Poland Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

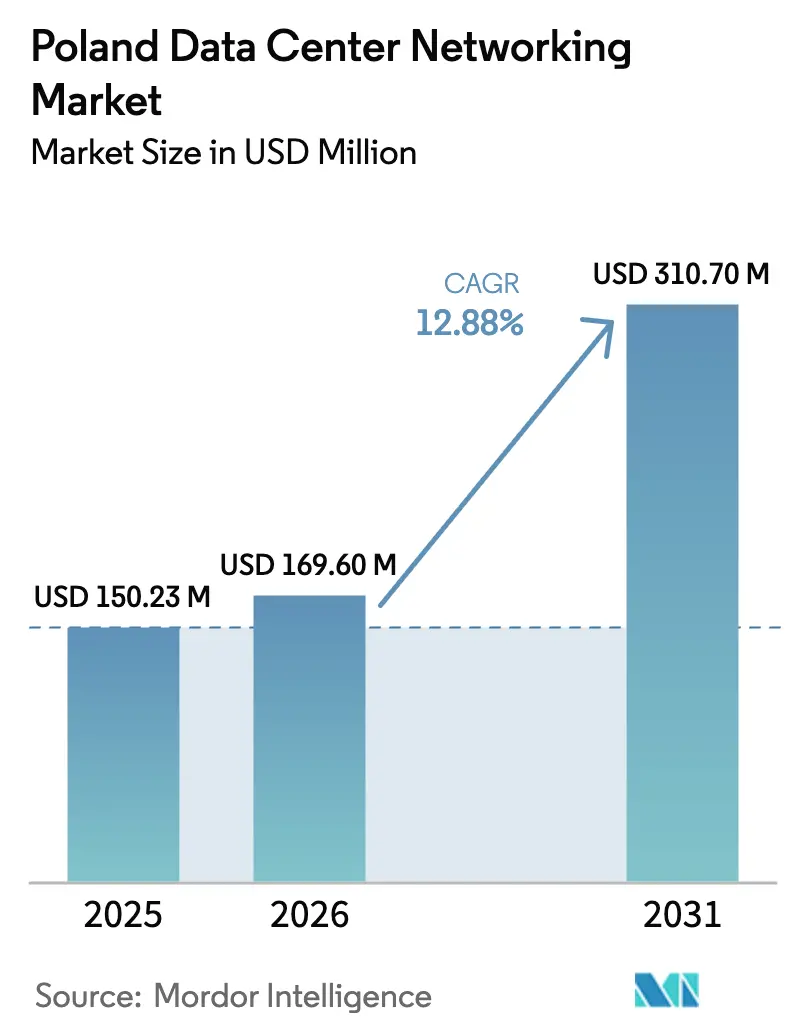

| Base Year Market Size (2025) | USD 150.23 Million |

| Market Size (2026) | USD 169.6 Million |

| Market Size (2031) | USD 310.7 Million |

| Growth Rate (2026 - 2031) | 12.88% CAGR |

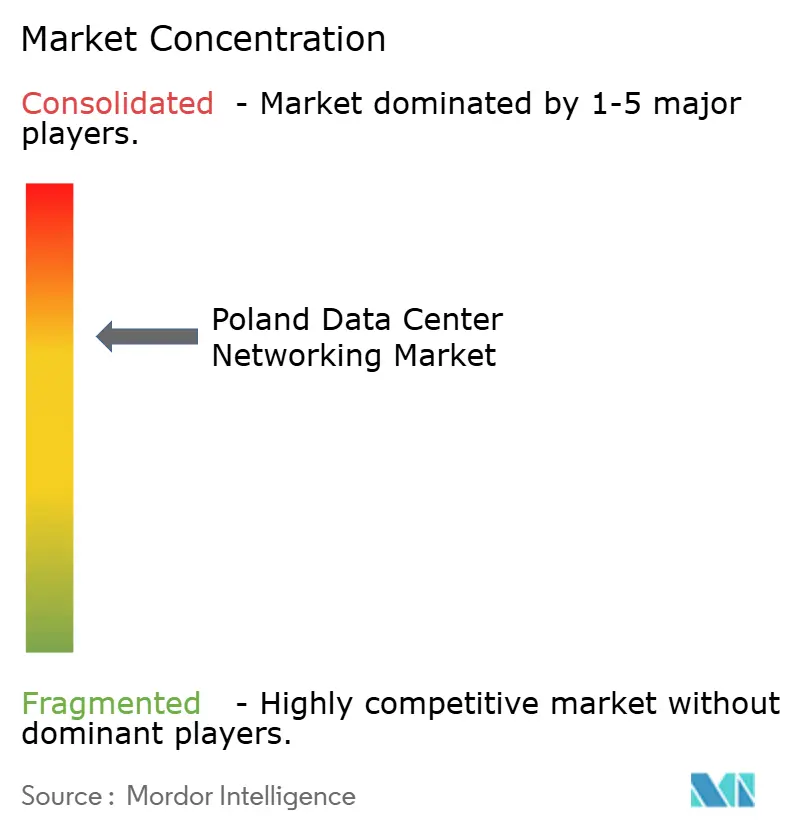

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Data Center Networking Market Analysis by Mordor Intelligence

The Poland data center networking market size is expected to grow from USD 150.23 million in 2025 to USD 169.6 million in 2026 and is forecast to reach USD 310.7 million by 2031 at 12.88% CAGR over 2026-2031. This robust outlook positions the Poland data center networking market as a pivotal node for European digital infrastructure, buoyed by hyperscale cloud commitments, accelerating AI adoption, and targeted EU funding. Microsoft’s USD 700 million hyperscale and AI deployment, slated for completion by June 2026, underscores the confidence global providers place in the country’s regulatory alignment and geographic advantage. Grid-connected capacity climbed to 174 MW in mid-2024, yet signed power purchase agreements point toward 500 MW by 2030, confirming that high-density builds are rapidly outpacing legacy capacity. Enterprises upgrading to 400/800 GbE, combined with the EU’s Recovery and Resilience Facility that earmarks 21.3% for digital transformation, funnel demand toward next-generation optical fabrics and software-defined networking. While energy tariffs remain a constraint, Poland’s cool climate and district-heating networks help lower PUE values, making the Poland data center networking market cost-competitive against Frankfurt, Amsterdam, and Dublin.

Key Report Takeaways

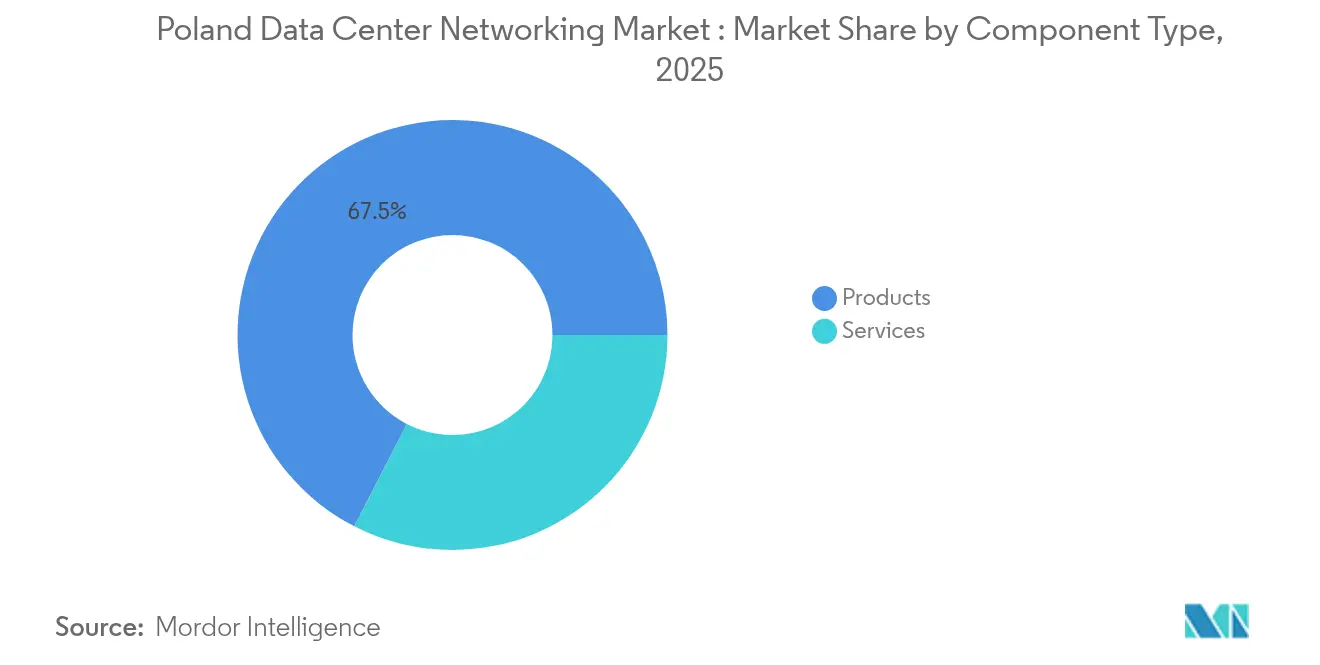

- By component, Products led with 67.45% of Poland data center networking market share in 2025; Services are projected to register the fastest 15.05% CAGR through 2031.

- By end user, IT & Telecommunications held 35.92% of Poland data center networking market size in 2025, whereas Healthcare & Life Sciences is poised for the highest 14.01% CAGR to 2031.

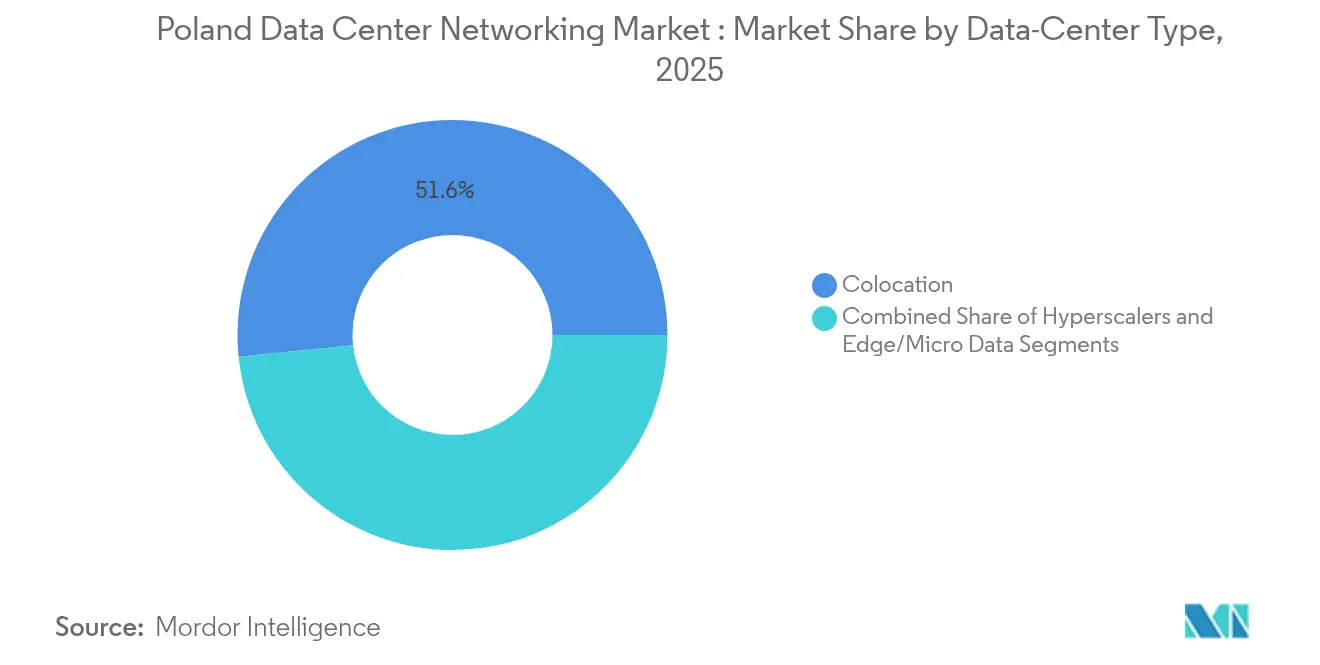

- By data-center type, Colocation facilities commanded 51.62% share of the Poland data center networking market size in 2025, while Hyperscalers & Cloud Service Providers are advancing at a 16.38% CAGR toward 2031.

- By bandwidth, 50-100 GbE configurations represented 35.88% of Poland data center networking market share in 2025; >100 GbE deployments will scale at a 15.53% CAGR as AI workloads intensify.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Understanding the full system requires moving beyond Poland boundaries into a wider international view. Mordor Intelligence captures the global data center networking market scope in its worldwide coverage.

Poland Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale and cloud expansion in Poland | +3.2% | Warsaw metro, spillover to Kraków & Poznań | Medium term (2-4 years) |

| AI-driven 400/800 GbE upgrades | +2.8% | National hubs | Short term (≤2 years) |

| EU digital-transition funds and incentives | +2.1% | Nationwide, focus on Eastern regions | Long term (≥4 years) |

| 5G-edge compute demand for local interconnect | +1.8% | Warsaw, Kraków, Gdańsk, Wrocław | Medium term (2-4 years) |

| Poland-EU low-latency disaster-recovery hubs | +1.5% | Cross-border Warsaw financial district | Long term (≥4 years) |

| On-site renewable micro-grids | +1.3% | Rural & suburban campuses | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Hyperscale and cloud expansion in Poland

Microsoft’s USD 700 million build signals the shift of hyperscale build-outs eastward, establishing anchor tenancy that spurs auxiliary investments from local providers seeking interconnection nodes. The Poland data center networking market benefits as operators accelerate purchase orders for spine-leaf fabrics, high-density optics and automated management suites. Warsaw’s proximity to key internet exchanges keeps latency within stringent EU sovereignty requirements, luring enterprise workloads migrating from saturated Frankfurt and Amsterdam racks. Domestic players such as Atman and EdgeConneX scale footprints to meet colocation overflow created when hyperscalers pre-lease entire halls. As multi-tenant facilities fill, integrators upsell managed network services that optimize ingress-egress traffic and harden security postures

AI-driven 400/800 GbE upgrades

Soaring GPU cluster sizes are overwhelming 100 GbE links, forcing immediate migrations to 400 GbE ToR switches and 800 GbE DWDM optics.[1]PacketLight Communications, “PacketLight Demonstrates 800G Transport Over ER Fiber,” packetlight.com PacketLight’s 1.6 Tbps Muxponder proof-of-concept confirms commercial viability, while NVIDIA’s Spectrum-X fabrics shrink training times by dynamically rerouting congestion hotspots. Academic HPC centers now demand east-west bandwidth rivaling hyperscale tenants, escalating purchase volumes for coherent pluggables. Channel partners capitalize on the shift by bundling telemetry software that identifies microbursts and automates queue-depth tuning. This technology leap positions the Poland data center networking market as an attractive testbed for European AI consortiums seeking sovereign compute capacity.

EU digital-transition funds & incentives

The Recovery and Resilience Facility dedicates USD 149 billion to Poland, with more than one-fifth tagged for digital projects.[2]International Trade Administration, “Poland – Country Commercial Guide,” trade.gov Subsidized fiber backbones and tax credits for green builds reduce capex hurdles for data-center operators, allowing aggressive roll-outs in regions previously deemed unviable. Regulatory certainty improves after the Electronic Communications Act harmonizes local statutes with EU frameworks, accelerating permit approvals for ducting and dark-fiber leases. Public investment in 4,200 5G base stations multiplies edge-traffic that must backhaul into regional data hubs, stimulating orders for compact aggregation switches and SR-MPLS capable routers. As funds disperse over a multi-year horizon, integrators enjoy predictable demand pipelines that justify warehouse stocking of advanced optics.

5G-edge compute demand for local interconnect

European regulators anticipate 80% of workloads processing at the edge by 2025, making proximity networking a decisive factor.[3]BEREC Office, “Report on Cloud and Edge Computing Services,” berec.europa.eu T-Mobile Polska’s metro facilities, connected via low-loss fiber rings, validate telecom-data center convergence needed for latency-sensitive AR/VR and V2X applications. Vendors such as Cisco deploy Multi-Access Edge Computing blueprints that federate micro-pods under a single APIC domain, ensuring consistent policy enforcement. Demand for compact 1RU routers with full-table SR-v6 support grows as operators interlink street-level cabinets to regional cores. The Poland data center networking market thus captures incremental revenue from mobile operators pivoting toward edge disaggregation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of advanced networking talent | -2.4% | Nationwide, acute Warsaw and Kraków | Short term (≤2 years) |

| Rising electricity tariffs and grid congestion | -1.9% | Industrial corridors, metro Warsaw | Medium term (2-4 years) |

| Lengthy fibre-route permitting | -1.2% | Cross-regional and rural builds | Long term (≥4 years) |

| Import dependence for 800 G optics | -0.8% | National supply chain | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Shortage of advanced networking talent

More than half of European operators cannot recruit enough certified engineers for 400 G and 800 G deployments. Although Poland’s business-services headcount rose 3.8% year-on-year, only 21.2% of functions are automated, highlighting persistent skill gaps. Incoming Ukrainian specialists ease pressure, yet expertise in SONiC, SD-WAN scripting, and intent-based Fabric Controllers remains limited. Salary inflation surpasses 12% among senior network architects, inflating opex for managed-service providers. Training subsidies tied to EU funds are helping upskill 380,000 professionals, but the pipeline lags immediate project roll-outs, tempering near-term growth in the Poland data center networking market.

Rising electricity tariffs and grid congestion

Coal still underpins a significant share of Poland’s generation mix, exposing data-center operators to tariff volatility that erodes margin ceilings. Grid regulators increasingly reject new megawatt requests as distribution lines saturate with photovoltaic feed-in, compelling developers to bankroll substation upgrades that delay time-to-revenue. While on-site solar plus battery installations mitigate peak charges, capex climbs in tandem, straining ROI models. The government’s 72% renewables target by 2030 and planned nuclear blocks offer relief, but will not materially lower tariffs within the next two build cycles. Consequently, some hyperscalers hedge by pre-leasing sites in the Nordics, curbing upside for the Poland data center networking market during periods of acute power scarcity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground amid Complex Upgrades

The component mix continues to tilt toward Services, forecast to grow 15.05% annually through 2031 as enterprises outsource design, deployment and lifecycle management. Services already streamline 24/7 operations, but AI-centric designs push dependency higher: orchestration tools must be tuned to react to non-deterministic east-west spikes, and micro-segmentation policies require continuous compliance audits. Installation and Integration teams now piece together 800 G transceivers, liquid-cooled switches and single-mode fiber runners inside three-phase power cages, a complexity rarely handled fully in-house. Training and Consulting revenues are propelled by Healthcare CIOs racing to conform with GDPR-aligned e-health records, while BFSI boards demand zero-trust architectures validated against EU Digital Operational Resilience Act. Support and Maintenance further expand because SLAs now stipulate five-minute fault-isolation windows, a bar impossible without remote telemetry analytics. Managed Network Services stand out: enterprises caught by the talent crunch pivot to NOC-as-a-Service contracts that bundle predictive AIOps dashboards and on-prem compliance reporting.

Products still make up 67.45% of 2025 revenue and remain indispensable as the Poland data center networking market size accompanies unavoidable silicon refreshes. Switch ASIC roadmaps deliver port-doubling every two years; thus leaf blocks purchased in 2023 cannot keep pace with 2025 GPUs hosting trillion-parameter models. High-capacity DWDM optics see brisk uptake because Poland’s backbone fibers approach fill rates. Power-aware routers that down-clock unused cores appeal to operators facing carbon-neutral pledges. Even with Services outpacing, Products’ dollar base expands as hyperscalers sign multi-year framework agreements locking in bulk discounts yet amplifying shipment volumes. Consequently, the Poland data center networking market sustains balanced growth; hardware churn funds the professional services envelope, while service engagements drive follow-on hardware cycles.

By End User: Healthcare Accelerates Digital Care Pathways

The Healthcare & Life Sciences vertical is on track for a 14.01% CAGR, the fastest in any sector. Polish hospitals deploy high-resolution tele-diagnosis, genomics analytics and robot-assisted surgery that demand deterministic latency and secure multi-site data replication. Integrators roll in redundant 400 G core spines and micro-segmented VLAN overlays to keep patient data within national borders yet universally reachable by authorized clinicians. Research centers tapping EU Horizon grants stitch GPU clusters across Kraków and Poznań, necessitating WAN fabrics with bandwidth-slicing and real-time telemetry. Thanks to these investments, the Poland data center networking market size attributed to Healthcare is projected to surpass USD 45.2 million by 2031.

IT & Telecommunications remains the largest spender, shouldering 35.92% of 2025 outlays as operators race to monetize 5G and fiber roll-outs. Edge POPs house scalable TOR pairs feeding Cloud-Native Network Functions; every base-band upgrade cascades into incremental switch and router orders. BFSI maintains strong share because Warsaw hosts many EU clearing houses whose algorithmic trading engines cannot tolerate microsecond jitter. Government & Defense invests aggressively in air-gapped networks aligned with NATO-classified traffic rulings. Meanwhile, Manufacturing lines installing machine-vision sensors integrate campus fabric extensions back to regional data hubs. Collectively, these dynamics keep the Poland data center networking industry diversified, cushioning any single-vertical downturn.

By Data-Center Type: Hyperscalers Recast Supply Chains

Colocation sites controlled 51.62% of 2025 revenue, a testament to Poland’s legacy as a disaster-recovery haven for German and Scandinavian firms. These facilities now bulk-up power halls to court AI start-ups that cannot justify proprietary builds. Conversely, Hyperscalers & Cloud Service Providers record a 16.38% CAGR, the fastest among all types. Their buying patterns prioritize leaf-spine fabrics with 800 G uplinks, open-gear BMC access and telemetry hooks for fleet-wide AIOps. Microsoft’s campus near Warsaw alone is expected to absorb thousands of 51.2 Tbps chassis switches once live, inflating short-run vendor backlogs.

Edge and Micro Data Centers, though starting from a small base, harness 5G traffic growth along Poland’s smart-port and smart-factory corridors. These units rely on low-power ARM servers and compact ToR switches supporting PTP for industrial control loops. As decentralised topologies proliferate, the Poland data center networking market adapts: vendors bundle turnkey pods including prefabricated cable harnesses, while leasing firms craft novel colocation-edge hybrids. Over the forecast horizon, hyperscalers drive volume, but colocation keeps portfolio resilience by integrating cross-connect fabrics and sovereign cloud meet-me rooms for regulated verticals.

By Bandwidth: Greater than 100 GbE Surges with AI East-West Traffic

AI clusters working on large-language models flood east-west paths, pushing operators beyond 50-100 GbE’s 35.88% deployment dominance toward greater than 100 GbE links graduating at a 15.53% CAGR. 400 GbE leaf-pairs feed 800 GbE spine fabrics, enabling non-blocking topologies for thousands of GPUs. Fiber cost economics tilt in favor of higher-speed optics because per-bit pricing falls even as module tariffs climb. Poland’s HPC Competence Centre hitting 14th worldwide in server capacity demonstrates upstream demand for terabit lanes linking compute to NVMe-oF arrays.

Legacy less than or equals to 10 GbE builds contract as support contracts lapse and OEMs cease firmware updates. 25-40 GbE remains transitional: regional universities pair them with 100 GbE uplinks to stretch budgets until EU grants finalize. The Poland data center networking market, therefore, enters a replacement super-cycle that benefits transceiver suppliers ramping 400ZR+ modules and line-card vendors shipping 51.2 Tbps ASICs. Optical component import dependence remains a risk, yet local fiber cabling plants partially offset logistics delays by pre-terminating high-fiber-count bundles onshore.

Geography Analysis

Warsaw commands roughly 39.45% of national installed capacity, totaling 142 MW online and 109 MW in pipeline builds, owing to its confluence of financial institutions, tech start-ups, and superior peering routes. Sub-1 ms latency to Frankfurt and Prague exchanges positions Warsaw as a low-latency alternative for trading workloads that cannot risk trans-Alpine fiber cuts. Power availability remains tighter than land supply, incentivising first-movers to secure grid allocations years in advance. Municipal incentives covering property-tax abatements and fast-track permits further anchor the Poland data center networking market inside the capital.

Kraków, Poznań,ń and Wrocław rise as secondary hubs, each leveraging university ecosystems that churn out STEM graduates and host regional innovation parks. T-Mobile Polska’s tri-city metro interconnect proves the viability of federated data-center meshes where latency budgets tolerate 3–5 round-trip trips. Poznań’s PIONIER backbone upgrade, co-financed by EU research funds, injects 500 next-gen routers across 21 city rings, extending enterprise IX reach and spurring colocation fills. Kraków’s historic coal infrastructure repurposed into renewable micro-grids seduces ESG-driven tenants seeking green PPAs to offset Warsaw’s fossil-heavy mix.

Eastern Poland, historically underserved, gains traction as EU digital-transition grants target gigabit broadband builds along the Lublin–Rzeszów corridor, laying groundwork for edge nodes serving cross-border low-latency links into Ukraine. Local authorities bundle land concessions with district-heating tie-ins for waste-heat reuse, trimming PUE, and aligning with EU taxonomy rules. As these regions emerge, the Poland data center networking market benefits from diversified demand, de-risking reliance on Warsaw while opening new reseller channels for mid-range switching gear.

Mordor Intelligence examines the data center networking market across diverse other regional markets as well, including Europe, Middle East, and Asia, while also offering granular country-level perspectives for Denmark, France, Saudi Arabia, Thailand, Nigeria, and Israel and more.

Competitive Landscape

Global OEMs dominate core switch and router shipments; Cisco retains the lead due to the widest product span and incumbent relationships dating back two decades. Arista chips away in AI fabrics by marketing 800 G-ready line cards bundled with latency-aware EOS software. Juniper leverages automation credentials, though its planned USD 14 billion merger with HPE faces U.S. antitrust scrutiny that, if approved, could create a powerful challenger pairing Silicon Photonics with unified compute stacks. Such consolidation prompts Polish channel partners to reassess vendor diversification, seeking to avoid single-vendor lock-in for sovereign cloud tenders.

Local integrators, including Asseco Data Systems and Comarch, capitalize on knowledge of Polish procurement law and multilingual support needs. They package foreign-made hardware with managed SOC services adapted to EU GDPR and upcoming NIS2 mandates, winning contracts in provincial hospitals and utilities. Niche optical specialists like Salumanus supply CWDM/DWDM optics tailored for Warsaw metro fiber runs, adding value through rapid RMA and localized wavelengths planning.

Sustainability steers competitive messaging: vendors now publish Scope 3 emissions and offer lifecycle carbon calculators to differentiate bids. Liquid-cool-ready switches and SmartNIC offload cards promise 20% energy savings, aligning with tenants’ RE100 pledges. Meanwhile, cloud on-ramps proliferate: Equinix Fabric and Megaport extend virtual interconnect to Microsoft Azure Warsaw region, intensifying competition among carrier-neutral facilities. Overall, the Poland data center networking market rewards players delivering open architectures, automation depth and credible green-energy roadmaps.

Poland Data Center Networking Industry Leaders

Cisco Systems

Juniper Networks

Huawei Technologies

Arista Networks

Dell Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Microsoft confirmed a USD 700 million outlay to deploy hyperscale cloud and AI infrastructure completing June 2026, the largest single tech investment in Central Europe

- January 2025: The U.S. DOJ sued to block Hewlett-Packard Enterprise’s USD 14 billion acquisition of Juniper Networks, citing competition concerns that could reverberate through Polish equipment procurement.

- December 2024: Kyndryl and Nokia deepened their collaboration, integrating Nokia’s Event-Driven Automation with Kyndryl’s AI platform to serve hybrid IT environments.

- November 2024: Poland enacted the Electronic Communications Act, aligning telecom regulation with EU directives and catalyzing fiber investment.

- October 2024: Atman opened the first building of its Warsaw-3 campus, delivering 50 kW-per-rack density and aiming for Tier III+ certification by 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Poland's data center networking market as the annual value of Ethernet switches, routers, optical interconnects, SDN controllers, and the associated support contracts installed inside colocation, hyperscale, edge, and enterprise facilities to manage east-west and north-south traffic.

Scope Exclusion: We exclude passive cabling, facility-level power or cooling systems, and any telecom backbone assets that sit outside the data-center wall.

Segmentation Overview

- By Component

- Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

- Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

- Products

- By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

- By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

- By Bandwidth

- Less Than equals to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater Than 100 GbE

Detailed Research Methodology and Data Validation

Primary Research

We spoke with network architects at Warsaw colocation campuses, regional distributors of Layer 2 and Layer 3 gear, and cloud procurement managers across Krakow and Poznan. Their insight on port-speed migration and service-level pricing helped us validate secondary findings and refine each forecast input.

Desk Research

Mordor analysts began with public datasets that include Central Statistical Office import codes, Eurostat production tables, European Commission DESI cloud-adoption scores, and bulletins from the Polish Chamber of Information Technology and Telecommunications. Trade-lane intelligence from Volza, patent filings on Questel, and news stories archived on Dow Jones Factiva deepened visibility on vendor pipelines and price shifts. Company filings, investor presentations, and operator sustainability reports supplied cost benchmarks. The sources named here are illustrative, and many additional references informed our work.

Market-Sizing & Forecasting

Our top-down model starts with installed rack count and the average number of switch ports per rack, followed by multiplication with prevailing average selling prices to size 2024 spending. Target totals are then corroborated with bottom-up rollups of sampled OEM shipments and channel checks. Five core variables (25-100 GbE penetration, hyperscaler capital outlay, rack-density progression, local cloud-workload growth, and PLN-to-USD exchange movement) feed a multivariate regression that projects values through 2030. Gaps in shipment data are bridged with midpoint estimates agreed upon during primary discussions.

Data Validation & Update Cycle

Outputs pass two layers of analyst review; variance checks prompt rapid source re-contact, and numbers are benchmarked against independent metrics before sign-off. We refresh the model every year and issue interim revisions when material events, such as new hyperscale campus announcements, occur.

Why Mordor's Poland Data Center Networking Baseline Is Dependable

Published estimates often differ because each firm applies unique scope choices, currency treatments, and update rhythms. By keeping the lens tightly on active networking hardware and refreshing yearly, Mordor removes much of that noise.

Key gap drivers include others combining servers or storage with networking, converting construction CAPEX to revenue without utilization filters, and applying undisclosed PLN-to-USD rates. In contrast, our approach reflects in-country transaction prices and clearly documented variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 150.23 M (2025) | Mordor Intelligence | - |

| USD 2.28 B (2024) | Global Consultancy A | Includes complete data-center hardware stack and uses regional allocation keys |

| USD 1.16 B (2024) | Trade Journal B | Tracks construction investment rather than equipment spend; update cadence unclear |

The comparison shows that Mordor's disciplined, transparently sourced process delivers a balanced baseline that decision makers can trust.

Key Questions Answered in the Report

What is the current value of the Poland data center networking market?

The Poland data center networking market is valued at USD 169.6 million in 2026 and is projected to reach USD 310.7 million by 2031.

Which factors contribute most to market growth?

Hyperscale cloud investments, AI-driven 400/800 GbE upgrades and EU digital-transition funding together add more than 8% to forecast CAGR.

Which component segment is expanding the fastest?

Services are growing at a 15.05% CAGR through 2031 as enterprises outsource installation, integration and managed network operations.

What bandwidth category shows the highest growth rate?

100 GbE links will scale at a 15.53% CAGR, driven by AI workloads that overwhelm legacy 50-100 GbE deployments.

Which end-user vertical is the most dynamic?

Healthcare and Life Sciences lead with a 14.01% CAGR thanks to telemedicine, genomics and AI-assisted diagnostics needing low-latency networks.

Why is Warsaw the primary data center hub in Poland?

Warsaw hosts 142 MW of operational capacity, enjoys sub-1 ms latency to major EU exchanges and attracts large cloud providers, including Microsoft’s USD 700 million build.

Page last updated on: