Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

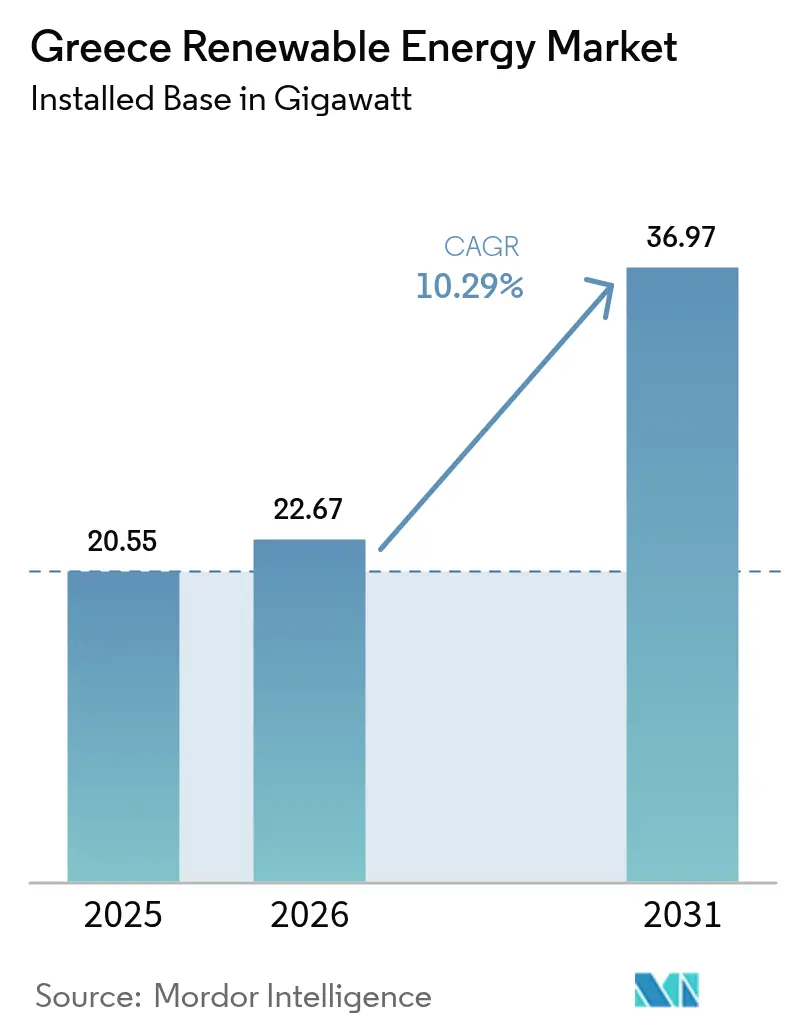

| Base Year Market Size (2025) | 20.55 gigawatt |

| Market Volume (2026) | 22.67 gigawatt |

| Market Volume (2031) | 36.97 gigawatt |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Renewable Energy Market Analysis by Mordor Intelligence

The Greece Renewable Energy Market size is expected to grow from 20.55 gigawatt in 2025 to 22.67 gigawatt in 2026 and is forecast to reach 36.97 gigawatt by 2031 at 10.29% CAGR over 2026-2031.

Solar technology retained 51.3% of capacity in 2024, while wind, hydropower, and fast-emerging geothermal resources are diversifying the generation mix. Falling utility-scale solar capital costs, accelerated offshore legislation, and EU-funded grid expansions are strengthening project fundamentals despite a higher cost-of-capital environment. Corporate power-purchase agreements are deepening demand from data-center operators and energy-intensive manufacturers, while HVDC export cables are unlocking cross-border revenue streams. Competitive positioning is evolving rapidly as large international utilities and sovereign investors consolidate portfolios and secure scarce grid-connection slots..[1]European Commission, “REPowerEU Country Factsheet—Greece,” ec.europa.eu

Key Report Takeaways

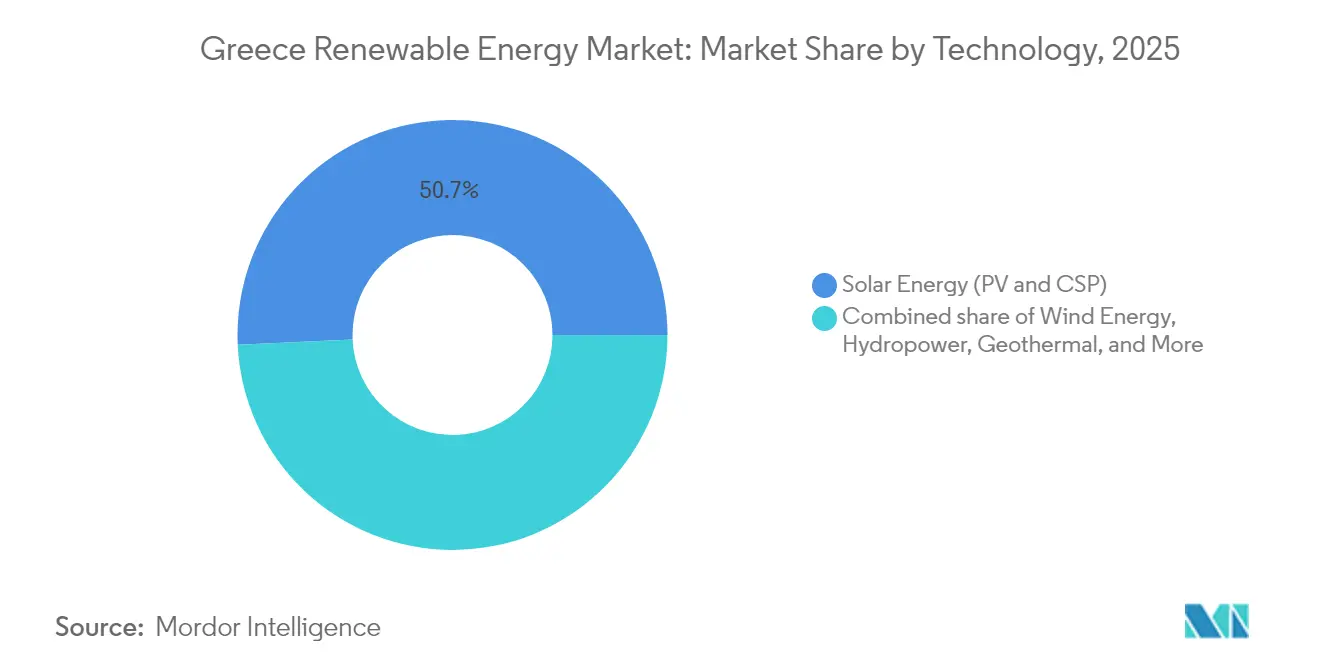

- By technology, solar retained 50.72% of the Greek renewable energy market share in 2025, whereas geothermal is forecast to post the fastest 78.46% CAGR through 2031.

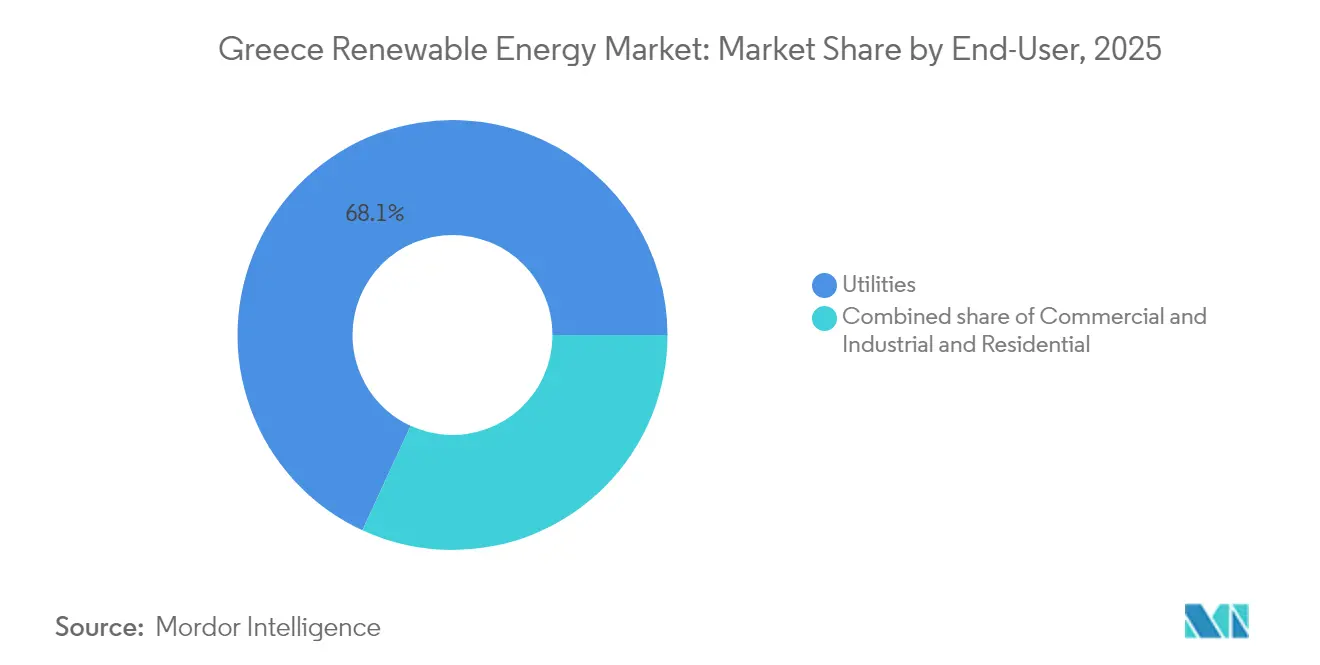

- By end-user, utilities commanded 68.12% of the Greek renewable energy market size in 2025, while commercial and industrial installations are projected to advance at a 10.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Greece Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated offshore wind legislation & 2 GW target | +2.1% | Aegean and Ionian priority zones | Medium term (2-4 years) |

| EU-funded grid and storage upgrades | +1.8% | Western Macedonia, Crete, Cyclades | Medium term (2-4 years) |

| Rapid decline in utility-scale solar CAPEX | +2.3% | Thessaly, Central Greece, Peloponnese | Short term (≤ 2 years) |

| Rise of corporate PPAs | +1.2% | Attica and Thessaloniki industrial clusters | Medium term (2-4 years) |

| Cross-Mediterranean export cables | +1.5% | Crete and mainland export hubs | Long term (≥ 4 years) |

| Pumped-hydro and battery tenders | +1.4% | Western Macedonia and island grids | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Offshore Wind Legislation & 2 GW Target by 2030

Greece enacted a comprehensive offshore wind framework in June 2024, setting a 2 GW deployment goal for 2030 and introducing streamlined licensing for floating platforms located in waters deeper than 50 meters. Priority development zones in the Aegean and Ionian Seas record average wind speeds above 8 m/s, positioning floating technology for high utilization factors.[2]Hellenic Parliament, “Offshore Wind Development Law 5082/2024,” hellenicparliament.gr International turbine suppliers quickly established Hellenic service hubs, enabling developers to sign grid connection agreements ahead of final investment decisions. The 2 GW target equates to nearly 6% of forecast capacity in 2030, yet its superior capacity factors promise outsized contributions to grid stability and export volumes.

EU-Funded Grid & Storage Upgrades Under REPowerEU/NECP

The European Commission allocated EUR 790 million in REPowerEU funding, and the European Investment Bank committed EUR 1.2 billion in loans to reinforce Greek transmission assets from 2024-2027. Projects include the Cyclades interconnection, which links seven islands to the mainland, and 400 kV substation upgrades in Western Macedonia. The National Energy and Climate Plan mandates 900 MW of new storage, split between pumped-hydro and lithium-ion batteries. Terna Energy’s 680 MW Amfilochia pumped-storage plant alone will supply 816 GWh of annual balancing energy, a critical buffer as thermal baseload retires.[3]Terna Energy, “Amfilochia Pumped-Storage Project Update,” terna-energy.gr

Rapid Decline in Utility-Scale Solar CAPEX

Utility-scale solar costs in Greece decreased by 48% between 2022 and 2023, to approximately USD 0.65/W, driven by module price deflation and efficient EPC practices on flat, high-irradiation sites.[4]IRENA, “Renewable Power Generation Costs in 2023,” irena.org Merchant projects now achieve levelized costs below EUR 40/MWh, beating natural-gas peakers. Lightsource bp’s 560 MW Enipeas solar complex, financed in April 2024, illustrates the robust bankability of large-scale solar without feed-in tariffs. Continued declines are expected as bifacial modules and single-axis trackers become more widely adopted, although land prices in prime zones are rising due to grid capacity scarcity.

Rise of Corporate PPAs from Greek Industrials & Data-Centers

Corporate renewable PPAs topped 1.5 GW of signed or advanced capacity in 2024. Amazon secured approximately 500 MW of wind power for its European data center network, underscoring the surging demand for hyperscale data centers. Aluminum, cement, and food-processing plants are locking in long-term PPAs to hedge wholesale price volatility that exceeded EUR 180/MWh during the 2024 winter gas crunch. The Regulatory Authority for Energy shortened PPA approval cycles to eight weeks, enabling direct contracts between generators and industrial offtakers. These developments underpin the double-digit growth outlook for the commercial and industrial segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regional permitting bottlenecks | −1.3% | Cyclades and forested mainland areas | Short term (≤ 2 years) |

| Grid hosting limits and curtailment risk | −1.1% | Island grids and Western Macedonia clusters | Medium term (2-4 years) |

| Community push-back on wind farms | −0.8% | Paros, Mykonos, Santorini, coastal Peloponnese | Medium term (2-4 years) |

| Higher post-2024 cost of capital | −1.2% | National, with sharper impact on merchant offshore | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regional Permitting Bottlenecks Delaying Projects

Despite the availability of a digital one-stop licensing portal, environmental impact assessments, archaeological clearances, and grid studies still extend the average approval time to 18-24 months.[5]Government of Greece, “Law 5037/2023—Renewable Licensing Reform,” gov.gr Staffing constraints at RAE left 800 connection requests pending in 2024, discouraging smaller developers. Tourism-driven Cyclades islands add local consultation layers that often end in municipal rejection, redirecting capital to faster-moving Balkan markets.

Grid Hosting Limits & Curtailment Risks

Island grids in Crete and Rhodes recorded curtailment rates exceeding 3% in 2024, as renewable energy injection outpaced local demand.[6]IPTO, “Dispatch Data 2024—Curtailment Report,” ipto.gr Crete–Attica and Cyclades interconnections will ease constraints from 2025 to 2026; however, Western Macedonia solar clusters already face midday voltage swings that demand reactive-power investments. Lenders apply 10-15% revenue haircuts in high-penetration zones, raising financing costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Dominance Meets Geothermal Surge

Solar accounted for 50.72% of the country's capacity in 2025, underscoring the Greek renewable energy market's reliance on photovoltaics. Geothermal capacity, currently under 0.90%, is forecast to scale at an 78.46% CAGR, increasing the segment's share of the Greek renewable energy market to approximately 2.85% by 2031. Mytilineos is drilling a 50 MW plant on Milos, supported by EU Innovation Fund grants that showcase enhanced geothermal systems. Wind, including nascent offshore projects, accounted for approximately 34.83% of installations in 2025, and floating platforms are expected to deliver capacity factors above 45%. Hydropower, at 12.05%, is expected to expand through the 680 MW Amfilochia pumped-storage complex, scheduled for commissioning in 2027. Bioenergy and ocean technologies remain niche due to barriers related to feedstock and cost.

New solar plants benefit from low installed costs and generous irradiation. However, competition for substation capacity is intensifying, prompting developers to shift toward hybrid solar-plus-storage projects that capitalize on higher peak pricing. Geothermal growth relies on successful exploration in the volcanic arc, where heat gradients reach 200°C at economically viable drilling depths. Should resource mapping confirm the presence of commercial reservoirs, geothermal energy could provide a baseload output that complements intermittent solar and wind energy, thereby smoothing the Greek renewable energy market share across technologies.

By End-User: Utilities Lead, C&I Accelerates

Utilities controlled 68.12% of installations in 2025, illustrating the historical dominance of PPC Renewables, Terna Energy, and Mytilineos. Nonetheless, commercial and industrial offtakers are set to raise their share of the Greek renewable energy market, expanding at a 10.62% CAGR on the back of streamlined corporate PPAs and REC-indexed pricing. Amazon’s 500 MW wind contracts in 2024 and Microsoft’s ongoing data-center expansion reflect the decarbonization drive among global cloud providers. The residential segment, assisted by zero-interest Recovery Fund loans, now allows rooftop systems of up to 10 kW to operate without utility approval and is piloting virtual net-metering for apartment dwellers.

Utilities are pivoting toward hybrid solar-plus-storage on rehabilitated lignite sites, adding flex capabilities that position them competitively in balancing markets. Industrial offtakers view PPAs as a hedge against wholesale price volatility, while residential prosumers are reducing bills by exporting excess generation at regulated feed-in premiums. This diversification helps distribute the Greek renewable energy market share more evenly across end-user categories.

Geography Analysis

Mainland regions, Thessaly, Central Greece, and Western Macedonia, hosted 54.26% of the installed capacity in 2025, thanks to their strong grid backbones. The EUR 1.6 billion EU Just Transition Fund supports 2.5 GW of renewables on rehabilitated lignite mines, exemplified by RWE’s 450 MW Amynteo solar cluster that employs 300 local staff. Hydropower and wind in Evia and the Peloponnese balance seasonal solar peaks with steady Meltemi winds.

Island grids present both opportunity and challenge. Crete’s 1,000 MW Crete–Attica interconnection goes live in mid-2025, integrating the island’s 1.2 GW portfolio into mainland dispatch. Seven Cyclades islands will be connected by 2026, unlocking 400-500 MW of new renewable capacity and displacing diesel generation. Pilot microgrids on Astypalaia and Chalki demonstrate the viability of a 100% renewable supply complemented by storage and demand response.

Offshore zones in the Aegean and Ionian Seas are the next frontier for growth. Legislation adopted in 2024 earmarks 10,000 km² for floating platforms in water depths beyond 50 m. Terna Energy and Ocean Winds are advancing a 1.5 GW joint venture off Crete that uses semi-submersible foundations to minimize seabed impact. The Hellenic Navy and the Ministry of Maritime Affairs are finalizing spatial plans to deconflict fishing and shipping lanes, paving the way for 2-3 GW of additional capacity decisions in 2025-2027.

Competitive Landscape

The top five operators, Terna Energy, PPC Renewables, Mytilineos, Motor Oil Renewables, and Enel Green Power, controlled nearly 60% of operational assets in 2024, yielding a moderate market concentration. Masdar’s EUR 3.2 billion purchase of 70% of Terna Energy positions the Abu Dhabi group to add 6 GW by 2029 and signals continued inbound investment. Mytilineos and PPC struck a EUR 2 billion solar partnership spanning Southeastern Europe, rotating mature Greek assets into PPC’s balance sheet and funneling proceeds into regional growth. RWE and PPC are co-developing 450 MW of solar energy with integrated battery storage on a former lignite mine.

Strategic differentiation is shifting toward storage integration, early grid access, and floating offshore intellectual property. Terna Energy locked a 35-year grid right for its 680 MW Amfilochia pumped-storage plant, while Lightsource bp leveraged BP’s balance sheet to finance 560 MW in Thessaly at competitive spreads. Mytilineos and Ocean Winds dominate patent activity in enhanced geothermal systems and floating foundations. As capital costs rise, well-capitalized incumbents are expected to widen their lead, although corporate PPAs offer a niche for agile developers willing to assume merchant exposure.

Greece Renewable Energy Industry Leaders

Terna Energy SA

PPC Renewables (PPC SA)

Mytilineos SA

Enel Green Power Hellas

Motor Oil Renewable Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Alpha Bank, a prominent Greek lender, unveiled plans to finance the construction of four solar parks in Greece, boasting a combined capacity of 267 MW. The projects, backed by investment fund managers Foresight and Mirova, are set to rise in Farsala and Fthiotida, Thessaly. With an estimated construction cost of €316 million, these solar initiatives represent a significant step forward in Greece's renewable energy landscape.

- April 2025: Meton Energy, a collaboration between RWE Renewables Europe & Australia, and PPC Renewables, has greenlit its final investment for two major photovoltaic projects in Central Macedonia, Greece. The solar farms, dubbed Kotyli and Neo Syrakio, boast a combined capacity of 567 megawatts peak (MWp). Construction is slated to commence in spring 2025, with a target commissioning date of 2027.

- September 2024: PPC Group signed a collaboration agreement with the Copelouzos and Samaras groups for acquiring a 66.6 MW operational renewable energy portfolio and a 1.7 GW development pipeline. The operational portfolio comprises two wind parks with a combined capacity of 43.3 MW in South Evia and Lakonia, as well as PV parks with a total capacity of 23.3 MW.

- April 2024: The European Commission greenlit a EUR 1 billion (USD 1.1 billion) state aid package for Greece, aimed at bolstering two solar-plus-storage initiatives. The first, dubbed the Faethon Project, features two solar plants, each boasting a capacity of 252MW. These plants will be paired with molten-salt thermal storage units and an extra-high voltage substation.

Greece Renewable Energy Market Report Scope

Renewable energy is energy derived from natural sources that are replenished at a faster rate than they are consumed. Sunlight and wind, for example, are such sources that are constantly replenished.

The Greek Renewable Energy Market is segmented by Technology (Solar Energy (PV and CSP), Wind Energy (Onshore and Offshore), Hydropower (Small, Large, PSH), Bioenergy, Geothermal, Ocean Energy (Tidal and Wave)), By End-User (Utilities, Commercial and Industrial, Residential). For each segment, the market sizing and forecasts have been done based on installed capacity in gigawatts (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How fast is renewable capacity in Greece expanding?

Installed capacity is forecast to rise from 22.67 GW in 2026 to 36.97 GW by 2031, equal to a 10.29% CAGR.

Which technology will grow the quickest by 2031?

Geothermal is projected to register an 78.46% CAGR, albeit from a small base of 30 MW.

What role do corporate PPAs play in new projects?

PPAs exceeding 1.5 GW are in negotiation or signed, enabling data-center operators and heavy industry to lock in long-term renewable supply.

How will new interconnectors affect the market?

The Greece–Egypt and Great Sea HVDC links will export surplus solar and wind, lowering curtailment risk and improving project bankability.

What storage capacity is being added?

RAE tendered 900 MW of storage in 2024, led by the 680 MW Amfilochia pumped-hydro plant and 300 MW of island batteries, to balance rising solar penetration.

Which regions attract the most new capacity?

Western Macedonia, Thessaly, and Central Greece lead due to grid strength and EU transition funds, while island grids gain once subsea links become operational.

Page last updated on: