High Purity Quartz Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

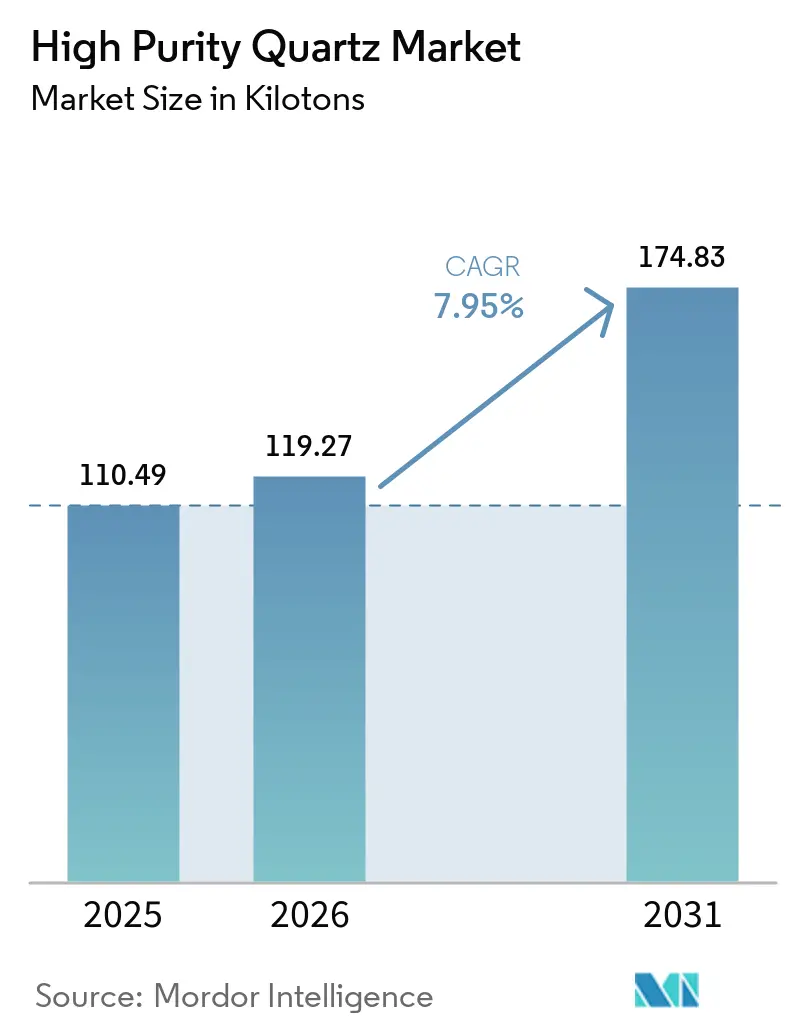

| Market Volume (2026) | 119.27 kilotons |

| Market Volume (2031) | 174.83 kilotons |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Purity Quartz Market Analysis by Mordor Intelligence

High Purity Quartz Market size in 2026 is estimated at 119.27 kilotons, growing from 2025 value of 110.49 kilotons with 2031 projections showing 174.83 kilotons, growing at 7.95% CAGR over 2026-2031. Demand accelerates as semiconductor device makers tighten contamination limits, solar ingot pullers ramp larger furnace fleets, and optics specialists pursue extreme laser stability. Capacity expansions in North Carolina and emerging Chinese deposits illustrate a strategic contest between incumbent Western producers and new entrants that seek to localize feedstock. Trade-aligned governments treat the material as a strategic mineral, shaping inward investment rules and subsidizing alternative supply routes. Equipment makers emphasize consistently low alkali levels, which favors synthetic grades in regions prioritizing supply sovereignty.

Key Report Takeaways

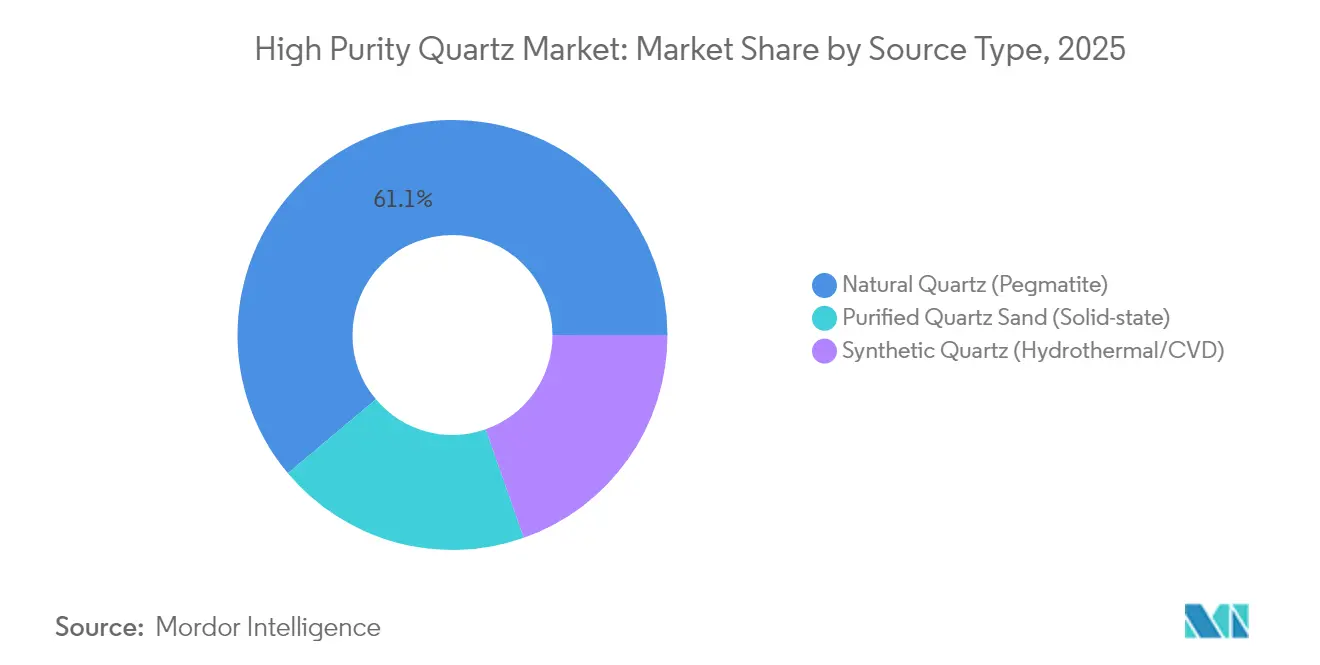

- By source type, natural quartz captured 61.12% of the high purity quartz market share in 2025; synthetic routes are projected to expand at an 8.68% CAGR to 2031.

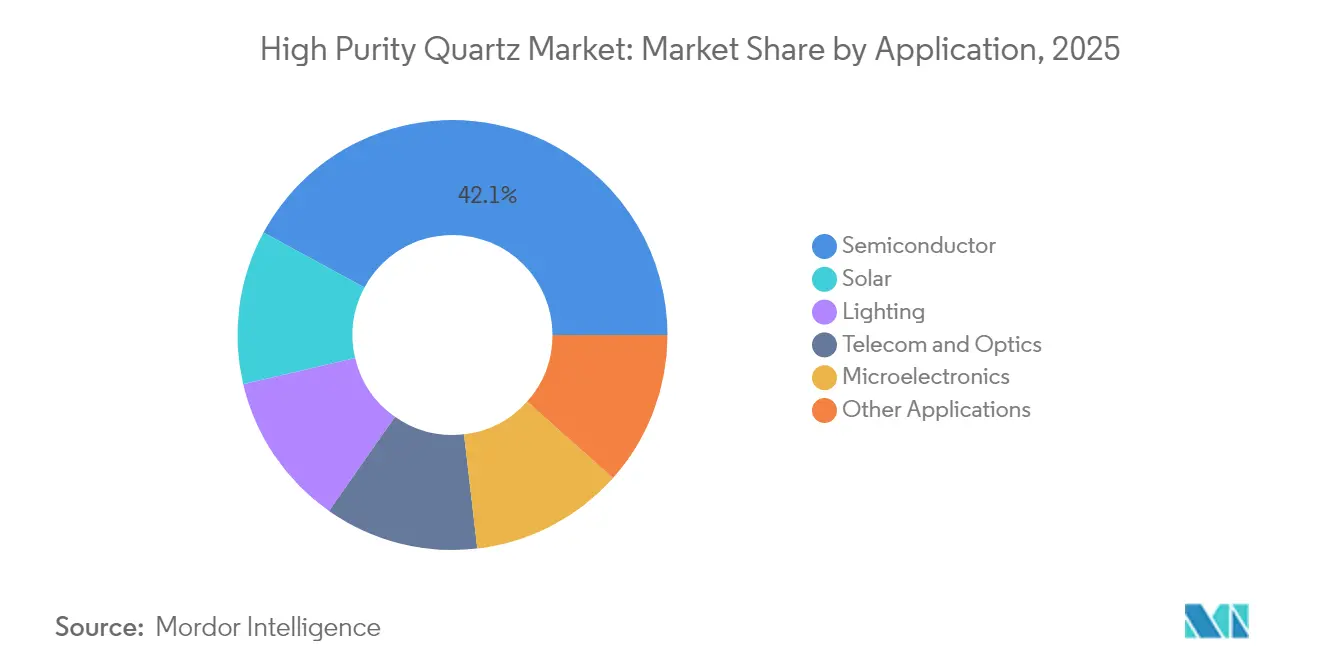

- By application, semiconductor production accounted for 42.10% share of the high purity quartz market size in 2025; solar applications will advance at a 12.15% CAGR through 2031.

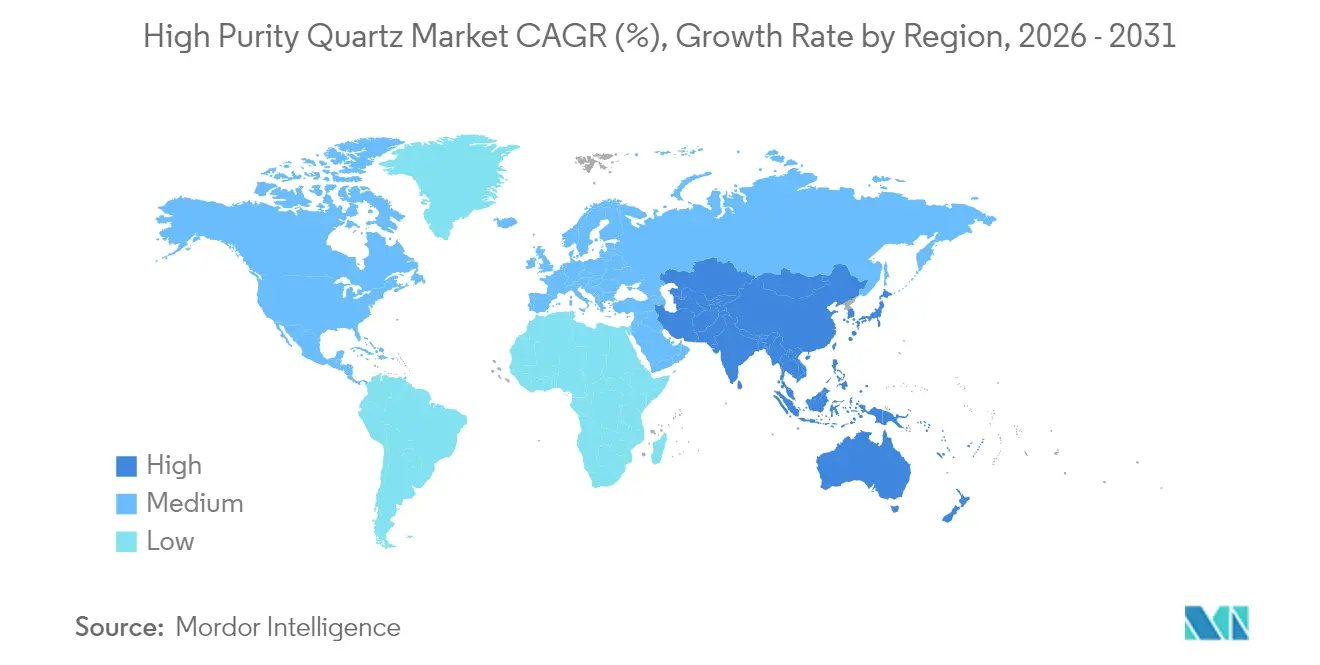

- By geography, Asia-Pacific led with 64.40% revenue share in 2025 and is expected to maintain the fastest 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Purity Quartz Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for next-gen logic and memory fabs | +2.8% | Global, concentrated in Asia-Pacific, North America | Medium term (2-4 years) |

| Rising solar-grade ingot capacity additions | +2.1% | APAC core, spill-over to Europe and Americas | Short term (≤ 2 years) |

| On-shoring of critical mineral supply chains (U.S./EU) | +1.7% | North America and EU, strategic partnerships globally | Long term (≥ 4 years) |

| Emerging ultrafast-laser optics applications | +0.9% | Global, early adoption in North America, Europe, Japan | Medium term (2-4 years) |

| Synthetic-quartz cost parity vs. natural feedstock | +0.5% | Global, manufacturing centers in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Next-Gen Logic and Memory Fabs

Global equipment outlays of USD 400 billion for new 300 mm facilities scheduled between 2025 and 2027 intensify consumption of high-purity process components, including quartz crucibles, tubes, and boats[1]SEMI, “Global Semiconductor Industry Plans to Invest $400 Billion in 300 mm Fab Equipment,” semi.org. Foundries migrating to 2 nm logic nodes must control metallic contaminants at parts-per-billion thresholds, which lifts per-wafer quartz usage. Memory makers scaling high-bandwidth modules adopt larger crystal-growth furnaces requiring crucibles with tighter thermal-shock resistance. Qualification programs at Korean and Taiwanese sites now specify 4N + purity benchmarks, prompting upstream suppliers to broaden refining capacity near Asia-Pacific fabs. In the United States, CHIPS-supported plants request dual-sourced synthetic alternatives to hedge against single-mine risk, embedding long-term offtake clauses in procurement contracts.

Rising Solar-Grade Ingot Capacity Additions

Global crystalline-silicon module demand underpins a 12.40% CAGR for solar-class quartz to 2030. Chinese and Southeast Asian producers accelerate 2600 mm diameter pullers that consume larger crucibles per cycle, increasing unit quartz loadings. European manufacturers leverage Inflation Reduction Act-style incentives to localize wafers, widening regional raw-material pull. Purity criteria remain stringent—iron below 5 ppm and total impurities under 300 ppm—driving deployment of advanced acid-leach circuits in Asian beneficiation hubs. Suppliers installing closed-loop water treatment secure faster environmental approvals, shortening time-to-market.

On-Shoring of Critical Mineral Supply Chains (U.S./EU)

The European Critical Raw Materials Act, effective May 2024, targets 40% domestic processing of strategic raw materials by 2030 and places silicon-metal inputs firmly within scope. Streamlined 15-month permitting for processing plants accelerates German and French feasibility studies for hydrothermal quartz growth. In North America, CHIPS incentives push device makers to adopt procurement scorecards that reward U.S. or allied feedstock. Australian firms position themselves as trusted partners, supported by Geoscience Australia’s mineral-systems mapping and pilot chlorination work streams. These policies extend buyer qualification windows but promise longer-term contract security once milestones are met.

Emerging Ultrafast-Laser Optics Applications

Femtosecond machining, glass interposers, and high-power ceramic lasers require synthetic quartz with absorption coefficients below 2.5 × 10⁻⁷ cm⁻¹, hydroxyl content under 20 ppm, and closely matched thermal expansion. Specialty grades attract premiums exceeding 4 × semiconductor bulk pricing due to tight dimensional tolerances. Optics firms in Germany and Japan codevelop fused-silica substrates that embed low-k interconnects for next-wave photonic ICs. Volumes remain niche, but margins encourage new entrants that master autoclave scale-up while maintaining dislocation-free crystals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile pegmatite mining output and price swings | -1.4% | Global, concentrated in traditional mining regions | Short term (≤ 2 years) |

| Stringent environmental licensing in APAC mines | -0.8% | APAC core, regulatory spillover effects globally | Medium term (2-4 years) |

| Slow qualification cycles for new HPQ vendors | -0.6% | Global, particularly affecting emerging suppliers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Pegmatite Mining Output and Price Swings

In 2024, extreme price fluctuations in Chinese markets highlighted the challenges of managing a natural high purity quartz supply and inventory for downstream manufacturers. Hurricane Helene's impact on Spruce Pine operations in September 2024 exposed supply concentration risks, with Sibelco and The Quartz Corp halting operations and The Quartz Corp reporting "no visibility" on restart timelines to CNBC. The geological variability of pegmatite deposits necessitates continuous assessments and grade control, while smaller mining operations face added unpredictability from weather disruptions, equipment failures, and permitting delays. High purity quartz price volatility significantly affects semiconductor and solar manufacturers, prompting procurement teams to adopt dual-sourcing strategies and inventory buffers to mitigate supply risks.

Stringent Environmental Licensing in APAC Mines

Stringent environmental regulations in the Asia-Pacific region are driving up production costs and limiting mining expansions in high purity quartz operations. In China, policies require comprehensive environmental assessments, water treatment systems, and dust control measures, favoring large-scale operations over smaller licenses. Water usage restrictions and air quality mandates further increase capital requirements for processing facilities. Extended permitting timelines and compliance complexities push the industry toward consolidation, disadvantaging smaller regional suppliers catering to niche markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Synthetic Routes Gain Qualification Momentum

Natural quartz retained a 61.12% share of the high purity quartz market in 2025, mainly due to ingrained supply ties with crucible and tube fabricators. However, synthetic output is rising at an 8.68% CAGR, supported by hydrothermal capacity additions in Japan, South Korea, and the United States. The high purity quartz market size for synthetic grades is driven by consistent impurity profiles that slash wafer scrap rates in 2 nm process lines. Synthetic producers also meet European content rules without relying on politically exposed mining concessions, a decisive factor under the Critical Raw Materials Act.

Natural-grade suppliers concentrate on beneficiation upgrades to stave off share erosion. New magnetic-separation circuits remove mica and feldspar phases, while high-temperature chlorination units reduce alkali traces. The combination lifts achievable purity to 4N +, narrowing quality gaps with synthetic alternatives. Still, pegmatite output remains vulnerable to climatic events and shovel-ready reserve depletion, prompting downstream firms to diversify purchase contracts. The convergence of cost structures between the two routes reshapes bargaining dynamics as buyers weigh supply security against crystal-size requirements for specialty optics.

By Application: Semiconductor Dominance Meets Solar Acceleration

Semiconductor commanded 42.10% usage in 2025 and is poised to maintain leadership, underpinned by continuous migration to larger wafer formats and higher aspect-ratio devices. At the same time, solar-grade demand will post the fastest 12.15% CAGR, reflecting aggressive PV installation targets across China, India, and the European Union. The high purity quartz sand market size for solar crucibles is expected to rise, with multi-GW puller parks in Inner Mongolia and Gujarat booking multi-year supply pacts.

Lighting, telecom, and advanced optics together make up a stable mid-single-digit proportion of global volume but secure higher unit revenues. Fiber-to-the-home rollouts lift preform cane requirements, where hydroxyl control below 0.2 ppm water equivalents reduces attenuation losses. Through-glass-via substrates for chiplet architectures emerge as a premium niche. Suppliers achieving defect-free surfaces below 0.1 µm roughness win early design-in positions, reinforcing a virtuous cycle of qualification and supply stability.

Geography Analysis

Asia-Pacific accounted for 64.40% of 2025 consumption and is projected to post the highest 8.22% CAGR through 2031 as China expands polysilicon and Taiwan inches toward 2 nm logic production. Beijing’s decision in April 2025 to classify high purity quartz as a strategic mineral accelerates exploration in Qinling and Altay while steering low-interest credit to processing hubs. Japan’s materials suppliers deepen ties with domestic fabs, emphasizing synthetic routes to reduce dependence on single-mine imports. South Korea maintains a steady pull anchored by memory leadership, while Australia commercializes coastal silica projects that shorten Asian shipping lanes.

North America ranks second in usage. Spruce Pine, North Carolina, remains the world’s largest source of natural HPQ blocks, and Sibelco’s USD 200 million line upgrade will lift milling throughput by 2025. Local fabs under CHIPS funding tap regional synthetic startups that tout near-zero transportation emissions. Canada positions its Atlantic quartz veins as strategic feedstock, supported by streamlined federal permitting for critical minerals. The region’s market trajectory hinges on the pace at which U.S. fabs ramp three new 300 mm lines, a swing factor that could shift 10 kilo tons of annual demand.

Europe high purity quartz sand market benefits from supportive policy. The Critical Raw Materials Act enforces a 10% extraction and 40% processing target within the Union by 2030. France high purity quartz sand market benefits from France’s optics valley and Germany’s microelectronics parks' joint pilot hydrothermal reactors that use local geothermal heat, lowering energy intensity. Scandinavian miners evaluate value addition instead of shipping crude sand. Emerging markets in South America and the Middle East start from a low base but pursue downstream integration with PV module and glass fiber chains, promising incremental yet persistent pull on global supply.

Competitive Landscape

The high purity quartz industry is consolidated. Two Spruce Pine producers dominate natural-grade supply to semiconductor fabs, while four Asian synthetic suppliers serve a growing share of solar crucible makers. Competitive strategy shifts toward resilience. Western fabs require dual sourcing and set penalty clauses for multi-week supply interruptions. Suppliers counter with satellite stock nodes near customer parks. Technology differentiation centers on multi-zone leach reactors and dust-free bagging, which reduce metallic contamination by 35%. Environmental credentials gain weight; companies advertising closed-loop acid recovery secure easier EU permitting. Intellectual property battles intensify around hydrothermal seed-crystal technology, where patent cliffs approach in 2027. However, new policy regimes in China and the European Union limit majority foreign ownership in critical mineral assets, complicating cross-border deals.

High Purity Quartz Industry Leaders

The Quartz Corp

Sibelco

Jiangsu Pacific Quartz Co., Ltd

Momentive Technologies

Imerys

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ultra HPQ completed its Pre-Feasibility Study for the Sugarbag Hill deposit in Queensland, reporting an NPV above AUD 1 billion with capex near AUD 500 million.

- October 2024: Sibelco restarted Spruce Pine operations after post-storm repairs, progressively restoring full output to support semiconductor crucible supply chains.

Global High Purity Quartz Market Report Scope

High-purity quartz contains less than 50μg g−1 of impurities or a grade of >99.997% silicon dioxide (SiO2). It mainly includes structurally bound trace elements in the quartz lattice, micromineral inclusions, and entrapped liquid. It is a material with superior mechanical, optical, and thermal properties, which make it indispensable in the production of an extensive range of high-tech products. High-purity quartz finds applications in solar panels, silicon metal, semiconductors, and high-tech glass.

The high-purity quartz market is segmented on the basis of application and geography. By application, the market is segmented into semiconductor, solar, lighting, telecom and optics, microelectronics, and other applications. The report also covers the market size and forecasts for the high-purity quartz market in 15 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Natural Quartz (Pegmatite) |

| Synthetic Quartz (Hydrothermal/CVD) |

| Purified Quartz Sand (Solid-state) |

| Semiconductor |

| Solar |

| Lighting |

| Telecom and Optics |

| Microelectronics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source Type | Natural Quartz (Pegmatite) | |

| Synthetic Quartz (Hydrothermal/CVD) | ||

| Purified Quartz Sand (Solid-state) | ||

| By Application | Semiconductor | |

| Solar | ||

| Lighting | ||

| Telecom and Optics | ||

| Microelectronics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for global demand from 2026 to 2031?

The high purity quartz market is forecast to register an 7.95% CAGR during 2026-2031.

Which region currently consumes the largest volume?

Asia-Pacific leads consumption with 64.40% of 2025 tonnage and remains the fastest-growing region.

Why are semiconductor fabs major consumers?

Advanced logic and memory production uses large quartz crucibles and process tubes that must meet ultra-low contaminant thresholds, raising per-wafer quartz intensity.

How is synthetic quartz gaining ground?

Hydrothermal and CVD routes now reach cost parity with mined material while offering superior batch consistency, making them attractive under supply-security strategies.

What policy shifts influence supply chains?

The European Critical Raw Materials Act and U.S. CHIPS incentives both encourage local processing and sourcing, reshaping long-term purchasing patterns.

What is the market size of High Purity Quartz Market?

The High Purity Quartz Market size is estimated at 119.27 kilotons in 2026, and is expected to reach 174.83 kilotons by 2031, at a CAGR of 7.95% during the forecast period (2026-2031).

Page last updated on: