Note: Segment shares of all individual segments available upon report purchase

The Primary Cell Culture Market Report is Segmented by Product Type (Primary Cells, and More), Cell Type (Animal Cells and Human Cells), Separation Method (Enzymatic Disaggregation, and More), Culture Platform (2D Monolayer Culture, and More), Applications (Vaccine Production, and More), End Users (Diagnostic Laboratories, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

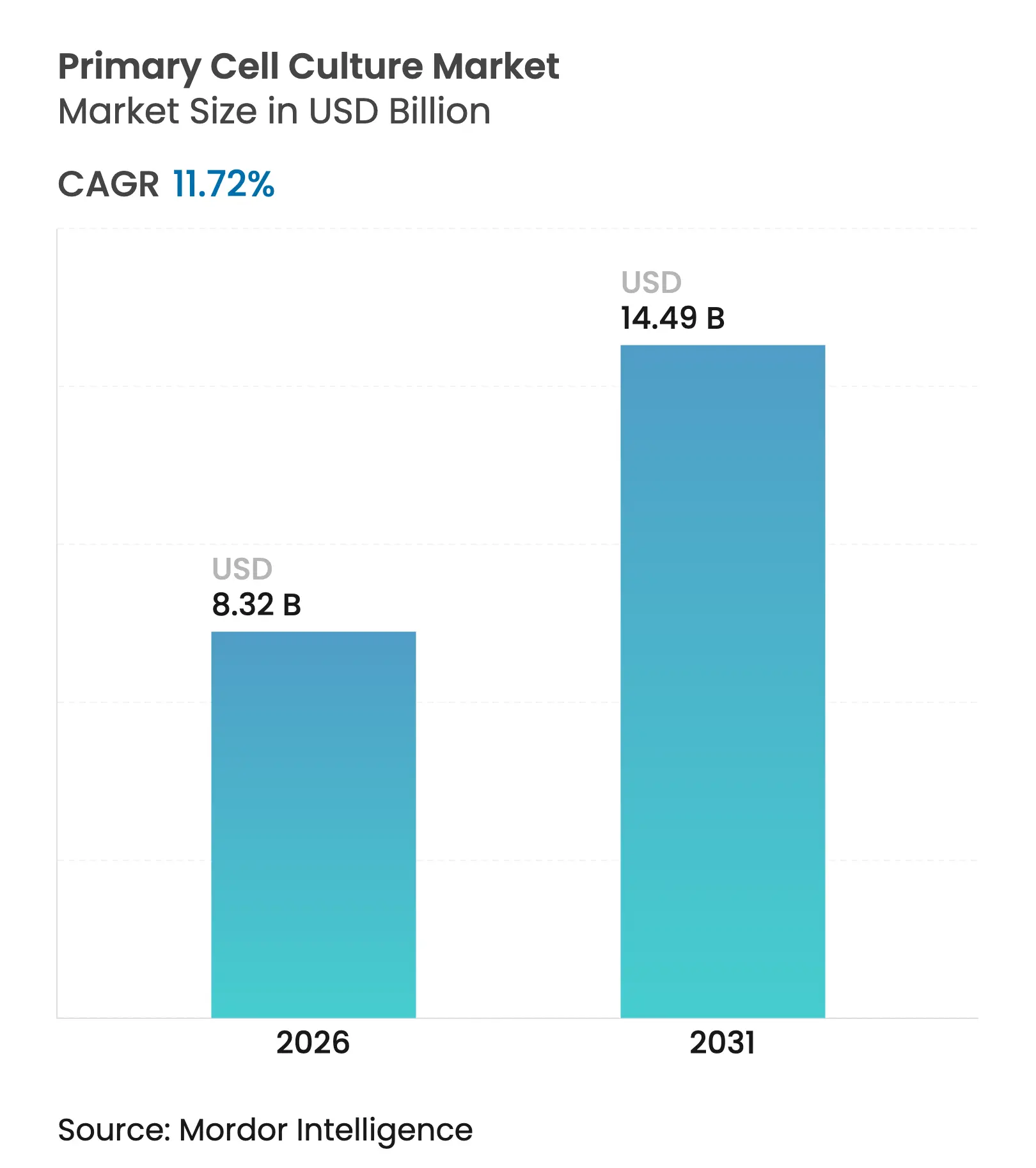

| Market Size (2026) | USD 8.32 Billion |

| Market Size (2031) | USD 14.49 Billion |

| Growth Rate (2026 - 2031) | 11.72 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The primary cell culture market size is expected to grow from USD 7.45 billion in 2025 to USD 8.32 billion in 2026 and is forecast to reach USD 14.49 billion by 2031 at 11.72% CAGR over 2026-2031. This robust trajectory reflects the decisive shift by researchers and drug developers toward physiologically relevant models that reduce late-stage clinical attrition. Pharmaceutical firms are accelerating investment in 3D and microfluidic systems, artificial-intelligence-guided analytics, and closed-system bioreactors, all of which sharpen the predictive power of preclinical studies. Reagents and supplements keep the largest revenue base because they are consumed continuously, while microfluidic organ-on-chip platforms post the fastest uptake. Growth is further amplified by a rising global burden of chronic disease, regulatory endorsement of non-animal test models, and increasing outsourcing of specialized cell-based assays to contract research organizations.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Prevalence of Chronic & Infectious Diseases

Necessitating Advanced Cell-based Research Models

Rising Prevalence of Chronic & Infectious Diseases

Necessitating Advanced Cell-based Research Models

| +3.6% | Global, with heightened impact in North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+3.6%

| Geographic Relevance:

Global, with heightened impact in North America and Europe

| Impact Timeline:

Medium term (2-4 years)

|

Growing Investment in Personalized & Precision

Medicine Initiatives Worldwide

Growing Investment in Personalized & Precision

Medicine Initiatives Worldwide

| +3.0% | North America, Europe, and emerging Asia-Pacific markets | Long term (≥ 4 years) | |||

Increasing Biopharmaceutical R&D Expenditure on Cell

& Gene Therapies

Increasing Biopharmaceutical R&D Expenditure on Cell

& Gene Therapies

| +2.4% | Global, with concentration in innovation hubs (Boston, San Francisco, Shanghai, Basel) | Medium term (2-4 years) | |||

Advancements in Automated & Closed-System Primary Cell

Culture Technologies

Advancements in Automated & Closed-System Primary Cell

Culture Technologies

| +1.8% | North America, Europe, and advanced Asia-Pacific markets | Short term (≤ 2 years) | |||

Favorable Regulatory Support & Fast-Track Approvals

for Cell-Based Therapeutics

Favorable Regulatory Support & Fast-Track Approvals

for Cell-Based Therapeutics

| +1.2% | North America and Europe, with emerging influence in Japan and South Korea | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Chronic Disease Burden Drives Demand for Physiologically Relevant Models

Escalating incidences of oncology, metabolic, and neurodegenerative disorders heighten the need for primary cells that mirror human tissue architecture. Drug candidates first screened on primary models show a 23% higher transition to successful clinical outcomes compared with those vetted only on immortalized lines. Pandemic-era respiratory studies underscored these benefits and steered funding toward human epithelial and immune primary cultures for vaccine and antiviral development. Hospitals and academic centers now routinely bank patient-derived biopsies, expanding supplies of ethically consented cells that enable disease-specific assays.

Precision Medicine Initiatives Fuel Primary Cell Culture Innovation

National programs such as the United States’ All of Us and Europe’s 1+ Million Genomes drive demand for patient-matched cell systems that reveal genomic and proteomic variability. In 2024 a landmark tumor-organoid trial predicted immunotherapy responses with 89% accuracy, far outperforming prior xenograft screens. Pharmaceutical pipelines increasingly incorporate such models at hit-to-lead stages, compressing decision timelines and reducing costly late failures. Bioinformatic platforms now pair organoids with multi-omics readouts to chart responder sub-populations, informing targeted trial design.

Biopharmaceutical R&D Shifts Toward Cell-Based Therapeutics

Cell and gene therapy pipelines grew 7% in Q4 2024, with 83% more programs at the pre-registration stage than the year before[2]American Society of Gene & Cell Therapy, “Gene, Cell, & RNA Therapy Landscape Report Q4 2024,” asgct.org. Primary T-cells, stem cells, and dendritic cells form the starting material for these therapies, stimulating double-digit annual growth in specialized isolation reagents, closed bioreactors, and GMP-grade media. FDA approvals of several autologous and allogeneic products in 2024–2025 validated commercial viability, drawing new capital into advanced cell expansion and characterization technologies[1]A. Mack & A. Fiedorowicz, “FDA’s Draft Guidance On Safety Testing Of Human Allogeneic Cells,” Cell & Gene, cellandgene.com.

Advancements in Automated & Closed-System Primary Cell Culture Technologies

Robotic workstations integrate enzymatic digestion, washing, and seeding steps, minimizing contamination risk and technician variability. Microfluidic chips equipped with optical and electrochemical sensors capture real-time metabolic flux, permitting adaptive media feeds that lengthen viable culture windows. Artificial-intelligence software evaluates large image libraries to flag sub-optimal morphologies early, preventing failed runs and conserving expensive reagents. These gains ease adoption by small laboratories that previously lacked the expertise to handle fragile primary cells.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Technical Complexity and Limited Standardization of

Primary Cell Isolation & Culture Protocols

Technical Complexity and Limited Standardization of

Primary Cell Isolation & Culture Protocols

| -1.8% | Global, with greater impact in emerging markets with limited technical expertise | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.8%

| Geographic Relevance:

Global, with greater impact in emerging markets with

limited technical expertise

| Impact Timeline:

Medium term (2-4 years)

|

Ethical & Regulatory Concerns Surrounding Procurement

of Human and Animal Tissues

Ethical & Regulatory Concerns Surrounding Procurement

of Human and Animal Tissues

| -1.2% | Global, with particular stringency in Europe and North America | Long term (≥ 4 years) | |||

High Cost & Supply-Chain Constraints of High-Quality

Primary Cell Culture Reagents and Media

High Cost & Supply-Chain Constraints of High-Quality

Primary Cell Culture Reagents and Media

| -0.6% | Emerging markets in Asia-Pacific, Middle East, and Latin America | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Technical Complexity Creates Barriers to Widespread Adoption

Primary cells demand tissue-specific isolation know-how, strict passage limits, and custom media recipes. A 2024 survey revealed 68% of researchers struggle to achieve reproducible results with primary cultures, citing inconsistent viability and phenotype drift. Scarcity of skilled personnel inflates labor costs, and short cell lifespans increase batch frequency, straining laboratory budgets. These hurdles slow uptake in smaller biotech firms and academic centers lacking specialized infrastructure.

Ethical and Regulatory Frameworks Constrain Tissue Sourcing

Stringent consent rules and animal welfare regulations limit access to fresh tissues, especially across borders with divergent legal standards. The European Medicines Agency, for example, mandates detailed donor screening and traceability, lengthening approval timelines for multi-site studies. Variability in regional guidelines complicates global supply chains, forcing companies to duplicate collections in each jurisdiction, which inflates cost and delays project starts.

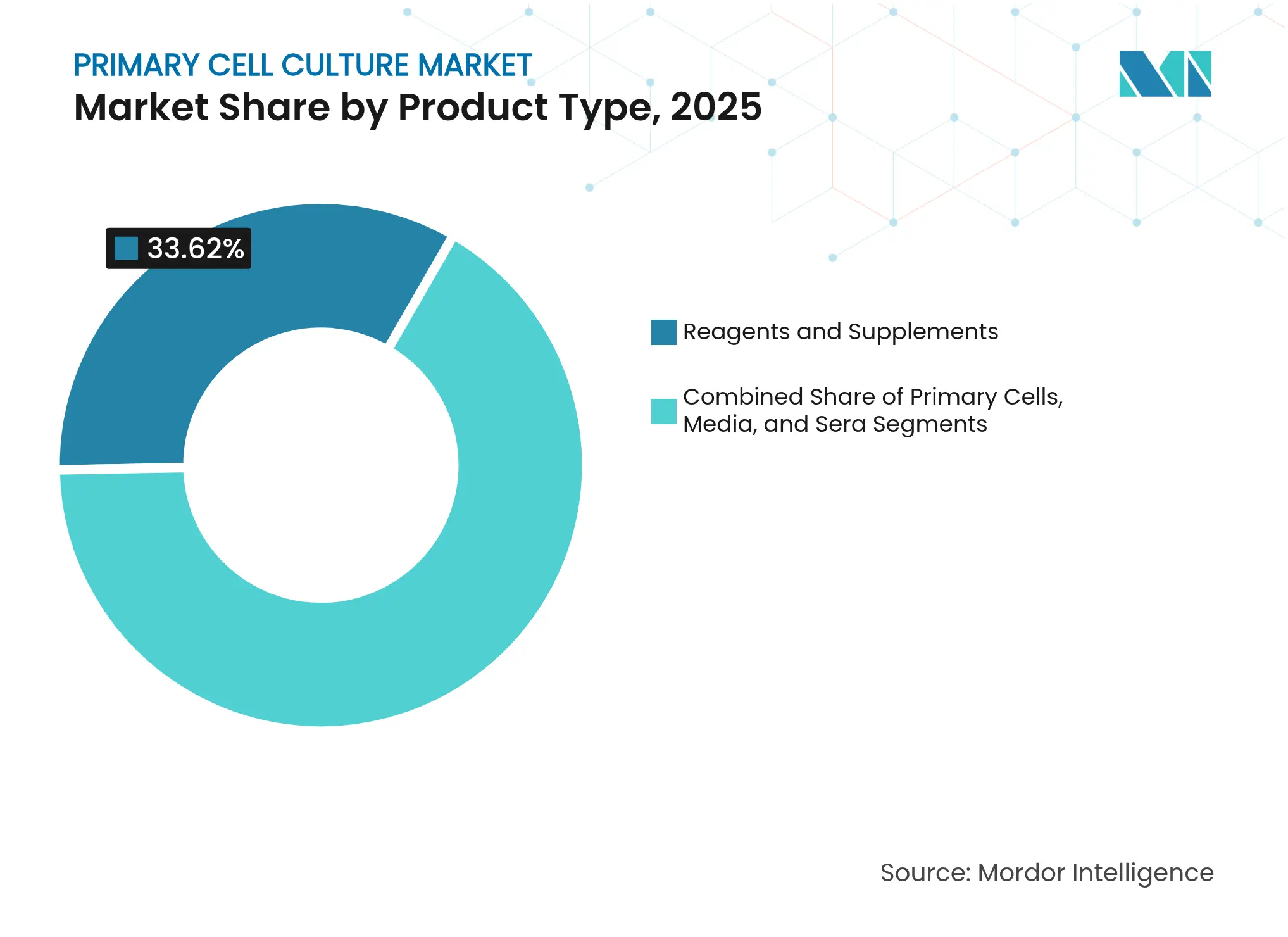

By Product Type: Reagents & Supplements Command Spend while Primary Cells Accelerate Growth

Reagents and supplements contributed 33.62% of primary cell culture market revenue in 2025, driven by recurrent purchase cycles and premium pricing for GMP-grade components. Serum-free and chemically defined formulations remove lot-to-lot variability, boosting experimental reproducibility. Proprietary mixes laced with recombinant growth factors carry margins exceeding those of basal media. BenchStable Media eliminates cold storage, trimming logistical costs and supporting wider geographic reach. Primary cells represent the fastest expanding sub-category at a 14.12% CAGR, propelled by heightened demand for patient-specific materials across precision oncology and regenerative medicine pipelines.

Specialized cryopreservation kits and rapid-thaw protocols now preserve delicate phenotypes, widening the shipping radius for suppliers. Regulatory pressure for human-relevant data fuels procurement of donor-matched hepatocytes, cardiomyocytes, and neural precursors. These trends consolidate supplier–researcher partnerships and reinforce reagent pull-through, sustaining strong revenue momentum for established vendors.

Note: Segment shares of all individual segments available upon report purchase

By Cell Type: Human Cells Overtake Growth Leadership amid Translational Priority

Animal cells still dominate with 58.10% share thanks to entrenched protocols and lower costs, yet human cells clock a 15.08% CAGR. FDA Modernization Act 2.0 endorses human cell-based tests, accelerating adoption in safety-pharmacology screens. Human primary hepatocytes predict drug-induced liver injury with higher specificity, saving millions in downstream attrition. Gene-editing advances, including CRISPR knock-in of fluorescent reporters, expand assay versatility while retaining endogenous genetic backgrounds.

Immune-cell sub-sets sourced from leukapheresis donors underpin emerging off-the-shelf CAR-T and NK platforms. As a result, suppliers scaling leukopak isolation and cryobanking services secure long-term supply contracts with therapy developers, reinforcing market stickiness and raising switching costs for end users.

By Separation Method: Enzymatic Disaggregation Retains Lead while Mechanical Innovation Gathers Pace

Enzymatic cocktails of collagenase, dispase, and liberase remain the first choice for rapid tissue dissociation, capturing 33.05% market share in 2025. High yield and broad tissue compatibility sustain their dominance. Yet mechanical separation approaches grow at a 13.42% CAGR as gentler shear devices and acoustophoretic systems safeguard surface epitopes vital for downstream functional assays. Akadeum’s microbubble technology lifts viable yields of delicate immune cells, reducing enzymatic exposure that can cleave receptor proteins.

Hybrid workflows that pair short enzyme pulses with controlled mechanical agitation strike a balance between throughput and phenotype integrity. Such protocols appeal to immuno-oncology teams concerned about altering checkpoint receptor expression, thereby raising demand for next-generation mechanical equipment and accessories.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Culture Platform: Microfluidic Systems Disrupt the 2D Status Quo

Traditional 2D monolayers still hold 69.40% of primary cell culture market revenue on the back of simplicity and legacy assay compatibility. However, microfluidic organ-on-chip systems headline segment growth at an 18.05% CAGR, mirroring industry pursuit of in-vivo-like spatial gradients and mechanical cues. A 2025 report showcased a flexible 3D-printed chip that hosted both primary myoblasts and induced pluripotent stem cell-derived organoids, achieving sustained contractility over four weeks.

Integrated oxygen and pH microsensors permit closed-loop media perfusion, stabilizing microenvironments and extending experiment windows. Drug developers value the platform’s ability to couple multiple organ chips, such as liver–heart, to forecast systemic toxicity early, reducing reliance on costly animal studies and improving clinical translation odds.

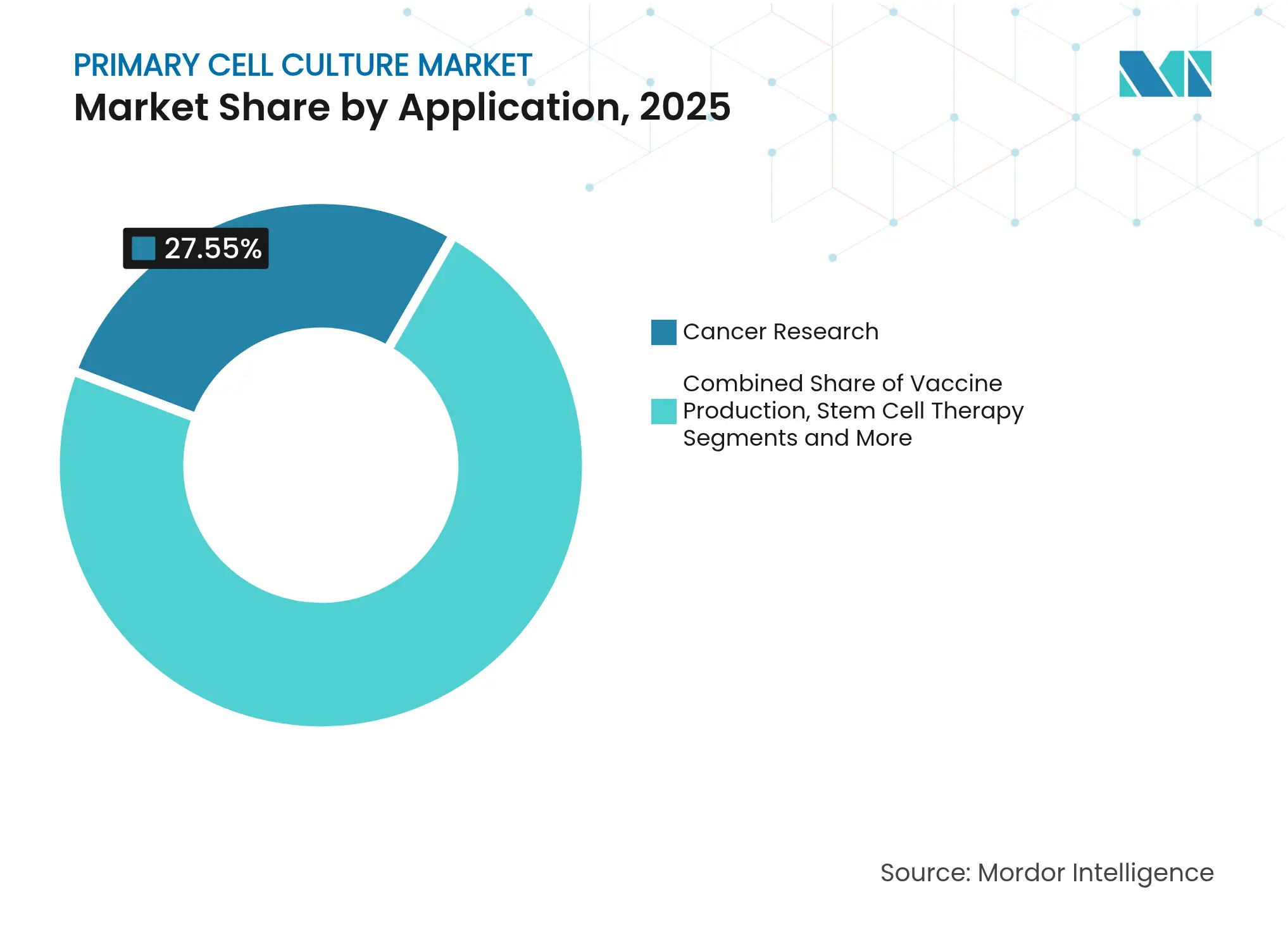

By Application: Cancer Research Dominates, Regenerative Medicine Accelerates

Cancer research consumed 27.55% of the primary cell culture market size in 2025, anchored by widespread use of patient-derived tumor organoids in drug screening pipelines. PromoCell’s kit for enriching cancer stem cells supports studies into metastasis and therapy resistance. Regenerative medicine, however, advances fastest at 14.36% CAGR, powered by stem-cell-based interventions for cardiac, retinal, and musculoskeletal repair. Corning’s low-attachment vessels and xeno-free matrices streamline expansion of mesenchymal stem cells destined for clinical manufacturing.

Global regulators have begun issuing expedited pathways for regenerative products, incentivizing early investment in scalable primary cell platforms. This regulatory tailwind combines with growing venture capital flows to escalate demand for consistency-enhancing culture tools.

Note: Segment shares of all individual segments available upon report purchase

By End User: Pharma Leads, CROs Accelerate through Outsourcing Wave

Pharmaceutical and biotechnology enterprises controlled 51.30% of 2025 demand, leveraging primary cells to validate targets and optimize lead compounds. Extensive internal budgets permit adoption of high-throughput 3D screening suites and specialized omics integration. In parallel, contract research organizations post a 12.94% CAGR as sponsor companies offload complex primary cell assays. STEMCELL Technologies’ expanded Contract Assay Services portfolio now handles toxicity screens using primary hepatocytes and cardiomyocytes, illustrating the outsourced-service boom.

Academic institutes remain vital for discovery research, yet constrained grant cycles temper spending growth. Diagnostic labs, though still a small niche, adopt primary epithelial cells for ex-vivo infection testing, foreshadowing future clinical diagnostic avenues.

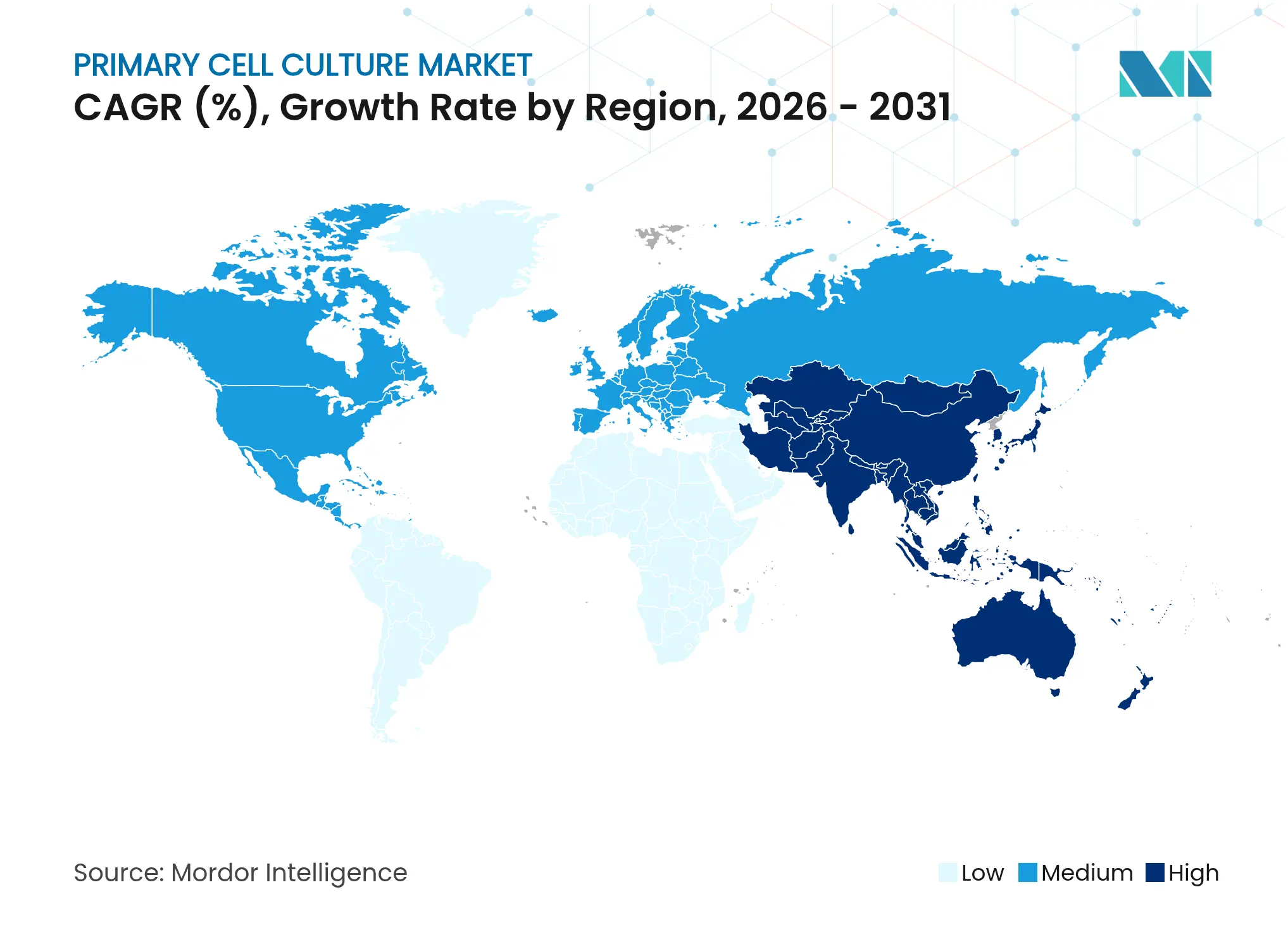

North America commanded 51.70% of 2025 revenue, buoyed by USD 45 billion in NIH funding and an FDA framework that openly supports human-cell alternatives to animal models. State-level incentives continue to draw biomanufacturing expansions, with multiple large-scale gene-therapy plants commencing operations in 2025. Venture investment clusters around Boston and the San Francisco Bay Area nurture numerous organ-on-chip and AI analytics start-ups, preserving the region’s innovation edge.

Europe holds the second-largest share. Germany and the United Kingdom anchor R&D spend, while Switzerland’s Lonza broke ground on an advanced fill-finish facility to serve cell-based products. The European Medicines Agency now furnishes guidance for microphysiological systems, prompting cross-border collaborations among academic and industrial labs. Grants under Horizon Europe allocate dedicated funds to human-cell-based safety assays, accelerating technology penetration.

Asia-Pacific represents the fastest expanding geography at a 13.82% CAGR. China, Japan, and South Korea funnel public and private capital into GMP cell-therapy suites and national biobanks. China’s dual-track regulatory model allows pilot clinical use of certain autologous therapies, stimulating demand for compliant primary cell supply chains. India’s growing CRO sector leverages cost advantages to secure global toxicology contracts, further enlarging the regional footprint of the primary cell culture market.

Middle East & Africa and South America collectively remain nascient but record double-digit advances. Saudi Arabia’s Vision 2030 added biotechnology clusters with subsidized cleanroom space. Brazil’s ANVISA approved its first domestically produced CAR-T trial in late 2024, underscoring momentum in Latin America. Technology transfer partnerships with established Western suppliers expedite capability building and de-risk early adoption.

Market Concentration

The primary cell culture market exhibits moderate concentration: the top five suppliers control significant global sales. Thermo Fisher Scientific, Merck KGaA, and Lonza Group integrate isolation kits, media, and downstream analytics into unified portfolios, locking in customer loyalty through bundle pricing and harmonized quality documentation. Merck’s 2024 acquisition spree added AI-driven bioprocess control software that dovetails with its media offerings, strengthening platform breadth.

Mid-tier specialists such as STEMCELL Technologies and Corning carve out high-growth niches. Corning’s ultra-low-attachment surfaces bolster stem-cell expansion, while STEMCELL markets defined cytokine cocktails tailored for hematopoietic progenitors. Niche innovators wield disruptive technologies: Akadeum’s buoyancy-based cell isolation shortens prep times, and PHC Corporation’s LiCellGrow bioreactor automates T-cell expansion, hastening CAR-T lot release.

Strategic alliances intensify. Lonza’s 2024 manufacturing pact with Vertex for type 1 diabetes cell therapy highlights a trend toward shared manufacturing risk, giving therapy developers instant GMP capacity while furnishing contract manufacturers with long-term volume visibility. Competitive differentiation increasingly hinges on demonstrating closed-system sterility, scalability, and regulatory-compliant data packages that smooth IND submissions.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value, USD)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

As per the scope of the report, primary cell culture is a technique where cells are isolated directly from an organism and grown in a controlled environment. It's a crucial tool in biomedical research, particularly in drug discovery, disease modeling, and personalized medicine. The primary cell culture market is segmented by product type, cell type, application, end user, and geography. By product type, the market is segmented into primary cell, reagents & supplements, and media. By cell type, the market is segmented into animal cells, and human cells. By application, the market is segmented into vaccine production, stem cell therapy, cancer research, drug discovery, and development, and others. By end user, the market is segmented into pharmaceutical and biotechnology companies, contract research organizations (CRO’s), and diagnostic laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

Market Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.