Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

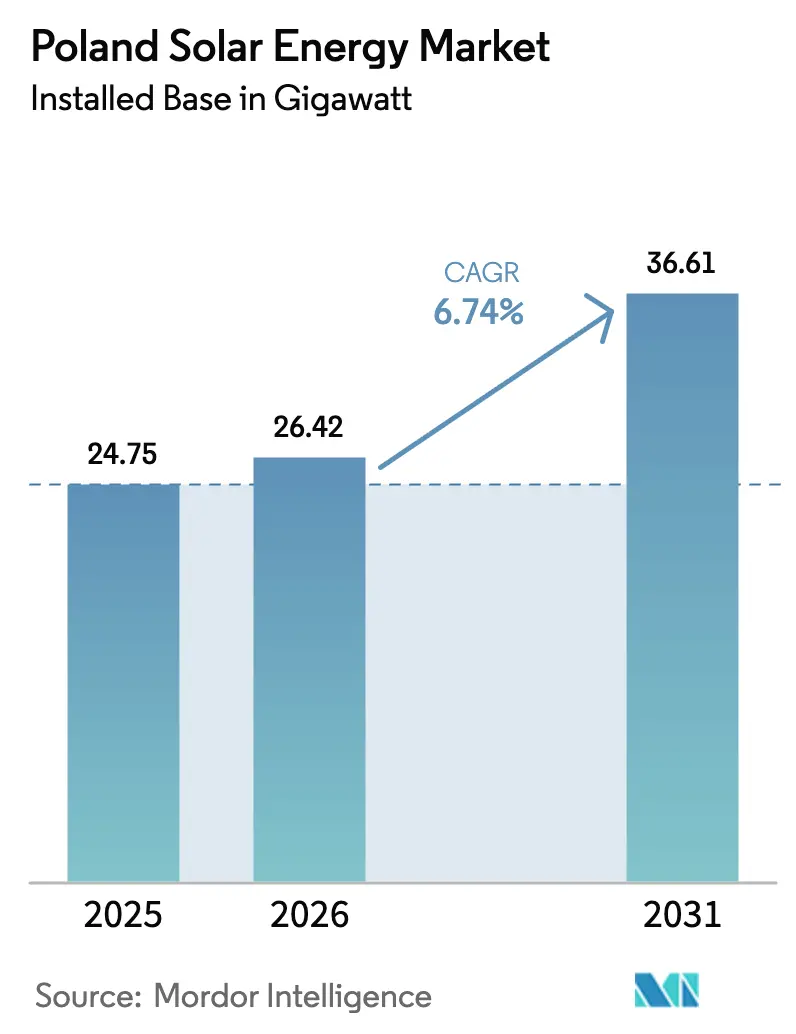

| Base Year Market Size (2025) | 24.75 gigawatt |

| Market Volume (2026) | 26.42 gigawatt |

| Market Volume (2031) | 36.61 gigawatt |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

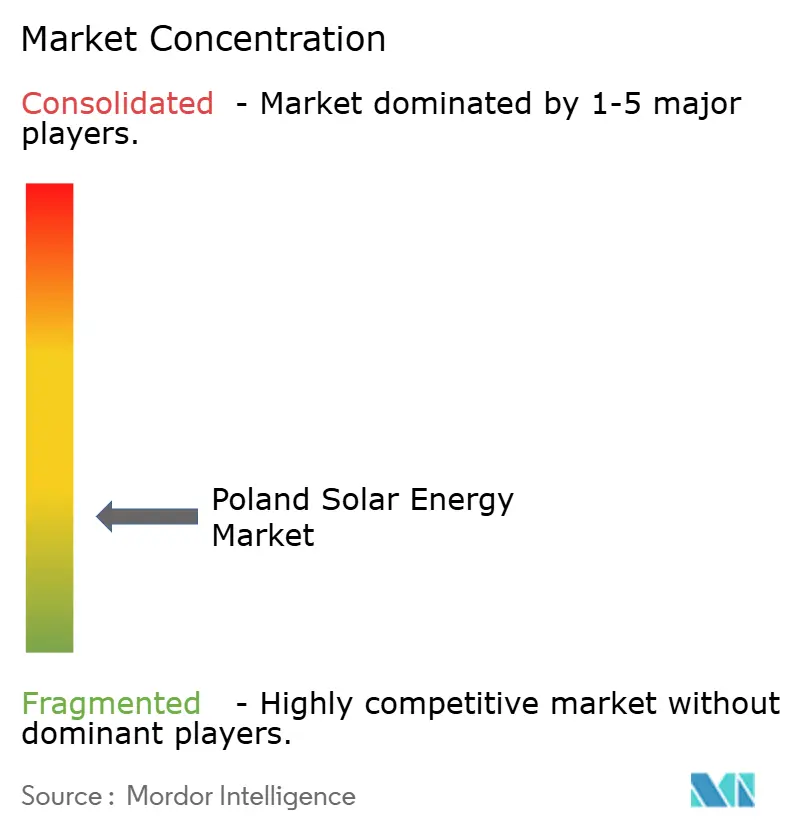

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Solar Energy Market Analysis by Mordor Intelligence

The Poland Solar Energy Market size is expected to grow from 24.75 gigawatt in 2025 to 26.42 gigawatt in 2026 and is forecast to reach 36.61 gigawatt by 2031 at 6.74% CAGR over 2026-2031.

This measured trajectory reflects the nation’s strategic transition away from coal, balanced by grid-upgrade timelines and evolving connection rules. Momentum remains firm as renewables supplied 29% of Poland’s power mix in 2024, with photovoltaic additions of 4 GW underscoring investor confidence. Utility auctions, corporate power-purchase agreements (PPAs), and rooftop incentives continue to attract capital, while domestic manufacturing of bifacial modules improves supply security and cost control. Grid-connection reforms, although slowing speculative applications, are expected to enhance build-out quality and system stability.

Key Report Takeaways

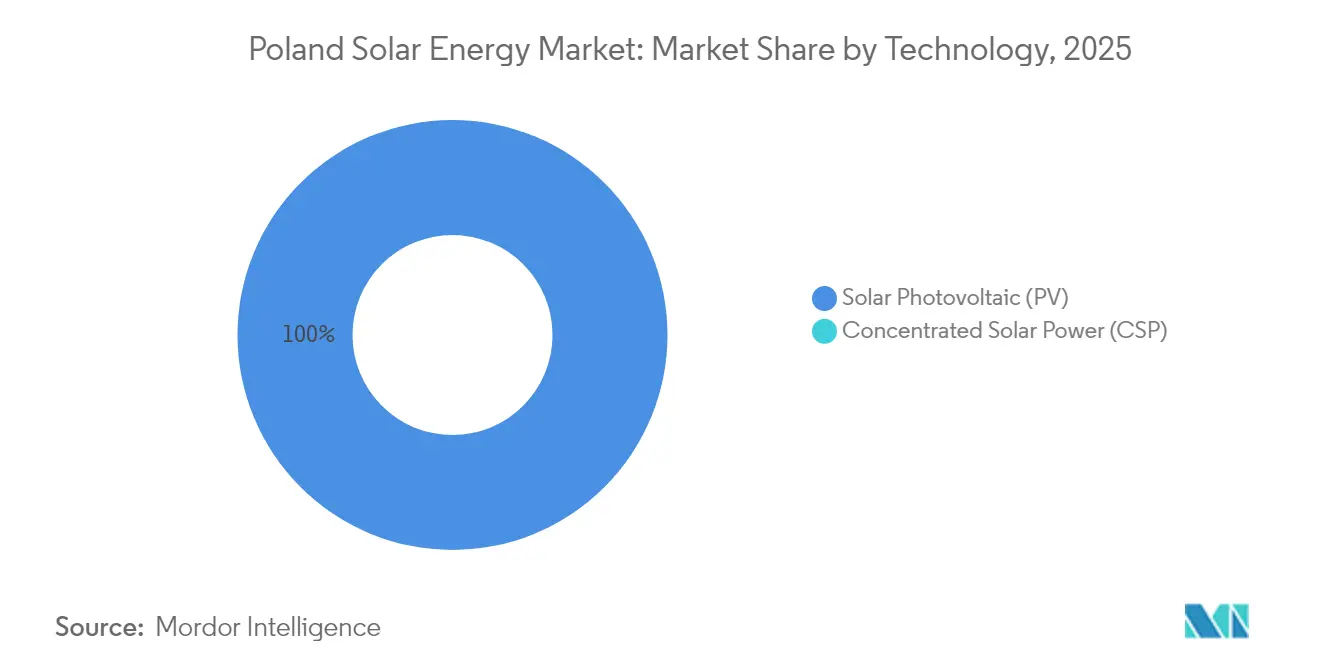

- By technology, photovoltaic systems held 100.00% of the installed capacity in 2025, and the segment is expected to post a 6.78% CAGR through 2031.

- By grid type, on-grid plants captured 93.65% of the Poland solar energy market share in 2025, while off-grid systems are projected to lag at a 3.98% CAGR.

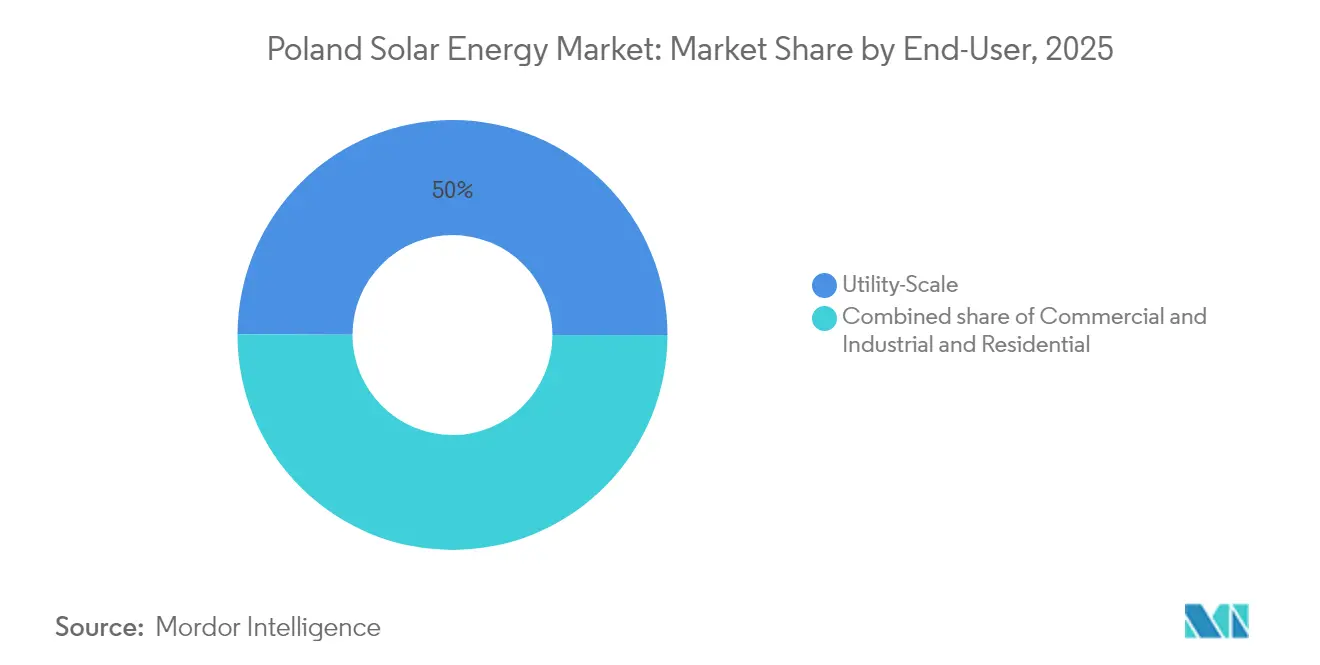

- By end-user, utility-scale farms accounted for 49.95% of the market in 2025; commercial and industrial installations are forecast to expand at a 13.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU renewable-energy targets & NECP mandates | +1.8% | National, with accelerated deployment in Mazowieckie, Wielkopolskie, and Małopolska voivodeships | Long term (≥ 4 years) |

| Declining LCOE of solar PV | +1.5% | National, with strongest impact in southern high-irradiance zones | Medium term (2-4 years) |

| Government auctions & rooftop incentives | +1.2% | National, with prosumer programs concentrated in Tauron and PGE distribution areas | Short term (≤ 2 years) |

| Coal-mine land fast-track grid access | +0.9% | Regional, focused on Silesia, Lower Silesia, and Greater Poland coal basins | Medium term (2-4 years) |

| Corporate PPAs from energy-intensive firms | +0.7% | National, with early adoption in manufacturing corridors and data center hubs | Short term (≤ 2 years) |

| Domestic bifacial module manufacturing | +0.4% | National, contingent on EUR 1.2B manufacturing scheme execution | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Renewable-Energy Targets & NECP Mandates

Binding European Union legislation compels Poland to lift renewables to 50% of national electricity output by 2030, anchoring long-range demand for photovoltaic capacity. The Renewable Energy Directive obliges annual gains across power, heat, and transport, while the updated National Energy and Climate Plan sets interim milestones that utilities must hit or risk funding cuts. An EU financing package of EUR 3.8 billion blends grants with private capital, easing the cost of grid upgrades, storage, and brownfield conversions. Legal clarity around sectoral quotas, therefore, keeps the Poland solar energy market on a steady growth path despite macro headwinds. Compliance monitoring by the European Commission provides additional certainty for lenders and developers.[1]European Commission, “Renewable Energy Directive and National Energy & Climate Plans,” ec.europa.eu

Declining LCOE of Solar PV

The levelized cost of electricity for utility-scale PV in Poland is expected to slide from USD 35/MWh in 2025 to USD 25/MWh by 2035, according to research that places crystalline-silicon modules firmly below the running cost of coal. Fraunhofer ISE reports that ground-mounted plants already reach 4.1 – 9.2 cents /kWh, a range that allows subsidy-free offtake agreements to flourish.[2]Fraunhofer ISE, “Photovoltaics Report 2025,” ise.fraunhofer.de Falling module prices, rising efficiencies, and expanding domestic supply lines underpin this trend. Corporates are seizing the economics: BayWa r.e. has secured multidecade PPAs for Polish solar parks without recourse to auction tariffs, signalling a sustainable merchant market.[3]BayWa r.e., “BayWa r.e. Sells First Polish Subsidy-Free Solar Project,” baywa-re.com

Government Auctions & Rooftop Incentives

Since 2016, competitive auctions have contracted more than 1.6 GW of PV, offering long-term index-linked revenue and crowding in bank finance. In parallel, the relaunched Mój Prąd scheme allocates PLN 400 million for residential panels and batteries, targeting owners of Poland’s 1.54 million micro-installations.[4]Energy Regulatory Office, “Micro-installation Statistics 2024,” ure.gov.pl The blend of commercial-scale auctions and consumer rebates diversifies the Poland solar energy market’s demand base and cushions it against policy swings.

Corporate PPAs from Energy-Intensive Firms

Steelmakers, chemical processors, telecom operators, and data center owners are using 10- to 15-year PPAs to hedge against price volatility and meet Scope 2 decarbonization goals under the Corporate Sustainability Reporting Directive. Notably, R.Power and Play agreed on a 240 GWh annual offtake in late 2024, while Statkraft and Better Energy expanded an arrangement covering 150 GWh per year across four solar farms. These transactions lower developers’ weighted average cost of capital by 100–150 basis points, opening a financing pathway that is independent of feed-in tariffs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion in high-irradiance zones | −1.1% | Southern Małopolska, Silesia, Podkarpackie | Medium term (2-4 years) |

| Volatile local-zoning permitting timelines | −0.6% | Municipalities lacking spatial development plans | Short term (≤ 2 years) |

| Net-metering compensation reduction | −0.5% | Nationwide, pronounced in Tauron and PGE networks | Short term (≤ 2 years) |

| Rising land-lease costs near coal sites | −0.3% | Silesia and Lower Silesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion in High-Irradiance Zones

Rapid connection of projects in the country’s sunniest belts is straining 110 kV and 220 kV lines, forcing the system operator to curb production during midday peaks. Curtailment lowers asset revenues and can deter investment until USD 16 billion of planned 400 kV upgrades are delivered by 2034. Storage roll-outs and demand-response schemes partially mitigate the short-term bottleneck, yet developers still queue for capacity allocations that align with transformer and circuit-breaker upgrades.

Volatile Local-Zoning Permitting Timelines

Municipalities wield discretion over land-use studies and environmental clearances, resulting in unpredictable lead times that complicate project finance. Draft Energy Law amendments add higher upfront fees meant to weed out speculative grid requests, but they also raise capital at risk for genuine sponsors. Standardized zoning templates and digital portals are under discussion yet remain unevenly adopted, making local government engagement a critical competency for players in the Polish solar energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Photovoltaic Dominance Reflects Northern-Latitude Economics

Photovoltaic systems captured 100.00% of installed generation in 2025, and the segment is projected to rise at a 6.78% CAGR, reinforcing its monopoly within the Polish solar energy market. Bifacial modules are gaining popularity rapidly as developers aim to achieve up to 15% additional yield from rear-side reflection, as demonstrated by Enefit Green’s 74 MW Sopi farm, slated for commissioning in 2025. Concentrated solar power remains absent because Poland’s moderate irradiance profile translates into lower direct-normal-irradiance values insufficient to justify CSP’s higher capital outlay. The Poland solar energy market size linked to utility-scale PV is forecast to expand from 12.36 GW in 2025 to 17.95 GW by 2031, underscoring the country’s PV-centric trajectory.

Domestic manufacturing incentives are accelerating vertical integration: a EUR 1.2 billion package is backing the development of new bifacial lines that could supply up to 10 GW annually by 2028. Inverter vendors are testing 29 models for compliance with reactive-power and ride-through requirements, and variants that fail certification face market exclusion. Fixed-tilt racking still dominates because Poland’s modest solar angles temper the benefit of single-axis trackers. The integration of 2.3 GWh of new battery capacity, announced by R.Power and others, signals that hybrid architectures will be pivotal for tapping capacity market premiums. As storage scales, the Poland solar energy market share commanded by standalone PV will decrease, but total PV output will grow, reinforcing its lead in national generation.

By Grid Type: On-Grid Capacity Captures Payment Premiums

On-grid plants held 93.65% of installed capacity in 2025 and are expected to post an 8.32% CAGR to 2031, reflecting investors’ preference for capacity-market contracts and wholesale-market access. Off-grid assets hold a modest 6.35% share and are expected to grow at only 3.98% annually, as rural electrification is already near saturation.

Under State-aid ruling SA.46100, grid-tied PV and storage assets can lock in 15-year capacity payments that underpin debt service even when wholesale prices sag. Photon Energy’s 139 MW of awarded contracts for 2026 delivery demonstrate how hybrid systems capitalize on dispatchability premiums. Conversely, off-grid uptake stays confined to farms and emergency sites where grid extension costs exceed EUR 50,000 per kilometer. Unless Poland introduces peer-to-peer tariffs or wider energy community schemes, the Polish solar energy industry will continue to focus on utility-scale, grid-connected projects.

By End-User: Commercial & Industrial Offtakers Drive Growth

Utility-scale projects accounted for 49.95% of installed capacity in 2025, driven by economies of scale and auction-driven strike prices. Yet commercial and industrial facilities are forecast to accelerate at a 13.92% CAGR through 2031, shifting the Poland solar energy market structure toward private offtake.

R.Power’s 240 GWh annual PPA with Play and Statkraft’s 150 GWh arrangement with Better Energy typify the appetite for fixed-price electricity among data center and manufacturing operators seeking to cap costs and meet ESG metrics. Residential prosumers totaled 12.7 GW by the end of 2024, but new installations dropped 30% after net-metering terms were tightened. Fast-track permitting on reclaimed coal sites is directing utility developers toward Silesia and Lower Silesia, where grid hookups are more affordable, while rooftop PV paired with storage is carving out a niche for resilience in logistics hubs. Collectively, these shifts ensure that the Poland solar energy market size attached to C&I users will widen faster than any other customer class over the outlook period.

Geography Analysis

Installations cluster in Mazovia, Greater Poland, and Silesia, where irradiation, demand centres, and legacy high-voltage lines intersect. Southern and central provinces together host more than half of the operational capacity, though they also experience the sharpest curtailments during spring and summer peaks. The Poland solar energy market size in these heartlands benefits from brownfield coal-site conversions that supply shovel-ready acreage with robust export lines.

Northern coastal regions, historically focused on offshore wind, are now luring hybrid solar projects that share grid upgrades tied to marine farms. Cross-border links with Germany and the Czech Republic enable surplus PV output to flow westward when prices warrant, reinforcing merchant-price signals for new builds. East-central voivodeships are seeing a rooftop boom as agricultural processors and light-industry clusters hedge retail-power inflation with self-generation.

Warsaw’s metropolitan area exemplifies distributed growth, pairing smart-billing schemes with high consumption density. Regional disparities in planning approvals persist, yet the national grid-investment roadmap prioritizes transformers and looped circuits in zones where auction pipelines are thickest. Over the forecast window, balanced geographic build-out is expected to temper locational price volatility and curtailment risk.

Competitive Landscape

The Poland solar energy market hosts a balanced mix of state utilities, European majors, and home-grown specialists. PGE, Energa, and TAURON leverage customer books and capital budgets to integrate PV with planned 900 MWh storage tenders, while RWE, Engie, and SSE Renewables bring cross-border project-finance know-how. Mid-sized developers such as Columbus Energy, R.Power, and ML System carve niches in turnkey rooftop portfolios, bifacial module supply, and perovskite research.

Strategic pivots toward battery storage are escalating: PGE’s USD 4.7 billion commitment ranks among Central Europe’s largest and is expected to unlock flexible capacity that raises solar hosting limits. Acquisition activity also intensifies; ORLEN’s purchase of a 280 MW portfolio and European Energy’s debt-financed farms illustrate consolidation’s role in scaling pipelines and securing grid slots ahead of permitting reforms.

Technology partnerships deliver competitive edges. Developers tie up with inverter makers for grid-forming capabilities, while insurers and recyclers line up extended-warranty products that ease bankability concerns. No single participant exceeds 10% of installed capacity, keeping the arena moderately fragmented and innovative.

Poland Solar Energy Industry Leaders

R. Power Sp. Z O.o.

PGE Polska Grupa Energetyczna SA

Columbus Energy SA

BayWa r.e. AG

Energa SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: PGE unveiled a USD 4.7 billion battery-storage program aimed at firming renewable output and supporting 45 GW of expected PV by 2034.

- October 2024: RWE energized its first Polish solar park, marking the German utility’s formal entry into the market.

- September 2024: Relaunch of the Mój Prąd rebate scheme injected PLN 400 million into residential PV-plus-storage incentives.

- June 2024: Equinor began test production at its inaugural Polish solar facility, underscoring diversification beyond hydrocarbons.

Poland Solar Energy Market Report Scope

Solar energy is a type of renewable energy that utilizes solar panels to generate electricity. Solar panels deployed on rooftops or mounted on the grounds are utilized effectively by energy consumers. In Poland, solar energy is the fastest-growing source of all renewable energy, and it is expected to outperform all rival sectors in the Polish energy industry.

The Polish solar energy market is segmented by technology, grid type, and end user. By technology, the market is segmented into Solar Photovoltaic (PV) and Concentrated Solar Power (CSP). By grid type, the market is segmented into on-grid and off-grid. By end user, the market is segmented into residential, commercial and industrial, and utility. The market sizing and forecasts for each segment have been considered based on the installed capacity (MW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How fast is installed solar capacity expected to grow in Poland between 2026 and 2031?

Aggregate capacity is forecast to climb from 26.42 GW in 2026 to 36.61 GW in 2031, translating into a 6.74% CAGR in the Poland Solar Energy Market.

Which customer segment is expanding the quickest?

Commercial and industrial installations are projected to advance at a 13.92% CAGR through 2031 in the Poland Solar Energy Market, outpacing utility-scale and residential additions.

What share do on-grid systems currently hold?

On-grid plants accounted for 93.65% of installations in 2025 in the Poland Solar Energy Market and will remain dominant because they qualify for capacity-market revenues.

How is Poland addressing grid congestion in solar-dense regions?

The transmission operator is rolling out multiple 400 kV upgrades scheduled for completion by 2026 and encouraging co-located storage to shift output to evening peaks.

What role will domestic manufacturing play by 2031?

A EUR 1.2 billion incentive aims to localize bifacial-module lines, targeting up to 40% of annual panel demand in line with the Net-Zero Industry Act.

Why are corporate PPAs important for Polish solar developers?

Long-term PPAs with creditworthy offtakers lower financing risk, cutting the weighted average cost of capital by up to 150 basis points and enabling projects to proceed without feed-in tariffs.

Page last updated on: