Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

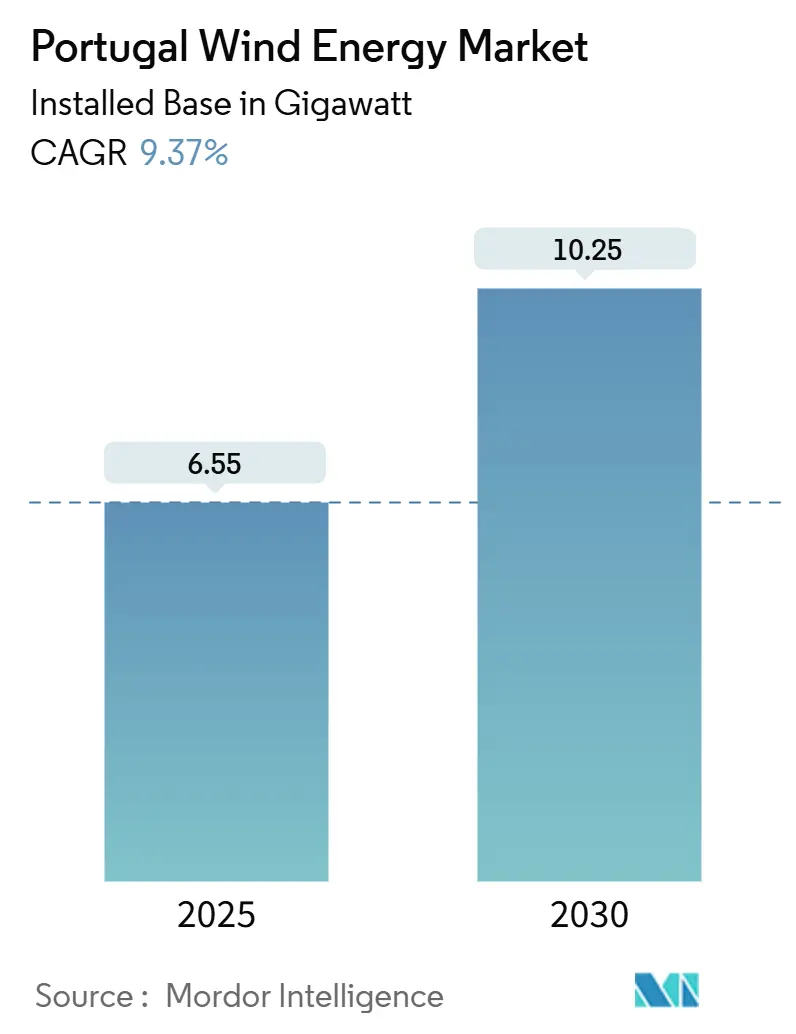

| Market Volume (2025) | 6.55 gigawatt |

| Market Volume (2030) | 10.25 gigawatt |

| Growth Rate (2025 - 2030) | 9.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Wind Energy Market Analysis by Mordor Intelligence

The Portugal Wind Energy Market size in terms of installed base is expected to grow from 6.55 gigawatt in 2025 to 10.25 gigawatt by 2030, at a CAGR of 9.37% during the forecast period (2025-2030).

Policy reforms, streamlined permitting, and a strategic turn toward floating offshore platforms underpin this growth momentum. Corporate procurement led by data-center and tech firms is widening the buyer base beyond utilities, while grid-scale hybrid tenders slated for 2026 signal a structural pivot toward storage-backed projects. Accelerated repowering of aging onshore fleets, the availability of 9.4 GW of offshore zones approved in February 2025, and interest-rate normalization that trims financing spreads by 50–100 basis points collectively enhance project economics. Headline risks include grid congestion in Centro and Norte, rare-earth supply concentration, and the uncertainty surrounding Portugal’s inaugural floating-wind auction now scheduled for late 2025.

Key Report Takeaways

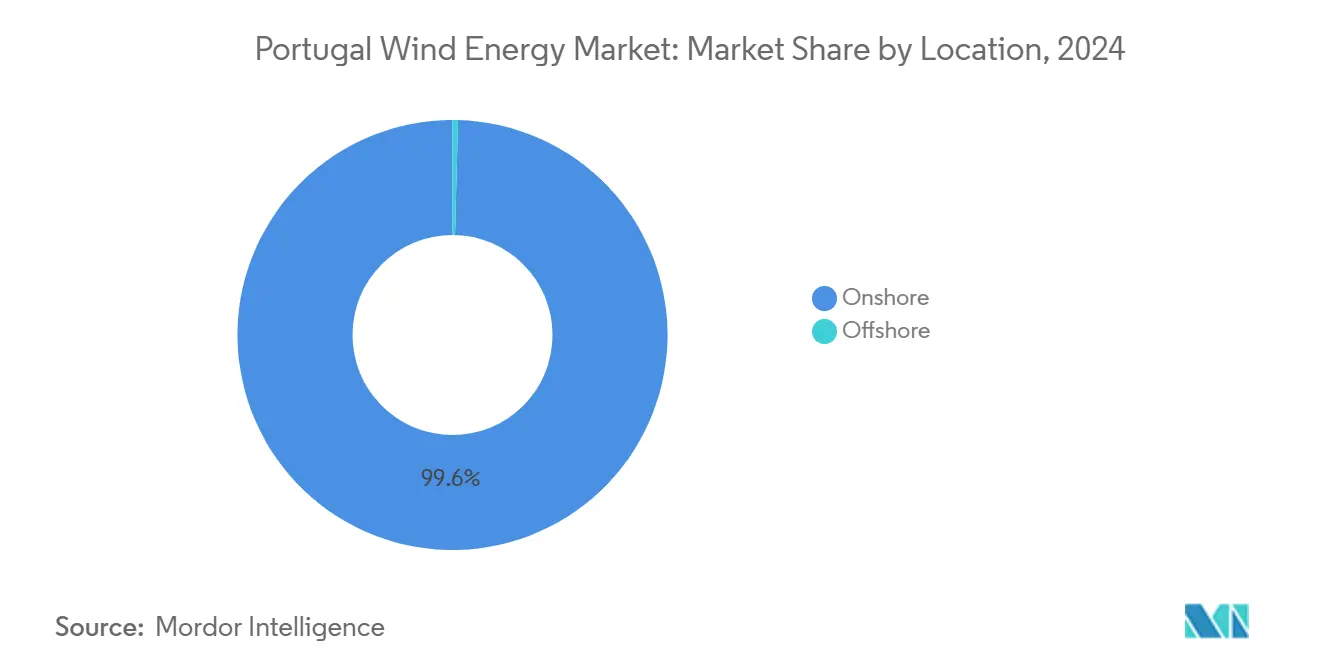

- Onshore wind captured 99.6% of the Portugal wind energy market share in 2024 and is advancing at a 9.4% CAGR to 2030.

- Turbines above 6 MW accounted for 27.9% of the Portugal wind energy market size in 2024 and represent the fastest-growing capacity tier at 27.9% CAGR through 2030.

- Utility-scale assets held 61.8% revenue share in 2024, while the commercial-and-industrial segment is forecast to expand at 16.5% CAGR between 2025-2030.

- Viana do Castelo–Leixões led offshore zone allocations with 45% of the designated capacity in the February 2025 PAER.

Portugal Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining LCOE for on- & offshore projects | +2.1% | National, with offshore zones in Viana do Castelo, Leixões, Figueira da Foz, Sines | Medium term (2-4 years) |

| EU RepowerEU wind capacity targets 2025-2030 | +1.8% | National, aligned with EU-wide mandates | Long term (≥ 4 years) |

| Grid-scale hybrid tenders including storage | +1.3% | Centro & Norte priority regions | Medium term (2-4 years) |

| Offshore supply-chain localisation incentives | +0.9% | Coastal zones, Port of Sines industrial cluster | Long term (≥ 4 years) |

| Corporate PPA boom from tech firms | +1.5% | Near Lisbon & Porto metro areas | Short term (≤ 2 years) |

| Port of Sines green-hydrogen corridor | +0.7% | Sines industrial zone, exports to Northern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining LCOE For On- & Offshore Projects

Auction clearing prices for onshore wind narrowed to EUR 40–50 /MWh in 2024, rendering new builds cheaper than combined-cycle gas even before carbon costs.[1]Fraunhofer ISE, “Cost Reduction Potentials for Floating Wind,” ise.fraunhofer.de Floating-wind LCOE still ranges between EUR 80–120 /MWh, yet serial fabrication of semi-submersible hulls could trim costs by 30% once the first 1 GW tranche is awarded. Repowering drives extra savings: replacing 2 MW machines with 6 MW models on existing pads cuts balance-of-system spending by 40% and doubles energy yield. Interest-rate normalization since late 2024 shaved 50–100 basis points off debt costs, lifting project internal returns. Material inflation lingers, however, with neodymium oxide hovering near USD 55.4/kg and China controlling 90% of rare-earth processing.[2]International Energy Agency, “Electricity 2025,” iea.org

EU RepowerEU Wind Capacity Targets 2025-2030

Portugal’s December 2024 National Energy and Climate Plan pledges a 51% renewable share by 2030 and 80% renewable electricity by 2026, implying ~800 MW of fresh wind capacity each year, double historic build rates.[3]Government of Portugal, “Plano Nacional Energia e Clima 2030,” portugal.gov.pt Reforms include a one-stop-shop permitting portal and elimination of environmental impact assessments, slashing approval timelines from 5–7 years to roughly 2–3 years. Digital licensing is scheduled for Q2 2026, underpinned by Recovery and Resilience Plan funds EC. Grid capacity lags, with REN confirming only 24% of queued renewables can connect under the present infrastructure. The postponed late-2025 offshore tender will test investor appetite amid floating-wind risk premiums.

Corporate PPA Boom From Data-Center & Tech Firms

Amazon’s 219 MW PPA with Iberdrola in February 2025 inaugurated hyperscale procurement in Portugal, locking long-term price certainty for cloud operations. EDP’s 2026-2028 plan allocates EUR 7.5 billion toward Iberian renewables, citing data-center electrification as a growth lever. Commercial-and-industrial demand is expanding at 16.5% CAGR as corporates seek additionality and hedge against volatility exposed during 2024 Dunkelflaute events IEA.ORG. Virtual PPA rules trail Spain’s maturity level, raising balancing-cost risk, but Decree-Law 99/2024 doubled energy-sharing radii, enabling medium-sized enterprises to tap proximal wind farms without grid fees.

Port of Sines Green-Hydrogen Export Corridor

GreenH2Atlantic’s 100 MW electrolyser, backed by EUR 30 million from the EU Innovation Fund, will absorb 450 GWh a year of renewable generation and export hydrogen to Northern Europe via repurposed pipelines. Private-wire links allow wind farms to monetize curtailed output without waiting for grid upgrades, an advantage in congestion-prone Centro and Norte. The European Hydrogen Backbone envisions 1,200 km of Portuguese lines by 2040, though tariff harmonization remains pending. If Sines proves reliable by 2027, electrolyser additions of 500–1,000 MW could materialize, effectively doubling wind-linked offtake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited onshore land & permitting delays | -1.2% | National, acute in Centro & Norte | Short term (≤ 2 years) |

| Fishermen & tourism opposition offshore | -0.8% | Viana do Castelo, Leixões, Figueira da Foz, Sines | Medium term (2-4 years) |

| Rising raw-material costs | -1.0% | Global supply, China-centric rare-earth processing | Short term (≤ 2 years) |

| Grid congestion | -1.5% | Centro & Norte | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Onshore Land Availability & Permitting Bottlenecks

Competing land uses and social pushback constrain new sites, but January 2025 legislation removed environmental impact assessments for renewables, halving approval times. ENSPRESO 2 shows that onshore potential could double if setback distances are optimized, though looser buffers risk local opposition. Repowering on legacy pads skirts new land acquisition, yet must satisfy updated noise standards. A 500-staff one-stop-shop set for Q2 2026 aims to centralize approvals, but municipal coordination remains critical.

Grid Congestion In Centro & Norte Regions

REN states only 24% of queued renewables can interconnect today, necessitating a 4.15-fold ARC expansion. The EUR 3.6 billion network-upgrade plan through 2028 targets new substations and 400 kV lines, yet build times average 4–6 years. Curtailment erased 3–5% of potential wind output in 2024, and Spanish interconnectors hit capacity 15% of the year, triggering negative Iberian prices. Hybrid wind-solar-battery projects, prioritized in 2026 tenders, lessen node stress, but transmission remains the binding constraint through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Ambition Meets Onshore Pragmatism

Onshore assets represented 99.6% of the Portugal wind energy market share in 2024 and will compound at 9.4% through 2030, anchored by repowering and larger 6 MW-plus turbines. The Portugal wind energy market size addition to onshore alone, is forecast at 3.4 GW over 2025-2030. Offshore capacity was negligible in 2024, but the February 2025 PAER carved out 9.4 GW of floating-wind zones, enough to meet the 2 GW 2030 target even after a 15% area reduction.

Floating projects face higher LCOE and contract-for-difference dependence, yet unlock growth in a land-constrained country. Ocean Winds and Principle Power intend to leverage WindFloat Atlantic experience in the late-2025 auction, while the Port of Sines positions itself as a fabrication hub offering deep-water assembly and local-content incentives.[4]Iberdrola, “Tâmega Project Factsheet,” iberdrola.com

By Turbine Capacity: The 6 MW Inflection Point

Turbines under 3 MW still cover 52.5% of installed units, but machines above 6 MW logged a 27.9% CAGR in 2024 and will dominate new builds by 2027, capturing the largest slice of the Portugal wind energy market size expansion. Direct-drive 10–15 MW models suit floating foundations, despite 30–40% higher rare-earth intensity. The 3–6 MW bracket fills repowering gaps where logistics or aviation rules cap tip heights, yet dwindles after 2028 as blade transport corridors improve and modular tower concepts spread.

Longer blades stress road infrastructure; hence, tower-base assembly at ports and segmental blade designs are under study. Rare-earth dependence spurs R&D into electrically excited generators, but commercialization is unlikely before 2030.

By Application: Corporate Procurement Reshapes Offtake Models

Utility-scale plants held a 61.8% share in 2024, yet commercial-and-industrial demand is set to triple utility growth at a 16.5% CAGR as hyperscalers and manufacturers lock in PPAs. The Portugal wind energy market size tied to corporate PPAs could exceed 1 GW by 2030, driven by data-center clusters near Lisbon and Porto that value long-run price certainty.

Community projects remain modest but gain traction under Decree-Law 99/2024, which widened energy-sharing radii to 40 km in sparsely populated areas. Hybridization with solar and storage further sweeps small municipalities into the value chain, although financing models for cooperatives still hinge on EU recovery grants.

Geography Analysis

Centro and Norte host most legacy capacity yet suffer the sharpest grid congestion, with only one-quarter of queued assets able to connect under the current Accelerating Renewable Connections (ARC). EUR 3.6 billion in network upgrades through 2028 targets new 400 kV backbones, but commissioning dates trail wind build schedules by several years. Southern Portugal leverages the Port of Sines’ deep-water berths and the GreenH2Atlantic electrolyser, which consumes 450 GWh per year via private wires, bypassing bottlenecks and creating export pathways to Germany and the Netherlands.

Offshore zones spanning 2,000 km², Viana do Castelo, Leixões, Figueira da Foz, Sines, enable floating foundations in 75–500 m depths, widening development prospects where onshore land is scarce. Viana do Castelo and Leixões enjoy proximity to Porto’s industrial base for supply-chain localization, while Sines integrates hydrogen and fabrication synergies. Spanish interconnectors hit technical limits 15% of 2024, amplifying Iberian price volatility and underlining the need for the proposed 1 GW Portugal-France line by 2029.

Competitive Landscape

The Portugal wind energy market shows moderate concentration. Vestas, Siemens Gamesa, and Nordex dominate onshore turbines, while GE Vernova eyes offshore entries. Iberdrola’s 38-unit Vestas Enventus order for the EUR 350 million Tâmega complex underscores Vestas’ lead in 6–8 MW machines. Ocean Winds and Principle Power target floating projects leveraging WindFloat credentials, and local IPPs such as Greenvolt are divesting mature assets to recycle capital, signaling consolidation.

Technology competition pivots on drivetrain choices: direct-drive permanent-magnet models excel offshore but heighten rare-earth exposure. Electrically excited alternatives remain pre-commercial. Asset-rotation strategies, such as Masdar’s 2024 acquisition of Saeta Yield, illustrate foreign capital’s appetite for operational portfolios underpinned by stable Iberian PPAs. Regulatory acumen confers an edge; January 2025’s EIA waiver favors developers with shovel-ready sites, while a Q2 2026 one-stop shop aims to standardize approvals.

Portugal Wind Energy Industry Leaders

EDP Renováveis S.A.

Iberdrola Renovables Portugal

Finerge

Greenvolt

Voltalia Portugal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Etermar Energia has been awarded a contract by Ørsted and PGE Polska Grupa Energetyczna (PGE) for the delivery of secondary foundation structures for the 1.5 GW Baltica 2 offshore wind farm in Poland.

- February 2025: Quadrante unveiled a 244 MW onshore development at the repurposed Pego Thermal plant, enough to supply 24,000 households and displace 1% of national electricity demand.

- January 2025: Tokyo Gas acquired 21.2% of the WindFloat Atlantic floating offshore project, marking its first direct overseas floating-wind stake, to build experience ahead of commercial auctions.

- December 2024: Iberdrola has secured a production license for what will be Portugal's largest wind farm, a 274 MW project in the Vila Real and Braga districts. This project, which will integrate with the Tâmega Power Plant System, highlights the ongoing interest of utilities in developing new, large-scale renewable energy projects.

Portugal Wind Energy Market Report Scope

Wind energy refers to the process of harnessing the power of wind to generate electricity. It is a form of renewable energy that uses kinetic energy present in moving air masses to produce electrical power. Wind energy is commonly harvested using wind turbines, which consist of large rotating blades mounted on a tall tower.

The Portugal wind energy market is segmented by location, turbine capacity, and application. By location, the market is segmented into onshore and offshore. By turbine capacity, the market is segmented into up to 3 MW, 3 to 6 MW, and above 6 MW. By application, the market is segmented into utility-scale, commercial and industrial, and community projects. The report offers market sizes and forecasts in terms of installed capacity (GW) for all the above segments.

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How large is the Portugal wind energy market today?

Installed capacity stood at 6.55 GW in 2025 and is on track for 10.25 GW by 2030, growing at 9.37% CAGR.

What share of capacity is onshore versus offshore?

Onshore assets held 99.6% in 2024; offshore is negligible now but aims for 2 GW by 2030.

Which turbine class is expanding the fastest?

Units above 6 MW are rising at 27.9% CAGR as repowering and offshore projects favor larger machines.

Why are corporate PPAs important in Portugal?

Data-center and tech firms are driving a 16.5% CAGR in commercial-and-industrial demand, locking in stable prices and underwriting new builds.

Where are the main grid bottlenecks?

Centro and Norte regions can connect only 24% of queued renewables under current capacity, necessitating major transmission upgrades.

How will hydrogen impact wind development?

The 100 MW GreenH2Atlantic electrolyser at Sines will absorb curtailed wind output and could catalyze 5001,000 MW of additional capacity by 2030.

Page last updated on: