Post-Harvest Treatment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 2.73 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

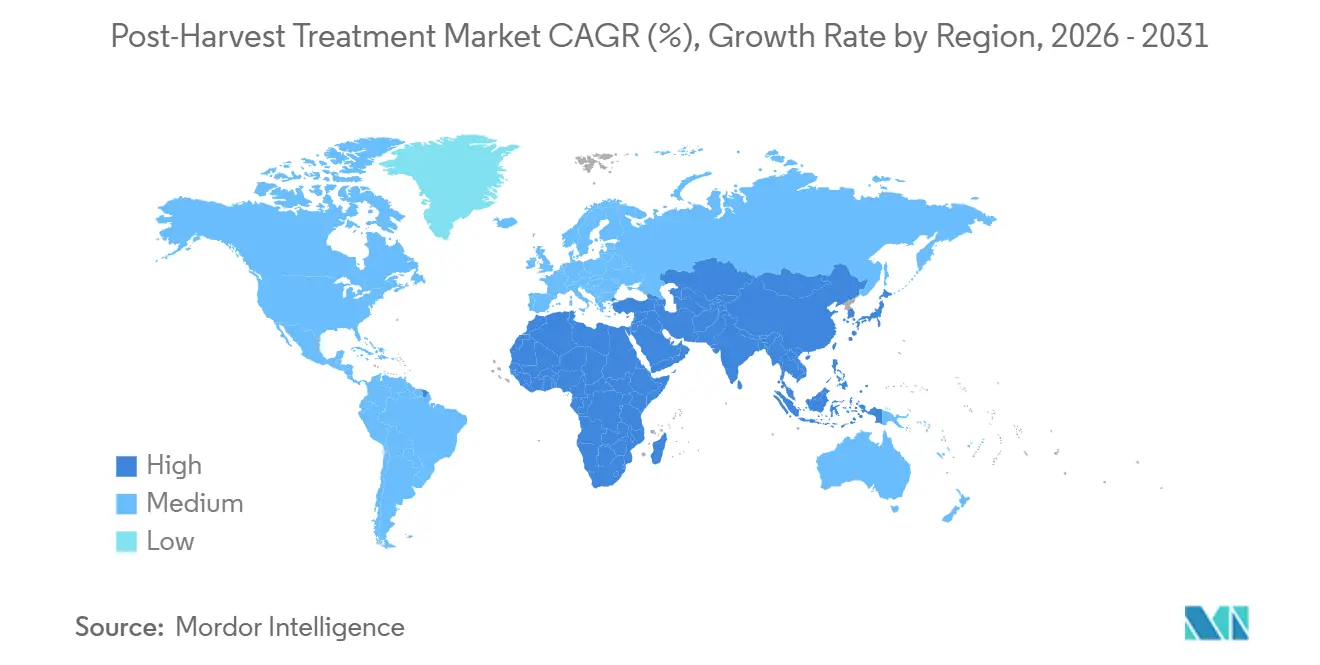

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

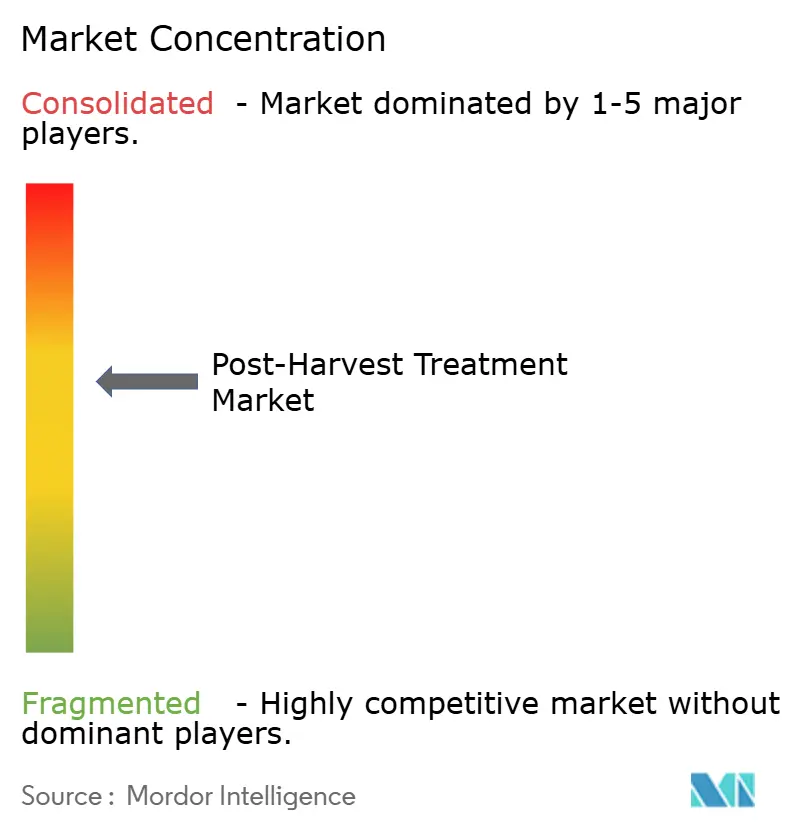

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Post-Harvest Treatment Market Analysis by Mordor Intelligence

The post-harvest treatment market size was valued at USD 1.80 billion in 2025 and is projected to grow from USD 1.93 billion in 2026 to USD 2.73 billion by 2031, registering a CAGR of 7.20% between 2026 and 2031. Key factors influencing this growth include strong demand for coatings and films, the rapid adoption of sprout inhibitors, and significant investments in cold-chain infrastructure in emerging regions. Retailers are increasingly imposing stricter residue limits, driving a shift toward bio-rational chemistries and reducing the reliance on synthetic fungicides in premium export supply chains. Gas formulations, particularly one-methylcyclopropene used in controlled-atmosphere (CA) facilities, are gaining market share as pack-house operators upgrade warehouses to comply with low-residue requirements. Additionally, advancements in edge-computing sensors and machine-learning shelf-life models are transforming how the market evaluates return on investment, enabling operators to connect real-time decay suppression data with dynamic pricing strategies. Furthermore, infrastructure funding aimed at reducing post-harvest losses in regions such as Africa and South Asia is shortening payback periods for applicators and expanding the addressable market base.

Key Report Takeaways

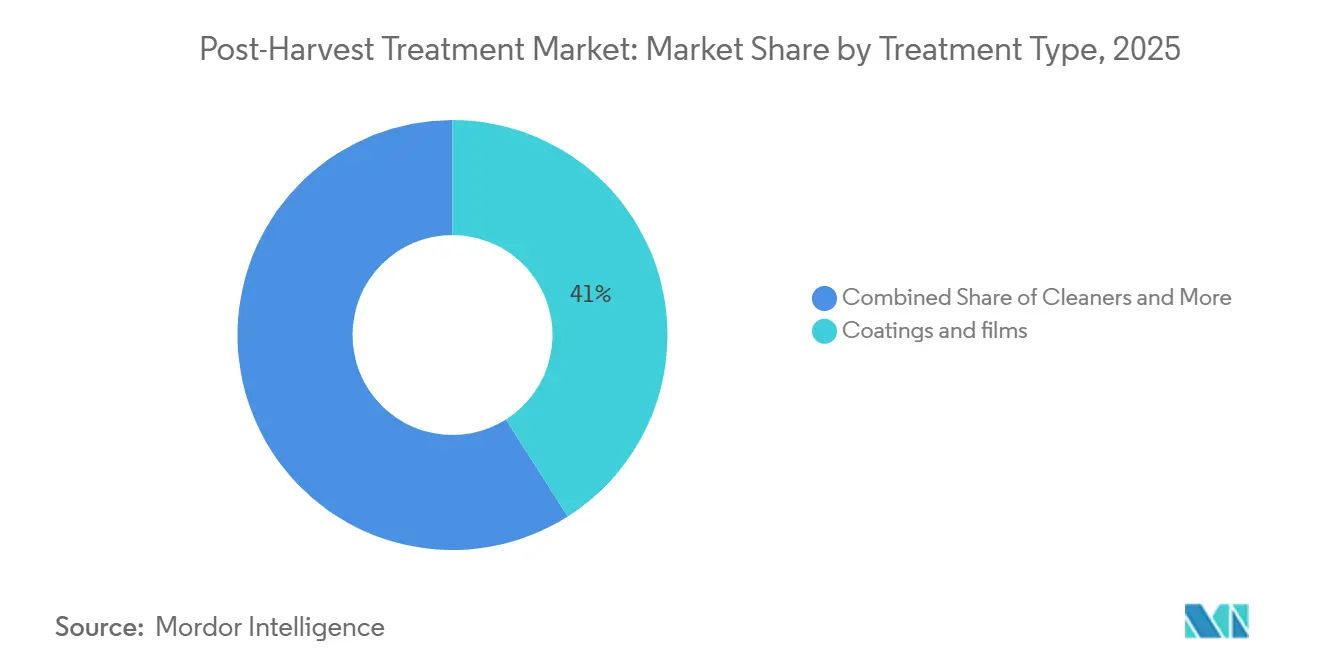

By treatment type, coatings and films accounted for the largest 41.0% of the post-harvest treatment market share in 2025, whereas the post-harvest treatment market size for the sprout inhibitors segment is projected to grow at the fastest 10.8% CAGR from 2026 to 2031.

By formulation, liquid held the largest 58.0% share of the market in 2025, while the gas segment is projected to grow at the fastest CAGR of 9.4% from 2026 to 2031.

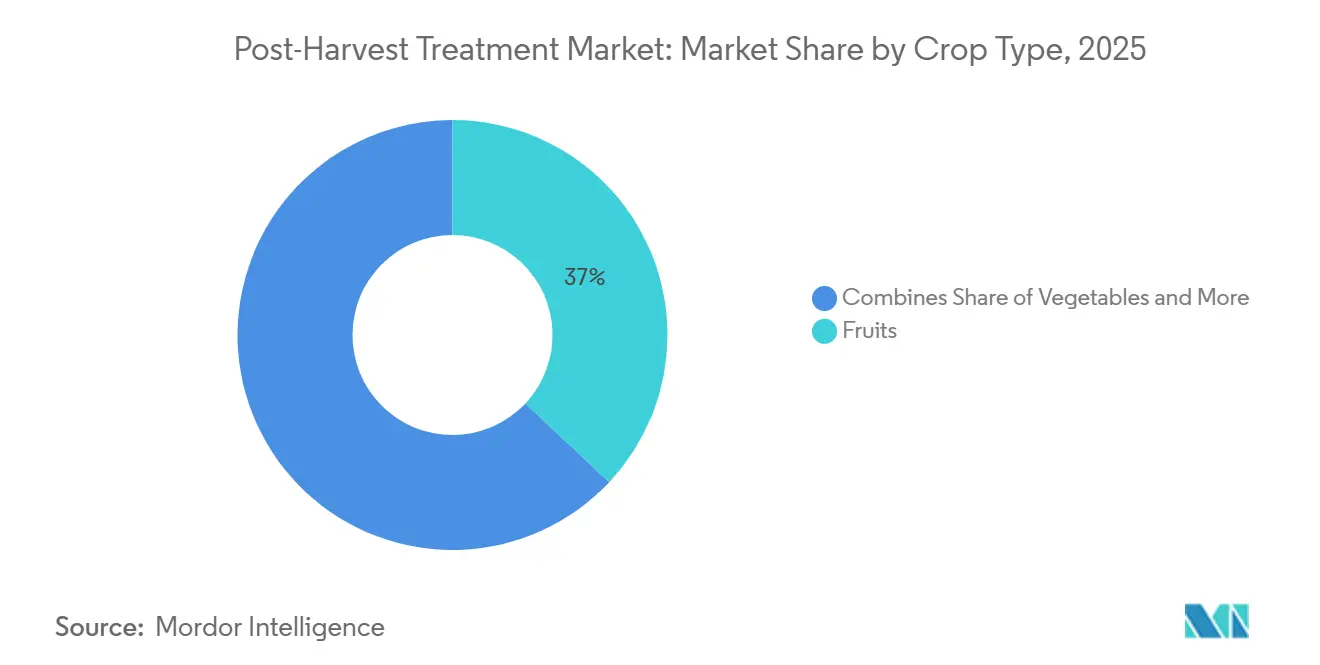

By crop type, fruits captured the largest 37.0% share of the market in 2025, whereas the vegetable segment is anticipated to grow at the fastest CAGR of 8.9% from 2026 to 2031.

By origin type, the synthetic segment accounted for the largest share of the market at 64.3% in 2025, while the natural segment is forecast to grow at the fastest CAGR of 12.1% from 2026 to 2031.

By geography, Asia-Pacific held the largest 33.0% share of the post-harvest treatment market in 2025, whereas the market in Africa is projected to grow at the fastest CAGR of 9.7% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Post-Harvest Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain expansion in emerging markets | +1.2% | Africa, South Asia, and Southeast Asia | Medium term (2-4 years) |

| Stringent supermarket residue specifications | +1.0% | North America, and Europe | Short term (≤ 2 years) |

| Proliferation of controlled-atmosphere packaging lines | +0.9% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Increasing adoption of edible antimicrobial coatings | +0.8% | North America, Europe, and South America premium export corridors | Long term (≥ 4 years) |

| Rise of e-commerce grocery fulfillment centers | +1.1% | Global urban hubs | Short term (≤ 2 years) |

| AI-enabled shelf-life prediction analytics | +0.7% | North America, Europe, and advanced Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold-chain Expansion in Emerging Markets

Inadequate refrigeration infrastructure continues to result in substantial post-harvest losses, emphasizing the need for cold-chain development. According to the Food and Agriculture Organization (FAO), 526 million metric tons of food, accounting for approximately 12% of global production, are lost due to insufficient refrigeration[1]Source: Food and Agriculture Organization (FAO), “Cooling the Chain, Cutting the Waste,” fao.org. This highlights the necessity of investing in cold storage facilities, packhouses, and logistics networks to improve the handling of perishable produce. Such investments also facilitate the adoption of post-harvest treatment solutions, including fungicides, coatings, and ethylene management technologies, thereby driving market demand.

Stringent Supermarket Residue Specifications

Stringent residue specifications in major retail markets are increasing compliance demands on growers and exporters. For instance, the European Commission has reduced the maximum residue level for chlorpropham in potatoes from 0.35 mg/kg to 0.2 mg/kg under Regulation (EU) 2025/1163[2]Source: European Commission, “EU Pesticides Database – Maximum Residue Levels for Chlorpropham,” ec.europa.eu . This reduction reflects a broader regulatory trend toward stricter food safety standards and lower tolerance levels. Consequently, producers are adopting precision application technologies, residue-compliant fungicides, and bio-based post-harvest treatments to meet retailer requirements, driving growth in the post-harvest treatment market.

Proliferation of Controlled-Atmosphere Packaging Lines

The expansion of controlled-atmosphere packaging lines is improving post-harvest handling by allowing precise control of oxygen, carbon dioxide, and humidity levels during storage and transportation. For example, exporters of perishable fruits like peaches and stone fruits are increasingly adopting controlled-atmosphere systems to preserve product quality during extended transit times, particularly for long-distance shipments. These systems are often used alongside post-harvest treatments such as coatings and fungicides to enhance preservation. Consequently, there is growing demand for integrated solutions, including gas-monitoring and treatment technologies, driving growth in the post-harvest treatment market.

Increasing Adoption of Edible Antimicrobial Coatings

The adoption of edible antimicrobial coatings is increasing due to their demonstrated effectiveness in preserving quality and extending shelf life during storage. A researcher from the Universidade Federal de Pernambuco, Brazil, found in 2025 that alginate–chitosan edible coatings containing Lacticaseibacillus casei preserved microbial quality and maintained key physicochemical parameters, such as a moisture content of 90.74 ± 0.27%, in strawberries over 12 days of cold storage. This highlights the efficacy of bio-based coatings in post-harvest preservation, contributing to their growing use and driving value growth in the post-harvest treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory tightening on certain fungicides | -0.9% | North America and Europe | Short term (≤ 2 years) |

| Growing consumer resistance to synthetic chemicals | -0.6% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Price volatility of bio-based raw materials | -0.5% | Global | Medium term (2-4 years) |

| Post-harvest mechanization gaps in developing countries | -0.8% | Sub-Saharan Africa, South Asia, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Tightening on Certain Fungicides

Regulatory scrutiny of synthetic fungicides is increasing as authorities enforce stricter safety and risk mitigation measures. In January 2025, the United States Environmental Protection Agency issued interim registration review decisions for chlorothalonil, thiophanate-methyl, and carbendazim, introducing updated controls to mitigate potential risks to human health and the environment. These measures align with a broader trend of tightening pesticide regulations and reassessing commonly used fungicides. As compliance requirements grow more stringent, manufacturers are investing in safer formulations and alternative solutions, leading to changes in product portfolios and influencing growth patterns in the post-harvest treatment market.

Growing Consumer Resistance to Synthetic Chemicals

Consumer preference for chemical-free and organic food products is increasingly shaping post-harvest treatment practices. According to the Organic Trade Association, United States sales of certified organic products reached USD 76.6 billion in 2025, reflecting a 6.8% year-over-year growth and surpassing the growth rate of the conventional food market[3]Source: Organic Trade Association, “U.S. Organic Market Report 2026,” ota.com . This trend highlights the growing demand for residue-free produce. However, the higher costs associated with these alternatives compared to synthetic chemicals continue to pressure profit margins, posing a structural challenge to the post-harvest treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Coatings and Films Dominate, Sprout Inhibitors Accelerate

The coatings and films segment accounted for the largest 41.0% of the post-harvest treatment market share in 2025, highlighting their essential role in maintaining freshness and minimizing moisture loss in fruits and vegetables. These solutions are widely utilized due to their compatibility with existing supply chains and compliance with export standards. The growing demand for residue-compliant and bio-based coatings is further reinforcing their market position, particularly in regions with stringent food safety regulations and increasing consumption of organic produce.

The post-harvest treatment market size for the sprout inhibitors segment is projected to grow at the fastest CAGR of 10.8% from 2026 to 2031, driven by increasing demand in storage-intensive crops such as potatoes and onions. Regulatory limitations on traditional chemicals are accelerating the shift toward safer and alternative sprout control methods. Additionally, ethylene blockers and fungicides continue to play a key role in preservation strategies, while cleaners and disinfectants are gaining significance in ensuring hygiene standards across post-harvest handling facilities.

By Formulation: Liquid Leads, Gas Shows Emerging Growth

The liquid formulations segment held the largest 58.0% of the post-harvest treatment market share in 2025, driven by their extensive use in spray and dip applications within pack-houses. These formulations are favored for their ease of application, uniform coverage, and compatibility with existing infrastructure. Their versatility across various crop types and treatment methods supports their dominant role in commercial post-harvest operations.

The gas segment is projected to grow at the fastest CAGR of 9.4% from 2026 to 2031, fueled by the increasing adoption of controlled atmosphere storage and ethylene management systems. These formulations allow precise control over ripening and spoilage processes, making them particularly valuable in long-distance trade. Meanwhile, powder formulations continue to see steady demand in grain storage applications, with advancements in delivery mechanisms further improving their efficiency and effectiveness.

By Crop Type: Fruits Hold Leadership, Vegetables Grow Fastest

The fruits segment accounted for the largest 37.0% of the post-harvest treatment market share in 2025. This dominance is attributed to high export volumes and the need to extend shelf life during transportation. Common treatments, including coatings, fungicides, and ethylene blockers, are extensively used to preserve quality and minimize spoilage. The perishability of fruits continues to drive the adoption of advanced preservation techniques across global supply chains, ensuring that fruits maintain their quality and freshness during long-distance transportation and storage.

The post-harvest treatment market size for the vegetables segment is forecast to grow at the fastest CAGR of 8.9% from 2026 to 2031. This growth is supported by rising consumption of fresh produce and the expansion of organized retail channels. Increased emphasis on quality control and waste reduction in urban distribution systems is further driving the adoption of post-harvest treatments. These treatments help maintain the freshness of vegetables, reduce spoilage, and support the growing demand for high-quality produce in urban and suburban markets.

By Origin: Synthetic Formulations Dominate, but Natural Options Gain Ground

The synthetic segment accounted for the largest 64.3% share of the post-harvest treatment market in 2025, driven by a long-standing reliance on petroleum-derived fungicides, waxes, and sprout inhibitors. Hybrid offerings that blend synthetic carriers with bio-based actives fill the middle ground for packers looking to cut residues without a full switch. Regulatory pressure is nudging the mix toward naturals. The United States Environmental Protection Agency lowered tolerances for chlorothalonil and thiophanate-methyl in 2024, and the European Union tightened limits on carbendazim and thiabendazole in April 2025, forcing suppliers to speed up work on natural portfolios.

The post-harvest treatment market size for the natural segment is projected to grow at the fastest CAGR of 12.1% from 2026 to 2031. Coatings built around chitosan-alginate blends, essential-oil antimicrobials, and microbial fermentation products cost 20–40% more than synthetic equivalents, but organic channels absorb the premium to secure shelf space and avoid residue flags. Commercial momentum accelerated after the United States Food and Drug Administration granted Generally Recognized as Safe (GRAS) status to sodium alginate and chitosan in 2024, clearing a critical regulatory hurdle and enabling firm such as bio-ferm GmbH to widen their bio-based lines.

Geography Analysis

Asia-Pacific accounted for the largest 33.0% of the post-harvest treatment market share in 2025, driven by expanding agricultural output and increased investment in cold-chain infrastructure. Countries such as China and India are enhancing post-harvest handling systems to minimize food losses and boost export competitiveness. The growing adoption of advanced preservation technologies, such as coatings and controlled atmosphere storage, is further driving regional demand. Additionally, rapid urbanization and rising consumption of fresh produce are fostering the integration of post-harvest treatment solutions across supply chains.

Africa is projected to grow at the fastest CAGR of 9.7% from 2026 to 2031, supported by initiatives to reduce significant post-harvest losses and enhance food security. Governments and international organizations are investing in storage infrastructure and modernizing supply chains. The expansion of horticulture exports and increasing awareness of preservation technologies are contributing to market growth. While infrastructure gaps remain, improved access to cold storage and handling facilities is gradually enabling the adoption of post-harvest treatment solutions across the region.

North America also accounted for a significant share of global revenue in 2025, driven by advanced agricultural practices and strict regulatory frameworks related to food safety. Heightened regulatory focus on pesticide residues and food safety compliance is encouraging growers and distributors to implement more effective preservation solutions. The region's well-structured retail and export-oriented supply chains demand extended shelf life and consistent product quality. This has led to increased adoption of coatings, fungicides, and ethylene management technologies to minimize spoilage, enhance storage efficiency, and meet stringent food safety standards in both domestic and international markets.

Competitive Landscape

The market is moderately concentrated, with key players such as Syngenta AG, AgroFresh Solutions, Inc., Bayer AG, Decco Post-Harvest Inc. (UPL Limited), and Nufarm Limited maintaining strong positions through integrated agricultural solutions. Strategic investments in research and development are driving the introduction of residue-compliant and bio-based treatments. Additionally, companies are focusing on partnerships and acquisitions to strengthen their capabilities in coatings, fungicides, and ethylene management technologies, ensuring they remain competitive in addressing evolving market demands and customer needs.

Mid-sized and regional players are increasingly competing by specializing in niche product segments, including bio-based coatings and microbial solutions. Innovation in formulation technologies and adherence to evolving regulatory standards are critical competitive factors. Companies are differentiating themselves by offering tailored solutions for specific crops and storage conditions. The growing focus on sustainability and food safety is fostering continuous product development and diversification across the competitive landscape, enabling these players to carve out unique positions in the market.

Industry consolidation is accelerating as companies aim to enhance their technological capabilities and expand their global presence. For example, John Bean Technologies Corporation completed the acquisition of Marel hf. for USD 4.4 billion in 2025, bolstering its processing and preservation technology portfolio. This reflects a broader trend of integrating equipment and treatment solutions to provide comprehensive post-harvest systems. Such consolidation efforts are reshaping the competitive dynamics, allowing companies to deliver more efficient and innovative solutions to meet market demands.

Post-Harvest Treatment Industry Leaders

Syngenta AG

AgroFresh Solutions, Inc

Bayer AG

Decco Post-Harvest Inc. (UPL Limited)

Nufarm Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: John Bean Technologies Corporation completed the acquisition of Marel hf. for approximately USD 4.4 billion. This strategic move led to the formation of JBT Marel Corporation.

- November 2024: Citrosol, S.A. enhanced its international expansion strategy in the post-harvest treatment market by establishing Citrosol Uruguay S.A. This initiative aims to support citrus, apple, and pear producers in South America with post-harvest preservation, sanitation, and coating solutions.

- March 2024: AgroFresh Solutions, Inc. acquired Pace International LLC, including its global operations, to enhance its post-harvest solutions portfolio. This acquisition bolstered AgroFresh’s presence in major fruit-growing regions and expanded its range of offerings, including coatings, fungicides, and storage solutions.

Global Post-Harvest Treatment Market Report Scope

Post-harvest treatment involves the use of physical, chemical, or biological methods on crops after harvesting to maintain quality, extend shelf life, and minimize spoilage during storage and transportation. These treatments include coatings, fungicides, ethylene blockers, and sprout inhibitors, which help control decay, delay ripening, and preserve product freshness.

The post-harvest treatment market report is segmented by treatment type, including coatings and films, cleaners, fungicides, ethylene blockers, sprout inhibitors, and other treatments; by formulation, including liquid, powder, and gas; by crop type, including fruits, vegetables, grains, and flowers and ornamentals; by origin type, natural and synthetic; and by geography, covering North America, South America, Europe, Asia-Pacific, the Middle East, and Africa. The market forecasts are provided in terms of value (USD).

| Coatings and Films |

| Cleaners |

| Fungicides |

| Ethylene Blockers |

| Sprout Inhibitors |

| Others |

| Liquid |

| Powder |

| Gas |

| Fruits |

| Vegetables |

| Grains |

| Flowers and Ornamentals |

| Natural |

| Synthetic |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Treatment Type | Coatings and Films | |

| Cleaners | ||

| Fungicides | ||

| Ethylene Blockers | ||

| Sprout Inhibitors | ||

| Others | ||

| By Formulation | Liquid | |

| Powder | ||

| Gas | ||

| By Crop Type | Fruits | |

| Vegetables | ||

| Grains | ||

| Flowers and Ornamentals | ||

| By Origin | Natural | |

| Synthetic | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the post-harvest treatment market in 2026?

The post-harvest treatment market size is estimated at USD 1.93 billion in 2026 and is projected to reach USD 2.73 billion by 2031, registering a CAGR of 7.20% during 2026–2031.

Which treatment category will grow the fastest through 2031?

Sprout inhibitors are positioned to expand at the fastest 10.8% CAGR from 2026 to 2031.

What region offers the highest growth rate for post-harvest treatments?

Africa is forecast to post a fastest 9.7% CAGR from 2026 to 2031.

How do supermarket residue limits influence product demand?

Private residue limits, which are stricter than statutory standards, drive packers to adopt bio-rational coatings and precision application methods. This shift increases the value per metric ton in the post-harvest treatment market.

Page last updated on: