectious agents, foreshadowing new label claims that could reset buyers’ specification lists. AAMI PB70 Level 4 remains the North American gold standard for high-risk zones, keeping demand strong for multi-layer fabrics.[2]U.S. Food and Drug Administration, “Warning Letters and Enforcement Actions,” fda.gov

Growth In Biotechnology and Healthcare Spending

Advanced therapy medicinal product pipelines are scaling aggressively as R&D budgets stay in double-digit territory. CDMOs booked USD 173 billion revenue in 2024 and are tracking toward USD 323 billion by 2033, stoking appetite for validated garment inventories at new fill-finish suites. Mega-facilities in Chengdu, Singapore, and North Carolina each need millions of cleanroom pieces per year once fully online. Capital intensity is high, so sponsors embed garment lifecycle cost models into project economics from day one. Asia-Pacific capacity adds are diversifying sourcing, yet North America still anchors premium-priced biologics runs that specify low-lint fabrics.[3]KPMG, “Biotechnology R and D Expenditure Trends,” kpmg.com

Rising Adoption of Single-Use Cleanroom Apparel

Disposable coveralls are accelerating because they remove revalidation cycles and trim cross-contamination risk when plants pivot between multiple drug substances. DuPont’s Tyvek 500 Xpert BioCircle debut shows how bio-circular feedstocks can meet Type 5 and Type 6 norms while cutting greenhouse gas footprints by 58%. Corporates with science-based targets now quantify cradle-to-gate emissions in bid evaluations, lifting demand for environmental product declarations. California SB 707 and an impending EU textile EPR add a compliance surcharge to disposables after 2031, nudging some buyers toward mixed fleets that pair single-use suits with reusable hoods and boots. Nearshoring of glove production by major distributors is another hedge against pandemic-style supply crunches.

Expansion Of Cell and Gene Therapy Manufacturing Facilities

A wave of USD 1 billion-plus campuses in Pennsylvania, California, and South Korea requires ISO Class 7 suites outfitted with full-body barrier systems. Seam-sealed coveralls with integrated hoods and boots are now the default bill of materials because they minimize skin flakes in unidirectional airflow zones. Robotic gowning modules introduced by automated cell therapy platforms cut human touchpoints and support more consistent aseptic technique. The FDA’s updated gene therapy CMC guidance tightens environmental monitoring expectations, translating to larger inventories of pre-sterilized garments to avoid downtime. Investors consequently factor garment logistics into overall facility throughput models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Technical Fabric Supply Chains | -1.20% | Global, with acute pressure in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Higher Lifecycle Cost of Reusable Garments | -0.90% | North America and EU, limited impact in Asia-Pacific | Medium term (2-4 years) |

| Stringent Environmental Rules on Disposal and Incineration | -0.60% | EU primary, California secondary, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Skill Shortage Hampering Correct Gowning Compliance | -0.80% | Global, with higher incidence in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Technical Fabric Supply Chains

Middle East geopolitical disruption lifted polypropylene resin to a USD 890-1,030 per ton band in 2026, squeezing SMS fabric converters. Force-majeure notices from Gulf suppliers forced apparel makers to shift volumes to higher-cost European mills, inflating finished-goods prices within weeks. Limited petrochemical integration means buyers have little leverage when naphtha crackers idle for security reasons. Tyvek production depends on proprietary flash-spun lines, which buffer resin swings yet concentrate single-source risk. Buyers now negotiate dual-supply clauses and safety-stock buffers that raise working capital requirements.

Higher Lifecycle Cost of Reusable Garments

Reusable suits demand laundering, sterilization, and requalification, pushing total ownership above disposables unless a 50-cycle threshold is met. Gamma irradiation at 25 kGy degrades polyester fibers, so filtration efficiency can dip below 90% before end-of-life, creating unplanned replacement costs. One multinational saw gowning violation jump 30% post transition, attributing non-compliance to insufficient retraining on inspection routines. Average contamination remediation tops USD 3.1 million per year, quickly erasing any projected savings from reuse. Smaller CDMOs often lack in-house validation labs, leaving them dependent on specialty laundries with long lead times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Gloves Dominate, Suits Accelerate

Gloves accounted for 37.29% of the protective clothing market size in 2025 because every cleanroom task mandates hand coverage. Demand spans compounding labs to ISO Class 5 aseptic cores, giving glove vendors a stable replacement cycle. Suits and coveralls trail in revenue yet register the fastest 8.99% CAGR, buoyed by cell therapy operators that require integrated hoods and boots. Aprons remain niche for splash zones where mobility trumps full-body coverage, while face masks, hats, goggles, and footwear ride along in bundled sterile kits that simplify warehouse picking. Wipes, though technically consumables, stay on the same purchase orders because they sanitize gowning benches and carts. As workers favor lighter fabrics, Tyvek APX’s improved breathability is expected to lift compliance and cut heat-stress breaks, trends that enhance throughput in high-volume fill-finish suites.

The protective clothing market continues to gravitate toward kits that pre-bundle coveralls, gloves, and masks, reducing picking errors and gowning time. Vendor-managed inventory programs place radio-frequency tags on each component, enabling real-time consumption analytics that feed enterprise planning systems. That transparency, coupled with ISO 14644-5 competency logs, is now a differentiator in bid evaluations. Full-body systems also dovetail with robotic filling lines, which require fewer human interventions and thus fewer gown changes per shift. Overall, the product mix evolution supports a higher average selling price trajectory for the protective clothing market.

By Material: Microporous Films Challenge Tyvek

Tyvek and other HDPE flash-spun fabrics commanded 28.41% share in 2025 on the back of decades of validated bioburden data. Microporous film laminates are growing at 8.91% as their liquid repellence and ultralow lint rates outperform SMS in ISO Class 5 suites. SMS fabric still dominates routine Grade C&D zones thanks to attractive unit economics, but resin volatility is eroding that advantage. Polyethylene-coated polypropylene satisfies inspection rooms where splash risk is minimal, making it a budget pick for late-stage packaging. Reusable woven polyester, grouped under the rest-of-materials bucket, is gaining traction in Europe, where EPR rules penalize single-use waste, yet its adoption remains tied to the availability of validated laundering hubs.

Sustainability themes now push material science forward. Bio-circular feedstocks in Tyvek 500 Xpert BioCircle reduce cradle-to-gate emissions by more than half, and such environmental product declarations are starting to appear in public tenders. Microporous films additionally answer liquid chemical challenges in advanced therapy production, where accidental spills can compromise batch sterility. Vendors that blend barrier performance with climate metrics will likely secure preferred-supplier status as procurement teams add Scope 3 emissions to scorecards. The protective clothing market must therefore juggle cost, compliance, and carbon goals simultaneously.

By Type: Reusables Narrow Disposable Lead

Disposable items represented 63.15% value in 2025, buoyed by pandemic-era stockpiling and convenience. Yet reusable garments are pacing at a 9.01% CAGR as California and EU textile laws impose stewardship fees on throw-away apparel from 2031 onward. Lifecycle analyses show reusables cut water use by up to 77% and solid waste by as much as 96%, though only when laundering hits 50 cycles without barrier loss. Training gaps can erode those gains, as evidenced by spike in gowning deviations at plants that switched too quickly. CDMOs with lean staff often lack autoclave redundancy, so third-party laundries fill the void but extend turnaround times.

Single-use producers counter with closed-loop recycling pilots that convert post-consumer gowns into construction panels, aiming to offset future EPR fees. Meanwhile, hybrid programs pair reusable coveralls with disposable hoods and gloves, striking a middle ground on cost and waste. Such flexibility keeps procurement options open while regulatory details finalize. The competitive narrative shows each type carving space, and the protective clothing market benefits from dual-track innovation.

By Application: Cell Therapy Cleanrooms Surge

Cleanroom clothing captured 46.74% of 2025 demand across pharma, biotech, and device plants. Inside that total, cell and gene therapy suites are expanding at 9.06% as multiple USD 1 billion campuses come online. Radiation protection garments, mainly lead-lined aprons, continue steady replacement in diagnostic labs, while bacterial and viral apparel volumes have normalized post pandemic but stay elevated in BSL-3 sites. Chemical splash protection remains essential in high-potency API synthesis, with ASTM F739 permeation data guiding fabric selection. Particulate control in ISO Class 8 packaging uses lighter, cost-optimized coveralls.

New ISO 14644-5 rules mean every application now requires documented gowning competency, pushing facilities to integrate learning-management modules with badge readers at airlocks. Consequently, vendors offering digital training alongside garments gain share. As advanced therapies move toward closed and automated systems, some Grade B zones may downgrade to Grade C, altering garment perf requirements and potentially shrinking volumes per batch. Even so, overall order frequency still rises because the protective clothing market ties directly to the growing therapy pipeline.

By End User: Outsourcing Model Expands

Pharmaceutical manufacturers retained 42.53% spending in 2025, yet the fastest 8.84% CAGR comes from CMOs and CROs that ride the biologics outsourcing boom. WuXi Biologics alone will need roughly 2 million garments a year once Chengdu and Singapore lines hit full tilt. Biotechnology labs, often early-stage startups, emphasize cost, selecting disposable kits that minimize upfront capital. Medical device firms follow ISO 13485:2016 mandates, keeping steady baseline demand for low-lint fabric. Diagnostic and research labs continue modest growth, especially where governments fund infectious disease surveillance.

Wholesalers, compounding pharmacies, and contract sterilizers form a fragmented tail end but still influence volume buys because they aggregate multi-site orders. Investment in RFID-based inventory management by large distributors gives those smaller customers real-time visibility, encouraging predictable reorder patterns. Consequently, channel partnerships matter more than ever, and vendors that lock in multi-year agreements with logistics intermediaries gain scale quickly. The outsourcing wave cements a diverse purchasing base, underpinning resilience in the protective clothing market.

Geography Analysis

Protective Clothing Market for Life Sciences Industry in North America

North America led the protective clothing market with 39.84% share in 2025, supported by a dense cluster of contract development and manufacturing organizations and strict FDA oversight. Ongoing automation in U.S. and Canadian plants tempers labor needs but raises per-worker apparel specifications because each operator now services more critical steps. Mexico’s nearshoring incentives bolster garment assembly lines that feed North American buyers, shortening replenishment cycles.

Asia-Pacific is on track for a 9.15% CAGR to 2031, narrowing the gap with North America. China’s May 2026 Hazardous Chemicals Safety Law obligates employers to fund certified personal protective equipment, expanding addressable volumes across thousands of provincial biotech labs. South Korea’s Samsung Biologics Plant 5 came online with 180,000 liters of capacity, while India’s revised Labour Codes place legal liability squarely on employers for exposure events, prompting local subsidiaries of multinationals to upgrade from SMS to microporous suits. Japan’s aging workforce drives adoption of lighter, ergonomically cut garments that reduce fatigue in prolonged aseptic shifts.

Europe remains a regulation-driven market where Commission Implementing Decision 2025/2078 harmonizes four apparel standards under a single CE-marking pathway. Germany and the United Kingdom continue as the largest spending pockets, although France and Italy see renewed investment tied to on-shoring of high-value sterile injectables. Eastern European sites gain attractiveness because of skilled labour pools and lower utility tariffs, a dynamic that balances overall pricing tension. South America increments moderately, centered on Brazil’s contract vaccine capacity, whereas the Middle East and Africa cluster expands mainly in Saudi Arabia and Egypt where pharma industrial zones receive tax holidays. Collectively, these regional nuances sustain diversified growth in the protective clothing market.

Competitive Landscape

The top five suppliers hold roughly one-half of global revenue, defining a moderate concentration that leaves space for specialists. Ansell’s USD 640 million purchase of Kimberly-Clark’s PPE arm unifies Kimtech and KleenGuard labels under one distributor, yielding procurement leverage and broader catalog depth. Honeywell’s USD 1.325 billion divestiture to PIP removes a diversified industrial player, freeing shelf space for niche biosciences brands. DuPont retains technology leadership with Tyvek and its new BioCircle line that cuts cradle-to-gate emissions by 58%, appealing to buyers with net-zero pledges.

Emerging disruptors focus on automation and smart textiles. Cellares’ robotic gowning modules reduce human contact, meeting revised ISO 14644-5 competency requirements with data logs that auditors can trace. Riverstone Holdings, a Malaysian glove manufacturer posting FY 2025 net profit of RM 207.8 million (USD 49 million), scales through multi-national plants that hedge geopolitical risk.

University-born prototypes embed sensors directly into fabric, promising real-time alerts on particulate breaches once sterilization durability is solved. Channel power is gravitating to distributors that overlay RFID analytics, so vendors able to integrate digital inventory dashboards are winning long-term agreements. Overall, innovation runs on parallel tracks of sustainability and data, reshaping competitive priorities in the protective clothing market.

Leaders of Protective Clothing Market for Life Sciences Industry

E. I. DuPont De Nemours and Company

Kimberly Clark Corporation

Ansell Limited

3M Company

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DuPont launched Tyvek 500 Xpert BioCircle, integrating bio-circular feedstock and delivering a 58% lower climate impact while retaining Type 5 and Type 6 certification.

- March 2026: Cintas Corporation acquired UniFirst Corporation for USD 5.5 billion, creating a network of 500 sites that expands validated reusable garment services.

- December 2025: Medline Industries completed a USD 54 billion IPO earmarked for single-use cleanroom expansion and RFID-enabled inventory platforms.

- November 2025: DuPont introduced Tyvek APX, a breathable coverall aimed at reducing heat stress inside Grade B suites.

Scope of Report on Protective Clothing Market for Life Sciences Industry

The Protective Clothing Market refers to the global industry focused on the design, production, and distribution of specialized garments that safeguard individuals from physical, chemical, biological, thermal, and mechanical hazards across various sectors such as healthcare, manufacturing, construction, defense, and firefighting.

The Protective Clothing Market for Life Sciences Industry Report is Segmented by Product (Suits / Coveralls, Gloves, Aprons, Face Masks and Hats, Protective Eyewear and Cleanroom Goggles, Footwear and Overshoes, Wipes, and Other Products), Material (Spun-bond-Melt-blown-Spun-bond (SMS) Fabric, Tyvek and Other High-Density Polyethylene, Microporous Film Laminates, Polyethylene-Coated Polypropylene, and Other Materials), Type (Disposable and Reusable), Application (Cleanroom Clothing, [Pharmaceutical, Biotechnology, and Medical], Radiation Protection, Bacterial / Viral Protection, Chemical Protection, and Other Applications), End User (Pharmaceutical Manufacturing Companies, Biotechnology Laboratories, Medical Device Manufacturers, Diagnostic and Research Laboratories, Contract Manufacturing and Contract Research Organizations, and Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Suits / Coveralls |

| Gloves |

| Aprons |

| Face Masks and Hats |

| Protective Eyewear and Cleanroom Goggles |

| Footwear and Overshoes |

| Wipes |

| Other Products |

| Spun-bond-Melt-blown-Spun-bond (SMS) Fabric |

| Tyvek and Other High-Density Polyethylene |

| Microporous Film Laminates |

| Polyethylene-Coated Polypropylene |

| Other Materials |

| Disposable |

| Reusable |

| Cleanroom Clothing | Pharmaceutical |

| Biotechnology | |

| Medical | |

| Radiation Protection | |

| Bacterial / Viral Protection | |

| Chemical Protection | |

| Other Applications |

| Pharmaceutical Manufacturing Companies |

| Biotechnology Laboratories |

| Medical Device Manufacturers |

| Diagnostic and Research Laboratories |

| Contract Manufacturing and Contract Research Organizations |

| Other End-Users |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product | Suits / Coveralls | |

| Gloves | ||

| Aprons | ||

| Face Masks and Hats | ||

| Protective Eyewear and Cleanroom Goggles | ||

| Footwear and Overshoes | ||

| Wipes | ||

| Other Products | ||

| By Material | Spun-bond-Melt-blown-Spun-bond (SMS) Fabric | |

| Tyvek and Other High-Density Polyethylene | ||

| Microporous Film Laminates | ||

| Polyethylene-Coated Polypropylene | ||

| Other Materials | ||

| By Type | Disposable | |

| Reusable | ||

| By Application | Cleanroom Clothing | Pharmaceutical |

| Biotechnology | ||

| Medical | ||

| Radiation Protection | ||

| Bacterial / Viral Protection | ||

| Chemical Protection | ||

| Other Applications | ||

| By End User | Pharmaceutical Manufacturing Companies | |

| Biotechnology Laboratories | ||

| Medical Device Manufacturers | ||

| Diagnostic and Research Laboratories | ||

| Contract Manufacturing and Contract Research Organizations | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the protective clothing market be by 2031?

Forecasts indicate USD 7.49 billion by 2031, reflecting an 8.01% CAGR from 2026.

Which region shows the fastest demand growth for protective garments?

Asia-Pacific leads with a projected 9.15% CAGR through 2031, driven by China’s new safety law and expanding biologics capacity.

What product category is expanding quickest within protective apparel?

Suits and coveralls will climb at an 8.99% CAGR as cell and gene therapy plants require full-body barriers.

How are sustainability mandates influencing buying decisions?

Upcoming textile EPR laws and corporate climate targets are shifting purchases toward bio-circular disposables and validated reusables.

Why are CMOs and CROs boosting their apparel spending?

Outsourced biologics production is expanding at 15% annually, which lifts garment orders for new fill-finish suites and ISO 7 cleanrooms.

What is the main supply-chain risk facing protective clothing makers?

Polypropylene resin volatility and single-source dependence for flash-spun fabrics can spike input costs and disrupt deliveries.

Page last updated on: