Probiotic Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

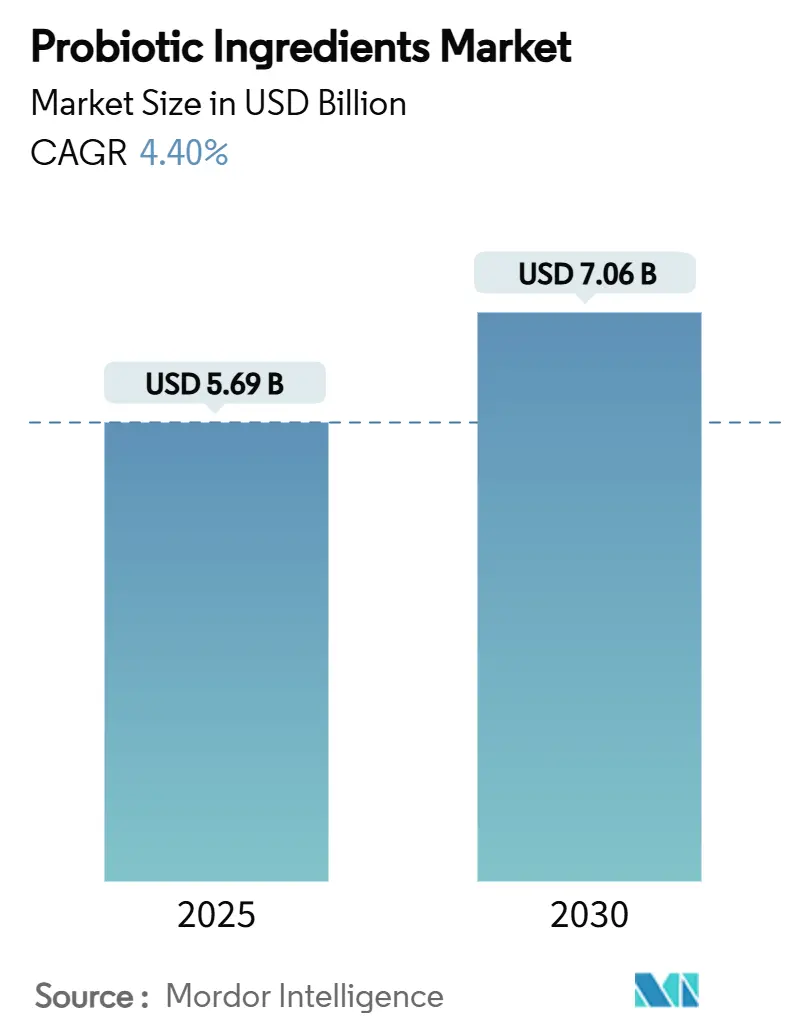

| Market Size (2025) | USD 5.69 Billion |

| Market Size (2030) | USD 7.06 Billion |

| Growth Rate (2025 - 2030) | 4.40% CAGR |

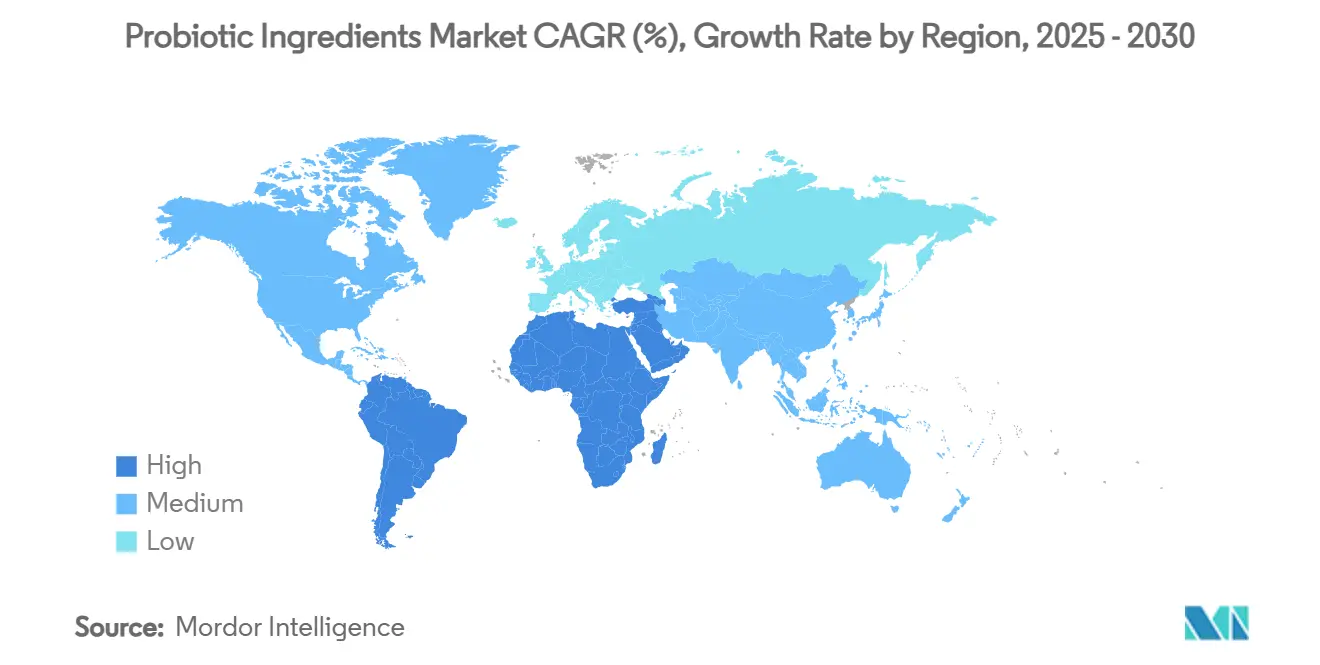

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

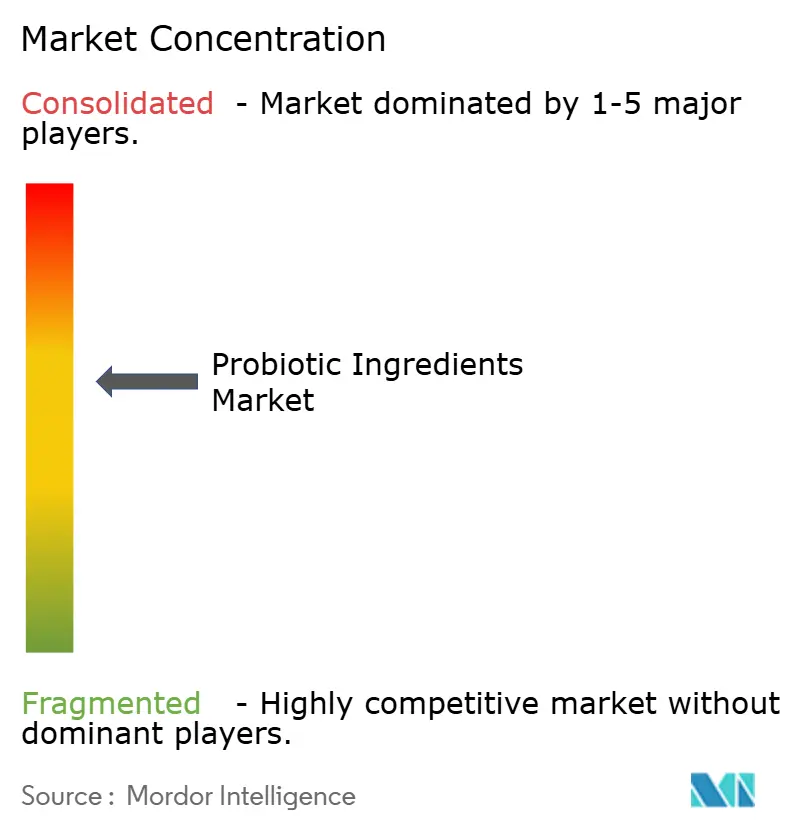

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Probiotic Ingredients Market Analysis by Mordor Intelligence

The probiotic ingredients market is estimated to be USD 5.69 billion in 2025 and is projected to reach USD 7.06 billion by 2030, growing at a steady CAGR of 4.40% during the forecast period. The market growth is attributed to increased consumer adoption of preventive healthcare, continuous scientific validation of strain-specific benefits, and supportive regulatory frameworks. The dietary supplements segment is projected to grow at a 7.33% annual rate through 2030, driven by demand for personalized nutrition solutions. Besides, Asia-Pacific remains the primary market by volume, supported by an established consumer base and manufacturing infrastructure. Additionally, South America is forecasted to demonstrate the highest growth rate due to rising consumer awareness and increased purchasing power. Manufacturers are implementing technologies such as microencapsulation to enhance product stability and longevity. Industry consolidation continues, as demonstrated by the January 2024 formation of Novonesis, highlighting the requirement for operational scale in research, manufacturing, and distribution to maintain market competitiveness.

Key Report Takeaways

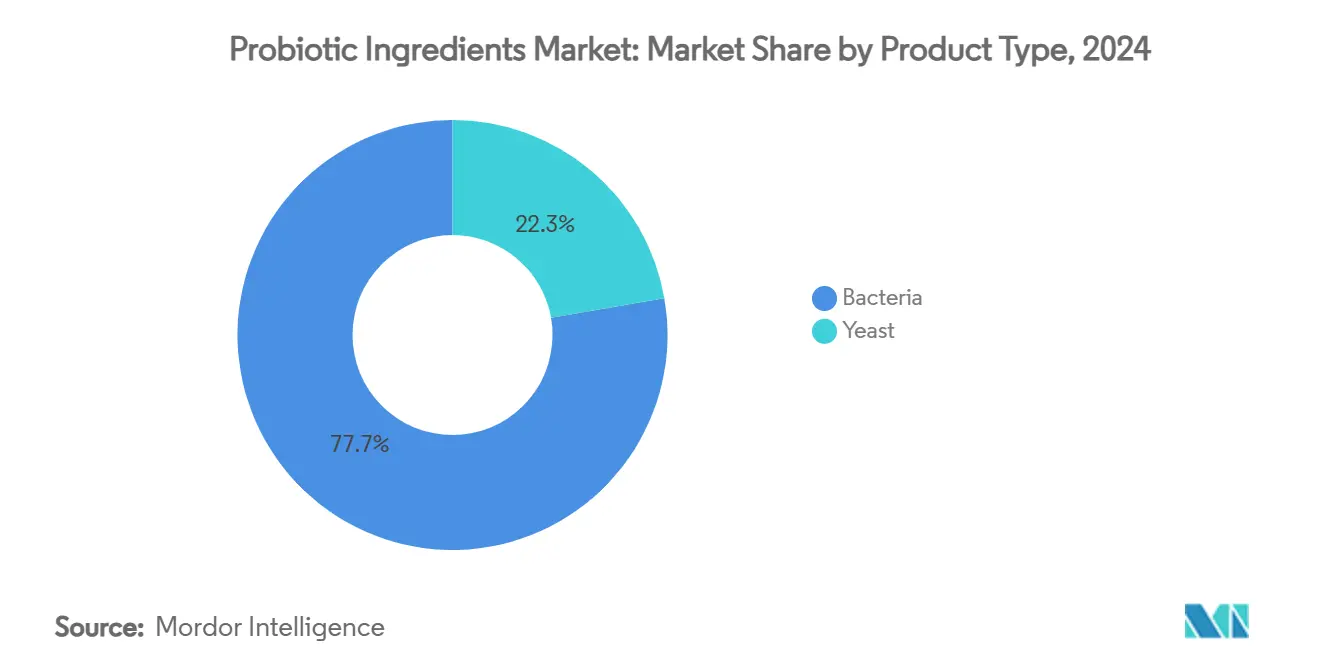

- By product type, bacteria-based formulations captured 77.74% of the probiotic ingredients market share in 2024, while yeast-based alternatives are projected to expand at 7.27% CAGR through 2030.

- By form, powder formats held 54.54% share of the probiotic ingredients market in 2024; liquid formats are forecast to post a 6.33% CAGR to 2030.

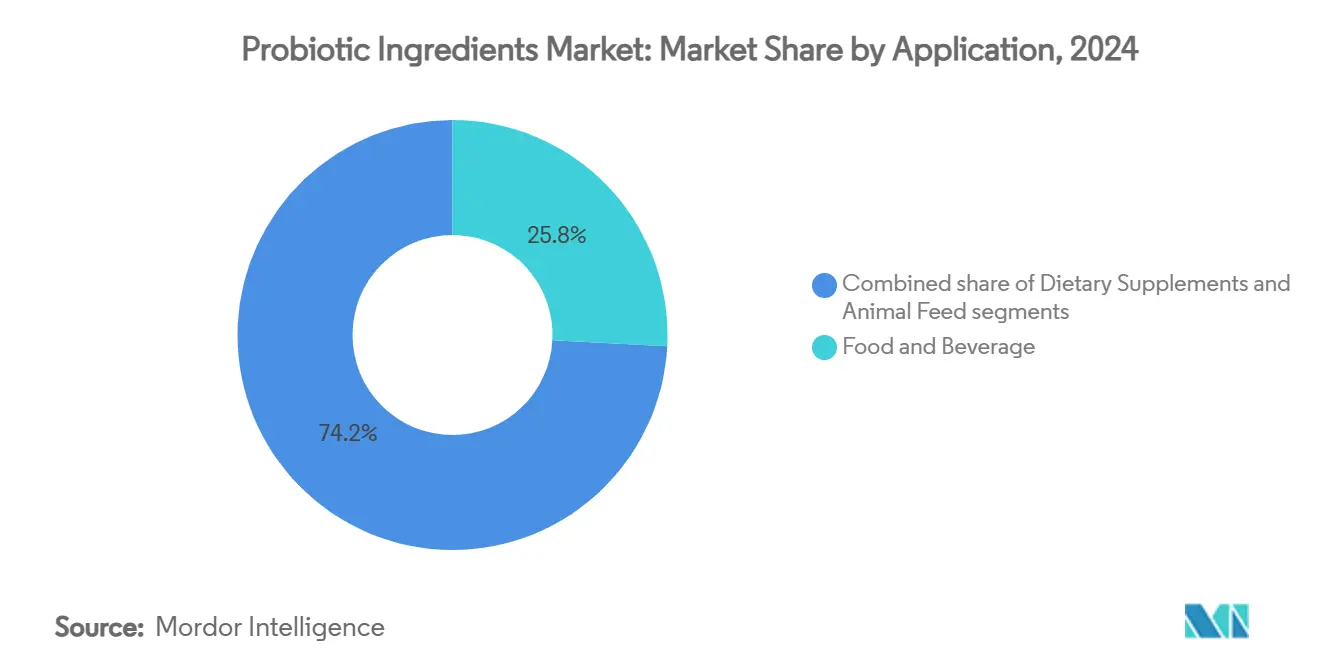

- By application, food and beverage accounted for 25.83% revenue in 2024, whereas dietary supplements are progressing at a 7.33% CAGR between 2025 and 2030.

- By geography, Asia-Pacific commanded 33.45% of revenue in 2024, and South America is expected to grow 5.12% annually from 2025 to 2030.

Global Probiotic Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for digestive health products | +1.5% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Growing demand for functional foods and beverages | +1.0% | Global, with significant impact in Asia-Pacific | Short term (≤ 2 years) |

| Expanding application in animal feed for gut health | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Popularity of plant-based and fermented probiotic products | +0.8% | Global, with higher impact in Europe and North America | Short term (≤ 2 years) |

| Innovations in probiotic formulations | +0.9% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Favorable regulations boost probiotic credibility | +0.7% | Europe, North America, with spillover to Asia-Pacific | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Demand for Digestive Health Products

The increasing awareness of the integral relationship between gut health and overall wellness has significantly boosted the demand for digestive health products, with probiotics at the forefront of this growth. This paradigm shift from reactive to preventive healthcare has firmly established probiotics as a staple in daily wellness regimens. Advancements in scientific research continue to reveal their multifaceted benefits, extending beyond digestive support to include immune system enhancement and potential mental health improvements through the gut-brain axis. For instance, studies conducted by Stanford University have highlighted the evolving role of probiotics, uncovering new opportunities for market expansion [1]Source: Stanford University, "Probiotics, Prebiotics, and Postbiotics: What Are They and Why Are They Important?", stanford.edu . This scientific backing resonates with a more informed and health-conscious consumer base, which increasingly favors strain-specific probiotics designed to address targeted health concerns over generic, one-size-fits-all solutions. As the trend toward personalized nutrition accelerates, companies are strategically adapting their product development strategies to focus on clinically validated probiotic strains with proven efficacy. This approach not only meets consumer demand but also positions businesses to thrive in an increasingly competitive and dynamic market.

Growing Demand for Functional Foods and Beverages

The probiotic market has expanded beyond traditional dairy products into functional foods and beverages, reflecting consumer demand for health-enhancing food products. The market growth is driven by new product development, including probiotic-enriched granola bars, salad dressings, plant-based yogurts, and fermented beverages such as kombucha and kefir. Companies like Danone and PepsiCo are diversifying their probiotic product portfolios with convenient formats for health-conscious consumers, while new market entrants focus on specific consumer segments with gut health products. Also, advancements in microencapsulation technology have enhanced probiotic stability during manufacturing, extended product shelf life, and improved survival through digestion. This technology enables the integration of live cultures into products with high heat or acidity, such as baked goods and citrus beverages, while maintaining their efficacy. Companies like Ganeden, acquired by Kerry Group, have developed shelf-stable probiotic products, improving distribution efficiency and market penetration, particularly in developing regions. The integration of convenience, taste, and digestive health benefits is increasing consumer adoption of probiotic products.

Expanding Application in Animal Feed for Gut Health

Driven by regulatory pressures to curtail antibiotic use in livestock, the shift towards probiotics in animal nutrition is carving out a significant market opportunity. Research from Penn State University in 2024 highlights that probiotic feed additives not only bolster intestinal health in poultry but also enhance growth rates, positioning them as a credible substitute for traditional growth-promoting antibiotics [2]Source: The Pennsylvania State University, "Probiotic Feed Additive Boosts Growth, Health in Poultry in Place of Antibiotics", psu.edu. This trend gains momentum as global regulations tighten their grip on antibiotic use in animal husbandry, amplifying the demand for alternatives that uphold production efficiency and address rising consumer concerns over antibiotic resistance. The animal feed probiotics market is evolving, with a pronounced emphasis on strain selection and formulation, tailoring products to meet the unique needs of specific species and production hurdles. Illustrating the segment's strategic significance, recent collaborations, like the April 2024 partnership between BIO-CAT and Caldic North America, aim to roll out OPTIFEED-branded probiotic solutions in the companion animal health arena.

Popularity of Plant-based and Fermented Probiotic Products

As plant-based diets gain traction and probiotics showcase their health benefits, a burgeoning market segment emerges, catering to diverse consumer needs. These innovative products resonate with lactose-intolerant individuals, vegans, and those pursuing sustainable diets, broadening the market's reach beyond the conventional dairy-centric probiotic audience. Noteworthy innovations include probiotic-infused plant milks, fermented vegetables, and even fresh produce, with Israeli startup Wonder Veggies set to debut the world's inaugural probiotic-infused fresh produce in 2025. Additionally, advancements in fermentation technology are enabling the development of more stable and effective probiotic strains, ensuring longer shelf life and enhanced functionality. Fermenting plant foods not only boosts their nutritional value but also enhances nutrient absorption, offering a plethora of health advantages beyond just probiotics. The growing consumer awareness of gut health and its link to overall well-being further drives demand in this market segment.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf life and stability challenges | -0.7% | Global, with higher impact in regions with less developed cold chain infrastructure | Short term (≤ 2 years) |

| Storage and distribution challenges in hot climates | -0.5% | Middle East and Africa, South Asia, Latin America | Medium term (2-4 years) |

| Alternative health solutions overshadow probiotics | -0.4% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Premium pricing limits adoption in price-sensitive markets | -0.6% | Asia-Pacific emerging markets, Latin America, Africa | Medium term (2-4 years) |

Source: Mordor Intelligence

Limited Shelf Life and Stability Challenges

Maintaining probiotic organism viability throughout shelf life represents a significant operational challenge that limits market growth. The World Health Organization (WHO) and Food and Agriculture Organization (FAO) require probiotics to contain 10^6 to 10^7 CFU of viable bacteria to provide health benefits. However, maintaining these levels from production through consumption remains a key operational issue. Besides, real-time PCR stability analyses demonstrate that viable counts frequently decrease below stated label claims, particularly in expired products, impacting consumer trust and product performance. This operational constraint specifically affects smaller manufacturers with restricted access to stabilization technologies, while larger companies leverage their established formulation capabilities. The industry has implemented technical solutions, including microencapsulation, protective delivery systems, and moisture-controlling packaging, to improve probiotic viability. However, these solutions increase operational complexity and manufacturing costs.

Storage and Distribution Challenges in Hot Climates

In regions with hot climates and limited cold chain infrastructure, temperature sensitivity poses significant barriers to market expansion. Elevated temperatures during transportation and storage compromise probiotic viability. Research highlights that fluctuations in temperature are among the most significant stressors impacting product efficacy. This challenge is especially pronounced in emerging markets located in hotter regions. These markets, however, present substantial growth opportunities, driven by rising health awareness and increasing disposable incomes. Thus, manufacturers, aiming to broaden their geographic reach, have made the development of thermostable probiotic formulations a strategic priority. Their research emphasizes strain selection for heat resistance and innovative formulation techniques. Furthermore, recent advancements in biopolymer encapsulation methods hold promise for enhancing probiotic delivery in challenging conditions, potentially alleviating this market constraint. Economically, these challenges not only lead to missed sales opportunities but also escalate production costs. This is due to the need for overages (adding excess probiotics to counteract die-off) and specialized packaging solutions.

Segment Analysis

By Product Type: Bacteria Dominates Through Established Applications

In 2024, bacteria-based probiotics dominate the market, holding a commanding 77.74% share. Lactobacillus and bifidobacterium strains, known for their safety and health benefits, are the backbone of most commercial formulations. This stronghold of bacterial probiotics is rooted in their extensive research history and consumer trust, especially in traditional uses like yogurt and fermented foods. Recent breakthroughs in identifying and characterizing bacterial strains have broadened their application scope. Next-generation probiotics (NGPs) are now emerging, targeting specific health issues beyond just digestive wellness. A notable frontier in this realm is the rise of precision microbiome therapies. Here, researchers harness cutting-edge technologies, including genomics and AI, to scrutinize microbiota, crafting personalized treatments that pinpoint specific core probiotics to bolster health and tackle diseases.

Yeast-based probiotics, though commanding a smaller slice of the market, are on an upswing, boasting a robust 7.27% CAGR from 2025 to 2030. This growth is attributed to their unique advantages in select applications. Leading this yeast segment are Saccharomyces cerevisiae and Saccharomyces boulardii. Research underscores their resilience in gastrointestinal settings and their potential to ease lactose intolerance. Yeast cells come with inherent stability perks, showcasing resistance to antibiotics, bile salts, and acidic environments. This resilience gives them an edge in applications where bacterial probiotics might struggle. Current studies on yeast-based probiotics in dairy highlight the critical nature of strain selection, focusing on gastrointestinal survival, safety, and unique probiotic traits, hinting at a vibrant future for innovation in this domain.

By Form: Powder Formats Maintain Market Leadership

In 2024, powder forms command a dominant 54.54% share of the probiotics market, largely owing to their extended shelf stability and manufacturing benefits. The stronghold of powder formats is underscored by a well-established production infrastructure and consumer familiarity, especially in dietary supplements. Here, capsules, tablets, and sachets are the go-to delivery systems. Additionally, technological strides, such as lyophilization (freeze-drying) and microencapsulation, have bolstered powder stabilization, reinforcing this segment's market leadership by overcoming past stability hurdles. A May 2024 study in Plant Foods for Human Nutrition highlighted the innovative potential of powders, showing that microencapsulated probiotics can remain viable for up to five months at room temperature when paired with low water activity fillings like peanut butter.

Liquid probiotics, on the other hand, are on a rapid ascent, boasting a 6.33% CAGR from 2025 to 2030. This surge is fueled by emerging studies underscoring their enhanced bioavailability and effectiveness. A pivotal December 2024 study in the Journal of Biochemistry and Physiology unveiled that juice-based probiotics outshine their dry powder counterparts in acidic stomach conditions. The findings were striking: juice-based probiotics exhibited a 50-fold better survival rate immediately, a staggering 3,700 times better after 30 minutes, and 2,188 times better after an hour, as reported by SciTechnol. This superior survivability is linked to factors like cellular hydration, the juice's buffering capacity, and the presence of glucose, highlighting the inherent advantages of liquid delivery systems. Innovations in the liquid segment are noteworthy, with advancements like shelf-stable liquid formulations and unique product offerings such as probiotic-infused beverages, salad dressings, and cooking oils, broadening consumption opportunities beyond the conventional supplement realm.

By Application: Food and Beverage Maintains Market Leadership

In 2024, food and beverage applications dominate the probiotics market, holding a 25.83% share. Traditionally, this category has served as the primary gateway for probiotic consumption. While yogurt has long been the flagship product, recent innovations have broadened the probiotic landscape to encompass a variety of food categories. These now include beverages, infant formulas, and even non-dairy options. This shift towards embedding probiotics in everyday foods resonates with consumers' preferences for deriving nutrients from their diet rather than relying on supplements. This trend has opened avenues for manufacturers to craft functional foods boasting enhanced value propositions. Noteworthy innovations, such as probiotic-infused salad dressings and new whole milk kefir flavors, were unveiled by Lifeway Foods at the 2025 Natural Products Expo West, underscoring the segment's dynamic evolution.

Dietary supplements are emerging as the fastest-growing segment, boasting a 7.33% CAGR from 2025 to 2030. This surge is fueled by a more discerning consumer base, increasingly aware of specific probiotic strains and their associated health benefits. This trend underscores a broader movement towards personalized nutrition, with consumers now gravitating towards supplements tailored for distinct health concerns, rather than generic wellness. The dietary supplement format stands out for its dosage precision and stability, empowering manufacturers to provide clinically significant amounts of targeted probiotic strains. Regulatory milestones, like the Food Safety Authority of Ireland's directives on probiotics in food supplements in 2024, highlight the segment's burgeoning prominence. These guidelines set forth safety benchmarks for probiotics, emphasizing criteria such as a proven history of safe use, precise species-level identification, and the absence of infectious traits, potentially shaping global regulatory standards.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, the Asia-Pacific region commands a dominant 33.45% share of the probiotic ingredients market, fueled by cultural affinities for fermented foods, heightened health awareness, and brisk economic growth. Within this landscape, China, Japan, and India emerge as the primary growth engines, each showcasing unique market dynamics and consumer inclinations. Japan's deep-rooted probiotic traditions pave the way for ongoing innovations. In contrast, China's burgeoning middle class is opening doors to premium probiotic offerings. Unlike Europe, where regulations can be stringent, the Asia-Pacific's more lenient regulatory stance facilitates broader probiotic marketing, bolstering market growth. A July 2024 study in Frontiers in Microbiology underscores the pivotal role of gut microbiota and probiotics in leukemia treatments among Asian demographics. The findings hint at probiotics' potential in alleviating chemotherapy's side effects and enhancing patient recovery. Such insights not only broaden the perception of probiotics beyond mere digestive aids but also spotlight burgeoning avenues in medical nutrition and adjunctive therapies.

South America, starting from a smaller market size than Asia-Pacific or North America, is on a rapid ascent, projected to grow at a 5.12% CAGR from 2025 to 2030. Brazil, with its strong dairy sector and a populace increasingly attuned to health, stands as the region's probiotic powerhouse. While the South American market is buoyed by rising yogurt consumption and a burgeoning functional food segment, economic fluctuations in certain nations pose hurdles. As the probiotic market burgeons, South American regulatory bodies are adapting, with Brazil often leading the way and influencing its neighbors. A special feature in SciELO Press Releases spotlights the innovative edge of probiotic-infused functional foods, underscoring their pronounced health benefits. This sentiment resonates strongly in Brazil and Argentina, where a surge in gut health awareness is prompting manufacturers to roll out products that align with local tastes and dietary habits.

In North America, the probiotic ingredients market is bolstered by high consumer awareness of digestive and immune health, a strong presence of functional food and supplement brands, and ongoing innovations in delivery formats that appeal to diverse consumer groups. Moreover, the United States market exhibits substantial growth in probiotic supplement consumption. According to the Council for Responsible Nutrition, 74% of Americans utilized dietary supplements, including probiotics, in 2023 [3]Source: Council for Responsible Nutrition, "Dietary Supplements Usage in the U.S.", crnusa.org. . This market behavior reflects the systematic integration of probiotic ingredients into mainstream dietary supplement formulations, driven by increasing consumer demand for digestive health products. Additionally, Europe constitutes a significant market segment due to its established fermented food industry and regulatory framework supporting probiotic health claims, contributing to growth in both mainstream and specialty segments. The Middle East and Africa market demonstrates substantial growth potential, driven by heightened health awareness, increasing urbanization, and strategic investments from food and beverage manufacturers responding to consumer demand for gut health products.

Competitive Landscape

The probiotic ingredients market is moderately consolidated, with a few players vying for a market share. Some of the leading players in the market, including Novonesis A/S, Kerry Group plc, DSM-Firmenich, and International Flavors & Fragrances Inc., dominate the probiotic ingredients market. These industry leaders are heavily investing in research and development, with a focus on unveiling groundbreaking products. Their efforts are concentrated on pioneering next-generation probiotic microorganisms and refining delivery systems. Innovations abound in the sector, ranging from nano-encapsulated probiotic cultures to multi-strain formulations and tailored probiotic solutions.

In response to rising demand, companies are ramping up production capabilities, establishing new manufacturing units, and forming strategic partnerships. Aligning with evolving consumer preferences, market leaders are emphasizing the development of vegan-friendly, non-GMO, and clean-label probiotic ingredients. Their agility is underscored by investments in advanced fermentation facilities and state-of-the-art production technologies. Moreover, they're expanding not just through organic growth but also via strategic acquisitions.

Emerging application areas like skin health, mental wellness, and metabolic health present white space opportunities. While preliminary research hints at the probiotic potential in these domains, commercial development remains sparse. The U.S. Food and Drug Administration (FDA) oversees animal food products under the Federal Food, Drug, and Cosmetic Act (FD&C Act). The Center for Veterinary Medicine (CVM) plays a pivotal role, ensuring these products meet safety standards. Such regulatory oversight shapes competitive strategies in the probiotics market's animal feed segment, highlighting the critical nature of proper labeling and safety assessments.

Probiotic Ingredients Industry Leaders

-

Novonesis A/S

-

Kerry Group plc

-

DSM-Firmenich

-

International Flavors & Fragrances Inc.

-

Lallemand Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lallemand Health Solutions had introduced Cerenity, a probiotic formula that supported healthy aging through gut-muscle axis modulation. The formula combined three probiotic strains: Lactobacillus helveticus Rosell-52, Bifidobacterium longum Rosell-175, and Bifidobacterium lactis Lafti B94.

- November 2024: Symrise completed the acquisition of a 90% stake in a Swedish probiotics company, which strengthened its position in the health and wellness market. The acquisition expanded Symrise's capabilities in probiotics and functional ingredients, enabling the company to address the global demand for gut health and immunity products. The investment aligned with Symrise's growth strategy and focus on nutrition and health markets.

- April 2024: ADM obtained approval from China's National Health Commission to launch its spore-forming probiotic DE111TM (Bacillus subtilis) in the country. The approval confirmed that DE111TM probiotic met the Commission's quality and safety requirements for sale in the Chinese market.

- January 2024: Novozymes and Chr. Hansen merged their operations to establish Novonesis, which integrated their biotechnology capabilities to serve the food, agriculture, and health industries. The newly formed company focused on expanding its product offerings and improving operational efficiency.

Global Probiotic Ingredients Market Report Scope

Probiotics are live microorganisms marketed with health claims, including claims to improve or restore gut flora.

The global probiotic ingredients market is segmented by product type, form, application, and geography. The probiotic ingredients market is segmented by product type into bacteria and yeast. The bacteria segment is further sub-segmented into lactobacillus, bifidobacterium, and others. The yeast segment is further sub-segmented into Saccharomyces cerevisiae and Saccharomyces boulardi, and others. By form, the market is segmented into powder and liquid. Based on application, probiotic ingredients are differentiated by their use in foods and beverages, dietary supplements, and animal feed. The food and beverages are further sub-segmented into yogurt, infant formula, probiotic drinks, and other food and beverages. The market is also segmented based on geography into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| By Product Type | Bacteria | Lactobacillus | |

| Bifidobacterium | |||

| Others | |||

| Yeast | Saccharomyces Cerevisiae | ||

| Saccharomyces Boulardi | |||

| Others | |||

| By Form | Powder | ||

| Liquid | |||

| By Application | Food and Beverage | Yogurt | |

| Infant Formula | |||

| Probiotic Drinks | |||

| Other Food and Beverages | |||

| Dietary Supplements | |||

| Animal Feed | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

| Bacteria | Lactobacillus |

| Bifidobacterium | |

| Others | |

| Yeast | Saccharomyces Cerevisiae |

| Saccharomyces Boulardi | |

| Others |

| Powder |

| Liquid |

| Food and Beverage | Yogurt |

| Infant Formula | |

| Probiotic Drinks | |

| Other Food and Beverages | |

| Dietary Supplements | |

| Animal Feed |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the probiotics market?

The probiotics market stands at USD 5.69 billion in 2025 and is projected to reach USD 7.06 billion by 2030.

Which application is growing the fastest?

Dietary supplements are expanding at a 7.33% CAGR through 2030 as consumers pursue personalized strain-specific benefits.

Why are yeast-based probiotics gaining attention?

Yeast strains like Saccharomyces boulardii show superior gastric resilience and are advancing at 7.27% CAGR, opening avenues in gut, immune, and skin health.

Which region leads the probiotics market?

Asia-Pacific accounts for 33.45% of global revenue owing to strong cultural acceptance of fermented foods and rising disposable incomes.

Page last updated on: June 29, 2025