Power Amplifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.15 Billion |

| Market Size (2031) | USD 42.13 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

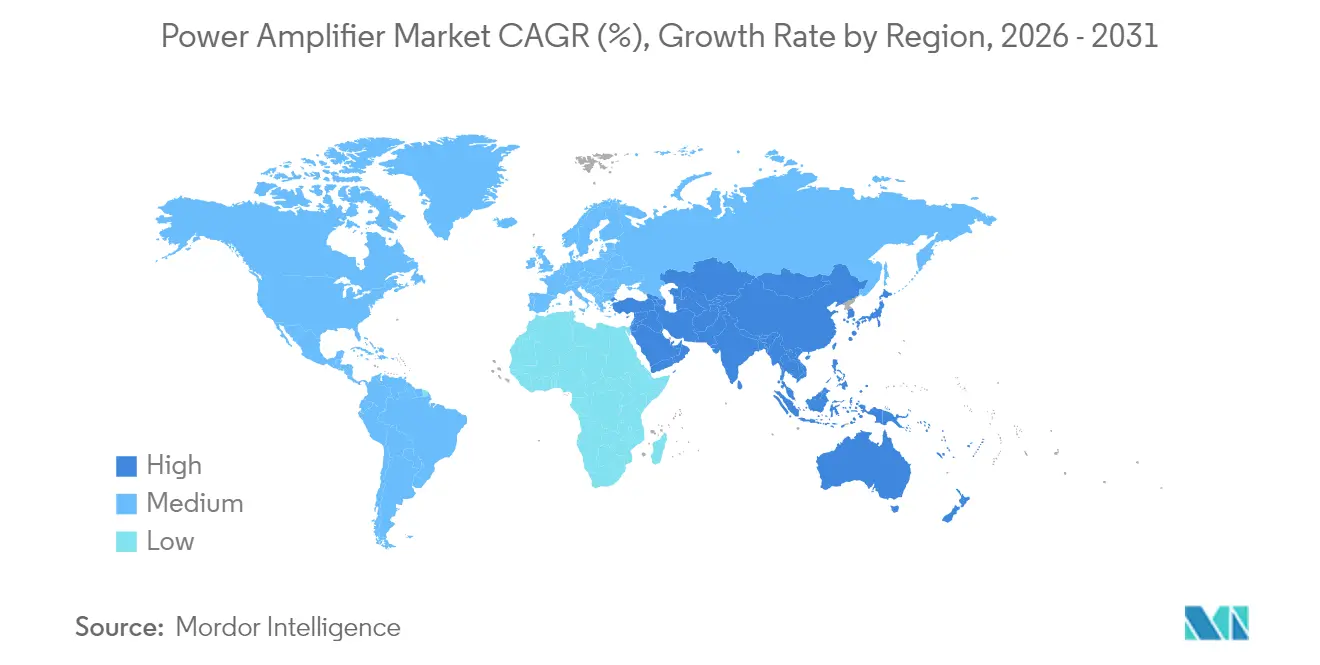

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Power Amplifier Market Analysis by Mordor Intelligence

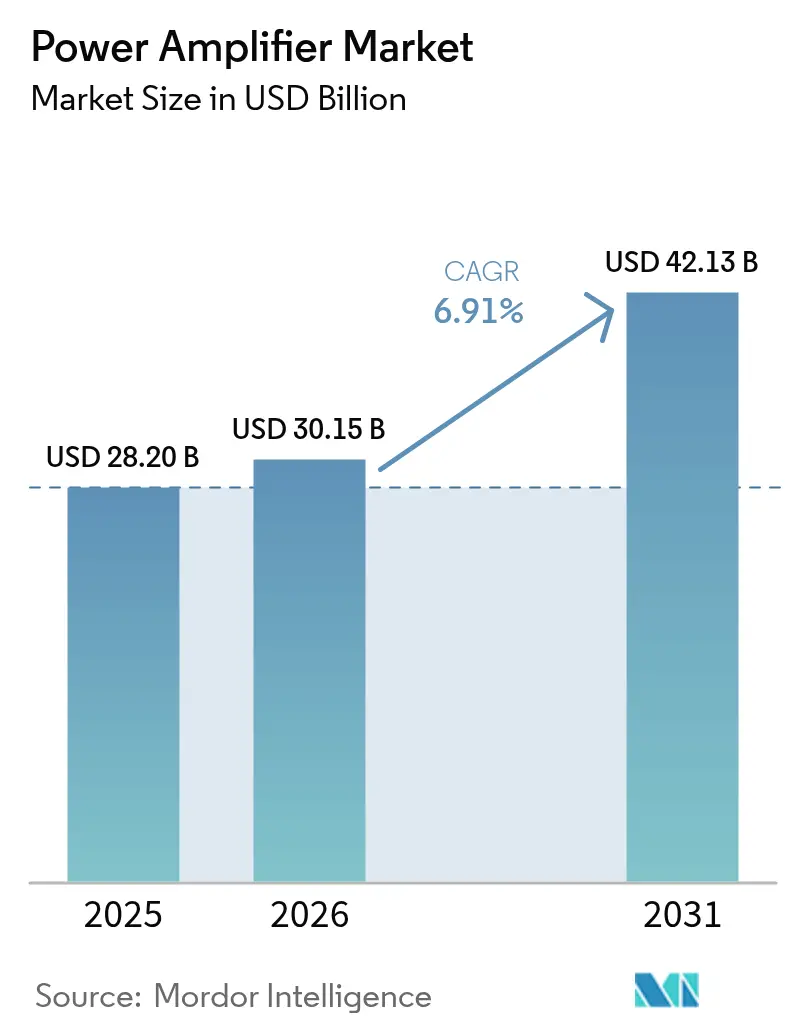

The power amplifier market size was valued at USD 28.20 billion in 2025 and estimated to grow from USD 30.15 billion in 2026 to reach USD 42.13 billion by 2031, at a CAGR of 6.91% during the forecast period (2026-2031). Rapid 5G roll-outs, expanding Wi-Fi 6/7 refresh cycles, and growing automotive demand for high-efficiency Class-D audio platforms have underpinned revenue expansion over the past year. GaN devices continued to displace legacy GaAs in macro-cell radios, offering higher power density and reduced energy consumption for operators. Meanwhile, Asia-Pacific kept its cost-leadership advantage in handset power-amplifier back-end assembly, enabling regional vendors to accelerate time-to-market for multi-band RF front ends. Mid-band spectrum (1–6 GHz) remained the performance-price sweet spot for both infrastructure and consumer electronics, yet mmWave amplifiers above 20 GHz recorded the fastest unit growth as satellite broadband and fixed-wireless access scaled in 2024 and early 2025.

Key Report Takeaways

- By geography, Asia-Pacific led with 48.12% revenue share in 2025; the Middle East and Africa are projected to expand at an 11.18% CAGR through 2031.

- By industry vertical, consumer electronics accounted for 37.98% of the power amplifier market share in 2025, while automotive is advancing at 11.86% CAGR to 2031.

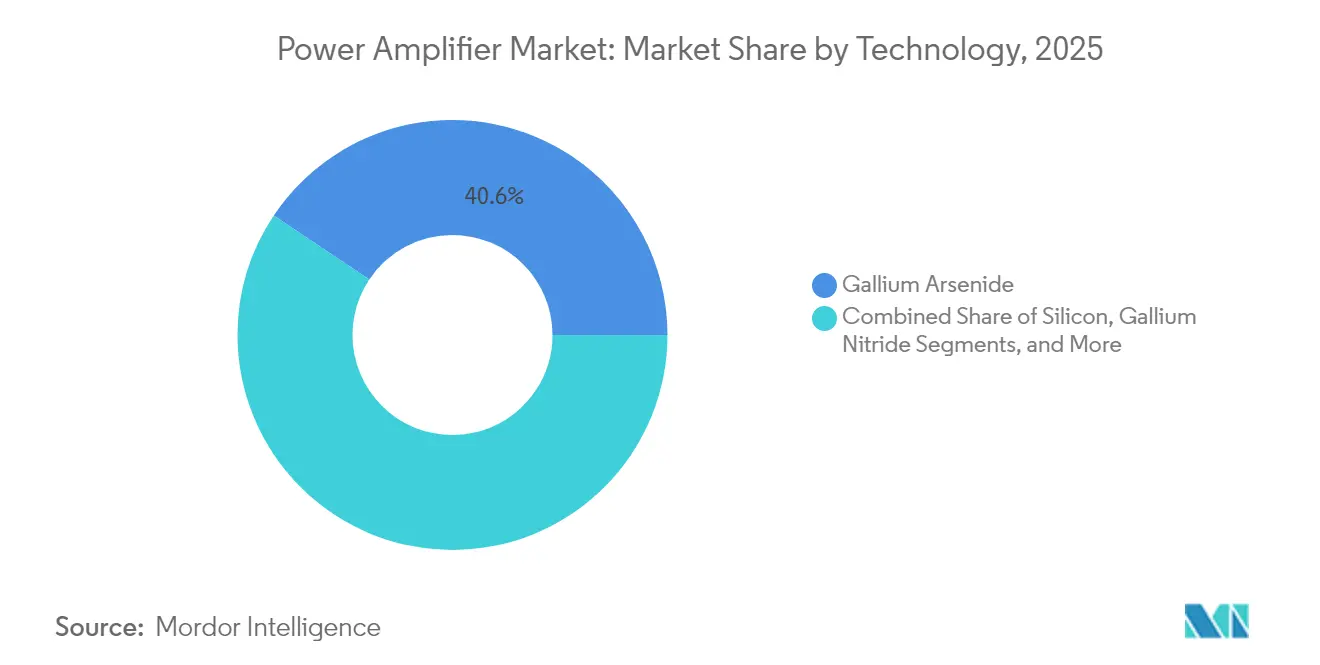

- By technology, GaAs held a 40.62% share in 2025; GaN is forecast to grow at a 16.92% CAGR over 2026-2031.

- By frequency band, 1 – 6 GHz accounted for 45.53% of the power amplifier market share in 2025, while the >20 GHz segment is set to post a 18.54% CAGR through 2031.

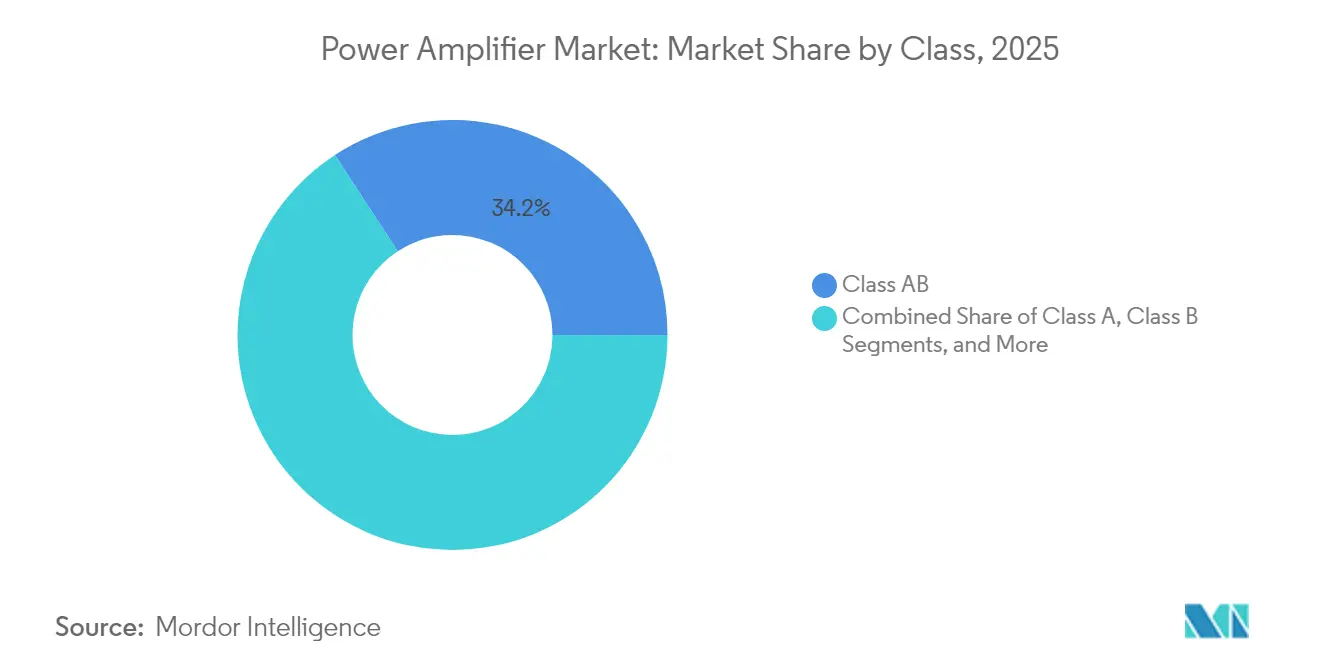

- By class, Class AB commanded 34.21% of the power amplifier market size in 2025; Class D is scaling at 13.49% CAGR.

- By product, RF/microwave amplifiers captured 56.85% revenue in 2025, whereas audio amplifiers are projected to rise at 9.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Power Amplifier Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GaN PAs in 5G massive-MIMO | +1.8% | East Asia, spillover to North America | Medium term (2-4 years) |

| Wi-Fi 6/7 router refresh | +1.2% | North America, Europe | Short term (≤ 2 years) |

| EV infotainment and ADAS Class-D audio | +0.9% | Europe, North America, China | Medium term (2-4 years) |

| LEO satellite Ku/Ka-band SSPAs | +1.3% | Global, strength in the Middle East and Africa | Long term (≥ 4 years) |

| Smart-factory RF heating | +0.7% | Germany, South Korea, Japan | Medium term (2-4 years) |

| O-RAN multi-vendor architectures | +1.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GaN PAs in 5G Massive-MIMO

Typical macro-cell radio units operating from 1.35 GHz to 7.6 GHz reported up to 38% drain efficiency in field deployments during 2024, cutting operating expenditure for carriers.[1]RFHIC Corporation, “RFHIC and MaxLinear Collaborate to Introduce High-Efficiency Power Amplifier Solution for 5G Macrocell Radio Units,” rfhic.com The smaller footprint of GaN die enabled denser antenna panels and simplified thermal layouts, allowing 64-T/64-R arrays to ship in volume for urban densification projects. Regional operators in Japan and South Korea capitalized on the efficiency gains to comply with carbon-reduction roadmaps, reinforcing procurement of GaN front-end modules across 2025 bid cycles. As costs per watt continue to fall, GaN penetration in the power amplifier market should approach parity with GaAs in macro-cells before 2028.

Wi-Fi 6/7 Router Refresh

Home and enterprise access-point vendors accelerated second-generation Wi-Fi 6 and early Wi-Fi 7 launches in 2024, requiring mid-power linear PAs capable of sustaining multi-link operation across 5 GHz and 6 GHz. Solutions such as AsiaRF’s AP7988-002 platform integrated a high-power front-end module that extended throughput to 19 Gbps, thereby lifting unit ASPs for RF front ends. In Q1 2025, HPE Aruba Networking released tri-band Wi-Fi 7 access points that improved aggregate capacity by 30%, intensifying demand for premium silicon with tighter EVM and adjacent-channel leakage specifications. This refresh cycle is set to keep the power amplifier market on a robust shipment trajectory through at least 2027.

EV Infotainment and ADAS Adoption of Class-D Audio PAs

Europe’s battery-electric vehicle (BEV) platforms adopted quad-bridge Class-D amplifiers such as STMicroelectronics’ FDA801, which delivers 93% efficiency at 50 W per channel and integrates a low-latency DAC. The devices support both immersive audio and warning-sound synthesis for driver-assistance functions. Tier-1 infotainment suppliers disclosed that moving from Class AB to Class D saved 0.5 kWh per 100 km drive cycle, a material figure given range anxiety. As BEV penetration climbs, automotive design wins are expected to elevate Class-D’s revenue share in the power amplifier market at a significant rate by 2030.

LEO Satellite Constellations Driving Ku/Ka-band SSPAs

Regional operators in the Middle East and Africa continued to invest in hundreds of Ku-band gateways paired with solid-state power amplifiers that offer mean-time-between-failures exceeding 100,000 hours. Gilat’s Endurance line replaced traveling-wave tube amplifiers at several teleport sites, reducing maintenance cost and improving linearity for high-order QAM. In parallel, MACOM began sampling a linearized Q-band GaN MMIC that pushes PAE above 25% at 45 GHz, paving the way for higher-throughput laser-com feeder links. With nearly 5,000 LEO craft launched during 2024-2025, Ku/Ka shipments are poised to anchor double-digit revenue growth in the high-frequency tier of the power amplifier market.

Restraints Impact Analysis of Power Amplifier Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GaAs wafer supply constraints | -0.8% | Global, focus on Asia-Pacific | Medium term (2-4 years) |

| EU Eco-Design idle-power caps | -0.6% | European Union | Long term (≥ 4 years) |

| Low-end CMOS PA price erosion | -0.5% | Global, Asia-Pacific | Short term (≤ 2 years) |

| Thermal limits on >28 GHz silicon PAs | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GaAs Wafer Supply Constraints Elevating BOM Costs

Gallium availability tightened in late 2024 after export-control measures constrained Chinese refinery output, inflating GaAs epi-wafer pricing by up to 18%. Multilayer RF front-end modules, therefore, faced higher bill-of-materials outlays, pressuring handset OEM margins and encouraging an accelerated pivot toward GaN-on-silicon processes. Finwave Semiconductor signed a foundry pact with GlobalFoundries to commercialize enhancement-mode GaN-on-Si for sub-6 GHz phones, aiming to neutralize GaAs cost volatility. While long-term diversification will damp inflationary risk, short-run sourcing difficulties are trimming the headline CAGR of the power amplifier market by nearly one percentage point.

EU Eco-Design Idle-Power Caps on Audio PAs

Revised Eco-Design directives effective 2024 mandated idle-power draw below 1 W for consumer and commercial audio gear sold in the European Economic Area. Vendors such as Extron updated Class-D network amplifiers with Eco Standby modes that attain 0.5 W quiescent consumption without compromising rapid wake-up. Compliance engineering costs and requalification testing have lengthened product-development cycles, limiting smaller brands’ ability to compete and tempering unit demand in legacy Class AB channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Power Amplifier Market Segment Analysis

By Technology:

GaN Disrupts GaAs DominanceGaAs devices retained a 40.62% revenue position in 2025 on the strength of entrenched 1–6 GHz handset sockets, yet GaN shipments surged on macro-cell roll-outs and Ku-band gateways. GaN’s 16.92% CAGR through 2031 is projected to lift its portion of the power amplifier market size for radio-access infrastructure to almost half by the end of the forecast window. Qorvo documented a 15 °C reduction in junction temperature at identical output power after migrating a 3.5 GHz Doherty stage to GaN-on-SiC, validating cost-of-ownership savings for operators.

Silicon-germanium remained integral to phased-array beamforming cores, whereas bulk CMOS stayed relevant in low-power Bluetooth and Wi-Fi IoT nodes. Research at IMEC on GaN MISHEMT bias stability removed gate-lag barriers that previously capped drain efficiency above 30 GHz, clearing a pathway for GaN proliferation in handset mmWave modules. Emerging GaN-on-diamond substrates promise further thermal headroom, a key enabler for subsequent 6G and X-band radar design-ins.

By Product:

RF/Microwave Amplifiers Lead Market ShareRF and microwave categories generated 56.85% of 2025 revenue, anchored by 5G macros, small cells, and satcom earth stations. Filtronic shipped Ku-band GaN MMICs rated at 80 W that outperformed preceding GaAs line-ups by 40% PAE, unlocking more compact array apertures. Audio power amplifiers contributed a smaller but fast-growing slice: proliferation of smart-speakers and multi-driver in-vehicle entertainment lifted shipments, and GaN FETs removed dead-time limitations that constrained silicon MOSFET fidelity in high-power class-D boards.

Industrial and scientific RF generators for plasma and heating also elevated SiC and GaN transistor demand. Texas Instruments expanded its wideband LDMOS pre-driver catalog to service industrial laser and MRI magnet power stages, reinforcing the RF product category’s role as the revenue mainstay of the power amplifier market.

By Frequency Band:

Mid-Band Dominates, mmWave SurgesThe sub-6 GHz tier controlled 45.53% of 2025 turnover, given ubiquitous LTE and early 5G mid-band allocations. Nevertheless, the >20 GHz bracket is forecast to register a 18.54% CAGR, adding disproportionate value to the power amplifier market share in satellite backhaul and fixed-wireless access. Qorvo’s TGA4548-SM MMIC showed 25% PAE at 18 GHz while delivering 10 W saturated power, marking a step forward for airborne X-band radars. GaN-on-diamond evaluations conducted by academic consortia recorded thermal conductivity near 1,700 W/m·K, twice that of SiC, paving the way for 40 GHz and higher nodes under the 6G agenda.

Below-1 GHz remained vital for NB-IoT asset tracking and utility metering, but revenue upside appeared capped owing to ASP compression. Bands spanning 6–20 GHz gained modest lift from point-to-point microwave links that decongested fiber-scarce rural backbones.

By Class:

Class AB Balances Performance and EfficiencyClass AB retained leadership at 34.21% of 2025 sales as its linearity metrics satisfied adjacent-channel leakage masks in cellular handsets. Design wins spanned 700 MHz paging to 5 GHz Wi-Fi router boosters. In contrast, Class D’s 13.49% CAGR is converting automotive and smart-speaker sockets at speed; Extron’s NetPA Ultra amplifier family demonstrated 77% efficiency in a Dante-enabled rack unit, underlining the class’s green credentials.

High-efficiency switch-mode topologies like Class E/F continued to surface in wireless-power transmitters and energy-harvester blocks, but their aggregate revenue remained niche.

By Industry Vertical:

Consumer Electronics Leads, Automotive AcceleratesHandsets, tablets, and wearables sustained 37.98% of 2025 turnover, ensuring the consumer-electronics vertical’s primacy in the power amplifier market. Device OEMs incorporated dual-connectivity front-end modules (5G + Wi-Fi 7) that increased RF content per unit by 12% year on year, boosting silicon demand. Skyworks forecasted a 15% jump in 5G attach rates for mid-priced phones, reinforcing its mobile revenue pipeline.

Automotive contributed the fastest growth at 11.86% CAGR, shaped by EV infotainment and radar domain controllers that require multi-die cascade amplifiers with low phase noise. Microchip underscored that premium SUV trims deploy up to 20 audio channels at 50 W each, a material uplift from 2023 figures. Industrial adoption rose alongside Industry 4.0 retrofits that swapped magnetrons for solid-state RF heaters, while telecom operators continued to drive infrastructural volume.

Geography Analysis

APAC Power Amplifier Market

Asia-Pacific generated 48.12% of global revenue in 2025, anchored by China’s handset assembly corridors, which consumed more than half of the region’s low-band GaAs die. Korean fabs leveraged vertical integration to ramp 5G RF front ends, while Japanese material suppliers expanded SiC wafer output to mitigate GaN substrate gaps. India’s production-linked incentives for smartphone EMS houses widened domestic demand, creating a nascent yet vibrant cluster of RF test and packaging firms. Over the near term, Asia’s policy emphasis on indigenous compound-semiconductor supply chains is positioned to strengthen regional control over the power amplifier market.

North America Power Amplifier Market

North America ranked second by value. Dominant players such as Qorvo, Broadcom, and Wolfspeed exploited patent portfolios in GaN power density and thermal packaging to capture new defense and 5G O-RAN awards. The Pentagon’s radar-modernization programs adopted X-band GaN tiles, pushing device ASPs significantly above commercial grades. Telecom operators remained central buyers, upgrading mid-band carriers to 64T/64R arrays in dense urban clusters.

Europe Power Amplifier Market

Europe’s share centered on Germany and France, where automotive and aerospace manufacturers absorbed high-linearity PAs for in-cabin audio, ADAS, and multi-band sat-comms. The EU Eco-Design idle-power regulation prompted a swift transition toward Class-D, creating a temporary mismatch between legacy inventory and new-build specs. United Kingdom fabs explored GaN-on-diamond epitaxy through public-private consortia to retain competitiveness against Asian peers.

MEA and South America Power Amplifier Market

The Middle East and Africa region, though smaller, exhibited the fastest growth at an 11.18% CAGR, fueled by Ka-band teleport expansion and sovereign LEO connectivity programs. National operators in Saudi Arabia and Nigeria earmarked capex for gateways that integrate 40 W Ku-band SSPAs, broadening the addressable slice of the power amplifier market. South America followed with moderate uptake, led by Brazil’s 5G mid-band auctions and state-backed rural broadband.

Regulatory Landscape

Power-amplifier shipments for RF devices are shaped by market-access rules around RF emissions and equipment authorization. In the United States, FCC equipment authorization requirements under 47 CFR Part 2 and Part 15 govern marketing and operation of RF devices, and 47 CFR 2.815 restricts the marketing, sale, or import of external RF power amplifiers capable of operation below 144 MHz unless they have a grant of certification. This shapes how vendors position discrete and module offerings into end equipment.

Trade compliance is also tightening for advanced compound-semiconductor devices used in high-performance RF power stages. In May 2026, the U.S. Department of Commerce Bureau of Industry and Security (BIS) published a temporary final rule adding certain thermally enhanced QFN-packaged GaN power modules to the Export Administration Regulations (EAR) control framework. In July 2026, BIS issued an interim final rule that brought 1200 V and higher SiC MOSFETs into the EAR Appendix E1 control list, increasing licensing friction for exports to China and select emerging markets. In Europe, the Radio Equipment Directive (2014/53/EU) continues to apply to radio equipment and active antennas with embedded amplifiers, and Delegated Regulation (EU) 2026/339 updates the RED framework with provisions tied to cybersecurity, personal data protection, and network integrity, adding compliance workload for connected radio products that integrate RF front ends and PAs.

Value Chain Analysis

The power amplifier value chain starts with raw materials and substrates (gallium, arsenic, SiC boules, and silicon), then moves to epi growth and wafer fabrication (GaAs, GaN-on-SiC, GaN-on-Si, SiGe, and CMOS), followed by device fabrication, test, and advanced packaging (multi-chip modules, front-end modules, and thermally enhanced packages). Assembly, RF calibration, and system integration are downstream with OEMs and tiered integrators across smartphones, Wi-Fi access points, 5G radios (including O-RAN), automotive infotainment and radar, and satellite ground equipment, after which distribution flows through direct sales and authorized channel partners.

Wide-bandgap supply is increasingly constrained by substrate and epi capacity, particularly low-defect GaN-on-SiC wafer availability, while GaAs input-cost volatility has also shown up in the chain. Product and platform moves in 2026 reflect a shift toward higher integration and faster design cycles: Ampleon introduced a fully integrated 70 W GaN Doherty PA module with integrated bias control for 5G massive MIMO, WIN Semiconductors qualified a 40 V GaN-on-SiC platform (NP12-0B) to increase power density for RF front ends, and UMS launched a 27.5-31 GHz Ka-band GaN-on-SiC high-power amplifier. Foundry enablement and device R&D feed this pipeline as well, including Fujitsu reporting 74.3% power conversion efficiency at 8 GHz on GaN-on-SiC HEMT PA technology for future FR3-oriented systems.

Competitive Landscape

Five leading vendors, Broadcom, Qorvo, Skyworks Solutions, Murata Manufacturing, and Infineon Technologies, collectively held the majority of the global revenue share in 2024. Their scale advantages stemmed from captive epi-growth, wafer processing, and multi-chip module integration that compressed cost curves. Broadcom extended GaN Doherty PAs into cable infrastructure, while Qorvo deepened GaN-on-SiC capacity through its Richardson, Texas, fab expansion. Skyworks widened participation by aligning with Chinese handset OEM reference designs, countering aggressive low-end CMOS entrants.

White-space disruptors exploited architectural shifts. Falcomm introduced Dual-Drive™ architectures that posted theoretical 78.5% efficiency at 28 GHz, signaling a potential inflection in mmWave design economics. Finwave’s enhancement-mode GaN-on-Si roadmap targeted handset sockets historically dominated by GaAs. At the systems level, open-ran macro-cells opened procurement to specialized PA vendors, eroding incumbent share and intensifying competition on linearity-plus-efficiency benchmarks.

Thermal-management innovation remained a prime battleground. Research consortiums demonstrated GaN-on-diamond junction resistance below 0.25 K mm²/W, enabling 10 W mmWave die within smartphone footprints.[4]Journal of Semiconductors, “GaN-on-Diamond Technology for Next-Generation Power Devices,” springer.com Vendors pairing material advances with digital predistortion ASICs secured premium margins in defense and satellite. Price competition persisted at the low-power Bluetooth tier, with Chinese fabless companies pushing single-band CMOS PAs below USD 0.05 in high volume.

Power Amplifier Industry Leaders

-

Broadcom Inc.

-

Qorvo Inc.

-

Skyworks Solutions Inc.

-

Qualcomm Technologies Inc.

-

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Power Amplifier Market Companies Covered in this Report

- Broadcom Inc.

- Qorvo Inc.

- Skyworks Solutions Inc.

- Qualcomm Technologies Inc.

- Infineon Technologies AG

- Texas Instruments Inc.

- Analog Devices Inc.

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Renesas Electronics Corp.

- Wolfspeed Inc.

- MACOM Technology Solutions Inc.

- ON Semiconductor Corp.

- Microchip Technology Inc.

- Rohm Semiconductor

- Panasonic Corp.

- Murata Manufacturing Co. Ltd.

- Mini-Circuits

- CAES (Cobham Advanced Electronics)

- Sumitomo Electric Device Innovations

- Empower RF Systems

- Falcomm Inc.

- Finwave Semiconductor Inc.

Market Opportunities and Future Outlook

A key whitespace is emerging at the intersection of higher-frequency radios and thermally constrained form factors, where efficiency, linearity, and packaging shape adoption decisions more than transistor cost alone. mmWave and satellite payload and gateway builds are pulling more value into the >20 GHz tier, which also raises demand for advanced thermal solutions (for example, GaN-on-SiC today and GaN-on-diamond research referenced across the ecosystem) and for modules that reduce system bring-up time through built-in monitoring and bias control. In parallel, the EU Eco-Design idle-power cap (effective 2024) continues to favor architectures and control features that reduce standby consumption in audio amplification, creating room for differentiated Class-D platforms and networked audio products that can demonstrate low quiescent power while meeting performance targets.

On the supply and commercialization side, opportunities center on vendors that can combine device performance with manufacturability and compliance-ready productization. Market signals include Ampleon releasing an integrated 70 W GaN Doherty PA module for massive MIMO base stations with integrated bias control (2026) and WIN Semiconductors qualifying a 40 V GaN-on-SiC process platform for higher power density RF designs (2026). These moves shorten OEM design cycles and raise content per radio. Early 6G and advanced radar work also supports FR3 and X-band development paths, and Fujitsu reported 74.3% power conversion efficiency at 8 GHz on GaN HEMT technology (March 2026). That result reinforces an engineering route for higher-efficiency RF power stages where energy use and thermal headroom are becoming gating constraints for infrastructure and defense programs.

Recent Industry Developments in Power Amplifier Market

- July 2026: Apple announced a multiyear commitment exceeding USD 30 billion with Broadcom to expand US manufacturing of RF components, including at facilities in Fort Collins, Colorado, alongside a planned USD 1.5 billion capital expenditure. The announcement supports domestic supply assurance for critical RF content used in connectivity platforms that rely on high-performance power amplifier chains and adjacent front-end components.

- June 2026: Ampleon launched the G1M3438P70C, a fully integrated 70 W GaN Doherty power amplifier module for 5G massive MIMO base stations with integrated bias control. By embedding bias control at the module level, the design reduces radio OEM integration effort and supports faster time-to-market for high-power macro radio upgrades.

- April 2025: HPE Aruba Networking released tri-band Wi-Fi 7 access points that raised aggregate wireless capacity by about 30% and required upgraded mid-power RF amplification across 5 GHz and 6 GHz operation. The product cycle increased demand for tighter linearity and efficiency in access-point PA designs, supporting higher-value RF front-end content in enterprise Wi-Fi refreshes.

Power Amplifier Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers power amplifier devices and modules that boost an electrical or RF signal to a usable output level inside end equipment, spanning consumer electronics, telecom, industrial systems, automotive electronics, and defense-grade applications.

Scope exclusions: The sizing excludes standalone low-power driver or pre-amplifier ICs that only condition signals and are not used as power amplification stages in an end application.

Segments Covered in This Report

-

By Technology

- Silicon (Si)

- Gallium Arsenide (GaAs)

- Gallium Nitride (GaN)

- Silicon Germanium (SiGe)

- Complementary MOS (CMOS)

- Other Technologies

-

By Product

- Audio Power Amplifiers

- RF / Microwave Power Amplifiers

-

By Frequency Band

- < 1 GHz

- 1 – 6 GHz

- 6 – 20 GHz

- > 20 GHz

-

By Class

- Class A

- Class B

- Class AB

- Class D

- Class E/F and Other Classes

-

By Industry Vertical

- Consumer Electronics

- Industrial

- Telecommunications

- Automotive

- Other Industry Verticals

-

By Geography

-

North America

- United States

- Canada

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Sweden

- Denmark

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the market and to keep assumptions tied to observable indicators. We referenced public sources such as the International Telecommunication Union for connectivity indicators, the Federal Communications Commission for spectrum and network-related releases, the United States International Trade Commission for trade classifications and import signals, and the International Energy Agency for energy efficiency context that influences power device choices. Where useful, we also used patent databases to track materials and architecture shifts, such as GaN-related filings, and peer-reviewed journals to sanity-check typical performance ranges by band and output class.

To translate those signals into a workable sizing model, we reviewed company filings, annual reports, investor presentations, and press releases for product mix cues and capacity-related statements. A paid subscription focused on company financials and news was applied selectively to cross-check revenue timelines and corporate actions, and an import and export shipment-level database was used in a limited way to validate directional flows for electronics categories linked to amplifier-containing modules. The desk sources listed here are illustrative only, and many other public references were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work helped us confirm what is actually counted in purchasing and design decisions, and to test the share of demand coming from telecom, consumer audio, automotive electronics, industrial RF, and defense programs. We spoke with a mix of component suppliers, module integrators, distributors, and downstream OEM-facing roles across major geographies so gaps from public data could be closed, and then key inputs could be triangulated before the totals were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 19% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 35% |

| Smaller Players: 22% | Managers: 48% | Americas: 20% |

Market-Sizing & Forecasting

The core model is built using a top-down approach, where end-demand pools are reconstructed from application activity and adoption levels, and then converted into power amplifier value using typical content and pricing logic. For power amplifiers, the main inputs we track include smartphone and consumer audio device shipments, telecom network rollouts and radio upgrades, vehicle production trends tied to infotainment and connectivity, defense communications procurement signals, and the ongoing shift in materials, for example GaN adoption in higher frequency and higher efficiency designs. When those drivers are stable, they anchor the demand curve, and when they move, the model is adjusted in a traceable way.

To avoid relying on a single calculation path, results are corroborated with selective bottom-up approximations, such as sampled average selling price bands multiplied by estimated unit volumes for key applications, plus channel checks on how product mix is shifting between RF, audio, and power conversion use cases. When a bottom-up input is missing for a region or niche application, we apply proxy ratios from comparable end markets and then pressure-test them during follow-up calls. For forecasting, scenario analysis is used so different rollout speeds for wireless infrastructure and different consumer device cycles can be reflected, and then the final trajectory is aligned to the consensus range heard from practitioners on expected volume and pricing progression.

Data Validation & Update Cycle

Validation is done through multiple checks so that outliers are caught early and corrected with evidence. We compare model outputs against independent signals such as device shipment momentum, network deployment timelines, and trade movements for relevant electronics categories, and then reconcile any large variance before sign-off. If an assumption is driving an unusual swing, it is flagged, reviewed by another analyst, and then re-checked through targeted re-contacts with industry participants.

The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp changes in end-market shipments, major policy actions affecting spectrum and telecom spending, or notable technology shifts that impact pricing. Before delivery, a final review pass is completed so the latest public releases and interview learnings are reflected in the numbers clients receive.

Mordor Intelligence's Power Amplifier Market Size Versus Other Published Estimates

Published market values for power amplifiers can look far apart even when they sound like they cover the same products. The spread usually comes from differences in what is counted as a power amplifier, the mix of end uses included, how pricing is moved over time, and how often assumptions are refreshed.

Some sources fold a wider set of amplification components into the same bucket, and they may apply faster pricing expansion tied to technology shifts without re-checking the implied unit volumes. In contrast, the estimate from Mordor Intelligence is kept to power amplification stages used in end equipment and it excludes standalone low-power driver or pre-amplifier ICs, with pricing trends pressure-tested against shipment and deployment signals before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 30.15 B (2026) | |

| Global Consultancy A | USD 45.85 B (2026) | Uses a broader definition that appears to include adjacent amplifier and driver categories, and the implied pricing and mix shifts are more aggressive for the same base year, which can lift the total without matching volume checks. |

| Industry Publisher B | USD 40.79 B (2025) | Anchors on a different base year and likely counts a wider set of amplifier types across audio and RF, and currency timing plus faster assumed ASP progression can increase the stated value compared with a tighter power-stage-only count. |

The table shows that scope choices and price progression logic explain most of the gap, not just forecast optimism. By keeping the counted device set consistent and then validating demand drivers like device shipments and telecom rollouts, our sizing stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the power amplifier market?

The power amplifier market was valued at USD 30.15 billion in 2026 and is projected to reach USD 42.13 billion by 2031.

Which region holds the largest power amplifier market share?

Asia-Pacific led with 48.12% of global revenue in 2025, driven by robust electronics manufacturing and aggressive 5G deployments.

Why are GaN devices gaining adoption over GaAs?

GaN offers higher power density, improved thermal performance, and better efficiency, helping operators reduce energy costs and shrink radio footprints.

Which industry vertical is expanding fastest within the power amplifier market?

Automotive is growing at a 11.86% CAGR through 2031 due to rising demand for high-efficiency Class-D audio and radar systems in electric vehicles.

How will EU Eco-Design rules impact amplifier vendors?

New idle-power caps below 1 W force redesigns toward more efficient standby modes, increasing engineering complexity but favoring Class-D architectures.

What is the growth outlook for mmWave (>20 GHz) power amplifiers?

MmWave segments are forecast to grow at 18.54% CAGR as LEO satellite constellations and fixed-wireless access drive demand for high-frequency PAs.

Page last updated on: