Abrasives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

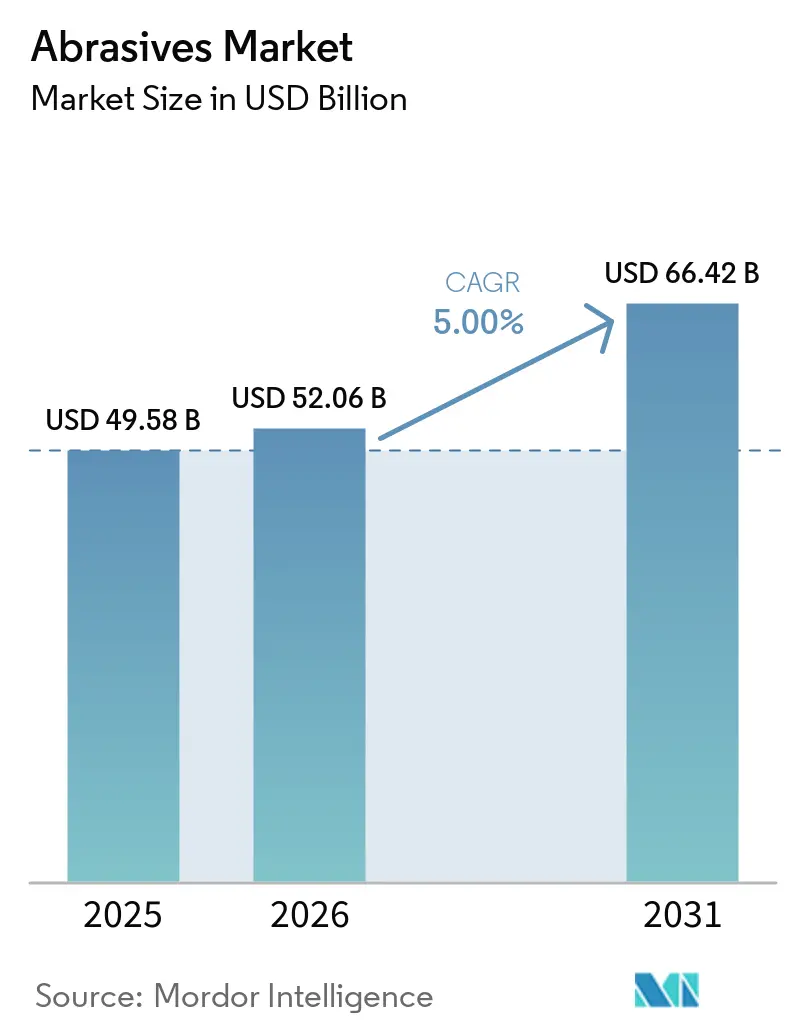

| Market Size (2026) | USD 52.06 Billion |

| Market Size (2031) | USD 66.42 Billion |

| Growth Rate (2026 - 2031) | 5.00% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Abrasives Market Analysis by Mordor Intelligence

The Abrasives Market size is expected to grow from USD 49.58 billion in 2025 to USD 52.06 billion in 2026 and is forecast to reach USD 66.42 billion by 2031 at 5.0% CAGR over 2026-2031. Sales momentum reflects rising demand for high-performance materials that can hold tight tolerances on advanced CNC equipment, especially in electric vehicle (EV) and aerospace component machining. Synthetic grades continue to capture orders because they deliver reliable hardness and thermal stability, while bonded formats remain the workhorse for high-temperature grinding. Rapid industrialization in Asia, the pivot toward precision electronics, and the emergence of post-processing needs for additive manufacturing all reinforce the growth runway for the abrasives market. Competitive rivalry is intensifying: large incumbents are refining product portfolios around eco-friendly chemistries as regulators tighten particulate and volatile-organic-compound (VOC) standards, and niche producers are carving share in specialty niches such as diamond-based super-abrasives.

Key Report Takeaways

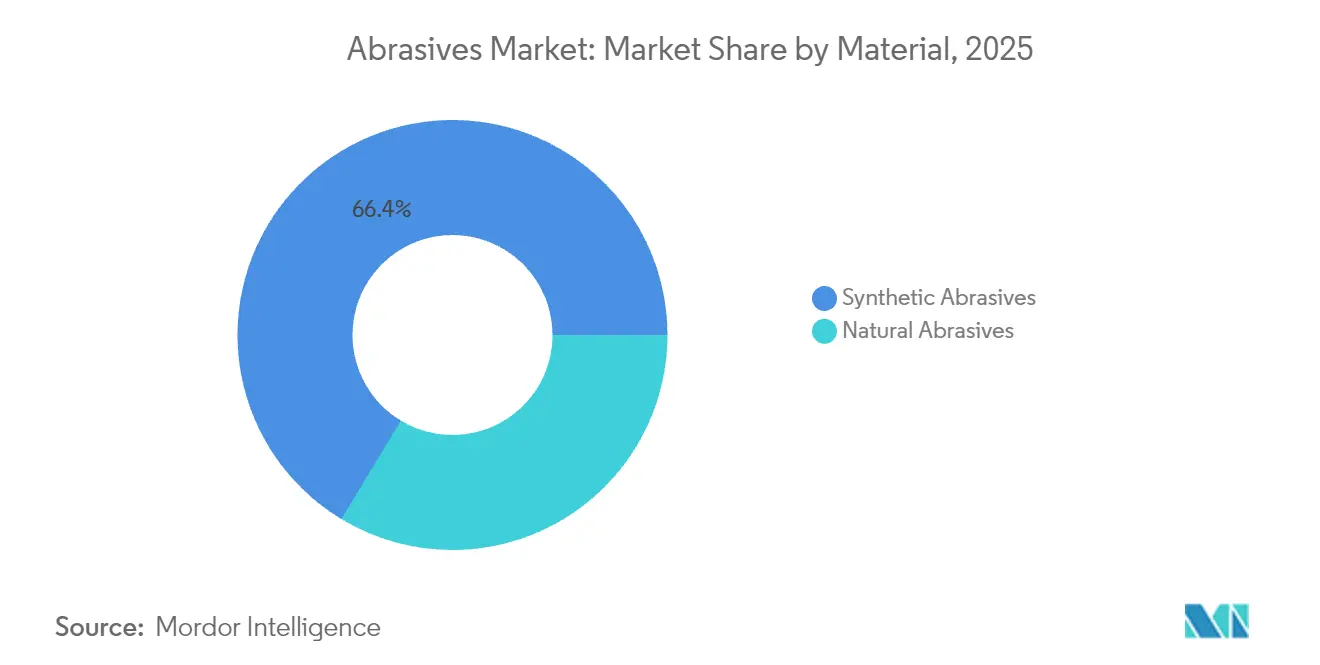

- By material, synthetic abrasives captured 66.35% of the abrasives market share in 2025, and are projected to expand at 5.74% CAGR through 2031.

- By type, bonded abrasives led with 47.55% revenue share in 2025; coated abrasives posted the fastest CAGR of 5.46% to 2031.

- By abrasive grain, aluminum oxide accounted for 39.10% of the abrasives market size in 2025; silicon carbide is projected to expand at 5.49% CAGR through 2031.

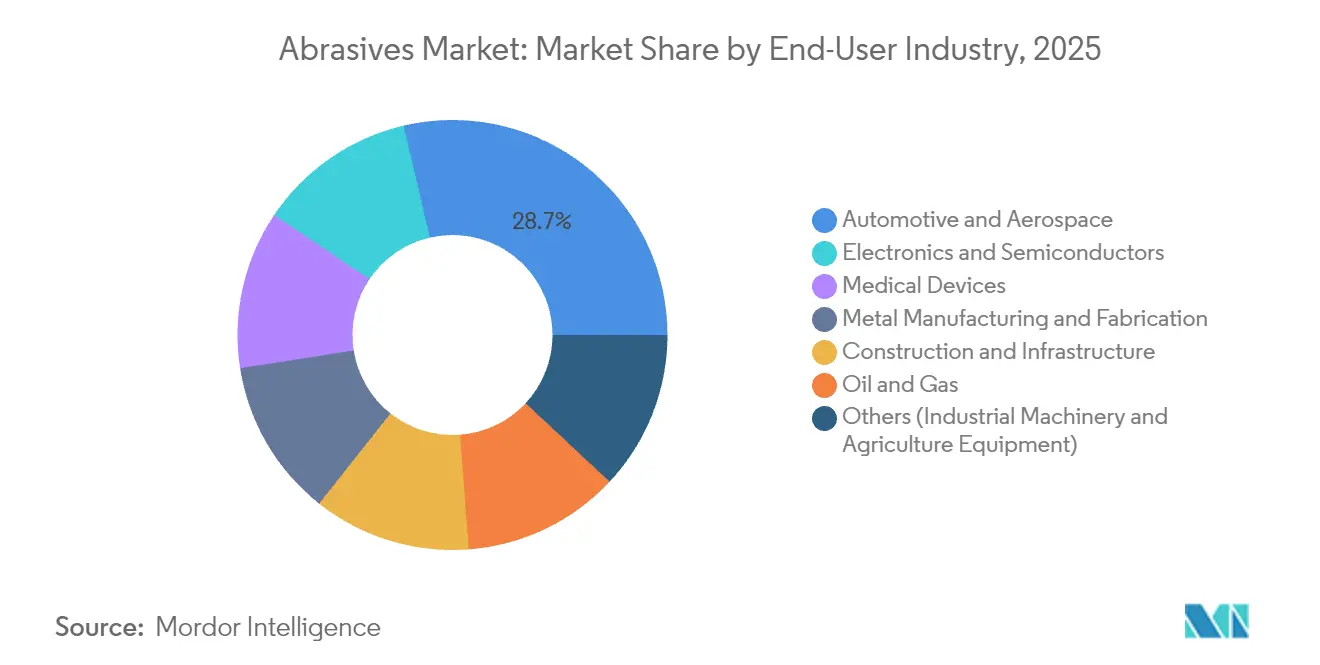

- By end-user, automotive and aerospace represented 28.65% of 2025 demand, while electronics and semiconductors are growing at 5.88% CAGR to 2031.

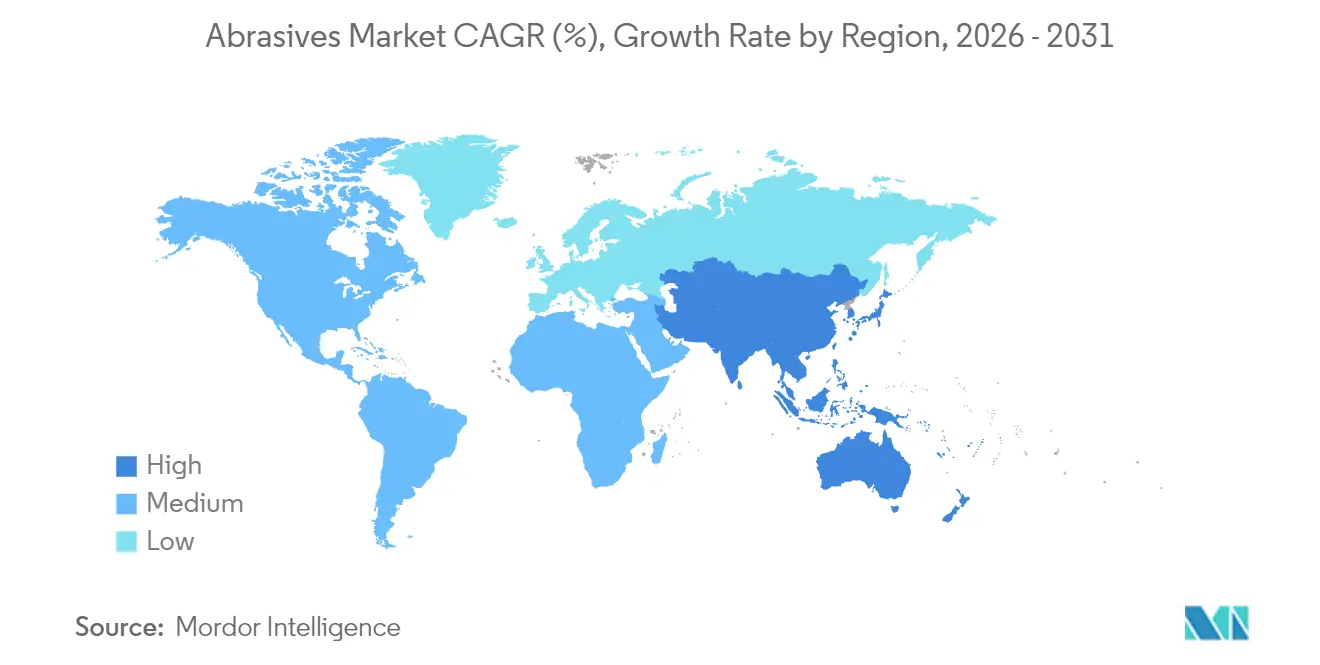

- By geography, Asia-Pacific commanded 55.40% of global revenues in 2025. and is forecast to log a 6.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Abrasives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Use in the Aerospace and Automotive Industries | +1.40% | North America, Asia | Medium term (2-4 years) |

| Growing Metal Manufacturing and Fabrication Industries | +1.20% | Asia, Europe | Short term (≤ 2 years) |

| Growing Manufacturing Activities in Emerging Economies | +0.90% | Asia-Pacific, South America | Long term (≥ 4 years) |

| Additive-Manufacturing Post-processing Requiring Super-abrasives | +0.60% | North America, Europe | Medium term (2-4 years) |

| Increased Adoption of Precision & CNC Machinery | +1.10% | Asia, North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing use in aerospace and automotive industries

Demand for advanced aircraft alloys and lightweight EV drivetrains is pushing producers to specify cubic boron nitride (CBN) and diamond wheels that maintain form at high speeds. Tier-one suppliers are optimizing E-Axle, rotor shaft, and battery-housing machining lines with vitrified CBN and ceramic media that cut cycle time and extend dresser intervals. Norton Abrasives reports measurable reductions in scrap rates when diamond tools are paired with automated load-sensing systems, illustrating why OEMs are standardizing on premium grades for repeatability. As robotics proliferate on assembly lines, the abrasives market gains from consistent surface-finish requirements that manual grinding cannot meet.

Growing metal manufacturing and fabrication industries

Steel service centers, pressure-vessel shops, and contract fabricators have upgraded grinding stations with ceramic-grain belts that increase stock removal by up to 40% while lowering power draw. Lower downtime for belt changes translates into higher overall equipment effectiveness (OEE), a metric increasingly monitored under lean programs. Specialized top-coats such as VSM TOP SIZE mitigate heat discoloration on stainless workpieces, enabling higher feed pressures without thermal distortion. These productivity gains support rapid order throughput, making high-end ceramic grades essential in cost-sensitive mass-production settings.

Growing manufacturing activities in emerging economies

China and India continue to commission new machining centers for automotive, electronics, and construction equipment, a trend that absorbs high volumes of intermediate sandpaper, cutting discs, and grinding wheels. Local subsidiaries of global players are building regional inventories and in some cases establishing fusion furnaces for aluminum oxide to reduce logistical costs. Abrasives market entrants targeting these geographies frequently bundle application engineering services to shorten learning curves for first-time CNC adopters. The presence of competitive labor costs further reinforces Asia’s status as a manufacturing hub that anchors order volumes for the abrasives market.

Additive-manufacturing post-processing requiring super-abrasives

Three-dimensional printed metal components often exit build chambers with surface roughness above 10 µm, necessitating multiple finishing passes. Cavitation abrasive surface finishing (CASF) using diamond media lowers roughness below 5 µm and induces compressive residual stress, improving fatigue performance[1]Chih-Chi Wang, “Cavitation Abrasive Surface Finishing of L-PBF Ti6Al4V,” Metals, mdpi.com . Because AM powders range from nickel super-alloys to titanium, toolmakers rely on super-abrasives that remain chemically inert at elevated temperatures. Growth prospects for the abrasives market are therefore tied to adoption rates of direct-metal laser sintering and electron-beam melting, both of which demand specialized finishing solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and Equipment Cost | -0.80% | Global | Short term (≤ 2 years) |

| Stringent Regulations on Usage of Abrasives | -0.60% | North America, Europe | Medium term (2-4 years) |

| Substitution by Alternative Materials or Methods | -0.50% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production and equipment cost

Synthetic diamond and CBN crystals are grown under pressures and temperatures that exceed geological conditions, pushing capital intensity for reactor vessels well above conventional fused-alumina lines. Single-head CNC grinders configured for diamond wheels require precision spindles and closed-loop coolant systems, raising acquisition costs. While these tools deliver longer life and lower per-part expense, small and midsize job shops in price-sensitive economies still defer upgrades. Vendors are experimenting with leasing models and consumable-credit programs, but adoption remains gated by financing constraints.

Stringent regulations on usage of abrasives

Environmental Protection Agency (EPA) standards on particulate emissions during calcining and crushing force U.S. facilities to install baghouses and scrubbers, elevating operating overhead[2]“Emission Factors for Abrasive Manufacturing,” U.S. Environmental Protection Agency, epa.gov. Worker-safety mandates on silica exposure levels within blasting enclosures are prompting transitions from slag to garnet media with lower dust profiles. European Union regulations focused on circular-economy objectives are driving recyclability targets that favor aluminum-oxide reclamation systems. Compliance costs reduce margin flexibility for suppliers and may slow new-plant approvals, moderating growth in regulated markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Synthetic abrasives support precision manufacturing

Synthetic grades commanded 66.35% share of the abrasives market in 2025, underlining user preference for consistent crystal morphology that translates into predictable wear patterns during production runs. Aluminum oxide remains the volume leader; however, silicon carbide addresses non-ferrous machining, while CBN is preferred for hardened steels. Novel nano-polycrystalline diamonds under development by Sumitomo Electric promise superior fracture toughness, positioning the abrasives market to tackle nickel-based super-alloys at lower wheel wear rates. Natural garnet retains a foothold in waterjet and blasting tasks where recyclable bulk media and low free-silica content improve site safety, making it attractive for infrastructure refurbishment projects.

The shift toward synthetic offerings aligns with automated feed systems that demand tight grit distributions, a parameter easier to achieve through engineered production routes. With Asia ramping fused-alumina capacity, supply security is improving, although power-tariff volatility can swing output costs. Manufacturers pursuing eco-labels are investing in renewable-powered arc furnaces and closed-loop water quench circuits to retain share in regulated regions. As a result, the abrasives market continues to upgrade quality benchmarks even in high-volume segments.

By Type: Bonded wheels hold leadership in heavy stock removal

Bonded wheels generated 47.55% of 2025 revenue, reflecting their role in cutting, sharpening, and surface-conditioning jobs across automotive, aerospace, and general engineering workshops. Resinoid and vitrified matrices provide thermal stability during deep-cut operations, enabling consistent tolerances on crankshafts and turbine blades where metallurgical integrity is critical. Advances in sol-gel alumina and engineered pore structures improve chip evacuation, permitting higher metal removal rates without risk of burn.

Coated abrasives, while lighter in tonnage, enjoy widespread use in finishing and deburring. Backings ranging from flexible film to fiber discs optimize performance across curved surfaces and hard-to-reach areas. Super-abrasives hold a niche position today, but their double-digit growth underpins the future direction of the abrasives market. Additive manufacturing shops specify diamond pads and CBN mandrels for thin-wall titanium parts where conventional wheels load quickly. Suppliers such as Imerys offer tailor-made fused alumina and sol-gel grains that extend dresser intervals, reinforcing bonded wheels’ dominance while bridging performance gaps with super-abrasives.

By Abrasive Grain: Aluminum oxide remains the workhorse

Aluminum oxide contributed 39.10% to the abrasives market size in 2025 thanks to its favorable cost-performance ratio and adaptability across steel and alloy substrate families. Its moderate friability promotes self-sharpening under controlled pressure, making it suitable for coarse removal and intermediate finishing. Silicon carbide supports operations on ceramics, glass, and non-ferrous alloys, ensuring sharper edges to prevent surface cracking. Ceramics and zirconia alumina, characterized by micro-fracturing behavior, unlock up to 40% higher stock removal in heavy fabrication.

Emerging demand for diamond-coated wires in wafer slicing and CBN-impregnated hone stones for engine blocks signals broader diversification of grain choice. Garnet retains specialty status in waterjet or blast cleaning under regulatory constraints on silica dust. Major players continue to refine grain morphology via seeded-gel and plasma-fusion processes that lower impurity levels, a trend strengthening premium-tier segments of the abrasives market.

By End-user Industry: Mobility and electronics dictate specifications

Automotive and aerospace consumed 28.65% of 2025 volume, driven by the push to lightweight driveline designs and ramp-up of EV component output. Rotor shafts, inverter substrates, and battery housings require tight parallelism and burr-free edges that bonded CBN wheels provide. Aerospace customers specify ceramic grain belts for nickel-based turbine alloys that operate at elevated temperatures. Metal fabrication remains a core consumer, powering growth in aluminum oxide and zirconia alumina wheels for plate beveling and structural welding prep. Semiconductor and electronics lines depend on slurries and pads for chemical-mechanical planarization (CMP), where fumed silica abrasives from Cabot deliver planar surfaces critical to nanometer-scale circuitry. Medical device machining, from hypodermic needle tips to orthopedic implants, relies on micron-level finish achievable through diamond pastes. The oil and gas value chain leans on durable cutting wheels for rig maintenance and pipeline refurbishment, confirming the diverse application reach of the abrasives market.

Geography Analysis

Asia-Pacific accounted for 55.40% of global purchases in 2025, reflecting China’s large machining base and India’s accelerated infrastructure build-out. Government incentives for domestic EV battery manufacturing and electronics assembly further stimulate local demand. Japan and South Korea leverage advanced diamond semiconductor research to create new downstream uses for super-abrasives, such as slicing large-area diamond wafers. These factors collectively sustain Asia’s leadership position and encourage multinationals to localize mixing and pressing operations.

North America retains strong momentum in aerospace, medical, and additive-manufacturing segments. Regulatory scrutiny on VOCs and particulate emissions propels shifts toward garnet blasting media and water-based coolants, generating product-mix upgrades.

Europe emphasizes sustainability and circular-economy principles, with suppliers like Saint-Gobain implementing recycled-bond systems to curtail carbon intensity. Adoption of super-abrasives is accelerating in Germany’s precision engineering clusters, while southern Europe focuses on construction-related blasting and cutting disc consumption. South America, the Middle East, and Africa remain smaller in volume yet register healthy growth as industrialization deepens; Brazil’s shipbuilding yards and Gulf petrochemical projects illustrate expanding end-user diversity. Local converting partnerships help global brands penetrate these regions, strengthening global coverage of the abrasives market.

Competitive Landscape

The abrasives market exhibits moderately fragmented concentration, with the top five suppliers controlling approximately 39% of 2024 turnover. 3M leverages a broad patent portfolio and centralized R&D hubs to release resin-bond wheels that integrate active grinding aids, improving material removal on stainless steels. The company’s global business transformation program streamlines ERP platforms to enhance customer fulfillment. Saint-Gobain is upgrading its Worcester campus with a 47,000-sq-ft administration complex scheduled for 2026, aligning manufacturing, digital labs, and customer-demo centers to accelerate product rollout.

Imerys integrates vertically into fused-alumina feedstock and specialty mineral additives, mitigating raw-material volatility and offering tailored grain blends for high-value wheels. Automation and data analytics are increasingly part of competitive arsenals; machine-learning algorithms predict wheel-life and feed-rate adjustments, reducing scrap at customer sites.

Strategic themes include eco-friendly formulations, omni-channel distribution, and strategic sourcing of renewable power. Suppliers investing in closed-loop recycling and take-back programs are well positioned to fulfill customer sustainability commitments. The abrasives industry thus balances cost, performance, and environmental credentials as critical buying criteria.

Abrasives Industry Leaders

3M

CUMI

Robert Bosch GmbH

Saint-Gobain

Tyrolit – Schleifmittelwerke Swarovski AG & Co KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Saint-Gobain has commenced the construction of a 47,000-square-foot administration building at its flagship abrasives manufacturing campus in Worcester, Massachusetts, United States. The facility is expected to become operational in January 2026.

- March 2024: Saint-Gobain Abrasives has launched RazorStar, an innovative breakthrough in abrasive technology. RazorStar incorporates precision-engineered, shaped ceramic grains. This advancement redefines performance standards and strengthens the company's competitive edge in the abrasives market.

Global Abrasives Market Report Scope

Abrasives are materials or substances that wear away or remove material from surfaces through friction or rubbing. Commonly found in forms like powders, pastes, and solid blocks, abrasives shape and clean or polish surfaces. Their applications span across the metal manufacturing, electronics, automotive, and aerospace industries.

The abrasives market is segmented by material, type, end-user industry, and geography. By material, the market is segmented into natural abrasives and synthetic abrasives. By type, the market is segmented into bonded abrasives, coated abrasives, and super abrasives. By end-user industry, the market is segmented into metal manufacturing, electronics, construction, automotive and aerospace, medical, oil and gas, and other end-user industries. The report also covers the market sizes and forecasts for the global abrasives market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Natural Abrasives |

| Synthetic Abrasives |

| Bonded Abrasives |

| Coated Abrasives |

| Super Abrasives |

| Aluminum Oxide |

| Silicon Carbide |

| Ceramic and Zirconia Alumina |

| Others (Including Garnet) |

| Metal Manufacturing and Fabrication |

| Automotive and Aerospace |

| Electronics and Semiconductors |

| Construction and Infrastructure |

| Medical Devices |

| Oil and Gas |

| Others (Industrial Machinery and Agriculture Equipment) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material | Natural Abrasives | |

| Synthetic Abrasives | ||

| By Type | Bonded Abrasives | |

| Coated Abrasives | ||

| Super Abrasives | ||

| By Abrasive Grain/Raw Material | Aluminum Oxide | |

| Silicon Carbide | ||

| Ceramic and Zirconia Alumina | ||

| Others (Including Garnet) | ||

| By End-user Industry | Metal Manufacturing and Fabrication | |

| Automotive and Aerospace | ||

| Electronics and Semiconductors | ||

| Construction and Infrastructure | ||

| Medical Devices | ||

| Oil and Gas | ||

| Others (Industrial Machinery and Agriculture Equipment) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the abrasives market?

The abrasives market is valued at USD 52.06 billion in 2026 and is expected to reach USD 66.42 billion by 2031.

Which region dominates the abrasives market?

Asia leads with 55.40% of global revenue in 2025, supported by large-scale manufacturing in China, India, Japan, and South Korea.

Which abrasive type holds the largest market share?

Bonded abrasives accounted for 47.55% of 2025 sales due to their versatility in heavy grinding and cutting applications.

Why are synthetic abrasives preferred over natural alternatives?

Synthetic grades offer consistent hardness, thermal stability, and predictable wear, enabling tighter process control in precision machining.

How do environmental regulations affect the abrasives market?

Stringent emission and dust-exposure rules increase compliance costs and accelerate the shift toward eco-friendly media such as garnet and recycled-bond wheels.

Page last updated on: