Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.22 Billion |

| Market Size (2031) | USD 7.03 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

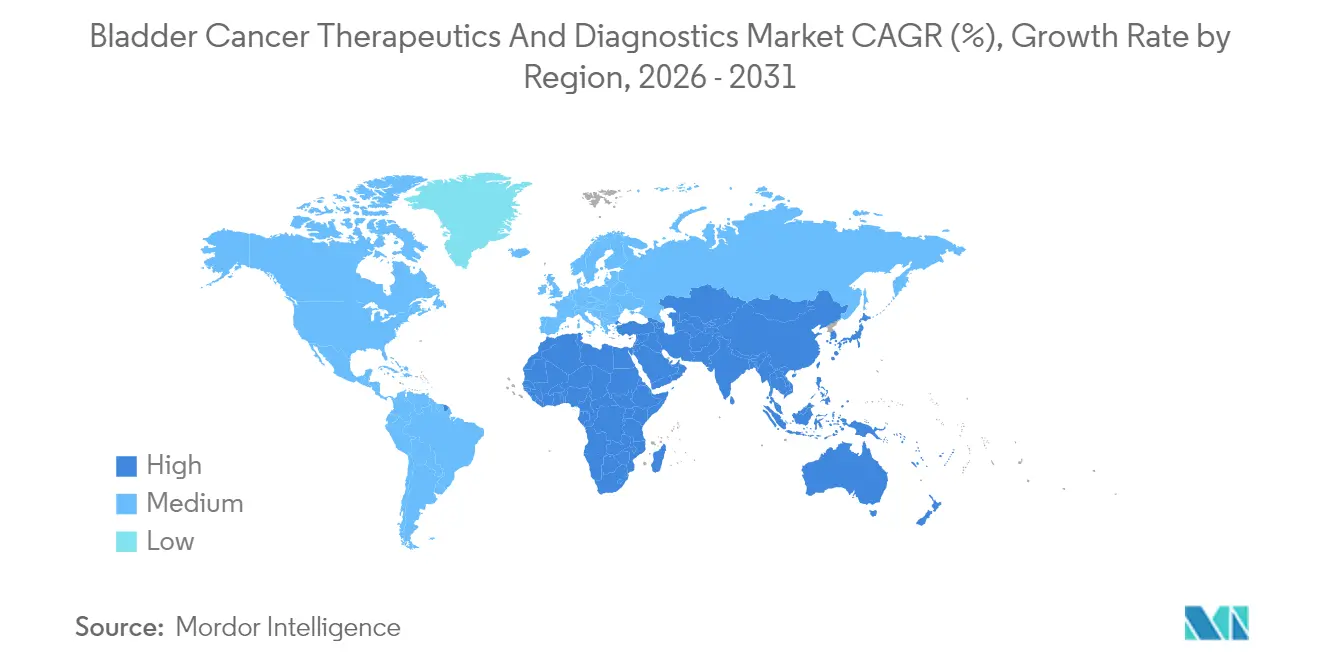

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bladder Cancer Therapeutics And Diagnostics Market Analysis by Mordor Intelligence

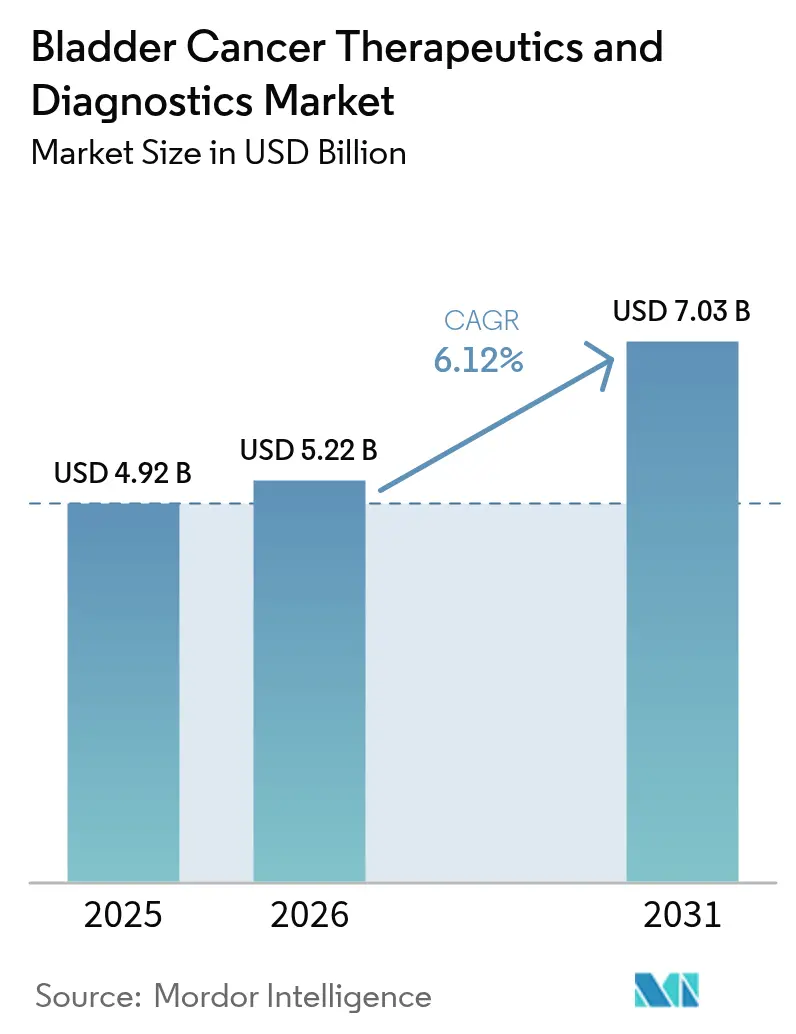

The Bladder Cancer Therapeutics And Diagnostics Market size in 2026 is estimated at USD 5.22 billion, growing from 2025 value of USD 4.92 billion with 2031 projections showing USD 7.03 billion, growing at 6.12% CAGR over 2026-2031.

The advance reflects a structural pivot from legacy chemotherapy toward precision immunotherapy, propelled by rapid FDA approvals for checkpoint inhibitors and antibody-drug conjugates that now form the backbone of combination protocols. Rising global incidence, earlier detection through blue-light cystoscopy, and reimbursement support for novel biologics further accelerate demand. New intravesical drug-delivery devices and AI-based urine-biomarker algorithms enhance clinical outcomes and streamline follow-up, magnifying procedural volumes in both inpatient and outpatient settings. Competitive intensity is increasing as pharmaceutical majors partner with focused biotechnology firms to align therapeutic and diagnostic innovations with value-based care metrics.

Key Report Takeaways

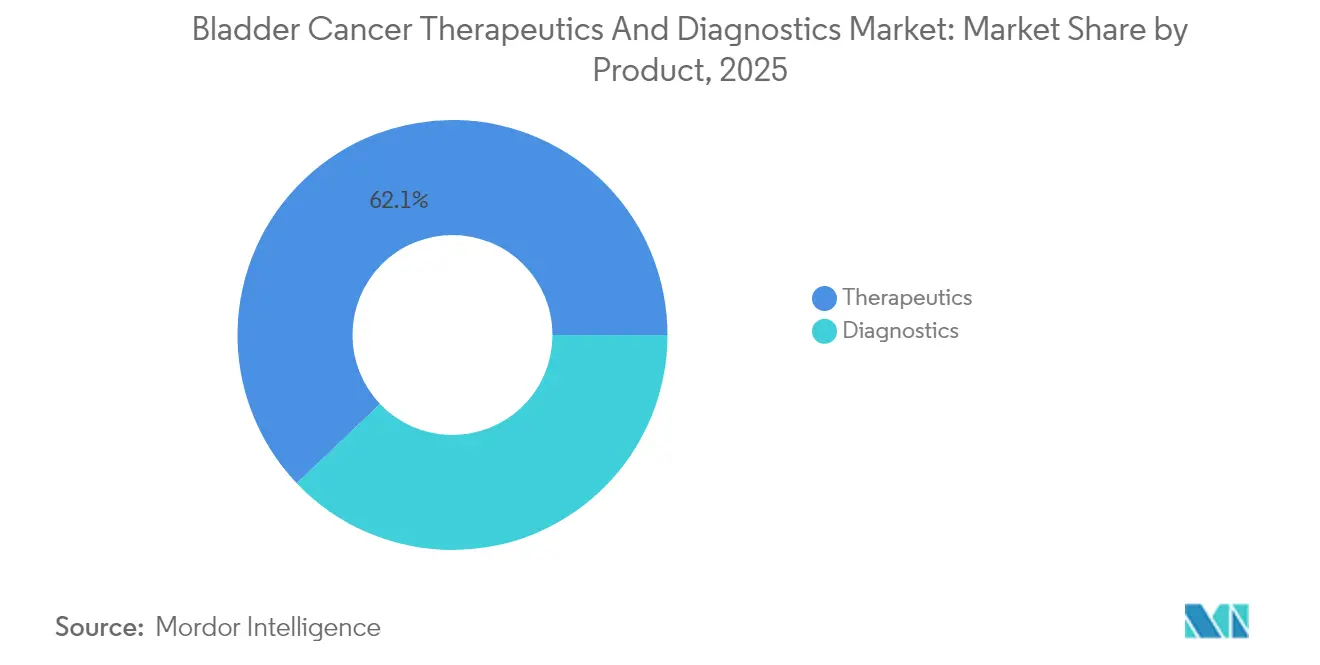

- By product category, therapeutics held a 62.10% share of the bladder cancer therapeutic and diagnostic market in 2025, while immunotherapy was projected to register the highest growth at an 8.25% CAGR through 2031.

- By cancer type, urothelial carcinoma accounted for 84.10% of the bladder cancer therapeutic and diagnostics market size in 2025 and is expected to expand at a 9.00% CAGR to 2031.

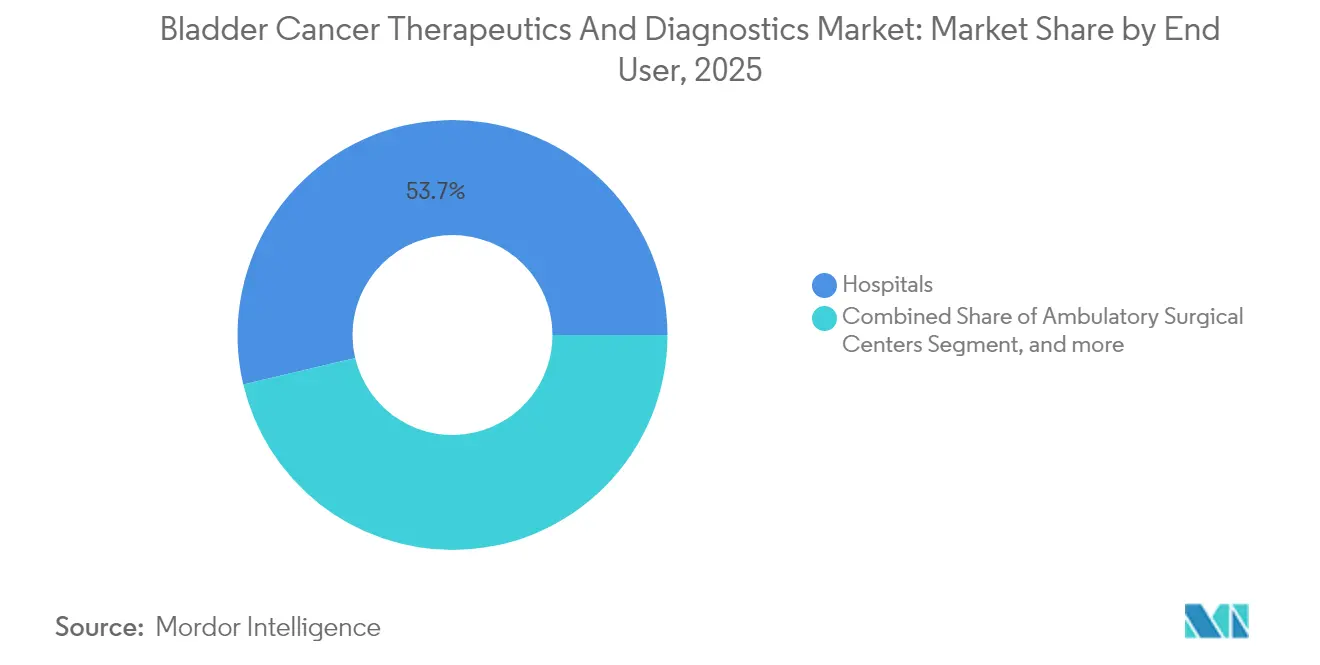

- By end user, hospitals retained 53.70% of 2025 revenue, whereas ambulatory surgical centers are forecast to advance at a 7.65% CAGR during the outlook period.

- By geography, North America led with 44.20% of 2025 revenue, and Asia Pacific is set to grow at a 10.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bladder Cancer Therapeutics And Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global bladder-cancer incidence | +1.5% | Global; highest in North America and Europe | Long term (≥ 4 years) |

| Rapid approvals of immune-checkpoint inhibitors and ADCs | +1.8% | North America and EU leading; APAC following | Medium term (2-4 years) |

| Wider adoption of blue-light and 4K cystoscopy | +1.2% | North America and Europe; expanding to APAC | Medium term (2-4 years) |

| AI-driven urine-biomarker algorithms | +0.9% | Global; early adoption in developed markets | Long term (≥ 4 years) |

| Growth of ASC-based cystoscopy volumes | +0.7% | North America; expanding to Europe | Short term (≤ 2 years) |

| Re-fillable intravesical drug-delivery devices | +0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Bladder-Cancer Incidence

Incidence continues to climb as aging populations expand and occupational carcinogen exposure persists. Epidemiological data indicate a steady rise among individuals ≥65 years, heightening demand for diagnostic surveillance and multi-line therapies.[1]Michael Guterbock, “Sustainable Oncology Care: A European Perspective,” The Economist, economist.com Earlier detection through imaging and urine-based assays swells the treatment-eligible cohort, particularly for non-muscle invasive disease. Health systems are scaling specialized urology centers and investing in trained personnel to cope with repeat interventions linked to high recurrence rates. These recurrent episodes sustain revenue generation for cystoscopy equipment, consumables, and adjuvant therapies. Economic models now incorporate indirect costs tied to lifetime monitoring, reinforcing the shift toward technologies that reduce recurrence risk.

Rapid Approvals of Immune-Checkpoint Inhibitors & ADCs

Accelerated regulatory pathways compress development cycles and hasten patient access to novel biologics. The FDA granted breakthrough status to agents such as enfortumab vedotin and durvalumab, enabling commercial launch within five years of pivotal trials.[2]Youssef Rddad, “‘Unprecedented’ Data Reinforce First-Line Enfortumab Vedotin Combo for Advanced Bladder Cancer,” Oncology News Central, oncologynewscentral.com Survival gains are persuasive; combining pembrolizumab with enfortumab vedotin delivers 33.8-month median overall survival versus 15.9 months for chemotherapy. Market entrants with robust pipelines secure first-mover advantages and command premium pricing. Traditional chemotherapy suppliers must now co-develop biologics or risk market erosion in the bladder cancer therapeutic and diagnostics market.

Wider Adoption of Blue-Light & 4K Cystoscopy

Enhanced visualization improves detection accuracy by revealing flat and multifocal lesions that are often missed by white-light scopes. Medicare reimbursement decisions in 2024 removed cost barriers, thereby catalyzing the adoption of outpatient services.[3]Blue Cross Blue Shield of North Carolina, “Urinary Tumor Markers for Bladder Cancer AHS – G2125,” bcbsnc.com Integration with 4K imaging enhances clarity during resection, resulting in lower recurrence and reoperation rates. Ambulatory surgical centers leverage shorter turnaround times to absorb elective cystoscopy volume, expanding the bladder cancer therapeutic and diagnostic market beyond hospital walls. Equipment manufacturers respond with compact, portable stacks designed for use in limited surgical suites.

AI-Driven Urine-Biomarker Algorithms

Machine-learning platforms combine cytology, protein markers, and genomic signatures to flag malignant cells at sensitivity levels nearing 90% in validation studies. Cloud-based analytics standardize interpretation across laboratories, reducing operator variability. These tests could partially replace invasive cystoscopy in surveillance protocols, thereby boosting patient compliance and reducing procedure-related morbidity. Commercial rollouts focus on high-incidence regions where surveillance caseloads place a significant burden on health systems. Challenges persist around reimbursement coding and clinician adoption, but pilot programs report favorable cost-utility ratios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expiries and generic erosion of key chemo drugs | -0.8% | Global; price-sensitive markets hit hardest | Short term (≤ 2 years) |

| High cost and reimbursement hurdles for novel biologics | -0.6% | Emerging markets; selective impact in developed regions | Medium term (2-4 years) |

| Global BCG shortages disrupting therapy patterns | -0.5% | Global; severe in Latin America and Asia | Short term (≤ 2 years) |

| Limited blue-light equipment availability in emerging settings | -0.4% | Emerging markets and rural areas in developed countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries & Generic Erosion of Key Chemo Drugs

The expiration of mitomycin C and cisplatin patents invites generic competition that compresses therapy margins. Price declines favour payers but constrain manufacturer revenues needed for R&D reinvestment. Although generics widen access, they split volumes across multiple suppliers, diluting scale efficiencies. Stakeholders explore hybrid regimens that pair low-cost cytotoxics with premium biologics, balancing affordability with efficacy. Yet negotiations over bundled pricing introduce complexity into procurement processes for hospital systems already under budget pressure.

High Cost / Reimbursement Hurdles for Novel Biologics

Checkpoint inhibitors and ADCs list above USD 100,000 per course in several markets, straining payer budgets that balance multiple oncology priorities. Access in middle-income economies remains uneven, with prior authorization and step-therapy requirements delaying initiation. Value-based contracts, pegging payment to sustained response, surface as compromise solutions but require data capture infrastructure not uniformly available. Manufacturers deploy tiered pricing or local production partnerships to mitigate affordability gaps, yet uptake in low-resource settings lags expected clinical benefit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutics Maintain Leadership While Diagnostics Scale Quickly

Therapeutics commanded 62.10% of 2025 revenue within the bladder cancer therapeutic and diagnostics market, reflecting the repeated dosing and high unit prices of systemic and intravesical agents. Immunotherapy alone is forecast to grow at an 8.25% CAGR, backed by expanding labels for pembrolizumab, durvalumab, and nivolumab. Antibody-drug conjugates such as enfortumab vedotin open new salvage pathways, especially for platinum-ineligible cohorts. The bladder cancer therapeutic and diagnostics market size for diagnostics is climbing, driven by blue-light scopes, 4K imaging towers, and AI-enabled urine assays that collectively enhance early detection.

Intravesical delivery platforms like TAR-200 and UGN-102 gain traction by releasing chemotherapy directly into the bladder wall, reducing systemic exposure while preserving efficacy. Diagnostic firms scale production of single-use scopes and fluorescent dyes as procedure volumes migrate to ambulatory settings. Molecular panels that combine DNA methylation and protein markers edge toward guideline endorsement, poised to redefine surveillance algorithms once reimbursement alignment occurs.

By Cancer Type: Urothelial Carcinoma Dominates Development Efforts

Urothelial carcinoma accounted for 84.10% of 2025 revenue and is projected to deliver a 9.00% CAGR, solidifying its position as the focal point for clinical innovation in the bladder cancer therapeutic and diagnostic market. Its molecular landscape accommodates PD-1 blockade, FGFR inhibition, and ADC therapy, providing multiple commercialization routes for pharmaceutical pipelines. In parallel, the bladder cancer therapeutic and diagnostics market share linked to urothelial carcinoma will expand as additional first-line combinations reach approval.

Squamous-cell carcinoma and adenocarcinoma remain underserved, together accounting for a modest fraction of the bladder cancer therapeutic and diagnostic market size. Limited clinical trial enrollment and heterogeneous molecular profiles slow drug discovery. Nevertheless, niche opportunities exist for developers who target rare-mutation pathways or exploit basket-trial frameworks to accelerate evidence generation.

By End User: Hospitals Anchor Care While ASC Participation Scales

Hospitals retained 53.70% of 2025 spending, acting as hubs for complex resections, systemic therapy initiation, and management of adverse events. They host multidisciplinary boards that align diagnostic findings with personalized treatment plans, reinforcing their central role in the bladder cancer therapeutic and diagnostics market. The market size attributable to ambulatory surgical centers is expected to grow rapidly as reimbursement equalizes and procedure times fall below two hours for many cystoscopy-based interventions.

ASCs optimize scheduling and reduce inpatient bed demand, benefitting both payers and patients through lower facility fees and shorter recovery times. Specialty centers emerge around academic institutions that secure NIH and EU grants for translational research, blending clinical care with protocol development. These sites often pilot AI-driven decision support tools, creating real-world evidence that shapes broader adoption trajectories.

Geography Analysis

North America contributed 44.20% of 2025 revenue, driven by strong FDA-accelerated programs, National Comprehensive Cancer Network guideline updates, and Medicare reimbursement that supports blue-light cystoscopy kits and urine-biomarker assays. Private payers are increasingly aligning with federal determinations, thereby smoothing nationwide access. Canada leverages pan-provincial buying groups to negotiate favorable biologic pricing, while Mexico expands public oncology coverage through reforms to Seguro Popular. Cross-border patient flows remain limited but could increase as novel therapies spread to tertiary centers along the US-Mexico border.

The Asia Pacific is expected to deliver the fastest regional CAGR of 10.40% through 2031, as China, Japan, and India undertake upgrades to their oncology infrastructure. China’s local manufacturing partnerships reduce unit costs for checkpoint inhibitors, catalyzing uptake in provincial cancer centers. Japan maintains a high adoption rate of enfortumab vedotin and pembrolizumab, mainly due to robust national health insurance coverage. Indian private chains are gradually introducing blue-light cystoscopy, prioritizing metropolitan cities where disposable incomes support out-of-pocket payments until wider insurance penetration occurs. ASEAN countries such as Singapore and Malaysia pilot AI-enabled urine diagnostics within value-based care pilots.

Europe exhibits balanced growth driven by the European Medicines Agency’s coordinated review process and national health technology assessments that emphasize cost–benefit clarity. Germany’s DRG system reimburses blue-light scopes within outpatient packages, encouraging migration away from admission-based cystoscopies. The United Kingdom’s Cancer Drugs Fund accelerates conditional access to novel ADCs while collecting registry data to inform full NHS funding decisions. Southern European markets harmonize procurement via joint tenders, using pooled volumes to negotiate biologic discounts while maintaining open access to guideline-backed innovations.

Competitive Landscape

The bladder cancer therapeutic and diagnostic market is fragmented. Roche, Merck, Bristol Myers Squibb, and AstraZeneca dominate immune-oncology sales, yet each holds a subset of indications. Enfortumab vedotin’s success spurred Seagen and Pfizer to accelerate the development of next-generation ADCs, including those directed at nectin-2 and nectin-3. Strategic alliances proliferate; Merck’s 2024 pact with Kelun-Biotech added seven ADC candidates to its urothelial pipeline. Johnson & Johnson’s TAR-200 inserts sustain-release gemcitabine within a biodegradable ring, enabling a 21-day dwell time without catheter removal, an advantage for non-muscle-invasive disease.

Diagnostic innovation adds new entrants. Photocure’s Cysview dye maintains its first-mover status in blue-light imaging, whereas Karl Storz and Olympus compete with 4K technologies that are not compatible with fluorescent filters. AI start-ups license urine biomarker classifiers to regional laboratories, creating scalable, platform-agnostic offerings. Competitive narrative is increasing, emphasizing bundled solutions that link test results to therapeutic choices, thereby shortening decision cycles and differentiating vendors in procurement bids. Intellectual-property portfolios emphasize device–drug combinations and algorithmic decision support, reflecting the convergence of software, hardware, and biologics.

Investor sentiment favors firms that can navigate both therapeutic and diagnostic reimbursement structures. Private equity groups acquire ASC chains equipped with blue-light suites, betting on predictable revenue growth and consolidation synergies. Meanwhile, larger pharma players hedge pipeline risk by securing option-to-buy clauses with early-stage biotech partners, ensuring access to breakthrough science without upfront integration costs.

Bladder Cancer Therapeutics And Diagnostics Industry Leaders

Bristol-Myers Squibb Company

GlaxoSmithKline PLC

Merck & Co. Inc.

Johnson & Johnson (Janssen)

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AstraZeneca received European Commission approval for durvalumab (Imfinzi) in combination with gemcitabine and cisplatin as first-line treatment for locally advanced or metastatic urothelial carcinoma.

- February 2025: Seagen and Pfizer reported unprecedented durability data for enfortumab vedotin plus pembrolizumab combination therapy, with median overall survival reaching 33.8 months compared to 15.9 months for chemotherapy in the EV-302/KEYNOTE-A39 trial.

- December 2024: UroGen Pharma announced positive Phase 3 results for UGN-102 (mitomycin gel) in treating low-grade upper tract urothelial carcinoma, demonstrating complete response rates that support regulatory filing preparations.

- December 2024: CG Oncology initiated Phase 3 BOND-003 trial for CG0070, an oncolytic immunotherapy targeting BCG-unresponsive non-muscle invasive bladder cancer.

Global Bladder Cancer Therapeutics And Diagnostics Market Report Scope

As per the scope of the report, bladder cancer is a tumor that starts in the cells of the bladder. Bladder cancer is the rapid, uncontrolled growth of abnormal cells in the urinary bladder lining with epithelial cells. These cancerous cells may even spread through the lining into the muscular wall of the bladder. Several therapies have been developed to treat bladder cancers, which, in turn, build a high demand for the bladder cancer therapeutics market. The Bladder Cancer Therapeutics and Diagnostics Market is segmented by Product (Therapeutics (Chemotherapy, Immunotherapy, Other Therapeutics), and Diagnostics (Cystoscopy, Bladder Ultrasound, Urinalysis, Other Diagnostics), Cancer Type (Transitional Cell Bladder Cancer, Squamous Cell Bladder Cancer, Other Cancer Types), and Geography (North America, Europe, Asia- Pacific, Middle East and Africa and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the abovementioned segments.

By Product

| Therapeutics | Chemotherapy |

| Immunotherapy | |

| Antibody-Drug Conjugates | |

| Intravesical Drug-Delivery Devices | |

| Diagnostics | Cystoscopy |

| Bladder Ultrasound & Imaging | |

| Urinalysis & Dipstick Tests | |

| Urine & Liquid-biopsy Biomarker Panels |

By Cancer Type

| Urothelial Carcinoma |

| Squamous-cell Carcinoma |

| Adenocarcinoma & Other Rare Types |

By End User

| Hospitals |

| Ambulatory Surgical Centers |

| Speciality Centers |

| Academic and Research Institutes |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Therapeutics | Chemotherapy |

| Immunotherapy | ||

| Antibody-Drug Conjugates | ||

| Intravesical Drug-Delivery Devices | ||

| Diagnostics | Cystoscopy | |

| Bladder Ultrasound & Imaging | ||

| Urinalysis & Dipstick Tests | ||

| Urine & Liquid-biopsy Biomarker Panels | ||

| By Cancer Type | Urothelial Carcinoma | |

| Squamous-cell Carcinoma | ||

| Adenocarcinoma & Other Rare Types | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Speciality Centers | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the bladder cancer therapeutic and diagnostics market?

The bladder cancer therapeutic and diagnostics market size is USD 5.22 billion in 2026.

Which treatment class is growing fastest?

Immunotherapy is advancing at an 8.25% CAGR through 2031 owing to rapid approvals of checkpoint inhibitors and antibody-drug conjugates.

Why are ambulatory surgical centers gaining importance?

Reimbursement alignment and blue-light cystoscopy efficiencies enable many diagnostic and surveillance procedures to shift from hospitals to ASC settings, driving a 7.65% CAGR.

Which region will grow most quickly through 2031?

Asia Pacific leads regional growth with a projected 10.40% CAGR, driven by infrastructure upgrades and demographic trends.

How are AI technologies influencing bladder cancer care?

AI-driven urine-biomarker algorithms offer high-sensitivity non-invasive surveillance, potentially reducing dependence on cystoscopy and improving patient adherence.

What key challenge limits access to novel biologics in emerging markets?

High acquisition costs and stringent reimbursement hurdles slow uptake, although tiered pricing and outcome-based contracts are beginning to address affordability barriers.

Page last updated on: