Hydraulic Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.64 Billion |

| Market Size (2031) | USD 18.99 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

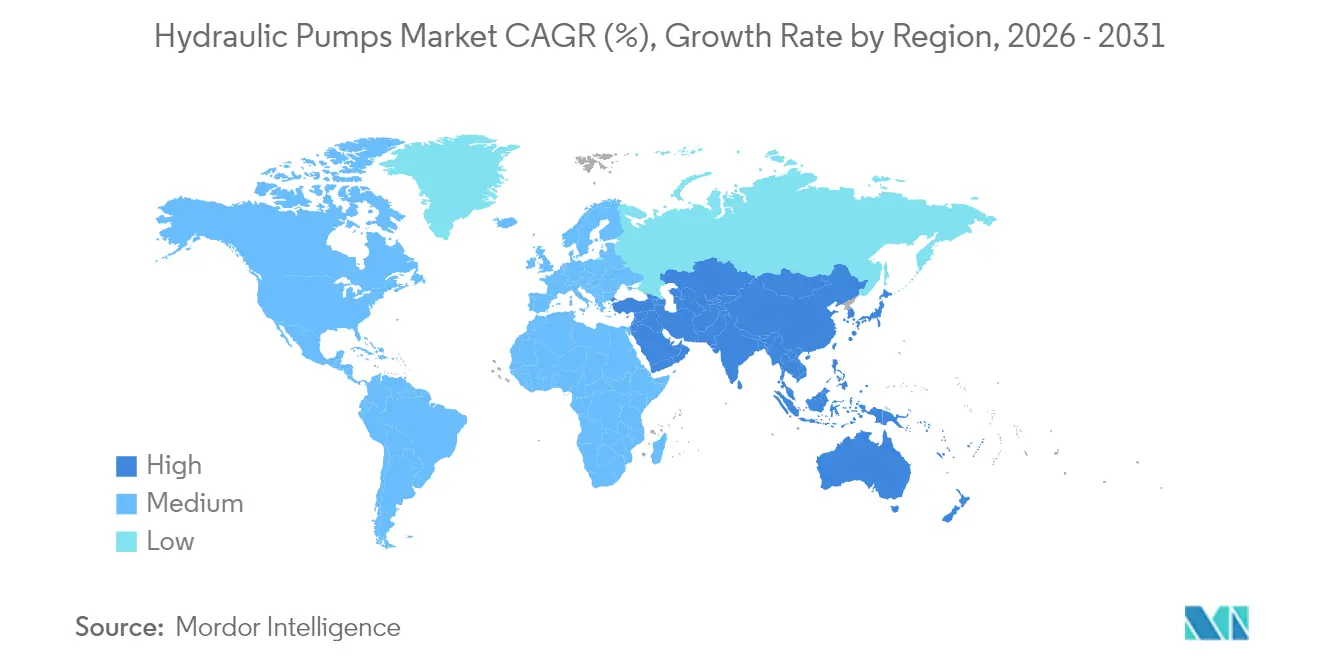

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hydraulic Pumps Market Analysis by Mordor Intelligence

The hydraulic pumps market size was valued at USD 13.9 billion in 2025 and estimated to grow from USD 14.64 billion in 2026 to reach USD 18.99 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031). Robust demand for high-capacity fluid-power equipment in construction, renewable energy, and automated manufacturing keeps the market on a steady expansion path. Infrastructure renewal programmes in China and India, combined with process-industry upgrades in the European Union and North America, continue to anchor baseline demand. Energy transition investments are unlocking new opportunities in wind-turbine pitch and yaw systems, hydrogen electrolyser compression modules, and grid-scale battery storage cooling circuits. Manufacturers are responding with higher-efficiency piston pump designs, intelligent control packages, and remanufacturing services that align with circular-economy mandates. Competition remains moderate, with global leaders reinforcing digital portfolios while regional suppliers target cost-sensitive applications. [1]European Commission, “Circular Economy Action Plan,” ec.europa.eu

Key Report Takeaways

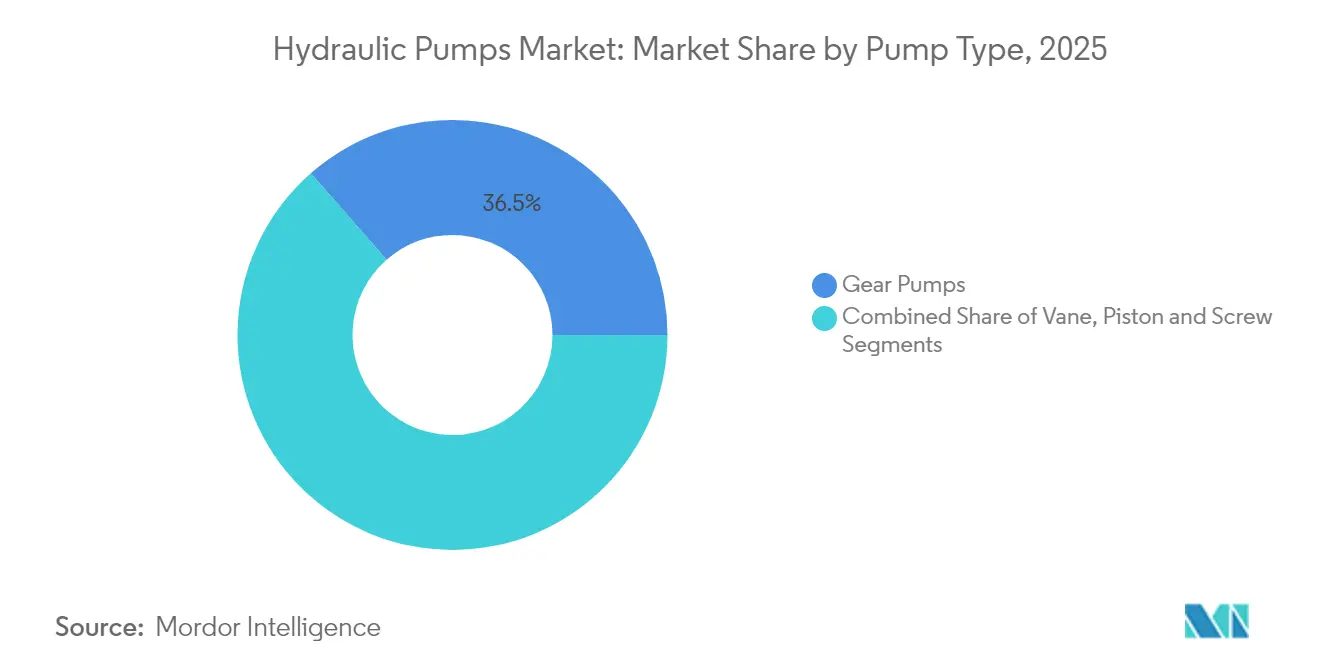

- By pump type, gear pumps led with 36.45% revenue share in 2025, while piston pumps are projected to expand at a 6.45% CAGR to 2031.

- By operating pressure, the 3000-5000 psi range held 41.35% of the hydraulic pumps market size in 2025; the >5000 psi bracket is advancing at an 7.95% CAGR through 2031.

- By application, Mobile Hydraulics accounted for 54.35% of the hydraulic pumps market share in 2025; Process & Energy is the fastest-growing application at 7.05% CAGR to 2031.

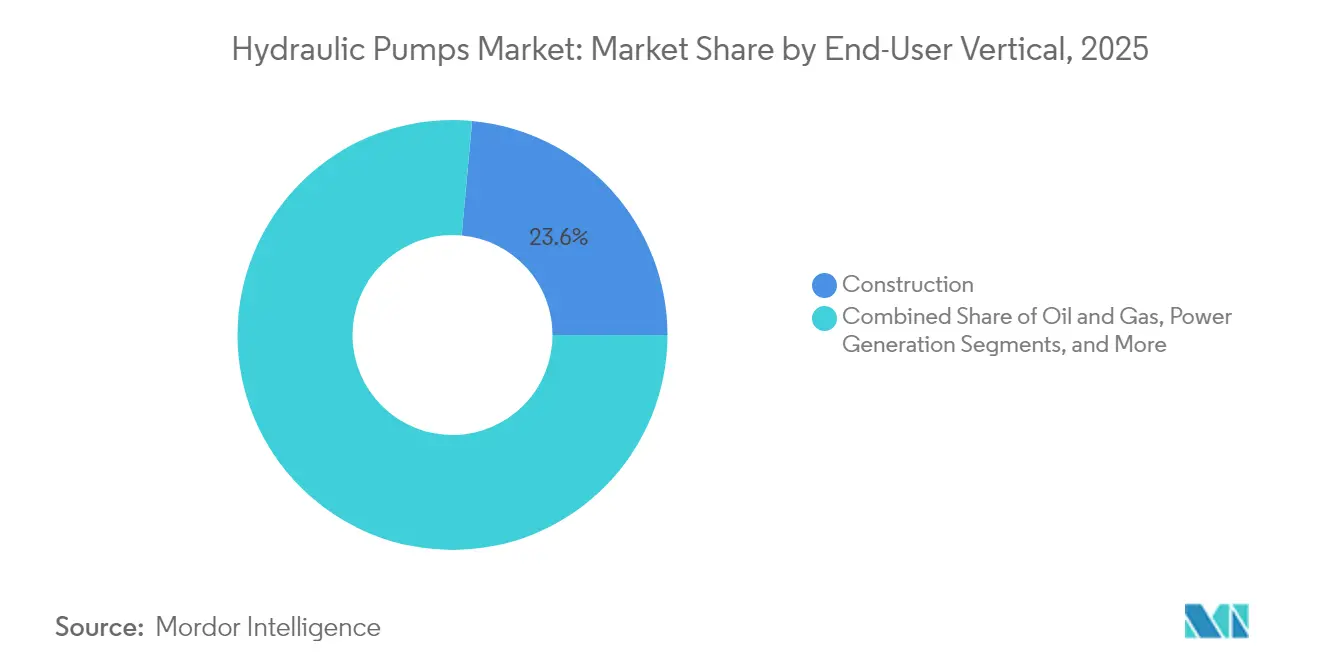

- By end-user vertical, Construction remained the largest with 23.55% share in 2025, while Power Generation is progressing at 6.85% CAGR.

- By geography, APAC dominated with 41.45% share in 2025; the Middle East is the fastest-growing region at 6.20% CAGR.

- Bosch Rexroth, Parker Hannifin, and Danfoss Power Solutions collectively held an estimated 28% of global revenue in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydraulic Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure renewal programs in China and India | +1.20% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Industrial automation (Industry 4.0 retrofits) | +0.90% | Global, concentrated in North America and EU | Long term (≥ 4 years) |

| Off-highway electrification needs electro-hydraulic pumps | +0.80% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Wind-turbine yaw and pitch system demand | +0.70% | Global, concentrated in offshore markets | Long term (≥ 4 years) |

| Hydrogen electrolyser build-out (>1000 bar pumps) | +0.60% | EU and North America, pilot projects in APAC | Long term (≥ 4 years) |

| Mandatory remanufacturing quotas (EU Circular Economy) | +0.40% | EU primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure renewal programs in China and India

Government-funded construction pipelines in both nations sustain annual demand for more than 13.5 million hydraulic pump units by 2025. Localization rules for public-sector projects incentivise joint ventures, channelling roughly USD 4.2 billion into high-tech pump production and accelerating domestic capability building. Regional contractors adopting Chinese equipment standards are extending the supply chain into the Middle East and Africa, broadening export prospects for APAC manufacturers. These programmes are expected to underpin baseline demand through 2027, particularly for units rated above 5000 psi. [2]Cybersecurity and Infrastructure Security Agency, “Osprey Pump Controller advisory,” cisa.gov

Industrial automation (Industry 4.0 retrofits)

Smart power units equipped with variable-frequency drives trim idle-time energy consumption by 25%. IoT gateways stream real-time data into predictive-maintenance platforms, cutting operating costs by 45% and reducing unplanned emissions events by 75%, as shown in UK water-utility trials with Sulzer controllers. Digital twin models enable remote optimisation that delivers 30% energy savings and 20% reduction in total cost of ownership. Cyber-security remains a rising concern following US CISA advisories on pump-controller vulnerabilities carrying CVSS scores up to 9.8.

Off-highway electrification needs electro-hydraulic pumps

Hybrid work machines require compact, high-flow electro hydrostatic units such as Moog’s EPU-G, which delivers 20-85 l/min at up to 345 bars while lowering system oil volume 90%. Construction-equipment makers embed these pumps within electric power-take-off drives to meet emissions targets without sacrificing load-handling performance. Demand is especially strong in aerial-lift and material-handling segments where precise, low-noise operation is mandatory.

Hydrogen electrolyser build-out (>1000 bar pumps)

Green-hydrogen projects across Europe and North America require multi-stage booster pumps fabricated from AISI 316 stainless steel and certified for ATEX zones. Flowrates and duty cycles demand piston designs that maintain volumetric efficiency above 92% at discharge pressures beyond 1000 bar. Suppliers offering service packages and remote-monitoring functions are securing long-term procurement contracts with electrolyser OEMs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile nickel-steel prices | -0.80% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Rapid penetration of all-electric actuators | -1.10% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Cyber-security risks in smart pumps | -0.30% | Global, concentrated in critical infrastructure | Short term (≤ 2 years) |

| Shortage of certified fluid-power technicians | -0.50% | Global, acute in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile nickel-steel prices

Nickel-bearing alloy costs climbed through late-2024 on renewed US infrastructure spending before receding, then rebounded in early-2025, compressing pump-maker margins and complicating inventory planning. High-pressure (>3000 psi) models suffer the most, as safety codes mandate premium steel grades. Chinese producers, reliant on imported high-grade alloy, face added currency risk and logistics surcharges.

Rapid penetration of all-electric actuators

Electric cylinders deliver 75–80% mechanical efficiency versus 40–55% for conventional hydraulics, in addition to leak-free operation and simplified maintenance. They gain fast ground in light-payload and precision-assembly lines, reducing addressable volume for smaller hydraulic units. Heavy-duty tasks still favour hydraulics for superior force density and thermal robustness, preserving market relevance in off-road and energy sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Piston pumps advance efficiency targets

Gear pumps retained 36.45% revenue share in 2025 on the strength of mobile-machinery demand. Piston pumps are outpacing at 6.45% CAGR to 2031 as OEMs migrate toward higher volumetric efficiency and precise displacement control. Parker Hannifin’s PV140 piston series recorded 14,000 operating hours between overhauls in Australian mining vehicles, illustrating lifecycle cost advantages. Vane and screw pumps continue serving niche applications requiring smooth flow or marine-grade reliability.

Second-generation piston designs use hardened spool valves and reinforced swash plates to extend mean-time-between-failure to 15,000 hours, doubling service life relative to legacy units. Their adoption in telehandlers, excavators, and injection-moulding machines underscores a systemic pivot toward energy optimisation and reduced CO₂ footprints. The hydraulic pumps market size for piston technology is expected to capture an incremental share in both industrial and renewable-energy installations.

By Operating-Pressure Range: >5000 psi segment accelerates

The 3000-5000 psi class represented 41.35% of global value in 2025, covering mainstream construction and agricultural rigs. Pumps rated above 5000 psi are growing 7.95% annually, propelled by hydrogen compression, offshore wind, and advanced machining centres. North Ridge Pumps’ multi-stage boosters, certified for ATEX zones, meet electrolyser developers’ need for continuous duty at 1000 bar. Below-3000-psi units maintain volume stability in cost-sensitive markets where performance thresholds remain modest.

Upstream innovation focuses on sealing systems and micro-finish surfaces to curb leakage at extreme pressures. Material-science breakthroughs in duplex stainless and nano-coatings aim to raise fatigue resistance, while real-time pressure-derating algorithms prevent catastrophic failures. These advances reinforce the hydraulic pumps market share held by high-pressure specialists amid energy-transition projects.

By End-user Vertical: Power Generation accelerates

Construction remained top of the table with 23.55% revenue in 2025, supported by megaproject pipelines across Asia, the Middle East, and the Americas. Power Generation is progressing at 6.85% CAGR, stemming from turbine, hydroelectric, and storage deployments. OEMs incorporate hydraulic tracking in utility-scale solar arrays to maximise irradiation capture, while hydro stations rely on variable-displacement pumps for governor systems. Oil and Gas, Food and Beverage, and Water and Wastewater retain steady baselines, demanding corrosion-resistant and sanitary-design pumps.Grid-modernisation incentives in the United States and Europe elevate funding for pumped-storage hydro and flexible peaking assets, each requiring rugged high-flow pumps. Manufacturers offering service-exchange programmes and remanufactured spares align with EU circular-economy directives, broadening lifecycle revenue.

By Application: Process and Energy segment leads growth

Mobile Hydraulics commanded 54.35% of the 2025 demand, covering earthmovers, tractors, and forklifts that underpin global construction and agriculture. The Process and Energy category is expanding 7.05% per year, driven by wind-turbine pitch systems and refinery modernisation programmes. Closed-loop hydraulic pitch drives in 600 kW turbines integrate bladder-accumulator energy storage, enabling smoother grid integration. Industrial-machinery users continue adopting smart power units that deploy condition monitoring to trim downtime by 30%.

The hydraulic pumps market size attached to Process and Energy is benefiting from ESG capital flows, which prioritise high-efficiency fluid-power circuits in renewable assets. Service providers bundling cloud-based analytics with field maintenance contracts are capturing premium margins. As electrolyser, carbon-capture, and biomass facilities proliferate, so does demand for specialised pumps able to withstand corrosive media and variable duty cycles.

Geography Analysis

APAC’s leadership derives from unmatched production scale and domestic consumption, with China alone purchasing 13.5 million units in 2025. Government programmes such as India’s Smart Cities Mission funnel capital into water-management, metro-rail, and affordable-housing projects requiring high-pressure hydraulic systems. Japanese suppliers continue to set benchmarks for reliability; Kawasaki’s K3VL axial piston line is frequently specified on premium excavators. Supply-chain disruptions and skilled-labour shortages encourage automation and regional diversification into Vietnam and Indonesia.

The Middle East’s swift growth rests on oil-and-gas reinvestment and renewable diversification agendas. Saudi Arabia’s Public Investment Fund channels billions into solar- and wind-farm construction, where hydraulic yaw and pitch drives underpin turbine uptime. UAE’s transmission grid upgrades import high-pressure pumps for substation cooling and seawater desalination. Joint-venture manufacturing in Dammam and Abu Dhabi shortens lead times and meets local-content mandates.

North America and Europe maintain technologically advanced fleets. The US Infrastructure Investment and Jobs Act revived civil works outlays, fuelling replacements across skid-steer loaders and pavers. EU regulations promoting circular-economy compliance create new remanufacturing revenue and elevate demand for eco-design pumps certified under EN ISO 14971. Both regions contend with an ageing technician workforce, prompting wider deployment of remote diagnostics to ease service bottlenecks.

Competitive Landscape

Global suppliers hold relatively balanced shares, yielding a moderately concentrated field. Bosch Rexroth lifted 2023 sales to EUR 7.6 billion after integrating HydraForce, reinforcing compact-hydraulics capacity and widening North American reach. Parker Hannifin posted USD 19.9 billion in fiscal-2024 revenue and reported a 25.2% EBITDA margin, leveraging aerospace and filtration divisions for cross-cycle resilience. Danfoss Power Solutions expanded its D1P pump family to 160 cc to target high-power excavators, emphasising modular electronics.[4]Danfoss Power Solutions, “D1P pump series expansion,” danfoss.com

R and D pipelines highlight electro hydrostatic pumps, noise-attenuation casings, and AI-driven fault detection. Patent filings for variable-swash-plate control algorithms grew 12% year-over-year, reflecting intensifying digital competition. Chinese entrants’ narrow quality gaps while maintaining low unit prices, prompting incumbents to focus on systems integration and aftermarket service bundles. Strategic alliances in hydrogen infrastructure and offshore wind offer new footholds for pump makers specialised in ultra-high-pressure and corrosion-resistant solutions.

Hydraulic Pumps Industry Leaders

-

Bosch Rexroth Ltd.

-

Parker Hannifin Corporation

-

Eaton Corporation plc

-

Danfoss Power Solutions A/S

-

Kawasaki Heavy Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bosch Rexroth announced a 7.5% sales lift to EUR 7.6 billion in 2023, and disclosed EUR 460 million R and D investment aimed at smart-hydraulics platforms.

- January 2025: Parker Hannifin reported Q2 FY 2025 sales of USD 4.7 billion and a 39% increase in net income to USD 949 million.

- October 2025: Ingersoll Rand acquired APSCO, Blutek, and UT Pumps for USD 135 million, adding USD 50 million to annual revenue.

- October 2025: Danfoss Power Solutions released a 160-cc D1P open-circuit pump for high-power mobile machinery.

Global Hydraulic Pumps Market Report Scope

Hydraulic pumps are devices that convert mechanical energy into hydraulic energy. These devices operate according to the displacement principle, which involves the existence of mechanically sealed chambers in the pump. These chambers transport fluid from the pump's inlet to the outlet.

The Hydraulic Pumps Market can be segmented by type (gear, vane, piston), end-user vertical (oil and gas, food and beverage, water and wastewater, power generation, construction, chemicals, and other end-user verticals (agriculture, automotive, mining, and others)), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle-East & Africa).

The market sizes and forecasts are in terms of value (USD million) for all the above segments.

| Gear |

| Vane |

| Piston |

| Screw |

| <3,000 psi |

| 3,000 - 5,000 psi |

| >5,000 psi |

| Construction |

| Oil and Gas |

| Power Generation |

| Food and Beverage |

| Water and Waste-water |

| Chemicals |

| Others (Agriculture, Mining, Automotive) |

| Mobile Hydraulics |

| Industrial Machinery |

| Process and Energy (incl. wind, hydro, hydrogen) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of Latin America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Pump Type | Gear | |

| Vane | ||

| Piston | ||

| Screw | ||

| By Operating-Pressure Range | <3,000 psi | |

| 3,000 - 5,000 psi | ||

| >5,000 psi | ||

| By End-user Vertical | Construction | |

| Oil and Gas | ||

| Power Generation | ||

| Food and Beverage | ||

| Water and Waste-water | ||

| Chemicals | ||

| Others (Agriculture, Mining, Automotive) | ||

| By Application | Mobile Hydraulics | |

| Industrial Machinery | ||

| Process and Energy (incl. wind, hydro, hydrogen) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of Latin America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hydraulic pumps market?

The hydraulic pumps market reached USD 14.64 billion in 2026 and is projected to grow to USD 18.99 billion by 2031 at a 5.35% CAGR.

Which pump type is growing fastest?

Piston pumps are expanding at a 6.45% CAGR thanks to superior efficiency and precision control that fit modern automation needs.

Which application area offers the highest growth potential?

Process and Energy, covering wind, hydrogen, and industrial process plants, is forecast to grow 7.05% annually through 2031.

Which region is poised for the highest CAGR?

The Middle East is the fastest-growing regional market, set to rise 6.20% per year due to large infrastructure and renewable-energy projects.

What key restraint could slow market growth?

Rapid adoption of all-electric actuators in light-duty precision applications may displace hydraulic solutions and reduce addressable demand.

Who are the leading companies in the hydraulic pumps industry?

Bosch Rexroth, Parker Hannifin, and Danfoss Power Solutions together hold an estimated 28% of global revenue, leveraging digital innovations to maintain share.

Page last updated on: