Probiotic Dietary Supplement Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 12.51 Billion |

| Market Size (2030) | USD 22.01 Billion |

| Growth Rate (2025 - 2030) | 11.96% CAGR |

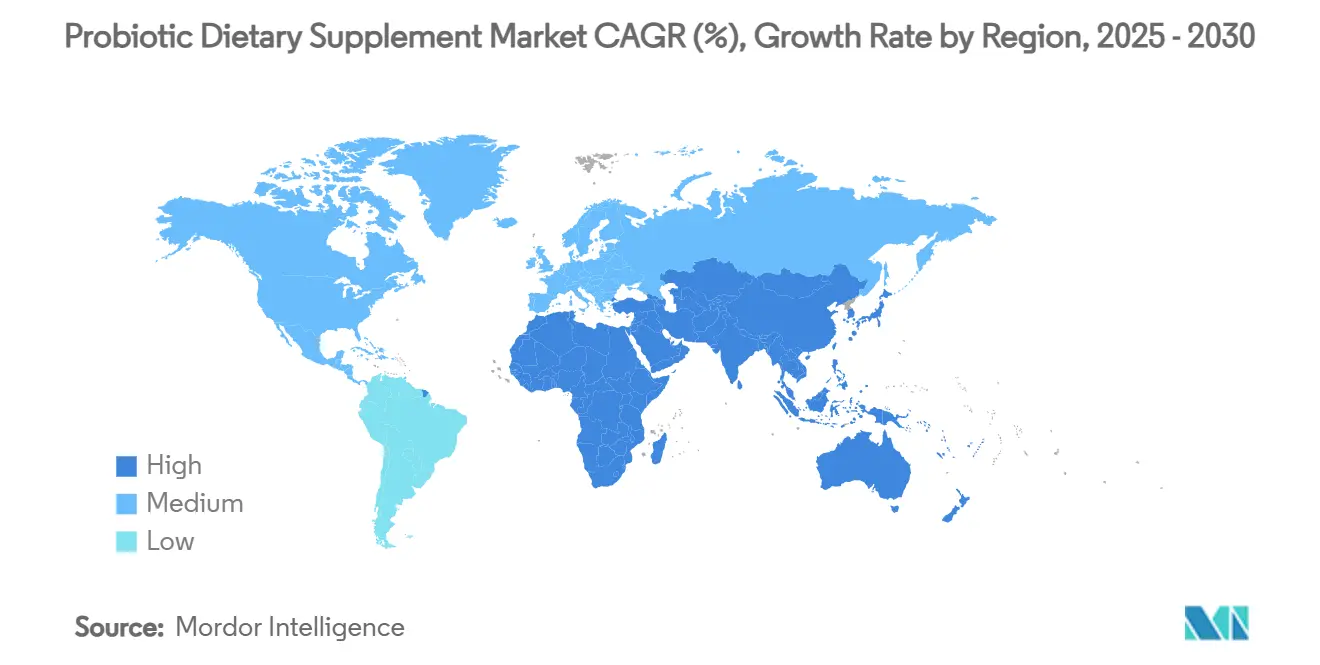

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

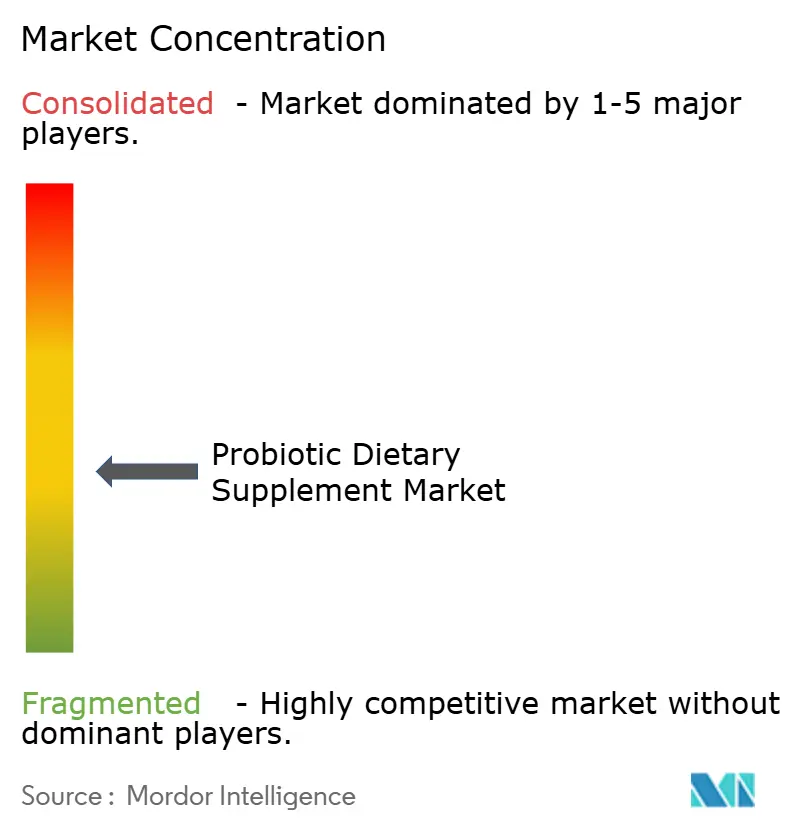

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Probiotic Dietary Supplement Market Analysis by Mordor Intelligence

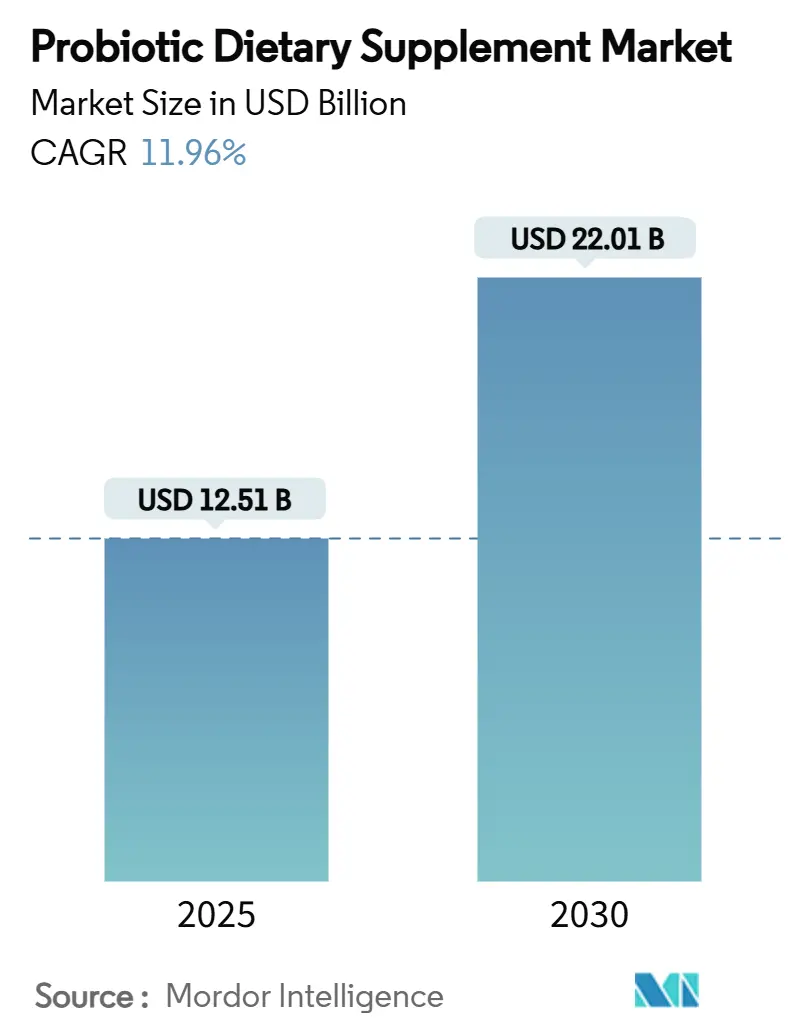

The probiotics supplements market size is estimated to be USD 12.51 billion in 2025, and is expected to reach USD 22.01 billion by 2030, growing at a CAGR of 11.96% during the forecast period (2025-2030). This robust growth trajectory reflects the market's resilience amid shifting consumer priorities toward preventative healthcare approaches. The increasing scientific validation of probiotic benefits has transformed what was once a niche segment into a mainstream wellness essential, particularly as consumers seek non-pharmaceutical interventions for digestive health. The market is experiencing significant growth due to increasing awareness about the importance of gut health in overall well-being. Consumers are increasingly incorporating these supplements into their daily routines to address digestive issues, boost immunity, and maintain a balanced gut microbiome. The market is also benefiting from advancements in research and development, which have led to the introduction of innovative formulations targeting specific health concerns, such as irritable bowel syndrome (IBS), lactose intolerance, and skin health.

Key Report Takeaways

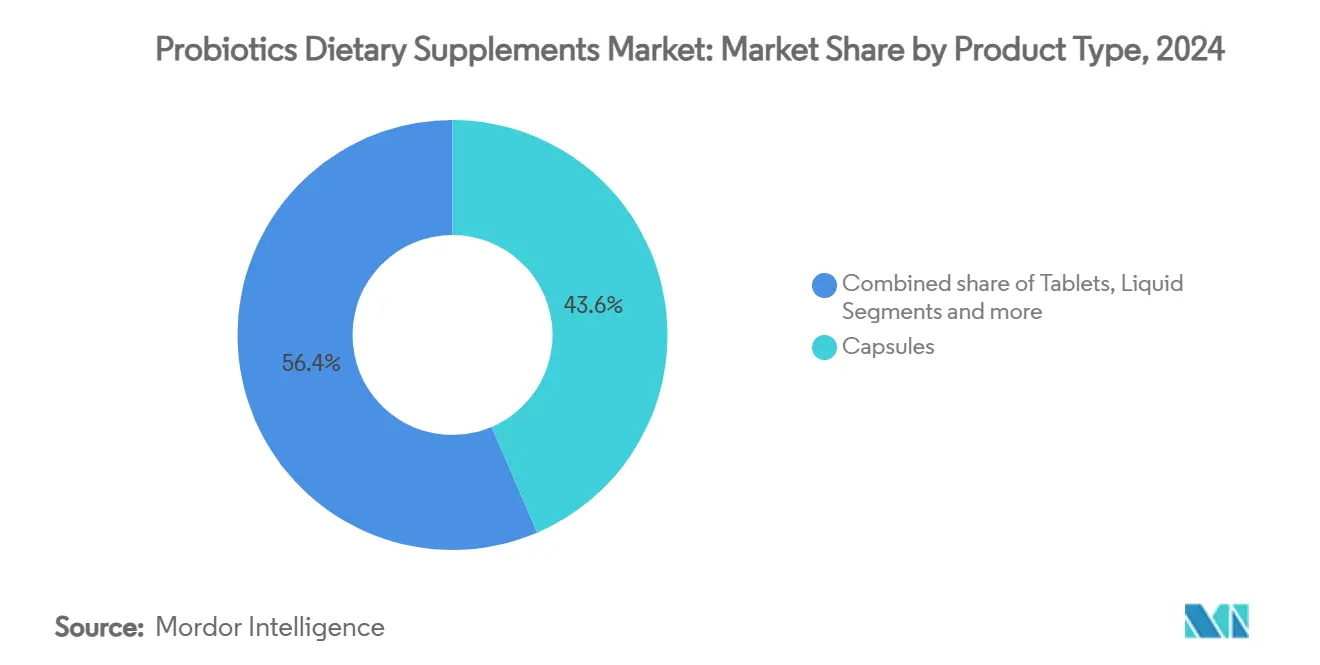

- By product type, capsules accounted for 43.56% of the probiotic dietary supplements market share in 2024, while gummies and chews are forecast to expand at a 13.56% CAGR through 2030.

- By consumer group, women represented 42.31% revenue share in 2024; the children segment is set to grow at a 12.22% CAGR until 2030.

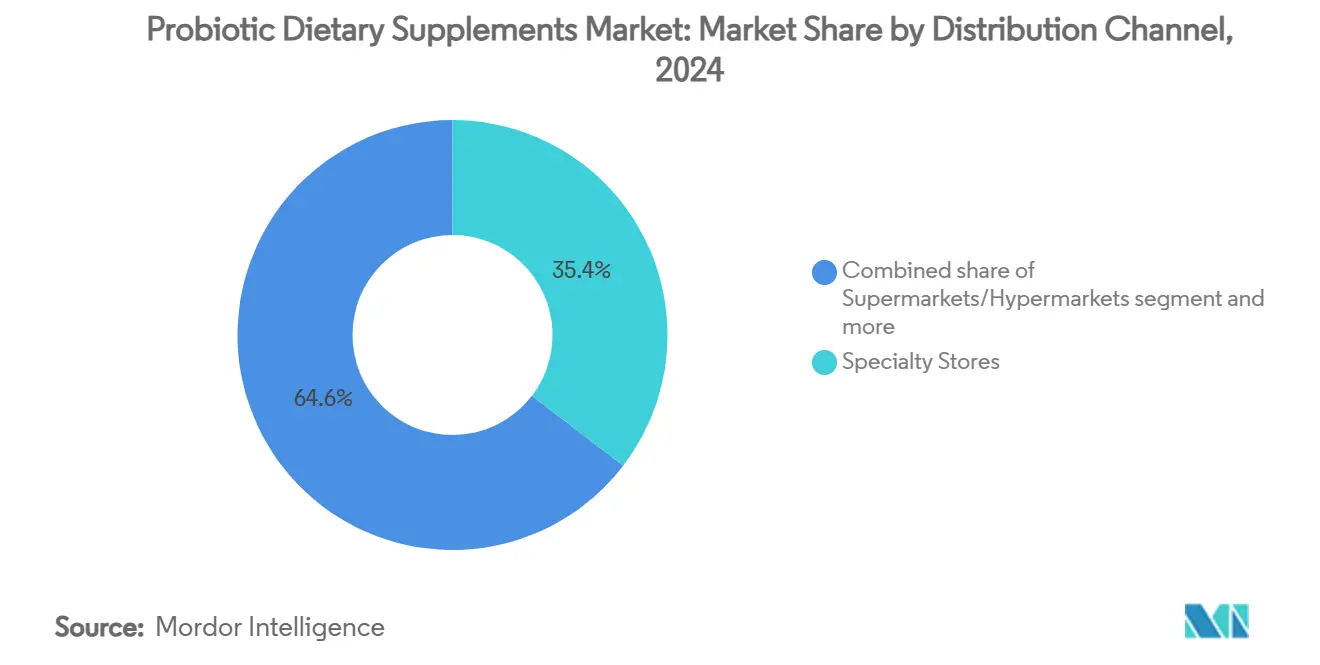

- By distribution channel, specialty stores captured 35.40% of the probiotic dietary supplements market share in 2024, whereas online stores will rise at a 13.66% CAGR between 2025-2030.

- By geography, Asia-Pacific led with 37.63% revenue share in 2024; the Middle East and Africa market is projected to register a 12.06% CAGR to 2030

Global Probiotic Dietary Supplement Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of digestive disorder and increasing demand among the geriatric consumers | +2.8% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Growing consumer awareness for gut health and preventive approach adoption | +2.4% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Rising demand for clean-label and natural solutions aids probiotic supplements growth | +1.9% | North America and Europe primarily, expanding to Asia-Pacific | Medium term (2-4 years) |

| Research advancements in probiotic strains and delivery systems drive market growth | +1.7% | Global, with Research and Development centers in North America and Europe | Long term (≥ 4 years) |

| Innovation in product formats and delivery systems | +1.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Increasing health consciousness among aging population | +1.2% | Global, strongest in developed economies | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Prevalence of Digestive Disorder and Increasing Demand among the Geriatric Consumers

The demand for probiotic dietary supplements is surging, as digestive disorders like irritable bowel syndrome (IBS) and inflammatory bowel disease (IBD) become more prevalent. These supplements are increasingly recognized for their ability to improve gut health by balancing the gut microbiota, which plays a crucial role in overall digestive function. Geriatric consumers, who are more susceptible to digestive health issues due to the natural aging process, are adopting probiotics as a preventive and therapeutic measure. Additionally, the growing body of scientific research supporting the efficacy of probiotics in managing digestive disorders has further boosted consumer confidence in these products. The National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) reports that around 60 to 70 million Americans grapple with digestive diseases each year, highlighting the widespread nature of these conditions [1]Source: National Institute of Diabetes and Digestive and Kidney Diseases, "Digestive Diseases Statistics for the United States", niddk.nih.gov. This has led to heightened awareness about the importance of maintaining digestive health, not only among older adults but also across other age groups. Probiotics are increasingly being marketed as a natural and effective solution, appealing to health-conscious consumers seeking alternatives to traditional medications. With rising awareness about digestive health and the scientifically backed advantages of probiotics, the market is poised for significant growth in the coming years, driven by both consumer demand and advancements in probiotic formulations.

Growing Consumer Awareness for Gut Health and Preventive approach Adoption

Consumers increasingly prioritize gut health, driving the demand for probiotic dietary supplements. This shift is fueled by growing awareness of the role gut health plays in overall well-being, including digestion, immunity, and mental health. Additionally, the adoption of a preventive approach to health management has encouraged individuals to incorporate probiotics into their daily routines to address potential health issues before they arise. According to the Council for Responsible Nutrition Survey 2023, nearly 74% of adults in the United States reported using dietary supplements, including probiotics, highlighting the growing consumer inclination toward such products [2]Source: Council for Responsible Nutrition Survey, "2023 CBN Survey on Dietary Supplements", crnusa.org. This trend is further supported by increasing access to information through digital platforms, enabling consumers to make informed decisions about their health and dietary choices. Moreover, the rising prevalence of digestive disorders, lifestyle-related health concerns, and the growing inclination toward natural and functional food products have further propelled the market. Probiotic dietary supplements are increasingly perceived as a convenient and effective solution for maintaining gut health, which has led to their widespread adoption across various demographics. The availability of diverse product formats, such as capsules, powders, and gummies, has also contributed to the market's growth by catering to consumer preferences and enhancing ease of consumption.

Rising Demand for Clean-Label and Natural Solutions Aids Probiotic Supplements Growth

Driven by clean-label preferences, formulators in the probiotic dietary supplements market are increasingly adopting naturally-derived strains and minimal processing techniques. This trend is fueled by a growing consumer demand for transparency and authenticity in product formulations. Consumers are becoming more cautious about the potential side effects of synthetic additives and pharmaceutical interventions, leading to a preference for products perceived as safer and more natural. As a result, manufacturers are focusing on developing innovative solutions that cater to these preferences, such as using fermentation-based processes and sourcing ingredients from natural origins. Additionally, the rising awareness of gut health and its connection to overall well-being has further amplified the demand for clean-label probiotic supplements. Companies are leveraging advancements in strain development and delivery systems to enhance product efficacy while maintaining clean-label standards. This shift not only aligns with consumer expectations but also provides opportunities for differentiation in an increasingly competitive market. Furthermore, regulatory bodies in various regions are emphasizing the importance of clear labeling and natural formulations, which is encouraging manufacturers to prioritize clean-label innovations.

Increasing Health Consciousness Among Aging Population

The increasing health consciousness among the aging population is a significant driver for the probiotic dietary supplements market. As individuals age, they become more aware of the importance of maintaining gut health and overall well-being. According to the Population Reference Bureau, the number of Americans ages 65 and older is projected to increase from 58 million in 2022 to 82 million by 2050 (a 47% increase), and this demographic is projected to grow further [3]Source: Population Reference Bureau, "Fact Sheet- Ageing in the United States", prb.org. The aging demographic generates demand for dietary supplements, specifically probiotics, to address age-related health conditions, including digestive disorders, immune system deficiencies, and insufficient nutrient absorption. Clinical studies validating the efficacy of probiotics in gastrointestinal health, immune response, and physiological functions have enhanced market acceptance. Government healthcare initiatives and awareness programs emphasize the preventive benefits of probiotics, influencing the older population to integrate these supplements into their health maintenance routines. These market drivers support continued growth as aging consumers implement supplement-based preventive healthcare strategies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory challenges and inconsistency in guidelines across markets | -1.8% | Global, particularly European Union vs United States divergence | Medium term (2-4 years) |

| Issues with product stability and shelf life | -1.4% | Global, acute in tropical regions | Short term (≤ 2 years) |

| Consumer skepticism due to inconsistent efficacy | -1.1% | Global, strongest in developed markets | Medium term (2-4 years) |

| High cost of production and competition from substitutes such as functional/fermented food and drinks | -0.9% | Global, with regional variations | Long term (≥ 4 years) |

Source: Mordor Intelligence

Regulatory Challenges and Inconsistency in Guidelines across Markets

The probiotic dietary supplements market faces significant challenges due to regulatory hurdles and inconsistencies in guidelines across various markets. Regulatory frameworks for probiotics differ widely between regions, creating confusion and compliance difficulties for manufacturers. For instance, some markets classify probiotics as dietary supplements, while others categorize them as pharmaceuticals, leading to varying approval processes and labeling requirements. This lack of standardization complicates product registration and delays market entry. Additionally, frequent changes in regulations and the absence of globally harmonized guidelines further exacerbate these challenges, increasing operational costs and limiting the ability of companies to scale their operations effectively. Such regulatory complexities act as a major restraint, hindering the growth potential of the probiotic dietary supplements market. Moreover, the lack of a unified definition for probiotics across regions adds to the complexity.

Issues with Product Stability and Shelf Life

One of the major restraints in the probiotic dietary supplements market is the issue of product stability and shelf life. Probiotic supplements contain live microorganisms that require specific conditions to remain viable and effective. Factors such as temperature, humidity, and exposure to light can significantly impact the stability of these products. Manufacturers face challenges in maintaining the potency of probiotics throughout the supply chain, from production to storage and distribution. Additionally, ensuring an extended shelf life without compromising the efficacy of the probiotics is a critical concern. The degradation of live cultures over time can lead to reduced effectiveness, which may affect consumer trust and satisfaction. This issue necessitates the development of advanced packaging solutions and innovative formulations to enhance stability. Moreover, regulatory requirements for labeling and claims regarding the viability of probiotics add another layer of complexity. Companies must invest in research and development to address these challenges while adhering to stringent quality standards. These factors collectively act as a restraint, limiting the growth potential of the probiotic dietary supplements market.

Segment Analysis

By Product Type: Gummies Disrupt Traditional Capsule Dominance

In 2024, capsules hold the largest market share at 43.56%, highlighting their established position in the probiotic dietary supplements market. This dominance can be attributed to consumer familiarity with capsules as a delivery format and their widespread acceptance across various demographics. Additionally, capsules offer manufacturing cost advantages, particularly for traditional probiotic strains, making them a preferred choice for producers. Their ability to preserve the stability and efficacy of probiotics further reinforces their popularity among consumers and manufacturers alike.

On the other hand, gummies and chews represent the fastest-growing segment in the probiotic dietary supplements market, with a remarkable CAGR of 13.56% projected through 2030. This growth is driven by significant improvements in palatability, making these formats more appealing to a broader audience. The segment is also benefiting from demographic expansion, particularly among pediatric populations and adults seeking convenient and enjoyable alternatives to traditional capsules. The convenience, taste, and ease of consumption offered by gummies and chews are key factors propelling their adoption, positioning them as a dynamic and rapidly evolving segment in the market.

Note: Segment shares of all individual segments available upon report purchase

By Consumer Group: Children Drive Demographic Expansion

In 2024, women will command the largest share of the probiotics supplement market, accounting for 42.31%. This trend is fueled by a surge in health awareness and targeted applications in areas like vaginal and digestive health. Such a stronghold underscores the industry's focus on product development and marketing strategies tailored to women's distinct health needs, spanning from pregnancy support and urinary tract health to hormonal balance. Additionally, the increasing availability of gender-specific probiotic formulations and the growing emphasis on women's wellness in the healthcare industry further contribute to this dominance. Companies are leveraging these factors by launching innovative products and campaigns that resonate with women's health priorities, ensuring sustained market leadership in this segment.

Yet, it's the children's segment that's rapidly becoming the market's powerhouse, projected to grow at a robust 12.22% CAGR from 2025 to 2030. This surge is largely driven by parents' growing inclination towards preventative health measures for their kids. Innovations play a pivotal role, with child-friendly formats like gummies and chewables addressing traditional compliance hurdles, all while ensuring potent probiotic doses. Furthermore, the rising prevalence of digestive issues and weakened immunity among children has heightened the demand for probiotics as a preventive and therapeutic solution. Manufacturers are increasingly focusing on creating appealing, nutrient-rich products that cater to children's taste preferences while meeting parental expectations for safety and efficacy, thereby driving growth in this segment.

By Distribution Channel: E-commerce Accelerates Market Access

Specialty stores command 35.40% market share in 2024, leveraging expert consultation and premium product positioning to maintain consumer trust in a category plagued by quality inconsistencies. These channels provide educational value and personalized recommendations that online platforms struggle to replicate, particularly for condition-specific probiotic applications requiring professional guidance. Online stores represent the fastest-growing channel at 13.66% CAGR through 2030, driven by subscription models, direct-to-consumer brands, and enhanced product information accessibility. The expansion of e-commerce in health and wellness products, specifically supplements, increased due to consumer acceptance of online purchasing during the pandemic.

Supermarkets/hypermarkets maintain significant volume through mass-market accessibility but face margin pressure from private-label competition and limited shelf space for specialized formulations. The channel dynamics favor brands with strong digital marketing capabilities and direct-to-consumer relationships, as traditional retail margins compress under competitive pressure. Other distribution channels, including pharmacies and health food stores, serve niche applications but struggle to compete with the convenience and pricing advantages of digital platforms.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, Asia-Pacific dominates the global probiotic dietary supplements market, holding a 37.63% market share. This leadership is attributed to the region's deep-rooted traditions of consuming fermented foods, which have naturally integrated probiotics into daily diets for centuries. Additionally, the regulatory framework in Asia-Pacific is progressively evolving, fostering a favorable environment for both traditional and innovative probiotic applications. Countries like China, Japan, and South Korea are key contributors to this dominance, driven by high consumer awareness, increasing health consciousness, and the presence of major market players investing in research and development.

The Middle East and Africa represent the fastest-growing geography in the probiotic dietary supplements market, with a projected CAGR of 12.06% through 2030. This growth is primarily driven by rapid advancements in healthcare infrastructure, which are improving access to dietary supplements across the region. Furthermore, rising disposable incomes and a growing awareness of the health benefits associated with probiotics are encouraging consumers to adopt these supplements. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are emerging as key markets, supported by government initiatives to enhance healthcare systems and promote wellness.

North America and Europe maintain significant positions in the probiotic dietary supplements market, but their growth rates are slowing due to regulatory complexities and market saturation in core consumer segments. In North America, the United States leads the market, supported by a well-established dietary supplement industry and high consumer demand for health and wellness products. However, stringent regulatory requirements and increasing competition are creating challenges for market players. Similarly, in Europe, countries like Germany, the United Kingdom, and France are key contributors, but the market faces hurdles such as strict labeling laws and a mature consumer base, which limit growth opportunities.

Competitive Landscape

The probiotic dietary supplements market demonstrates moderate fragmentation. This highlights the coexistence of diverse players, including multinational pharmaceutical giants, specialized probiotic companies, and emerging biotechnology firms. These entities adopt varied strategic approaches to establish their presence in the market. Multinational corporations leverage their extensive distribution networks, robust financial resources, and well-established brand recognition to maintain a competitive edge. On the other hand, smaller firms focus on niche markets and innovative product offerings to differentiate themselves in this competitive landscape.

Market leaders dominate the space by capitalizing on their global reach and economies of scale, enabling them to cater to a wide consumer base. Their strategies often include partnerships, acquisitions, and collaborations to expand their product portfolios and strengthen their market position. Additionally, these companies invest heavily in research and development to introduce advanced probiotic strains and formulations that address specific health concerns, such as digestive health, immunity, and mental well-being. This focus on innovation allows them to meet evolving consumer demands and maintain their leadership in the market.

In contrast, smaller players and emerging biotechnology firms adopt a more targeted approach, emphasizing strain-specific innovations and therapeutic applications. These companies often focus on developing probiotics tailored to specific health conditions or demographic groups, such as infants, the elderly, or athletes. By addressing unmet needs and offering personalized solutions, they carve out a niche in the market. Furthermore, these firms rely on direct-to-consumer channels and digital marketing strategies to reach their target audience effectively. This dynamic interplay between large and small players contributes to the moderate fragmentation observed in the probiotic dietary supplements market.

Probiotic Dietary Supplement Industry Leaders

-

BioGaia AB

-

Nestlé S.A.

-

Reckitt Benckiser Group PLC

-

Amway Corporation

-

Yakult Honsha Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Pharmavite's Nature Made brand had expanded its digestive health product line by introducing probiotic, prebiotic, and fiber supplements for daily gut health support. The new products included Nature Made Probiotic + Prebiotic Fiber Gummies, which contained Lactospore probiotic strain and 3 grams of prebiotic fiber in mixed berry flavor.

- December 2024: BioGaia released the Gastrus PURE ACTION probiotic supplement for sensitive digestive systems. The product incorporated patented L. reuteri strains, supported by clinical studies that demonstrated reduced IBS symptoms and enhanced quality of life.

- August 2024: Actial Nutrition had launched VSL4 Gut, a daily probiotic supplement formulated to improve digestive health and bowel regularity. The shelf-stable product supported gut function, targeting consumers seeking better digestion and gastrointestinal health.

Global Probiotic Dietary Supplement Market Report Scope

Probiotic dietary supplements are live microorganisms that, when consumed, offer health benefits to the host by improving gut health.

The global probiotic supplements market is segmented into product type, consumer group, distribution channel, and geography. The global probiotic supplements market offers a range of product types, including capsules, tablets, gummies & chews, liquids, and others. Based on the consumer group, the market is segmented into men, women, and children. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online stores, and other distribution channels. The study also covers the global analysis of North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing hathe s been done in value terms in USD for all the abovementioned segments.

| By Product Type | Tablets | ||

| Capsules | |||

| Gummies and Chews | |||

| Liquids | |||

| Others (sachets, oral strips etc.) | |||

| By Consumer Group | Men | ||

| Women | |||

| Children | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Specialty Stores | |||

| Online Stores | |||

| Other Distribution Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Sweden | |||

| Belgium | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Indonesia | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| South Africa | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Rest of Middle East and Africa | |||

| Tablets |

| Capsules |

| Gummies and Chews |

| Liquids |

| Others (sachets, oral strips etc.) |

| Men |

| Women |

| Children |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Sweden | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current probiotic dietary supplements market size in 2025?

The probiotic dietary supplements market size stands at USD 12.51 billion in 2025 and is projected to grow USD 22.01 through 2030.

Which product format holds the largest share of the probiotic dietary supplements market?

Capsules lead the category with 43.56% probiotic dietary supplements market share in 2024, supported by mature manufacturing and consumer familiarity.

Why are gummies and chews growing so quickly?

Palatable taste, child-friendly textures and new encapsulation technologies enable gummies to post a 13.56% CAGR, the fastest among all formats.

Which region is the fastest-growing for probiotic supplements?

The Middle East and Africa is expected to register a 12.06% CAGR through 2030 owing to healthcare investments and rising disposable incomes.