Polyphenylene Sulfide (PPS) Resin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

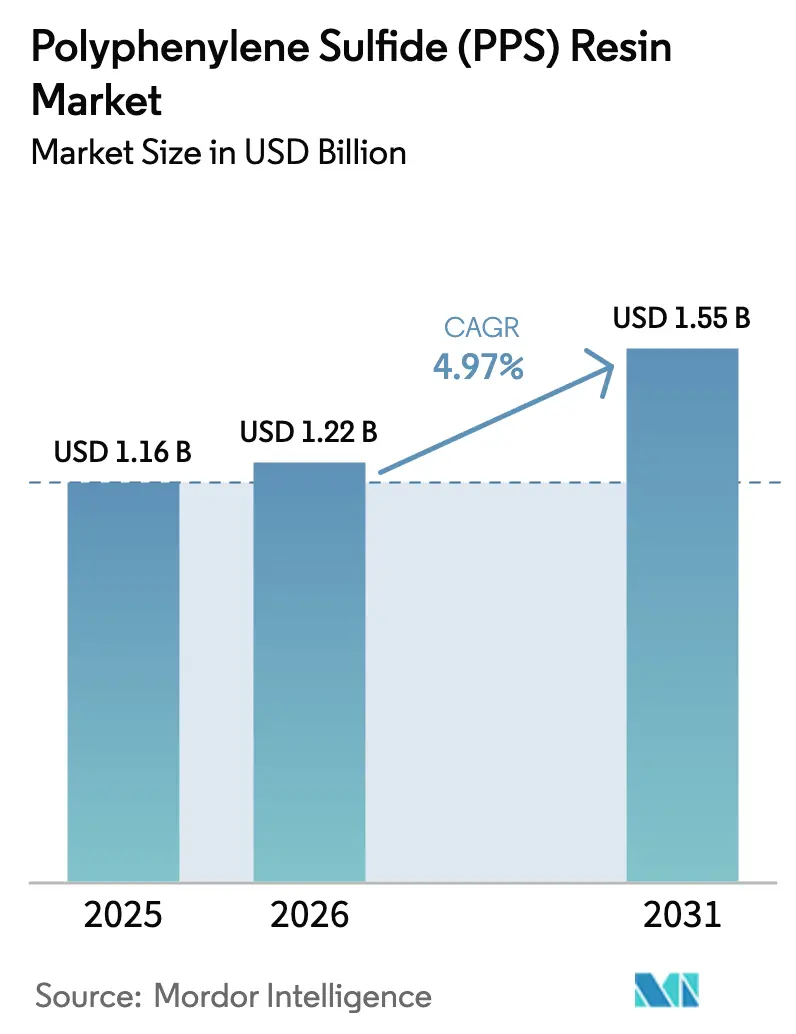

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyphenylene Sulfide (PPS) Resin Market Analysis by Mordor Intelligence

The Polyphenylene Sulfide Resin Market size was valued at USD 1.16 billion in 2025 and is estimated to grow from USD 1.22 billion in 2026 to reach USD 1.55 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). Driven by the miniaturization of electronics, a surge in hydrogen fuel-cell systems, and upgrades in industrial flue-gas filtration that require consistent service above 190°C, the market is witnessing steady momentum. The Asia-Pacific region leads in consumption, while North America is catching up, spurred by battery onshoring incentives. Meanwhile, Europe is pivoting toward halogen-free, flame-retardant resins. Although price increases are being moderated by capacity expansions in China, established suppliers are strategically repositioning themselves, focusing on specialty grades, vertically integrating into compounding, and enhancing digital processes. In essence, the Polyphenylene Sulfide (PPS) resin market is grappling with cost pressures but is distinctly shifting toward high-temperature, regulatory-compliant applications, an area where commodity thermoplastics struggle.

Key Report Takeaways

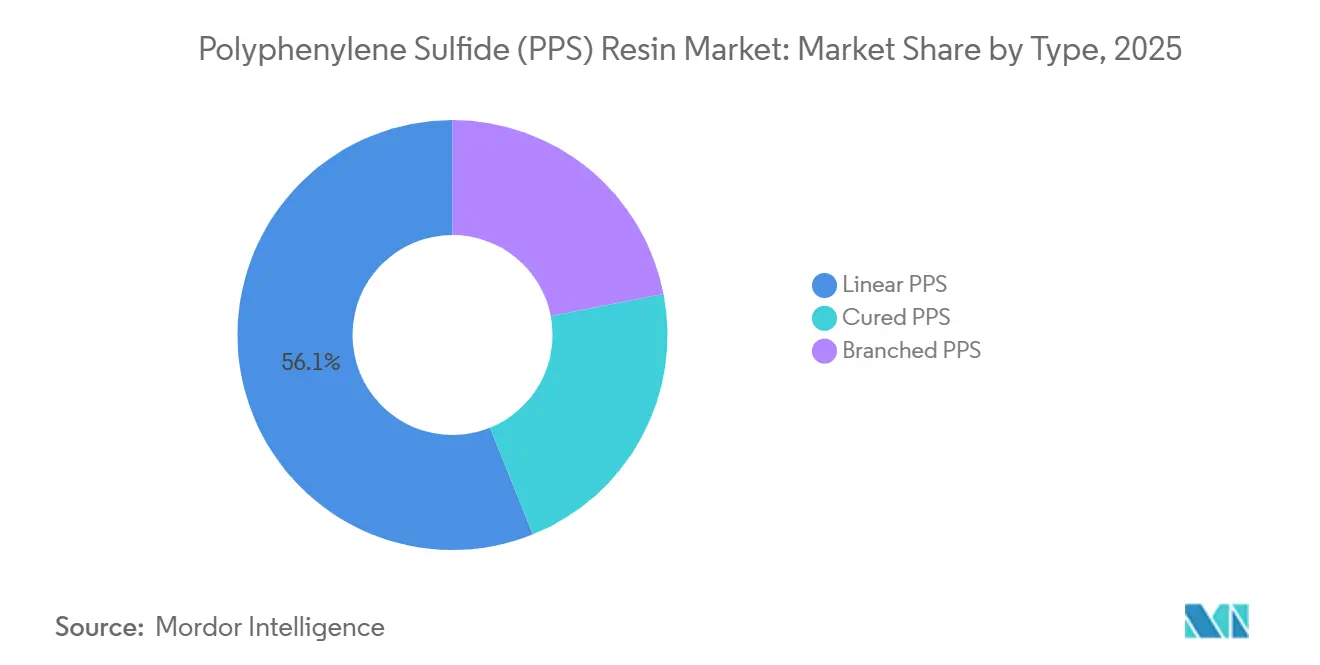

- By type, linear PPS held 56.11% of the polyphenylene sulfide (PPS) resin market share in 2025 and is projected to post a 5.03% CAGR to 2031.

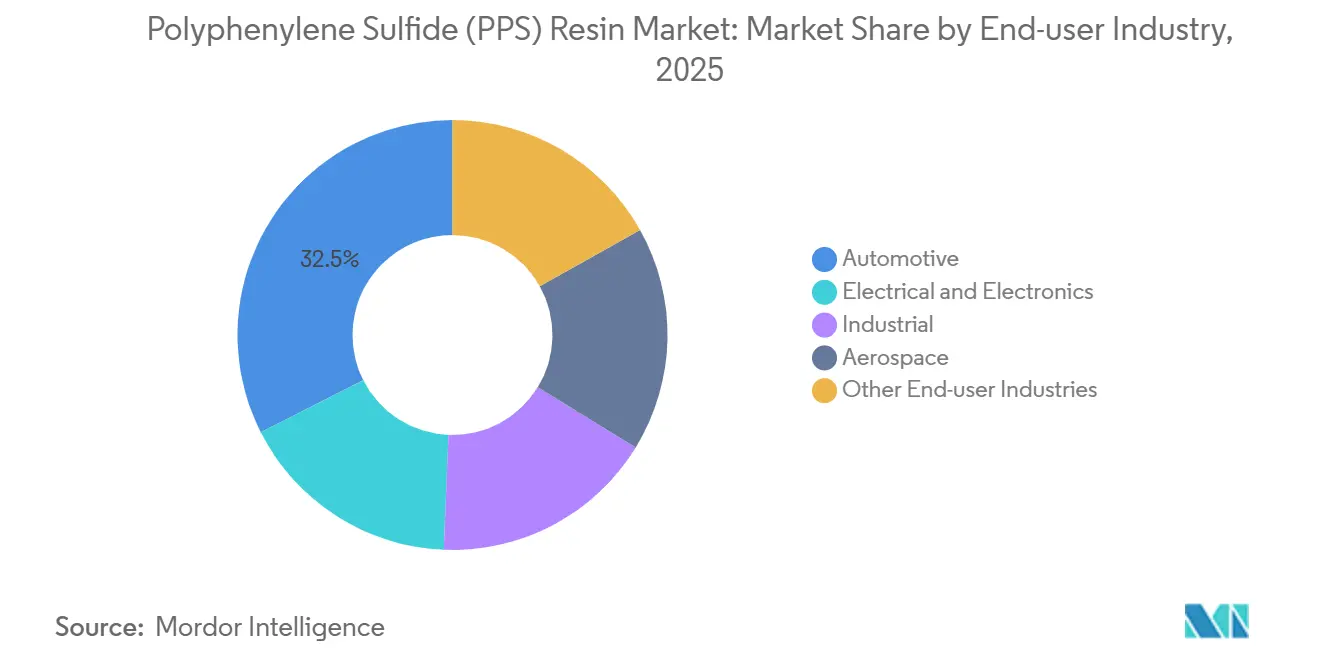

- By end-user industry, automotive held 32.48% revenue share in 2025, while the industrial segment is forecast to expand at a 5.75% CAGR to 2031.

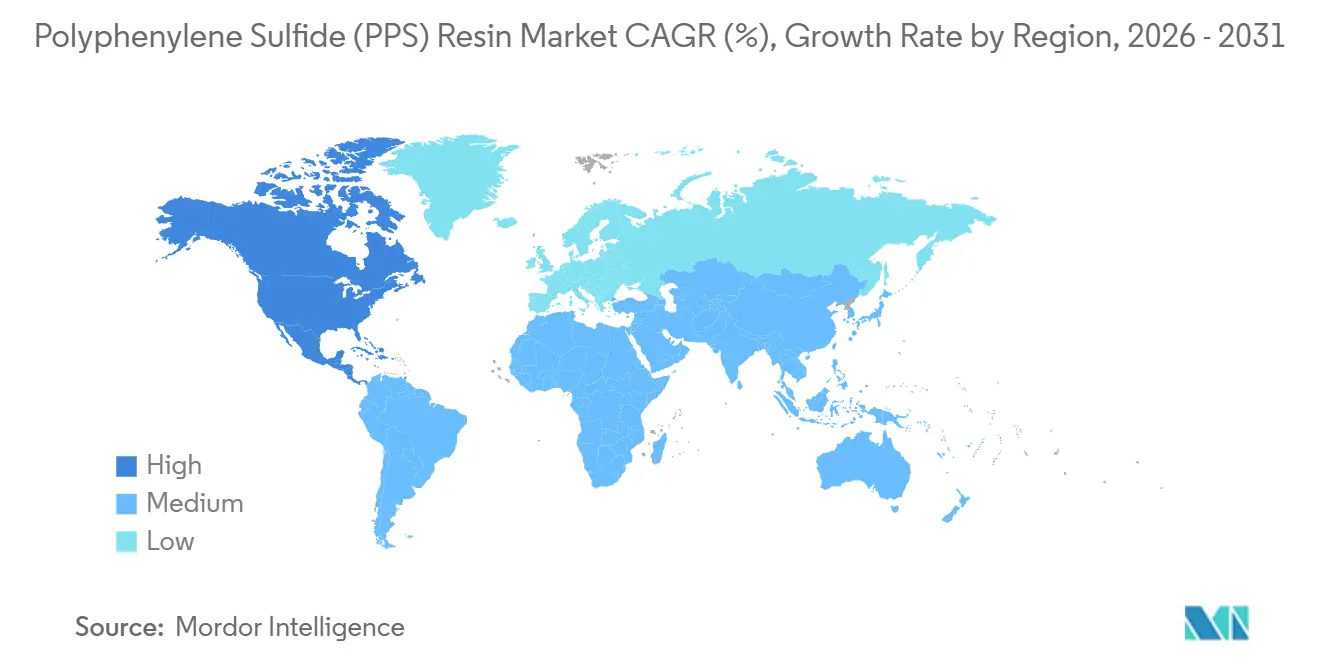

- By geography, Asia-Pacific accounted for 67.26% of the polyphenylene sulfide (PPS) resin market size in 2025, while North America is projected to grow at 5.16% through 2031, outpacing the global average.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyphenylene Sulfide (PPS) Resin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturized 5G/AI electronics need dielectric-stable PPS | +1.20% | Global, concentrated in Asia-Pacific (China, South Korea, Taiwan) and North America | Medium term (2-4 years) |

| Shift to chlorine-free PPS grades after 2025 US/EU toxicity regulations | +0.80% | North America and EU, spillover to export-oriented APAC manufacturers | Short term (≤ 2 years) |

| On-board hydrogen fuel-cell balance-of-plant adoption | +0.90% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| AI-optimized compounding cuts scrap and widens PPS use | +0.60% | Global, early adoption in APAC and North America | Long term (≥ 4 years) |

| Rapid Asia-Pacific filter-bag upgrades for ultra-low-NOx boilers | +1.30% | APAC core (China, India, ASEAN), limited spillover to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Miniaturized 5G and AI Electronics Need Dielectric-Stable PPS

5G millimeter-wave radios and edge AI hardware require substrates that not only exhibit low dielectric loss above 10 GHz but can also withstand lead-free solder reflow at 260°C. Newly commercialized low-dielectric PPS films meet these stringent criteria, boasting minimal moisture uptake and maintaining mechanical integrity even under repeated thermal shocks. Smartphone manufacturers, automotive ECU suppliers, and base-station producers are increasingly adopting these films as cost-effective alternatives to liquid-crystal polymers. In tandem with the expansion of 5G, industry giants Toray, DIC, and Unitika have rolled out new capacities in recent years. This collective momentum is propelling the Polyphenylene Sulfide (PPS) resin market, particularly in high-frequency connectors and antenna housings, which must achieve UL 94 V-0 standards at thinner sections without relying on halogenated additives.

Shift to Chlorine-Free PPS Grades After 2025 US and EU Toxicity Regulations

In 2025, Dechlorane Plus was added to the EU's Persistent Organic Pollutants Regulation, with a near-zero allowable concentration set for 2028. This regulatory shift has spurred electronics OEMs to move away from halogenated flame retardants. Importantly, PPS naturally meets the UL 94 V-0 standard at thin sections, enabling suppliers to avoid costly reformulations. Responding to the surging demand for halogen-free solutions, new compounding plants in Germany and the United States began operations in 2025, drastically cutting lead times for clients in Europe and North America. This rapid regulatory adaptation is expected to resonate with Asia-Pacific exporters, positioning the Polyphenylene Sulfide (PPS) resin market as the preferred choice for compliance across diverse value chains.

On-Board Hydrogen Fuel-Cell Balance-of-Plant Adoption

Fuel-cell trucks, passenger vehicles, and stationary backup systems rely on humidified hydrogen, heated and pressurized. Glass-fiber-reinforced PPS, celebrated for its chemical inertness and dimensional stability, can withstand thousands of cycles. This resilience paves the way for lighter, corrosion-resistant housings in pumps, valves, and humidifiers. Both Polyplastics and Solvay have launched new grades that maintain flexural strength even after prolonged hydrothermal exposure. This technological leap aligns perfectly with infrastructure investments in the United States and Europe, propelling the long-term growth of the Polyphenylene Sulfide (PPS) resin market.

AI-Optimized Compounding Cuts Scrap and Widens PPS Use

Machine-learning models are transforming automatic parameter-setting, significantly tightening the processing window for PPS. Kureha’s Innovation Technology Department, launched in 2024, employs digital twins to anticipate challenges like fiber attrition and warpage, resulting in less scrap and reduced energy consumption. This streamlined molding process paves the way for lower-volume connector programs and medical equipment components, previously considered too expensive, broadening the application range and boosting the economic appeal of the Polyphenylene Sulfide (PPS) resin market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising competition from lower-cost high-temperature nylons | -0.90% | Global, most acute in Europe and North America | Medium term (2-4 years) |

| Recycling end-of-life hurdles for cross-linked PPS | -0.50% | Europe, North America, spillover to APAC export supply chains | Long term (≥ 4 years) |

| Talent gap in high-temperature polymer processing | -0.40% | Global, concentrated in emerging manufacturing hubs (India, ASEAN, MEA) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Competition from Lower-Cost High-Temperature Nylons

Polyphthalamides have secured a Comparative Tracking Index of 600 V and achieved UL 94 V-0 certification at a thickness of 0.4 mm. These materials, processed in molds at temperatures between 90-110°C, are now rivaling PPS in numerous automotive connectors. In 2025, BASF introduced its Ultramid T6000[1]BASF, “Ultramid T6000 Press Release,” basf.com . Although a continuous-use temperature range of 150-160°C is adequate, OEMs are adjusting specifications to reduce bills of material, thereby decreasing their stake in the cost-sensitive Polyphenylene Sulfide (PPS) resin market.

Recycling End-of-Life Hurdles for Cross-Linked PPS

Cross-linked PPS grades, renowned for their creep resistance at temperatures exceeding 200°C, face a significant challenge: their inability to be remelted excludes them from conventional mechanical recycling methods. With EU regulations set to enforce recyclable designs for automotive and electronic plastics by 2030, OEMs are increasingly gravitating toward materials that offer easier reprocessing. In 2026, Toray unveiled a pilot method to recover fiber-reinforced PPS; however, scaling this technique will require several years. Meanwhile, the recyclability constraints of specific high-performance PPS variants raise concerns about their future adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Linear Grades Dominate Cost-Sensitive Applications

In 2025, Linear PPS held a 56.11% share of the Polyphenylene Sulfide (PPS) resin market and is projected to grow at a 5.03% CAGR through the forecast period of 2026-2031. Its lower viscosity and compatibility with standard injection equipment make Linear PPS ideal for thin-wall molding, particularly in automotive high-voltage connectors and pump impellers. Cured PPS, which undergoes post-polymerization cross-linking, maintains tight dimensional tolerances above 200°C and is used in niche applications such as aerospace ducts and industrial pump parts. Branched PPS offers a higher modulus while ensuring recyclability, making it suitable for structural components in electric vehicle (EV) batteries. In 2024, DIC launched a plateable PPS compound for 5G antenna housings, enabling direct metallization and eliminating the need for metal inserts, thereby reducing weight[2]DIC Corporation, “Plateable PPS Compound Launch,” dic-global.com . This broadened application spectrum boosts the volume of linear and branched grades, while specialty cured variants command premium prices.

By End-User Industry: Industrial Segment Leads Growth Trajectory

Industrial filtration, chemical processing, and power generation are the fastest-growing sectors, with a projected CAGR of 5.75% during 2026-2031. In the Asia-Pacific region, mandated ultra-low-NOx retrofits have driven consistent demand for PPS filter bags, which can operate for up to five years. While the automotive sector accounted for 32.48% of the PPS resin market in 2025, there has been a shift from traditional combustion engine components to electric vehicle (EV) battery busbars and fuel-cell balance-of-plant systems. Polyplastics' DURAFIDE 6150T73 grade, which withstands 1,000 thermal cycles between -40°C and 150°C, meets warranty standards for battery runaway mitigation. The electrical and electronic sectors value its flame-retardant properties and low moisture absorption, while the aerospace industry targets its high-margin niche, particularly for low-smoke, low-toxicity cabin interiors.

Geography Analysis

In 2025, the Asia-Pacific region dominated the Polyphenylene Sulfide (PPS) resin market, accounting for 67.26% of its size. This leadership position was strengthened by the burgeoning production of new-energy vehicles and a thriving electronics supply chain in nations such as China, Japan, South Korea, and Taiwan. China's production capacity saw a boost in 2024, with forecasts suggesting it could more than double by 2027, thanks to the momentum from several large-scale projects. In response to these market shifts, established suppliers are now focusing on differentiated grades and enhanced technical services to counter heightened price competition.

North America is on a growth trajectory, boasting the fastest rate at a CAGR of 5.16% through the forecast period of 2026-2031, driven by robust domestic investments in batteries and hydrogen. This growth is further supported by local consumption of PPS at Fortron Industries’ Wilmington plant.

On the other hand, Europe faces challenges with its stringent halogen and recycled-content regulations. While these rules open doors for substitutions, they also inflate compliance costs, making it tough for smaller converters. Meanwhile, South America, the Middle-East, and Africa are emerging as fledgling markets, with their limited demand for PPS being spurred by industrial filtration and oil-and-gas applications.

Competitive Landscape

The Polyphenylene Sulfide (PPS) resin market is moderately concentrated. Key players like Toray, Solvay, DIC, Celanese, and Kureha command a notable share of the global capacity. Japanese producers boast a competitive edge in processing expertise, yet their Chinese rivals are swiftly ramping up operations, tightening spot margins. Strategic maneuvers are apparent: Toray's debottlenecking in Gunsan and Solvay's upgrade in Changshu hint at a pivot toward value-added compounding and localized support. Envalior's newly launched compounding line in Europe, set to meet the automotive and electronics sectors' halogen-free demands, also emphasizes logistical optimization. The industry's innovation horizon is expanding, spotlighting recycling technologies, plateable compounds, and grades designed for higher hydrogen service temperatures. This evolution signals a shift from mere volume production to a more nuanced, application-driven strategy, vital for staying competitive in the PPS resin arena.

Polyphenylene Sulfide (PPS) Resin Industry Leaders

DIC Corporation

Solvay

Celanese Corporation

TORAY INDUSTRIES, INC.

KUREHA CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Toray Industries, Inc. has introduced an innovative flexible polyphenylene sulfide (PPS) resin that combines exceptional flame retardancy with superior heat resistance. The company asserts that this is the first PPS resin globally to offer these dual properties.

- November 2025: Toray Advanced Materials Korea, a subsidiary of Toray Industries, Inc., has announced the completion of the expansion of its second polyphenylene sulfide (PPS) production line at the Gunsan plant, situated in the Saemangeum Industrial Complex, Jeollabuk-do, Korea. The expanded line now offers an annual production capacity of 5,000 tons.

Global Polyphenylene Sulfide (PPS) Resin Market Report Scope

Polyphenylene Sulfide (PPS) resin is a crystalline heat-resistant polymer that has a simple chemical structure made from benzene and sulfur. PPS is a type of thermoplastic polymer with high thermal and mechanical performance that has wide applications in various industries, such as automobiles, precise electronics, electrical devices, chemical containers, aerospace components, and others.

The Polyphenylene Sulfide (PPS) Resin Market is segmented by type, end-user industry, and geography. By type, the market is segmented into linear PPS, cured PPS, and branched PPS. By end-user industry, the market is segmented into automotive, electrical and electronics, industrial, aerospace, and other end-user industries. The report also covers the market size and forecasts for polyphenylene sulfide (PPS) resin in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Linear PPS |

| Cured PPS |

| Branched PPS |

| Automotive |

| Electrical and Electronics |

| Industrial |

| Aerospace |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Linear PPS | |

| Cured PPS | ||

| Branched PPS | ||

| By End-user Industry | Automotive | |

| Electrical and Electronics | ||

| Industrial | ||

| Aerospace | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the Polyphenylene Sulfide (PPS) resin market in 2031?

The polyphenylene sulfide (PPS) resin market size stands at USD 1.22 billion in 2026, and it is projected to reach USD 1.55 billion by 2031 at a 4.97% CAGR.

Which segment is growing fastest within PPS applications?

Industrial filtration and process equipment is projected to expand at 5.75% CAGR due to stricter emission rules in Asia-Pacific.

Why are low-dielectric PPS grades important for 5G hardware?

They combine minimal signal loss above 10 GHz with solder-reflow stability at 260°C, improving performance in high-frequency connectors.

How large is the PPS presence in automotive components?

Automotive accounted for 32.48% of 2025 demand and is shifting toward EV battery busbars and fuel-cell balance-of-plant parts.

Which regions represent the strongest growth opportunities?

North America shows the highest regional CAGR at 5.16% through 2031, supported by battery and hydrogen investments.

Page last updated on: