Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.64 Billion |

| Market Size (2026) | USD 12.25 Billion |

| Market Size (2031) | USD 15.78 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Home Furniture Market Analysis by Mordor Intelligence

Poland home furniture market size in 2026 is estimated at USD 12.25 billion, growing from 2025 value of USD 11.64 billion with 2031 projections showing USD 15.78 billion, growing at 5.2% CAGR over 2026-2031. Rising first-time home purchases under the Bezpieczny Kredyt 2% scheme, persistent remote-work patterns, and a clear consumer tilt toward space-saving modular pieces sustain the growth momentum[1]Bezpieczny Kredyt 2% Factsheet, gov.pl. Manufacturers are broadening material portfolios with recyclable polymers to complement Poland’s long-standing woodworking heritage, while e-commerce penetration lifts direct-to-consumer sales, trimming retail mark-ups. Re-shoring by export-oriented producers is enlarging premium domestic offerings, and Masovian’s economic weight ensures a robust demand backbone even amid inflationary pressures. Supply-chain recalibration—especially on timber—remains the chief cost variable, yet high FSC certification rates help firms command price premiums in sustainability-minded urban demographics.

Key Report Takeaways

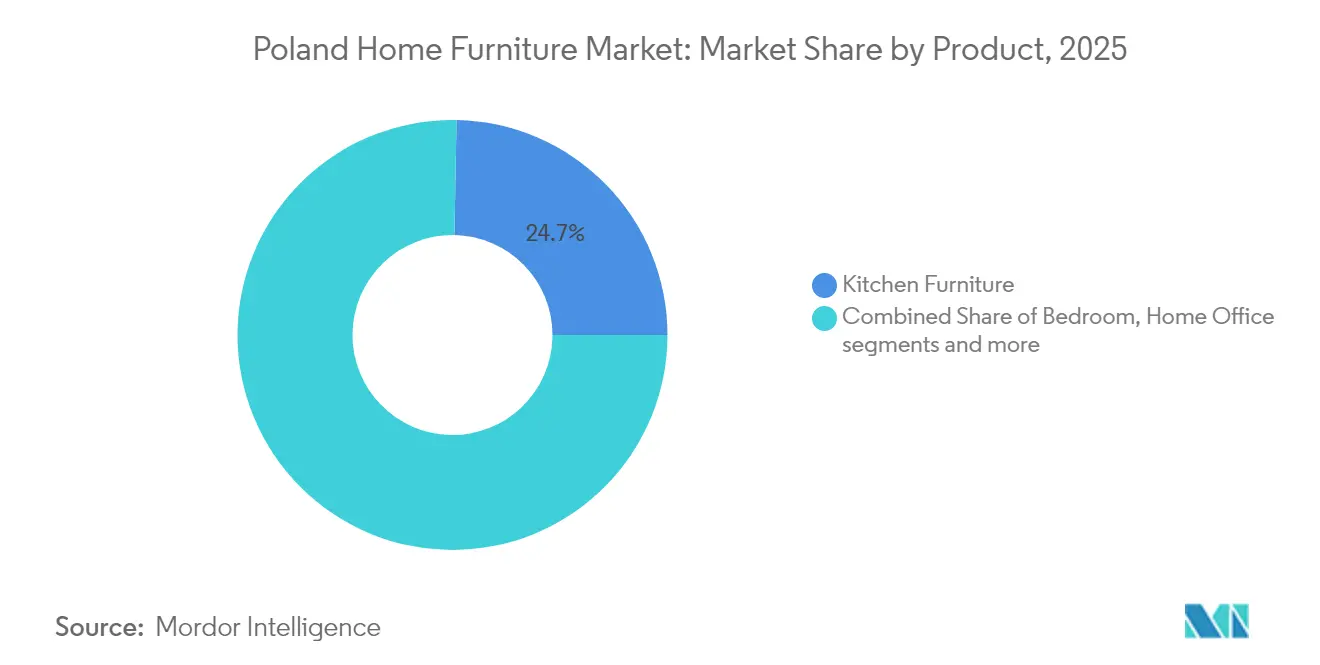

- By product, kitchen furniture led with 24.70% revenue share in 2025; home office furniture is projected to expand at a 5.75% CAGR to 2031.

- By material, wood held 44.35% of the Poland home furniture market share in 2025, while plastic & polymer is advancing at a 5.15% CAGR through 2031.

- By price range, mid-range captured 54.20% of the Poland home furniture market size in 2025; the premium tier is poised to grow at 5.65% CAGR through 2031.

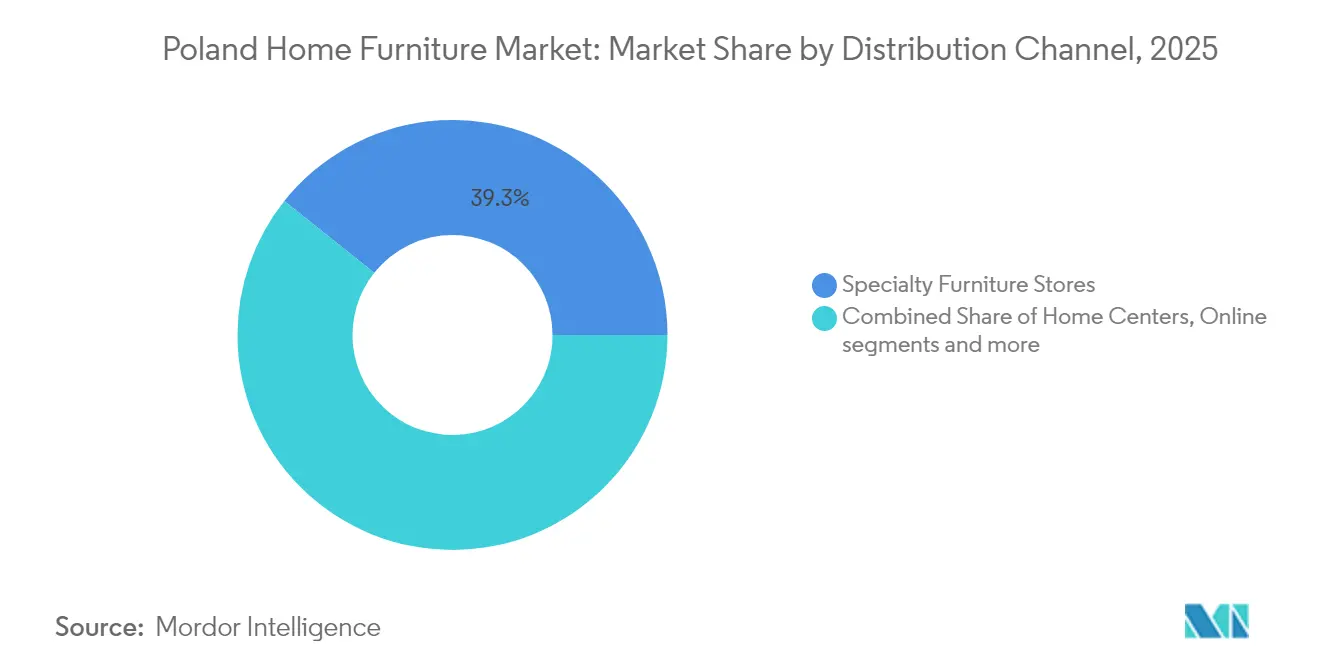

- By distribution channel, specialty stores controlled 39.30% revenue in 2025; online retail is rising at a 6.35% CAGR to 2031.

- By geography, Masovian (Mazowieckie) accounted for 19.85% share of the Poland home furniture market in 2025, while Lesser Poland (Małopolskie) is the fastest-growing region at a 5.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Re-Urbanization Fueling Small-Space Furniture Demand | +1.2% | National, concentrated in Warsaw, Kraków, Wrocław | Medium term (2–4 years) |

| Government “Mieszkanie Plus” Housing Program Boosting First-Time Furniture Purchases | +0.8% | National, higher impact in metropolitan areas | Short term (≤ 2 years) |

| Rise of Domestic E-Commerce Platforms Increasing Direct-to-Consumer Sales | +0.6% | National, with urban concentration | Medium term (2–4 years) |

| Export-Oriented Polish Producers Re-Shoring Capacity to Serve Domestic Premium Segment | +0.4% | Masovian, Wielkopolskie, Śląskie regions | Long term (≥ 4 years) |

| Growing Popularity of Sustainable FSC-Certified Wood Furniture Among Millennials | +0.3% | National, with urban millennial concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Re-Urbanization Fueling Small-Space Furniture Demand

Urban migration intensifies in Poland even as housing supply tightens, with 28% of adults still sharing homes with family and apartment completion cycles lengthening from 21 to 26.5 months. Average unit size is 90.8 m², nudging producers toward transformable sofas, fold-down desks, and storage-rich ottomans that permit multifunctional use in limited floorplates[2]“Housing Completions and Permit Statistics 2025,” stat.gov.pl. Warsaw tenants now devote 43% of wages to rent, prompting compact furnishing choices, while border cities absorbing Ukrainian refugees favor quick-assembly, budget-oriented lines[3]“Urban Rental Affordability in Poland,” infor.pl. Manufacturers pairing modular design with rapid delivery gain share as customers equate adaptability with value. Marketing that highlights dual-purpose utility resonates strongly with tech-savvy millennials and Gen Z households.

Government “Mieszkanie Plus” Housing Program Boosting First-Time Furniture Purchases

Ongoing government mortgage subsidies, an entrenched hybrid-work culture and a growing roster of premium domestic collections keep demand momentum intact even while raw-material inflation nudges production costs. The Bezpieczny Kredyt 2% plan cuts early mortgage outflows from PLN 5,400 to PLN 2,800, channeling freed funds straight into furnishing budgets. Loan ceilings of PLN 600,000 for families spark comprehensive room fit-outs, lifting demand peaks in kitchen, bedroom, and living zones. January 2025 housing completions rose 3.8% to 15,500 units, predominantly targeting subsidy beneficiaries. Retailers leverage the 10-year subsidy window to craft instalment bundles keyed to mortgage cycles. Retailers clustered near new-build complexes can expect a predictable revenue stream, as each subsidized buyer is projected to make significant expenditures on initial furniture purchases.

Rise of Domestic E-Commerce Platforms Increasing Direct-to-Consumer Sales

AI-driven configurators and AR visualization lift online average order values by 30% while slashing return rates for color or size mismatches[4]Furniture World, “Intiaro Visualization Boosts Sales,” furnitureworld.com . TikTok commerce helps brands court younger consumers through shoppable short videos, building brand equity without heavy store investments. Cross-border digital storefronts enable Polish makers to pilot Scandinavian demand before pursuing physical distribution. Omnichannel models merge showroom touchpoints with online convenience, allowing specialty chains to protect their 40% store share while scaling national reach.

Export-Oriented Polish Producers Re-Shoring Capacity to Serve Domestic Premium Segment

A decrease in export revenue spurring factories to tilt output toward affluent Polish buyers and avoid freight volatility. Premium lines fetch higher margins, offsetting volume decline and currency swings. Masovia’s dense high-income cluster provides a ready customer base, while Wielkopolskie workshops leverage proximity to automated plants and just-in-time systems for custom orders. The strategic pivot compresses lead times, supports personalized finishes, and upgrades perceived quality. Domestic brands thus challenge imported design houses on craftsmanship and sustainability, cementing the long-view trajectory of the Poland home furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Raw Material Prices Driven by Belarus/Russia Supply Disruptions | –1.1% | National, with a higher impact on wood-dependent manufacturers | Short term (≤ 2 years) |

| Lengthy Building Permit Cycles Delaying New-Build Furnishing Demand | –0.7% | National, with regional variations in bureaucratic efficiency | Medium term (2–4 years) |

| Fragmented Last-Mile Logistics Raising Return Costs for Online Retailers | –0.4% | National, with rural areas most affected | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging Raw Material Prices Driven by Belarus/Russia Supply Disruptions

EU sanctions curtailed Belarusian timber inflows, and suspect imports from Kazakhstan ballooned from EUR 14 million to EUR 68 million, destabilizing price benchmarks [5]“Kazakh Timber Routes Raise Sanction Alerts,” occrp.org. Smaller factories face a choice between absorbing losses or slowing production, both of which curb market momentum. Consumer push-back is already visible in delayed replacement cycles, softening near-term domestic demand. Import-substitution from Baltic, Slovak, and Ukrainian suppliers is underway, yet limited capacity and higher freight mean relief will be gradual. Raw-material volatility, therefore, remains the most immediate cost headwind for the Poland home furniture market through at least 2026.

Lengthy Building Permit Cycles Delaying New-Build Furnishing Demand

Construction timelines now stretch beyond 26 months, frustrating production planning for made-to-order cabinetry. Permit issuances plummeted 23.6% year-on-year in April 2025, while starts fell 5.5%, pushing furniture demand further into the future. Consumers often postpone bespoke orders until permit clarity emerges, diluting pipeline visibility for suppliers. Though easing digitization may shorten approvals mid-term, the drag will shave close to 0.7 percentage points from forecast growth until 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Kitchen Primacy and Home-Office Upswing

Kitchen furniture remains the anchor, holding 24.70% of the Poland home furniture market in 2025, thanks to the central role of cooking areas in compact homes. High remodel frequency guarantees baseline volumes, while smart storage solutions curb clutter. In parallel, home-office furniture records a 5.75% CAGR through 2031 as hybrid work cements. Living room and dining assortments widen with sectional sofas and extendable tables that morph into work surfaces. Bathroom upgrades gain pace, spurred by larger bathrooms in new apartments. Outdoor lines, once seasonal, now ride balcony-usage gains, favoring weatherproof composites. The unifying motif is modularity, allowing Polish households to extract utility from every square meter.

Kitchen’s 24.70% share should moderate gradually as other categories accelerate, yet its absolute value rises in tandem with real-estate completions. Vendors winning in the Poland home furniture market now push quick-ship flat-packs to match mortgage-driven move-in timelines. Tier-two producers leverage digital configurators to bundle cabinetry with appliances, raising basket sizes. Home-office makers integrate ergonomic norms and power-management features to justify premium tags. With rental churn high in Warsaw, pieces that dismantle and reassemble without toolkits earn loyalty and drive repeat sales cycles.

By Material: Wood Heritage, Polymer Innovation

Wood captures 44.35% revenue and underpins Poland home furniture market size leadership, owing to rich forestry assets and 861 FSC-certified firms fsc.org. Consumers view oak and ash finishes as quality markers, especially in Masovian premium dwellings. Yet plastic & polymer lines expand at 5.15% CAGR on the back of lightweight, modular frames ideal for elevator-constrained flats. Metals complement both categories, delivering slim industrial aesthetics for home-office desks. Composite innovations allow disassembly for recycling, aligning with EU circularity mandates.

Wooden producers invest in lean manufacturing to curb waste, raising yield amid raw-material price ascent. Polymer pioneers emphasize recyclability, countering perceptions of lower durability. As hybrid materials blur boundaries, product passports listing carbon footprints become common. Suppliers able to marry wood veneers with polymer cores for weight saving without sacrificing tactile warmth broaden appeal in the Poland home furniture industry.

By Price Range: Mid-Range Backbone, Premium Climb

Mid-range retains 54.20% share, giving the Poland home furniture market a stable revenue base that balances value and longevity. Shoppers in this tier accept mass customization, leading to predictable manufacturing runs. Premium sales, on a 5.65% CAGR track, reflect rising urban disposable incomes and a shift toward viewing furniture as multi-decade assets. Export-focused brands redirect domestic capacity, introducing globally recognized designers to local showrooms.

Mid-range resilience cushions economic shocks; manufacturers negotiate economies of scale to absorb lumber and energy hikes. Premium margins, though smaller in volume, provide useful buffers against input volatility. Economy lines stay relevant for student rentals and border-region demand but face profitability pressure. Differentiation now pivots on warranty length, sustainable sourcing proof, and digital visualization support that shortens purchase cycles.

By Distribution Channel: Specialty Store Authority, Digital Surge

Specialty furniture chains keep a 39.30% share by pairing tactile showrooms with interior-design counsel, reinforcing high-involvement purchase trust. Online outlets grow 6.35% annually, broadening the Poland home furniture market across rural zones via doorstep delivery. Home centers such as IKEA and Agata exploit economies of scale, while hypermarkets capture opportunistic buys. Omnichannel readiness is decisive; consumers browsing on phones expect stock visibility before in-person confirmation.

Specialty retailers integrate click-and-collect to preserve in-store traffic. Logistics partnerships mature as carriers adopt lift-gate trucks and room-of-choice delivery to lower damage claims. Returns management remains a pain point, but algorithmic fit prediction is mitigating mismatch risk.

Geography Analysis

Masovian voivodeship controls 19.85% of the Poland home furniture market, anchored by Warsaw’s premium customer base. High housing density and corporate HQ clusters sustain year-round demand while R&D institutions seed design innovation. Regional infrastructure grants producers fast access to national highways, compressing last-mile costs.

Lesser Poland (Małopolskie) is moving fastest, with a 5.85% CAGR forecast through 2031 as Kraków’s tourism boom lifts property prices and prompts more frequent furniture upgrades. International firms opening regional hubs are bringing in young professionals who prefer clean lines and modular builds. Greater Poland (Wielkopolskie) remains a manufacturing stronghold; plants around Poznań feed Western Europe through well-developed highways and VOX’s new pan-European distribution centre.

Lower Silesia (Dolnośląskie) leans on its industrial roots and cross-border links to Germany and the Czech Republic. Consumers outside the big hubs tend to favour classic wood finishes, while urban shoppers prefer minimalist, space-saving sets, giving producers room to tailor regional assortments. The spread of demand beyond Warsaw reduces market risk and supports steadier national growth as multiple local centres gain scale.

Competitive Landscape

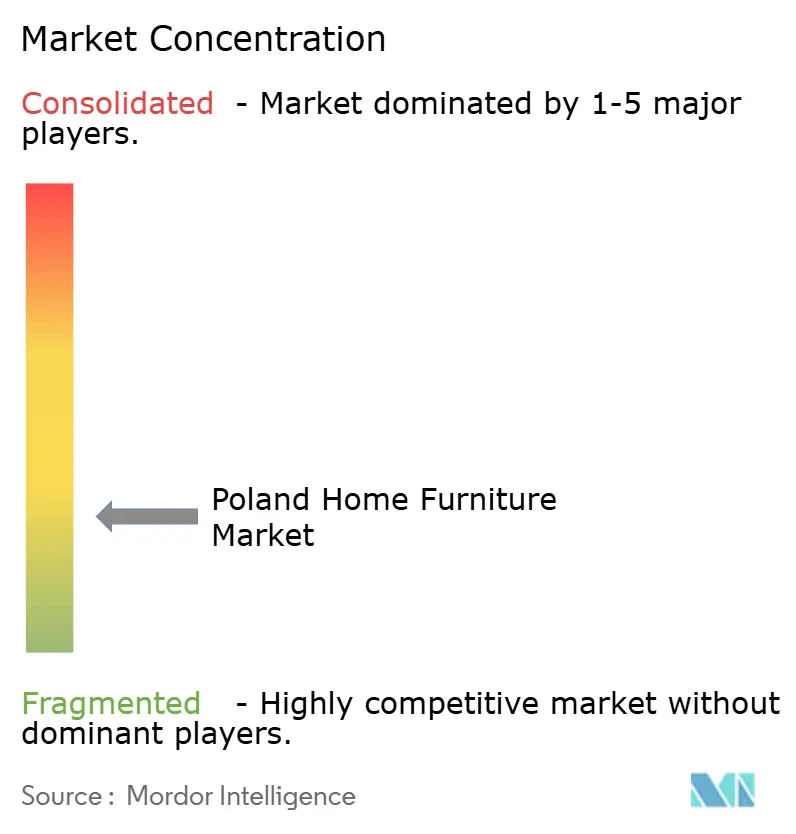

The Poland home furniture market remains fragmented. Dozens of regional mills and boutique upholsterers compete on design niches, making consolidation difficult. Market entry barriers stay low in specialty segments such as youth furniture, encouraging innovation but limiting pricing power.

Technology investment defines emerging leaders. Vendors adopting CNC routers and automated edge-banding shorten lead times and support mass customization. Retailers integrating 3D visualization tools from partners like Intiaro report reduced return rates and higher customer satisfaction. Sustainability remains a branding weapon; firms flaunting FSC tags justify 15–20% premiums. Geographic clusters near Poznań and Wrocław forge supplier networks that share prototypes rapidly and co-market abroad.

E-commerce newcomers leverage influencer channels to scale nationally without large store footprints. Established chains counter by adding design-consult subscription services that build annuity revenue. Partnerships with fintechs for split-payment financing further widen consumer reach. Competitive intensity is expected to persist as no single player breaches a 25% share threshold, aligning the Poland home furniture industry with mid-range concentration norms.

Poland Home Furniture Industry Leaders

IKEA

Black Red White SA

VOX Furniture (Poland Sales Arm)

Fabryki Mebli “Forte” SA

Szynaka-Meble Sp. z o.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Krysiak Furniture secured new U.S. accounts at High Point Market, including Idea Furniture and a major Florida retailer, after meetings with 17 potential buyers exceeding USD 20 million annual volume

- April 2025: Over a dozen Polish manufacturers showcased at the Spring High Point Market in North Carolina via a Polish National Stand organised by the Polish Investment and Trade Agency; BIM SP z.o.o. highlighted coffee tables and TV stands aimed at U.S. residential projects.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Poland home furniture market as the annual retail value (at point of sale, including VAT) of new movable furnishings designed for residential living, dining, bedroom, kitchen, bathroom, home-office, outdoor, and ancillary spaces. Items built onsite, fitted wardrobes, mattresses, décor accessories, and appliances remain outside this value pool, ensuring clean comparability across years.

Scope Exclusion: Contract-grade office suites and hospitality fixtures are expressly omitted to keep the focus on household demand.

Segmentation Overview

- By Product

- Living Room and Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers (for e.g., IKEA, Black Red White, Agata, etc.)

- Specialty Furniture Stores (including exclusive brand outlets)

- Online

- Other Distribution Channels (hypermarkets, supermarkets, teleshopping, warehouse clubs, departmental stores, etc.)

- By Geography

- Masovian (Mazowieckie)

- Silesian (Śląskie)

- Greater Poland (Wielkopolskie)

- Lower Silesian (Dolnośląskie)

- Lesser Poland (Małopolskie)

- Rest of Poland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted semi-structured interviews with Polish specialty retailers, multi-channel e-tail managers, cabinetry fabricators, and regional buying groups across Masovian, Lesser Poland, and Pomeranian voivodeships. Conversations clarified discounting cycles, premium-tier penetration, and home-office tailwinds, letting us fine-tune price ladders and validate elasticity assumptions.

Desk Research

We began by extracting macro-series from Statistics Poland on household disposable income, housing completions, and retail trade for the furniture & electronics basket; these set the demand envelope. Trade flows from UN Comtrade and Eurostat's PRODCOM showed imported share shifts that signal pricing pressure. We then reviewed insight papers from the Polish Chamber of Furniture Manufacturers, sustainability guidelines from the Ministry of Climate, and consumer sentiment trackers released by GfK. Annual reports and investor decks of listed manufacturers added cost and channel color. Select paid sources include D&B Hoovers for company revenue splits and Dow Jones Factiva for timely news-filled disclosure gaps. The sources named are illustrative; many additional references fed our evidence stack.

These open and paid feeds gave base-year benchmarks for unit deliveries, average selling prices, and material cost drifts, which we next mapped against urbanization clusters to create provisional provincial demand curves.

Market-Sizing & Forecasting

A top-down model converts national household spend potential into furniture outlays through penetration ratios tied to first-time home purchases, renovation intensity, and room-level replacement cycles; results are then corroborated with selective bottom-up roll-ups of sampled retailer sales tickets and manufacturer shipments to adjust for informal channels. Key variables include housing completions, mortgage disbursements, median furnishing ticket size, wood panel input costs, and e-commerce share gains. Forecasts employ multivariate regression, where disposable income growth and urban housing starts act as leading indicators, subsequently stress-tested under optimistic and conservative scenarios. Gap areas in retailer disclosure are bridged using patterned ASP interpolation informed by expert outreach.

Data Validation & Update Cycle

Before sign-off, outputs undergo variance checks against historical trade, production, and retail baselines; anomalies trigger re-contact with field sources. Two analysts review every calculation, and a senior reviewer performs a final sanity pass. Reports refresh each year, with rapid updates when currency swings or policy shifts materially change market math.

Why Our Poland Home Furniture Baseline Earns Trust

Published estimates rarely match because firms diverge on scope, input breadth, currency treatment, and refresh timing. By anchoring results to end-market spend and scrubbing double counts, Mordor provides a stable decision-grade figure clients can trace back to clear variables.

Key gap drivers include: some publishers fold cabinetry into building materials, others rely on production-value proxies that double count VAT, and a few freeze their models for two-year stretches, missing Poland's volatile mortgage subsidy impacts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.64 B (2025) | Mordor Intelligence | |

| USD 8.29 B (2024) | Global Consultancy A | Excludes kitchen & bathroom units; relies on limited store sample for ASPs |

| USD 11.6 B (2024) | Regional Consultancy B | Blends factory-gate output with retail sales, causing double count; updates biennially |

Taken together, the comparison underscores that Mordor's disciplined scoping, yearly refresh, and dual-lens validation deliver the most balanced, transparent baseline for Poland's home furniture opportunity.

Key Questions Answered in the Report

What is the current value of the Poland home furniture market?

The Poland home furniture market is valued at USD 12.25 billion in 2026.

How fast will the market grow through 2031?

Market revenue is projected to expand at a 5.2% CAGR, reaching USD 15.78 billion by 2031.

Which product segment generates the highest revenue?

Kitchen furniture leads with 24.70% revenue share, driven by frequent remodels and essential status in new homes.

Why is home-office furniture gaining traction?

Persistent hybrid work models fuel a 5.75% CAGR for the segment as consumers seek ergonomic, space-saving office setups.

Which region is growing the fastest?

Lesser Poland (Małopolskie) posts the highest growth at a 5.85% CAGR, helped by rising urbanization, tech-driven development, and increasing disposable incomes.

How are online channels affecting sales?

Online retail is climbing at 6.35% CAGR, aided by augmented-reality visualization tools that reduce purchase uncertainty and returns.

Page last updated on: