Market Overview

| Study Period | 2019 - 2030 |

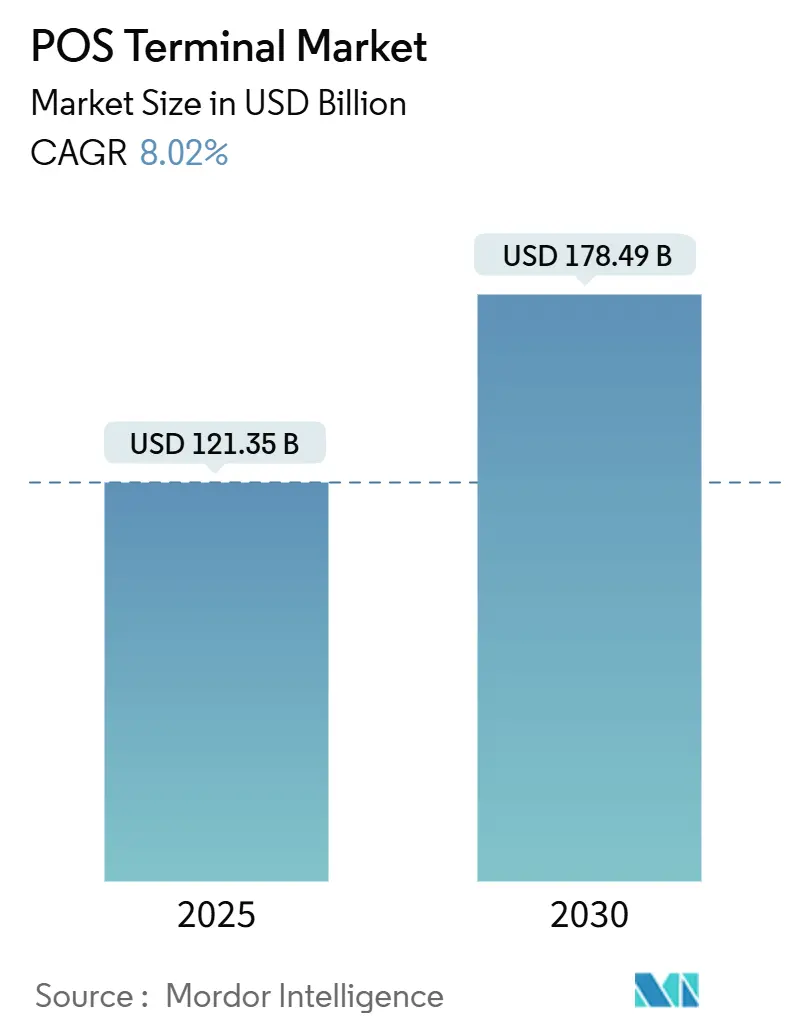

| Market Size (2025) | USD 121.35 Billion |

| Market Size (2030) | USD 178.49 Billion |

| Growth Rate (2025 - 2030) | 8.02% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

POS Terminal Market Analysis by Mordor Intelligence

The global POS terminal market is valued at USD 121.35 billion in 2025 and is forecast to reach USD 178.49 billion by 2030, advancing at an 8.02% CAGR. Growth stems from merchants replacing legacy cash registers with cloud-enabled, analytics-driven systems that blend payment acceptance with inventory, customer, and compliance management. Contactless capability, biometric authentication, and artificial intelligence are moving the POS terminal market beyond transaction handling toward real-time business intelligence. Supply-chain pressure on semiconductor components continues to constrain hardware output, but software subscriptions and hybrid deployment models are lifting adoption despite hardware bottlenecks. Vendors that can combine omnichannel payments, regulatory compliance, and low total cost of ownership are best placed to capture incremental demand across retail, hospitality, healthcare, and transportation.

Key Report Takeaways

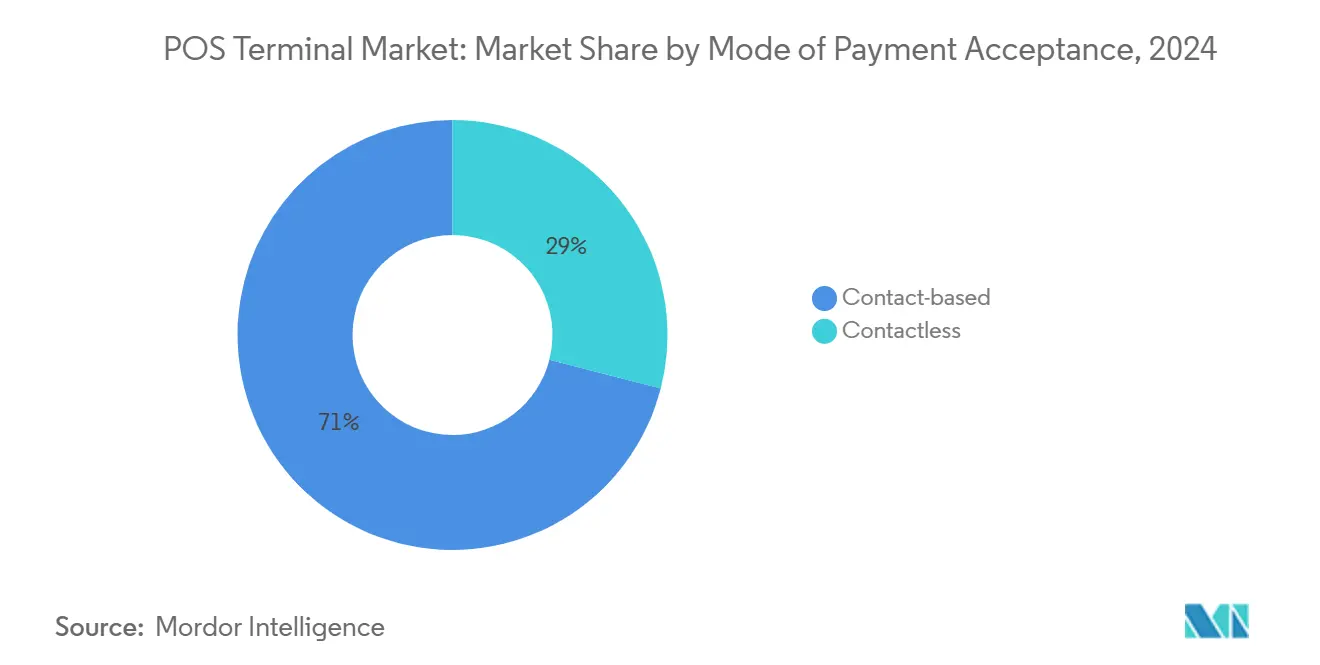

- By mode of payment, contact-based terminals held 71% of the POS terminal market share in 2024, while contactless solutions are forecast to expand at a 14.9% CAGR through 2030.

- By POS type, fixed units retained 54% of the POS terminal market size in 2024, whereas mobile and portable POS is projected to grow at 12.8% CAGR to 2030.

- By component, hardware commanded 63% revenue in 2024; software is the fastest-growing element at 11.5% CAGR over 2025-2030.

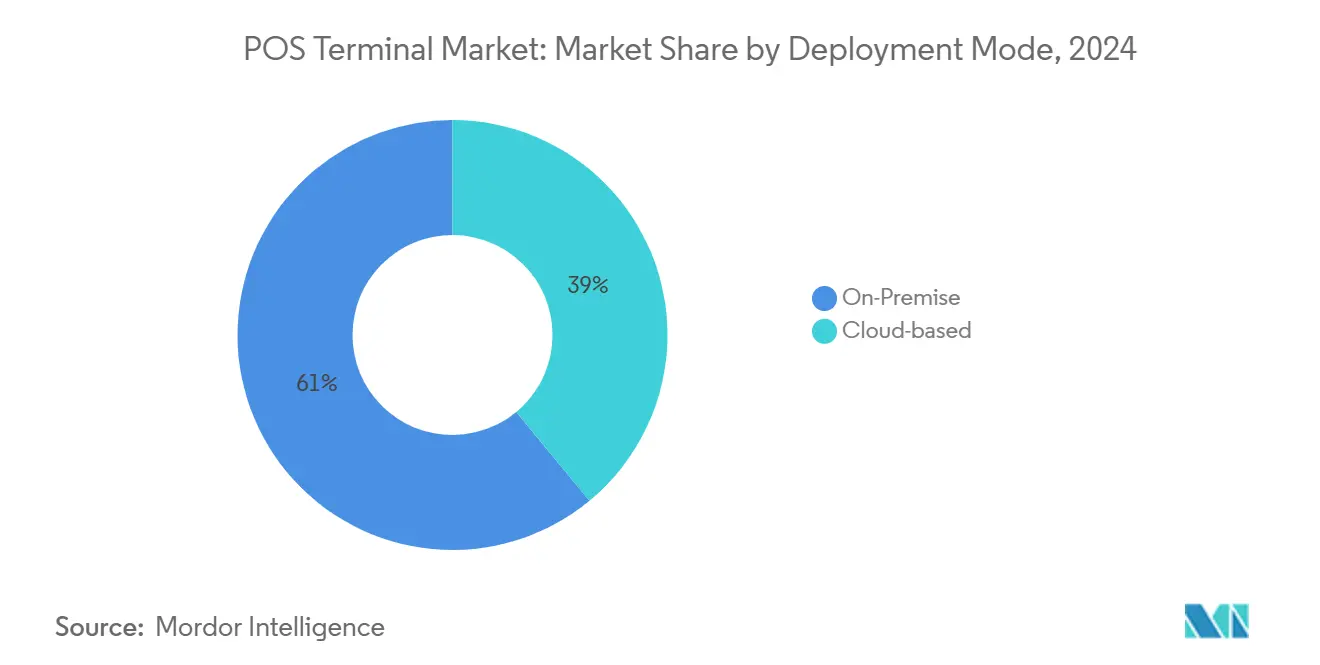

- By deployment, on-premise systems represented 61% of the POS terminal market size in 2024, while cloud platforms are set to rise at a 13.6% CAGR.

- By end-user, retail captured 35% of the POS terminal market share in 2024; healthcare leads future expansion with a 14.1% CAGR to 2030.

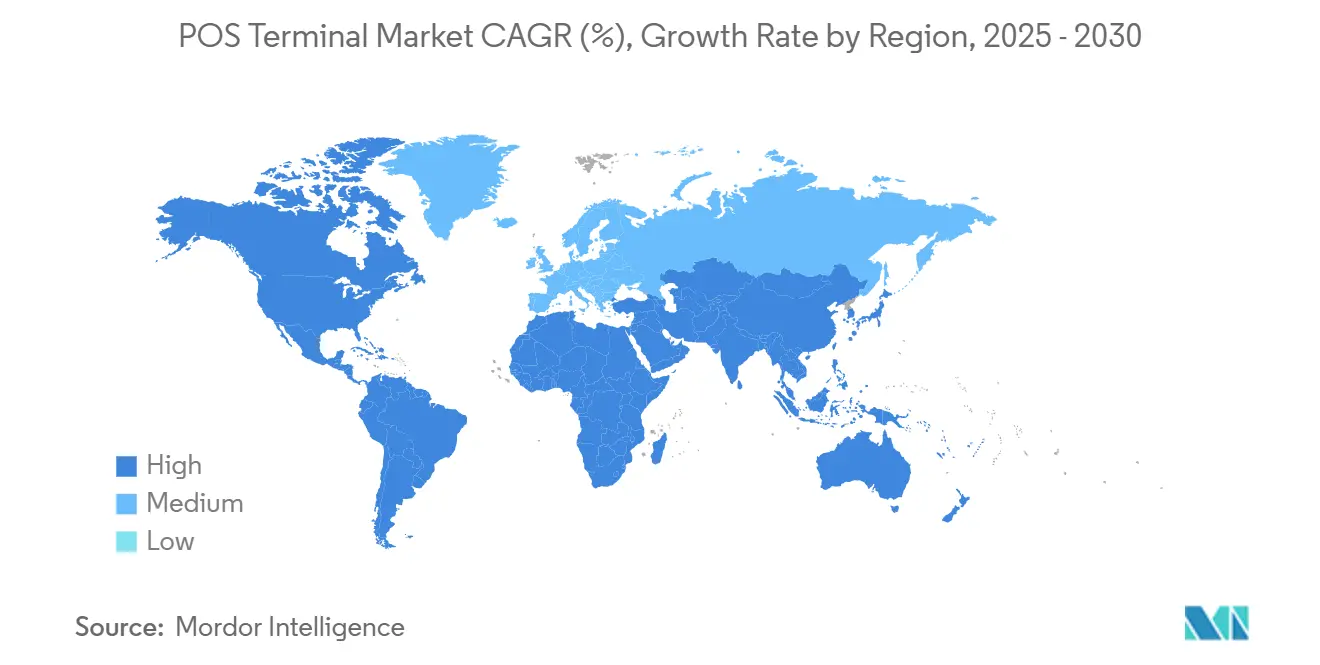

- By geography, Asia-Pacific led revenue in 2024; South America shows the quickest regional pace with a projected 10.4% CAGR through 2030.

Global POS Terminal Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption in the retail sector | 2.1% | Global, with higher impact in Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of cloud-based POS platforms | 1.8% | North America, Europe, developed APAC | Short term (≤ 2 years) |

| Accelerating demand for contactless & mobile payments | 1.6% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Integration of POS data with advanced analytics & CRM | 1.3% | North America, Europe, developed APAC | Medium term (2-4 years) |

| Regulatory push for fiscalisation & e-invoicing mandates | 0.9% | Europe, Latin America | Medium term (2-4 years) |

| "POS-as-a-Service" subscription models lowering cap-ex | 0.7% | Global, with higher impact in emerging markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Growing Adoption in the Retail Sector

Retailers now deploy unified commerce platforms that connect in-store and online transactions, generating 15-20% efficiency gains and cutting queues by 40%. [1]Shopify, “Understanding Enterprise POS Systems (2025),” shopify.com Inventory linked to the POS terminal market enables real-time stock visibility, which trims stockouts by 30% and excess inventory costs by 25%. Small merchants are bypassing legacy registers and embracing enterprise-grade cloud systems, a pattern most visible across Asia-Pacific where retail POS roll-outs outpace global averages by 1.5 times. The momentum reinforces demand for terminals that merge payment, promotion and fulfilment functions. Suppliers that tailor pricing and support to smaller retailers gain share as brick-and-mortar stores pivot toward omnichannel models.

Rising Adoption of Cloud-Based POS Platforms

Cloud solutions account for 73% of new installations in 2025, up sharply among small and mid-sized enterprises that convert capital expense to operating outflow. [2]Star Micronics, “Why Businesses Are Moving to Cloud-Based POS,” starmicronics.com Continuous software updates extend terminal life by as much as 60% compared with traditional systems and allow rapid alignment with changing fiscal rules. Hospitality operators highlight the advantage; real-time menu and table management using cloud POS typically lifts average ticket values by 12-18%. Multi-jurisdiction retailers value the ability to roll out new tax rules through a single update rather than hardware swaps. The trend accelerates penetration of the POS terminal market, where broadband quality supports always-on cloud connectivity.

Accelerating Demand for Contactless & Mobile Payments

Contactless transactions now exceed two-thirds of in-person payments worldwide, while 90% of smartphone users engage digital wallets. Eighty-three percent of retailers name NFC capability as a main reason to refresh terminals in 2025. The shift enables new layouts, including self-serve kiosks and tableside checkout, that raise floor productivity. Usage intensity differs by ticket size: convenience stores see up to 90% contactless penetration on low-value items, whereas high-value specialty purchases still rely on card-present or wallet-based verification. Suppliers that deliver configurable security tiers can match these divergent needs across the POS terminal market.

Integration of POS Data with Advanced Analytics and CRM

Sixty-five percent of enterprise retailers prioritize analytics before payment features when sourcing new systems. AI-enhanced software embedded into the POS terminal market cuts carrying costs by 20-30% and stockouts by 25-35% through predictive replenishment. Dynamic offers based on real-time basket data increase average transaction values by up to 25%. Supply-chain partners seek secure access to point-of-sale data to fine-tune production schedules, creating ancillary revenue channels for vendors that broker anonymised data feeds. Success hinges on compliance with privacy mandates and granular user-consent controls.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security & cyber-fraud concerns | -1.2% | Global, with higher impact in North America and Europe | Short term (≤ 2 years) |

| Hardware reliability & maintenance-cost issues | -0.9% | Emerging markets in Asia-Pacific, Africa, and Latin America | Medium term (2-4 years) |

| Fragmentation of regional payment standards | -0.8% | Global, with particular impact on cross-border merchants | Long term (≥ 4 years) |

| Semiconductor supply-chain volatility | -0.7% | Global, with higher impact on hardware-centric vendors | Short term (≤ 2 years) |

Source: Mordor Intelligence

Data-Security and Cyber-Fraud Concerns

A 37% rise in fraud attempts during 2024 heightens scrutiny of POS environments. Mobile POS broadens attack surfaces through wireless links, prompting annual security outlays of USD 18,000–25,000 per merchant for compliance and monitoring. Hardware refresh cycles lag evolving threats, creating gaps that require software patches, which may erode performance. Biometrics harden authentication yet introduce privacy issues that differ across regions, complicating global roll-outs within the POS terminal market.

Hardware Reliability and Maintenance-Cost Issues

Annual upkeep adds 15-20% to lifetime ownership costs, and constant use elevates failure rates 30-40% above benchmarks in busy venues. Small firms lacking IT staff endure 4-6 hours of downtime per incident, double the delay at enterprise peers. Complexity rises as printers, scanners, and sensors integrate into single units, multiplying failure points. Cloud-oriented designs with fewer moving parts lessen servicing burdens and allow remote diagnosis that mitigates this drag on the POS terminal market.

Segment Analysis

By Mode of Payment Acceptance: Contactless Surge Reshapes Infrastructure

Contact-based devices retained 71% of the POS terminal market share in 2024, but contactless solutions are scaling at a 14.9% CAGR through 2030. The POS terminal market size for contactless-enabled hardware is set to widen rapidly as 78% of 2025 deployments include NFC. Consumer preference is clear: more than 51% regularly choose tap-and-go cards or wallets, especially for purchases below USD 25. Hybrid terminals that process both chip-and-PIN and contactless help merchants manage the transition without alienating security-minded shoppers.

Wearables, mobile devices and biometric taps expand authentication options and open the door to frictionless journeys in transit, hospitality and healthcare. Fingerprint-secured contactless payments cut fraud by 60% versus standard NFC. Such capability positions vendors to cross-sell analytics subscriptions tied to tokenised identity data. As regulations tighten around strong customer authentication, contactless solutions that embed biometric checks are expected to outperform generic NFC in the POS terminal market.

By POS Type: Mobile Flexibility Drives Operational Transformation

Fixed units still account for 54% of the POS terminal market size in 2024, yet mobile systems are accelerating at 12.8% CAGR. Retail chains deploying handheld devices report 28% shorter queues and 15-20% higher associate productivity. Cellular-enabled terminals operating with integrated SIM cards guarantee connectivity even where Wi-Fi falters.

In healthcare, bedside payment devices cut billing delays by up to 35% and improve collection rates by 25%. Mobility also underpins curbside pickup and event-based commerce. Security remains an issue, with 43% of merchants flagging data protection as the top hurdle when evaluating mobile platforms, but progress in encrypted communication and device management is gradually closing the gap. Providers that lock in government-grade security protocols can unlock further growth in the POS terminal market.

By Component: Software Innovation Outpaces Hardware Growth

Hardware represented 63% of revenue in 2024, yet software is rising at 11.5% CAGR as merchants pursue richer functionality. AI modules that forecast demand reduce inventory overhead by up to 30%. Modular app marketplaces let users extend capability without swapping physical units, stretching hardware life by 40-60%.

Healthcare pharmacies illustrate software upside: a POS-integrated lighted will-call system cut wait times 35% and errors 42%. Meanwhile, biometric sensors such as miniaturised fingerprint readers strengthen transaction security, differentiating premium devices. Vendors able to orchestrate seamless hardware-software integration retain pricing power amid the commoditisation of entry-level terminals across the POS terminal market.

By Deployment Mode: Cloud Platforms Redefine Accessibility

On-premise installations still hold a 61% share in 2024, yet cloud deployments are forecast to grow 13.6% annually. Switching to subscription models trims upfront expenses by up to 70% and delivers enterprise-grade capability to SMEs. Remote dashboards let managers supervise dispersed outlets, which proved vital during recent disruptions.

Hotels cite 25-30% efficiency gains when cloud POS unifies front desk, dining, and amenities. Concerns about unstable connectivity in some markets encourage hybrid architectures that cache transactions locally and sync when networks resume. Providers aligning service-level agreements with uptime guarantees can capture cautious adopters, driving deeper penetration of the POS terminal market.

By End-User Industry: Healthcare Emerges as Growth Leader

Retail kept 35% of the POS terminal market share in 2024, but healthcare is scaling at 14.1% CAGR as hospitals integrate payments with electronic patient records. Streamlined insurance checks and compliant billing workflows drop error rates by 30-35% and lift collections by a quarter. Retailers continue to modernise omnichannel capabilities, prioritising seamless cart recovery between e-commerce and brick-and-mortar.

Restaurants apply AI-based menu optimisation, securing 8-12% margin uplifts. Transportation agencies tap mobile POS to shorten boarding, enhancing capacity utilisation. Tailored functionality rather than generic payment acceptance is becoming the main purchase criterion, prompting vendors to release vertical-specific bundles that broaden exposure across the POS terminal market.

Geography Analysis

Asia-Pacific leads the POS terminal market, propelled by government campaigns for cashless economies and a mobile-first consumer culture. China, Japan, and South Korea supply high transaction volumes, while India and Singapore climb rapidly under Digital India and Smart Nation initiatives, respectively. Regional card payments are expected to reach USD 24.7 trillion in 2025. Biometric verification adoption is rising, smoothing identity checks across densely populated cities. Yet, rural connectivity gaps and heterogeneous regulations require flexible architectures that support offline processing.

South America represents the fastest-growing region with a 10.4% CAGR forecast to 2030. Brazil drives momentum through partnerships between terminal makers and digital acquirers such as Stone and Pagseguro. Financial inclusion programmes create demand for devices that manage alternative payments, as 70% of adults remain unbanked in several countries. Fiscal e-invoicing laws across Mexico, Costa Rica, and others compel rapid hardware or software upgrades.

North America maintains scale through early adoption of contactless and AI-driven analytics. The United States alone accounted for a USD 29.11 billion POS segment in 2025. [3]Independent Banker, “Maximizing Profitability with Today’s Point-of-Sale Tech,” independentbanker.org Europe progresses under mandatory fiscalisation; Spain’s Verifactu rollout is a prominent trigger for replacements. The Middle East and Africa offer pockets of high growth where smartphone penetration and urbanisation intersect, though infrastructure limitations continue to slow rural uptake.

Competitive Landscape

The POS terminal market remains moderately concentrated around Ingenico, Verifone, and PAX Technology, yet hardware commoditisation opens space for software-led challengers. Traditional vendors now bundle Android-based tablets with curated app stores to sustain margin and relevance. Hardware sales in North America softened during 2024, but EMEA demand partly offset the decline as regulatory upgrades accelerated.

Strategic pivots show in Verifone’s emphasis on connected services that complement next-generation devices, as detailed in its SEC filings. [4]SEC, “Verifone Systems, Inc. Form 10-K,” sec.gov Niche specialists such as ZCS leverage vertical focus to process high transaction volumes across emerging markets, validating a strategy of customised service layers. Biometric innovators collaborate with card manufacturers to place fingerprint sensors in cards, hinting at a future where authentication shifts into portable form factors and sidelines traditional terminals.

Supply-chain fragility, especially around microcontrollers, favours vendors whose revenue mix leans toward platform fees over hardware margin. Software-as-a-Service pricing also lowers merchant entry barriers, strengthening installed-base expansion. Consolidation among acquirers and processors, such as Global Payments’ proposed Worldpay takeover, indicates a race to control end-to-end payment value chains and secure data streams generated across the POS terminal market.

POS Terminal Industry Leaders

-

Ingenico SA (Worldline)

-

VeriFone Systems Inc.

-

PAX Technology Ltd.

-

NCR Corporation

-

Diebold Nixdorf Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Global Payments proposed acquiring Worldpay, potentially creating the largest merchant acquirer with USD 3.5 trillion in annual payments volume, though the deal faces regulatory scrutiny and market skepticism as evidenced by a 22% drop in Global's share price following the announcement.

- April 2025: ZCS (Zhongcheng Smart) was recognized as the Top Merchant by Transaction Volume for processing over 150 million transactions in 2024, highlighting the company's growing influence in the global POS terminal market, where it serves clients in over 80 countries.

- April 2025: Barclays announced a restructuring of Barclaycard Payments in partnership with Brookfield, aiming to modernize its payment technology infrastructure to compete more effectively with fintech companies like Adyen and Stripe.

- March 2025: Fiserv acquired CCV, a European payment solutions provider, to enhance the distribution of its Clover platform across Europe, strengthening its position in the region's increasingly competitive POS market.

Global POS Terminal Market Report Scope

The POS terminal system is the time and location where a transaction is completed. A point-of-sale system is computer hardware and software that manages the marketing while selling a product or a service. It helps to store, capture, share, and report data related to sales transactions. It eases the shopping experience and helps expedite the checkout process, resulting in customer satisfaction. Inventory management, stock in hand, availability of a product, and pricing information are primary data acquired from the systems.

The point-of-sale (POS) terminal market is segmented by component (hardware, software, service), type (fixed point-of-sale terminals, mobile/portable point-of-sale terminals), end-user industry (entertainment, hospitality, healthcare, retail), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Mode of Payment Acceptance | Contact-based | |||

| Contactless | ||||

| By POS Type | Fixed Point-of-Sale Systems | |||

| Mobile / Portable Point-of-Sale Systems | ||||

| By Component | Hardware | |||

| Software | ||||

| Services | ||||

| By Deployment Mode | Cloud-based | |||

| On-Premise | ||||

| By End-User Industry | Retail | |||

| Hospitality | ||||

| Healthcare | ||||

| Transportation and Logistics | ||||

| Other End-user Industries | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Spain | ||||

| Italy | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Southeast Asia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Middle East and Africa | Middle East | GCC | ||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

By Component

| Hardware |

| Software |

| Services |

By Deployment Mode

| Cloud-based |

| On-Premise |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-user Industries |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What factors are driving the current growth of the POS terminal market?

Rapid adoption of cloud platforms, expansion of contactless payments, and mandatory fiscal compliance upgrades are lifting demand while AI-powered analytics turn terminals into business intelligence hubs.

Which region is projected to grow the fastest through 2030?

South America is forecast to lead growth at a 10.4% CAGR as Brazil, Mexico and others expand digital payment infrastructure and pursue financial inclusion.

How is the healthcare sector influencing POS terminal adoption?

Hospitals and clinics adopting integrated billing and insurance verification terminals are fueling a 14.1% CAGR, the strongest among end-user segments.

Why are merchants favoring cloud-based POS systems over on-premise setups?

Subscriptions cut upfront costs by up to 70% and enable automatic software updates that extend hardware life and simplify compliance across multiple jurisdictions.

What security challenges threaten POS terminal deployments?

Rising cyber-fraud, especially in mobile environments, forces merchants to invest heavily in encryption, biometric authentication and compliance monitoring.

How are semiconductor shortages affecting the POS terminal market?

Chip scarcity lengthens production lead times and pressures margins, prompting manufacturers to redesign hardware and merchants to prioritise suppliers with diversified sourcing.