Polypropylene Catalyst Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

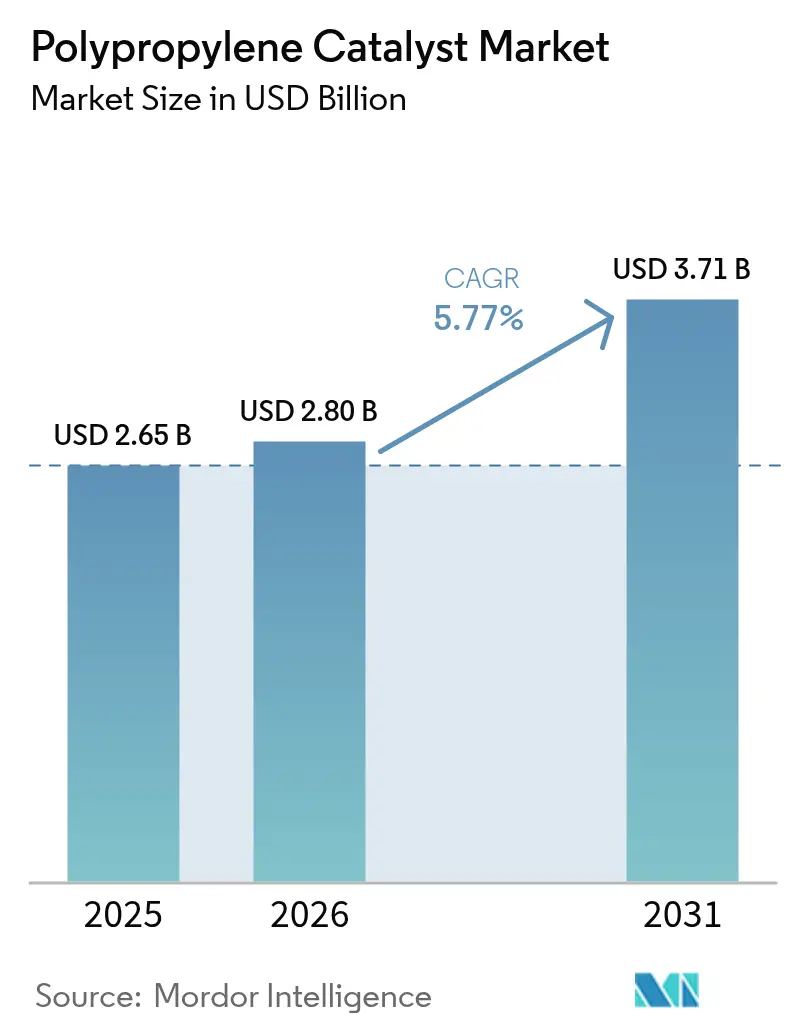

| Market Size (2026) | USD 2.8 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polypropylene Catalyst Market Analysis by Mordor Intelligence

The polypropylene catalyst market size in 2026 is estimated at USD 2.8 billion, growing from 2025 value of USD 2.65 billion with 2031 projections showing USD 3.71 billion, growing at 5.77% CAGR over 2026-2031. Capacity additions in Asia-Pacific, swift adoption of phthalate-free technologies, and a steady pull from applications such as flexible packaging and medical devices reinforce near-term resilience. Robust e-commerce activity drives thin-wall packaging demand, while automotive lightweighting and additive-manufacturing grades open premium niches that favour metallocene and other high-performance systems. Intensifying industry consolidation—exemplified by Honeywell’s pending acquisition of Johnson Matthey’s Catalyst Technologies unit—signals a decisive push for scale and integrated R&D. Ongoing propylene price volatility and stricter global regulations on phthalates, however, continue to pressure margins and accelerate the shift toward novel catalyst formulations.

Key Report Takeaways

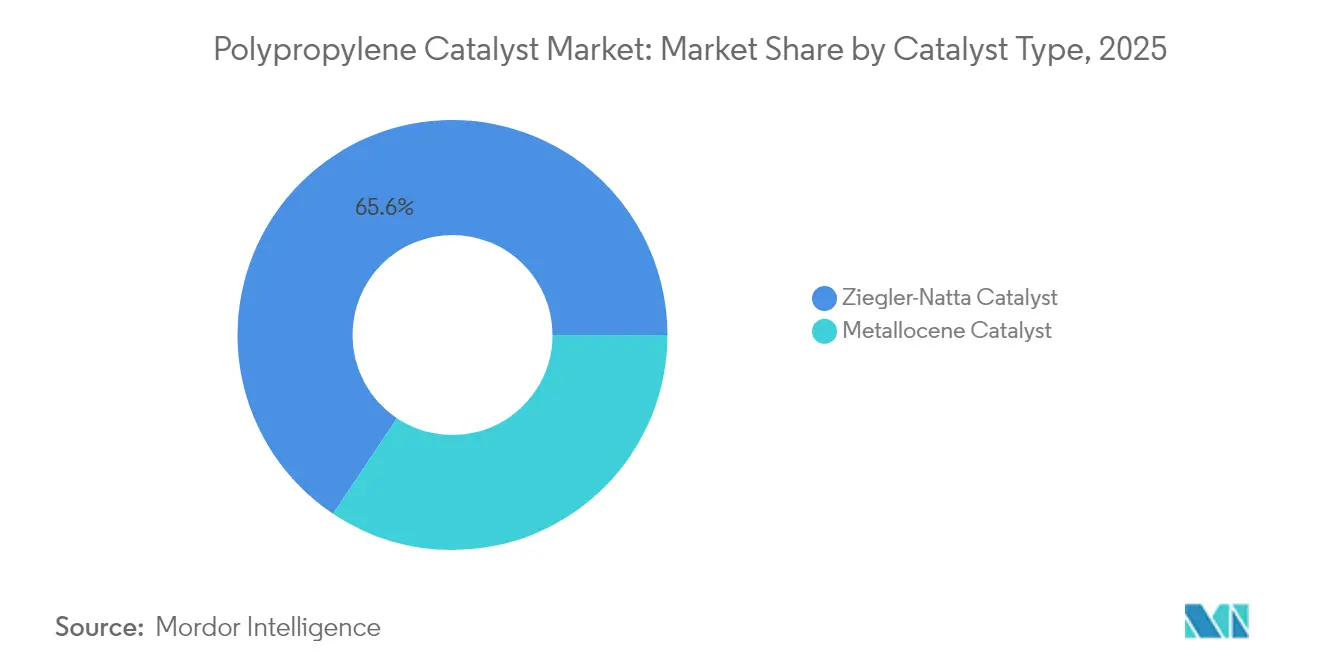

- By catalyst type, Ziegler-Natta systems led with 65.62% of polypropylene catalyst market share in 2025, whereas metallocene variants are projected to deliver the fastest 7.79% CAGR to 2031.

- By production process, gas-phase technology accounted for 46.55% of the polypropylene catalyst market size in 2025; hybrid/multi-reactor configurations offer the highest 6.44% CAGR through 2031.

- By application, the polypropylene segment captured 63.75% revenue share in 2025, advancing at the fastest CAGR of 8.25% through 2031.

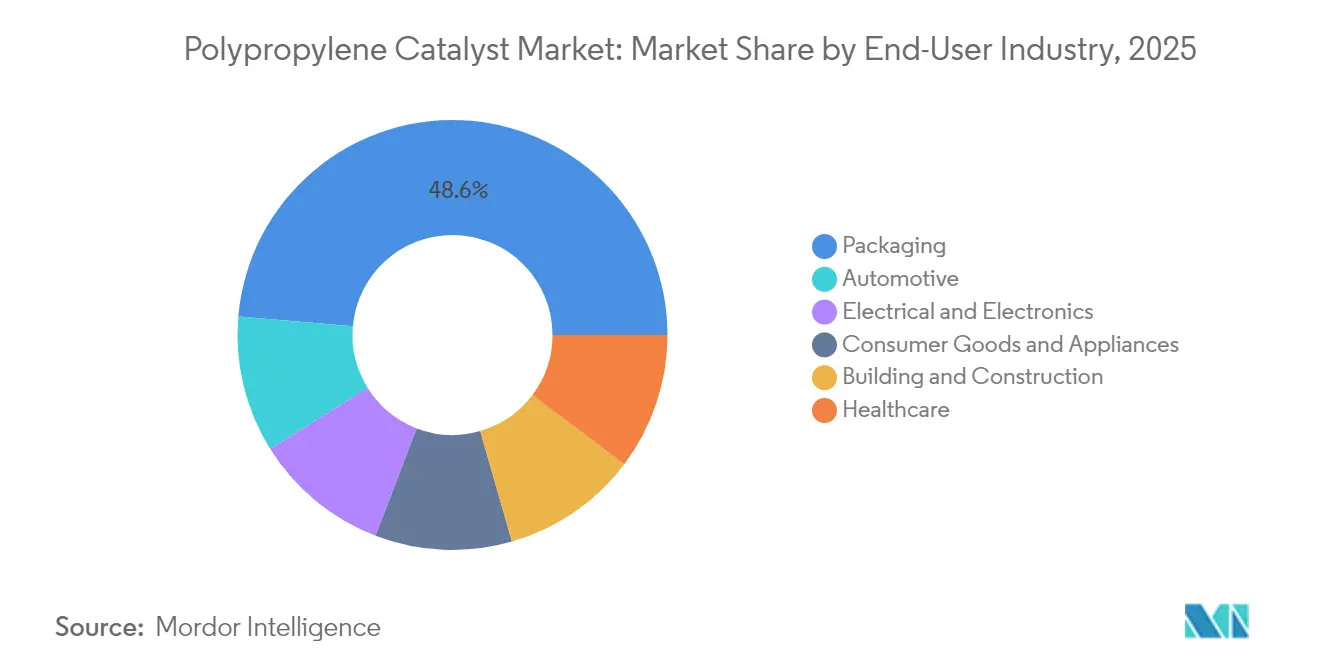

- By end-user industry, packaging sustained its dominance in the polypropylene catalyst market share during 2025, yet healthcare underpins the steepest CAGR through the forecast window.

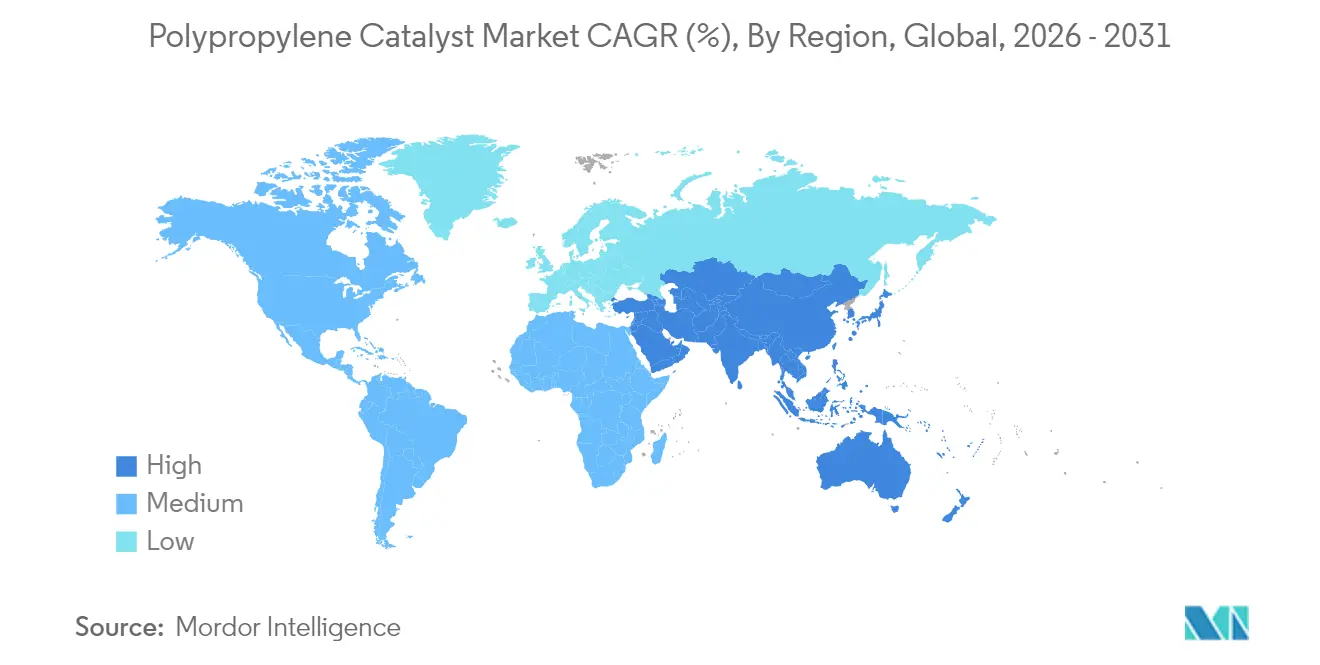

- By region, Asia-Pacific accounted for the largest share of 51.64% in 2025, and is expected to grow at the fastest CAGR of 6.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polypropylene Catalyst Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capacity expansions in emerging PP hubs | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| E-commerce-led surge in flexible packaging demand | +0.8% | Global, with concentration in North America & APAC | Short term (≤ 2 years) |

| Automotive lightweighting initiatives | +0.6% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Regulatory shift toward phthalate-free catalysts | +0.7% | Global, led by EU and North America | Medium term (2-4 years) |

| In-house catalyst recycling & regeneration | +0.4% | Developed markets, gradual APAC adoption | Long term (≥ 4 years) |

| High-melt-flow PP for additive manufacturing | +0.3% | North America & EU, niche APAC segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capacity Expansions in Emerging PP Hubs

Ongoing megaprojects, such as SABIC’s USD 6.4 billion Fujian Petrochemical Complex slated for 2026 commissioning, illustrate how large-scale investments are redefining regional supply nodes and pulling through catalyst demand at massive volumes[1]SABIC, “SABIC To Build Fujian Petrochemical Complex,” sabic.com. China alone plans 26 million tons of new ethylene capacity between 2023 and 2027, tilting global balances and compelling catalyst producers to localize manufacturing footprints to capture freight and service advantages[2]Nikkei Asia, “Japan Ethylene Output Hits 35-Year Low,” nikkei.com. This expansion also heightens oversupply risk, forcing older crackers in Japan and parts of Southeast Asia to slow or suspend operations. As Gulf producers build domestic catalyst capabilities, proprietary know-how is becoming pivotal to sustain cost leadership and differentiate in tight-margin environments.

E-commerce-Led Surge in Flexible Packaging Demand

A sharp rise in online retail continues to swell thin-wall packaging volumes. Asia-Pacific remains the largest consumption zone as China and India expand packaging lines to serve urbanizing populations. Brands are mandating fully recyclable solutions, steering investments toward high-melt-strength PP grades and non-phthalate catalysts that improve clarity and stiffness while satisfying regulatory thresholds. Capacity build-outs, however, have outpaced demand in India, trimming average industry operating margins to near-decade lows and underscoring the sector’s cyclical character.

Automotive Lightweighting Initiatives

Original equipment manufacturers are shifting aggressively toward lightweight plastics to compensate for heavier electric-vehicle battery packs. High-melt-flow PP foams produced with sophisticated metallocene or modified Ziegler-Natta catalysts support complex geometries and crash-resistance targets. Recent investments exceeding EUR 100 million to triple Daploy high-melt-strength PP capacity in Europe highlight technology leverage in this arena. Catalyst suppliers must deliver tight molecular-weight distributions and narrow comonomer incorporation windows that enable low-density foams without sacrificing impact strength, opening premium pricing latitude despite feedstock headwinds.

Regulatory Shift Toward Phthalate-Free Catalysts

The European Union’s Regulation (EU) 2025/351 introduces stringent migration limits and traceability requirements that effectively steer the global industry away from phthalate ester donors[3].European Commission, “Regulation (EU) 2025/351,” eur-lex.europa.eu China’s January 2026 RoHS revisions impose ≤ 0.1% by-weight phthalate caps, accelerating the adoption of sixth-generation non-phthalate solutions such as W.R. Grace’s CONSISTA C601 platform. Catalyst vendors are pivoting R&D to balance activity, stereospecificity, and regulatory compliance, while polypropylene producers face line-conversion costs and temporary output inefficiencies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global bans on phthalate donors | -0.9% | Global, led by EU and North America | Medium term (2-4 years) |

| Propylene price volatility | -1.1% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Scarcity of tri-ethyl-aluminium supply | -0.6% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Bans on Phthalate Donors

Expanded chemical-safety frameworks in the EU, China, and select US states are driving expensive compliance upgrades, including on-line spectroscopic monitoring and enhanced traceability protocols for non-intentionally added substances. The transition to phthalate-free catalysts often requires higher co-catalyst loadings and refined reactor conditions, escalating production complexity and capital expenditure for many operators.

Propylene Price Volatility

Propylene benchmarks remain prone to supply shocks from refinery rationalizations and cracker outages. US polymer-grade propylene is expected to rise by 5 ¢/lb into mid-2025 as new polypropylene plants ramp while refinery cuts tighten feedstock pools. Similar gyrations in Asia, aggravated by uneven LPG flows, complicate inventory and pricing strategies for catalyst makers tethered to contractual pricing formulas linked to propylene indices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Catalyst Type: Metallocene Gains Despite Ziegler-Natta Dominance

Ziegler-Natta catalysts held 65.62% of the polypropylene catalyst market share in 2025 because of proven efficiency and broad application compatibility. The polypropylene catalyst market size for metallocene variants is projected to expand at a 7.79% CAGR, reflecting their precision in molecular architecture and compliance with phthalate-free mandates. Innovations such as chromophore quench-labelling indicate meaningful headroom to raise active-site utilization, boosting catalyst output per pound of titanium and shrinking total installed costs. Producers are thus running dual portfolios: cost-efficient Ziegler-Natta grades for mass market volumes, and metallocene lines for premium clarity film, medical, and automotive projects.

In competitive terms, W.R. Grace’s sixth-generation CONSISTA C601 non-phthalate Ziegler-Natta catalyst bridges regulatory compliance and optical performance, challenging metallocene incumbents in high-clarity packaging. The resulting overlap is intensifying price-performance comparisons across customer accounts, prompting fresh licensing deals that bundle catalyst offerings with process automation software.

By Production Process: Gas Phase Leads Amid Hybrid Innovation

Gas-phase technology captured 46.55% of the polypropylene catalyst market share in 2025, owing to low capital intensity, modular debottlenecking, and short start-up timelines. The polypropylene catalyst market size attributed to hybrid bulk-loop/gas lines is forecast to grow at 6.44% CAGR through 2031 as producers install sequential reactors capable of toggling between homopolymer and impact-copolymer grades without major downtime. These twin-reactor schemes maximise catalyst residence-time efficiency and fine-tune block comonomer distribution for property gradation.

Bulk loop-slurry and slurry-phase routes persist in niche domains where melt-index control and narrow molecular-weight dispersions override cost arguments. Process licensors are therefore leveraging data analytics and catalyst-specific digital twins to help operators execute grade swings swiftly, minimising off-spec resin and raising plant utilisation in volatile demand cycles.

By Application: Polypropylene Dominance Reflects Market Maturity

Polypropylene production itself accounted for 63.75% of global catalyst demand in 2025, yet it also logs the swiftest 8.25% CAGR to 2031, underscoring continued substitution into polyolefin blends and new recyclate streams. High-clarity random-copolymer film, thin-wall injection moulding, and thermoform sheets dominate capacity expansions, sustaining a feedback loop of catalyst innovation focused on comonomer distribution, peroxide-free melt-flow tuning, and low-residue ash profiles.

Sustainability imperatives are injecting new life into recycling-compatible catalysts. Purification systems such as Clariant’s HDMax line, deployed to upgrade pyrolysis oils, require propylene catalysts tolerant to trace olefinic impurities while delivering on-spec molecular weight. These specifications push vendors to pioneer highly selective, poison-resistant formulations.

By End-User Industry: Healthcare Emerges as Growth Driver

Packaging maintained a 48.62% share of the polypropylene catalyst market size in 2025, reflecting a reliable pull from food safety regulation and e-commerce. Healthcare, however, lead growth at 7.05% CAGR. Hospitals and device makers demand resin grades meeting USP Class VI and ISO 10993 biocompatibility, translating into catalyst purity thresholds below parts-per-billion on heavy-metal residues. Suppliers are co-engineering metallocene catalysts with melt-blown non-woven producers to ensure sterilisability and kink-resistance in surgical gowns and syringe barrels.

Automotive interiors and under-hood applications continue to evolve toward foamed structures as OEMs shave vehicle mass to offset battery weights. Catalysts enabling high-melt-strength PP are therefore in tight supply, signifying a potential price up-cycle despite overarching commoditisation trends.

Geography Analysis

Asia-Pacific retained 51.64% share of global revenue in 2025 and is growing at 6.83% CAGR, underscoring its status as the axis of new capacity and demand. Government-backed complexes such as the SABIC Fujian project will anchor localized supply chains, while India’s petrochemical roadmap forecasts USD 350–370 billion of consumption by 2040, signifying multiple world-scale facilities across the subcontinent. Excess capacity from Chinese builds, however, is rippling across Japan and other mature markets, prompting strategic shutdowns of ageing crackers.

North America remains a technology hub, buoyed by feedstock optionality from shale gas liquids. LyondellBasell’s propylene oxide complex and associated polypropylene debottlenecks in Texas reinforce regional demand for advanced Ziegler-Natta and metallocene systems fit for food-contact and healthcare applications. Yet refinery rationalisation constricts propylene pools, amplifying spot-price swings that challenge inventory planning.

Europe, though facing elevated energy costs, charts policy leadership in circularity. The EU’s food-contact amendment and national plastic taxes spur adoption of phthalate-free catalysts and high-MFR resins suited to mechanical recycling loops. Borealis’ EUR 100 million outlay to triple Daploy capacity in Germany underlines niche specialisation in value-added grades. Middle East and Africa, leveraging advantaged feedstocks, is scaling specialty polyolefin complexes, while South America advances more modest brownfield debottlenecks to match domestic consumption.

Regulatory Landscape

Regulatory pressure continues to accelerate the shift away from phthalate-based internal donors in polypropylene catalysts, particularly for packaging and healthcare grades. In Europe, REACH (Regulation (EC) 1907/2006) and related restrictions on phthalates such as DBP, DIBP, and DEHP reinforce tighter substance-control expectations, while food-contact compliance is governed by Commission Regulation (EU) No 10/2011 and its ongoing amendments.

In North America, oversight falls under the US EPA framework via TSCA risk-evaluation and reporting procedures, shaping how catalyst components and additives are documented across supply chains. In Asia, food-contact rules such as China GB 4806.7-2023, alongside the January 2026 context for tighter phthalate caps and China RoHS revisions, increases compliance burdens. That, in turn, supports traceability requirements, low-residue catalyst design, and broader adoption of non-phthalate Ziegler-Natta and single-site systems.

Value Chain Analysis

The polypropylene catalyst value chain starts with upstream inorganic and organometallic inputs such as magnesium chloride and titanium tetrachloride for Ziegler-Natta systems, supported by co-catalysts and electron donors. Catalyst producers convert these inputs into supported catalyst formulations, then supply them as merchant products or for captive consumption inside integrated petrochemical complexes, where logistics and handling aim to preserve activity and morphology.

Downstream, process technology licensors and catalyst suppliers increasingly compete through bundled offerings that pair proprietary catalysts with reactor technologies and operating software to improve yield and grade flexibility. This integration shows up in UNIPOL polypropylene deployments that use W.R. Grace CONSISTA catalysts and UNIPPAC software, and in LyondellBasell offerings tied to Spheripol and Spherizone process routes. In India, Grace expanded licensing with Bharat Petroleum Corporation Limited in June 2024 for new 400 KTA and 550 KTA units, and Nayara Energy commissioned a 450 KTA UNIPOL PP plant in Gujarat in October 2024. Together, these capacity additions pull through long-cycle catalyst supply, technical service, and digital process-control support.

Competitive Landscape

The polypropylene catalyst market shows moderate concentration. Incumbents are doubling down on phthalate-free and recycling-ready innovations. Grace and Milliken co-developed additive-catalyst packages that cut cycle times and raise clarity in random-copolymer containers. Clariant’s HDMax catalysts and CLARIT adsorbents enable chemical recycling streams to meet polymerisation purity specs, reflecting a broader pivot toward circular-economy profit pools. Emerging disruptors focus on AI-driven catalyst discovery, yet face high qualification barriers at commercial scale.

Polypropylene Catalyst Industry Leaders

Clariant

LyondellBasell Industries Holdings B.V.

Mitsui Chemicals, Inc.

Sinopec Catalyst CO.,LTD.

W. R. Grace & Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The regulatory-led pivot to non-phthalate catalyst systems creates whitespace in plant conversions and new-build qualification programs, especially where food-contact and healthcare grades are central. The report-context anchors include the EU move toward stricter migration limits and traceability under Regulation (EU) 2025/351, and the China RoHS revisions referenced for January 2026. Those requirements push polypropylene producers toward sixth-generation non-phthalate Ziegler-Natta options and toward higher-performance single-site systems, and commercial pull-through is strongest when technology is packaged as a drop-in upgrade, as in UNIPOL PP process deployments using CONSISTA catalysts and UNIPPAC software.

A second opportunity is catalyst and process control that improves grade precision for thin-wall packaging, high-melt-strength foams, and medical applications where residue limits and tight molecular architecture matter. Alongside that, 2026-focused academic work points to faster scale-up and tighter quality control during catalyst synthesis, including in-line imaging approaches to monitor Ziegler-Natta morphology during preparation and comparisons of internal electron donors and preparation methods that affect catalyst activity and polypropylene properties. These strands support differentiation around reproducibility, active-site utilization, and faster qualification cycles for premium polypropylene grades.

Recent Industry Developments

- May 2026: Clariant reported that its catalysts helped customers avoid 45 million tons of CO2e in 2025. This supports procurement momentum for catalyst platforms that pair yield improvements with lower byproducts and reduced energy intensity, influencing integrated propylene-to-polypropylene economics.

- September 2025: Clariant announced a supply agreement with SYPOX to deliver catalysts for a 10 MW electric steam methane reformer (e-SMR) project targeted to begin operations in 2026. The move strengthens Clariant's presence in electrified, lower-carbon hydrogen and syngas pathways that connect to upstream building blocks used across polyolefins value chains.

- November 2024: The UNIPOL polypropylene plant owned by Nayara Energy Limited in Gujarat, India, was commissioned using non-phthalate CONSISTA catalysts and UNIPOL UNIPPAC software to produce PP grades for pharmaceutical, health, and hygiene applications. The commissioning provides a concrete reference point for non-phthalate catalyst adoption at scale and supports broader plant conversion activity tied to tightening phthalate restrictions. It also signals growing demand for resin-grade process-control offerings that enable fast-track qualification of premium grades.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers catalysts used to polymerize propylene into polypropylene, including commercial Ziegler-Natta and single-site systems used across common industrial reactor routes. The sizing reflects value generated from catalyst demand tied to polypropylene production, using both merchant supply and internal consumption at integrated sites.

Scope exclusions: We exclude catalysts used only for polyethylene, lab or pilot-scale catalyst use, and adjacent polyolefin catalyst uses that are not tied to polypropylene resin output.

Segmentation Overview

- By Catalyst Type

- Ziegler-Natta Catalyst

- Metallocene Catalyst

- By Production Process

- Bulk (Loop-Slurry) Process

- Gas-Phase Process

- Slurry Phase

- By Application

- Polypropylene

- Other Applications

- By End-User Industry

- Packaging

- Automotive

- Electrical and Electronics

- Consumer Goods and Appliances

- Building and Construction

- Healthcare

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping polypropylene production economics and operating patterns because catalyst demand is closely linked to resin output and plant run rates. We rely on public sources such as the US Energy Information Administration (feedstock signals), US International Trade Commission trade statistics, UN Comtrade, World Bank commodity indicators, and Eurostat to understand regional production footprint and the resin trade flows that can affect throughput.

We then cross-check the direction of demand using materials and plastics association publications, peer-reviewed polymer science journals (catalyst technology and adoption), and company filings and investor presentations for production expansions, shutdowns, and technology shifts. Patent databases are also reviewed to track where new catalyst families and process improvements are being commercialized. In addition, we use paid subscriptions for company financials and intelligence, along with news and financials and patent coverage, to fill gaps in ownership structures and capacity timing. The sources listed here are illustrative, and we also used other public references to collect inputs, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to test how catalyst types are chosen in real procurement cycles and how consumption intensity changes by process route and product mix. We spoke with respondents from catalyst suppliers, polypropylene producers, distributors, and technical specialists across APAC, EMEA, and the Americas, so regional operating practices and price conventions could be compared.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 44% |

| Mid tier: 51% | Functional/Unit leaders: 39% | EMEA: 35% |

| Smaller Players: 18% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built with a top-down approach where polypropylene production and trade patterns are used to reconstruct a demand pool for catalysts by region, and then adjusted using process-route exposure. To keep the model practical, we track market fingerprints such as polypropylene operating rates and announced capacity additions, the process mix across gas-phase versus bulk or slurry routes, the adoption pace of single-site catalysts versus Ziegler-Natta, typical catalyst dosage intensity ranges per ton of resin, and regional pricing and currency timing that can shift reported value.

Those totals are corroborated with selective bottom-up approximations, including sampled ASP multiplied by estimated consumption volumes for key producer clusters, plus channel checks on the share of merchant supply versus captive use. Where bottom-up visibility is weaker, we apply conservative intensity bands that were validated through interviews, and then reconcile the outcome with resin output constraints. Forecasting is mainly done through scenario analysis, where capacity ramp-ups, operating rate cycles, and technology substitution are varied, and then aligned to the consensus view provided by industry respondents on the most likely base case.

Data Validation & Update Cycle

Validation is done through cross-checks that tie the final value to independent signals, such as regional polypropylene capacity and utilization, trade direction for resins, and the implied catalyst spend per ton. If the model shows a spike or drop that does not match these signals, we re-review the drivers and trigger a fresh set of expert calls to confirm whether pricing, process mix, or operating rates changed.

Before sign-off, the model goes through multiple analyst reviews, including variance checks across regions and reasonability checks of intensity and ASP assumptions. Reports are refreshed annually, with interim updates when material events occur, such as major plant startups, extended outages, or noticeable technology shifts. Right before delivery, a final sweep is performed so the latest updated view is reflected consistently across regions.

Mordor Intelligence's Polypropylene Catalyst Market Size Compared Against Other Published Estimates

Published market sizes for polypropylene catalysts can look far apart, even when they describe similar demand drivers, because the counting rules are often not the same. The main differences are what is counted as a polypropylene catalyst, how captive consumption is treated, and which year is used for the stated current value when price levels are moving.

Some estimates fold in broader polyolefin catalyst spending or include polyethylene-adjacent catalyst demand, which inflates the value versus a polypropylene-only view. Others rely on aggressive technology substitution assumptions for single-site catalysts, or they apply uniform global pricing without reflecting regional contract structures and currency timing. A clearer spread also appears when captive use inside integrated polypropylene sites is either excluded or double-counted, and when the model is not refreshed around major capacity start-ups and operating rate shifts, which are handled differently here and then reconciled through plant-level throughput checks before being finalized by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.80 B (2026) | |

| Global Consultancy A | USD 3.20 B (2026) | Typically broadens scope to polyolefin catalysts or includes polyethylene-adjacent catalyst demand, and may apply blended global pricing that lifts value in high-volume regions. |

| Industry Association B | USD 2.40 B (2026) | Often reflects merchant sales only, which can understate total demand where catalysts are consumed internally at integrated polypropylene sites, and may lag on capacity ramp timing. |

The table shows that the spread mainly comes from scope and counting choices, not from a single forecasting trick. When the demand pool is tied to polypropylene resin output, and then checked against process mix, intensity ranges, and regional pricing, the resulting number stays traceable to clear inputs and can be repeated with the same steps.

Key Questions Answered in the Report

What is the current Polypropylene Catalyst Market size?

The market stands at USD 2.8 billion in 2026 and is projected to reach USD 3.71 billion by 2031.

Which region leads polypropylene catalyst demand?

Asia-Pacific accounts for 51.64% of global revenue due to extensive capacity additions and rapid downstream consumption.

Which catalyst type is growing fastest?

Metallocene catalysts post the highest 7.79% CAGR, driven by superior property control and regulatory compliance advantages.

How does propylene price volatility influence the market?

Fluctuating propylene costs squeeze producer margins and compel flexible pricing and inventory strategies for catalyst suppliers.

Page last updated on: