Plant Genomics Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

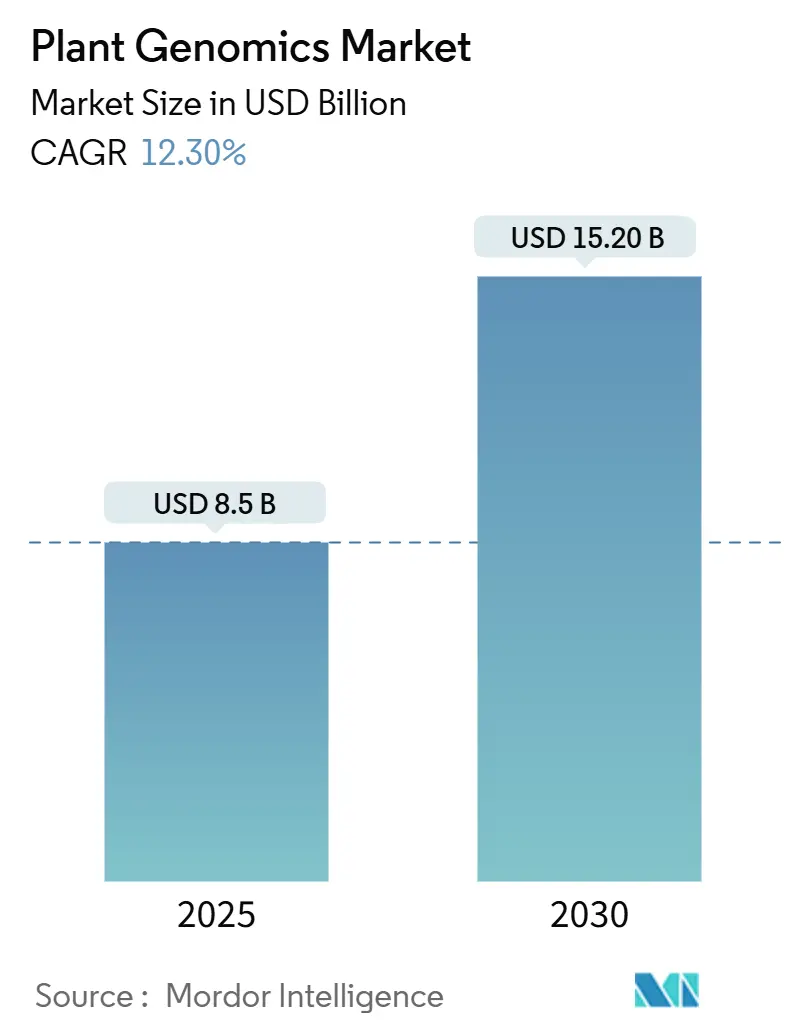

| Market Size (2025) | USD 8.5 Billion |

| Market Size (2030) | USD 15.20 Billion |

| Growth Rate (2025 - 2030) | 12.30% CAGR |

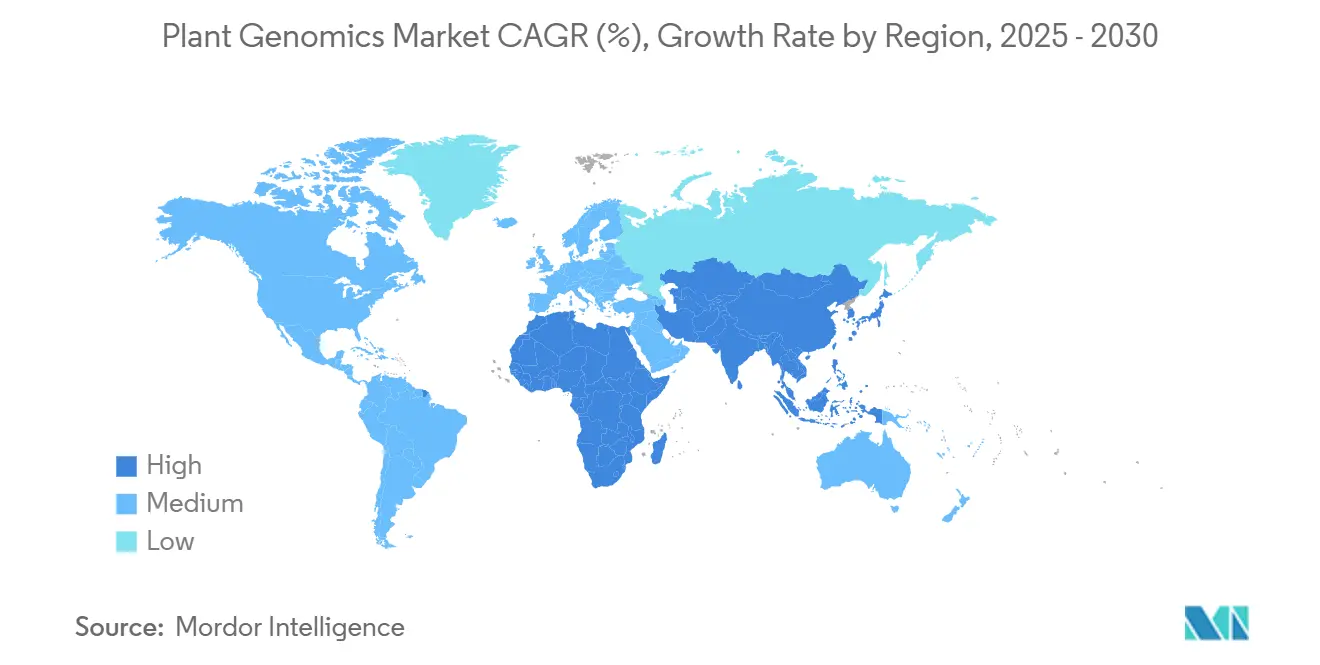

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

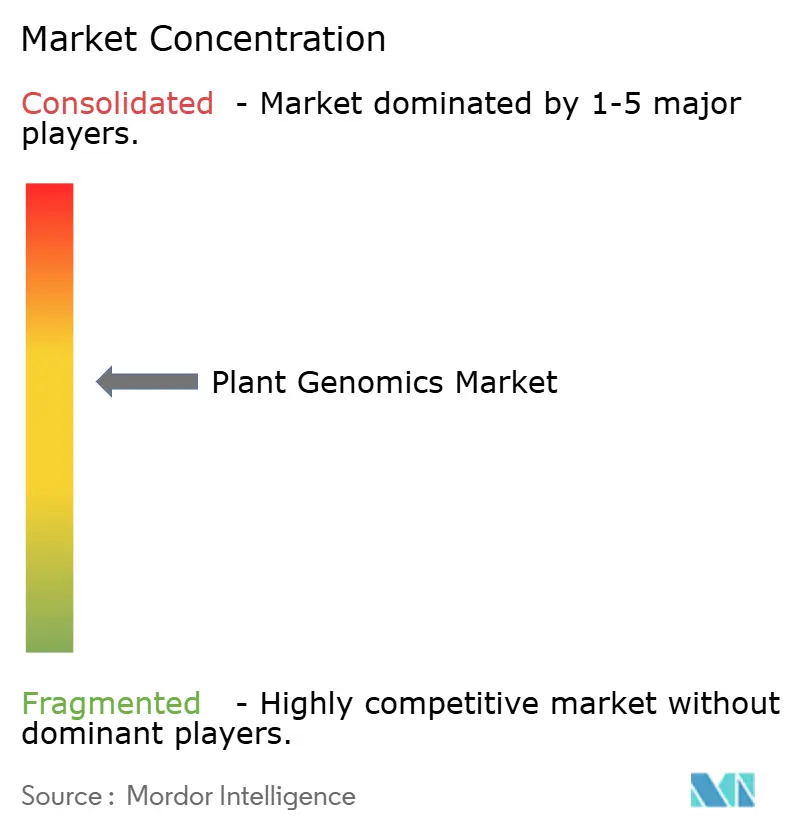

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Plant Genomics Market Analysis by Mordor Intelligence

The plant genomics market size stands at USD 8.5 billion in 2025 and is forecast to reach USD 15.2 billion by 2030, reflecting a 12.3% CAGR through the period. Continued cost declines in next-generation sequencing, the regulatory green light for gene-edited crops, and wider use of genomic tools across breeding pipelines are accelerating adoption. DNA sequencing remains the cornerstone technology, while gene editing is scaling vigorously as breeding groups transition CRISPR (Clustered regularly interspaced short palindromic repeats) workflows from proof-of-concept to commercial seed production. The competitive landscape reflects strategic consolidation around core technologies, with established sequencing platform providers expanding into agricultural applications while seed companies integrate genomic capabilities through partnerships and acquisitions. Market dynamics are increasingly influenced by regulatory harmonization efforts, carbon credit mechanisms for gene-edited cover crops, and the emergence of portable sequencing technologies enabling on-farm genomic applications.

Key Report Takeaways

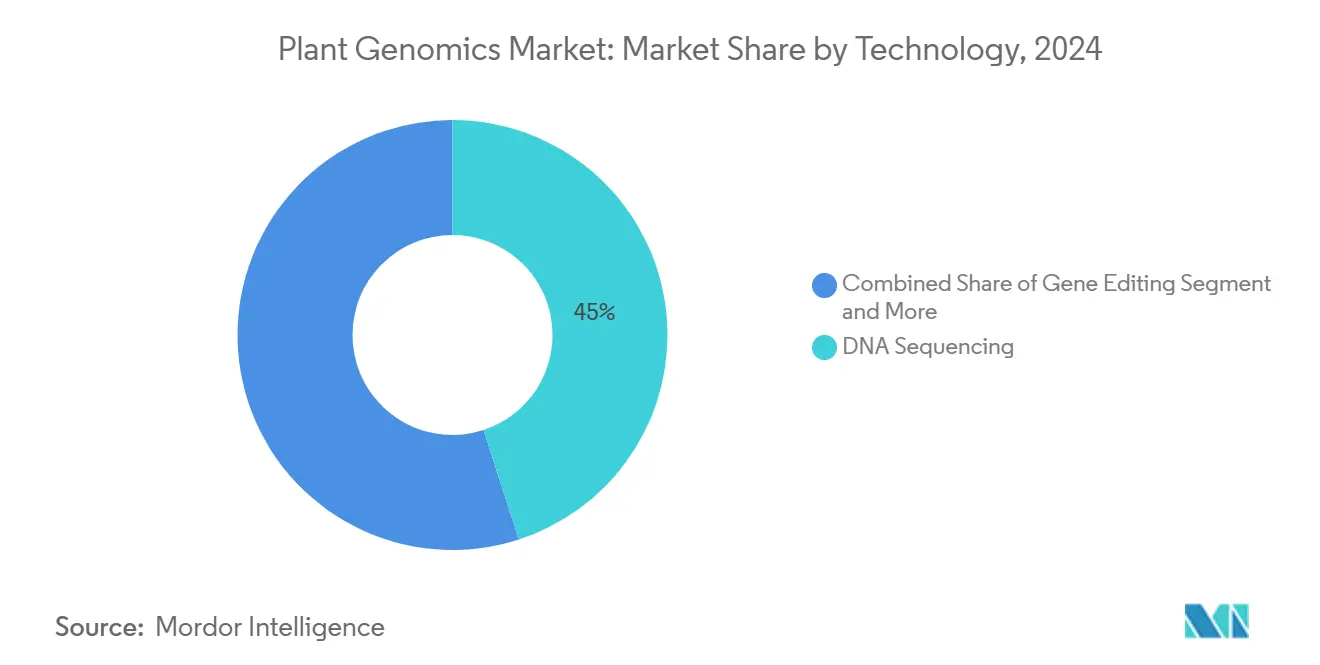

- By technology, DNA sequencing held 45.0% of the plant genomics market share in 2024, while gene editing is on track for an 18.8% CAGR through 2030.

- By trait, disease resistance commanded a 37.0% share of the plant genomics market size in 2024, while nutritional enhancement is set for a 16.9% CAGR between 2025 and 2030.

- By crop type, cereals and grains represented 39.0% of the plant genomics market in 2024, whereas fruits and vegetables are forecast to rise at a 15.5% CAGR through 2030.

- By geography, North America maintained 40.0% of the plant genomics market share in 2024, and Asia-Pacific is predicted to post a 14.0% CAGR over the forecast horizon.

Global Plant Genomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cost declines in next-generation sequencing | +2.1% | Global, with accelerated adoption in North America and Europe | Short term (≤ 2 years) |

| Growing demand for climate-resilient crops | +1.8% | Global, with highest impact in Asia-Pacific and Africa | Medium term (2-4 years) |

| Government funding for agricultural genomics research | +1.5% | North America, Europe, and Asia-Pacific core markets | Medium term (2-4 years) |

| Expansion of commercial seed R&D pipelines | +1.3% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Rise of on-farm portable sequencers | +0.9% | North America and Europe early adoption, spillover to Asia-Pacific | Medium term (2-4 years) |

| Carbon-credit premiums for gene-edited cover crops | +0.7% | North America and Europe regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Declines in Next-Generation Sequencing

The democratization of genomic sequencing through dramatic cost reductions is fundamentally reshaping plant genomics accessibility and adoption patterns. Illumina's achievement of the USD 600 genome milestone in 2024 represents a 50% cost reduction from previous benchmarks, enabling smaller agricultural research institutions and breeding programs to integrate genomic tools into their workflows. This cost trajectory is accelerated by competitive pressure from Oxford Nanopore Technologies' portable sequencing platforms, which have reduced per-sample costs for targeted agricultural applications by approximately 40% since 2024. The convergence of lower sequencing costs with improved bioinformatics tools is particularly impactful for marker-assisted selection programs, where cost-per-sample economics now favor genomic approaches over traditional phenotypic screening for many breeding applications.

Growing Demand for Climate-Resilient Crops

Climate volatility is driving unprecedented demand for genomically-enhanced crop varieties capable of withstanding extreme weather events and changing environmental conditions. The 2024 growing season witnessed significant crop losses across major agricultural regions, with drought-related yield reductions exceeding 15% in key grain-producing areas, intensifying focus on genomic solutions for stress tolerance. Plant genomics companies are responding by accelerating the development of multi-stress tolerance traits, with CRISPR(Clustered regularly interspaced short palindromic repeats)-edited varieties showing superior performance under combined heat and drought stress conditions. Demand is particularly strong in the Asia-Pacific region, where government initiatives prioritize genomic approaches to food security, and China allocated USD 2.8 billion to agricultural biotechnology research in 2024.

Government Funding for Agricultural Genomics Research

Strategic government investments are catalyzing plant genomics innovation through targeted funding programs and research infrastructure development. The USDA's National Institute of Food and Agriculture expanded its plant genomics funding by 35% in 2024, reaching USD 450 million annually, with specific emphasis on climate adaptation and nutritional enhancement applications. The European Union's Horizon Europe program allocated EUR 380 million (USD 410 million) to agricultural genomics research in 2024, focusing on sustainable crop production and biodiversity conservation[1]Source: USDA National Institute of Food and Agriculture, “USDA announces 450 million plant genomics initiative,” nifa.usda.gov. These investments are complemented by regulatory framework development, with agencies like the USDA Animal and Plant Health Inspection Service streamlining approval processes for gene-edited crops, reducing regulatory timelines by an average of 18 months.

Expansion of Commercial Seed R&D Pipelines

Major seed companies are substantially increasing their genomics-enabled R&D investments, with pipeline expansions targeting both traditional breeding enhancement and novel trait development. Corteva Agriscience increased its genomics R&D spending by 28% in 2024, reaching USD 1.2 billion, while expanding its gene editing capabilities through strategic partnerships with specialized biotechnology firms[2]Source: Corteva Annual Report 2024, "Genomics R&D Investment Expansion," corteva.com. Bayer's Crop Science division allocated EUR 2.1 billion (USD 2.3 billion) to genomics-enhanced breeding programs in 2024, with particular emphasis on developing crops optimized for regenerative agriculture practices. This investment surge is driven by competitive pressure to deliver differentiated traits and the recognition that genomic tools can reduce breeding cycle times from 8-10 years to 4-6 years for many crop improvement objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of sequencing platforms | -1.4% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Complex global regulatory approvals for gene-edited seeds | -1.1% | Global, with varying regional intensity | Medium term (2-4 years) |

| Data-privacy concerns around crop genomes | -0.8% | Global, with emphasis in Europe and North America | Long term (≥ 4 years) |

| Limited bioinformatic workforce in emerging markets | -0.6% | Asia-Pacific, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Sequencing Platforms

Despite declining per-sample costs, the substantial capital investment required for comprehensive genomic platforms continues to limit market penetration, particularly among smaller breeding programs and emerging market institutions. High-throughput sequencing systems require initial investments of USD 500,000 to USD 1.5 million, with annual maintenance and consumable costs adding USD 200,000 to USD 400,000 for typical agricultural applications. This capital intensity is compounded by the need for specialized laboratory infrastructure, including controlled environmental conditions and data storage systems, which can double total implementation costs.

Complex Global Regulatory Approvals for Gene-Edited Seeds

Regulatory fragmentation across major agricultural markets creates significant barriers to commercialization and increases development costs for gene-edited crop varieties. The European Union's evolving regulatory framework for new genomic techniques has created uncertainty for developers, with approval timelines extending 24-36 months beyond initial projections[3]Source: European Food Safety Authority, "New genomic techniques: EFSA publishes updated guidance," efsa.europa.eu. Divergent regulatory approaches between the United States, European Union, and Asia-Pacific markets require separate approval processes, with total regulatory compliance costs ranging from USD 15 million to USD 35 million per trait across major markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Gene Editing Accelerates Commercialization

Although DNA sequencing still accounts for 45.0% 2024 revenue, editing platforms are scaling behind an 18.8% CAGR as intellectual-property barriers ease and multiplex editing tools gain precision. Gene editing reduces linkage drag, delivers non-transgenic edits, and shortcuts backcrossing, allowing faster cultivar release. Marker-assisted selection persists where low-density genotyping panels remain cost-efficient, yet the convergence of whole-genome prediction and high-density single-nucleotide polymorphism arrays is lifting breeding accuracy for polygenic traits.

Bioinformatics handles increasingly complex multi-trait datasets and employs machine learning to rank progenies before field evaluation. Cloud compute delivery removes hardware barriers for smallholders, expanding the addressable user base. Continuous chemistry improvements in sequencing reduce read costs, enabling routine methylome and transcriptome profiling that feed into predictive trait networks. The plant genomics market increasingly values technology suites that integrate edits, reads, and analytics under one interface.

By Crop Type: High-Value Produce Outpaces Staples

Cereals and grains command 39.0% revenue thanks to scale, global calorie dependence, and well-funded breeding programs. Yet fruits and vegetables are surging at a 15.5% CAGR as consumers pay for flavor, shelf-life, and nutritional enhancements. Oilseeds and pulses enjoy steady demand from plant-based protein trends, while specialty crops, including medicinal plants, attract niche investment due to high per-hectare margins.

Reference genomes for wheat, rice, and maize enable rapid deployment of genomic selection at scale, whereas fruits and vegetables benefit from targeted investment in flavor chemistry and texture. Precision agriculture tools synchronized with genomic data allow variable-rate inputs calibrated to genotype-specific needs, boosting field performance and sustainability. The plant genomics market size tied to specialty crops is projected to expand as bio-industrial applications and functional foods gain momentum.

By Trait: Nutrition Commands Premium Growth

Disease resistance keeps the largest revenue slice at 37.0% as pathogen pressure rises and pesticide regulations tighten. Nutritional enhancement, advancing at 16.9% CAGR, taps consumer willingness to pay for biofortified crops rich in vitamins or improved amino-acid profiles. Herbicide-tolerant crops experience moderate growth, given resistance concerns in weed populations and stricter chemical regulations. Abiotic stress tolerance gains importance as climate variability intensifies, with drought and heat packages topping breeder wish lists.

Yield improvement work now emphasizes stability under fluctuating growing conditions rather than absolute maximum output. Stacking edits that combine stress tolerance, disease resistance, and nutrition offers synergistic value, unlocking premium segmentation in downstream food markets. The plant genomics market size attached to premium traits continues to rise as retailers add sustainability and nutrition metrics to procurement specifications.

Geography Analysis

North America generated 40.0% of 2024 revenue, anchored by established research networks, abundant venture capital, and clear regulatory pathways. The USDA Sustainable, Ecological, Consistent, Uniform, Responsible, Efficient (SECURE) rule streamlines approvals, cutting average timelines by 18 months. Public agencies allocated USD 450 million in 2024 for genomics grants, while private breeders integrated cloud pipelines into seed selection to save two breeding cycles per product release. Carbon-credit incentives further spur investment in gene-edited cover crops, aligning genomic innovation with sustainable farming programs.

Asia-Pacific posts the fastest expansion at a 14.0% CAGR as China, India, and Southeast Asia intensify food security policies. China apportioned USD 2.8 billion to agricultural biotechnology in 2024, channeling funds toward drought-resilient rice and CRISPR (Clustered regularly interspaced short palindromic repeats)-edited cash crops. India’s National Mission on Agricultural Extension and Technology promotes molecular breeding in smallholder systems, providing handheld genotyping devices to extension officers. Rising sequencing capacity in agri-biotech hubs such as Shenzhen and Bangalore bolsters local service ecosystems, lowering barriers for regional breeders.

Europe presents a sophisticated yet cautious environment. Horizon Europe distributed EUR 380 million (USD 410 million) in 2024 for sustainable crop genomics, focusing on biodiversity and low-input systems. Pending rules for new genomic techniques create uncertainty, delaying some commercial launches. Nevertheless, the region houses advanced phenotyping facilities and strong public-private partnerships. South America leverages soybean and maize acreage to justify investments in predictive breeding, while the Middle East and Africa concentrate on drought-tolerant staples using portable sequencing to bridge infrastructure gaps. Together, emerging regions represent the next wave of customer acquisition for cloud-driven platforms.

Competitive Landscape

The plant genomics market carries a moderate concentration profile. Illumina, Inc. dominates high-throughput sequencing hardware, Thermo Fisher Scientific Inc. leads in reagents and outsourced services, Eurofins Scientific advances contract research and genotyping, Agilent Technologies Inc. supplies sample-prep and bioinformatics modules, and Qiagen provides extraction kits and mid-throughput platforms.

Leading vendors now pair hardware sales with subscription analytics to defend margins. Thermo Fisher Scientific Inc. bundled cloud analytical suites with consumables to lock in recurring revenue. Illumina, Inc. introduced turnkey agrigenomics pipelines that embed crop-specific variant panels into workflow presets. Eurofins Scientific expanded genotyping capacity to capture service contracts from breeders that downsize internal labs. Agilent Technologies Inc. focuses on long-read sample prep to support reference genome improvement. Qiagen launched plant-optimized extraction spin columns that cut processing time by 30%, addressing throughput bottlenecks in seed labs.

Competition is shifting toward integrated ecosystems where users move raw reads into cloud dashboards for real-time trait prediction. Partnerships between platform suppliers and seed companies accelerate the deployment of predictive models that connect genotype to phenotype. Patents for CRISPR-based editing in staple crops climbed 45% during 2024, revealing a crowded innovation field. Service differentiation increasingly hinges on regulatory support packages and data privacy safeguards as customers weigh cross-border commercialization strategies.

Plant Genomics Industry Leaders

-

Illumina, Inc.

-

Thermo Fisher Scientific Inc.

-

Eurofins Scientific

-

Agilent Technologies Inc.

-

Qiagen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Corteva established a USD 27.5 million research and development laboratory in Midland to develop crop protection solutions and traits using genomics and molecular tools. The facility enhances Corteva's plant genomics capabilities for sustainable agriculture and precision breeding.

- January 2025: At PAG (The Plant and Animal Genome Conference) 2025, Oxford Nanopore presented advancements in telomere-to-telomere (T2T) plant genome assembly, conservation epigenomics, and biodiversity sequencing. The workshop demonstrated Corteva's progress in T2T assembly and introduced new assembly tools, including hifiasm(ONT) and MetaMDBG, which enhance plant de novo genome and metagenome assembly quality.

- July 2024: Murdoch University's Centre for Crop and Food Innovation conducted a global study on telomere-to-telomere (T2T) genome assemblies, which enabled complete mapping of crop genomes including, wheat, chickpea, banana, and papaya. This advancement supports molecular breeding for traits such as drought tolerance, salinity resistance, and pest resistance, enabling the development of new crop varieties.

Global Plant Genomics Market Report Scope

| DNA Sequencing |

| Genotyping |

| Gene Editing |

| Marker-Assisted Selection |

| Bioinformatics |

| Disease Resistance |

| Herbicide Tolerance |

| Abiotic Stress Tolerance |

| Yield Improvement |

| Nutritional Enhancement |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Technology | DNA Sequencing | |

| Genotyping | ||

| Gene Editing | ||

| Marker-Assisted Selection | ||

| Bioinformatics | ||

| By Trait | Disease Resistance | |

| Herbicide Tolerance | ||

| Abiotic Stress Tolerance | ||

| Yield Improvement | ||

| Nutritional Enhancement | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the plant genomics market?

The plant genomics market size is USD 8.5 billion in 2025 and projects to USD 15.2 billion by 2030.

Which technology grows the quickest in plant genomics applications?

Gene editing is expanding at an 18.8% CAGR as breeders deploy CRISPR workflows for commercial seed production.

Which region shows the fastest revenue growth for plant genomics tools?

Asia-Pacific records a 14.0% CAGR as governments in China and India scale biotechnology programs.

Which trait category experiences the highest growth through 2030?

Nutritional enhancement rises at a 16.9% CAGR as consumers favor biofortified crops.

Page last updated on: