Pneumococcal Vaccines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

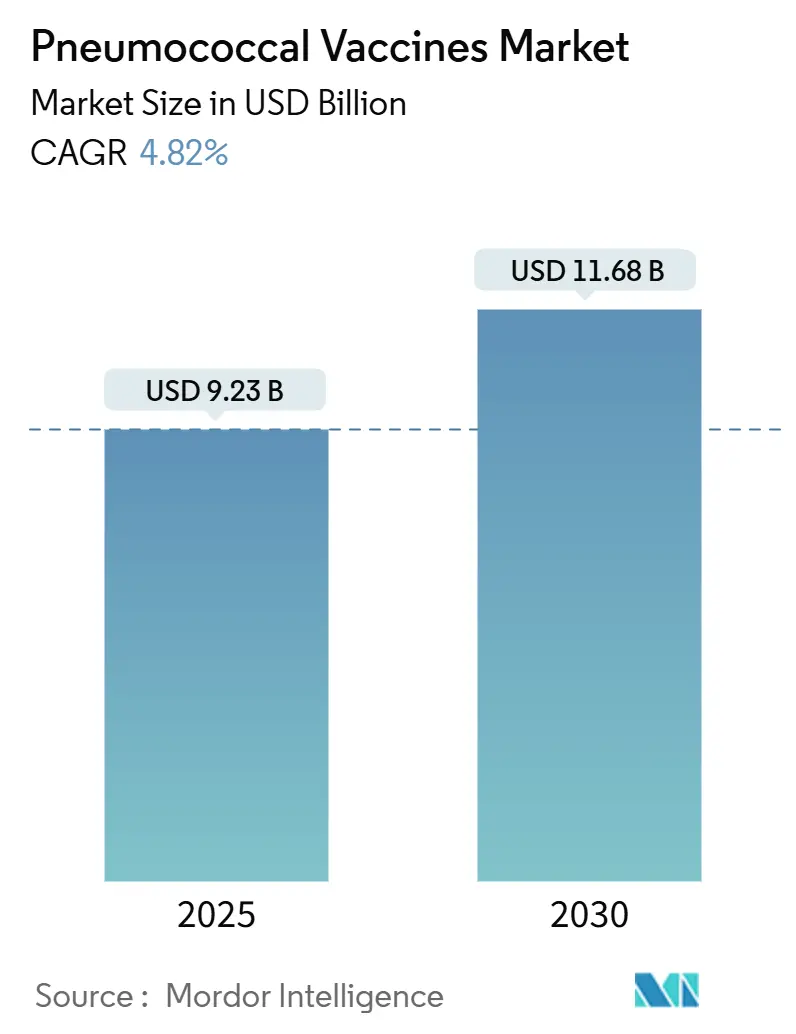

| Market Size (2025) | USD 9.23 Billion |

| Market Size (2030) | USD 11.68 Billion |

| Growth Rate (2025 - 2030) | 4.82% CAGR |

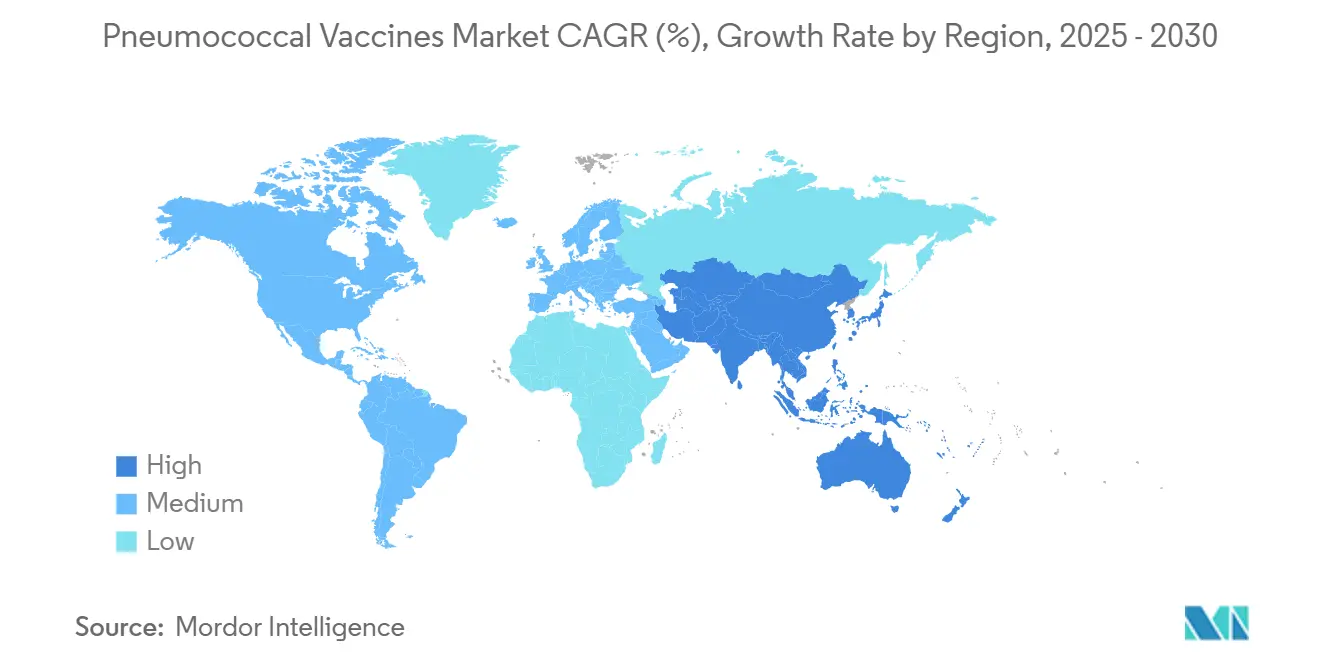

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pneumococcal Vaccines Market Analysis by Mordor Intelligence

The pneumococcal vaccines market is valued at USD 9.23 billion in 2025 and is forecast to reach USD 11.68 billion by 2030, reflecting a 4.82% CAGR. Continued shifts from 7-, 10- and 13-valent formulations toward 15-, 20- and 21-valent conjugate vaccines, broader adult vaccination guidelines, and expanded rollouts in emerging economies anchor this steady growth trajectory. North America remains the primary revenue center, yet Asia-Pacific shows the strongest momentum as domestic manufacturers scale up output and governments integrate pneumococcal conjugate vaccines into routine schedules. Intensifying competition follows Merck’s adult-specific Capvaxive launch [1]Merck & Co., “Capvaxive press release,” merck.com, the European approval of PCV21 and Vaxcyte’s well-funded 31-valent pipeline [2]Vaxcyte, "Vaxcyte Announces Pricing of $1.3 Billion Public Offering," vaxcyte.com. Meanwhile, GAVI-driven procurement, declining dose prices and evolving cold-chain technologies widen access in resource-constrained regions. The entrance of serotype-independent, protein-based candidates forms a long-term disruptive undercurrent that could reset product differentiation, manufacturing footprints and pricing strategies.

Key Report Takeaways

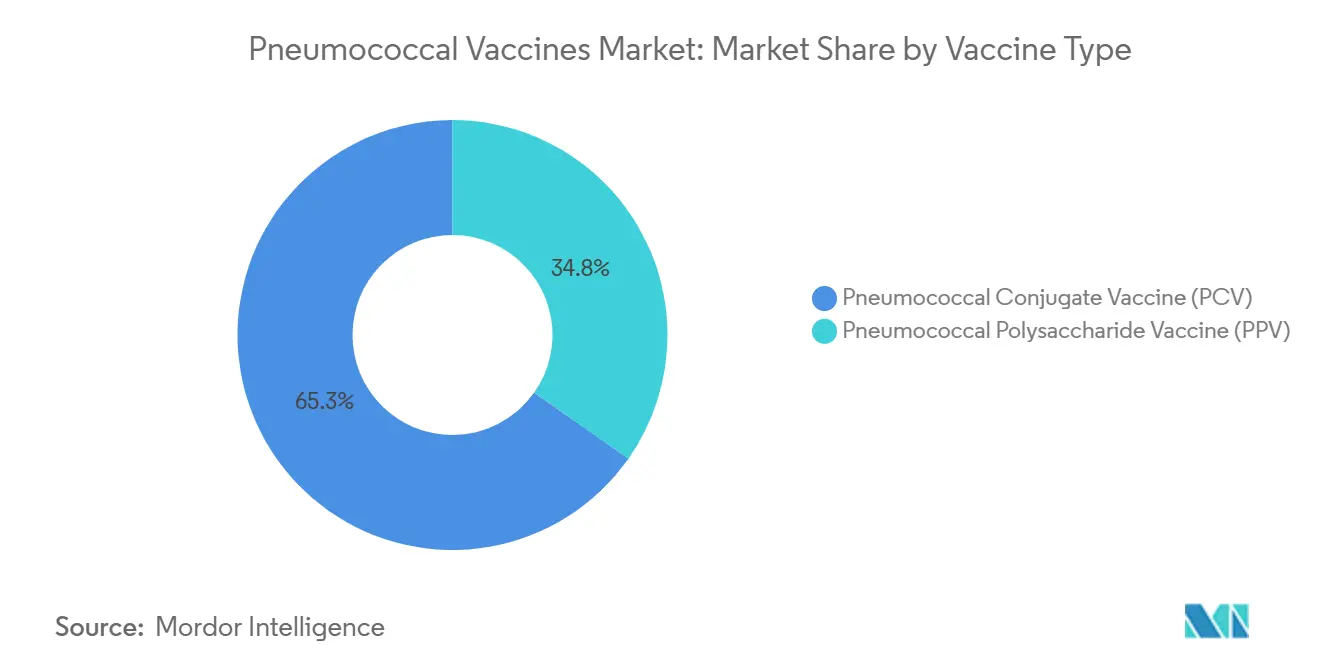

- By vaccine type, pneumococcal conjugate vaccines led with 65.25% of the pneumococcal vaccines market share in 2024; pneumococcal polysaccharide vaccines are projected to expand at a 5.25% CAGR through 2030.

- By product type, Prevnar 13 commanded 42.22% share of the pneumococcal vaccines market in 2024, while Pneumovax 23 posts the highest forecast CAGR at 5.48% to 2030.

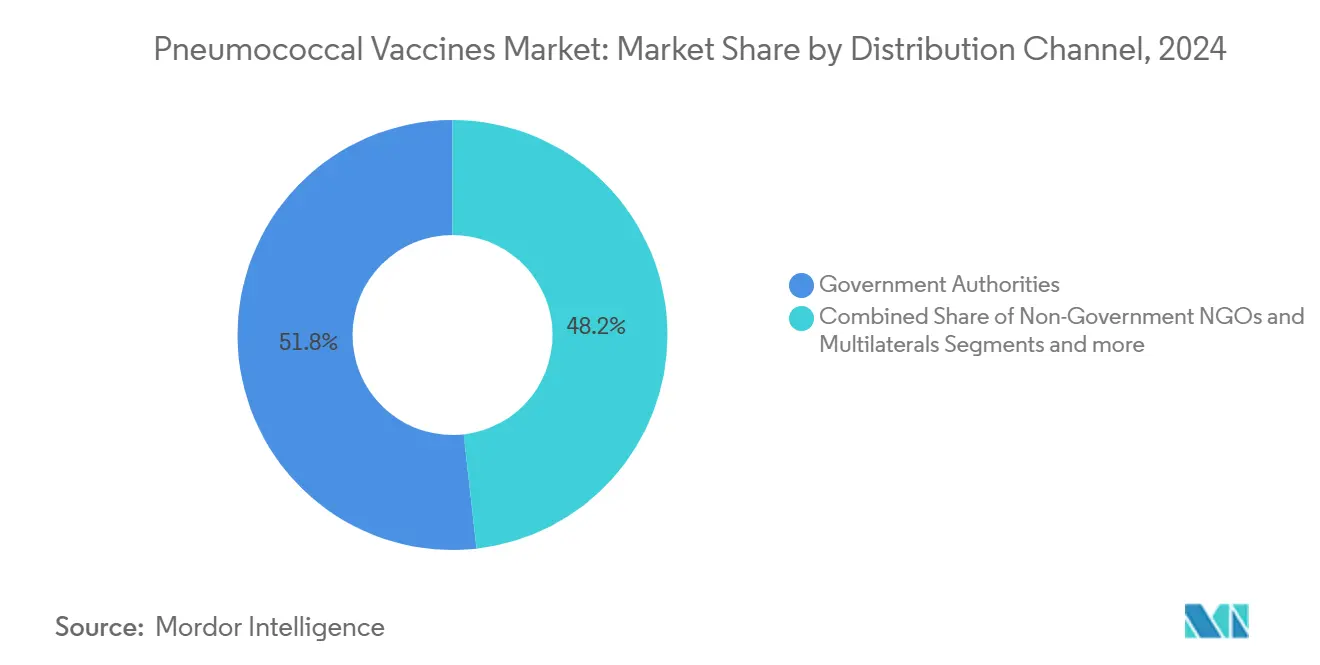

- By distribution channel, government authorities accounted for 51.78% share of the pneumococcal vaccines market size in 2024; non-government organizations and multilaterals are set to advance at a 5.55% CAGR during 2025-2030.

- By age group, adults held 53.23% share of the pneumococcal vaccines market in 2024, whereas the pediatric segment is on track for 5.45% CAGR through 2030.

- By geography, North America contributed 40.56% revenue share in 2024, with Asia-Pacific forecast to be the fastest-growing region at 5.65% CAGR to 2030.

Global Pneumococcal Vaccines Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing government awareness programs on pneumonia immunization | +0.8% | Global, with concentrated efforts in GAVI-eligible countries | Medium term (2-4 years) |

| Rising prevalence of pneumococcal infections | +0.7% | Global, particularly in aging populations of developed markets | Long term (≥ 4 years) |

| Launch of higher-valent PCVs (PCV15/20/21) | +1.2% | North America & EU initially, expanding to APAC | Short term (≤ 2 years) |

| Adult vaccination expansion to 50–64 age group (ACIP draft) | +0.9% | North America primarily, with spillover to developed markets | Medium term (2-4 years) |

| Low-cost India-made PCVs (e.g., Pneumosil) boosting GAVI uptake | +0.6% | GAVI-eligible countries, concentrated in Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Rapidly ageing global population | +0.5% | Global, with highest impact in developed economies | Long term (≥ 4 years) |

Source: Mordor Intelligence

Increasing Government Awareness Programs on Pneumonia Immunization

Large-scale campaigns transform vaccination coverage by embedding pneumococcal conjugate vaccines into national schedules and securing multiyear procurement budgets. India’s program now protects more than 90% of annual births, preventing an estimated 50,000 childhood deaths each year. Indonesia follows a similar path with 1.6 million doses financed through GAVI, underscoring the influence of public-private alliances on demand stability. The WHO Defeat Meningitis 2030 Roadmap aligns donor priorities toward at-risk displaced populations, while climate-driven disease spread compels portfolio reviews that favor thermostable presentations over traditional cold-chain-intensive formats. Persistent government advocacy, coupled with donor subsidies and tiered pricing, therefore sustains predictable order flow for producers across the pneumococcal vaccines market [3]Molly Cliff, "Strategies for controlling pneumococcal disease and outbreaks during humanitarian emergencies," Nature Medicine, nature.com.

Rising Prevalence of Pneumococcal Infections

Despite decades of immunization progress, pneumococcal pneumonia and meningitis remain leading infectious killers of children under five and older adults. Outbreaks such as Togo’s 2023 meningitis surge confirm lingering vulnerability in the Sub-Saharan meningitis belt. Adult coverage gaps are pronounced: only 13.4% of US adults aged 19-64 with chronic conditions are fully vaccinated, with state-level rates ranging from 0-34%. Hospitals in Hong Kong report less than one-third of eligible patients receiving a dose even after pneumococcal disease hospitalization. Alongside the emergence of antibiotic-resistant strains, these prevalence indicators reinforce the addressable burden underpinning growth in the pneumococcal vaccines market.

Launch of Higher-Valent PCVs (PCV15/20/21)

Next-generation conjugates deliver wider serotype coverage, directly countering replacement trends. Merck’s Capvaxive protects against strains responsible for 84% of invasive disease in adults ≥ 50 years compared with 52% for PCV20. The European Commission cleared Capvaxive in May 2025, and Singapore adopted PCV20 early, confirming rapid international uptake for broader valency products. Vaxcyte’s synthetic 31-valent candidate and Sanofi’s SK-bioscience partnership reflect a competitive race to push serotype breadth further, heightening innovation intensity in the pneumococcal vaccines market.

Adult Vaccination Expansion to the 50-64 Age Group (ACIP Draft)

Lowering the eligibility age unlocks a sizable cohort of working-age adults with elevated chronic-disease risk. The CDC’s October 2024 vote extends coverage to millions who previously waited until age 65. This recommendation rests on trials like CAPiTA, which confirmed conjugate vaccine efficacy in adults against both bacteremic and non-bacteremic pneumonia. Electronic health record-driven risk profiling already outperforms manual screening and is being embedded in primary-care workflows, reinforcing forecast uptake.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy development & regulatory timelines | -0.9% | Global, with varying intensity across regulatory jurisdictions | Long term (≥ 4 years) |

| High manufacturing cost of conjugate vaccines | -0.7% | Global, particularly impacting emerging market access | Medium term (2-4 years) |

| Serotype-replacement diminishing long-term efficacy | -0.6% | Global, with regional variations in serotype distribution | Long term (≥ 4 years) |

| Cold chain and supply chain issues | -0.4% | Emerging markets and remote regions primarily | Medium term (2-4 years) |

Source: Mordor Intelligence

Lengthy Development & Regulatory Timelines

Prevnar 20’s path to approval illustrates extended cycles: developers spent 1,434 days in testing phases and 244 days in formal review, stretching total time to 1,678 days. FDA requests for additional pediatric immunogenicity data on Vaxneuvance added further delays. As every additional serotype multiplies clinical workload, higher-valent programs face even longer and costlier pathways, which tempers near-term supply expansion in the pneumococcal vaccines market.

Serotype-Replacement Diminishing Long-Term Efficacy

England and Wales observed rapid emergence of non-vaccine serotypes between 2000-2017, undermining earlier public-health gains. Japan recorded a similar pattern in adult pneumonia cases, and UK surveillance confirmed near-complete carriage replacement within five seasons. Continuous reformulation, robust genomic surveillance and new antigen targets are therefore essential but costly countermeasures, capping long-run market CAGR.

Segment Analysis

By Vaccine Type: Conjugates Sustain Leadership While Polysaccharides Regain Momentum

Pneumococcal conjugate vaccines held 65.25% revenue share in 2024, driven by evidence of superior immune memory and the ongoing shift to higher-valent PCV15, PCV20 and PCV21. This dominant position translates into a proportional contribution to the pneumococcal vaccines market. In contrast, polysaccharide offerings attract attention for adult catch-up campaigns and cost-sensitive tenders, producing a 5.25% CAGR that outpaces the total market. Conjugate innovators continue to push valency boundaries, while polysaccharide producers emphasize scale efficiencies to maintain competitiveness. Emerging protein-based concepts that target conserved lipoproteins such as MalX and PrsA could eventually blur current categorizations by offering serotype-agnostic protection. Early animal data showing cross-serotype efficacy drives investment interest.

The pneumococcal vaccines market size for conjugate formulations is projected to climb in absolute terms even as polysaccharides accelerate. Conjugate value growth is underpinned by premium pricing, diverse tender volumes and uptake in high-income adult populations. Meanwhile, polysaccharide expansion is volume-led, with governments procuring cost-effective doses to close coverage gaps in older adults. Both approaches remain complementary, and many national guidelines recommend sequential administration of conjugate followed by polysaccharide strains to maximize serotype breadth and immune response durability.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Prevnar Franchise Faces Disruption From Next-Generation Rivals

Prevnar 13 captured 42.22% share of the pneumococcal vaccines market in 2024 thanks to long-standing clinical data, consistent supply and global regulatory recognition. Its successor, Prevnar 20, extends protection but still competes head-to-head with Merck’s Capvaxive in adults and with Synflorix in low-income pediatric segments. Pneumovax 23, although an older polysaccharide product, benefits from strong physician familiarity and a lower dose price that attracts tender wins in middle-income economies, which explains its 5.48% CAGR. The “Others” cluster—including Capvaxive and potential 24- and 31-valent entrants—adds diversity and is likely to claim incremental share post-2027.

Multiple antigen presenting system candidates and synthetic glycoconjugate pipelines position newer firms to erode incumbent dominance over time. Yet brand equity, cold-chain networks and post-marketing safety surveillance infrastructure still reinforce incumbents’ negotiating leverage during national procurements. Future competitive positioning will hinge on breadth of coverage, targeted adult or pediatric indications and total cost per fully immunized person rather than per-dose sticker price.

By Distribution Channel: Public Procurement Dominates While NGO Footprint Expands

Government authorities purchased 51.78% of global doses in 2024, validating the central role of publicly funded immunization. This channel anchors the base volume for manufacturers and underpins forecast predictability in the pneumococcal vaccines market. NGOs and multilaterals are projected to grow fastest at 5.55% CAGR as GAVI’s Pneumococcal Advance Market Commitment lowers dose prices from USD 3.50 to USD 2.00 and funds national rollouts for Burkina Faso, Mozambique and other eligible nations. The private sector, including clinics and pharmacies, retains steady mid-single-digit growth as insurers expand adult coverage benefits in high-income markets.

The pneumococcal vaccines market size for the government channel remains unmatched, yet NGOs exert outsized influence on serotype choice and supply lead times. Their pooled forecasts guide manufacturer capacity investments and push for flexible presentations that reduce logistics costs. Virtual-care platforms collaborating with donor agencies also boost coverage among immunocompromised adults who fall outside national routine programs.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Adult Expansion Opens Headroom as Pediatric Innovations Gain Pace

Adults accounted for 53.23% revenue in 2024 following expanded recommendations for individuals aged 50-64. This demographic shift creates sustained multi-dose opportunities as healthcare systems adopt risk-based reminders embedded in electronic medical records. In parallel, the pediatric segment grows fastest at 5.45% CAGR on the back of India’s and Indonesia’s universal introductions. Capvaxive’s adult-specific profile illustrates intensifying segmentation, whereas next-generation conjugates now in Phase 3 target infants with broader coverage and lower reactogenicity.

The pneumococcal vaccines market share for adult formulations should tick higher through 2027 before stabilizing, while combination vaccines and maternal immunization pilots lift pediatric volumes. Regional strain variation also drives age-tailored portfolios: serotypes 3, 22F and 33F dominate in older adults, whereas 6A, 19A and 19F remain critical for infants in Asia, prompting product differentiation.

Geography Analysis

North America contributed 40.56% revenue in 2024 and continues to benefit from insurance coverage, pharmacist vaccination authority and corporate wellness uptake. The CDC age-threshold change instantly enlarged the eligible pool, and Capvaxive’s adult-specific positioning drives brand-switching campaigns. Provincial programs in Canada align with US guidelines, and Mexico taps Pan American Health Organization revolving funds to co-finance PCV20 for adults at risk. Nevertheless, socio-economic disparities persist, with rural states recording adult coverage rates below 45%.

Asia-Pacific is projected to post a 5.65% CAGR to 2030, the fastest among all regions. India’s nationwide roll-out supplies more than 30 million doses annually, powered by domestic low-cost production under the PNEUMOSIL brand. China’s expansion of combination vaccine reimbursement, plus Singapore’s pioneering PCV20 uptake, confirm rising middle-class demand for premium conjugates. Indonesia’s 4.5 million-child target illustrates momentum among populous Association of Southeast Asian Nations (ASEAN) members. Local strain profiling influences product strategies, with region-specific serotypes like 1, 5 and 10A shaping national tenders.

Europe maintains moderate single-digit growth as the European Commission’s May 2025 approval of Capvaxive boosts adult coverage campaigns across Germany, Italy and France. Widespread surveillance capacity helps policymakers refine schedules promptly when replacement trends emerge. In the Middle East and Africa, GAVI funding remains the principal catalyst, complemented by innovative solar cold-chain projects such as South Sudan’s withstanding 40 °C daytime temperatures. Latin America leverages Brazil’s long-standing PCV10 evidence base, showing efficacy across income quartiles and informing tender renewals throughout the region.

Competitive Landscape

Competitive intensity in the pneumococcal vaccines market is moderately consolidated, with Pfizer, Merck and GSK holding entrenched share while newcomers deploy differentiated platforms. Pfizer relies on the Prevnar franchise, covering pediatric, adolescent and adult labels that generate cross-segment economies of scale. Merck leverages its Vaxneuvance pediatric footprint and the adult-exclusive Capvaxive approval to build dual-segment strength quickly. GSK capitalizes on Synflorix in low-income markets and integrates Affinivax’s MAPS technology for future high-valent launches.

Vaxcyte raised USD 1.3 billion in a September 2024 public offering, giving it USD 1.9 billion in cash to finance 31-valent clinical programs. Sanofi advanced into late-stage development through a EUR 50 million up-front collaboration with SK bioscience, reflecting appetite among diversified pharmas to re-enter the field. Patent landscapes reveal unique conjugation chemistries, synthetic oligosaccharide assembly and cell-free protein synthesis as the focal points for competitive edge. Digital-health supplements such as machine-learning serotype prediction tools and electronic health record-based eligibility algorithms in partnership with providers are emerging differentiators that reinforce brand preference and support post-licensure safety monitoring.

White-space innovation targets serotype-independent vaccines based on conserved proteins, nanoparticle carriers and messenger RNA encoding for pneumococcal antigens. If successful, such approaches could leapfrog valency escalation and ease manufacturing bottlenecks, expanding access in price-sensitive markets. Combined respiratory panels bundling pneumococcal antigens with influenza and respiratory syncytial virus components are also in exploratory phases, aiming to consolidate adult immunization visits and increase adherence.

Pneumococcal Vaccines Industry Leaders

-

Pfizer Inc.

-

CSL Ltd.

-

Serum Institute of India Pvt. Ltd.

-

GSK plc

-

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Merck received European Commission approval for CAPVAXIVE (Pneumococcal 21-valent Conjugate Vaccine) for prevention of invasive pneumococcal disease and pneumococcal pneumonia in adults, expanding the first adult-specific pneumococcal vaccine to European markets following successful US launch.

- December 2024: Sanofi initiated a Phase 3 clinical program for its 21-valent pneumococcal conjugate vaccine (PCV21) and expanded collaboration with SK bioscience, investing EUR 50 million upfront for next-generation pneumococcal vaccine development targeting both pediatric and adult populations across over 7,700 participants globally.

- December 2024: Vaxcyte dosed the first subject in its pneumococcal conjugate vaccine trial in infants, advancing its VAX-24 development program for pediatric populations while maintaining parallel adult vaccine development with VAX-31.

- October 2024: The CDC’s Advisory Committee on Immunization Practices unanimously recommended Merck’s CAPVAXIVE for pneumococcal vaccination in adults aged 50 years and older, expanding vaccination eligibility from the previous 65-year threshold and creating significant new market opportunities.

Global Pneumococcal Vaccines Market Report Scope

Pneumonia is a type of acute respiratory illness that affects the lungs, in which the alveoli are filled with pus and fluid, making breathing painful and limiting oxygen intake.

The pneumococcal vaccine market is segmented by vaccine type, product type, distribution channel, and geography. By vaccine type, the market is segmented into conjugate vaccines and polysaccharide vaccines. By product type, the market is segmented into Prevnar 13, SynflorIX, and Pneumovax2. By distribution channel, the market is segmented into distribution partner companies, non-governmental organizations, and government authorities. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. For each segment, the market size is provided in terms of value (USD).

| By Vaccine Type | Pneumococcal Conjugate Vaccine (PCV) | ||

| Pneumococcal Polysaccharide Vaccine (PPV) | |||

| By Product Type | Prevnar 13 | ||

| Synflorix | |||

| Pneumovax 23 | |||

| Others | |||

| By Distribution Channel | Government Authorities | ||

| Non-Government NGOs & Multilaterals | |||

| Distribution-partner Companies | |||

| By Age Group | Adults | ||

| Geriatric | |||

| Pediatric | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Pneumococcal Conjugate Vaccine (PCV) |

| Pneumococcal Polysaccharide Vaccine (PPV) |

| Prevnar 13 |

| Synflorix |

| Pneumovax 23 |

| Others |

| Government Authorities |

| Non-Government NGOs & Multilaterals |

| Distribution-partner Companies |

| Adults |

| Geriatric |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the pneumococcal vaccines market?

The pneumococcal vaccines market stands at USD 9.23 billion in 2025 and is projected to reach USD 11.68 billion by 2030.

Which region leads sales of pneumococcal vaccines?

North America holds the largest share at 40.56% in 2024, driven by mature immunization infrastructure and early adoption of higher-valent vaccines.

Which product type is growing fastest?

Pneumovax 23, a polysaccharide vaccine, is forecast to grow at 5.48% CAGR through 2030 as adult catch-up strategies expand.

Why are higher-valent conjugate vaccines important?

Formulations such as PCV20 and PCV21 cover more serotypes, addressing rising replacement strains and providing broader protection for adults and children.

How will lowering the adult vaccination age threshold affect demand?

Including adults aged 50-64 unlocks a new cohort and is expected to accelerate unit sales, especially in North America and other high-income markets adopting similar guidance.

What role do NGOs play in market expansion?

GAVI and other multilaterals fund procurement for low-income countries, enabling price reductions to USD 2.00 per dose and supporting the fastest growth channel at 5.55% CAGR.