Precipitated Silica Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

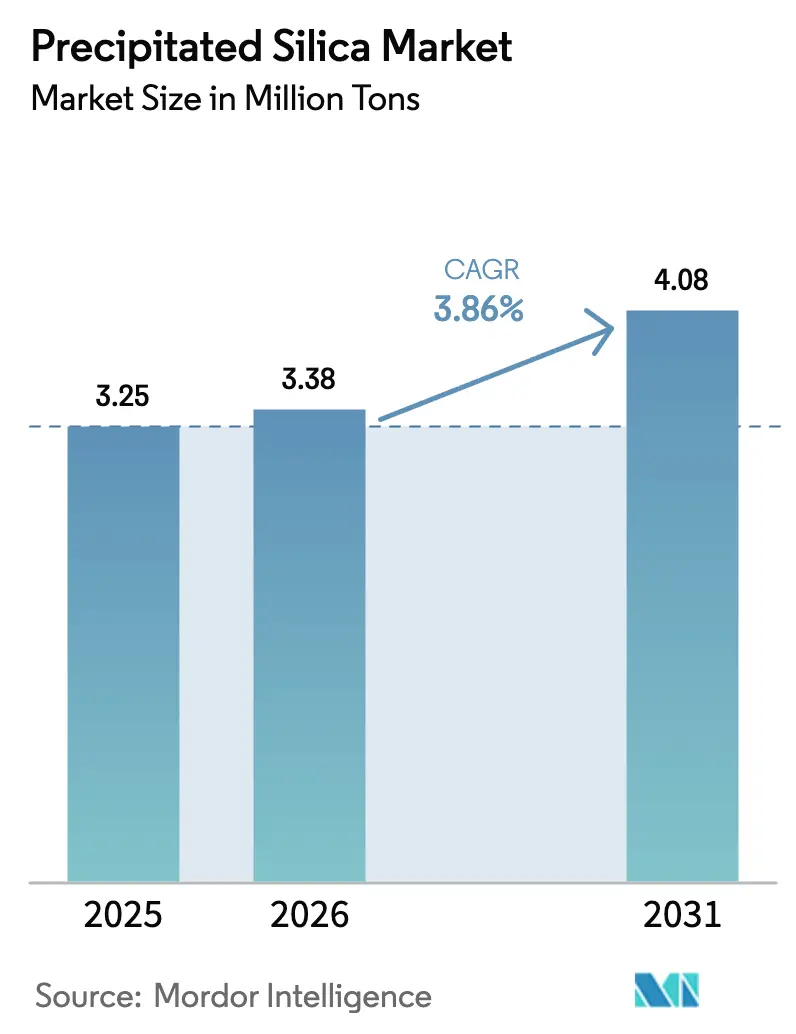

| Market Volume (2026) | 3.38 Million tons |

| Market Volume (2031) | 4.08 Million tons |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

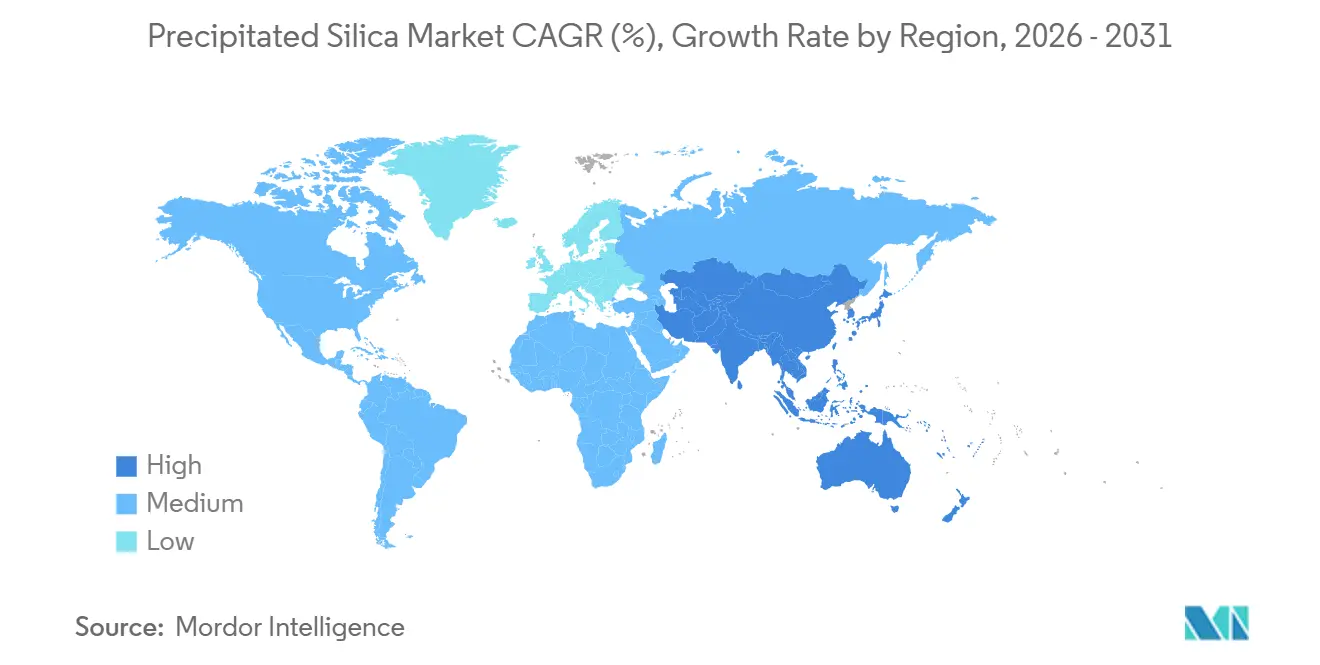

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precipitated Silica Market Analysis by Mordor Intelligence

The Precipitated Silica Market size is expected to increase from 3.25 Million tons in 2025 to 3.38 Million tons in 2026 and reach 4.08 Million tons by 2031, growing at a CAGR of 3.86% over 2026-2031. Momentum stems from electric-vehicle (EV) tire formulations that demand higher-performance rubber grades, coupled with food regulators endorsing ultra-pure amorphous silica for clean-label products. Wet-process routes still contribute 75.21% of 2025 volume, yet dry-process output is expanding at 4.89% annually as producers seek lower energy intensity and niche battery-separator applications. Asia-Pacific commands a 50.24% share in 2025 and leads future growth at a 3.95% CAGR in 2026-2031, helped by rice-husk-ash valorization projects that trim raw-material costs by 15-20% against conventional sodium-silicate pathways. Competitive intensity remains moderate, with the five largest suppliers holding roughly half of installed capacity, while mid-tier players scale biomass-based lines and ultra-pure grades for lithium-ion batteries.

Key Report Takeaways

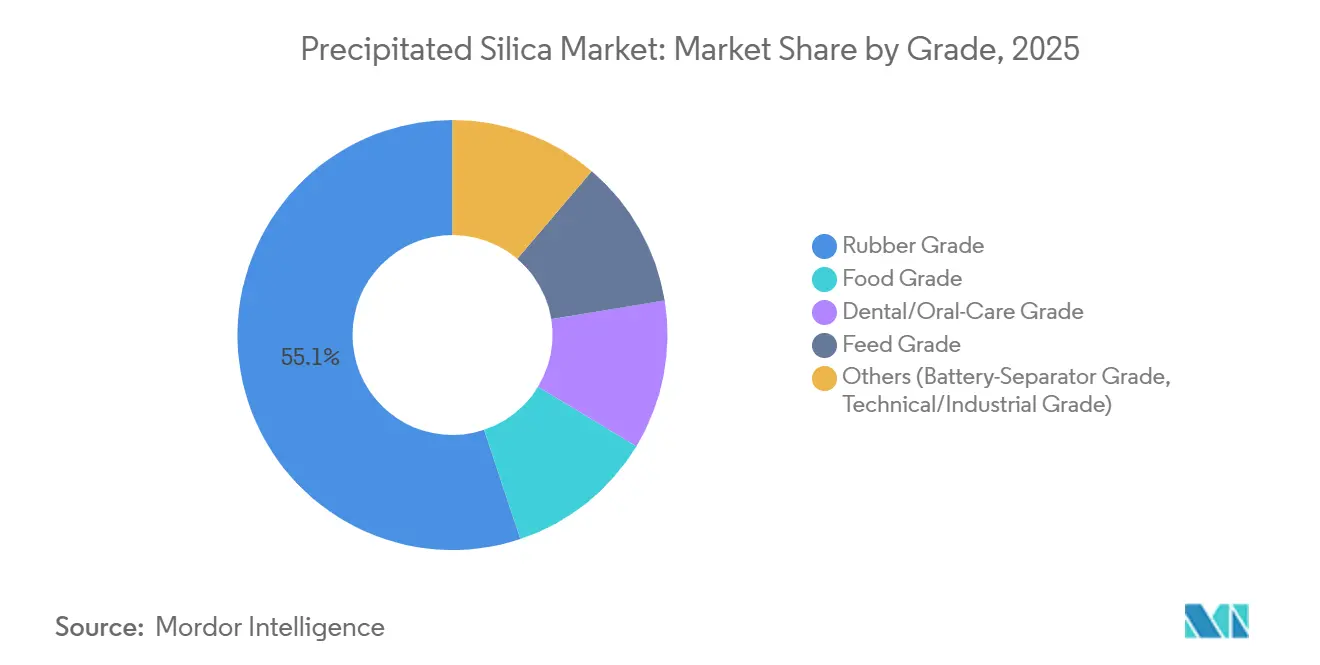

- By grade, rubber grade held 55.12% of the precipitated silica market share in 2025, while food grade is projected to post the fastest 4.56% CAGR through 2031.

- By form, powder dominated with 48.31% revenue share in 2025; beads are set to expand at a 6.34% CAGR to 2031.

- By production process, the wet route commanded 75.21% of the precipitated silica market in 2025, whereas the dry route is forecast to grow 4.89% annually during 2026-2031.

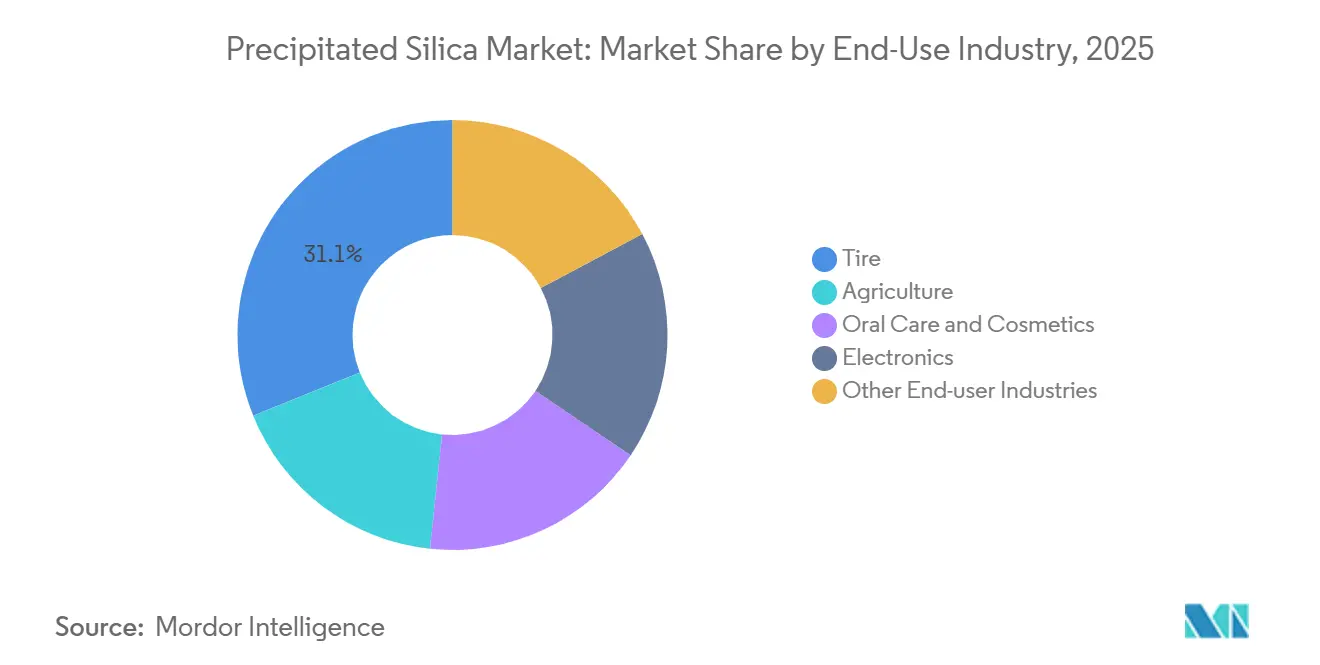

- By end-use industry, tires accounted for 31.12% of global volume in 2025; oral-care and cosmetics applications are advancing at a 4.20% CAGR through 2031.

- By geography, the Asia Pacific captured 50.24% of global demand in 2025 and leads growth at a 3.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Precipitated Silica Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification-driven demand for silica-enhanced EV tires | +0.9% | Global, concentrated in China, EU, North America | Medium term (2-4 years) |

| Regulatory push for low-rolling-resistance green tires | +0.7% | EU, North America, Japan, South Korea | Short term (≤ 2 years) |

| Food-grade silica uptake in clean-label formulations | +0.5% | North America, EU, urban Asia-Pacific | Medium term (2-4 years) |

| Rice-husk-ash circular-economy silica scale-up | +0.6% | China, India, Thailand, Vietnam | Long term (≥ 4 years) |

| High-purity silica for Li-ion battery separators | +0.4% | Asia-Pacific, North American EV hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification-Driven Demand for Silica-Enhanced EV Tires

Instant torque and heavier battery packs make EV tires wear faster, yet range targets force automakers to curb rolling resistance. Raising precipitated silica loadings from 10–15 phr to 20–30 phr cuts hysteresis by up to 25% while preserving grip[1]Corporate Communications, Evonik Industries, evonik.com. China built 9.5 million battery-electric and plug-in hybrid vehicles in 2025, each consuming four to five tires with silica content 40–60% higher than combustion models, equating to roughly 50,000–70,000 t of incremental annual demand locally. Tightened EU tire-labeling thresholds that took effect mid-2024 reinforce the shift, and North American OEMs have adopted similar procurement specs, embedding silica into baseline tire designs irrespective of oil-price swings. The trend locks in structural growth for the precipitated silica market, encouraging producers to invest in dedicated EV-grade capacity across all regions.

Regulatory Push for Low-Rolling-Resistance Green Tires

Corporate Average Fuel Economy rules set 49 mpg targets for model-year 2026 passenger cars in the United States, compelling automakers to mandate low-rolling-resistance tires that can deliver 3–5% fuel savings[2]Statistical Center, National Highway Traffic Safety Administration, nhtsa.dot.gov. ASTM F2493 test procedures and ISO 28580 harmonization let tire makers validate silica formulations consistently worldwide. Japan and South Korea award top tire-label grades only for rolling-resistance coefficients under 9.0, a level nearly unreachable without silica reinforcement, and both markets exceeded 70% silica penetration in passenger-car tires during 2025. These synchronized policies form a compliance floor that shields the precipitated silica market from short-term price cycles, thereby sustaining capacity-expansion pipelines.

Food-Grade Silica Uptake in Clean-Label Formulations

Retailers and consumers favor short ingredient lists, prompting food processors to replace synthetic anti-caking agents with amorphous precipitated silica. The U.S. FDA lists silicon dioxide as Generally Recognized as Safe up to 2 wt% in food powders. Its 150–200 m²/g surface area adsorbs ambient moisture efficiently, preventing caking in salt, beverage mixes, and spice blends even at tropical warehouse humidity. Innova Market Insights recorded an 8% rise in global clean-label launches during 2024, and 22% of new dry-mix items contained silicon dioxide. Suppliers now certify production lines under ISO 22000 and FSSC 22000, bolstering brand confidence. Consequently, food-grade volumes underpin part of the 4.56% CAGR forecast and broaden the geographic spread of the precipitated silica market beyond automotive hubs.

Rice-Husk-Ash Circular-Economy Silica Scale-Up

Asia burns roughly 200 million t of rice husk annually, yielding ash that contains 85–95% silica. Converting this biomass by-product avoids virgin quartz mining and lowers feedstock cost to USD 30–50 t⁻¹, against USD 150–180 t⁻¹ for sodium silicate and sulfuric acid. China’s ash-based silica revenue stood at CNY 430 million (USD 60 million) in 2024 and is expected to top CNY 1 billion (USD 140 million) by 2030. Evonik’s 2024 supply agreement with Phichit Bio Power in Thailand trims raw-material spend by 15–20% and cuts Scope-3 emissions, aligning with EU Carbon Border Adjustment mechanisms. The model scales readily across India, Vietnam, and Indonesia, giving local players a structural cost edge and nudging global producers to rethink feedstock portfolios. This resource efficiency adds resilience to the precipitated silica market over the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight sulphuric-acid supply inflating costs | -0.60% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Automotive OEM production-cycle volatility | -0.50% | Global, concentrated in North America, EU, China | Medium term (2-4 years) |

| Consumer backlash on silica micro-plastics (personal care) | -0.10% | EU, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight Sulfuric-Acid Supply Inflating Costs

Precipitated silica synthesis needs 0.3–0.4 t of sulfuric acid per tonne of product. US elemental sulfur output slid 5% to 8.2 million t in 2024, driving Tampa contract acid prices from USD 69/t in Q1 2024 to USD 116/t by year-end, a 68% surge. Chinese spot prices climbed even faster due to smelter shutdowns and export curbs. Producers weigh backward integration into sulfur recovery, yet regeneration plants cost more than USD 50 million, and paybacks stretch past five years. These cost spikes compress gross margins, particularly for commodity powder grades, and temper near-term investment appetite in the precipitated silica market.

Automotive OEM Production-Cycle Volatility

Tires account for 31.12% of 2025 volumes, and original-equipment orders swing with light-vehicle output. Semiconductor shortages, labor actions, and fluctuating credit costs pushed global production down 3% in early 2025, whipsawing tire plant schedules. A 1-point decline in vehicle builds removes roughly 15,000–20,000 t of silica demand, pressuring capacity utilization below the 75% breakeven threshold. Suppliers diversified into food, oral care, and electronics weather shocks better, yet mono-product tire specialists feel more acute volatility. Persistent cyclicality caps upside potential for the precipitated silica market, even as long-term electrification trends remain favorable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Rubber Still Dominates While Food Accelerates

Rubber-grade silica held 55.12% of volume in 2025, reflecting entrenched use in low-rolling-resistance tire tread. Food-grade volumes, though smaller, are growing at 4.56% CAGR through 2031, the fastest among all grades, as global brand owners adopt clean-label anti-caking agents. Dental-silica abrasives reached about USD 500 million in 2025, backed by rising toothpaste penetration in emerging economies. These dynamics keep rubber volumes high, yet incremental growth increasingly stems from food and oral-care niches, diversifying revenue streams inside the precipitated silica market.

Steady regulatory frameworks, the FDA’s GRAS rule 21 CFR 172.480, and EFSA’s 2018 opinion, lower reformulation risk for food processors, underpinning the grade’s expansion. Meanwhile, rice-husk-ash feedstock demonstrates that biomass routes can deliver tire-grade surface areas, narrowing cost gaps with wet-process incumbents. By 2031, food and oral-care grades together could approach one-third of the precipitated silica market size for specialty applications, challenging the traditional dominance of rubber compounds.

By Form: Powder Leads but Beads Surge

Powder accounted for 48.31% of 2025 shipments because it disperses easily into rubber and plastics. Beads, however, are advancing at 6.34% CAGR on the back of toothpaste and cosmetic gel demand, where uniform spheres prevent grit and maintain flow. Spray-drying investments of USD 5–10 million per line have lifted bead capacity across Taiwan, Japan, and India, trimming supply-chain lead times. Powder will remain the workhorse, yet beads are set to carve a premium sub-segment of the precipitated silica market, bolstered by microplastics regulations that exclude inorganic silica from polymer restrictions.

Consistent particle morphology allows beads to meet European microbead replacements, and oral-care brands capitalize on marketing claims around faster dissolution. Granules continue serving agricultural blends, while micro-pearls hold niche cosmetic and coating positions. As a result, beads could exceed 20% of form sales by 2031, shifting revenue mix and raising average selling prices across the precipitated silica market.

By Production Process: Wet Route Prevails While Dry Gains Share

Wet processing generated 75.21% of 2025 volume thanks to its ability to hit surface areas of 150–250 m²/g, vital for premium tire and oral-care grades. Dry processing is catching up, growing at 4.89% CAGR, especially in coatings and plastics, where 80–100 m²/g suffices. Dry plants avoid acid entirely and can tap flue-gas CO₂, fitting circular-economy narratives in Europe and China. Capital costs run 20% lower than wet plants, yet product versatility remains narrower. Still, lower energy intensity positions dry processing as a credible alternative for commodity applications within the precipitated silica market.

Wet plants face variable-cost exposure to sulfuric acid and must manage sodium-sulfate by-product, sometimes incurring USD 20–30/t in disposal or logistics. Hybrid biomass-wet routes under pilot in China seek 15–20% energy cuts, hinting at convergence. Over the long run, dry technologies could rise above 30% share of the precipitated silica market size as sustainability metrics tighten.

By End-Use Industry: Tires Anchor, Oral Care Outpaces

Tires absorbed 31.12% of 2025 demand, cementing the sector’s anchor role. Yet oral-care and cosmetics are climbing at 4.20% CAGR through 2031 as toothpaste penetration widens in Asia and Latin America. Electronics, chiefly battery-separator coatings, offer small but fast-growing volumes, while agriculture and industrial coatings scale in line with GDP. If EV adoption meets policy targets, tire silica intensity may climb another 10–15 phr, keeping absolute tire tonnage growing despite mature vehicle markets. Meanwhile, oral-care demand dispersion across geographies balances cyclical automotive swings, stabilizing the precipitated silica market revenue mix.

Regulatory clarity helps; the FDA anticaries monograph permits up to 10 wt% silicon dioxide in toothpaste, and the EU Cosmetics Regulation lists it without concentration caps. These guardrails embolden formulators. Battery separator demand, although nascent, commands premium pricing and raises the technological barrier to entry, reinforcing competitive moats for incumbents with ultra-pure processing capabilities. This interplay sustains multi-segment growth avenues for the precipitated silica market.

Geography Analysis

Asia-Pacific retained 50.24% of 2025 volume and is set for 3.95% CAGR through 2031. China’s 9.5 million EV output in 2025 underpins local tire-grade silica demand, while rice-husk-ash projects across China, India, and Thailand unlock low-cost supply. Japan and South Korea enforce stringent tire-label grades that require silica reinforcement, pushing regional penetration above 70%. Thai biomass tie-ups, such as Evonik’s Map Ta Phut venture, enhance feedstock security and carbon credentials. This momentum keeps Asia at the core of the precipitated silica market investment cycle.

In North America and Europe, Evonik’s Charleston expansion, operational in January 2026, boosts wet-process capacity by 50% to serve rising EV-tire orders, while Qemetica’s purchase of PPG’s assets added 200,000 t pa across Lake Charles and Delfzijl. EU tire-label tightening and microplastics bans accelerate silica substitution in both automotive and personal-care channels. However, sulfuric-acid price inflation weighs on European and US producers, highlighting cost-structure disparities across the precipitated silica market.

South America and the Middle East & Africa show selective growth pockets. Brazil’s tire industry recovered alongside 2.1 million vehicle sales in 2024, spurring local demand. Argentina’s fertilizer blenders employ silica as a flow agent, while Gulf Cooperation Council nations aim to backward-integrate specialty silica into downstream petrochemicals clusters. Logistics costs from Asia often add USD 100–150/t, protecting entrenched wet-process suppliers. These regions thus remain strategic second-tier opportunities within the precipitated silica market landscape.

Mordor Intelligence provides coverage of the precipitated silica market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The precipitated silica market is moderately consolidated. Technology differentiation centers on surface modification and process efficiency. Evonik’s Weston, Michigan, plant produces more than 99.5% purity colloidal silica for battery separators, while Solvay’s bio-circular pathway in Livorno harvests rice-husk ash to shave off Scope-3 emissions. Patent filings around organosilane treatments climbed to 47 in 2024, signaling elevated R&D intensity. Chinese producers deploy machine-learning algorithms to trim batch variability below 3%, translating to USD 15–20/t savings and raising competitive bars. Such moves reinforce the dynamic, innovation-oriented profile of the precipitated silica market.

Precipitated Silica Industry Leaders

Cabot Corporation

Evonik Industries AG

Solvay

W. R. Grace & Co.

Quechen Silicon Chemical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Tata Chemicals greenlit an investment aimed at expanding its manufacturing facilities in Gujarat and Tamil Nadu, India. A segment of this investment is earmarked for boosting the precipitated silica manufacturing capacity at the company's Cuddalore plant in Tamil Nadu.

- July 2025: Aksharchem India Ltd. expanded its precipitated silica plant in Gujarat, India, boosting its capacity by 6,000 tonnes per year. This expansion brings the company's total precipitated silica production capacity to 18,000 tonnes annually. The increased capacity aims to better serve the tire and rubber industries.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines precipitated silica as the amorphous silicon-dioxide produced when sodium silicate is neutralized with a mineral acid, then precipitated, filtered, washed, dried, and milled. The scope covers powder, bead, and micro-pearl grades applied as reinforcing, thickening, flow-control, or anti-caking additives across tires, technical rubber, toothpastes, agrochemicals, food, and industrial coatings.

(Scope exclusions) Fumed silica, silica gel, crystalline quartz, and natural silica sand are not considered.

Segmentation Overview

- By Grade

- Rubber Grade

- Food Grade

- Dental/Oral-Care Grade

- Feed Grade

- Others (Battery-Separator Grade and Technical/Industrial Grade)

- By Form

- Powder

- Beads

- Micro-pearls

- Granules

- By Production Process

- Wet Process

- Dry Process

- By End-use Industry

- Agriculture

- Oral Care and Cosmetics

- Tire

- Electronics

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement heads at Asian tire makers, EMEA oral-care formulators, and North American silica producers. These conversations verified utilization rates, captured region-specific price spreads, and reconciled any gaps spotted during secondary collection.

Desk Research

We gathered baseline signals from tier-1 sources such as UN Comtrade HS 281122/281123 flows, Eurostat PRODCOM, and U.S. Geological Survey silica chapters, then paired them with tire shipment tallies from the U.S. Tire Manufacturers Association and trade-body notes issued by IRSG and Cefic. Company 10-Ks, environmental reports, and patent clusters accessed through Questel and D&B Hoovers clarified installed capacities, new projects, and typical selling prices. Government customs gazettes and national statistics rounded out regional demand insights. The sources cited are illustrative; many additional publications informed our desk work.

Market-Sizing & Forecasting

We begin with a top-down production-plus-trade reconstruction that converts local sodium-silicate output and net imports into precipitated-silica supply, which is balanced against demand pools in tires, dentifrice, coatings, and crop-protection carriers. Select bottom-up checks, producer capacity roll-ups and sampled ASP × volume estimates, fine-tune totals. Key drivers such as new-tire production, electric-vehicle share, oral-care penetration, rice-husk-ash substitution, and regional sulfuric-acid availability feed a multivariate regression that extends volumes to 2030. When disclosures are partial, output is inferred from energy and acid consumption norms.

Data Validation & Update Cycle

Outputs undergo variance screening versus historical trade curves, peer review by senior analysts, and a last-minute refresh before publication. We update models annually and issue interim revisions when plant shutdowns, regulatory shifts, or major M&A events materially alter supply-demand balances.

Why Mordor's Precipitated Silica Baseline Is Dependable

Market figures often diverge because some firms mix value and volume units, bundle other specialty silicas, or apply blanket price escalators. Our volume-first model, refreshed every year, anchors on verifiable production and trade evidence, then layers selective price checks to ensure internal coherence.

The comparison shows that our disciplined scope selection, evidence-based variables, and regular refresh cadence give decision-makers a balanced, transparent baseline they can replicate with confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 3.32 million tons (2025) | Mordor Intelligence | - |

| USD 4.20 billion (2024) | Global Consultancy A | Applies single global ASP, omits bead premium and regional mix differences |

| USD 2.29 billion (2023) | Industry Association B | Excludes agrochemical carriers, back-casts from 2019 tire data with straight CAGR |

The comparison shows that our disciplined scope selection, evidence-based variables, and regular refresh cadence give decision-makers a balanced, transparent baseline they can replicate with confidence.

Key Questions Answered in the Report

What is the current size of the precipitated silica market?

The precipitated silica market size reached 3.38 million tons in 2026 and is projected to hit 4.08 million tons by 2031.

Which region leads demand for precipitated silica?

Asia-Pacific holds 50.24% of global volume and is forecast to grow at 3.95% CAGR through 2031, driven by EV tire production and rice-husk-ash projects.

How fast is food-grade precipitated silica growing?

Food-grade volume is expanding at a 4.56% CAGR as brands pursue clean-label anti-caking alternatives approved by the FDA and EFSA.

What factor most impacts silica production costs today?

Tight sulfuric-acid supply has lifted variable costs by up to 68% in North America, pressuring wet-process margins.

Who are the top players in precipitated silica?

Evonik, Solvay, Quechen Silicon Chemical, W.R. Grace, and Cabot collectively hold about 47% of global capacity.

Page last updated on: