Market Overview

| Study Period | 2019 - 2030 |

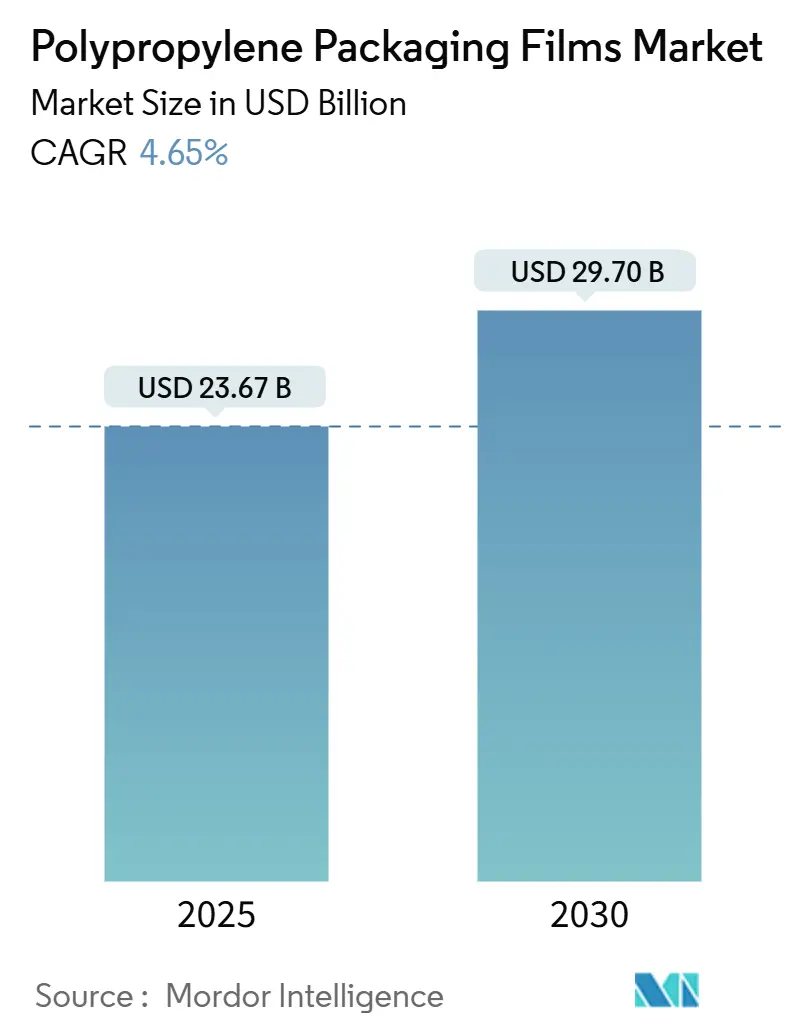

| Market Size (2025) | USD 23.67 Billion |

| Market Size (2030) | USD 29.70 Billion |

| Growth Rate (2025 - 2030) | 4.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

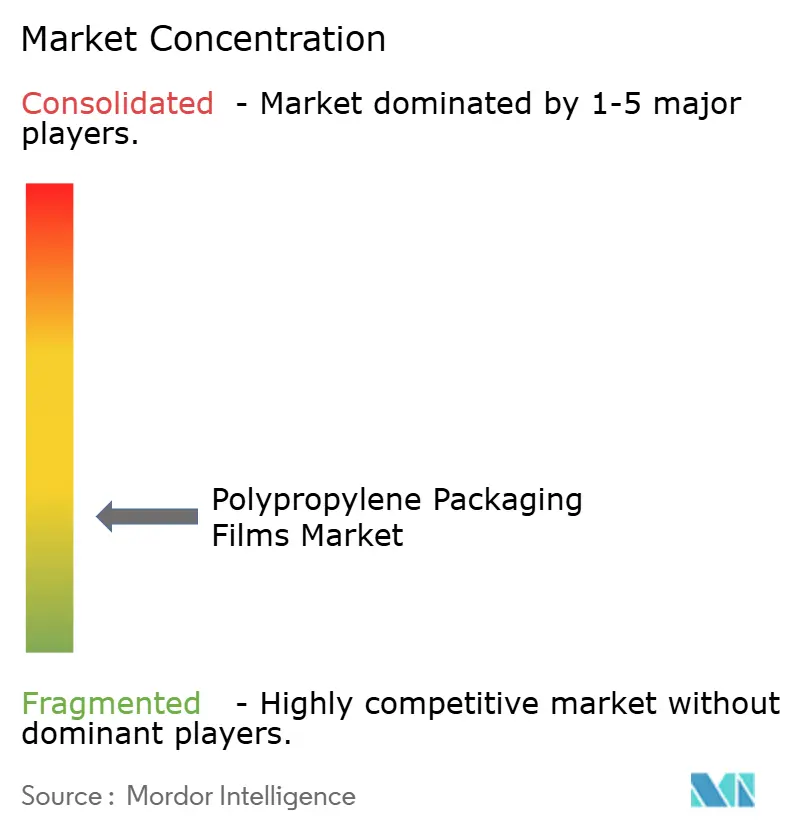

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polypropylene Packaging Films Market Analysis by Mordor Intelligence

The polypropylene packaging films market size reached USD 23.67 billion in 2025 and is forecast to climb to USD 29.70 billion by 2030, advancing at a 4.65% CAGR. Growth is propelled by brand‐owner commitments to recyclable mono-material laminates, regulatory pressure in Europe and North America, and faster commercial deployment of chemical-recycled polypropylene resins. Producers are expanding capacity in Southeast Asia, trimming average global film prices and supporting demand from cost-sensitive applications. Feedstock volatility remains a headwind, yet converters continue to substitute rigid formats with flexible solutions that trim logistics costs and carbon footprints.

Key Report Takeaways

- By film type, BOPP led with 66.43% of polypropylene packaging films market share in 2024, while CPP is projected to log the fastest 7.08% CAGR to 2030.

- By packaging format, wraps and over-wraps held a 28.45% share of the polypropylene packaging films market size in 2024; labels and pressure-sensitive tapes are expected to grow at an 8.16% CAGR through 2030.

- By end-use industry, food applications accounted for 41.56% of the polypropylene packaging films market size in 2024; pharmaceutical and healthcare is poised for a 6.29% CAGR to 2030.

- By geography, Asia-Pacific commanded 44.01% revenue in 2024 and is forecast to expand at a 6.42% CAGR to 2030.

Global Polypropylene Packaging Films Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable shift from rigid to flexible formats | +1.2% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Brand owner demand for mono-material recycle-ready laminates | +0.8% | Europe and North America primarily, expanding to APAC | Short term (≤ 2 years) |

| Retort-grade CPP replacing multilayer high-barrier structures | +0.6% | Global, with concentration in developed food markets | Medium term (2-4 years) |

| E-commerce boom driving high-clarity over-wrap films | +0.7% | Global, with highest impact in APAC and North America | Short term (≤ 2 years) |

| Rapid capacity additions in Southeast Asia lowering film prices | +0.5% | APAC core, spill-over to global markets | Long term (≥ 4 years) |

| Chemical-recycling derived PP resin commercialization | +0.4% | North America and Europe initially, expanding globally | Long term (≥ 4 years) |

Source: Mordor Intelligence

Sustainable Shift from Rigid to Flexible Formats

Reducing package weight by as much as 75% versus rigid plastics, flexible polypropylene films help brand owners curb freight emissions and material costs. Klöckner Pentaplast’s kp FlexiFlow range delivers recyclable flow-wrap structures containing more than 93% polypropylene, illustrating performance parity with legacy formats while offering circularity.[1]Klöckner Pentaplast, “kp launches best-in-class duo of recyclable barrier flow wrap films,” kpfilms.com Multinationals adopt refill pouches for home-care and personal-care goods, lowering source-reduction fees under Extended Producer Responsibility rules. Film producers leverage downgauging and higher post-consumer-recycled resin loads without sacrificing puncture strength, solidifying polypropylene’s role as a lightweight alternative across e-commerce and retail channels.

Brand Owner Demand for Mono-Material Recycle-Ready Laminates

DNP’s polypropylene-based mono-material laminates meet CEFLEX design guidelines, allowing high-speed form-fill-seal operations while entering existing recycling streams.[2]DNP Group, “DNP's Mono-Material Packaging,” global.dnp European Packaging and Packaging Waste Regulation targets accelerate adoption, prompting Saica Flex to develop 100% recyclable solutions that incorporate 5% certified post-consumer content. Barrier-coating advances such as ORMOCER and new acrylic chemistries achieve oxygen transmission rates below 0.1 cm³/m²·day·bar, aligning shelf-life demands with recyclability. Brand owners accept small cost premiums to reach 2030 circularity pledges, spurring rapid substitution of mixed-material foil laminates.

Retort-Grade CPP Replacing Multilayer High-Barrier Structures

Polyplex retort-grade CPP withstands 135 °C sterilization cycles for 30 minutes and maintains seal integrity, enabling producers of ready-to-eat meals to migrate from complex PET/aluminum/PP laminates toward single-material packaging streams.[3]Polyplex Corporation Ltd., “Retort,” polyplex.com New copolymer architectures boost flexibility, solving brittleness concerns and expanding usage in tuna pouches, wet pet food, and baby foods. Metallized CPP variants now deliver water vapor transmission rates under 0.4 g/m²·day, eliminating extra barrier layers and cutting laminate thickness by up to 15%. Regulatory moves that penalize unrecyclable structures further accelerate CPP penetration.

E-commerce Boom Driving High-Clarity Over-Wrap Films

Online grocery and electronics channels raise demand for transparent over-wraps that combine shelf appeal with abrasion resistance. India’s e-commerce packaging spend is projected to more than double between 2019 and 2025, with flexible films minimizing shipping breakage. [4]International Business Portal, “Indian Packaging Industry Riding on the E-Commerce Wave,” ibef.orgConverters formulate BOPP grades offering gloss above 90 GU and haze below 2% while retaining tear resistance suited to automated wrapping lines. Over-wrap adoption extends into fresh produce and bakery bags, where visual quality signals freshness to online shoppers. High-clarity films also support printed brand messaging that survives the rigors of last-mile delivery.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in propylene and naphtha feedstock prices | -0.9% | Global, with highest impact in import-dependent regions | Short term (≤ 2 years) |

| Growing PET and PE mono-material barrier film substitutes | -0.6% | Europe and North America primarily | Medium term (2-4 years) |

| Trade-flow disruptions from carbon-border-adjustment tariffs | -0.4% | Southeast Asia to EU trade corridors | Medium term (2-4 years) |

| Extended Producer Responsibility compliance costs | -0.3% | Europe primarily, expanding to other regions | Long term (≥ 4 years) |

Source: Mordor Intelligence

Volatility in Propylene and Naphtha Feedstock Prices

Polymer-grade propylene rose 4–5 cents / lb in early 2025 after refinery closures tightened supply, squeezing converter margins. South Asian raffia grades climbed to USD 970–990 / t, reflecting geopolitical pressures on crude benchmarks. Film makers struggle to pass through surcharges in commoditized snack wraps, prompting some regional packers to trial less volatile polyethylene films. Persistent uncertainty complicates annual supply tenders and deters capital spending on new orientation lines.

Growing PET and PE Mono-Material Barrier Film Substitutes

Recyclable full-PE barrier pouches with >95% polyethylene content showcase oxygen barriers once exclusive to polypropylene, intensifying competition in coffee and condiments. PET boasts robust bottle-to-bottle infrastructure, appealing to beverage brands chasing high post-consumer content targets. Cost convergence and superior recyclate clarity persuade several North American personal-care labels to reevaluate substrate choices. Polypropylene suppliers counter by enhancing barrier coatings and funding chemical-recycling startups, yet substitution pressure persists in premium niches.

Segment Analysis

By Film Type: BOPP Dominance Challenged by CPP Innovation

BOPP led the polypropylene packaging films market with 66.43% share in 2024, reflecting broad adoption in snack, bakery, and tobacco over-wraps. Coated BOPP grades with acrylic or PVDC layers extend shelf life in confectionery while retaining low density advantages. Cosmo Films operates 196,000 t / y capacity that supports global distribution, reinforcing BOPP supply security. Volume also flows from new Southeast Asian lines that lower delivered costs into price-sensitive African markets.

CPP posted the quickest 7.08% CAGR forecast, propelled by retort pouches and metallized snack wraps. Mitsui’s RXC-22 cast film seals at lower temperatures, trimming energy use on high-speed form-fill-seal machinery. Specialty CPP competes in medical packaging where clarity, chemical resistance, and gamma sterilization tolerance matter. The polypropylene packaging films market size for CPP is set to expand alongside demand for mono-material pouch laminates that facilitate recycling streams. Other niche grades, including breathable microporous films for produce, carve out incremental revenue by solving specific moisture and gas-exchange needs.

By Packaging Format: E-commerce Drives Label Innovation

Wraps and over-wraps retained 28.45% of polypropylene packaging films market share in 2024, serving as the default protection for confectionery multipacks, fresh produce trays, and CDs. Brand owners blur the line between protection and branding by printing QR codes that link to product authenticity checks. In parallel, labels and pressure-sensitive tapes record an anticipated 8.16% CAGR, outperforming other formats as e-retailers automate fulfillment centres. Ultra-clear BOPP label stock enables see-through imagery on personal-care bottles, reinforcing shelf differentiation for premium shampoos.

Pouches gain momentum in soups, sauces, and dry mixes because of improved consumer convenience. Lidding films capitalize on microwave-ready meals, integrating anti-fog coatings that keep condensation off the viewing window. The polypropylene packaging films market size for bags and pouches benefits from the pandemic-induced rise in single-serve portions, especially in Asia’s fast-moving consumer goods sector. Blister and strip packs stay niche but defensible in pharmaceuticals; polypropylene ensures moisture protection and meets ISO 10993 biocompatibility requirements for medical-device components.

By End-use Industry: Healthcare Acceleration Amid Food Dominance

Food retained 41.56% of polypropylene packaging films market size in 2024, spanning muffins to frozen seafood. High-clarity BOPP stabilizes flavor compounds and supports vivid reverse printing, aiding brand recognition on crowded shelves. Breathable TPX specialty films extend shelf life for fresh produce by balancing CO₂ and O₂ exchange. Snack manufacturers also down-gauge film thickness by 8–10 %, cutting material costs without compromising machinability.

Pharmaceutical and healthcare segments are projected to grow at 6.29% CAGR, fueled by stricter sterility demands and aging demographics. LyondellBasell’s Purell grades offer pre-qualified compliance dossiers, streamlining drug-master-file submissions for blister and IV-bag converters. Polypropylene’s chemical resistance outperforms PVC in aggressive topical ointments, encouraging switchovers. Personal-care products leverage glossy BOPP for monolayer tubes that stand upright on retail shelves, while industrial applications such as fertilizer bag liners value polypropylene’s tensile strength and moisture barrier.

Geography Analysis

Asia-Pacific controlled 44.01% of global revenue in 2024 and is poised for a 6.42% CAGR through 2030. China’s forecast 2.6 million-ton polypropylene export pool underpins ample film resin supply. Indonesia’s national demand of 5.2 million t outstrips domestic capacity of 2.4 million t, necessitating imports even as anti-dumping duties target regional suppliers. Vietnam’s Long Son cracker restart in late 2025 will add 400,000 t / y of polypropylene, narrowing deficits and supporting regional downstream processors. Cost-competitive labor and an expanding middle class sustain robust demand across FMCG, pharmaceutical, and electronics supply chains.

Europe remains a technology leader despite modest volume growth. Extended Producer Responsibility fees now vary by recyclability, nudging brands toward mono-material polypropylene solutions. The forthcoming Carbon Border Adjustment Mechanism may impose reporting obligations and implicit carbon costs on imported films, potentially eroding Southeast Asian price advantages. European converters invest in advanced de-inking and solvent-based recycling plants to close material loops, while Ineos ramps recycled-plastic output at its French cracker to comply with EU PPWR mandates.

North America benefits from high food-safety standards and deep e-commerce penetration but battles feedstock-linked cost swings. PureCycle’s Ohio plant now produces 107 million lb / y of ultra-pure recycled polypropylene, supplying converters that need FDA-compliant recyclate. US polypropylene imports totaled USD 789.2 million in 2021, revealing reliance on overseas monomer when domestic crackers prioritize polyethylene derivatives. Investment in chemical recycling pilot lines accelerates as state legislation sets recycled-content thresholds for flexible packaging.

Competitive Landscape

The polypropylene packaging films market sits at a fragmented level. Large players pursue vertical integration to secure resin supply and speed recyclate adoption. Cosmo Films leverages global thermal-laminate leadership to cross-sell coated BOPP into emerging snack brands, sustaining economies of scale. SRF Limited’s order for a third BOBST EXPERT K5 metallizer evidences capital intensity needed to offer high-barrier clear films that meet oxygen-sensitive food needs.

Strategic alliances focus on recycled feedstock access. Amcor’s memorandum with NOVA Chemicals guarantees mechanically recycled polyethylene for film blends that must hit 30% post-consumer content targets by 2030. Producers also evaluate bio-based routes; Braskem’s US feasibility study on carbon-negative polypropylene would supply converters seeking low-carbon footprints for premium goods. Smaller Asian converters consolidate—Plastchim-T’s acquisition of Manucor raises combined BOPP tonnage above 200,000 t, enabling competitive pricing into EMEA snack accounts.

Advanced recycling technologies serve as competitive differentiators. Honeywell granted Evertis its newest solvent-based barrier-film recycling license, facilitating pharmaceutical pack circularity while maintaining stringent purity levels. Innovators offering metallized polypropylene that delaminates in aqueous media gain traction as converters look to preserve aluminum barrier while easing recycling. Overall, rivalry intensifies around sustainable performance attributes rather than price alone.

Polypropylene Packaging Films Industry Leaders

-

Jindal Poly Films Ltd

-

CCL Industries ( Innovia Films)

-

Cosmo Films Ltd.

-

SRF Limited

-

Plastchim-T

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Amcor and Berry Global announced an USD 8.4 billion all-stock merger that will pool their BOPP, CPP and specialty-film assets, forming the world’s largest supplier of polypropylene packaging films.

- October 2024: Klöckner Pentaplast introduced kp FlexiFlow EH 155 R and kp FlexiFlow PH 255 R flow-wrap films containing 93% polypropylene, cutting pack weight by up to 75% versus comparable rigid formats

- September 2024: SRF Limited ordered a third BOBST EXPERT K5 metallizer for its Rayong, Thailand plant, expanding high-barrier BOPP film capacity aimed at snack and confectionery customers.

- May 2024: Bulgaria’s Plastchim-T acquired Italian BOPP producer Manucor, adding 200,000 t per year of oriented polypropylene film capacity and strengthening supply across Europe, the Middle East and Africa.

Global Polypropylene Packaging Films Market Report Scope

Polypropylene packaging film, a thermoplastic material, stands out for its cost-effectiveness and 100% recyclability. This low-density plastic film boasts clarity, a high gloss finish, and impressive tensile strength. Designed to protect surfaces from permanent damage, polypropylene packaging films also provide excellent optical clarity at a lower cost, making them the preferred choice for flexible packaging applications.

The polypropylene packaging films market is segmented by type (BOPP and CPP), application (food, beverage, pharmaceutical and healthcare, and industrial), and geography (North America [United States, and Canada], Europe [United Kingdom, Germany, France, and Rest of Europe], Asia-Pacific [China, India, Japan, and Rest of Asia-Pacific], Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of volume (tonnes) for all the above segments.

| By Film Type | Biaxially Oriented Polypropylene (BOPP) Film | Coated BOPP (PVDC, Acrylic, EVOH) | ||

| Uncoated BOPP | ||||

| Chlorinated Polypropylene (CPP) Film | General-purpose CPP | |||

| Retort-grade CPP | ||||

| Metalized CPP | ||||

| Other Polypropylene (PP) Packaging Films | ||||

| By Packaging Format | Wraps and Over-wraps | |||

| Labels and Pressure-sensitive Tapes | ||||

| Bags and Pouches | ||||

| Lidding and Flow-wrap Films | ||||

| Blister and Strip Packs | ||||

| By End-use Industry | Food | Bakery and Confectionery | ||

| Snacks and Breakfast Cereals | ||||

| Fresh Produce | ||||

| Meat, Poultry and Seafood | ||||

| Dairy Products | ||||

| Beverage | Non-Alcoholic | Bottled Water | ||

| Carbonated Drinks | ||||

| Juices | ||||

| Other Non-Alcoholic Beverages | ||||

| Alcoholic | Beer | |||

| Spirits | ||||

| Other Alcoholic Beverages | ||||

| Pharmaceutical and Healthcare | ||||

| Personal Care and Cosmetics | ||||

| Industrial | ||||

| Other End-use Industry | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Kenya | ||||

| Rest of Africa | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

By Film Type

| Biaxially Oriented Polypropylene (BOPP) Film | Coated BOPP (PVDC, Acrylic, EVOH) |

| Uncoated BOPP | |

| Chlorinated Polypropylene (CPP) Film | General-purpose CPP |

| Retort-grade CPP | |

| Metalized CPP | |

| Other Polypropylene (PP) Packaging Films |

By Packaging Format

| Wraps and Over-wraps |

| Labels and Pressure-sensitive Tapes |

| Bags and Pouches |

| Lidding and Flow-wrap Films |

| Blister and Strip Packs |

By End-use Industry

| Food | Bakery and Confectionery | ||

| Snacks and Breakfast Cereals | |||

| Fresh Produce | |||

| Meat, Poultry and Seafood | |||

| Dairy Products | |||

| Beverage | Non-Alcoholic | Bottled Water | |

| Carbonated Drinks | |||

| Juices | |||

| Other Non-Alcoholic Beverages | |||

| Alcoholic | Beer | ||

| Spirits | |||

| Other Alcoholic Beverages | |||

| Pharmaceutical and Healthcare | |||

| Personal Care and Cosmetics | |||

| Industrial | |||

| Other End-use Industry | |||

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the polypropylene packaging films market?

The market generated USD 23.67 billion in 2025 and is forecast to reach USD 29.70 billion by 2030.

Which region leads demand for polypropylene packaging films?

Asia-Pacific holds 44.01% of global revenue and is also the fastest-growing region with a projected 6.42% CAGR to 2030.

Why are cast polypropylene (CPP) films growing faster than BOPP?

CPP gains from retort-grade innovations that let food brands shift to mono-material pouches capable of high-temperature sterilization, driving a 7.08% CAGR.

How are sustainability regulations affecting market dynamics?

EU Extended Producer Responsibility fees and the upcoming Carbon Border Adjustment Mechanism push converters toward recyclable mono-material laminates and local recycled-content sourcing.

What impact does feedstock volatility have on film pricing?

Unpredictable propylene and naphtha costs add short-term margin pressure, with early-2025 polymer-grade propylene prices up 4–5 cents / lb, encouraging some users to explore PET or PE alternatives.

Which end-use sector shows the highest growth potential?

Pharmaceutical and healthcare packaging is forecast to expand at a 6.29% CAGR thanks to demand for medical-grade polypropylene films that meet sterility and regulatory benchmarks.

Page last updated on: June 23, 2025