Gear Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.04 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 2.93% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gear Pumps Market Analysis by Mordor Intelligence

The gear pumps market size is expected to grow from USD 4.9 billion in 2025 to USD 5.04 billion in 2026 and is forecast to reach USD 5.82 billion by 2031 at 2.93% CAGR over 2026-2031. This growth indicates a mature yet resilient market that continues to benefit from essential industrial demand even as energy-efficiency rules and specialty alloy shortages introduce headwinds. Strong capital spending in the upstream oil and gas sector, rapid petrochemical build-outs in the Asia-Pacific region, and the adoption of modular hydraulics in mobile machinery underpin steady order inflows. Simultaneously, product development centers on low-noise, variable-displacement systems that complement electrified off-highway equipment and comply with sustainability mandates. Ongoing shifts toward bio-based hydraulic fluids also drive innovation in materials for seals, bearings, and coatings, aiming to preserve performance while supporting environmental goals.

Key Report Takeaways

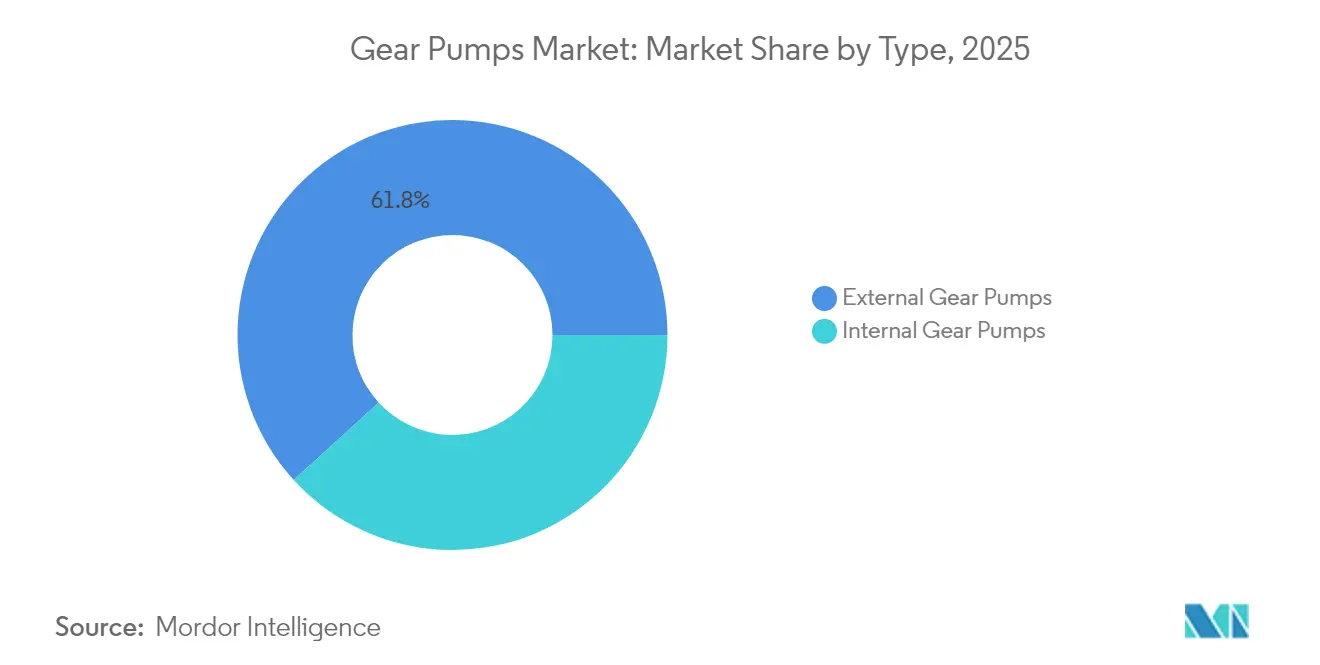

- By type, external gear pumps accounted for 61.78% of the gear pump market share in 2025, while Internal Gear Pumps are projected to rise at a 4.55% CAGR.

- By displacement, fixed displacement accounted for 71.45% of the gear pump market share in 2025, while variable displacement units are forecast to expand at a 4.39% CAGR through 2031.

- By material, cast iron captured 50.88% of revenue in 2025, while stainless steel is projected to rise at a 4.01% CAGR.

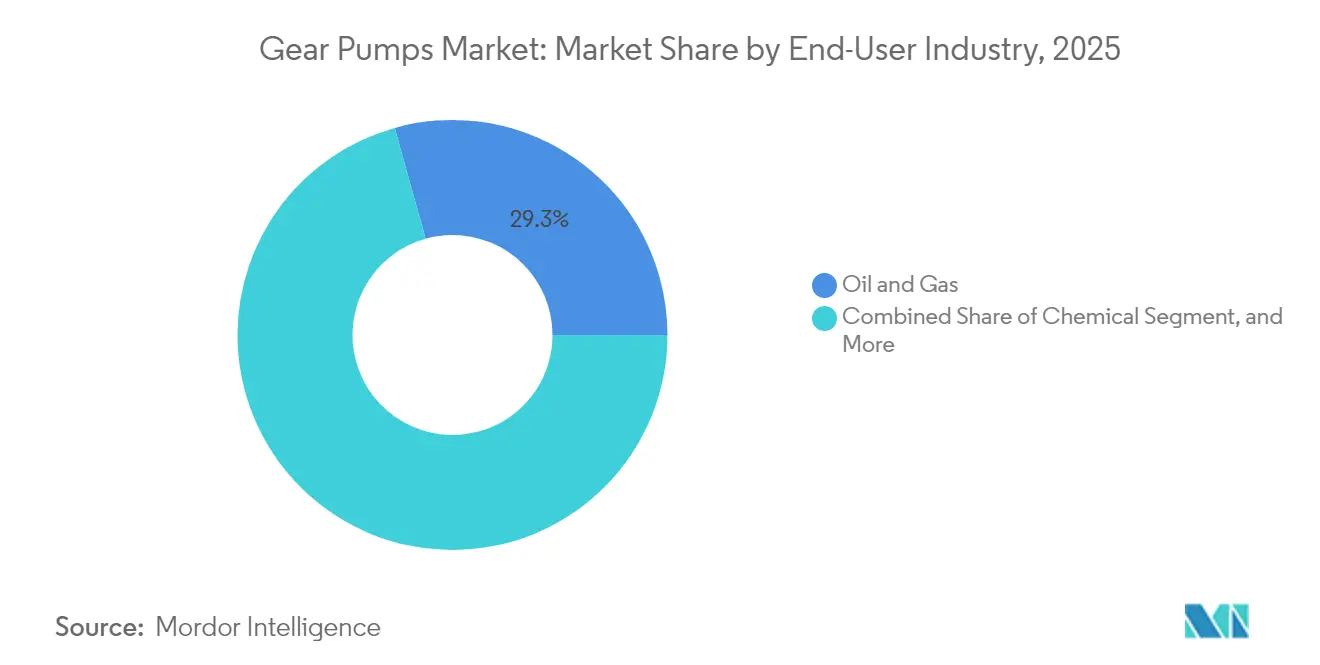

- By end-user, the oil and gas sector accounted for 29.33% of the gear pumps market size in 2025, while the pharmaceuticals sector recorded the highest growth at a 3.34% CAGR.

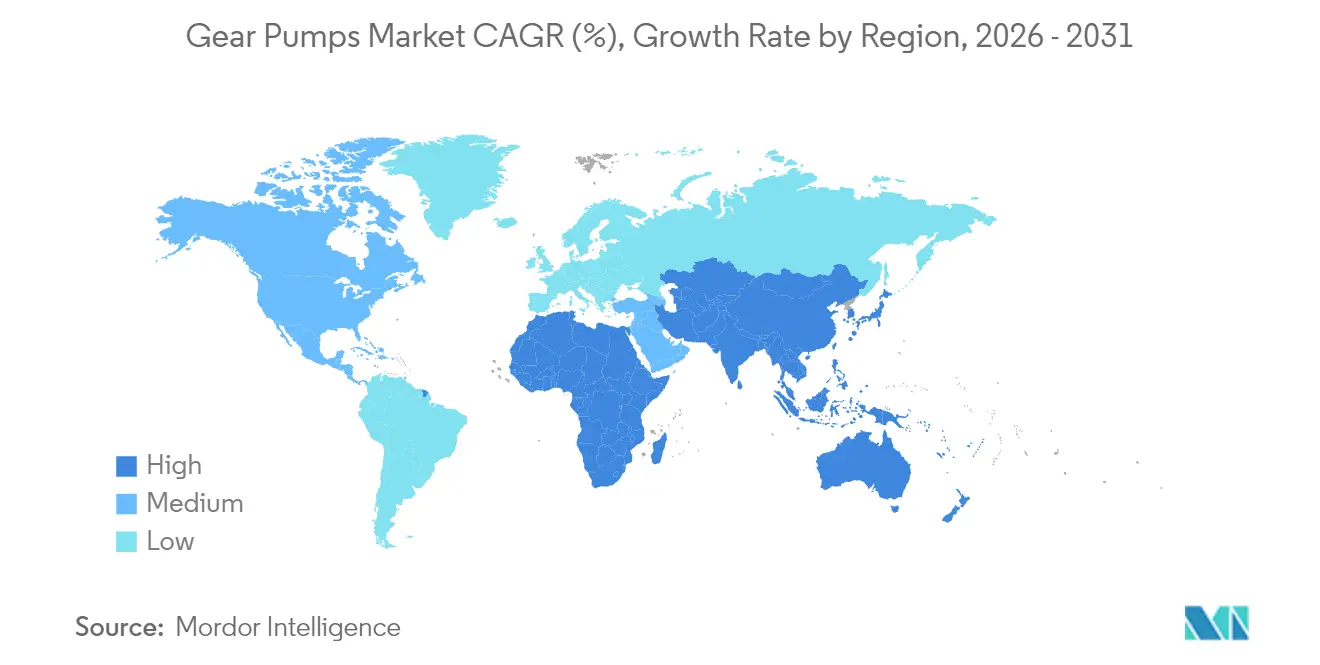

- By geography, the Asia-Pacific region led with a 35.29% revenue share in 2025, whereas the Middle East posted the fastest regional CAGR at 3.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gear Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand from oil and gas upstream projects | +0.8% | North America, Middle East, offshore basins | Medium term (2-4 years) |

| Rapid capacity expansion in petrochemical complexes | +0.6% | Asia-Pacific core, spill-over to Middle East and North America | Long term (≥ 4 years) |

| Shift toward modular hydraulic systems in mobile machinery | +0.4% | Europe and North America leading, global spread | Short term (≤ 2 years) |

| Electrification of off-highway equipment requires silent hydraulic sources | +0.3% | Europe and North America front-runner, Asia-Pacific following | Medium term (2-4 years) |

| Smart factory adoption driving predictive-maintenance retrofit pumps | +0.2% | Developed manufacturing regions worldwide | Long term (≥ 4 years) |

| Transition to bio-based hydraulic fluids necessitates compatible gear pumps | +0.2% | Europe leadership, global adoption later | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand from Oil and Gas Upstream Projects

Rebounding capital spending across unconventional shale and offshore plays is driving orders for high-pressure external gear pumps that can withstand abrasive drilling muds and aggressive fracturing fluids. Floating production, storage, and offloading vessels rely on robust hydraulic packages, which maintain high reliability requirements.[1]Schlumberger, “Technology and Innovation Report,” slb.com Drillers specify advanced surface treatments and tighter tolerances to prolong service life in corrosive, high-temperature wells, driving continued design upgrades.

Rapid Capacity Expansion in Petrochemical Complexes

Asia-Pacific’s multi-billion-dollar cracker and polymer projects dominate global capacity additions, each requiring hundreds of specialty gear pumps for catalyst circulation, polymer transfer, and metering duties.[2]China Petroleum and Chemical Industry Federation, “Industry Development Report 2024,” cpcia.org.cn Local content policies in China and preferential financing in the Middle East further stimulate demand, while U.S. Gulf Coast debottlenecking secures a secondary growth stream.

Shift Toward Modular Hydraulic Systems in Mobile Machinery

Agricultural and construction OEMs now build equipment around standardized hydraulic modules that simplify maintenance, cut inventory, and shorten model changeovers. Interchangeable gear pumps slot into these modules, boosting volume repeatability and lowering unit cost. Deere’s latest tractor family leverages this architecture to streamline assembly and field service.[3]Deere and Company, “Annual Report 2024,” deere.com

Electrification of Off-Highway Equipment Requires Silent Hydraulic Sources

Electric excavators, loaders, and drills need quiet, energy-efficient hydraulics to preserve overall acoustic and efficiency benefits. New helical-tooth external gear pumps, paired with vibration-damped housings, reduce noise to below 70 dB while limiting parasitic losses that drain battery packs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in industrial capex cycles | -0.5% | Global, peaked in cyclical resource segments | Short term (≤ 2 years) |

| Growing penetration of screw and vane pumps in high-viscosity duties | -0.3% | Chemical and food processing hubs worldwide | Medium term (2-4 years) |

| Price sensitivity in commodity end-markets | -0.2% | Emerging regions and small-scale fabricators | Short term (≤ 2 years) |

| Compliance costs linked to tightening efficiency standards | -0.1% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Industrial Capex Cycles

Boom-and-bust investment patterns in energy, mining, and chemicals result in uneven project backlogs, which tax production planning and cash-flow management. Inflationary raw material spikes and lengthening lead times add further uncertainty, prompting suppliers to hold larger inventories and offer more flexible delivery schedules.

Growing Penetration of Screw and Vane Pumps in High-Viscosity Duties

Alternative rotary technologies are gaining market share in viscous media due to their smoother flow, lower shear, and broader controllability. Progressive cavity designs supply chocolate, resins, and slurries more gently, eroding legacy gear pump positions in the specialty food and chemical industries. Gear pump makers respond with niche formulations and variable displacement designs to defend incumbency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: External Gear Pumps Dominate Industrial Applications

External gear pumps accounted for 61.78% of the gear pumps market in 2025, reflecting superior pressure capability above 3,000 psi and robust tolerance of contaminated fluids. Fixed-tooth geometry simplifies machining and lowers service costs, sustaining dominance in drilling, fracturing, and heavy manufacturing. Internal gear pumps, although smaller in share, advance at a 4.55% CAGR due to their higher volumetric efficiency and quiet, pulse-free delivery. The gear pumps market size for internal variants is set to widen as food, pharma, and fine-chemical operators demand sanitary, low-noise performance.

Pharmaceutical facilities are increasingly specifying crevice-free internal designs in 316L stainless steel to comply with hygiene regulations. Parker Hannifin’s FDA-compliant series exemplifies this pivot, pairing magnetic drives with polished internals for CIP-compatible transfer duties. External units retain primacy in the oil and gas industry, where rugged metallurgy and field-service familiarity often trump noise or efficiency. Aerospace OEMs, however, are exploring compact internal pumps to reduce weight and power draw in next-generation flight control systems.

By Material: Cast Iron Leads Despite Stainless Steel Growth

Cast iron accounted for 50.88% of 2025 revenue due to its low cost, proven machinability, and ample mechanical strength in non-corrosive applications. The gear pumps market size derived from cast iron applications spans industrial hydraulics, drilling mud circulation, and general factory service. Stainless steel, projected to grow at a 4.01% annual rate, is capturing adoption across bioprocess, dairy, and specialty chemicals, where corrosion or hygiene drives total cost of ownership. Duplex alloys are gaining a foothold in offshore topside packages, striking a balance between resistance and price.

Material upgrades track stricter validation demands, especially FDA 21 CFR Part 11 electronic record requirements that favor stainless units to reduce cleaning protocol complexity. Cast iron’s share endures in rugged mobile machines, where abrasion and impact, not corrosion, govern lifecycle economics. Hybrid assemblies that combine cast iron housings with stainless gears offer a compromise for mid-tier chemical plants pursuing incremental upgrades.

By End-User Industry: Oil and Gas Leads Amid Diversification

Oil and gas contributed 29.33% of gear pumps market share in 2025, spanning upstream blow-out preventer hydraulics, midstream pipeline boosters, and downstream lube skids. However, pharma emerges as the fastest-expanding customer vertical, with a 3.34% CAGR through 2031, as global biologics and vaccine capacity scales. Food and beverage processors similarly pivot to hygienic gear units to move sugars, syrups, and dairy concentrates without foaming or contamination.

Biopharma single-use reactors rely on low-shear pumps that integrate gamma-irradiated disposable wet ends to safeguard sterility. Chemical plants remain a large installed base, yet many lines now favor screw pumps for viscous monomers, requiring gear pump suppliers to reposition toward catalyst injection and utility tasks. Power generation maintains a steady demand for lubrication oil and fuel handling circuits in combined-cycle and nuclear power stations.

By Displacement: Fixed Displacement Dominates with Variable Gaining Ground

Fixed displacement models accounted for 71.45% of the 2025 turnover, prized for their simplicity, reliability, and ease of troubleshooting. Nevertheless, energy-focused regulations push OEMs toward variable displacement units that modulate flow on demand, supporting a 4.39% CAGR. The gear pumps market size tied to variable technology is buoyed by smart electronics that link pump output to telematics, trimming idle losses in excavators and harvesters.

Caterpillar’s latest excavators feature load-sensing variable displacement pumps, which reduce fuel consumption by 15% compared to legacy fixed designs. Factory automation platforms integrate servo-controlled gear pumps that sync with PLCs, balancing inertia with speed to save kilowatt-hours and lower Scope 2 emissions. Fixed pumps still dominate small skid-steer loaders and shop presses where ruggedness outweighs efficiency.

Geography Analysis

Asia-Pacific’s 35.29% share underscores its role as the center of gravity for petrochemical, electronics, and heavy equipment manufacturing. Large-scale projects in China’s coastal industrial zones and India’s new dedicated freight corridors underpin a steady pipeline of hydraulic installations. Southeast Asian nations attract factory relocations from higher-cost locales, further expanding the installed base of smaller gear pumps. Government incentives for clean energy, including solar wafer fabs and battery plants, introduce new hygienic and chemical-resistant pump requirements.

The Middle East is projected to record a 3.41% CAGR, driven by USD 20 billion in petrochemical investments under Saudi Vision 2030, which will demand corrosion-resistant gear pumps for ethylene, polyethylene, and specialty chemical units. The UAE aims to establish itself as a regional manufacturing hub, commissioning aluminum, steel, and modular housing factories that utilize decentralized hydraulic networks. Qatar’s harbor expansions and industrial cities require robust construction machinery equipped with high-pressure external pumps.

North America and Europe remain mature yet innovative. U.S. shale drillers order abrasion-tolerant pumping packages while embracing predictive maintenance sensors that feed real-time data to cloud platforms. European regulations on noise and efficiency are pushing OEMs toward variable, low-decibel designs, thereby bolstering R&D. Germany’s machine builders are embedding smart gear pumps into automated lines, aligning with the country’s Industry 4.0 blueprint.

Competitive Landscape

The gear pumps market exhibits moderate concentration as global players pursue scale and technology leadership through acquisitions. Bosch Rexroth’s EUR 1.2 billion (USD 1.3 billion) purchase of Hawe Hydraulik extends its mobile hydraulics reach, exemplifying the strategic imperative to control a full systems portfolio. Parker Hannifin and Eaton deploy integrated electronics and IoT-ready sensors to differentiate on performance monitoring and predictive uptime.

Digital transformation shapes competition: embedded vibration sensors, edge analytics, and cloud dashboards convert pumps from commodity components to data-rich assets. Vendors invest in additive manufacturing to speed prototype cycles and in wear-resistant surface coatings for bio-fluid compatibility. Niche entrants target biopharma and aerospace, where stringent quality factors allow premium pricing and protect against volume-driven rivalry. Meanwhile, large incumbents partner with lubricant formulators to validate seal materials for bio-based fluids, locking in future compatibility contracts.

The fragmentation index sits in the mid-range as top suppliers hold notable but not dominant shares across diverse end-markets. Continuous consolidation is expected as regional specialists seek global distribution while majors plug product gaps and secure local content credentials in emerging clusters.

Gear Pumps Industry Leaders

Bosch Rexroth AG

Parker-Hannifin Corporation

Hydac International GmbH

Viking Pump, Inc.

IDEX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kawasaki Precision Machinery unveiled its Smart Pump line at Bauma 2025. The pumps use non-contact swash-angle sensors and proprietary controllers that can switch among pressure-cutoff, torque-limit, and displacement-control modes. Real-time torque data comes straight from the motor, so contractors no longer need external torque meters when setting up construction equipment.

- March 2025: Eaton began distributing Bezares variable-flow gear pumps with load-sensing technology in 95, 110, and 130 cc/rev sizes. Each pump delivers maximum flow until system pressure reaches the compensator setting, then automatically de-strokes to supply only what the circuit needs—an approach that can trim energy use by up to 15% for agricultural, forestry, and waste-collection machinery.

- April 2025: Hydraulic Technologies released its PE60 Series hydraulic pump. The new model offers an autocycle function for continuous torque applications, a modular platform that accepts a broad mix of valves and controls without custom factory work, and ergonomic hand controls with optional LCD displays for digital pressure readouts and diagnostics.

- January 2025: Moog introduced the EPU-G electrohydrostatic pump unit, pairing a four-quadrant internal gear pump with a high-dynamic servomotor. Designed for flows of 20-85 L/min and pressures up to 345 bar, the compact module can cut hydraulic oil volume by up to 90% and features an axial manifold interface for direct mounting—helping industrial users meet sustainability targets while saving space.

Global Gear Pumps Market Report Scope

A gear pump is a type of positive displacement pump. It transfers a fluid by continually enclosing a defined volume with interlocking cogs or gears and mechanically transferring it via a cyclic pumping motion. It produces a smooth, pulse-free flow that is proportionate to the rotational speed of its gears.

The Gear Pumps Market Report is Segmented by Type (External Gear Pumps, and Internal Gear Pumps), Material (Cast Iron, Stainless Steel, and More), End-User Industry (Oil and Gas, Chemical, Pharmaceutical, and More), Displacement (Fixed Displacement, and Variable Displacement), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| External Gear Pumps |

| Internal Gear Pumps |

| Cast Iron |

| Stainless Steel |

| Other Materials |

| Oil and Gas |

| Chemical |

| Food and Beverage |

| Pharmaceutical |

| Power Generation |

| Other End-User Industries |

| Fixed Displacement |

| Variable Displacement |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Type | External Gear Pumps | ||

| Internal Gear Pumps | |||

| By Material | Cast Iron | ||

| Stainless Steel | |||

| Other Materials | |||

| By End-User Industry | Oil and Gas | ||

| Chemical | |||

| Food and Beverage | |||

| Pharmaceutical | |||

| Power Generation | |||

| Other End-User Industries | |||

| By Displacement | Fixed Displacement | ||

| Variable Displacement | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the gear pumps market in 2026?

The market is valued at USD 5.04 billion in 2026 with a projected 2.93% CAGR to 2031.

Which segment holds the highest gear pumps market share today?

External gear pumps lead with 61.78% revenue share in 2025.

What drives faster growth in stainless steel gear pumps?

Rising pharmaceutical and food processing demand for corrosion-resistant, hygienic pumping solutions is lifting stainless steel sales at a 4.01% CAGR.

Why are variable displacement gear pumps gaining popularity?

Energy-efficiency mandates and the need for precise flow control in mobile and industrial equipment boost adoption, supporting a 4.39% CAGR through 2031.

Which region is the fastest growing for gear pumps?

The Middle East shows the highest regional growth at a 3.41% CAGR, supported by massive petrochemical investments and diversification programs.

How are gear pump makers addressing the shift to bio-based hydraulic fluids?

Manufacturers develop compatible seals and coatings, validate materials with lubricant suppliers, and launch product lines expressly certified for bio-fluid use.

Page last updated on: