Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

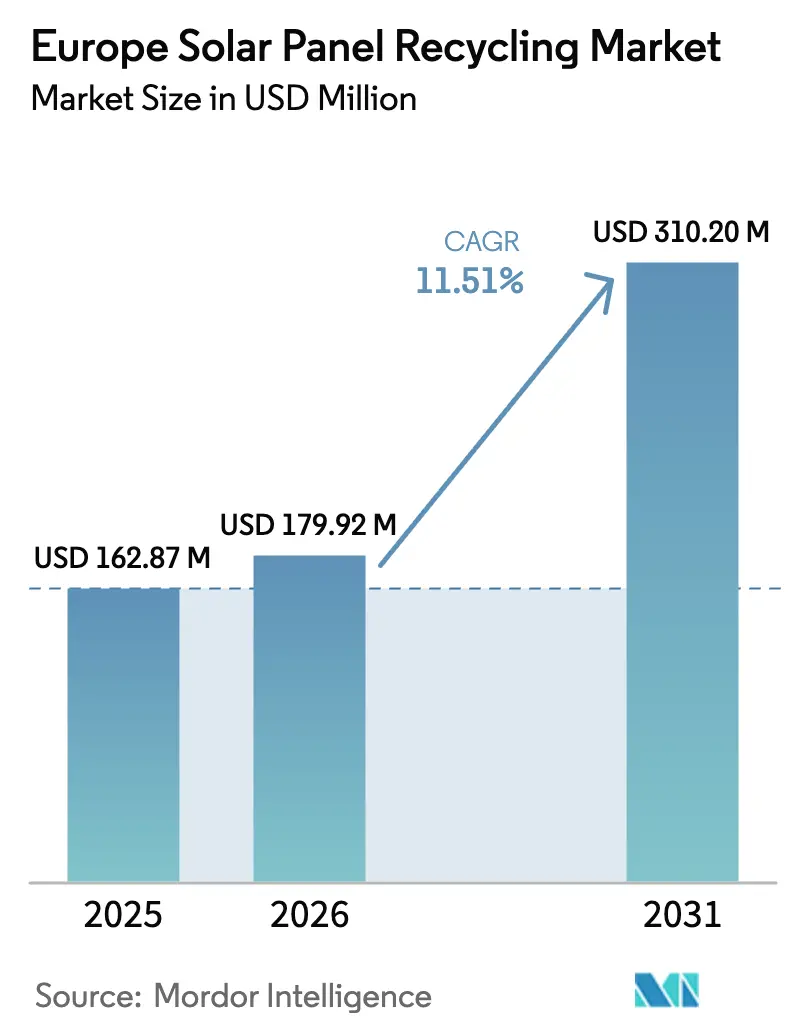

| Base Year Market Size (2025) | USD 162.87 Million |

| Market Size (2026) | USD 179.92 Million |

| Market Size (2031) | USD 310.20 Million |

| Growth Rate (2026 - 2031) | 11.51% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Solar Panel Recycling Market Analysis by Mordor Intelligence

The Europe Solar Panel Recycling Market size is expected to grow from USD 162.87 million in 2025 to USD 179.92 million in 2026 and is forecast to reach USD 310.20 million by 2031 at 11.51% CAGR over 2026-2031.

The momentum results from a convergence of strict waste-electrical rules, geopolitical pressure to secure critical raw materials, and proven technologies that now extract glass, silver, and silicon at an industrial scale. Mandatory producer financing under WEEE and expanding Extended Producer Responsibility (EPR) schemes guarantee an expanding feedstock pipeline, while the EU Critical Raw Materials Act unlocks Innovation Fund grants that de-risk capital expenditures. Cross-sector pull from automotive battery makers keeps a floor under recycled silicon prices, counterbalancing historic revenue swings linked only to silver markets. At the same time, process innovation is trimming operating costs: laser delamination lifts recovery yields, and regional pre-processing hubs compress logistics outlays. Collectively, these shifts are pushing the European solar panel recycling market toward a self-sustaining circular model anchored in resource security rather than landfill avoidance.[1]European Commission, “Proposal for a Regulation on Critical Raw Materials,” europa.eu

Key Report Takeaways

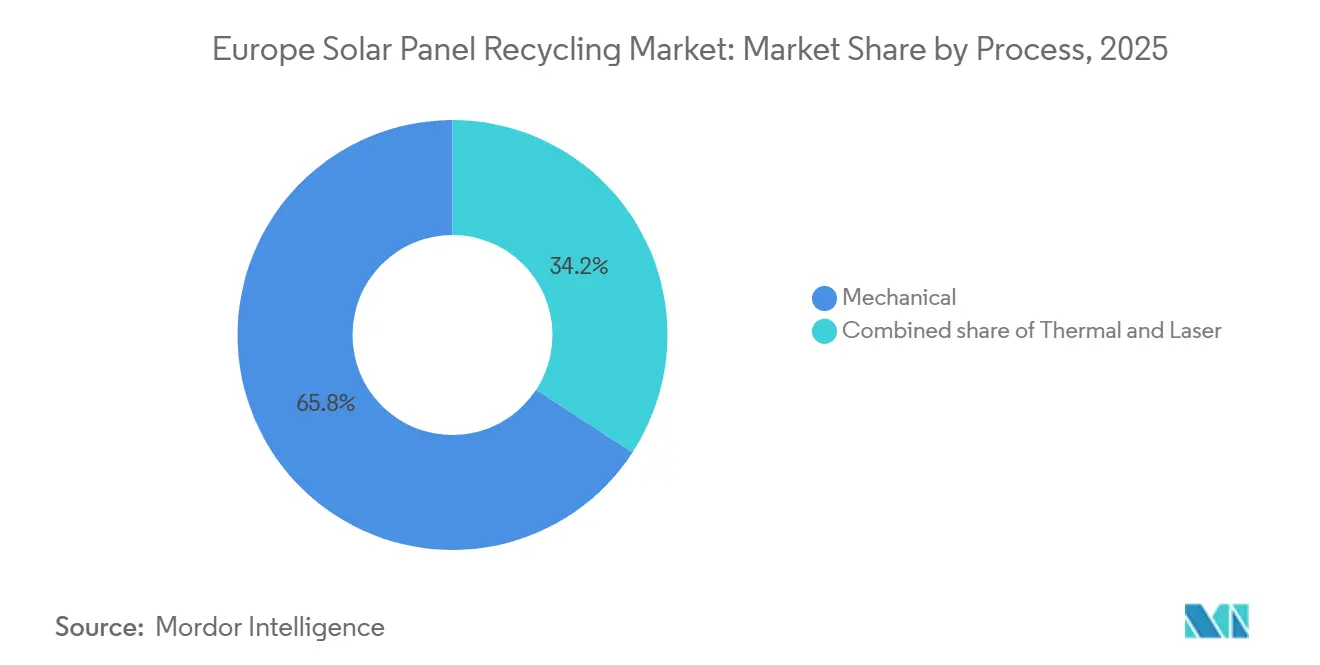

- By process, mechanical methods led with 65.8% revenue share in 2025; laser-based delamination is forecast to post the highest 16.9% CAGR to 2031.

- By panel type, crystalline silicon captured 81.6% of the European solar panel recycling market share in 2025, whereas thin-film CIGS panels are projected to expand at a 19.1% CAGR through 2031.

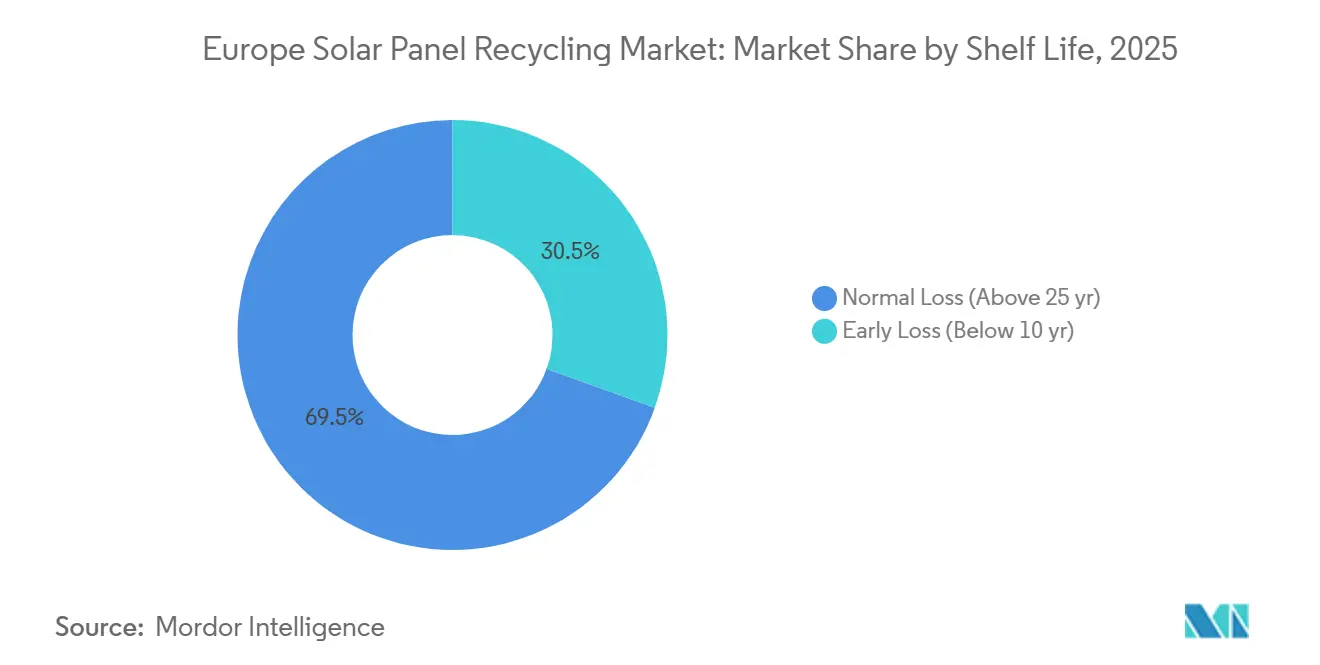

- By shelf life, normal-loss modules older than 25 years represented 69.5% of inbound waste in 2025; early-loss units under 10 years will advance at a 16.2% CAGR to 2031.

- By material recovered, glass held a 48.2% share of the European solar panel recycling market size in 2025, yet silver recovery is expected to rise at a 15.3% CAGR over the outlook period.

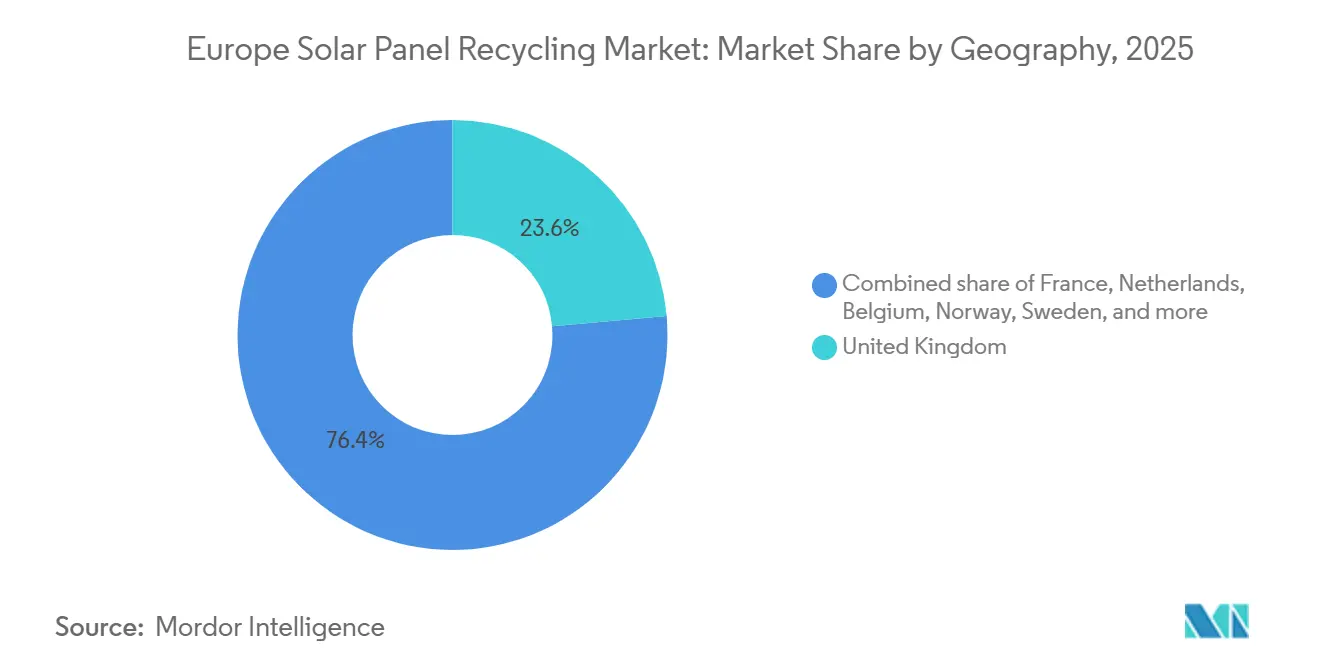

- By geography, the United Kingdom accounted for 23.7% of revenue in 2025 and is projected to maintain the fastest 13.7% CAGR between 2026-2031.

- Veolia, Reiling, ROSI Solar, PV Cycle, and First Solar collectively controlled roughly 35-40% of 2025 revenues, reflecting a market that is consolidating but still offers headroom for technology-driven challengers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Solar Panel Recycling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of EU PV installations reaching >70 GW p.a. | +3.2% | EU-wide, with concentration in Germany, France, Spain, Netherlands | Medium term (2-4 years) |

| Mandatory producer-financed recycling under WEEE & EPR | +2.8% | EU-wide, with stricter enforcement in UK, Germany, France | Short term (≤ 2 years) |

| Commercialisation of high-value silicon & silver recovery technologies | +2.1% | Germany, France, Italy, Netherlands | Medium term (2-4 years) |

| EU Critical Raw Materials Act prioritising PV waste streams | +1.9% | EU-wide, strategic focus in Germany, France, Poland | Long term (≥ 4 years) |

| Automotive OEM demand for recycled solar-grade silicon for EV batteries | +1.5% | Germany, France, UK, with spillover to Central Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of EU PV Installations Reaching >70 GW Annually

Photovoltaic build-outs exceeded 70 GW in 2024 and remain on pace for similar yearly additions, front-loading a deferred waste surge estimated at 2.5 million tonnes by 2031.[2]SolarPower Europe, “EU Market Outlook 2024-2028,” solarpowereurope.org Rising volumes give recyclers long-term visibility that supports 10-plus-year plant lifetimes. Germany and Spain contributed over 14 GW each in 2024, accelerating the need for collection partnerships that pre-book fleet decommissioning. The growth also tightens landfill restrictions because environmental agencies now track module flows against installation registries. Collectively, these forces create a predictable, sizable feedstock that encourages creditors to underwrite large-scale capacity.

Mandatory Producer-Financed Recycling Under WEEE & EPR

The 2012 WEEE amendment, and its country-specific EPR transpositions, compel manufacturers to absorb all collection and processing costs, eliminating volume risk for recyclers but compressing fee margins when the distance to the plant exceeds 400 km. France’s SOREN scheme gathered 6,200 tonnes of PV waste in 2024, a 40% increase over 2023, proving regulatory teeth are now fully in place.[3]SOREN, “Annual Report 2024,” soren.fr Germany’s Stiftung EAR issued fines for non-registered imports, signaling that passive compliance is no longer tolerated. These penalties encourage module redesign for easier disassembly, indirectly improving recycling yields.

Commercialization of High-Value Silicon & Silver Recovery Technologies

Laser-based delamination and thermo-chemical silicon extraction demonstrated pilot-scale success in 2024, lifting wafer recovery to 87% and securing 99.99%-pure silver fractions when paired with METALOR refining lines. By cutting contamination, recyclers can sell silicon at 60-70% of virgin polysilicon prices, bringing an additional USD 20-30 per module in value capture. These margins justify capital budgets near EUR 3 million per line when throughput tops 5,000 tonnes annually, tipping ROI calculations decisively in favor of advanced systems.

EU Critical Raw Materials Act Prioritizing PV Waste Streams

Adopted in March 2024, the Act earmarks EUR 400 million in Innovation Fund grants for recycling plants that secure silicon, silver, and indium domestically. It also sets a 15% recycled-content requirement for public-procured panels post-2027, creating a guaranteed offtake channel for recovered fractions. Poland and the Czech Republic are positioning themselves as processing hubs by offering fast-track permits and lower labor costs, but must still align with EU certification protocols slated for release in mid-2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics cost for bulky modules across EU borders | -1.8% | Cross-border routes, particularly Eastern Europe to Western Europe | Short term (≤ 2 years) |

| Slow scale-up of purpose-built recycling lines (<30 kt/yr capacity) | -1.5% | EU-wide, with bottlenecks in Spain, Italy, Poland | Medium term (2-4 years) |

| Silver price volatility undermining recycler ROI | -1.2% | EU-wide, affecting all recyclers dependent on precious-metal recovery | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Logistics Cost for Bulky Modules Across EU Borders

Transport dominates cost structures when modules travel beyond 300 km, reaching EUR 0.12 per kilogram on some Poland-to-France routes.[4]Transport & Environment, “PV Module Logistics Cost Study 2024,” transportenvironment.org Basel Convention paperwork and lead-cadmium testing add week-long delays, eroding recycler cash flow. Regional shredding hubs cut weight by up to 70%, but replicating equipment across 10-15 satellite sites strains balance sheets for small operators.

Slow Scale-Up of Purpose-Built Recycling Lines (< 30 kt/yr)

Europe had only 30 kt of annual capacity in 2025 against 200 kt of waste looming by 2030. Veolia’s Rousset plant, though pioneering, maxes out at 4 kt per year and took 24 months to permit. Financing hurdles persist because revenue depends on uncertain future waste flows; EIB loans to ROSI Solar are disbursed only after offtake contracts are signed, prolonging start-up timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process: Laser Delamination Challenges Mechanical Dominance

Mechanical shredding controlled 65.8% of 2025 revenue because legacy lines are fully depreciated and remain easy to operate. However, laser systems are expanding at a 16.9% CAGR, the sharpest among all processes, thanks to 95% glass purity and residue-free wafer output that garners higher sale prices. In USD terms, laser-enabled plants add USD 25-30 per tonne in incremental value, a differential sufficient to amortize EUR 3 million equipment packages when annual volumes exceed 5,000 tonnes. ROSI Solar’s hybrid flow pairs low-cost shredding for aluminum removal with laser finishing for high-grade fractions, demonstrating a pragmatic bridging strategy that aligns with evolving WEEE air-emission norms. Over the forecast horizon, mechanical methods will still serve thin-film modules and small-scale feeders, but laser units are poised to command premium fractions and set new benchmarks for environmental compliance within the European solar panel recycling market.

Operational scale remains the decisive adoption filter. Below 2,500 tonnes per year, simple shredders outcompete in capex and uptime, giving them an embedded base in smaller Eastern European and Mediterranean markets. Yet national tenders increasingly score bids on recovery rates, gradually shifting procurement in favor of laser or thermo-chemical lines. Public funding under the EU Innovation Fund specifically prioritizes > 85% recovery thresholds, effectively nudging future capacity toward advanced configurations and trimming the long-term share of basic mechanical plants within the European solar panel recycling market landscape.

By Panel Type: Thin-Film Waste Accelerates Despite Crystalline Prevalence

Crystalline silicon modules represented 81.6% of inbound waste in 2025, mirroring their installation share. Their diversified material mix, glass, aluminum, silicon, and silver, keeps them the economic backbone of the European solar panel recycling market. Thin-film CIGS, however, is growing at a 19.1% CAGR because many first-wave utility arrays are failing earlier than projected. Although CIGS panels lack silver, they contain indium and gallium, which the Critical Raw Materials Act now ranks as strategic, propelling specialized recovery ventures in Germany and Italy. Early adopters such as First Solar illustrate closed-loop viability, recovering 90% of cadmium-telluride material for re-use.

Variations in regulatory costs further shape segment economics. Thin-film recyclers must manage hazardous-waste permits, adding EUR 50-100 per tonne. Crystalline processors steer clear of these surcharges, but they may face diminishing silver returns as modern modules adopt lower metallization loadings. Panel OEMs are responding with take-back programs that interlock with their own recycling pilots, a trend exemplified by Trina Solar’s 2024 fully recycled module, which showcases how manufacturer control can shorten material loops and reshape competition across panel categories within the European solar panel recycling market.

By Shelf Life: Early-Loss Failures Move Center Stage

Modules older than 25 years accounted for 69.5% of 2025 waste, but units under 10 years will rise at a 16.2% CAGR, fueled by storm damage, manufacturing defects, and grid-code upgrades. Early-loss modules complicate planning because they appear unpredictably, yet they offer higher residual performance, enabling resale into off-grid uses. ROSI Solar’s April 2025 pact with Yingli segregates such modules through automated flash testing, extracting a secondary revenue stream that offsets recycling costs. Parallel trends in insurance, hail-damage claims jumped 60% in Germany and France in 2024, meaning that decommissioning decisions now rest as much with underwriters as asset owners.

Normal-loss modules still deliver superior silver yields because older cells used heavier metallization. Yet they also suffer deeper encapsulant browning and micro-cracking, requiring aggressive mechanical or thermal treatment that elevates energy input. By 2031, recyclers anticipate processing equal volumes from both age cohorts, demanding flexible plant layouts that can switch between resale screening and material shredding without lengthy changeovers.

By Material Recovered: Silver Growth Outpaces Glass Volume

Glass accounted for 48.2% of 2025 material value owing to its mass share, but price points remain low at EUR 30-70 per tonne. Silver, only a few hundred grams per tonne, is projected to post the fastest 15.3% CAGR because purity upgrades unlock direct sales to electronics and jewelry supply chains that pay 10-15% above bullion traders. Fixed-price agreements, such as ROSI Solar’s tie-up with METALOR, illustrate how vertical deals hedge market swings, stabilizing EBITDA even when spot markets soften. Silicon wafer recovery, showcased by the FORESi consortium’s 87% yield pilot, may scale to 5,000 tonnes yearly by 2027, but still faces high chem-refining costs that limit near-term margin contribution.

Aluminum and copper remain quick-cash fractions, easy to process and liquid to sell, yet they deliver limited upside. Conversely, indium and gallium from CIGS lines could command strategic premiums once hydrometallurgical routes mature, backed by Innovation Fund calls that reward critical-material extraction. The evolving hierarchy underscores why glass tonnage may shrink in relative value even as volumes climb, while high-purity metals and silicon dictate profitability arcs inside the European solar panel recycling market.

Geography Analysis

The United Kingdom dominated the European solar panel recycling market in 2025 with 23.7% revenue share and is set to grow at 13.7% CAGR through 2031. The advance reflects stringent WEEE enforcement, dense rooftop fleets, and ROSI Solar’s partnership with Waste Experts, which extends collection to 95% of postal codes and lowers per-module logistics costs by 25%. Government grants aimed at “green jobs” further sweeten project economics, encouraging domestic processing rather than export to continental plants.

France and Germany together supplied over 40% of regional capacity in 2025. Veolia’s Rousset plant and Reiling’s dual German sites anchor Western Europe’s infrastructure, processing 12,000-plus tonnes annually. Both countries benefit from transparent compliance registries, SOREN and Stiftung EAR, that provide recyclers with advance visibility into decommissioning schedules, enabling feedstock contracts that run five years or longer. Germany’s industrial clusters also host glass and metal buyers, trimming transport legs for recovered fractions.

Southern and Eastern Europe are emerging fast. Spain, propelled by the Trabede and Greening Group’s 8,000-tonne plant planned for 2027, leverages lower labor costs and proximity to Iberian utility portfolios facing EPR mandates. Italy, with 9-Tech’s Venice laser pilot, positions itself as a technology testbed, though national capacity remains under 3 kt per year. Poland and the Czech Republic advertise rapid-permit zones to lure investors under the Critical Raw Materials Act, but capital deployment is lagging due to financing constraints and refining bottlenecks. Nordic markets remain niche, yet Norsk Solar Recycling’s 1,500-tonne line offers a template for high-latitude nations seeking localized processing that avoids expensive cross-Baltic transport.

Competitive Landscape

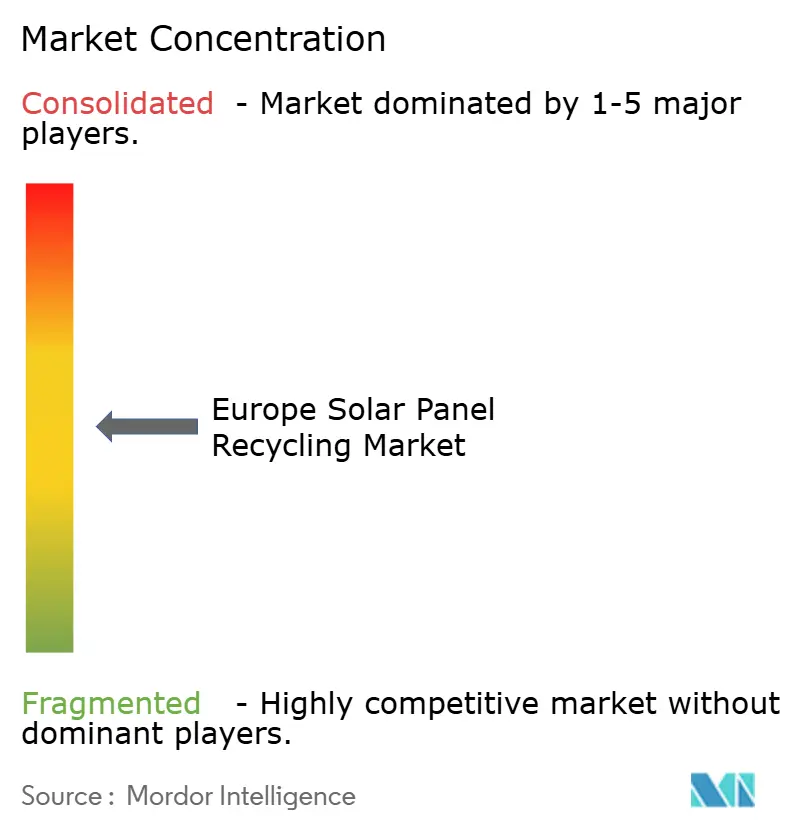

Competition in the European solar panel recycling market is moderate and technology-centric. Veolia, Reiling, ROSI Solar, PV Cycle, and First Solar hold 35-40% combined revenue, but entry barriers are falling as Innovation Fund grants cover up to 60% of eligible capex. Veolia’s 2024 move to purchase aging solar farms illustrates a vertical strategy that locks in feedstock before rivals bid. ROSI Solar counters with a refining ecosystem, AGC Glass for cullet, METALOR for silver, Yingli for resale testing, tightening its grip on value-add steps and achieving margins smaller plants struggle to match.

Manufacturers are entering the fray. Trina Solar’s fully recycled module, shielded by 37 patents, stakes a claim that OEMs can internalize circularity, leveraging brand and scale to outflank independent recyclers. First Solar remains the thin-film specialist, operating closed-loop CdTe lines since 2018 and supplying tales of 90% material recovery that resonate with policymakers targeting hazardous-waste reduction. Laser trailblazers 9-Tech and Apellix differentiate on purity and carbon metrics; however, capital needs above EUR 2 million per line pose a hurdle unless throughput tops 5,000 tonnes annually.

Consolidation is expected as midsize firms lacking proprietary technology pair with collection specialists to survive. Cross-border partnerships, typified by ROSI Solar’s UK and Swiss logistics tie-ups, foreshadow a regional supply-web where high-value fractions flow to centralized refiners while low-value glass remains local. Regulatory harmonization on recycled-content verification, due mid-2026, will likely raise compliance costs, nudging the market toward fewer but larger, certified operators.

Europe Solar Panel Recycling Industry Leaders

-

Veolia Environnement S.A.

-

Reiling PV-Recycling GmbH

-

ROSI Solar

-

PV Cycle (incl. Soren)

-

First Solar Inc. (Europe ops)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: AGC Glass Europe, a leading flat glass manufacturer in Europe, has teamed up with SOLAR MATERIALS, a German cleantech startup. Their collaboration aims to incorporate high-purity recycled flat glass, or cullet, sourced from decommissioned solar panels, into AGC's float glass production.

- March 2025: Lotus Energy, a solar module recycling firm from Australia, has announced plans for a USD 250 million recycling facility in Saxony, Germany. The 24,000 square metre facility will be developed with the backing of Invest Region Leipzig, an entity supported by both the German federal government and the state of Saxony.

- January 2025: EMR, with its extensive history in recycling and repurposing both ferrous and non-ferrous metals, has partnered with Solar Energy UK. Together, they aim to explore the solar industry's potential in fostering a circular economy. EMR boasts the capability to process a diverse array of solar panel components.

Europe Solar Panel Recycling Market Report Scope

Recycling solar modules is a complex task in which materials/layers of a solar module can be separated, and metals, such as lead, copper, gallium, cadmium, aluminum, and silicon, can be recovered and reused in new products.

The European solar panel recycling market is segmented by process, panel type, shelf life, material recovered, and geography. By process, the market is segmented into thermal, mechanical, and laser. By panel type, the market is segmented into crystalline silicon and thin film. By shelf life, the market is segmented into normal loss above 25 years and early loss below 10 years. By material recovered, the market is segmented into glass, silicon wafers, silver, aluminium, and other metals. The report also covers the market size and forecasts for the Aviation fuels market across major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Process

| Thermal |

| Mechanical |

| Laser |

By Panel Type

| Crystalline Silicon |

| Thin Film |

By Shelf Life

| Normal Loss (Above 25 yr) |

| Early Loss (Below 10 yr) |

By Material Recovered

| Glass |

| Silicon Wafers |

| Silver |

| Aluminium |

| Other Metals (Cu, Indium, etc.) |

By Geography

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Poland |

| Sweden |

| Norway |

| Russia |

| Rest of Europe |

| By Process | Thermal |

| Mechanical | |

| Laser | |

| By Panel Type | Crystalline Silicon |

| Thin Film | |

| By Shelf Life | Normal Loss (Above 25 yr) |

| Early Loss (Below 10 yr) | |

| By Material Recovered | Glass |

| Silicon Wafers | |

| Silver | |

| Aluminium | |

| Other Metals (Cu, Indium, etc.) | |

| By Geography | United Kingdom |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Belgium | |

| Poland | |

| Sweden | |

| Norway | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe solar panel recycling market in 2026?

The Europe solar panel recycling market size is estimated at USD 179.92 million in 2026, keeping pace with the 11.51% CAGR projected through 2031.

Which recycling process is growing fastest in Europe?

Laser-based delamination leads with a 16.9% CAGR because it achieves 95% glass purity and high-grade silver and silicon recovery.

Why is the United Kingdom the largest national market?

Stringent WEEE enforcement, dense rooftop installations, and ROSI Solar's nationwide collection partnership give the UK a 23.7% revenue share.

How do silver price swings affect recycler profitability?

Silver contributes up to 25% of recovered value, so price drops below USD 24/oz can wipe out margins unless firms hold hedging contracts or fixed-price refinery deals.

What role does the EU Critical Raw Materials Act play?

The Act channels EUR 400 million in grants and enforces a 15% recycled-content rule for publicly procured panels, ensuring steady demand for recovered silicon and silver.

Which companies are the current market leaders?

Veolia, Reiling, ROSI Solar, PV Cycle, and First Solar collectively hold 35-40% market share, leveraging integrated collection networks and proprietary technologies.

Page last updated on: