Potting Compound Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 34.19 Billion |

| Market Size (2031) | USD 40.12 Billion |

| Growth Rate (2026 - 2031) | 3.25% CAGR |

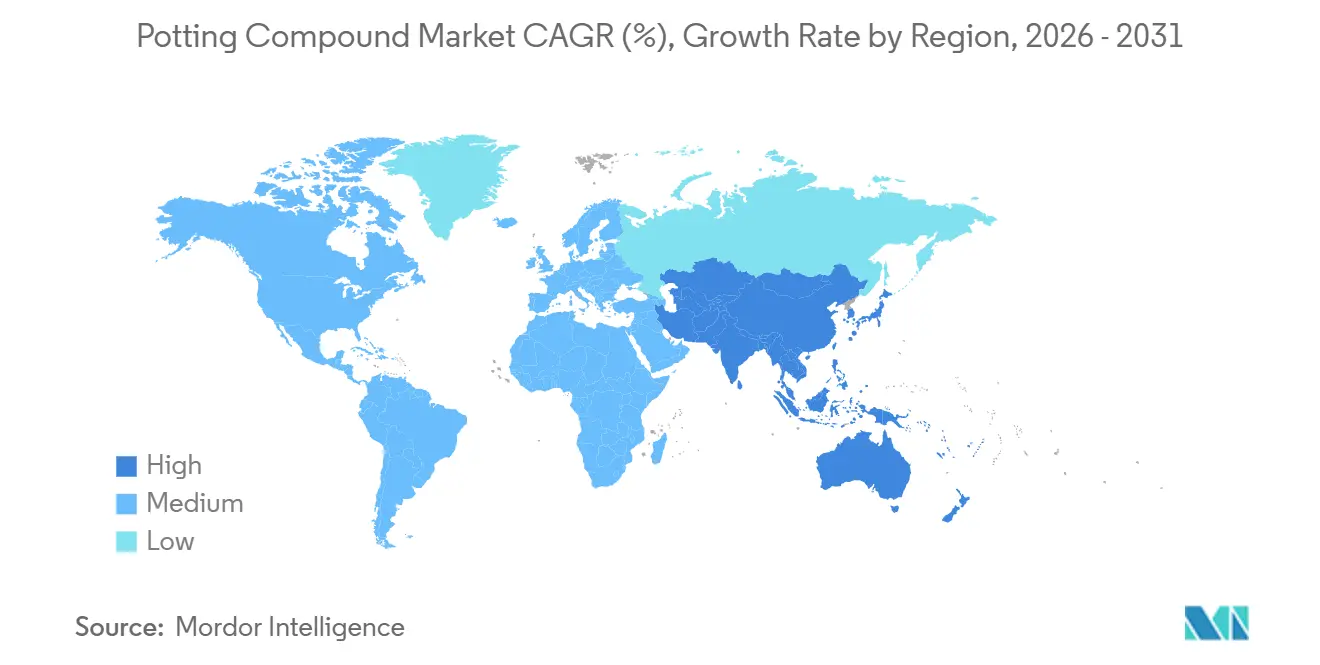

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Potting Compound Market Analysis by Mordor Intelligence

The Potting Compound Market size is expected to grow from USD 33.11 billion in 2025 to USD 34.19 billion in 2026 and is forecast to reach USD 40.12 billion by 2031 at 3.25% CAGR over 2026-2031. Demand tracks the electrification of mobility, the densification of consumer devices, and the expansion of offshore wind farms, all of which impose higher thermal-management and reliability thresholds on encapsulation materials. OEMs are shifting from cost-driven epoxies toward thermally conductive silicone and polyurethane hybrids that dissipate ≥200 W/mK, a change most visible in EV traction inverters and 1,500-volt wind converters. Asia-Pacific drives volume, holding 42.77% of 2025 revenue, as Chinese smartphone assemblers and South Korean semiconductor packagers demand sub-millimeter potting precision. Electronics remains the largest and fastest-growing end-user, benefiting from 5G infrastructure build-outs and edge-computing nodes that favor low-CTE, high-thermal-conductivity chemistries. At the same time, regulators tighten VOC ceilings and REACH-listed substances, accelerating the pivot to water-borne and 100%-solids formulations and rewarding suppliers that invest in low-emission chemistries.

Key Report Takeaways

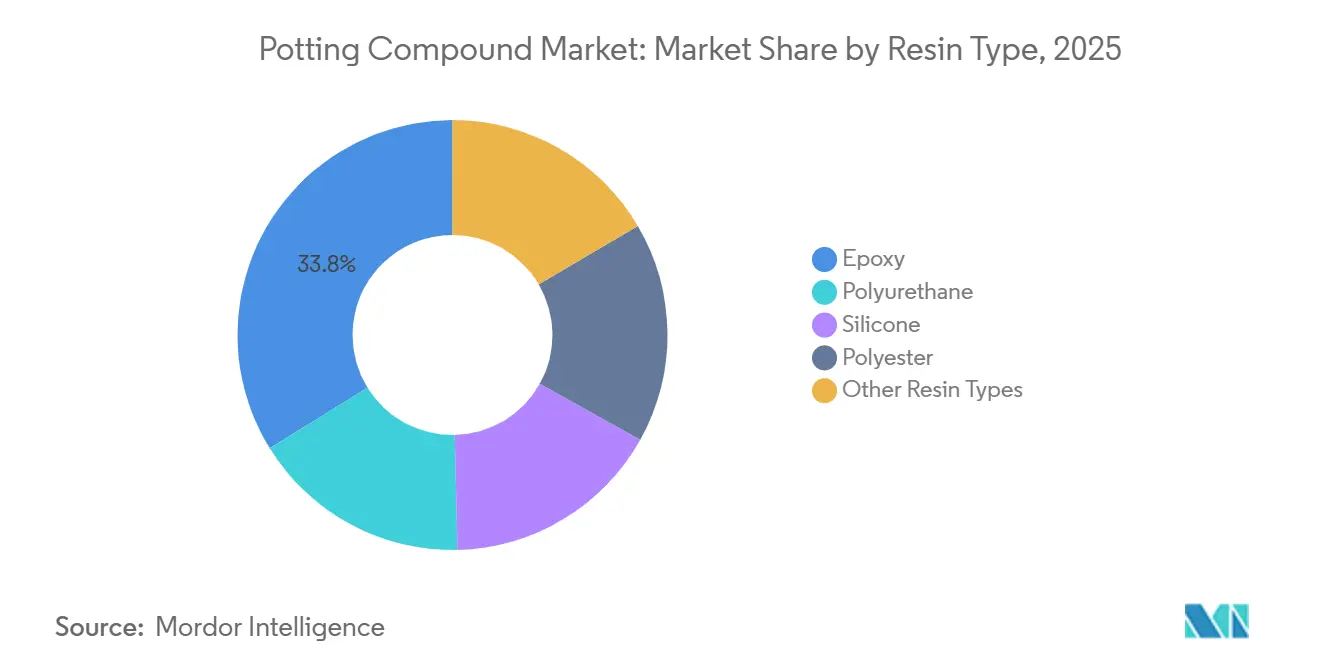

- By resin type, epoxy led with 33.81% revenue share in 2025; silicone is projected to advance at a 4.26% CAGR through 2031.

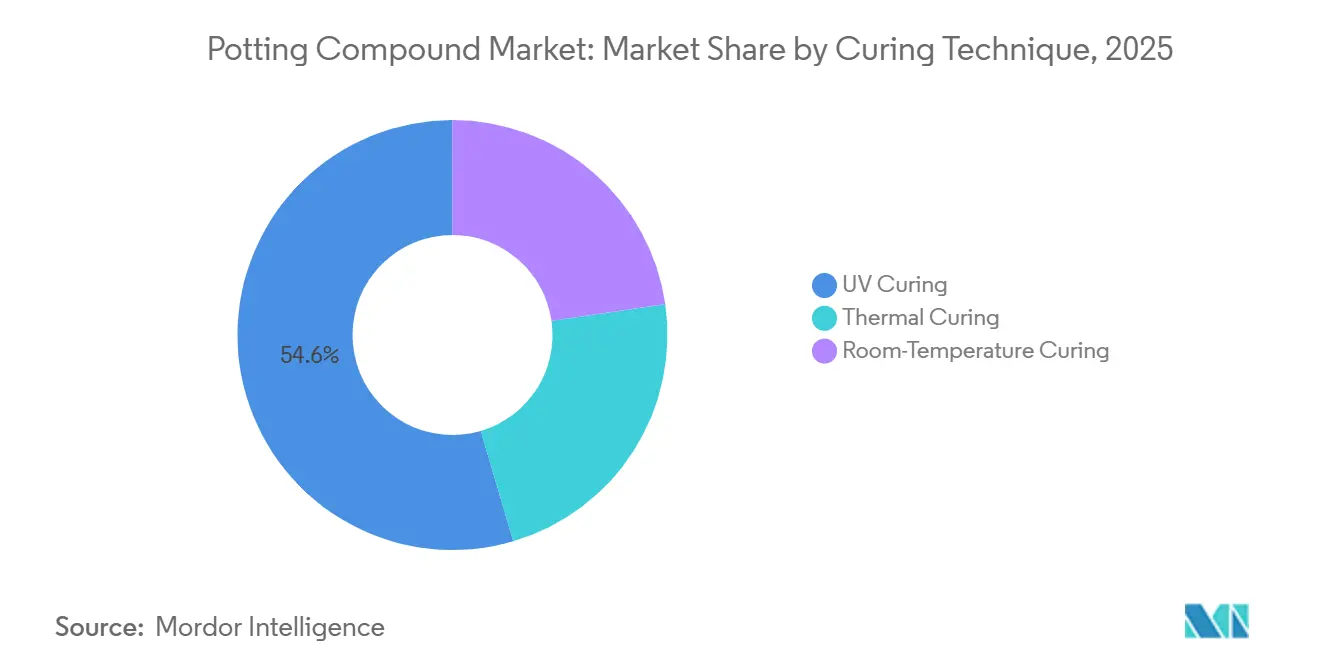

- By curing technique, UV curing held 54.56% share in 2025, while thermal curing records the highest projected CAGR at 4.19% through 2031.

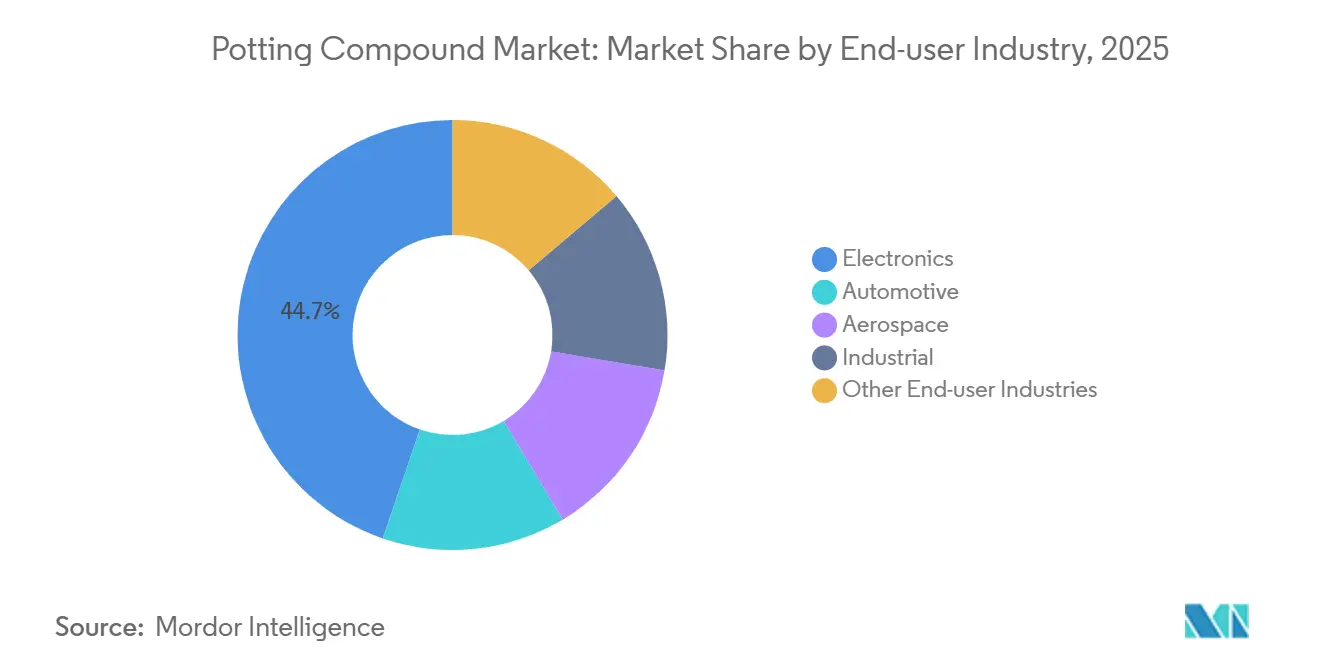

- By end-user industry, electronics accounted for 44.74% share of the potting compound market size in 2025 and is set to grow at a 4.45% CAGR through 2031.

- By geography, Asia-Pacific dominated with 42.77% revenue share in 2025 and is poised to expand at a 3.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Potting Compound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturisation of High-Density Consumer Electronics in Asia | +0.8% | Asia-Pacific core, spillover to North America | Short term (≤ 2 years) |

| Rapid Adoption of Power Electronics in EV Battery Packs | +1.1% | Global, with early gains in China, Europe, North America | Medium term (2-4 years) |

| Aerospace Shift to More-Electric Aircraft Platforms in North America | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Investments in Offshore Wind-Turbine Power Electronics | +0.5% | Europe core, APAC coastal regions | Medium term (2-4 years) |

| Rise of Thermally-Conductive Formulations for SiC Traction Inverters | +0.9% | Global, concentrated in automotive hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Miniaturisation of High-Density Consumer Electronics in Asia

Smartphone and wearable brands now engineer cavities below 5 mm³, compelling formulators to deliver sub-100-micron viscosity profiles that fill void-free at room temperature. Samsung’s 2025 foldable hinges embed 47 components in a 12 mm × 8 mm × 3 mm volume, forcing epoxies to cure below 80 °C to avoid flex-PCB warpage. Apple’s A18 chip drives thermal-design-power densities past 15 W/cm², so potting compounds carry more than 60 wt% ceramic filler to channel heat into an aluminum frame. Shenzhen contract manufacturers report cycle-time reductions from 45 minutes to less than 20 minutes after switching to UV-curable acrylate systems, which eliminate oven bottlenecks. IPC-HDBK-830 compliance further mandates ≤0.1% water absorption, protecting moisture-sensitive components in humid climates. As a result, electronics already consume 44.74% of global demand and are on pace to widen that lead through 2031.

Rapid Adoption of Power Electronics in EV Battery Packs

EV manufacturers transition battery housings from passive structures to active thermal-management modules that double as crash-energy absorbers. Tesla’s 4680 cell packs rely on a 3.5 W/m·K polyurethane potting compound to bond cylindrical cells into structural panels, meeting UL 94 V-0 flame rating while shaving vehicle mass. BYD’s Blade Battery employs flame-retardant epoxy compliant with GB 38031 to control thermal-runaway propagation. European OEMs favor silicone potting for 800-volt architectures because dielectric strength remains more than 20 kV/mm after 2,000 thermal cycles from -40 °C to 125 °C. The U.S. DOE funded USD 12 million of R&D into self-healing potting compounds that restore isolation after micro-cracking, targeting 30% warranty-claim cuts. ISO 26262 validation under six-month accelerated aging adds differentiation for large formulators that can finance extensive reliability testing.

Aerospace Shift to More-Electric Aircraft Platforms in North America

Next-generation narrow-body platforms will electrify primary flight controls and environmental systems, embedding potting compounds that withstand pressure cycling to 43,000 feet. Honeywell’s 2025 fly-by-wire controllers replaced silicone with flame-retardant polyurethane, slicing unit weight by 18% while meeting FAA FAR 25.853. Lockheed Martin’s 2024 F-35 avionics upgrade adopted conformal potting that cures to Shore D 75, protecting mission computers from 20 Grms vibration during carrier landings. AFRL funds research into impedance-sensing nanoparticles for predictive maintenance, embedding health monitoring directly into encapsulants. RTCA DO-160G salt-fog and thermal-shock requirements narrow the approved supplier list, concentrating aerospace volume among a handful of certified vendors.

Investments in Offshore Wind-Turbine Power Electronics

15-MW turbines expose nacelle converters to chloride-rich environments and 30-bar pressures. Siemens Gamesa’s SG 14-236 DD installs silicone potting that meets IEC 60068-2-52 salt-mist testing, enabling 25-year maintenance-free service. Orsted traced 9% of legacy fleet downtime to epoxy-potting failures and began retrofitting polyurethane systems offering superior hydrolytic stability. Vestas partnered with Dow in 2026 to infuse graphene, targeting a 40% junction-temperature drop and converter efficiency of 97.8%. The EU earmarked EUR 800 million for subsea converter stations, expanding demand for deep-water-rated encapsulants. DNV-GL certification cycles now span 18 months, elevating the compliance hurdle for market entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Feedstock Pricing (BPA, Epichlorohydrin, Silicone Monomers) | -0.6% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stringent Global VOC and REACH Regulations | -0.4% | Europe core, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Recycling Challenges for Multi-Component Potting Waste Streams | -0.3% | Global, most acute in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Feedstock Pricing (BPA, Epichlorohydrin, Silicone Monomers)

BPA prices in Asia spiked 28% in H1 2025 after a phenol-plant force majeure in Taiwan, and formulators absorbed 60% of the increase to protect automotive contracts. A fire at Solvay’s Belgian unit halved European epichlorohydrin supply, doubling prices to EUR 2,400/ton. Chinese export limits on metallurgical silicon trimmed global dimethyldichlorosilane availability by 12%, stretching silicone lead times to 12 weeks. Huntsman reported a 180-basis-point margin erosion in Q3 2025, prompting reformulation toward lower-cost polyurethane. Three European SMEs exited the market in 2025, consolidating share among larger players.

Stringent Global VOC and REACH Regulations

The EU added four epoxy precursors to its SVHC list in 2024, forcing authorization dossiers by 2027 or market exit[1]European Chemicals Agency, “REACH SVHC Updates 2024,” Echa.europa.eu . The U.S. EPA caps VOCs at 420 g/L from January 2026, disqualifying 30% of legacy epoxies. Henkel invested EUR 45 million retrofitting water-borne lines, yet early trials show 20% adhesion loss on polycarbonate, requiring plasma pre-treatment. California’s SCAQMD tightens the limit to 250 g/L, effectively banning solvent-borne products in the Los Angeles basin. Compliance costs weigh heavier on regional formulators, accelerating consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Gains as Thermal Demands Intensify

Epoxy retains 33.81% of 2025 revenue, yet silicone is forecast to be the fastest-growing category, expanding 4.26% annually through 2031, as EV inverters and offshore wind converters demand wide-temperature flexibility and low modulus. Polyurethane sits between the two, valued for impact resistance in automotive sensors and outdoor LED drivers. Polyester retains niche share in low-cost consumer goods, and early bio-based variants aim to satisfy sustainability mandates. Hybrid chemistries - epoxy-silicone blends and UV-curable acrylates - emerge for optically clear LED encapsulation, underscoring the fragmentation of material needs.

Silicone’s rise maps to escalating thermal loads. GE Renewable Energy specifies silicone for its Haliade-X wind turbine, citing elasticity at -60 °C and UV stability across a 25-year duty cycle. Momentive recorded 19% sales growth in 2025 on EV traction-inverter demand. Epoxy faces price pressure as Chinese suppliers cut 2025 list prices by 8%, sacrificing margins to defend volume. Polyurethane adoption accelerates in radar modules where 10-minute pot-life two-part systems meet ISO 16750 requirements. Regulatory headwinds intensify as REACH narrows amine hardener options, lifting raw-material costs 5-10%.

By Curing Technique: Thermal Systems Gain Ground

UV curing dominates with 54.56% of 2025 share on smartphone-scale throughput, curing in less than 30 seconds and slicing Scope 2 emissions by 70% relative to convection ovens. Yet thermal curing is set to grow at 4.19% through 2031 as SiC modules and aerospace electronics demand post-cure stability above 175 °C, unattainable by UV systems. Room-temperature systems linger in field repairs and subsea splices, tolerating long cure cycles where equipment access is limited.

Electronics assembly lines champion UV to match pick-and-place cadence, while Boeing’s D6-82479 mandates a four-hour 150 °C post-cure for flight-control electronics, locking in thermal systems[2]Boeing, “D6-82479 Material Specification,” Boeing.com . Thermal-cure epoxy delivers lap-shear strengths 35% higher than UV acrylate on aluminum, critical for vibration-prone automotive powertrains. Hybrid UV-thermally activated epoxies blur lines, with Electrolube’s 60-second full-cure product capturing applications previously locked to thermal alone. Room-temperature silicone has resurged in offshore wind, enabling on-site encapsulation without portable ovens.

By End-user Industry: Electronics Leads While Automotive Broadens Thermal Requirements

Electronics accounted for 44.74% share of the potting compound market size in 2025 and is projected to post the fastest 4.45% CAGR through 2031, lifted by 5G base-stations, high-density edge servers, and a surge in AI-enabled consumer devices. Smartphone assemblers demand low-viscosity, UV-curable chemistries that fill cavities smaller than 5 mm³ in cycle times under 30 seconds, while data-center power supplies specify high-thermal-conductivity silicones rated above 4 W/m·K to manage more than 15 W/cm² heat flux. The expanding electronics footprint in Asia-Pacific underpins regional dominance, with Chinese smartphone hubs alone consuming more potting compound than the entire European automotive sector.

Automotive’s share is driven by potting for EV battery packs, traction inverters, and radar modules that require flame-retardant ratings up to UL 94 V-0 and thermal conductivity above 3 W/m·K. Polyurethane and silicone hybrids are favored because they retain dielectric strength after 2,000 thermal cycles between -40 °C and 125 °C, a performance envelope that commodity epoxy cannot match. Aerospace remains a high-margin niche in which qualification cycles span 36 months and materials must pass RTCA DO-160G salt-fog and thermal-shock protocols, limiting the field to a handful of AS9100-certified suppliers. Industrial applications prioritize low cost and rapid availability, keeping commodity epoxies relevant even as regulatory VOC caps tighten.

Geography Analysis

Asia-Pacific captures 42.77% of 2025 revenue, and its 3.96% CAGR keeps the region atop the potting compound market through 2031. China accounts for major regional demand, driven by smartphone and IoT assembly in Guangdong, Jiangsu, and Zhejiang, where annual output tops 2 billion units. Japan’s market is smaller but premium, anchored by Nagase and Resonac silicone lines qualified for hybrid-vehicle inverters. South Korea’s demand is tethered to semiconductor packaging; sub-7 nm nodes consume high-thermal-conductivity epoxy underfills that dissipate 300 W/cm². India accelerates under the Production-Linked Incentive scheme, with Tata Electronics sourcing UV-curable potting domestically since 2025. Vietnam’s imports jumped 41% in 2025 as brands diversify assembly beyond China.

North America is also growing amid mature electronics and automotive bases. U.S. consumption rises on CHIPS-funded packaging lines; Intel’s Arizona plant will require 1,200 t/year of potting once fully operational in 2026. Canada’s automotive cluster pivots to bio-based epoxies to trim Scope 3 emissions, while Mexico attracts near-shored EV assemblies served by Henkel’s Querétaro technical center. VOC caps and Proposition 65 labeling elevate compliance costs but also raise entry barriers that favor established players.

Europe's demand is driven by Germany’s EV traction inverters and industrial drives. The U.K. leans on aerospace and defense, with BAE Systems standardizing thermal-cure epoxy in avionics. France’s silicone usage grows via offshore wind and solar inverters, as seen in TotalEnergies’ 1-GW Normandy project. Nordic procurement policies prefer formulations with ≥20% recycled content, accelerating R&D into circular chemistries.

South America and the Middle East and Africa jointly account for a lower market share. Brazil’s automotive electronics and Embraer avionics are sourcing thermal-cure epoxy from overseas suppliers. Saudi Arabia and the UAE spur regional demand through gigawatt-scale solar complexes, specifying silicone potting rated for 65 °C ambient. South Africa leverages potting for smart-meter rollouts in Eskom’s grid upgrade, though local formulation capabilities remain limited.

Competitive Landscape

The potting compound market shows moderate concentration: the top five suppliers - 3M, Dow, Henkel, Huntsman, and Momentive - control roughly 38% of installed capacity. Henkel’s 2025 acquisition of Scheugenpflug embeds dispensing robotics into its portfolio, enabling turnkey EV battery-pack lines that cut cycle times 15%. Dow’s 2026 partnership with Siemens Energy co-develops silicone potting optimized for 1,500-volt offshore converters, targeting a 15% boost in thermal-cycling endurance. BASF pilots chemically recyclable polyurethane, addressing upcoming right-to-repair mandates and REACH bisphenol-A restrictions.

Disruptors emerge with graphene and carbon-nanotube fillers surpassing 10 W/m·K thermal conductivity. Parker Hannifin’s Lord unit released an 8.2 W/m·K epoxy qualified by two Tier 1 EV suppliers for SiC inverters. Automation vendors Nordson and Graco reduce material waste 12-18% via precision dispensing, lowering cost per unit and extending pot life through just-in-time mixing. Niche formulators such as Master Bond secure aerospace and medical device projects by customizing chemistries; its NASA-certified EP42HT-2FG commands a 40% premium. Certification regimes - ISO 9001, IATF 16949, AS9100 - remain high hurdles, limiting new entrants and reinforcing supplier stickiness.

Regional specialists exploit localized niches. Nagase and Resonac dominate Japan’s specialty silicone market, while ELANTAS opened a water-borne epoxy line in Shanghai to meet China’s January 2026 VOC limits. Momentive’s 2025 Gujarat plant aligns with India’s PLI incentives, shortening lead times for domestic electronics assemblers. LG Energy Solution and Huntsman formed a joint venture to deliver polyurethane potting for 800-volt battery packs, signalling deeper OEM-supplier integration.

Potting Compound Industry Leaders

3M

Momentive

Henkel AG & Co. KGaA

Dow

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: WEVO-CHEMIE GmbH developed transformer potting compounds with rail approval. These materials met fire protection requirements as per EN 45545-2 standards, offering high thermal conductivity, excellent partial discharge resistance, and low cracking tendency.

- May 2024: Henkel AG & Co. KGaA introduced three new potting compounds designed to protect automotive components from moisture and fluid ingress. Loctite SI 5035 was a single-component silicone potting compound offering corrosion-free protection for sensitive components, including control unit connectors, while Loctite AA 5832 was a dual-cure polyacrylate potting compound formulated for sealing against automatic transmission fluids and oil.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the potting compound market as the worldwide revenues generated from dedicated epoxy, polyurethane, silicone, polyester, and other specialty resins that are dispensed or cast to fully encapsulate electronic or electrical sub-assemblies, thereby providing insulation, moisture sealing, vibration damping, and thermal dissipation. Sales are captured at factory gate from formulators and contract mixers to OEMs and service centers, and they include replacement kits used during repair cycles.

Thin conformal coatings, over-molding plastics, and general-purpose structural adhesives fall outside this measurement.

Segmentation Overview

- By Resin Type

- Epoxy

- Polyurethane

- Silicone

- Polyester

- Other Resin Types

- By Curing Technique

- UV Curing

- Thermal Curing

- Room-Temperature Curing

- By End-user Industry

- Electronics

- Automotive

- Aerospace

- Industrial

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We interviewed formulators in Germany and South Korea, electronics EMS managers in Mexico, harness suppliers serving EV platforms in the United States, and inverter assemblers across India and China. Their inputs helped us validate typical fill volumes per unit, regional ASP spreads, and the shift toward low-VOC silicones, letting us correct desk-based estimates and assumptions.

Desk Research

Our analysts first pulled export-import codes for HS 3911, 3919, and 3506 from UN Comtrade and US ITC to size cross-border resin flows, and then matched those with production statistics published by the American Chemistry Council, Japan Chemical Fibers Association, and China Chemical Industry Federation. Price corridors came from quarterly filings mined via D&B Hoovers and Dow Jones Factiva, while reliability benchmarks were drawn from IEC-60664 and IPC-J-STD standards, plus failure-rate data shared by the International Electronics Manufacturing Initiative. These publicly available signals underpin the initial demand curve. This list is illustrative; many other open sources were consulted to ground the desk analysis.

Market-Sizing & Forecasting

A top-down model reconstructs global demand by linking resin output and trade with application-level penetration rates across circuit boards, sensors, power modules, and lighting drivers, which are then cross-checked with sampled bottom-up roll-ups of supplier sales and channel checks. Key variables include surface-mount board production, EV battery pack counts, photovoltaic inverter shipments, average resin loading per unit, and quarterly ASP trends. Multivariate regression tied to industrial production and semiconductor billings drives the 2025-2030 forecast, while scenario analyses capture regulatory or supply shocks. Where bottom-up samples undershoot, gaps are proportionally distributed using regional electronics output indices before final triangulation.

Data Validation & Update Cycle

Model outputs pass variance checks against import parity prices, EMS margin bands, and trade-weighted volume estimates. Senior reviewers challenge anomalies and, if needed, we re-contact sources. Reports refresh annually, with mid-cycle touchpoints when major events, such as raw-material disruptions, occur, ensuring clients always receive our latest viewpoint.

Why Our Potting Compound Baseline Stands Up to Scrutiny

Published numbers vary because research groups choose different resin baskets, customer channels, and update cadences.

Our disciplined scope, live primary checks, and annual refresh keep the baseline steady yet responsive.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.15 billion (2025) | Mordor Intelligence | - |

| USD 3.63 billion (2023) | Regional Consultancy A | Counts only epoxy and polyurethane sales in five regions; omits aftermarket and silicone share |

| USD 34.32 billion (2024) | Trade Journal B | Bundles conformal coatings and internal OEM captive use, inflating totals |

| USD 3.76 billion (2024) | Industry Association C | Uses supplier-reported average prices without currency harmonization; limited country coverage |

In short, divergences stem from scope breadth, price bases, and refresh cycles. By anchoring figures to verifiable trade flows, validated usage factors, and timely expert feedback, Mordor Intelligence delivers a dependable, decision-ready baseline that managers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the potting compound market?

The potting compound market is valued at USD 34.19 billion in 2026 and is forecast to reach USD 40.12 billion by 2031.

Which resin type is expected to grow fastest?

Silicone is projected to expand at a 4.26% CAGR through 2031 as thermal-management demands intensify.

Why is UV curing so prevalent in electronics manufacturing?

UV curing offers sub-30-second cycle times and lower energy use, aligning with high-volume smartphone and IoT assembly lines.

Which region holds the largest share of demand?

Asia-Pacific leads with 42.77% of global revenue in 2025, driven by China’s electronics output and South Korea’s semiconductor packaging.

Page last updated on: