Colposcopy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

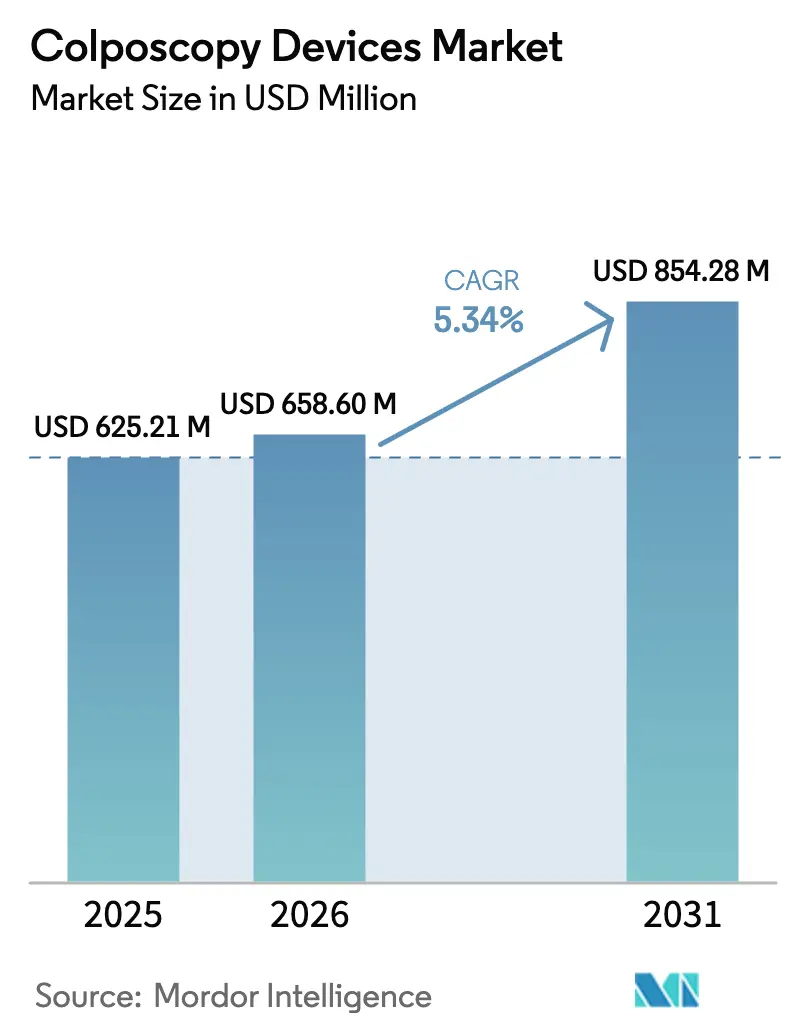

| Market Size (2026) | USD 658.6 Million |

| Market Size (2031) | USD 854.28 Million |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colposcopy Devices Market Analysis by Mordor Intelligence

The Colposcopy Devices Market size was valued at USD 625.21 million in 2025 and estimated to grow from USD 658.6 million in 2026 to reach USD 854.28 million by 2031, at a CAGR of 5.34% during the forecast period (2026-2031).

Global expansion stems from national screening targets, notably the WHO objective to test 70% of women aged 35-45 by 2030, coupled with rapid shifts from optical to AI-enhanced digital platforms. Handheld systems and tele-colposcopy programs are scaling quickly as governments and donors move diagnostics closer to primary care. Meanwhile, supply-chain strains for high-grade optics and chips heighten cost pressures, nudging manufacturers toward resilient component strategies. Across mature markets, premium technology adoption sustains revenues, whereas emerging economies drive volume growth through population-based screening mandates.

Key Report Takeaways

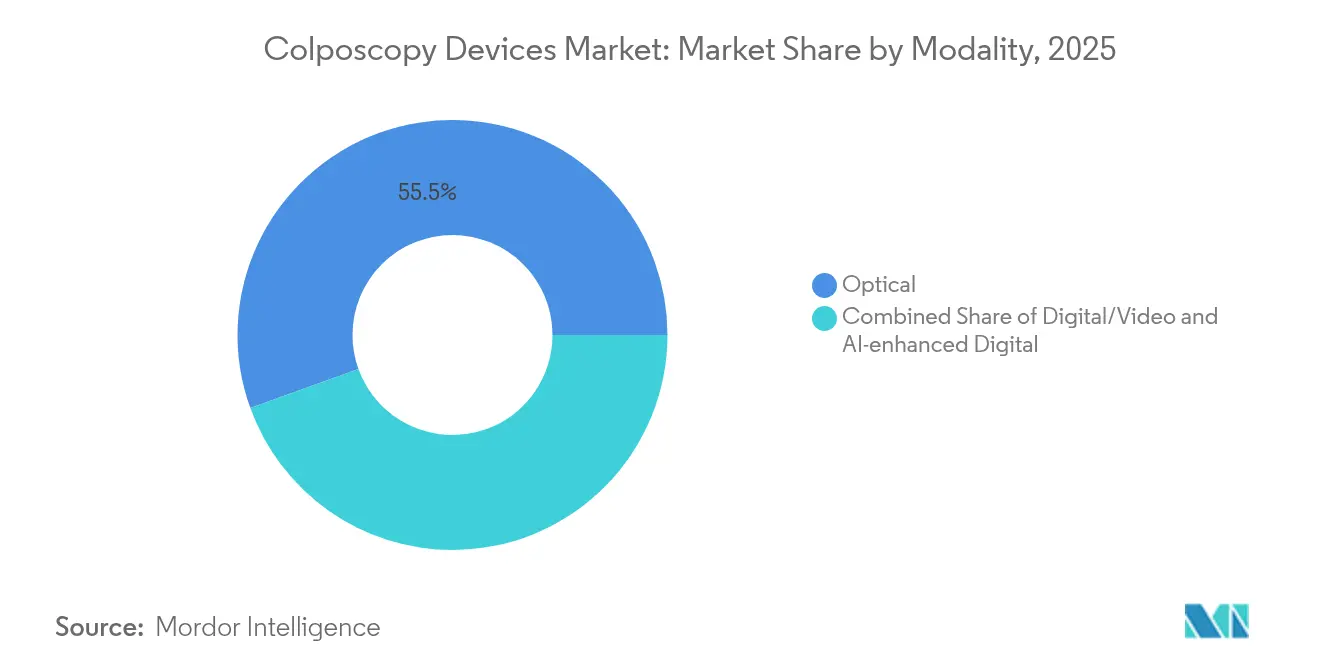

- By modality, optical systems held 55.52% of the colposcopy devices market share in 2025, while AI-enhanced digital platforms are projected to grow at 6.86% CAGR through 2031.

- By portability, stationary units accounted for 43.68% of the colposcopy devices market size in 2025; handheld devices record the fastest 8.49% CAGR to 2031.

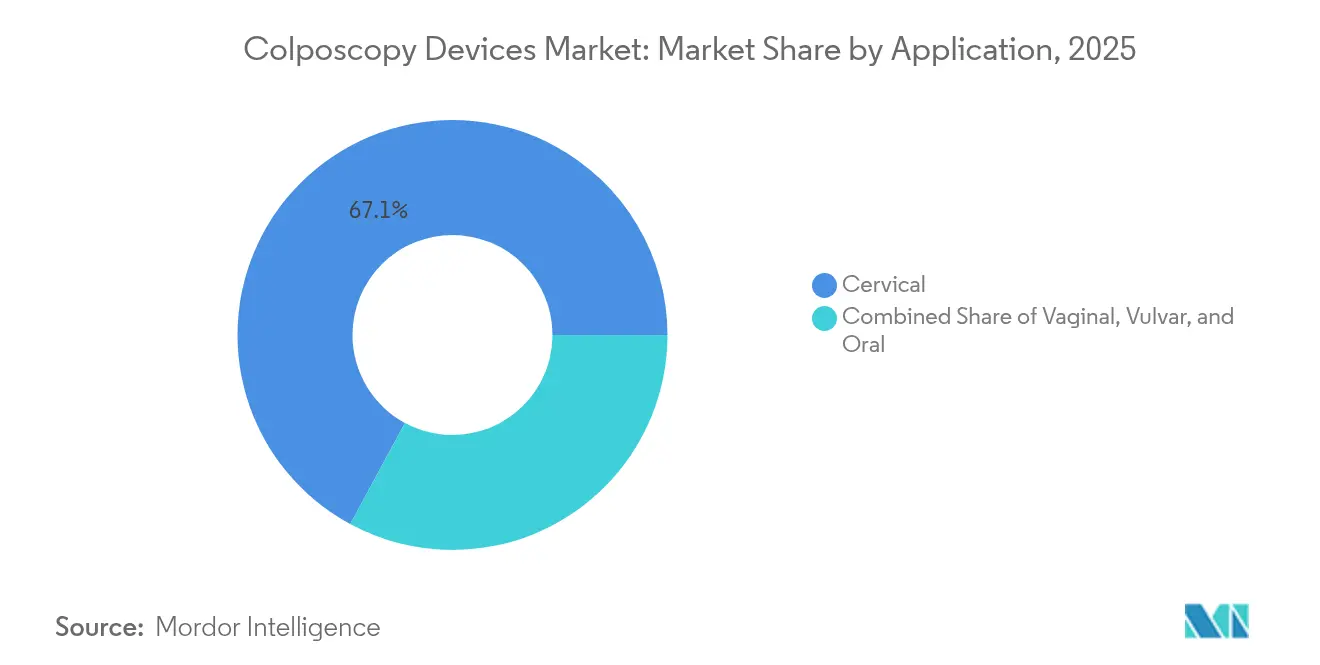

- By application, cervical examinations dominated with 67.11% share of the colposcopy devices market size in 2025, whereas oral screening is expanding at a 8.62% CAGR through 2031.

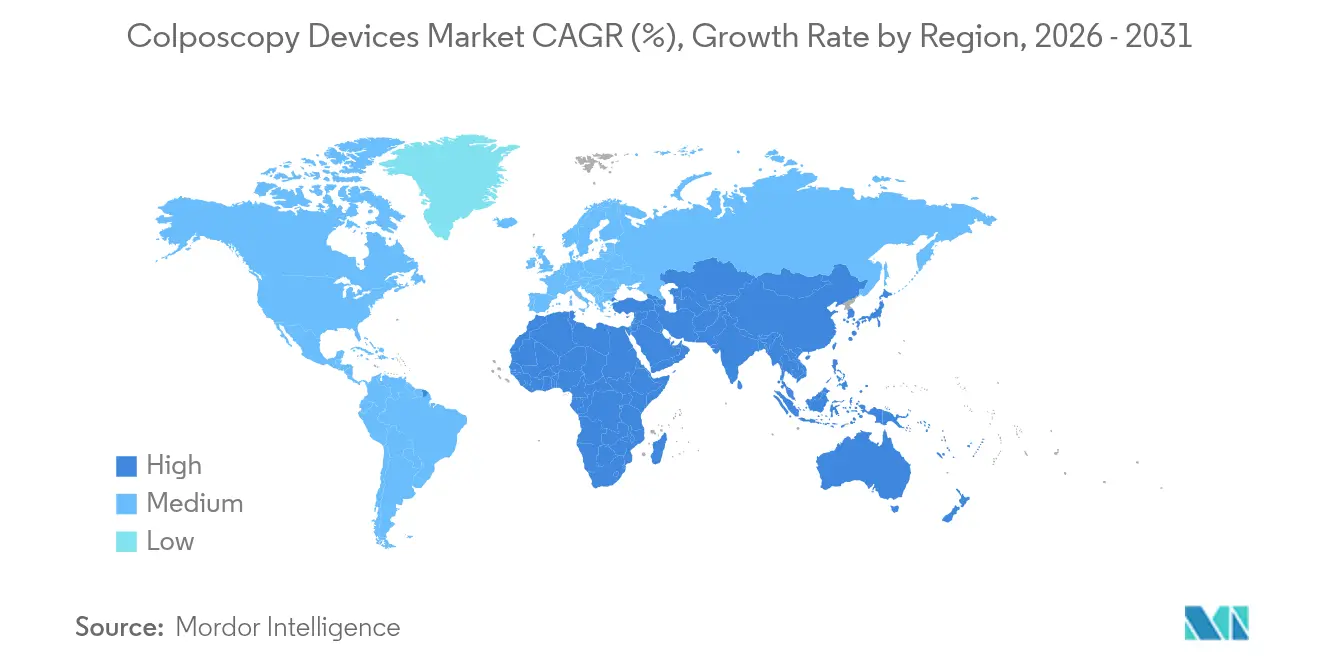

- By geography, North America led with 37.96% of colposcopy devices market share in 2025, while Asia-Pacific is set to advance at 7.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Colposcopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cervical cancer incidence & screening uptake | +1.2% | APAC, Sub-Saharan Africa | Medium term (2-4 years) |

| Accelerating shift from optical to digital/video systems | +0.9% | North America & EU core, widening to APAC | Short term (≤2 years) |

| AI-enabled spectral imaging raises diagnostic accuracy | +0.7% | North America, EU, select APAC | Long term (≥4 years) |

| Harmonised screening guidelines in emerging economies | +0.6% | APAC, Sub-Saharan Africa, Latin America | Long term (≥4 years) |

| Tele-colposcopy roll-outs for remote clinics | +0.6% | LMIC regions worldwide | Medium term (2-4 years) |

| Donor-funded handheld device procurement in LMICs | +0.4% | Sub-Saharan Africa & parts of APAC, Latin America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Cervical Cancer Incidence & Screening Uptake

Expanding disease burden fuels device demand, especially where screening coverage remains sparse. China’s goal of 70% coverage by 2030 highlights large-scale procurement prospects.[1]Qiao You-Lin, “Accelerating elimination of cervical cancer in China,” Cancer Biology & Medicine, cbmjournal.com South Asia’s projected mortality rise reinforces the urgency, and Brazil’s structured network illustrates how systematic programs quickly lift utilization.[2]Budukh A. M. et al., “South Asian cervical cancer projections,” Frontiers in Medicine, frontiersin.org Updated WHO guidelines recommending immediate colposcopy for dual-stain positive HPV cases further enlarge the eligible patient pool

Accelerating Shift from Optical to Digital/Video Systems

Digital platforms allow remote reading, standardized documentation and seamless data storage. Community clinics in the United States reported CIN2+ detection jumps when dynamic spectral imaging was deployed.[3]Boeke C. E. et al., “Dynamic spectral imaging in US clinics,” Journal of Lower Genital Tract Disease, lww.com Commercial launches such as Casio’s DZ-C100 COLPOCAMERA underscore mainstream acceptance. Evidence from Nature-backed trials shows automated systems reaching 94.6% sensitivity, validating payers’ willingness to fund higher-priced digital solutions.

AI-Enabled Spectral Imaging Raises Diagnostic Accuracy

Machine learning models remove much of the subjectivity inherent in visual assessment. Algorithms able to interpret acetowhitening and vascular cues now deliver over 98% sensitivity in pre-clinical testing.[4]Farias Santos Lima C. et al., “Deep learning for cervical precancer,” Nature Communications, nature.com Large commercial roll-outs, such as Labcorp’s adoption of Hologic’s AI cytology platform, reveal tangible workflow efficiencies when AI is integrated into routine screening.

Tele-Colposcopy Roll-Outs for Remote Clinics

Smartphone-based systems piloted on Nicaragua’s Caribbean Coast demonstrated high clinician acceptance even under limited connectivity. WHO technical guidance now endorses tele-colposcopy to bridge urban-rural gaps, prompting ministries of health to fund cloud-linked image servers and battery-operated scopes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce reimbursement & budget limits in developing nations | -0.8% | Sub-Saharan Africa, parts of APAC & Latin America | Long term (≥4 years) |

| Shortage of trained colposcopists & skill variability | -0.5% | Global, most acute in LMICs | Medium term (2-4 years) |

| Regulatory pushback on overdiagnosis/biopsy rates | -0.4% | North America & EU | Medium term (2-4 years) |

| Supply-chain volatility for high-grade optics & chips | -0.3% | Global, high concentration in APAC manufacturing | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Scarce Reimbursement & Budget Limits in Developing Nations

Health budgets in low-resource settings often favor basic Pap tests over capital-intensive colposcopy systems. Cost-effectiveness analyses in China show economic benefits for HPV triage, yet budget ceilings hamper nationwide adoption. South Africa’s public sector treats 85% of citizens but contends with limited device allocations. Such constraints perpetuate a two-tier market split.

Shortage of Trained Colposcopists & Skill Variability

Many regions face limited expertise. A UAE survey found only 8 adequately trained practitioners among 52 specialists. Low procedure volumes undermine proficiency, pushing stakeholders toward simulation-based curricula and AI decision support. Until training pipelines expand, device utilization will lag installed capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: AI Integration Accelerates Digital Transition

The colposcopy devices market posted a 55.52% optical share in 2025, yet AI-driven digital systems are set to compound at 6.86% annually. Digital platforms bridge documentation, remote consultation and algorithmic triage, motivating hospitals to upgrade legacy optics. Notably, automated spectral imaging improved CIN2+ detection from 31.25% to 87.50% in US community clinics, a clinical gain that translates into budget approval for premium products.

Rising AI capability also counterbalances the global shortfall of skilled operators. While optical scopes remain favored in resource-constrained sites, hybrid video systems increasingly represent an attainable mid-price option. Across both tiers, the colposcopy devices market continues to migrate toward data-rich ecosystems that support longitudinal patient records and centralized quality audits.

By Portability: Handheld Devices Drive Accessibility Revolution

Handheld platforms are projected to outpace other form factors at 8.49% CAGR, even as stationary units retain a 43.68% revenue base. Field studies confirmed handheld sensitivity of 88.3% for CIN2+ lesions, validating use in screening caravans and primary health posts. The portability upswing aligns with donor-funded roll-outs aimed at rural populations where fixed infrastructure is scarce.

Mobile-trolley models occupy the middle ground by offering in-clinic mobility without sacrificing optical precision. Battery-powered thermal ablation systems introduced alongside portable scopes hint at bundled treatment-diagnosis packages that could streamline workflows in district hospitals. Despite lower magnification relative to benchtop units, successive lens improvements are closing the performance gap, further propelling the colposcopy devices market toward point-of-care settings.

By Application: Oral Screening Emerges as Growth Frontier

With 67.11% share in 2025, cervical exams remain the backbone of the colposcopy devices market. Yet oral lesion assessment is the fastest-growing niche, advancing at 8.62% CAGR as clinicians apply mucosal visualization techniques to head-and-neck oncology. Fluorescence-based adjuncts like VELscope report 96% sensitivity, encouraging dental and ENT specialists to add colposcopy-style optics to their armamentarium.

Vaginal and vulvar uses also gain traction as comprehensive lower-genital tract strategies become standard. AI modules fine-tuned for multiple mucosal sites promise more uniform accuracy, promoting device utilization across gynecology, dermatology and oral health. This diversification fortifies revenue streams and cushions vendors against fluctuations in cervical screening volumes.

Geography Analysis

North America contributed 37.96% of 2025 revenue, reflecting mature reimbursement and rapid uptake of AI digital systems. Health networks increasingly embed cloud-linked scopes that feed centralized pathology review, driving steady replacement demand. FDA clearances for AI cytology and dynamic spectral imaging support continued premium pricing.

Asia-Pacific registers the highest growth at 7.93% CAGR. China’s 70% screening target underpins mass procurements, while India leverages blended models pairing self-sampling with referral colposcopy. Japan favors repeat HPV testing over immediate referral, yet still upgrades to digital optics to standardize archival images. Donor-backed tele-colposcopy pilots in Vietnam and Indonesia demonstrate scalable pathways for rural screening.

Europe prioritizes quality harmonization through federation guidelines, spurring conversions from analog to digital systems. In the Middle East, training shortfalls restrain volume despite rising device budgets.

Sub-Saharan Africa faces stark resource gaps, though battery-operated handhelds are now entering provincial clinics under global health grants. Latin America benefits from Brazil’s mature control network, adopting portable thermal ablation alongside diagnostics to enhance care continuity.

Competitive Landscape

Competitive intensity is moderate, with multinational device firms sharing space with niche innovators. Olympus recorded Yen 298.7 (USD 2.08) billion in endoscopy revenue for the six months to September 2024, illustrating the scale advantages enjoyed by diversified players. Carl Zeiss Meditec logged EUR 490.5 (USD 578.2) million in Q1 FY 2024/25, leveraging optics expertise to court high-resolution segments.

Technology convergence shapes strategy: incumbents bundle AI engines and telemedicine dashboards, while software-centric entrants focus on image analytics. Supply-chain resilience is rising on executive agendas as optical glass and semiconductor shortages lift component costs to 20% of sales for some firms. Vendors that dual-source key parts and localize assembly are better positioned to protect margins and delivery timelines.

Partnerships with diagnostic laboratories, cloud providers, and academic AI groups accelerate product evolution. Early-stage ventures targeting self-sampling or at-home cervical imaging may disrupt incumbent reliance on clinic-based workflows. To hedge, leading companies are either acquiring such start-ups or launching internal R&D programs aimed at lower-acuity settings, ensuring relevance across the full spectrum of the colposcopy devices market.

Colposcopy Devices Industry Leaders

McKesson Medical-Surgical Inc.

Olympus Corporation

CooperSurgical Inc.

Carl Zeiss Meditec AG

MedGyn Products Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Labcorp announced the implementation of Hologic's FDA-cleared Genius Digital Diagnostics System across its laboratory network, integrating artificial intelligence into Pap test analysis to improve cervical cancer screening accuracy and efficiency.

- September 2024: The World Health Organization updated its cervical cancer prevention guidelines to include CINtec PLUS Cytology, a dual-stain test that identifies HPV-positive individuals at risk for cervical precancer and cancer, recommending immediate colposcopy for positive results.

- May 2024: BD (Becton, Dickinson and Company) received FDA approval for self-collected vaginal specimens for HPV testing using the BD Onclarity HPV Assay, enabling women to collect samples in various settings and addressing barriers such as discomfort and lack of local healthcare providers.

- March 2024: Casio launched the DZ-C100 COLPOCAMERA in the United States, Australia, and New Zealand, expanding its presence in the colposcopy devices market with enhanced cervical imaging capabilities designed to improve diagnostic accuracy in clinical settings.

Global Colposcopy Devices Market Report Scope

Colposcopy is a medical diagnostic procedure to examine an illuminated, magnified view of the cervix as well as the vagina and vulva. Many pre-malignant lesions and malignant lesions in these areas have discernible characteristics that can be detected through examination. The Market is Segmented By Modality (Optical, Video), Portability (Stationary, Handheld), Application (Pelvic, Oral), Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Optical |

| Digital/Video |

| AI-enhanced Digital |

| Stationary |

| Mobile-trolley |

| Handheld |

| Cervical |

| Vaginal |

| Vulvar |

| Oral |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | Optical | |

| Digital/Video | ||

| AI-enhanced Digital | ||

| By Portability | Stationary | |

| Mobile-trolley | ||

| Handheld | ||

| By Application | Cervical | |

| Vaginal | ||

| Vulvar | ||

| Oral | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and projected value of the colposcopy devices market?

The colposcopy devices market stands at USD 658.6 million in 2026 and is forecast to reach USD 854.28 million by 2031, reflecting a 5.34% CAGR.

Which modality segment is expanding the fastest?

AI-enhanced digital systems register the quickest pace, growing at a 6.86% CAGR through 2031 while optical units still command the largest share.

What key factors drive market growth?

National screening mandates, the shift from optical to digital platforms, AI-enabled accuracy gains and tele-colposcopy programs are the main growth catalysts.

Which region will see the highest growth rate?

Asia-Pacific is projected to advance at an 7.93% CAGR, fueled by large population-based screening initiatives and donor-funded procurements.

How do handheld devices improve market accessibility?

Handheld colposcopes grow at 8.49% CAGR, allowing point-of-care diagnostics in rural clinics and supporting remote image interpretation.

What is the primary restraint on wider adoption?

Budget and reimbursement limits in low- and middle-income countries curb investment in advanced colposcopy systems despite high clinical need.

Page last updated on: