Plastic Compounding Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

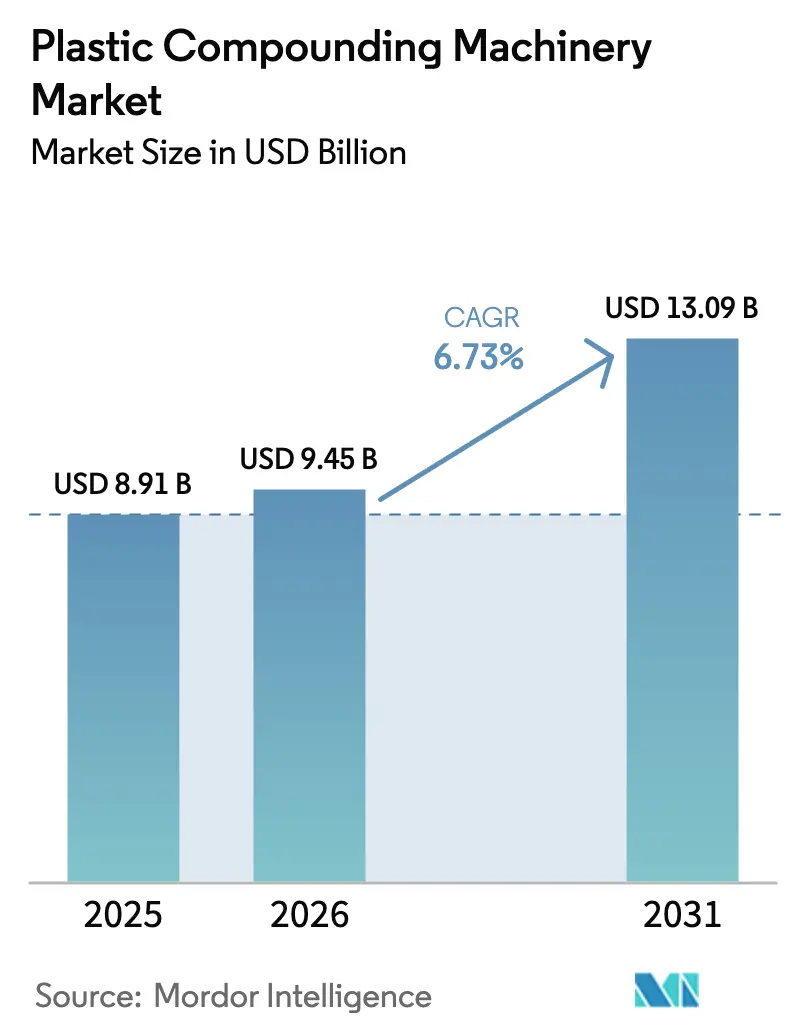

| Market Size (2026) | USD 9.45 Billion |

| Market Size (2031) | USD 13.09 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

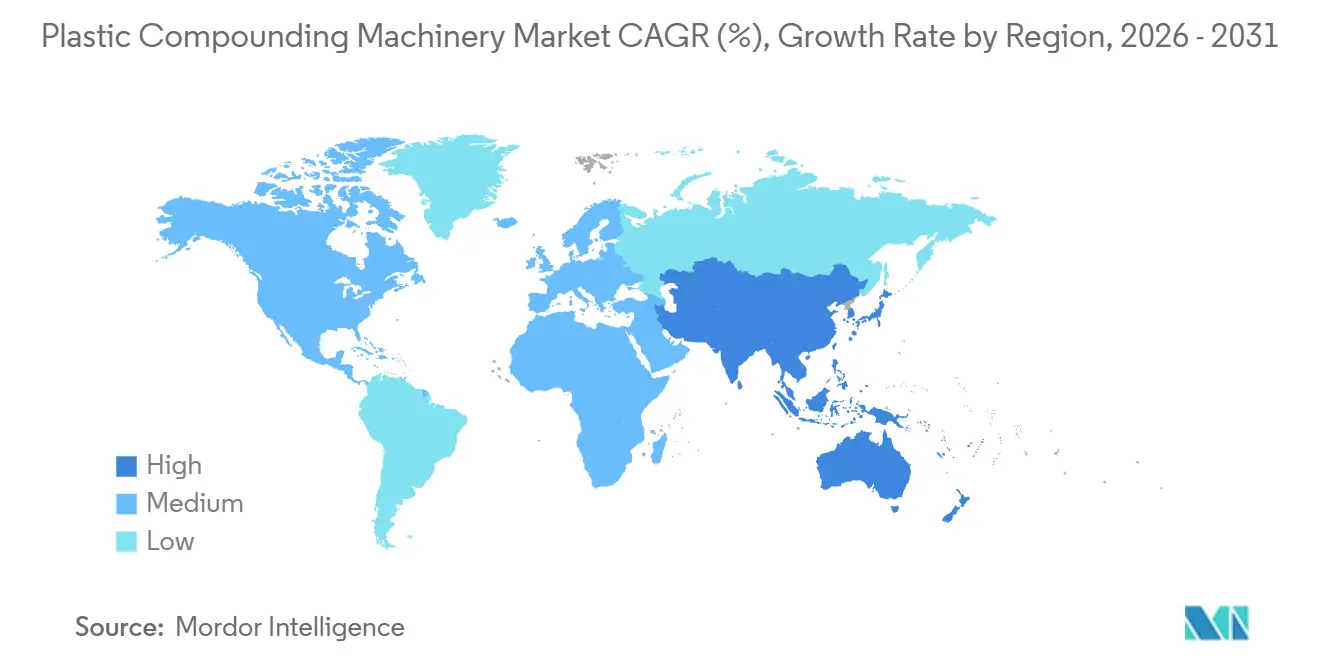

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Compounding Machinery Market Analysis by Mordor Intelligence

The plastic compounding machinery market size is expected to increase from USD 8.91 billion in 2025 to USD 9.45 billion in 2026 and reach USD 13.09 billion by 2031, growing at a CAGR of 6.73% over 2026-2031. This growth trajectory reflects stricter recycled-content mandates, rising traceability requirements for medical devices, and the spread of on-site compounding lines within electric-vehicle battery plants. Processors now prioritize modular twin-screw and planetary-roller systems that shorten changeovers, enable higher reclaimed-resin loadings, and embed cloud-connected predictive-maintenance tools. Asia-Pacific remains the volume anchor as China’s modified-plastics penetration climbs toward the global average, while Europe drives technology refreshes through aggressive packaging-waste regulations. Competitive differentiation hinges on screw-element libraries, alloy availability, and digital-twin services that help compounders validate new recipes quickly and conserve high-value additives. Key trends shaping the plastic compounding machinery market include the pivot to lightweight, recyclable packaging, the rapid uptake of medical-grade twin-screw extruders, and the commercialization of additive-manufacturing filament lines. Equipment builders able to demonstrate 15%–20% productivity gains through feed-enhancement technology or gear-pump integration are displacing legacy single-screw assets. Capital-expenditure momentum is tempered, however, by multi-million-dollar price tags, lengthy payback horizons, and supply-chain bottlenecks in specialty screw-barrel alloys. Polymer price volatility further compresses margins, prompting financially constrained converters in South America, the Middle East and Africa to defer upgrades or pursue leasing models.

Key Report Takeaways

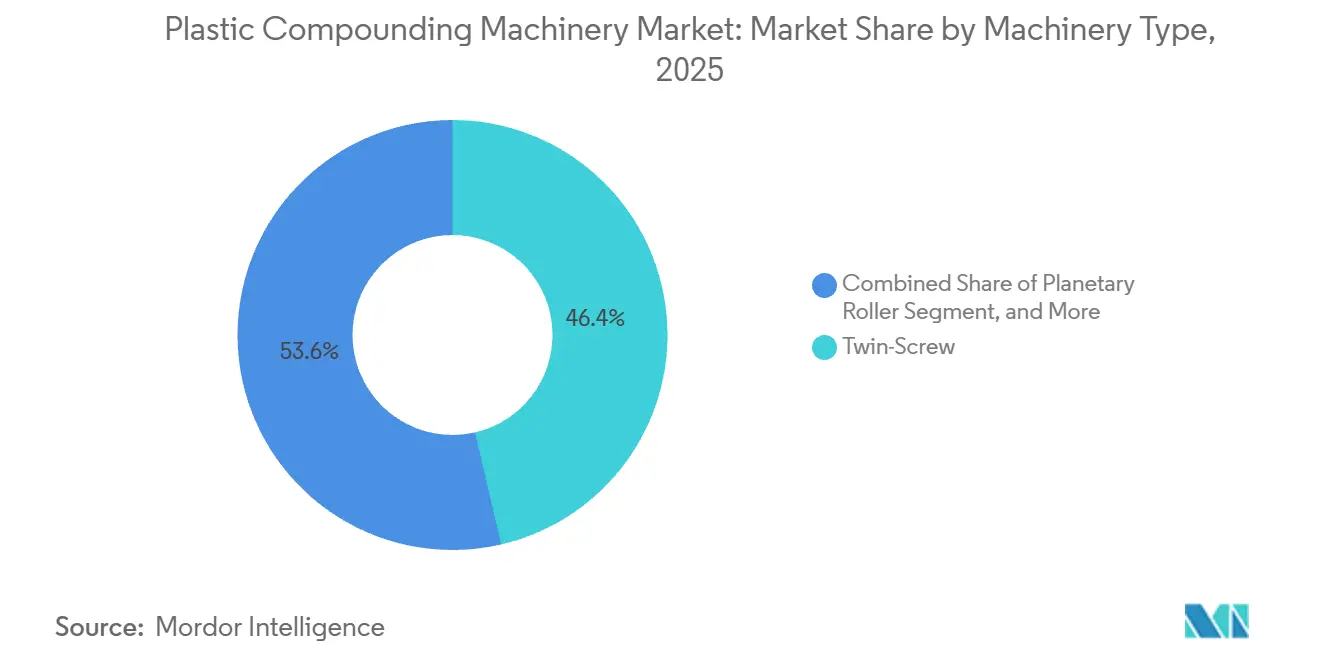

- By machinery type, twin-screw extruders held 46.37% of the plastic compounding machinery market share in 2025, whereas planetary-roller systems are forecast to grow at the fastest 7.23% CAGR through 2031.

- By application, the plastics segment accounted for 39.69% of the plastic compounding machinery market size in 2025 and is projected to expand at a 7.82% CAGR between 2026 and 2031.

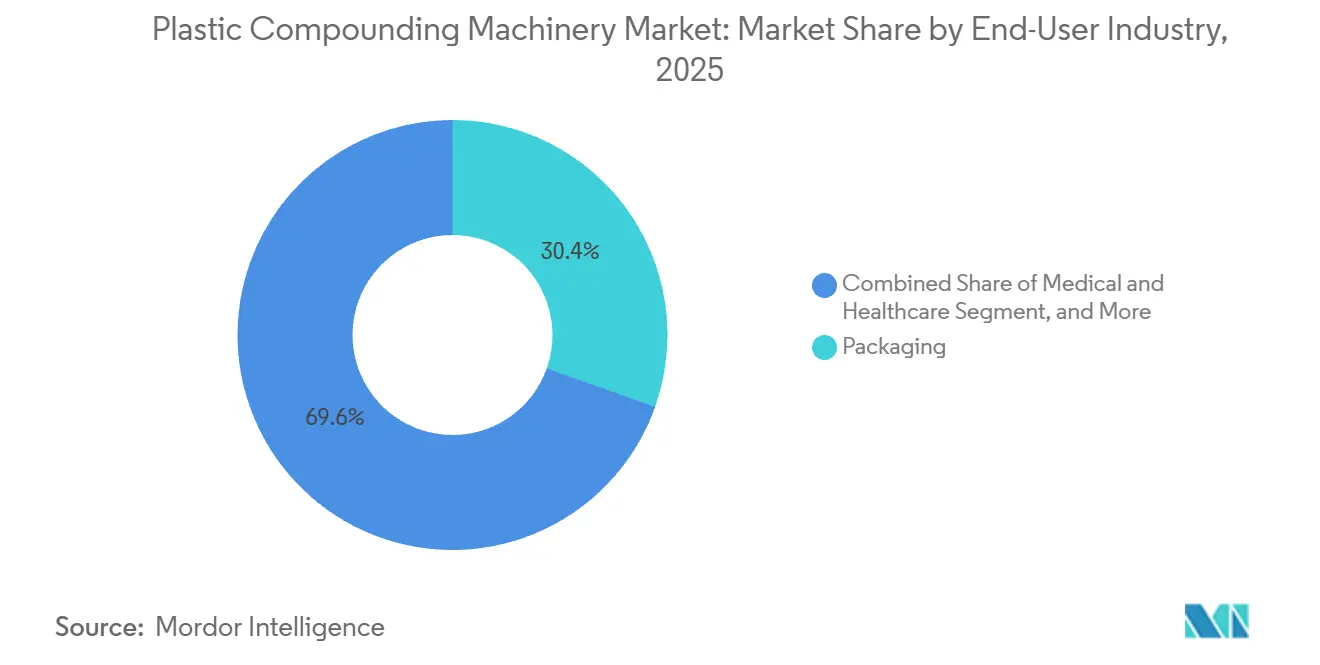

- By end-user industry, packaging led with 30.42% market share in 2025, while medical and healthcare applications are advancing at an 8.19% CAGR through 2031.

- By geography, Asia-Pacific captured 40.43% of share in 2025 and is expected to grow at a 7.79% CAGR, outpacing every other region over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plastic Compounding Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Global Demand for Lightweight, Recyclable Packaging | +1.2% | Global, with peak intensity in Europe and North America | Medium term (2-4 years) |

| Rapid Adoption of Twin-Screw Extruders in Medical-Grade Polymer Compounding | +0.9% | North America, Europe, Japan | Medium term (2-4 years) |

| Growth in Additive Manufacturing Filament Production Lines | +0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Push for Recycled-Content Mandates in Europe and North America | +1.4% | Europe, North America | Short term (≤ 2 years) |

| Shift Toward Decentralised, On-Site Compounding in EV Battery Plants | +0.8% | Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Emergence of AI-Driven Predictive Maintenance Lowering Total Cost of Ownership | +0.5% | Global, early adoption in North America and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Global Demand for Lightweight, Recyclable Packaging

Brand owners target 30%–65% recycled content by 2030 under new European law, forcing film and thermoforming converters to retrofit twin-screw lines with high-capacity melt filters that can remove label glue, ink, and food residue without degrading polymer chains.[1]European Commission, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” ec.europa.eu Japan’s Ministry of Economy, Trade and Industry committed JPY 30 billion (USD 199.5 million) to recycling infrastructure, unlocking capex for planetary-roller extruders that process closed-loop automotive and electronics waste.[2]Ministry of Economy, Trade and Industry, “Circular Economy Funding Allocation for Fiscal Year 2025,” meti.go.jp Processors adopting these lines reduce finished-pack weight by up to 50%, trimming freight emissions while maintaining barrier performance. The need to amortize costly filtration equipment pressures margins, yet twin-screw designs with self-wiping elements shorten clean-out time and preserve throughput, partially offsetting recycled-resin premiums. As more brand owners invoke supplier scorecards tied to recyclability, the demand uplift contributes a 1.2-percentage-point boost to the global CAGR.

Rapid Adoption of Twin-Screw Extruders in Medical-Grade Polymer Compounding

Orthopedic-implant makers migrate from batch mixers to continuous twin-screw extrusion because ASTM F648 and ISO 13485 traceability clauses demand consistent molecular-weight distribution and electronic data capture.[3]U.S. Food and Drug Administration, “Recognition of Consensus Standards for Medical Devices – ASTM F648,” fda.gov European Union Medical Device Regulation 2017/745 further obliges processors to log every temperature set-point and screw-torque value, accelerating orders for extruders with in-line near-infrared spectroscopy and automated quality dashboards. Digital-twin simulations offered by Japanese and German suppliers help engineers validate screw configurations without consuming medical-grade resin, saving thousands of dollars per qualification run. Medical and healthcare end users, growing at an 8.19% CAGR, therefore choose mid-diameter co-rotating screws that allow rapid formula changeovers with less than 0.5% residual contamination. The cumulative benefit adds 0.9 percentage points to overall market growth.

Growth in Additive-Manufacturing Filament Production Lines

Aerospace and surgical-instrument engineers now extrude polyetheretherketone, liquid-crystal polymer, and carbon-fiber-reinforced polyamide into 1.75 mm filaments with ±0.02 mm diameter accuracy, requiring compact twin-screw units that reach 450 °C barrel temperatures. Benchtop planetary-roller designs provide five to ten times more heat-transfer surface than equivalent screw diameters, allowing gentle processing of heat-sensitive specialty polymers. Research laboratories value interchangeable screws that facilitate small-lot trials under 25 kg without sacrificing dispersion quality, and cloud-based torque monitoring predicts wear before catastrophic failure, reducing unexpected downtime. As filament demand broadens from prototyping to limited-series production, machinery suppliers selling 5–50 kg-h units secure new recurring revenue streams from universities, contract manufacturers, and maintenance depots. This emerging customer base contributes a 0.6-percentage-point lift to the forecast CAGR.

Regulatory Push for Recycled-Content Mandates in Europe and North America

Extended producer-responsibility programs in France, Germany, and California penalize packaging with insufficient recycled content, immediately shifting capex toward twin-screw lines capable of devolatilizing post-consumer flakes down to 50 ppm volatile levels. The same statutes ban selected fluorinated additives, forcing formulators to develop alternative slip agents that tolerate narrower processing windows, a change that favors extruders with tightly zoned heating systems. Large converters hedge regulatory risk by commissioning multi-feed extruders that can alternate between virgin and reclaimed resin streams without lengthy screw swaps, while bottle-to-bottle PET recyclers adopt turnkey systems integrating optical sorting, washing, and compounding for 2,000 kg-h throughput. Because similar mandates are proposed in Canada and several U.S. states, the regulatory tailwind produces the single highest CAGR uplift at 1.4 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Long Pay-Back Period for Multi-Component Compounders | -0.7% | Global, acute in South America, Middle East, and Africa | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks in Specialty Screw-Barrel Alloys | -0.5% | Global, with tightest supply in Europe and North America | Medium term (2-4 years) |

| Volatility in Polymer Feedstock Prices | -0.6% | Global | Short term (≤ 2 years) |

| Skill Gap in Operating Industry 4.0-Enabled Lines | -0.4% | Asia-Pacific, South America, Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and Long Pay-Back Period for Multi-Component Compounders

Fully automated twin-screw lines with gravimetric feeders, side stuffing ports, and strand pelletizers range from USD 1.5 million to USD 3.5 million, a sum that strains converters operating on sub-7% EBITDA margins. In Brazil, Turkey, and South Africa, commercial lenders classify plastics compounding as mature and high-risk, demanding collateral that smaller processors seldom hold, further lengthening the project-finance queue. Some Western suppliers now pilot equipment-as-a-service contracts bundling machinery, maintenance, and analytics for a monthly fee, but adoption outside North America and Western Europe remains below 5% of new installations. Without concessional credit, converters stretch single-screw life cycles, deferring upgrades even when energy savings could exceed 15%. The resulting under-investment subtracts 0.7 percentage points from anticipated global CAGR.

Supply-Chain Bottlenecks in Specialty Screw-Barrel Alloys

Wear-resistant bimetallic barrels require cobalt and nickel, metals subject to geopolitical supply shocks and export restrictions, which inflate alloy surcharges and extend lead times past nine months. European and North American fabricators face capacity ceilings in nitriding-coating furnaces, forcing them to prioritize medical and aerospace orders over commodity lines and creating scheduling conflicts for mid-tier compounders. Asian alloy producers are scaling output, yet cross-border logistics delays and rigorous re-qualification protocols prevent quick substitution. Processors respond by stockpiling spare screws, tying up working capital that could fund line expansions or digital-twin software. The persistent shortage trims another 0.5 percentage points from the global CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Twin-Screw Leadership Faces Planetary-Roller Momentum

Twin-screw extruders commanded 46.37% of the share in 2025, underscoring their versatility in commodity blends, engineered plastics, and reactive extrusion across every major region of the plastic compounding machinery market. Counter-rotating versions dominate PVC pipe and profile extrusion, whereas co-rotating models handle high-fill masterbatch, devolatilization, and medical-grade compounds that must meet strict traceability rules. Planetary-roller technology is now the fastest-growing niche at a 7.23% CAGR through 2031 because specialty-polymer producers need low-shear environments that prevent thermal degradation and color shift. Modular roller barrels deliver surface areas five to ten times larger than twin-screw equivalents, ensuring narrow melt-temperature bands even with flame-retardant or conductive fillers. As processors retrofit brownfield plants, feed-enhancement attachments and gear-pump modules help twin-screws retain relevance, sustaining healthy order pipelines for established European and Japanese suppliers.

Scalability is driving incremental adoption of planetary-roller systems among contract compounders that must prove process equivalence from pilot to large-scale runs without repeated validation tests. Operators can extend barrel length or add additional roller spindles in the field, aligning installed capacity with fluctuating customer demand while preserving residence-time distribution. Meanwhile, single-screw machines persist in low-complexity color-concentrate let-down where price sensitivity outweighs mixing performance, indirectly anchoring installed-base service revenues. The coexistence of three core machine archetypes therefore sustains a multi-tier equipment hierarchy, reinforcing moderately concentrated competition that nevertheless allows regional entrants to win price-sensitive contracts. Collectively, varied machinery preferences keep growth balanced across throughput bands, insulating the plastic compounding machinery market from severe cyclical swings.

By Application Type: Plastics Segment Commands Volume While Masterbatch Specialization Accelerates

Plastic applications generated 39.69% of the share in 2025, and is projected to expand at a 7.82% CAGR during the forecast period, making them the largest single demand node within the plastic compounding machinery market. Engineering-resin formulations for lightweight automotive parts, flame-retardant grades for consumer electronics, and bio-based polyamides for premium packaging all require high-torque twin-screws equipped with advanced degassing sections. Masterbatch production, a key subset, increasingly relies on gravimetric dosing to limit pigment heat history and guarantee delta-E color deviations below 0.5, thereby protecting brand-owner aesthetics. Specialty-polymer lines designed for liquid-crystal polymers or polyetheretherketone integrate inert-gas purging and segmented screws with minimal free volume, preventing oxidative damage during long residence times. Suppliers that bundle cloud-connected torque sensors and automated cleaning programs frequently capture service contracts that equal 8%-10% of original machine value over five years.

Flooring compounds containing more than 60% calcium-carbonate filler use counter-rotating twin-screws or planetary-roller units fitted with chrome-plated liners to manage abrasive wear while maintaining throughput above 1,500 kg h. European building-efficiency regulations further stimulate demand for rigid PVC window profiles and wood-plastic composite decking, anchoring steady equipment replacement cycles. Cable jacketing, automotive under-hood clips, and 5G antenna connectors represent diverse but durable sub-niches that insulate total sales from sharp downturns in any single end market. The breadth of applications forces machinery builders to maintain extensive screw-element libraries, elevating intellectual-property barriers that discourage low-cost copycats. As converters chase recipe flexibility and short campaign times, suppliers able to guarantee less than 20 minutes between color changes grow wallet share within the plastic compounding machinery market.

By End-User Industry: Packaging Dominates, Medical and Healthcare Accelerate

Packaging retained a 30.42% market share in 2025, sustained by high film, bottle, and thermoformed-tray volumes that demand continuous upgrades to handle reclaimed resin streams without capacity loss. Yet medical and healthcare processors are expanding at an 8.19% CAGR as global aging drives orthopedic-implant and surgical-instrument consumption that must satisfy ISO 10993 biocompatibility tests. Construction shows renewed momentum in Asia-Pacific and the Middle East, where urban infrastructure growth is driving demand for polyvinyl-chloride pipes and profiles, reinforcing twin-screw retrofits tuned for high-filler formulations.

Automotive composite growth is directly linked to electrification, as polymer battery housings, cell spacers, and thermal-management pads displace heavier metal parts. Facility managers increasingly specify multi-feed twin-screws that switch between flame-retardant polyamide, conductive polypropylene, and recyclate-rich polycarbonate without extensive screw rebuilds, reducing inventories and downtime. Electronics manufacturers concurrently purchase high-temperature planetary-roller and twin-screw units that compound liquid-crystal-polymer grades for mmWave connectors, marrying tight dielectric constants with mechanical stability. Chemicals end users, mostly captive R and D lines inside resin producers, order smaller twin-screws outfitted with multiple side-stuffing ports and micro-feeders that handle nanofillers and reactive modifiers. This fragmentation across user verticals stabilizes long-term demand and further balances the plastic compounding machinery market.

Geography Analysis

Asia-Pacific generated 40.43% of share in 2025, and the region is poised to grow at a 7.79% CAGR through 2031 as China’s compounded-resin penetration climbs toward 50% of total plastics consumption. Chinese provinces such as Jiangsu and Guangdong host multi-line compounding clusters that benefit from state incentives, bulk resin availability, and proximity to electronics and automotive hubs. Japan’s JPY 30 billion (USD 199.5 million) recycling-fund allocation accelerates replacement of legacy single-screw extruders with co-rotating models fitted with twin-vent barrels for recycled flake processing. India and Southeast Asian nations leverage tariff-neutral export platforms to attract downstream investment, expanding regional demand for mid-throughput extruders that can handle frequent color changes and moderate recycled-resin loadings.

Europe’s equipment orders track the rollout of Regulation (EU) 2025/40, which imposes 30%–65% recycled-content thresholds and bans selected fluorinated additives in food-contact packs. Germany and Italy remain machinery-manufacturing strongholds that export planetary-roller and high-torque twin-screw units worldwide, while France, Spain, and the Netherlands prioritize twin-screw retrofits equipped with advanced melt-filtration systems. The United Kingdom briefly enjoys lower compliance costs due to deferred extended-producer-responsibility fees, giving domestic converters a temporary capital-expenditure window before alignment with continental standards. Eastern-European processors upgrade gradually, balancing euro-denominated equipment costs against domestic resin-price volatility and tight labor availability.

North America benefits from abundant ethane-based feedstocks and a tightly integrated petrochemical chain, yet frequent Gulf-Coast weather disruptions and force-majeure events inject resin-supply uncertainty. U.S. compounders hedge risk by distributing capacity across Midwest and Southeast corridors, driving orders for modular twin-screws that can relocate as needed. Canadian and Mexican plantscanchored by USMCA trade protectionscbuy mid-range systems to serve automotive transplants that demand rapid color changes and traceability. South America, the Middle East and Africa collectively remain smaller markets constrained by elevated borrowing costs and currency volatility, although Brazilian agricultural-film demand, Saudi downstream diversification, and South-African auto-component projects create localized hot spots that favor lower-cost Chinese twin-screw packages. Overall, geographic diversification helps smooth total-market revenue swings, reinforcing a steady medium-term growth path for the plastic compounding machinery market.

Competitive Landscape

European, Japanese, and North American original-equipment manufacturers capture roughly 60% - 70% of global revenue, underpinning a moderate concentration level that still leaves space for regional challengers. Coperion, KraussMaffei, and Leistritz leverage proprietary screw-element libraries, global service hubs, and decades of validation data to dominate high-margin medical and specialty-polymer niches where change-control documentation raises switching barriers. Kobe Steel and The Japan Steel Works focus on Asia-Pacific clients needing large-diameter co-rotating twin-screws optimized for glass-fiber-reinforced automotive parts, complemented by AI-driven predictive-maintenance suites that promise 15%–20% unplanned-downtime reductions.

Nordson and Bühler differentiate through downstream equipment such as gear-pumps and integrated PET recyclers, bundling extrusion, washing, melt-filtration, and pelletizing in turnkey packages that shrink project timelines for converters navigating stringent recycled-content laws. Chinese producers like Useon and Nanjing Giant offer twin-screw systems priced 30%–40% below European benchmarks, capturing price-sensitive commodity applications, while Indian firms such as Welset Plast Extrusions win domestic orders through localized spare-parts logistics. Certification hurdles ISO 13485 for medical machinery, CE safety marking for European sales, and UL listing for North American installations temper low-cost entrants’ penetration into regulated segments.

A third competitive tier is emerging around decentralized compounding solutions for electric-vehicle battery plants and additive-manufacturing filament producers. Suppliers now market compact skid-mounted twin-screws with throughputs under 150 kg h that fit inside battery-assembly halls, allowing real-time compounding of polypropylene housings with flame-retardant fillers. Modular benchtop extruders serving research institutions integrate plug-and-play barrel sections, touchscreen recipe recall, and cloud data export, creating new recurring-service opportunities. Over the next five years, manufacturers offering digital-twin modeling, remote-diagnostics packages, and leasing contracts are expected to outpace peers that rely solely on conventional hardware sales, further segmenting the competitive landscape of the plastic compounding machinery market.

Plastic Compounding Machinery Industry Leaders

Coperion GmbH

CPM Extricom Extrusion GmbH

Farrel Corporation

Kobe Steel, Ltd.

ICMA San Giorgio S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Kobe Steel completed factory-acceptance testing of a 96 mm twin-screw extruder with AI-based screw-configuration recommendation software for an Indonesian automotive compounder, marking the first commercial deployment of the system outside Japan.

- October 2025: Coperion unveiled the ZSK Mc18 modular twin-screw extruder at K 2025, integrating feed-enhancement technology that raises throughput 15%–20% without enlarging barrel diameter.

- October 2025: Nordson introduced BKG blueflux gear pumps, delivering 50% lower melt-pressure fluctuation on retrofit twin-screw and single-screw lines.

- October 2025: Bühler launched the Polytrack bottle-to-bottle PET recycling system, integrating optical sorting, washing, and twin-screw compounding at 2,000 kg h capacity.

Global Plastic Compounding Machinery Market Report Scope

The Plastic Compounding Machinery Market study encompasses an in-depth analysis of equipment used for blending polymers with additives, fillers, and colorants to produce customized plastic compounds.

The Plastic Compounding Machinery Market Report is Segmented by Machinery Type (Single-Screw, Twin-Screw, Planetary Roller, and Other Machinery Types), Application Type (Plastics, Masterbatch Production, Specialty Polymers, Flooring Compounds, and Other Application Types), End-User Industry (Packaging, Construction and Infrastructure, Medical and Healthcare, Automotive, Electronics, Chemicals, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Screw | |

| Twin-Screw | Co-Rotating Twin-Screw |

| Counter-Rotating Twin-Screw | |

| Planetary Roller | |

| Other Machinery Types |

| Plastics |

| Masterbatch Production |

| Specialty Polymers |

| Flooring Compounds |

| Other Application Types |

| Packaging |

| Construction and Infrastructure |

| Medical and Healthcare |

| Automotive |

| Electronics |

| Chemicals |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machinery Type | Single-Screw | ||

| Twin-Screw | Co-Rotating Twin-Screw | ||

| Counter-Rotating Twin-Screw | |||

| Planetary Roller | |||

| Other Machinery Types | |||

| By Application Type | Plastics | ||

| Masterbatch Production | |||

| Specialty Polymers | |||

| Flooring Compounds | |||

| Other Application Types | |||

| By End-User Industry | Packaging | ||

| Construction and Infrastructure | |||

| Medical and Healthcare | |||

| Automotive | |||

| Electronics | |||

| Chemicals | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue will plastic-compounding-equipment suppliers generate by 2031?

Combined sales are projected to reach USD 13.09 billion, growing at a 6.73% CAGR from 2026 to 2031.

Which machinery type leads current installations?

Twin-screw extruders hold 46.37% of 2025 global revenue due to unmatched mixing versatility.

Which end-user sector is expanding fastest?

Medical and healthcare processors show an 8.19% CAGR as regulators demand validated, traceable compounds.

Why is Asia-Pacific the largest regional buyer?

China’s shift toward modified plastics and Japan’s recycling incentives drive a 7.79% regional CAGR.

What main factor restrains small converters from upgrading?

High capex and four-to-six-year payback periods discourage investment in multi-component twin-screw lines.

Page last updated on: