Precision-Guided Munition Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

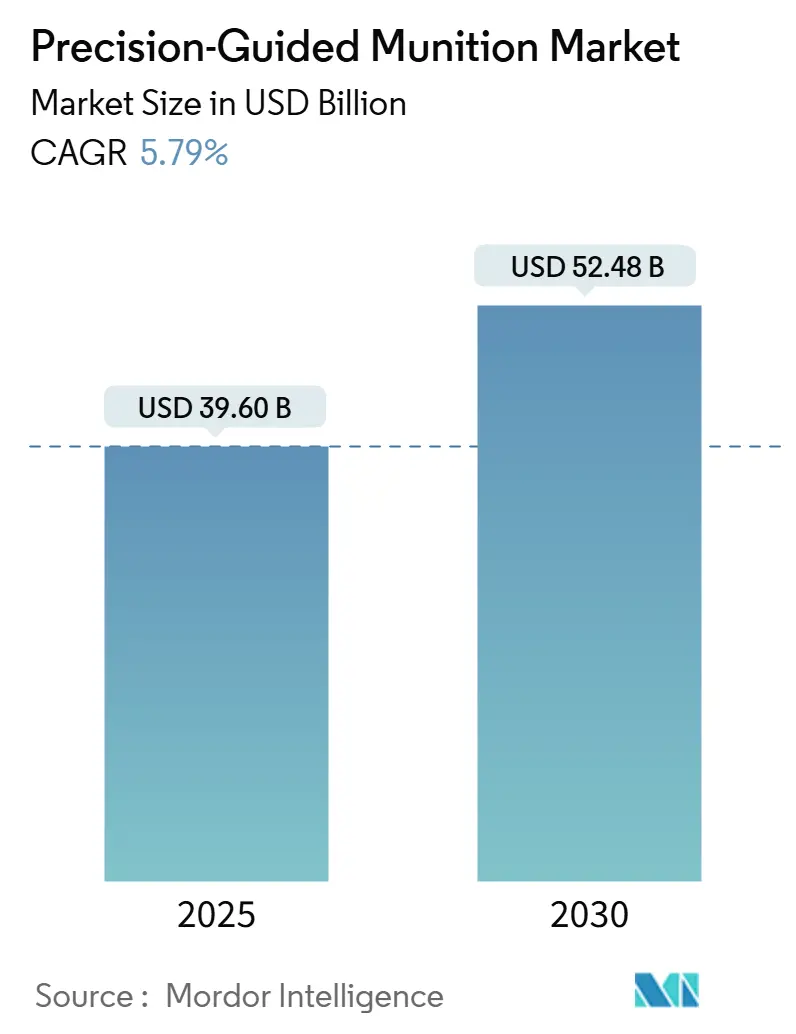

| Market Size (2025) | USD 39.60 Billion |

| Market Size (2030) | USD 52.48 Billion |

| Growth Rate (2025 - 2030) | 5.79% CAGR |

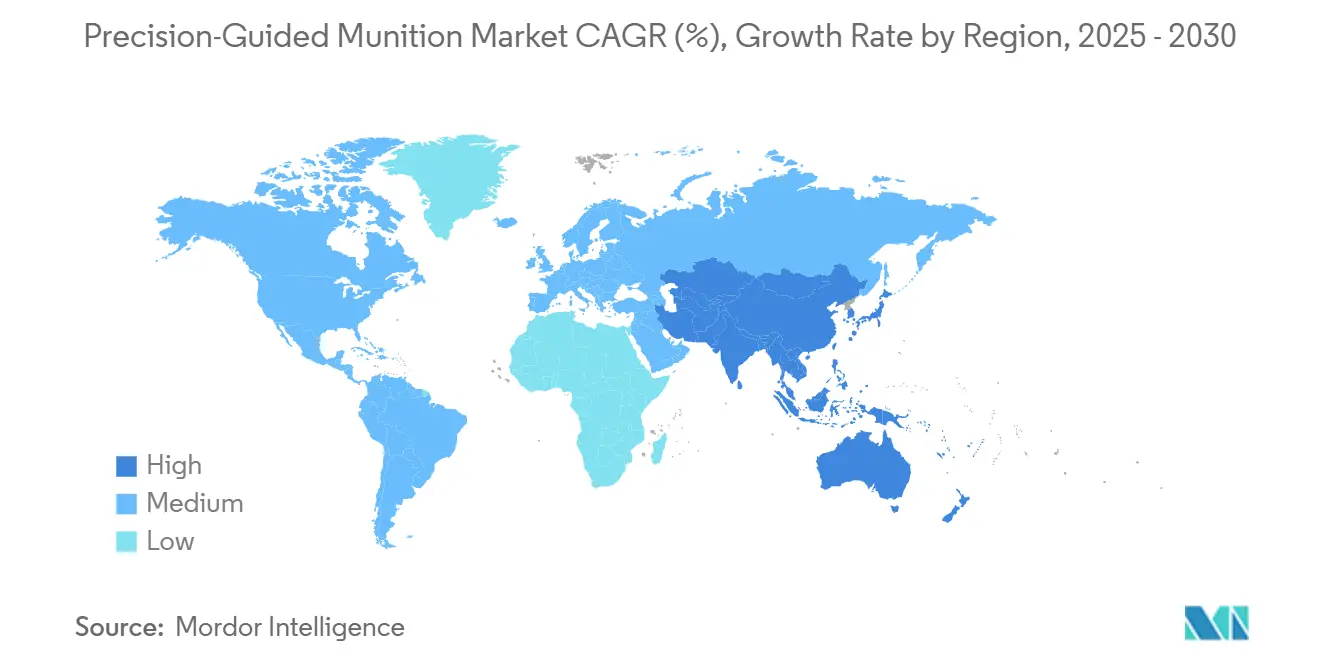

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision-Guided Munition Market Analysis by Mordor Intelligence

The precision-guided munition market size was USD 39.6 billion in 2025 and is projected to reach USD 52.48 billion by 2030, growing at a 5.79% CAGR. Defense ministries prioritize stand-off strike capabilities to counter anti-access/area-denial (A2/AD) networks, stimulate domestic production, and cut collateral damage in asymmetric conflicts. Multi-year procurement contracts, such as the US Army’s USD 4.94 billion Precision Strike Missile award, underpin a robust order pipeline. Miniaturization opens up new deployment options for unmanned aerial vehicles (UAVs), while modular, open-systems architectures shorten upgrade cycles and reduce life-cycle costs. Industrial capacity constraints and semiconductor shortages continue to be a brake on output, but investments in digital manufacturing and predictive analytics are gradually easing these bottlenecks.

Key Report Takeaways

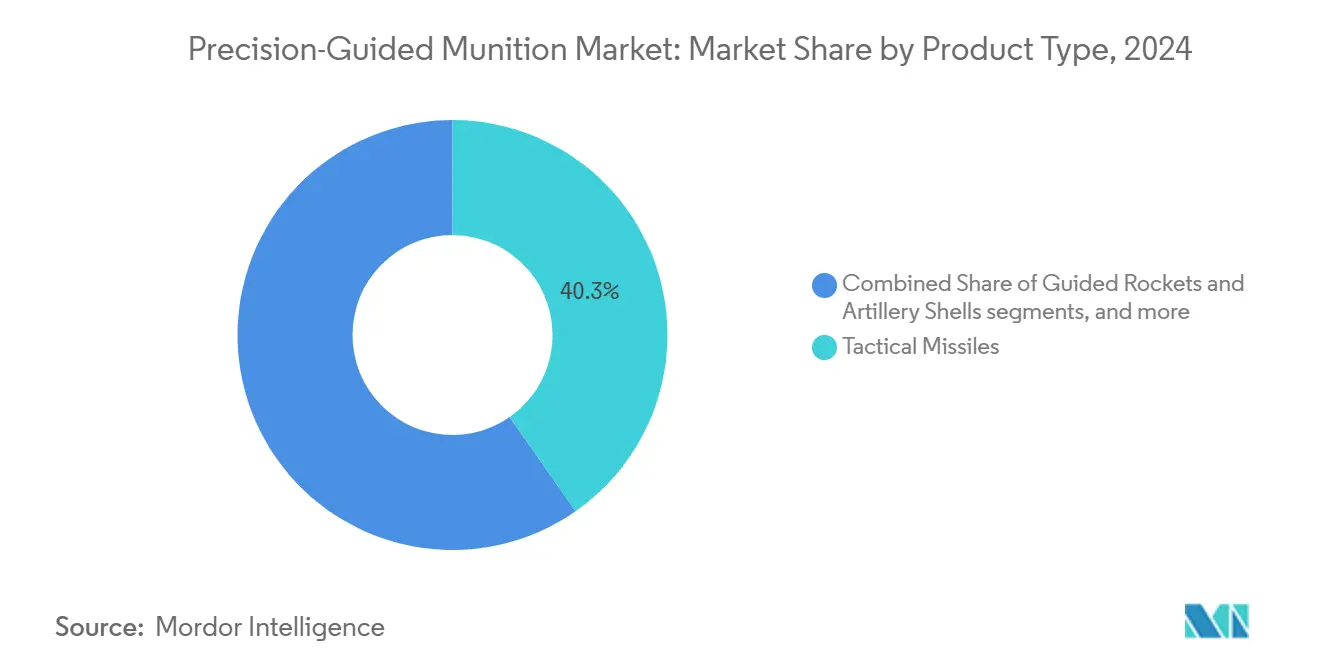

- By product type, tactical missiles led the precision-guided munition market, accounting for 40.31% of the market share in 2024. In contrast, loitering munitions are projected to expand at a 7.56% CAGR from 2025 to 2030, the fastest among all products.

- By launch platform, airborne systems accounted for 42.87% of the precision-guided munition market in 2024, maintaining their leadership position due to integrations with fighter and bomber aircraft. Unmanned systems are expected to post the highest 9.5% CAGR through 2030, as smaller UAV classes receive precision payloads.

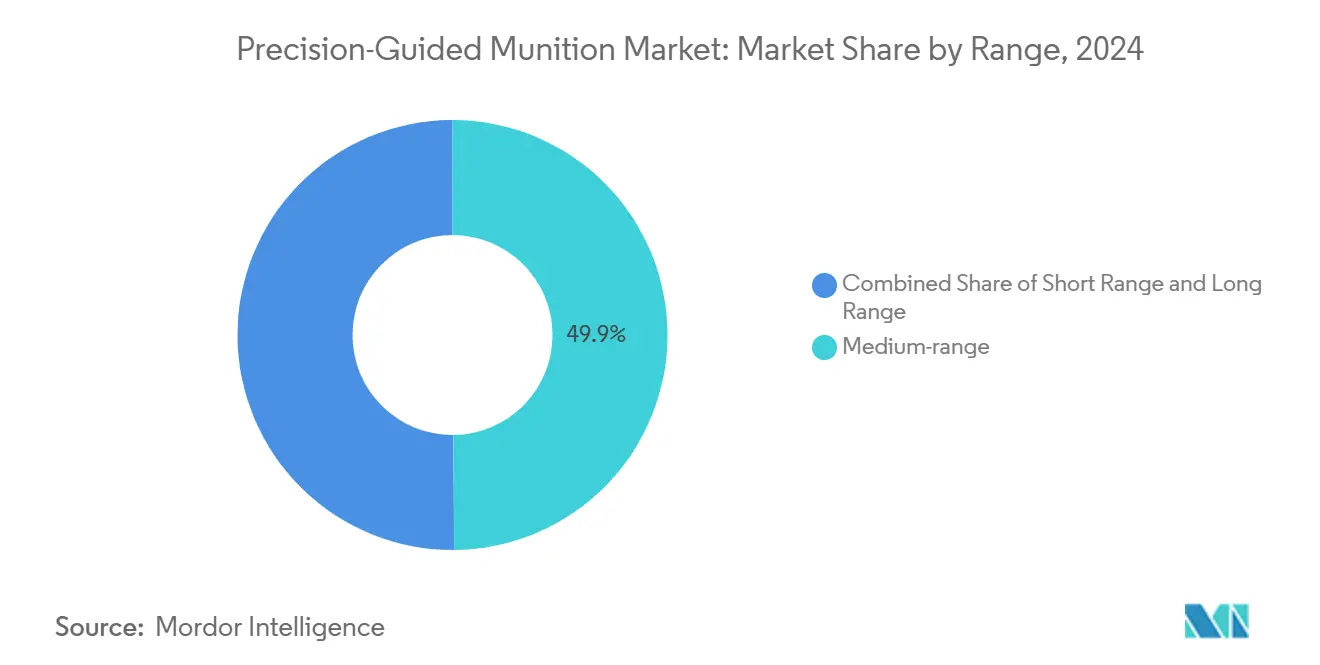

- By range, medium-range weapons (50 to 300 km) captured 49.87% revenue in 2024, topping the range category, while long-range weapons (greater than 300 km) represent the fastest-growing slot at an 8.43% CAGR through 2030.

- By speed, supersonic systems held 43.27% share in 2024, the largest within the speed segmentation, while hypersonic systems are forecasted to record a 10.29% CAGR, the quickest across all speed classes.

- By sub-system, guidance and navigation units delivered 38.31% of 2024 revenue, topping sub-system contributions, while target-acquisition modules will show the sharpest 6.21% CAGR to 2030 as artificial intelligence (AI) enhances seeker performance.

- By geography, North America commanded 39.92% of the revenue in 2024, remaining the largest regional buyer. The Asia-Pacific region is on track for the fastest growth, with a 6.82% CAGR, thanks to rapid force modernization programs.

Global Precision-Guided Munition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising asymmetric warfare and need for surgical strikes | + 1.20% | Global; early adoption in Ukraine, Middle East, Asia-Pacific | Medium term (2-4 years) |

| DoD modernization programs in US and allies | + 1.80% | North America and Europe; spill-over to AUKUS partners | Long term (≥ 4 years) |

| Growing demand for stand-off weapons in contested A2/AD zones | + 1.50% | Asia-Pacific core; Middle East spill-over | Medium term (2-4 years) |

| Miniaturization enabling deployment on UAVs and loitering munitions | + 0.90% | Global | Short term (≤ 2 years) |

| AI-enabled target recognition improving hit-to-kill probability | + 0.70% | North America, Europe, advanced Asia-Pacific markets | Medium term (2-4 years) |

| Emergence of low-cost glide kits for legacy bombs | + 0.60% | Global, especially emerging defense buyers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Asymmetric Warfare and Demand for Surgical Strikes

Precision weapons with sub-10 m circular error probabilities allow commanders to neutralize high-value targets hidden in urban terrain while limiting collateral damage. Ukraine’s battlefield experience has underscored the operational pay-off, forcing major powers and smaller states alike to stockpile comparable capabilities.[1]US Department of Defense, “Contracts for March 31 2025,” defense.gov The heightened lethality of non-state actors equipped with accurate rockets pushes regional militaries to invest in offensive precision assets and layered missile defenses. As a result, procurement budgets increasingly favor guided over unguided rounds, compressing the logistical footprint of sustained operations. The trend is expected to strengthen as urbanization and media scrutiny amplify the strategic cost of civilian casualties. Continued integration of dual-mode seekers ensures reliability when GPS is jammed, further widening the capability gap versus legacy ordnance.

DoD and Allied Modernization Programs

The US Army’s Precision Strike Missile, the Navy’s SM-6 multi-mission round, and allied programs, such as Germany’s Taurus Neo, collectively represent the most significant investment in guided munitions since the Cold War. Modular open-systems standards enhance upgrade agility, enabling electronics refreshes without scrapping airframes or launchers. Interoperability initiatives under NATO Standardization Agreements create bulk-buy economies and reduce per-unit prices for consortium members. However, congressional testimony highlights industrial base limitations, compelling primes to adopt digital twins and additive manufacturing to increase throughput.[2]Congressional Research Service, “Defense Primer: US Precision-Guided Munitions,” everycrsreport.com Parallel investments by Japan and Australia in domestic lines improve supply security and diversify the vendor pool. These synchronized roadmaps provide a stable, multi-year demand horizon that cushions suppliers against cyclical budget swings.

Growing Demand for Stand-Off Weapons in Contested A2/AD Zones

Anti-ship ballistic missiles, long-range surface-to-air systems, and over-the-horizon radars fielded by peer competitors force strike platforms to launch from beyond 400 km. Weapons such as the Joint Air-to-Surface Standoff Missile-Extended Range provide crews with the necessary reach while maintaining precision, a capability highly valued by Japan, Australia, and the Philippines.[3]Federation of American Scientists, “Missile Technology Control Regime Texts,” fas.org Satellite-based sensors now cue land-attack missiles in near real time, improving time-on-target performance. Regional air forces are upgrading tanker fleets to extend loiter windows for long-range shooters, further elevating demand for standoff ordnance. Procurement transparency laws in several Asia-Pacific democracies are accelerating competitive tenders, lowering barriers for non-traditional suppliers to gain footholds. Over the forecast period, long-range weapons are expected to capture budget share from medium-range incumbents steadily.

Miniaturization Enabling UAV and Loitering Deployments

New micro-electromechanical (MEMS) inertial units, compact power modules, and lightweight composite casings allow precision effects in warheads weighing under 10 lbs. Small UAVs equipped with multi-drop racks now deliver pinpoint strikes at a fraction of the cost of legacy sorties. European armed forces are fast-tracking loitering systems as a direct result of the Russia-Ukraine conflict; domestic suppliers benefit from less onerous airworthiness certification rules, as the platforms are classified as munitions rather than aircraft. Multi-mode guidance, combining GNSS, inertial, and optical seekers, mitigates jamming risk, thereby increasing mission assurance in electromagnetically contested airspace. Looking ahead, swarming software should multiply the volume of simultaneous strikes without proportionate increases in operator load. The cost-effectiveness makes loitering systems attractive for major powers and budget-constrained buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control regimes (ITAR, MTCR) limiting addressable market | −0.8% | Global; strongest effect on US-allied trade | Long term (≥ 4 years) |

| Counter-UAS and EW systems degrading GPS guidance | −1.1% | Global; concentrated in contested theaters | Medium term (2-4 years) |

| Escalating unit costs versus unguided ordnance | −0.6% | Global; budget-constrained militaries most affected | Medium term (2-4 years) |

| Semiconductor supply-chain fragility impacting guidance units | −0.7% | Global; acute for advanced guidance-electronics producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Export-Control Regimes (ITAR, MTCR) Limiting Addressable Market

International Traffic in Arms Regulations impose registration fees, compliance programs, and hefty civil penalties that deter small exporters and slow multinational sales campaigns.[4]US Department of State, “International Traffic in Arms Regulations,” state.gov The Missile Technology Control Regime (MTCR) thresholds block transfers of systems that can deliver payloads of 500 kg or more beyond 300 km, directly affecting strategic-range precision munitions. Several European governments are responding with sovereign development roadmaps to cut reliance on US export approvals. While category transfers from ITAR to Commerce rules have eased small-arms exports, precision-guided categories remain tightly controlled because of their strategic implications. Lengthy licensing lead times complicate just-in-time production schedules, often forcing primes to build speculative batches in advance, tying up working capital.

Counter-UAS and Electronic-Warfare Systems Degrading GPS Guidance

Adversaries increasingly field jammers and spoofers that target civilian L1 and military M-code GPS bands, compelling missile designers to embed redundant guidance modes. Cross-linked inertial sensors, terrain-following algorithms, and imaging infrared seekers mitigate, but do not eliminate, denial risks. The democratization of low-cost electronic warfare (EW) kits means that even non-state actors can erode the precision edge previously monopolized by great-power militaries. Counter-UAS laser and microwave systems also challenge small loitering munitions, raising survivability thresholds. Upgrading entire inventories with hardened receivers involves substantial retrofit budgets, which can delay adoption in fiscally constrained forces. Over the medium term, guidance-agnostic kill chains integrating multiple sensor modalities will be required to sustain accuracy in electromagnetic gray zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Loitering Systems Drive Innovation

Tactical missiles generated 40.31% of 2024 revenue, underpinning the most significant slice of the precision-guided munition market share. Their entrenched position stems from mature supply chains and established operator training pipelines across more than 50 nations. Yet the cost-per-kill advantage of loitering systems is reshaping budget allocations, allowing commanders to hover above targets until identification is confirmed. Historical data show tactical missiles advancing at a 6.2% CAGR between 2019 and 2024; growth moderates to 5.8% through 2030 as the segment matures. Guided bombs benefit from retrofit kits that upgrade legacy stocks, while hypersonic missiles, although smaller in volume, siphon away R&D funding due to their strategic deterrence value.

Loitering munitions are forecast to grow at a 7.56% CAGR, the fastest within the precision-guided munition market, as European and Middle Eastern customers adopt Ukrainian concepts of operation. Their unit cost undercuts cruise missiles by an order of magnitude, widening their applicability from high-value to time-sensitive targets. Therefore, the precision-guided munition market size for loitering munitions is expected to rise significantly from its low base in 2024. Proprietary data links highlight the expansion of domestic production in Germany and Türkiye, improving supply resilience. Suppliers are focusing on multi-drop dispensers and auto-swarm logic to cement competitive differentiation.

By Launch Platform: Unmanned Systems Transform Deployment

Airborne launchers, such as fighters, bombers, and rotary platforms, accounted for 42.87% of the revenue in 2024, bolstered by fleets of F-35, Rafale, and Su-30 aircraft that carry precision racks as standard. Continuous software drops under open-mission-system standards enable rapid weapons integration without costly avionics upgrades. However, growing operator reluctance to risk pilots in high-end fights is shifting attention toward unmanned combat aerial vehicles. The airborne segment’s 2025-2030 CAGR is forecasted at 4.3%, signaling stable yet slowing expansion as other platforms steal incremental share.

Unmanned launchers, such as fixed-wing MALE UAVs and rotary mini-drones, will record a 9.50% CAGR, the steepest among platforms, as shrinking guidance modules make sub-25 kg class drones viable shooters. The precision-guided munition market size for unmanned platforms is projected to surpass USD 9 billion by 2030. Containerized ground-control stations and improved SATCOM links enable expeditionary deployment with minimal logistical footprint. Modularity allows quick role changes from surveillance to strike, reinforcing the case for high-tempo operations in contested airspace.

By Sub-System: Target Acquisition Drives Growth

Guidance, navigation, and control electronics accounted for 38.31% of 2024 revenue, underscoring their indispensability in achieving hit-to-kill performance; the unit value of advanced seekers maintains healthy margins despite stiff competition. Hybrid GNSS-inertial solutions dominate, but emerging optically aided systems are gaining traction for GPS-denied scenarios. Propulsion subsystems follow, with dual-pulse rocket motors supporting extended-range rockets. Semiconductor scarcity has complicated supply, pushing primes to dual-source ASICs and gallium-nitride power components.

Target-acquisition modules are expected to clock a 6.21% CAGR, the fastest among subsystems, as artificial intelligence (AI) boosts real-time object recognition rates. Indigenous sensor fabrication by major European primes reduces reliance on imports and shields programs from export-control shocks. Therefore, the precision-guided munition market share for target acquisition subsystems is expected to rise incrementally through 2030. Simultaneous improvements in onboard processing speed and thermal management lower detection-to-firing timelines and enhance engagement envelopes.

By Range: Long-Range Capabilities Accelerate

Medium-range (50 to 300 km) weapons captured 49.87% of the 2024 turnover, balancing cost and coverage for most battlefield and coastal defense missions. Their popularity rests on compatibility with existing launchers and doctrine, ensuring brisk demand from replacement and recapitalization cycles. Yet their CAGR eases to 4.8% through 2030 as militaries migrate to longer-range options for deterrence and deep-strike tasks.

Long-range systems (greater than 300 km) will expand at an 8.43% CAGR, spurred by the imperative to engage high-value nodes without entering adversary air-defense umbrellas. The precision-guided munition market size allocated to long-range systems is set to double by 2030, propelled by contract awards for surface-launched cruise missiles and extended-range rockets. European joint projects aim to field systems exceeding 1,000 km by the early 2030s, signaling persistent momentum.

By Speed: Hypersonic Systems Lead Innovation

Supersonic rounds retained 43.27% market share in 2024, capitalizing on decades of platform integration and export precedents. Their mature production lines deliver predictable costs, a trait sought by budget-sensitive ministries. However, their strategic value is gradually diluted by advanced air defenses capable of intercepting Mach 3 targets.

Hypersonic weapons are projected to post a 10.29% CAGR, the fastest in the precision-guided munition market, despite unit prices exceeding USD 10 million and unresolved thermal-protection challenges. Successful live-fire tests show potential to pierce tier-1 integrated air-defense shields, triggering parallel spending on counter-hypersonic interceptors. Certification hurdles and material scarcity prolong development cycles, but the strategic deterrence benefits keep programs well funded across the US, China, and Russia.

Geography Analysis

North America generated 39.92% of 2024 revenue, anchored by consistent US funding for long-range precision fire and multi-million-round sustainment packages. Canada invests in niche research grants on guidance algorithms, while Foreign Military Sales (FMS) cases to allies sustain production volumes between domestic lots. Upgrade contracts within NATO partially offset export-control laws, which cap expansion to non-aligned buyers but block orders to them.

Asia-Pacific is on course for the fastest 6.82% CAGR as territorial disputes and gray-zone coercion spur demand for credible strike options.[5]Congressional Research Service, “Allied Defense Spending and Programs,” everycrsreport.com Australia’s Guided Weapons and Explosive Ordnance Enterprise, India’s "Make in India" offsets, and Japan’s carrier aviation upgrades collectively buoy regional expenditure. The Philippines’ USD 875 million modernization outlay includes anti-ship precision missiles, broadening the customer base beyond the usual top spenders. China’s opaque, state-funded programs indirectly fuel Southeast Asian procurement as neighbors seek deterrent parity.

Europe balances capability shortfalls exposed by the Ukraine war with sovereign production drives. Germany’s EUR 2.10 billion (USD 2.46 billion) Taurus Neo and France’s Foudre MLRS exemplify the pivot from import reliance to local manufacture. NATO’s push for 2% of GDP defense spending adds a tailwind that should keep regional CAGR at 5.60% through 2030. In the Middle East and Africa, threat perceptions from precision-armed non-state actors accelerate offensive and defensive buys, although fiscal headroom varies widely with hydrocarbon revenues.

Competitive Landscape

The top five vendors, including Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, BAE Systems plc, and The Boeing Company, collectively controlled a significant share of the 2024 revenue, signaling a moderately concentrated field. Incumbents leverage decades of classified know-how, captive sustainment streams, and proprietary software toolchains to secure follow-on awards. Vertical mergers, such as primes acquiring RF-component suppliers, aim to shield programs from semiconductor shortages.

Emerging challengers include Türkiye’s ASELSAN and Roketsan, which combine government backing with competitive labor costs to undercut Western peers in export tenders. The consortium model, seen in European Next Generation Effectors, pools R&D risk and accelerates the transition of technology. As illustrated by Godspeed Capital’s USD 675 million defense fund, private equity inflows signal a growing investor appetite for niche guidance and propulsion shops.

Strategic moves in 2024-2025 centered on capacity expansions and digitalization. Lockheed Martin opened a new Alabama assembly line for the Precision Strike Missile, adding 50,000 ft² of automated machining space. MBDA implemented augmented-reality work instructions that cut build times by 25%. Northrop Grumman’s Glide Phase Interceptor win positions the firm as an early mover in counter-hypersonics, a domain viewed as the next multi-billion-dollar frontier.

Precision-Guided Munition Industry Leaders

Lockheed Martin Corporation

RTX Corporation

The Boeing Compnay

Northrop Grumman Corporation

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Germany approved the mass procurement of domestic loitering munitions to accelerate frontline fielding.

- March 2025: Türkiye’s ASELSAN and Delta-V conducted the first Göktan ground-launch test, striking a target over 100 km away.

- March 2025: Lockheed Martin secured a USD 4.94 billion production contract for the Precision Strike Missile, ensuring multiyear manufacturing visibility.

- March 2025: ASELSAN unveiled the GÖZDE guidance kit that converts Mk-82 bombs into dual-mode precision rounds.

Global Precision-Guided Munition Market Report Scope

| Tactical Missiles |

| Guided Rockets and Artillery Shells |

| Guided Bombs (PGMs/Smart Bombs) |

| Loitering Munitions |

| Interceptor Missiles |

| Torpedoes |

| Hypersonic Missiles |

| Airborne |

| Land-based |

| Naval |

| Unmanned Systems |

| Guided and Navigation Systems |

| Target Acquisition Systems |

| Propulsion Systems |

| Warheads |

| Power Supply Systems |

| Short-Range (Less than 50 km) |

| Medium-Range (50 to 300 km) |

| Long-Range (Greater than 300 km) |

| Subsonic |

| Supersonic |

| Hypersonic |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Tactical Missiles | ||

| Guided Rockets and Artillery Shells | |||

| Guided Bombs (PGMs/Smart Bombs) | |||

| Loitering Munitions | |||

| Interceptor Missiles | |||

| Torpedoes | |||

| Hypersonic Missiles | |||

| By Launch Platform | Airborne | ||

| Land-based | |||

| Naval | |||

| Unmanned Systems | |||

| By Subsystem | Guided and Navigation Systems | ||

| Target Acquisition Systems | |||

| Propulsion Systems | |||

| Warheads | |||

| Power Supply Systems | |||

| By Range | Short-Range (Less than 50 km) | ||

| Medium-Range (50 to 300 km) | |||

| Long-Range (Greater than 300 km) | |||

| By Speed | Subsonic | ||

| Supersonic | |||

| Hypersonic | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the precision-guided munition market in 2025?

The precision-guided munition market stands at USD 39.6 billion in 2025 and is projected to hit USD 52.48 billion by 2030.

Which product segment grows fastest through 2030?

Loitering munitions are expected to advance at a 7.56% CAGR, outpacing all other products.

Which region records the quickest growth?

Asia-Pacific leads with a 6.82% CAGR owing to territorial tensions and modernization drives.

What are the main restraints on market expansion?

Strict export-control regimes and electronic-warfare systems that degrade GPS guidance exert the greatest drag.

Who are the top vendors?

Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, BAE Systems plc, and The Boieng Company collectively command about 55% of 2024 revenue.

Why are hypersonic weapons attracting investment?

Their ability to penetrate advanced air defenses at speeds above Mach 5 drives both offensive procurement and counter-hypersonic R&D.

Page last updated on: