Automatic Tea Bag Packaging Machinery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

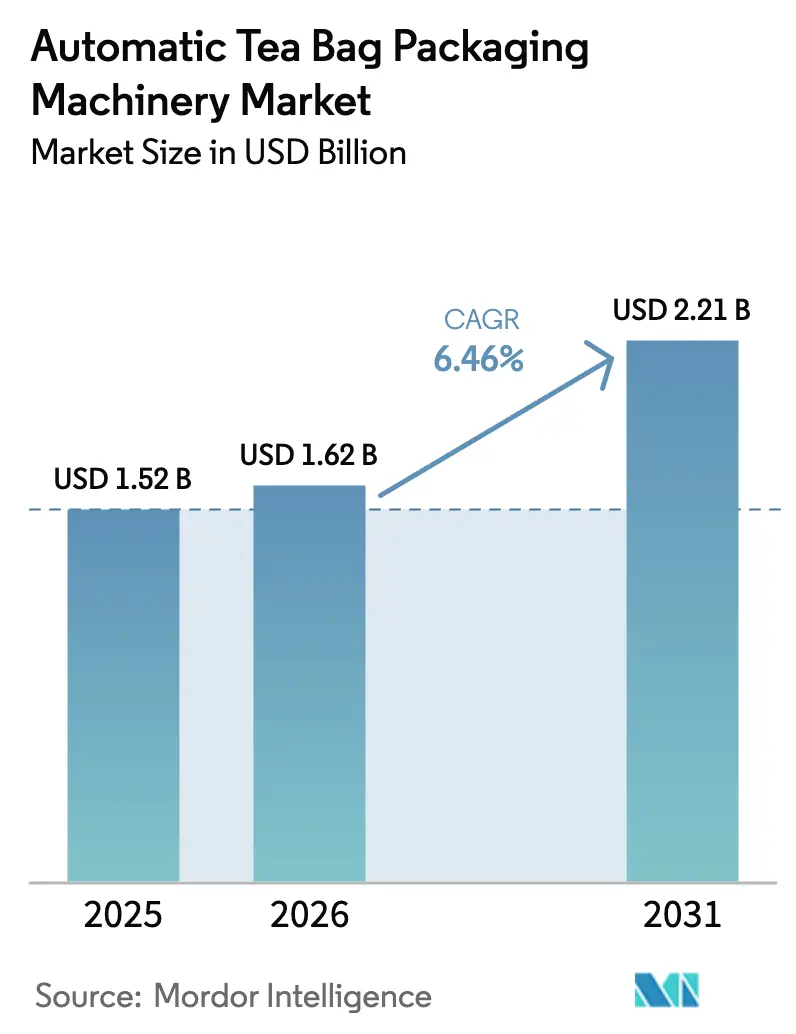

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

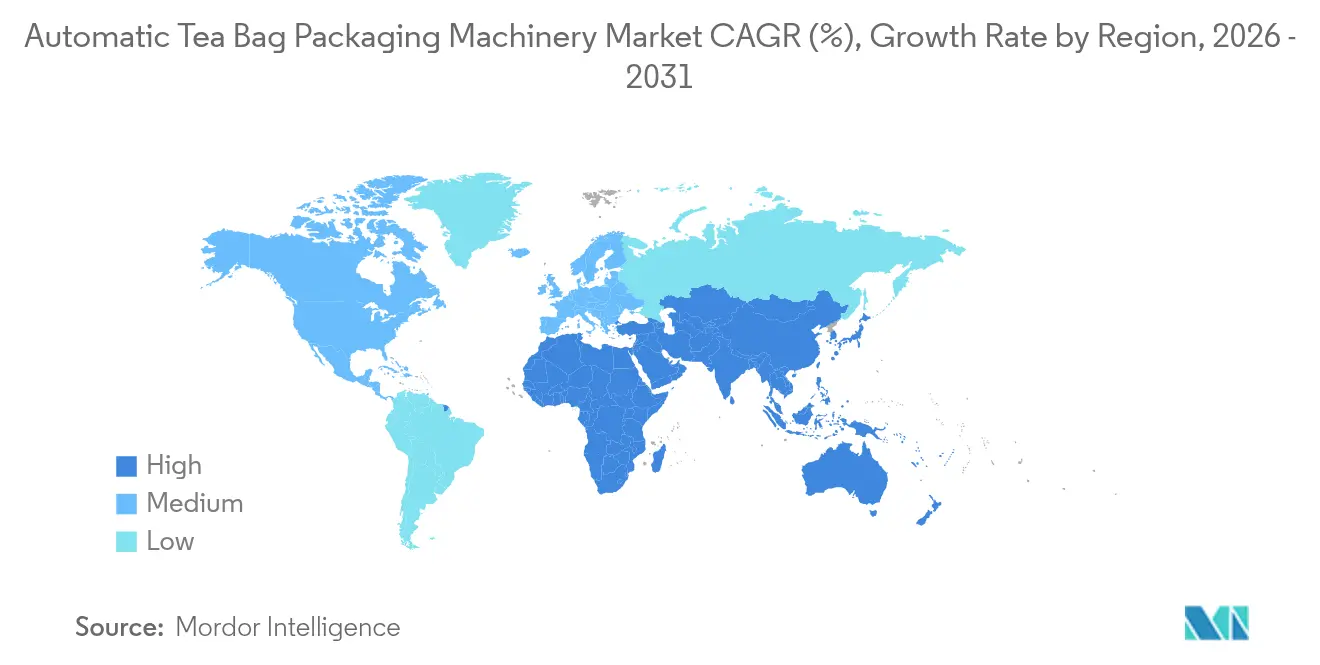

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic Tea Bag Packaging Machinery Market Analysis by Mordor Intelligence

The automatic tea bag packaging machinery market size is expected to grow from USD 1.52 billion in 2025 to USD 1.62 billion in 2026 and is forecast to reach USD 2.21 billion by 2031 at 6.46% CAGR over 2026-2031. Sustained gains stem from rising global tea consumption, premium single-serve adoption, and accelerating automation that allows processors to raise throughput while keeping exacting quality standards. The shift toward portion-controlled, visually appealing formats is pushing converters to adopt machines that combine high dosing accuracy with rapid changeovers. Sustainability mandates are equally influential, prompting steep uptake of PLA and other compostable substrates that demand recalibrated sealing and quality-control modules. Competitive intensity is increasing as leading European OEMs embed Industry 4.0 functions, while cost-competitive Asian suppliers scale production capacity and shorten delivery lead times.

Key Report Takeaways

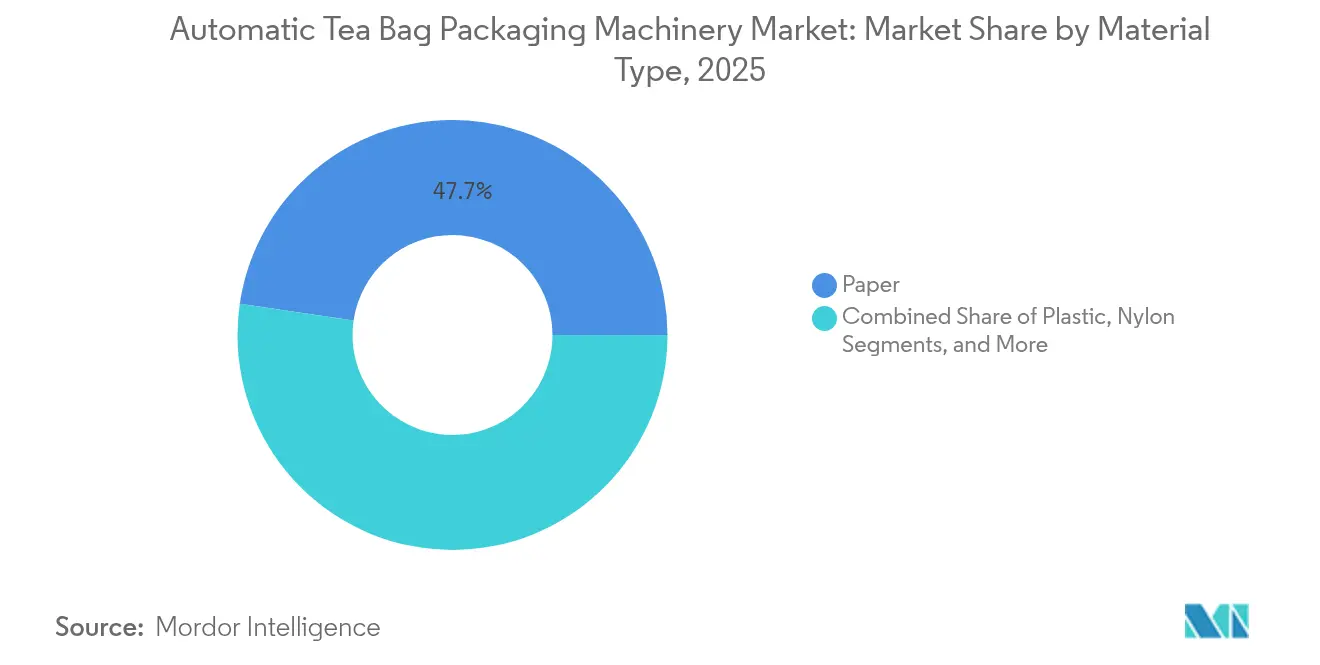

- By material type, paper captured 47.68% of the Automatic Tea Bag Packaging Machinery Market share in 2025.

- By packaging shape, Automatic Tea Bag Packaging Machinery Market size for pyramid bags is projected to grow at 8.45% CAGR between 2026-2031.

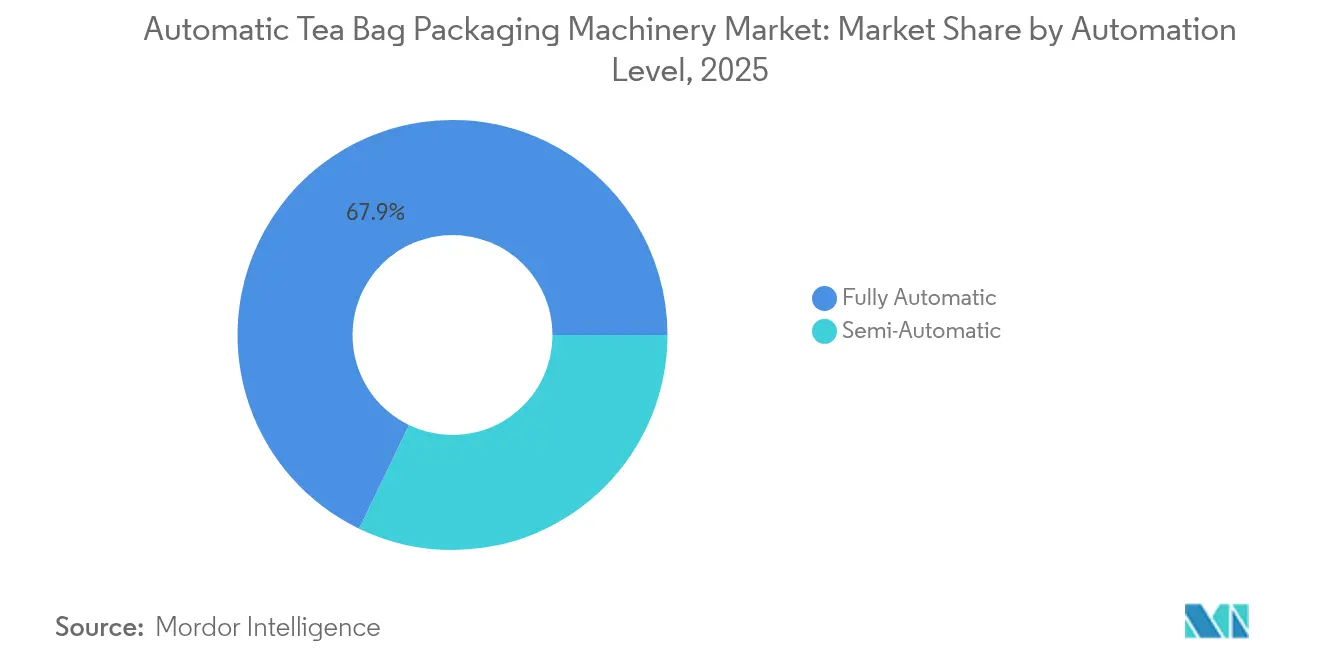

- By automation level, fully automatic systems captured 67.85% of the Automatic Tea Bag Packaging Machinery Market share in 2025.

- By line capacity, Automatic Tea Bag Packaging Machinery Market size for more than 120 bpm is projected to grow at 7.68% CAGR between 2026-2031.

- By geography, Asia-Pacific captured 42.18% of the Automatic Tea Bag Packaging Machinery Market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automatic Tea Bag Packaging Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Tea Consumption and Premium Single-Serve Demand | +1.8% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Growing Requirement for End-to-End Automation in Tea Packaging Plants | +2.1% | Global, focus on Europe and Asia-Pacific hubs | Long term (≥ 4 years) |

| Shift Toward Sustainable/Biodegradable Tea-Bag Substrates | +1.2% | Europe and North America are leading, and Asia-Pacific is catching up | Medium term (2-4 years) |

| Brand Differentiation Via Pyramid/Visual-Format Tea Bags | +0.9% | Premium segments worldwide | Short term (≤ 2 years) |

| Industry 4.0 Predictive-Maintenance Integration | +0.7% | Europe and North America are early adopters | Long term (≥ 4 years) |

| On-Demand Micro-Batch/D2C Flexibility Needs | +0.6% | North America and Europe e-commerce | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Tea Consumption and Premium Single-Serve Demand

Global tea intake is increasing by 3.3% each year, and a disproportionate share of that growth is directed towards premium single-serve formats that rely on reliable, high-speed packaging. Functional-herbal and organic blends now command shelf space in office pantries, hospitality amenities, and foodservice channels, all of which require individually wrapped bags that control portion size and preserve bioactive compounds. Premium brands often adopt pyramid shapes to showcase whole-leaf content, obliging converters to invest in machines that deliver precise volumetric dosing, as well as tight ultrasonic seals. Demand is particularly strong in the Asia-Pacific and North America regions, where processors are expanding high-throughput lines to match rapidly evolving consumer expectations.[1]ItaliaImballaggio, “ItaliaImballaggio July-August 2025,” packmedia.net

Growing Requirement for End-to-End Automation in Tea Packaging Plants

Automation upgrades are yielding up to 15% gains in overall equipment effectiveness while trimming labor costs, scrap, and energy consumption. Servo-driven changeovers reduce downtime when switching between rectangular, pyramid, or round bags, and integrated vision modules verify seam integrity in real-time. Robotics and machine-learning algorithms now coordinate case packing and palletizing, creating a seamless flow from dosing to secondary packaging. Europe and the Asia-Pacific lead installations because exporters confront stringent traceability rules tied to food safety audits.

Shift Toward Sustainable/Biodegradable Tea-Bag Substrates

Regulation (EU) 2025/40 requires brands selling into the European Economic Area to use recyclable or compostable packaging and to limit the use of substances of concern. Large tea companies have responded by certifying PLA, unbleached kraft, and mono-material filter meshes, which in turn requires new seal-temperature profiles, anti-static controls, and barrier-coating compatibilities on machinery. North American retailers echo similar requirements through private-label scorecards, pressuring co-packers to rapidly retrofit their lines. Asian substrate suppliers ramp PLA film output to ensure local processors comply with export standards.

Brand Differentiation Via Pyramid/Visual-Format Tea Bags

Pyramid bags enable larger cut leaves to unfurl, reinforcing perceptions of premium quality while bolstering flavor extraction. Converters that can flip from flat tags to 3-D shapes without extended downtime secure more seasonal and limited-edition contracts. Ultrasonic sealing heads ensure tamper-proof seams, and clear windows on outer envelopes offer shelf impact. The trend aligns with direct-to-consumer subscription services in North America and Western Europe, where unboxing aesthetics influence reorder rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial CAPEX For High-Speed Automated Lines | -1.4% | Global, most acute in developing regions | Long term (≥ 4 years) |

| Scarcity Of Skilled Mechatronics Technicians and Costly Downtime | -1.1% | Worldwide, severe in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Supply-Chain Fragility for Specialty Filter Meshes and PLA Films | -0.8% | Europe and Asia-Pacific | Short term (≤ 2 years) |

| Evolving Food-Contact Rules On Novel Bio-Polymers | -0.7% | Europe, North America, export-oriented Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX For High-Speed Automated Lines

The entry ticket for a fully automatic, multi-format packaging cell surpasses USD 500,000, excluding plant retrofits and operator training. Although leasing and machinery-as-a-service contracts have emerged, many mid-sized processors in Southeast Asia, Africa, and South America still face significant financing hurdles. This cost barrier consolidates market power among large, well-capitalized exporters that can amortize investments over high volumes. Financial pressure hinders the diffusion of technology in cost-sensitive clusters, despite clear productivity benefits.

Scarcity Of Skilled Mechatronics Technicians and Costly Downtime

More than 50,000 mechatronics roles remained unfilled worldwide in 2025, stretching maintenance cycles and inflating downtime that can cost USD 10,000 per hour at large sites. Advanced packaging cells integrate robotics, IoT sensors, and AI-based quality analytics, raising the skill threshold far above conventional mechanical proficiency. OEMs therefore bundle remote diagnostics and augmented-reality repair manuals; yet, talent shortages persist, especially in the Asia-Pacific and South America regions. Scholarship programs and vendor-led academies alleviate bottlenecks only gradually.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Sustainability Drives Substrate Shifts

Paper substrates held a 47.68% share of the automatic tea bag packaging machinery market in 2025, thanks to legacy equipment compatibility and shopper familiarity. Nevertheless, biodegradable PLA films are projected to post the quickest 9.21% CAGR through 2031 as governments tighten compostability rules and brands chase the eco-labeling advantage. Within the automatic tea bag packaging machinery market, the size of the materials segment is dominated by paper in cost-sensitive mass channels, whereas PLA is gaining momentum among specialty retailers that emphasize zero-plastic pledges. Machinery builders have extended sealing-bar profiles and nip-roller controls to accommodate lower-melting PLA, helping co-packers toggle between fiber and bio-polymer rolls without lengthy changeovers.

A residual niche persists for nylon and silk wraps catering to ceremonial and high-grade leaf infusions, but scrutiny over microplastics and food-contact amendments limits their expansion. Investment, therefore, focuses on hybrid modules that can run paper, PLA, and nylon at the push of a touchscreen, securing processors against upcoming EU recyclability obligations. Line audits reveal that multi-material machines lift uptime by 4% and reduce film waste by 7%, signaling tangible paybacks that offset higher capital outlays.

By Packaging Shape: Pyramid Bags Fuel Premiumization

Rectangular bags accounted for 46.12% of 2025 installations because they offer mature filling speeds above 200 bpm and rely on well-tested filter papers. Yet pyramid units, while slower per lane, deliver 8.45% CAGR as retailers curate artisanal lines featuring visible botanicals. The automatic tea bag packaging machinery market size, tied to pyramid lines, is expected to exceed USD 806 million by 2031, illustrating how premiumization accelerates capital rotation toward 3D forming stations.

To capitalize on both opportunities, converters utilize dual-lane frames that alternate between flat and pyramid bags within a single shift, ensuring minimal idle time and safeguarding per-SKU profitability. Vision sensors inspect apex formation and tea-weight uniformity, and quick-release mandrels simplify sanitation across shape changes. Momentum for windowed outer pouches, which spotlight pyramid geometry, further cements demand for vertically integrated primary and secondary wrappers.

By Automation Level: End-to-End Systems Dominate

Fully automatic lines held 67.85% share in 2025, supported by in-line tag threading, ultrasonic sealing, and stack-and-pack modules that minimize manual touches. These systems represent the core of the automatic tea bag packaging machinery market share because they boost throughput while embedding traceability codes that auditors demand. OEM dashboards aggregate temperature, vibration, and belt-tension data, triggering alerts before failures occur, a capability that lifts OEE into the 85-90% bracket.

Semi-automatic cells remain relevant among boutique roasters and limited-edition runs where flexibility outweighs speed. The automatic tea bag packaging machinery market size, aligned to semi-automatic units, nonetheless expands modestly as micro-brands proliferate online. Suppliers therefore ship modular kits that allow owners to upgrade to full autonomy as order volumes increase, protecting the initial investment and compressing the payback period.

By Line Capacity: Scaling for Flexibility and Throughput

Installations rated at 61-120 bpm captured 53.55% share in 2025, providing a sweet spot between mid-range throughput and manageable footprint. Higher-speed machines operating above 120 bpm are expected to advance at a 7.68% CAGR, reflecting export contracts that require mass production for private-label supermarket chains. Within the automatic tea bag packaging machinery market, OEMs tout servo-driven indexing that enables on-the-fly acceleration when downstream case packers clear jams, thereby avoiding bottlenecks and preserving bag integrity.

Lines below 60 bpm serve artisan operators who value the gentle handling of oversized botanicals. Modular belt architecture permits processors to insert extra dosing funnels over time, eliminating the need for whole-line replacements. Safety upgrades comply with ISO 22000 and EU machine-directive standards, ensuring that even low-volume lines can access regulated export markets.

Geography Analysis

The Asia-Pacific region accounted for 42.18% of 2025 sales and is growing at an annual rate of 8.27% as China and India integrate field-to-cup value chains with smart factories. Local OEMs, such as Xiamen Sengong, refine pyramid-forming heads and predictive maintenance toolkits to match global benchmarks while maintaining price agility. Indian packers retrofit vision modules to meet EU import tolerances for seal strength, and government subsidies help cushion the costs of automation.

Europe retains its role as an innovation test bed because Regulation (EU) 2025/40 compels the use of recyclable and compostable packaging, prompting machinery retrofits that adjust heat-seal bars, implement anti-static measures, and utilize inline chemical migration testers. Italian, German, and British converters upgrade to mono-material PLA or unbleached kraft film, resulting in double-digit drops in defect rates. North America follows with steady premiumization, aided by direct-to-consumer channels that valorize high-graphics envelopes and Instagram-ready pyramid sachets.

South America, the Middle East, and Africa are experiencing a surge in unit installations, driven by gains in disposable income and the growth of urban café culture, from a relatively small base. Multilateral development banks extend soft loans for food processing modernization, helping local firms import mid-range, fully automatic lines. Regional free-trade agreements incentivize processors in Mexico, Türkiye, and Kenya to adopt EU-compliant substrates for access to premium buyers, gradually aligning technical standards worldwide.

Competitive Landscape

The automatic tea bag packaging machinery market remains moderately fragmented, yet the top five suppliers steadily increase their combined share as they pursue capacity expansions and digital service bundles. European majors, such as IMA and TEEPACK, leverage modular frames and embedded analytics to secure high-value contracts with multinational tea companies. They also roll out subscription-based remote monitoring that cuts downtime and deepens client lock-in.

Asian challengers, notably Xiamen Sengong and Dongguan Sammi, differentiate via competitive pricing and quick lead times while racing to certify machines for PLA and other next-generation substrates. Several have begun exhibiting at IPACK-IMA and Interpack to court Western distributors, signaling a shift toward global brand visibility. Joint ventures between European control-system firms and Chinese fabricators accelerate technology transfer and lower unit costs.

Strategic investments emphasize Industry 4.0, with vendors integrating edge-computing nodes that analyze vibration and torque patterns against cloud-hosted failure models. Machinery-as-a-service pilots gain traction among mid-sized processors that wish to bypass CAPEX barriers, paying usage-based fees tied to bag output. Compliance with U.S. FDA food-contact norms and EU substance restrictions is now a non-negotiable selling point, steering R&D spend toward multi-format sealing heads and solvent-free adhesive technologies.[3]Publications Office of the European Union, “Regulation (EU) 2025/40 on packaging and packaging waste,” eur-lex.europa.eu

Automatic Tea Bag Packaging Machinery Industry Leaders

TEEPACK Spezialmaschinen GmbH & Co. KG

I.M.A. Industria Macchine Automatiche S.p.A.

ACMA S.p.A.

Xiamen Sengong Packing Equipment Co., Ltd.

FUSO International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: ULMA Packaging inaugurated a new EUR 12.5 million (USD 13.6 million) plant dedicated to automation solutions, thereby boosting global capacity for fully automatic lines and reducing lead times for tea packagers.

- June 2025: IMA Ilapak launched a compostable high-barrier film validated for both vertical and horizontal baggers, enabling smooth transitions to eco-friendly substrates without sacrificing speed.

- May 2025: Tecno Pack showcased its FP 100 Flow Wrapper, featuring ultrasonic sealing and paper-based capabilities, at IPACK-IMA 2025, highlighting advances in high-speed, sustainable tea packaging.

- March 2025: The European Commission released Regulation (EU) 2025/40, which mandates recyclability and substance restrictions for all packaging, triggering machinery upgrades throughout the tea value chain.

Global Automatic Tea Bag Packaging Machinery Market Report Scope

The scope of the study on the Automatic Tea Bag Packaging Machinery Market encompasses an in-depth analysis of machines designed for the automated production and packaging of tea bags. The study examines technological advancements like servo-driven systems, IoT-enabled monitoring, and energy-efficient designs, along with their applications in tea manufacturing plants and contract packaging facilities.

The Automatic Tea Bag Packaging Machinery Market Report is Segmented by Material Type (Paper, Nylon, Plastic, Silk, and Other Material Types), Packaging Shape (Rectangular, Round, Pyramid / Triangle, and Other Packaging Shape), Automation Level (Fully Automatic, and Semi-Automatic), Line Capacity (less than 60 bpm, 61–120 bpm, and more than 120 bpm), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Paper |

| Nylon |

| Plastic |

| Silk |

| Other Material Types |

| Rectangular |

| Round |

| Pyramid / Triangle |

| Other Packaging Shapes |

| Fully Automatic |

| Semi-Automatic |

| less than 60 bpm |

| 61 – 120 bpm |

| more than 120 bpm |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Paper | ||

| Nylon | |||

| Plastic | |||

| Silk | |||

| Other Material Types | |||

| By Packaging Shape | Rectangular | ||

| Round | |||

| Pyramid / Triangle | |||

| Other Packaging Shapes | |||

| By Automation Level | Fully Automatic | ||

| Semi-Automatic | |||

| By Line Capacity | less than 60 bpm | ||

| 61 – 120 bpm | |||

| more than 120 bpm | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the automatic tea bag packaging machinery market in 2026?

The market is valued at USD 1.62 billion in 2026 and is forecast to reach USD 2.21 billion by 2031.

Which region leads to demand for automated tea bag machinery?

The Asia-Pacific region captures 42.18% of global revenue in 2025 and is expanding at the fastest rate of 8.27% annually.

Which material segment is growing the quickest?

Machines configured for biodegradable PLA film are expected to show the highest 9.21% CAGR through 2031.

Why are pyramid bags gaining traction?

They visually showcase whole-leaf teas, support premium pricing, and enhance infusion quality, resulting in an 8.45% CAGR for related machinery.

What restrains wider automation adoption?

High initial CAPEX and a shortage of skilled mechatronics technicians limit uptake, especially in developing economies.

How are sustainability regulations shaping machinery design?

EU Regulation 2025/40 mandates recyclable or compostable packaging, compelling OEMs to certify machines for PLA, unbleached kraft, and other eco-friendly substrates.

Page last updated on: