Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 33.59 Billion |

| Market Size (2031) | USD 49.74 Billion |

| Growth Rate (2026 - 2031) | 8.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

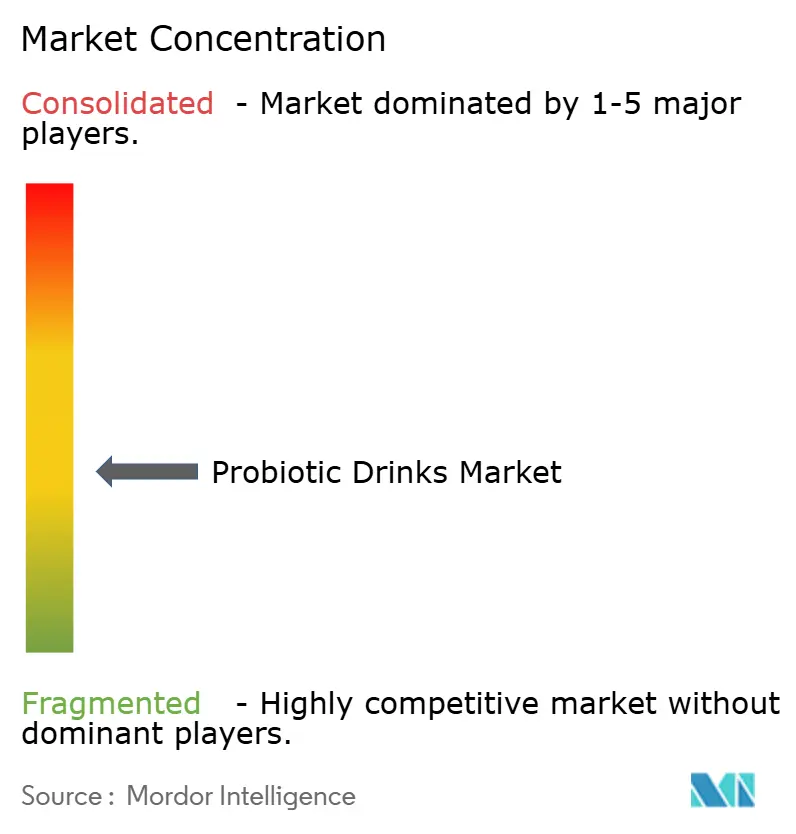

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Probiotic Drinks Market Analysis by Mordor Intelligence

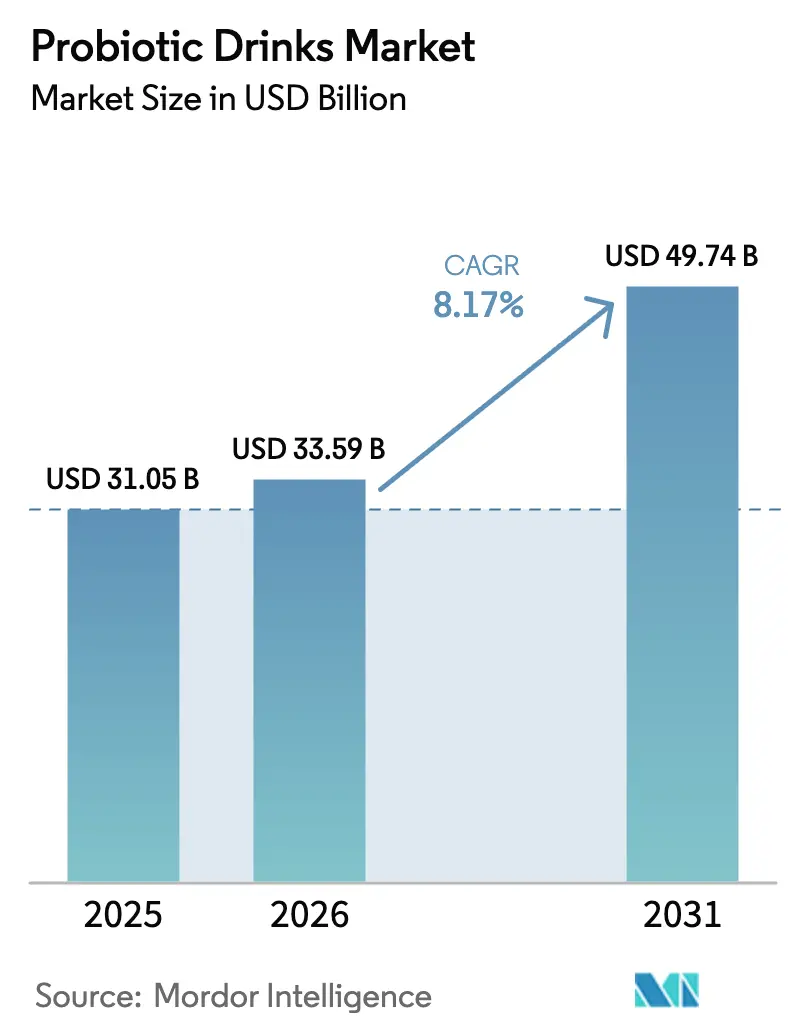

The probiotic drinks market size is expected to increase from USD 31.05 million in 2025 to USD 33.59 million in 2026 and reach USD 49.74 million by 2031, growing at a CAGR of 8.17% over 2026-2031. This growth is driven by increasing awareness of gut-microbiome science, a shift toward preventive nutrition, and rising disposable incomes in urban Asia. Yogurt drinks remain popular due to established consumption habits in Europe and Asia-Pacific, while probiotic juices are gaining traction with fruit-forward flavors and lactose-free options. Clean-label demand is rising as millennials and Gen Z prefer unflavored products free from artificial additives. Supermarkets dominate sales, but pharmacies are emerging as premium channels for live-culture beverages marketed as wellness aids. Innovations in aluminum packaging are also supporting sustainability and on-the-go consumption.

Key Report Takeaways

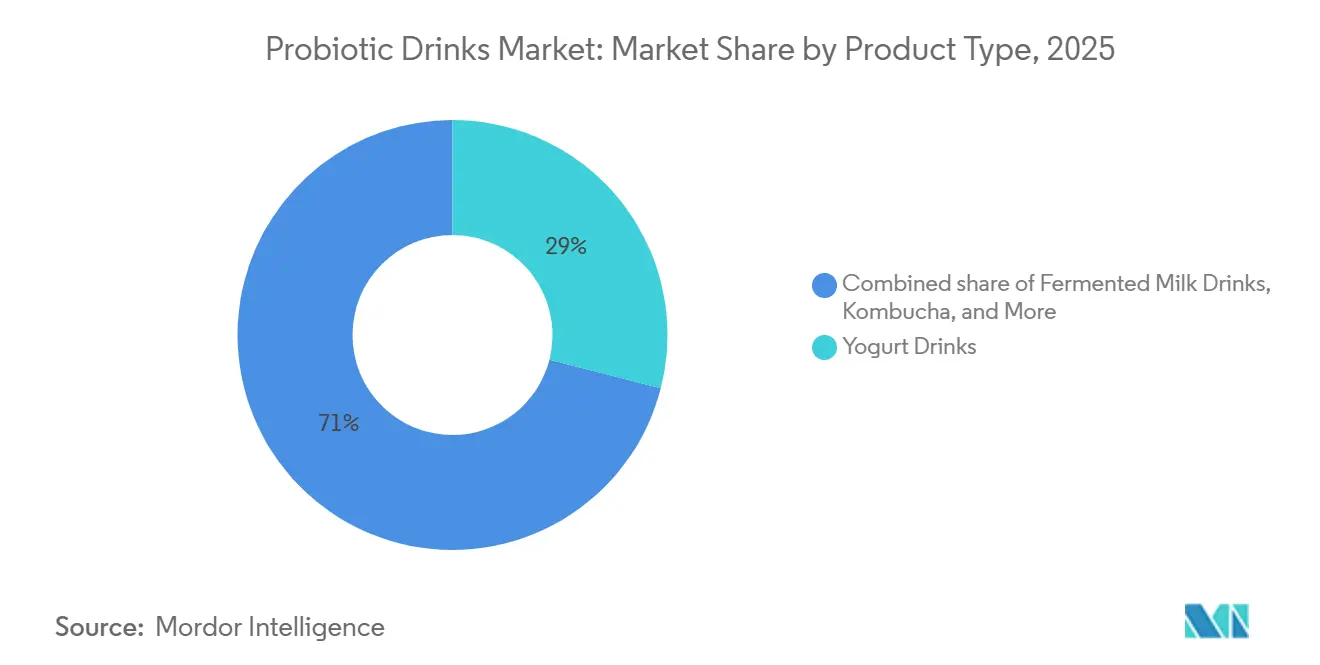

- By product type, yogurt drinks led with 28.98% revenue share in 2025; probiotic juices are projected to post a 9.21% CAGR through 2031.

- By flavor, flavored variants accounted for 67.81% of volume in 2025, while unflavored options are forecast to grow at 8.92% to 2031.

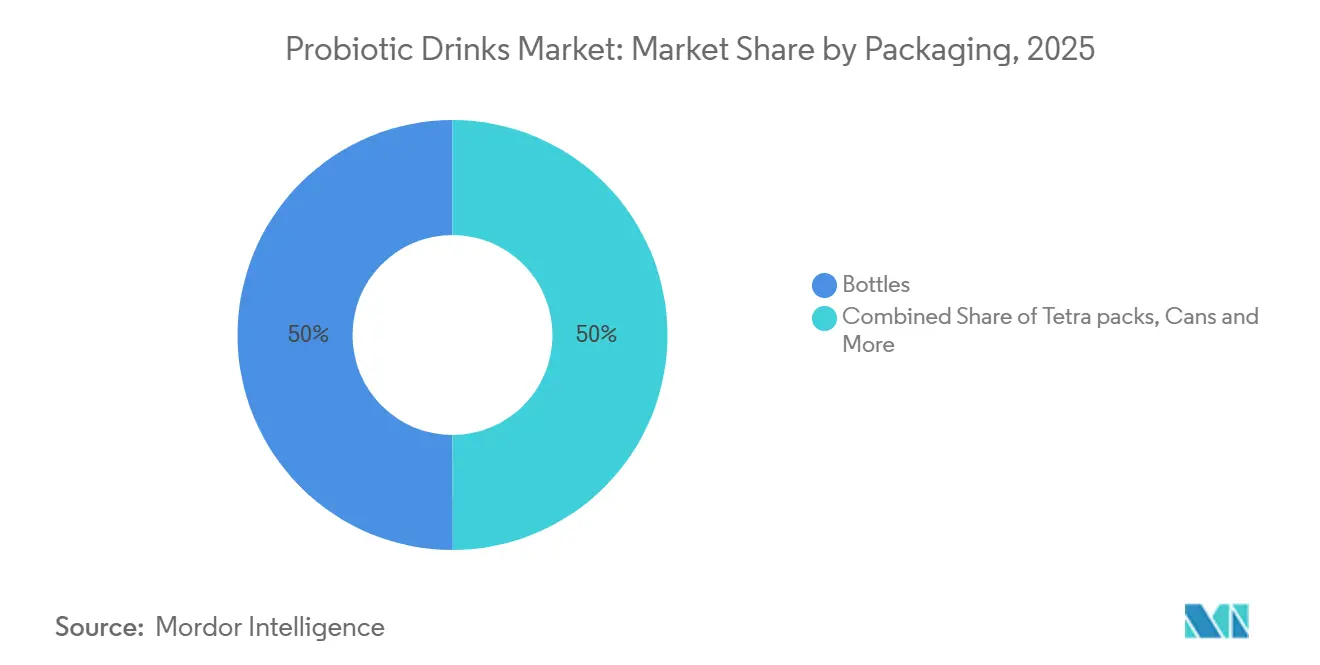

- By packaging, bottles held 50.01% share in 2025, whereas cans are set to expand at a 9.01% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 55.81% share in 2025, whereas pharmacies and drug stores are advancing at an 8.17% CAGR to 2031.

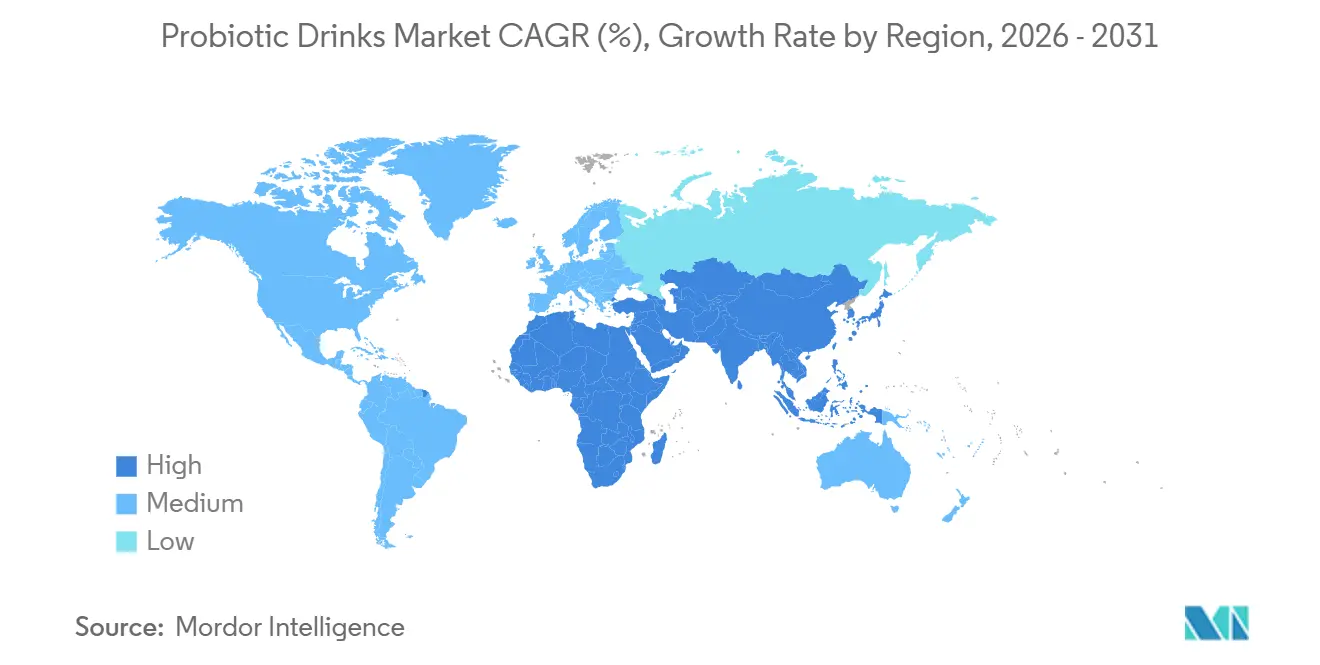

- By geography, Europe retained 42.02% share in 2025, and Asia-Pacific is anticipated to register a 9.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Probiotic Drinks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising digestive disorders drive demand for microbiota-supporting functional beverages | +1.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Low-sugar, low-calorie options attract health-conscious millennials and Gen Z | +1.5% | North America, Europe, Australia, urban China and India | Short term (≤ 2 years) |

| Clean-label demand for natural, organic ingredients drives innovation | +1.3% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Supermarkets with functional beverage aisles improve accessibility | +1.0% | Global, strongest in Europe and North America | Short term (≤ 2 years) |

| Fermented beverages like yogurt drinks and kefir integrate probiotics into diets | +1.2% | Europe, Asia-Pacific (Japan, South Korea, China), Middle East | Long term (≥ 4 years) |

| Novel flavors, sparkling varieties, and prebiotic blends boost product appeal | +1.4% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Digestive Disorders Drive Demand for Microbiota-Supporting Functional Beverages

Consumers are increasingly choosing preventive solutions over pharmaceuticals to manage gastrointestinal issues such as irritable bowel syndrome and antibiotic-related dysbiosis. The U.S. National Institutes of Health reports that functional gastrointestinal disorders affect 35% to 40% of adults globally, driving demand for products with live microorganisms[1]Source: National Institutes of Health, "NIH - Functional Gastrointestinal Disorders", nih.gov.. Probiotic drinks, a more appealing alternative to capsules, seamlessly integrate gut health into daily routines. In 2024, Lifeway Foods introduced "Muscle Mates," a blend of probiotic kefir and creatine designed to support post-exercise recovery and digestive health. While research on the gut-brain axis highlights potential mental health benefits, regulatory bodies have not yet approved mood-related claims. This trend is particularly strong in North America and Europe, where rising healthcare costs encourage self-care, and in urban Asia-Pacific regions, where Western diets are contributing to increased gastrointestinal issues.

Low-Sugar, Low-Calorie Options Attract Health-Conscious Millennials and Gen Z

Younger generations are increasingly shifting away from sugary sodas, opting for functional beverages that align with their clean-eating habits and macro-tracking goals. Traditional yogurt drinks often contain over 15 grams of sugar per serving, exceeding the American Heart Association's recommended daily limits of 25 grams for women and 36 grams for men[2]American Heart Association, "American Heart Association - Sugar Recommendations", heart.org. . In response, manufacturers are reformulating products by using natural sweeteners like stevia and monk fruit or removing sweeteners entirely, focusing on the unflavored segment, which is projected to grow at 8.92% through 2031. Lifeway's Probiotic Smoothie + Collagen, launching in 2025, is a zero-added-sugar product designed to meet the demand for beverages that promote both skin elasticity and gut health. This trend is most evident in North America, Western Europe, and Australia, where high nutrition-label literacy and social media influencers are driving the low-sugar movement. It is also expanding into urban centers in the Asia-Pacific region, particularly among affluent millennials in China and India, who increasingly view sugar reduction as a marker of social status.

Clean-Label Demand for Natural, Organic Ingredients Drives Innovation

Consumers are increasingly prioritizing recognizable, minimally processed ingredients, moving away from artificial colors, flavors, and preservatives. In 2024, U.S. organic beverage sales exceeded USD 3 billion, according to the Organic Trade Association, with probiotics emerging as a key growth driver[3]Source: Organic Trade Association, "Organic Trade Association - Organic Beverage Sales Report 2024", ota.com.. That same year, Danone partnered with Chr. Hansen to co-develop organic probiotic cultures that comply with European Union organic certification standards while ensuring shelf stability. Clean-label positioning remains particularly strong in North America and Western Europe, where regulatory frameworks like the USDA National Organic Program and EU Organic Regulation provide trusted third-party validation. This trend is also driving packaging innovations, with brands adopting glass bottles and recyclable aluminum cans to emphasize sustainability. However, balancing clean-label aesthetics with cost efficiency remains a challenge, as organic certification and premium ingredients can raise retail prices by 20% to 30%, potentially limiting broader market adoption.

Fermented Beverages Like Yogurt Drinks and Kefir Integrate Probiotics into Diets

Traditional fermentation practices in Europe, Asia, and the Middle East have established a strong cultural foundation for the consumption of cultured dairy, facilitating the adoption of probiotics. By 2025, yogurt drinks accounted for a 28.98% market share, driven by decades of brand-building efforts from companies like Danone (Actimel and Activia) and Yakult in key markets such as France, Japan, and South Korea. Kefir, a fermented milk beverage originating from the Caucasus region, is gaining popularity in North America as consumers increasingly seek alternatives to Greek yogurt. The American Chemical Society has highlighted kefir's superior microbial diversity, containing up to 30 bacterial and yeast strains, compared to the single-strain cultures in traditional yogurts. In 2024, Yakult expanded into China's tier-1 cities, leveraging its established distribution network in Japan to promote daily probiotic consumption among Chinese consumers. This shift represents a long-term trend, as taste preferences and consumption habits evolve gradually. While Europe and Asia-Pacific remain the primary markets, the Middle East is emerging as a significant player, with fermented dairy aligning well with Halal dietary norms.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory hurdles delay product launches and increase compliance costs | -0.9% | Global, most acute in EU and North America | Medium term (2-4 years) |

| Cold chain logistics increase risks and spoilage potential | -1.1% | Asia-Pacific (excluding Japan, South Korea), South America, Middle East and Africa | Short term (≤ 2 years) |

| Limited strain diversity and efficacy hinder reliable health outcomes | -0.7% | Global | Long term (≥ 4 years) |

| Competition from sugary beverages fragments market share | -0.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Hurdles Delay Product Launches and Increase Compliance Costs

Probiotic health claims face stringent pre-market scrutiny in major markets, with approval timelines of 18–24 months and costs of USD 500,000 to USD 1 million for dossier preparation. Between 2010 and 2020, the European Food Safety Authority rejected over 80% of such applications, forcing brands to use generic claims like "supports digestive health." In the U.S., the FDA's Generally Recognized as Safe pathway requires extensive safety data for novel strains, creating barriers for smaller innovators. Similarly, the EU's Novel Foods Regulation 2015/2283 mandates full safety assessments for strains not widely consumed before May 1997, delaying commercialization of next-generation species like Akkermansia muciniphila. These regulatory hurdles, particularly in Europe and North America, disproportionately affect emerging brands and result in a conservative product pipeline dominated by established Lactobacillus and Bifidobacterium strains, limiting innovation and breakthrough efficacy in the market.

Cold Chain Logistics Increase Risks and Spoilage Potential

Live probiotic cultures need consistent refrigeration to maintain colony-forming-unit counts above 1 billion CFU per serving. A 2024 study by the International Dairy Federation found that exposure to temperatures above 8°C for over 48 hours can reduce viable counts by 50% to 70%, rendering the products ineffective. Regions like Asia-Pacific (excluding Japan and South Korea), South America, and the Middle East and Africa face significant challenges due to fragmented cold-chain infrastructure, grid instability, and high ambient temperatures, which increase spoilage risks. Although brands are adopting freeze-dried and microencapsulated formats to reduce cold-chain dependency, these technologies add USD 0.50 to USD 1.00 per unit in production costs, squeezing margins in price-sensitive markets. Until ambient-stable formulations achieve the same efficacy as refrigerated ones, cold-chain limitations will continue to hinder growth in emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Yogurt Drinks Anchor Legacy Demand

In 2025, yogurt drinks held a 28.98% market share, driven by strong consumption habits in Europe and Asia-Pacific, where brands like Danone's Actimel and Yakult benefit from established distribution networks, consumer trust, and favorable regulatory frameworks. Danone launched Actimel+ Triple Action in 2024, adding vitamin D and zinc to meet rising immune-support demand. These drinks are staples in countries like France, Germany, Japan, and South Korea, supported by decades of marketing. However, private-label products in Europe challenge margins by offering similar live-culture counts at 20% to 30% lower prices. Meanwhile, kefir is gaining traction in North America for its diverse microbial content.

Probiotic juices, projected to grow at 9.21% through 2031, appeal to consumers seeking fruit-forward flavors or lactose-free options, with rapid growth in North America and urban Asia-Pacific. Lifeway Foods introduced Probiotic Smoothie + Collagen in 2025, combining fruit purees, kefir cultures, and collagen peptides for dual benefits. Kombucha, though niche, is attracting investment, as seen in PepsiCo's USD 1.95 billion acquisition of Poppi in March 2025, highlighting the demand for probiotic sodas. However, ensuring probiotic survival in acidic juices remains a challenge, requiring innovations like microencapsulation or strain selection.

By Flavor: Flavored Variants Dominate, Unflavored Gains Momentum

In 2025, flavored probiotic drinks dominated 67.81% of the market, using fruit essences, vanilla, and botanical extracts to offset the sourness of fermented products. This segment drives trial and repeat purchases, with sensory appeal converting first-time buyers into loyal consumers. Lifeway Foods launched 10 new Flavor Fusions in 2024, including mango-turmeric and blueberry-lavender, targeting millennials and Gen Z with innovative flavors and visually appealing packaging. Flavored options perform well in North America, where juice-based profiles align with preferences, and in urban Asia-Pacific markets, where tropical fruits hold cultural relevance. However, balancing flavor intensity with reduced sugar content remains a challenge, prompting reformulations with natural sweeteners like stevia, monk fruit, and allulose.

Meanwhile, unflavored probiotic drinks are growing at 8.92% through 2031, driven by clean-label trends and consumer demand for purity and authenticity. Popular in Europe and North America, these products attract ingredient-conscious buyers and culinary users who incorporate them into recipes. The American Chemical Society highlights kefir’s diverse microbial strains as superior for microbiome health, adding credibility to unflavored formats. Brands are educating consumers on their versatility and customization potential, but unflavored options risk staying niche unless manufacturers demonstrate clear benefits or cost savings to justify the sensory trade-off.

By Packaging: Bottles Lead, Cans Surge

In 2025, bottles accounted for 50.01% of the packaging market due to established filling lines, consumer familiarity, and the ability to display product color and texture through transparent PET or glass. Glass bottles, favored by organic and clean-label brands for their premium image and sustainability appeal, increase freight costs and retail prices by 10% to 15%. PET bottles dominate mass-market yogurt drinks and kefir, offering lightweight convenience and resealable closures, with companies like Danone and Yakult achieving sub-USD 0.10 packaging costs per unit through optimized supply chains. However, anti-plastic sentiment and regulatory bans in Europe and North America are driving demand for recyclable or compostable alternatives.

Cans, projected to grow at 9.01% through 2031, benefit from on-the-go consumption trends, superior recyclability, and UV protection for probiotic cultures. Aluminum cans, ideal for sparkling probiotic sodas and kombucha, align with sustainability goals, with recycling rates exceeding 70% in North America and Europe. PepsiCo’s USD 1.95 billion acquisition of Poppi in 2025 highlights the mainstream potential of canned probiotic drinks, though maintaining live-culture viability remains a challenge due to pasteurization. Tetra packs and aseptic cartons hold a smaller share, mainly in Asia-Pacific and the Middle East, where ambient distribution is preferred due to limited cold-chain infrastructure.

By Distribution Channel: Supermarkets Dominate, Pharmacies Accelerate

In 2025, supermarkets and hypermarkets dominated distribution with a 55.81% share, leveraging refrigerated-aisle visibility and volume throughput to drive mass-market penetration. These channels are vital in Europe and North America, where weekly grocery trips dominate, and consumers expect probiotic drinks near yogurt, milk, and juice. Lifeway Foods expanded into BJ's Wholesale Club, Publix, and Target in 2024, securing prime shelf space that boosted trial rates among price-sensitive households. Supermarkets also enable promotions like buy-one-get-one-free offers and end-cap displays to drive impulse purchases, though shelf-space competition remains a challenge, with slotting fees consuming up to 20% of gross revenue.

Pharmacies and drug stores, growing at 8.17% through 2031, benefit from a medicalization trend where probiotics are seen as wellness solutions. In January 2025, Florastor entered CVS pharmacy aisles, leveraging its 9,000-store network to target consumers seeking clinical-grade probiotics. Pharmacies command premium pricing, often 20% to 30% higher than supermarkets, due to perceived therapeutic value. Online platforms are also expanding, driven by direct-to-consumer models and subscription services, while convenience and grocery stores capture impulse purchases despite limited refrigeration capacity.

Geography Analysis

In 2025, Europe held a dominant 42.02% market share, bolstered by a long-standing tradition of probiotic consumption in countries like France, Germany, and the UK. Brands such as Danone and Yakult have ingrained daily probiotic intake into the culture, due to persistent marketing efforts. The European Food Safety Authority's rigorous health-claim standards lend credibility to these products; those that successfully navigate this approval process are viewed as scientifically validated by consumers. Germany boasts a particularly vibrant functional-beverage market, fueled by a cultural focus on preventive health and a willingness to spend on organic and natural products. The EU's Novel Foods Regulation 2015/2283, while ensuring product safety, poses challenges for brands eager to innovate, as they often find themselves in lengthy approval waits for new strains. Meanwhile, Eastern Europe, especially Poland and the Czech Republic, is emerging as a hotspot, with rising incomes and Westernized diets fueling a growing appetite for functional beverages.

Asia-Pacific is set to witness a robust growth rate of 9.52% through 2031, driven by increasing disposable incomes in China, India, and Indonesia. Urbanization in these nations is spurring a demand for products that prioritize health and convenience. In 2024, Yakult made a strategic move into China's tier-1 cities, capitalizing on its well-established distribution channels from Japan to promote daily probiotic habits. While India's kombucha scene is still in its infancy, it's rapidly gaining momentum, with startups like Atmosphere Kombucha and Boocha making waves in major cities such as Mumbai and Bangalore. Japan and South Korea, though boasting mature markets with high per-capita consumption, are witnessing a slowdown in growth as they near market saturation. Southeast Asia, particularly Thailand, Vietnam, and the Philippines, is emerging as a promising frontier, with beverages like kefir resonating with local fermentation traditions. However, the region grapples with cold-chain infrastructure challenges, especially in rural locales, restricting distribution primarily to urban and affluent suburban areas.

North America, South America, and the Middle East and Africa round out the global market landscape. North America shows moderate growth, with probiotic awareness reaching a plateau and competition heating up. A notable consolidation in 2025 saw PepsiCo shelling out USD 1.95 billion to acquire Poppi, underscoring the strategic value mainstream beverage giants place on probiotic platforms. Canada's market trajectory closely mirrors that of the U.S., with both kefir and kombucha carving out larger shares in natural-food outlets. In South America, while cold-chain challenges and economic fluctuations pose hurdles, urban middle-class consumers in Brazil and Argentina are leading the charge in adopting these products. The Middle East and Africa face analogous infrastructure issues, yet South Africa and the UAE stand out with their advanced modern retail penetration. However, the regulatory landscape in these regions is still maturing, presenting a dual-edged sword: swift market entry opportunities come with the risk of potential quality inconsistencies, which could jeopardize consumer trust.

Competitive Landscape

The probiotic drinks market is moderately fragmented, with participation from multinational dairy and beverage companies alongside regional brands and emerging functional drink startups. Large players benefit from established cold-chain infrastructure, strong brand recognition, and wide retail penetration, particularly in drinkable yogurt and cultured milk segments. Some of the major players in the market are Fonterra Co-op Group Ltd., Yakult Honsha Co. Ltd., Groupe Lactalis, and Groupe Danone SA, among others. However, the market does not exhibit high concentration, as consumption patterns, flavor preferences, and regulatory environments vary widely across regions, allowing multiple brands to compete effectively.

Smaller and local players contribute significantly to fragmentation by focusing on niche positioning such as plant-based, low-sugar, or clean-label probiotic drinks. Categories like kombucha, non-dairy fermented beverages, and probiotic waters have lower entry barriers, enabling startups to differentiate through formulation, sourcing, and lifestyle branding. These players often leverage e-commerce and specialty health channels to reach consumers directly, partially offsetting their limited scale and traditional retail access.

Competition in the probiotic drinks market is increasingly driven by innovation, strain credibility, and convenience rather than price alone. Leading companies are expanding portfolios with multi-strain formulations, functional blends, and improved shelf-stability to enhance consumer trust and usage frequency. While selective acquisitions and partnerships are occurring to capture high-growth niches, the coexistence of global leaders and numerous smaller innovators sustains the market’s moderately fragmented structure.

Probiotic Drinks Industry Leaders

-

Fonterra Co-op Group Ltd

-

Yakult Honsha Co. Ltd

-

Groupe Lactalis

-

Groupe Danone SA

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Danone has launched a drinkable yogurt product under its Oikos brand in the United States, targeted at users of Ozempic and other GLP-1 weight-loss drugs. The product, called Oikos Fusion, is designed to help consumers build and retain muscle mass during weight loss, according to the company.

- May 2025: Meiji has expanded its portfolio with the launch of a new product, Bulgaria Drinkable Yogurt Salt Lemon. According to the company, Bulgaria Drinkable Yogurt is designed to offer a unique combination of flavour and functionality. It features yogurt that is particularly effective at absorbing moisture, outperforming typical dairy drinks like milk.

- March 2025: Danone-owned yogurt brand Activia has expanded its kefir and fibre ranges to support consumers' gut health, with the launch of three new products. The new line includes a larger format of Activia Kefir Natural, Activia Kefir Peach Passion Fruit, and Activia Kefir Natural and Strawberry drinks.

- March 2024: Nova Easy Kombucha partnered with the San Diego Padres for City Connect-themed Sunset Slam Mango Lime hard kombucha, made available at Petco Park beginning on the stateside Opening Day of the 2024 Major League Baseball season.

Global Probiotic Drinks Market Report Scope

Probiotic drinks are functional beverages that help maintain a healthy balance of stomach bacteria, resulting in various health benefits such as digestive health, weight loss, and immune function. The global probiotic drinks market report is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into yogurt drinks, fermented milk drinks, kombucha, kefir, prebiotic juices, and other product types. Based on the distribution channel, the market is segmented into supermarkets, hypermarkets, convenience stores, pharmacies, health stores, and other distribution channels. Moreover, the study provides an analysis of the probiotic drinks market in emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, market sizing and forecasts have been provided on the basis of value in USD million.

Product Type

| Yogurt Drinks |

| Fermented Milk Drinks |

| Kombucha |

| Kefir |

| Probiotics Juices |

| Other Product Types |

Flavor

| Flavored |

| Unflavored |

Packaging

| Bottles |

| Cans |

| Tetra packs |

| Others |

Distribution Channels

| On-trade | |

| Off-trade | Supermarket/Hypermarkets |

| Pharmacies and Drug Stores | |

| Convenience/Grocery Stores | |

| Online Stores | |

| Others |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Yogurt Drinks | |

| Fermented Milk Drinks | ||

| Kombucha | ||

| Kefir | ||

| Probiotics Juices | ||

| Other Product Types | ||

| Flavor | Flavored | |

| Unflavored | ||

| Packaging | Bottles | |

| Cans | ||

| Tetra packs | ||

| Others | ||

| Distribution Channels | On-trade | |

| Off-trade | Supermarket/Hypermarkets | |

| Pharmacies and Drug Stores | ||

| Convenience/Grocery Stores | ||

| Online Stores | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the probiotic drinks market in 2026 and how fast is it growing?

The probiotic drinks market size is USD 33.59 billion in 2026 and is expected to climb to USD 49.74 billion by 2031, reflecting an 8.17% CAGR.

Which product type currently leads global sales?

Yogurt drinks command 28.98% of global revenue, benefiting from long-standing brand equity in Europe and Asia-Pacific.

What region offers the fastest growth opportunity through 2031?

Asia-Pacific is projected to expand at a 9.52% CAGR, driven by rising disposable incomes and increasing urbanization in China, India, and Indonesia.

Why are aluminum cans becoming popular in probiotic beverages?

Cans support on-the-go consumption, protect cultures from light exposure, and align with sustainability goals through recyclability rates above 70%.

Page last updated on: