Molecular Breeding Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

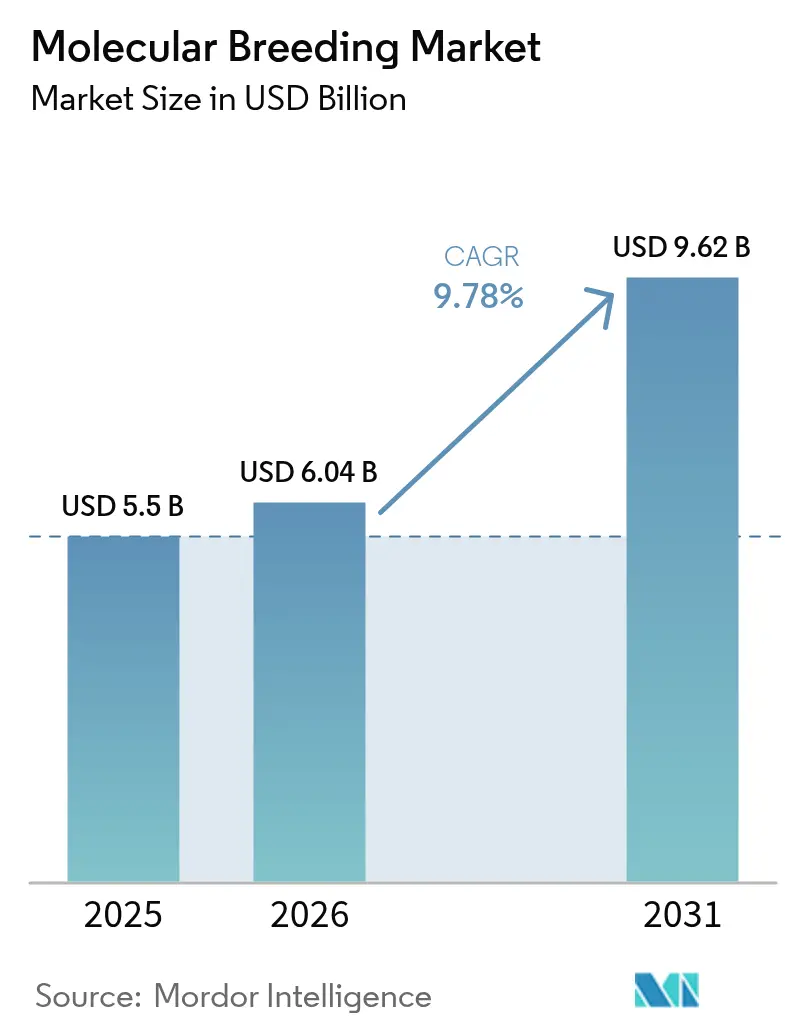

| Market Size (2026) | USD 6.04 Billion |

| Market Size (2031) | USD 9.62 Billion |

| Growth Rate (2026 - 2031) | 9.78% CAGR |

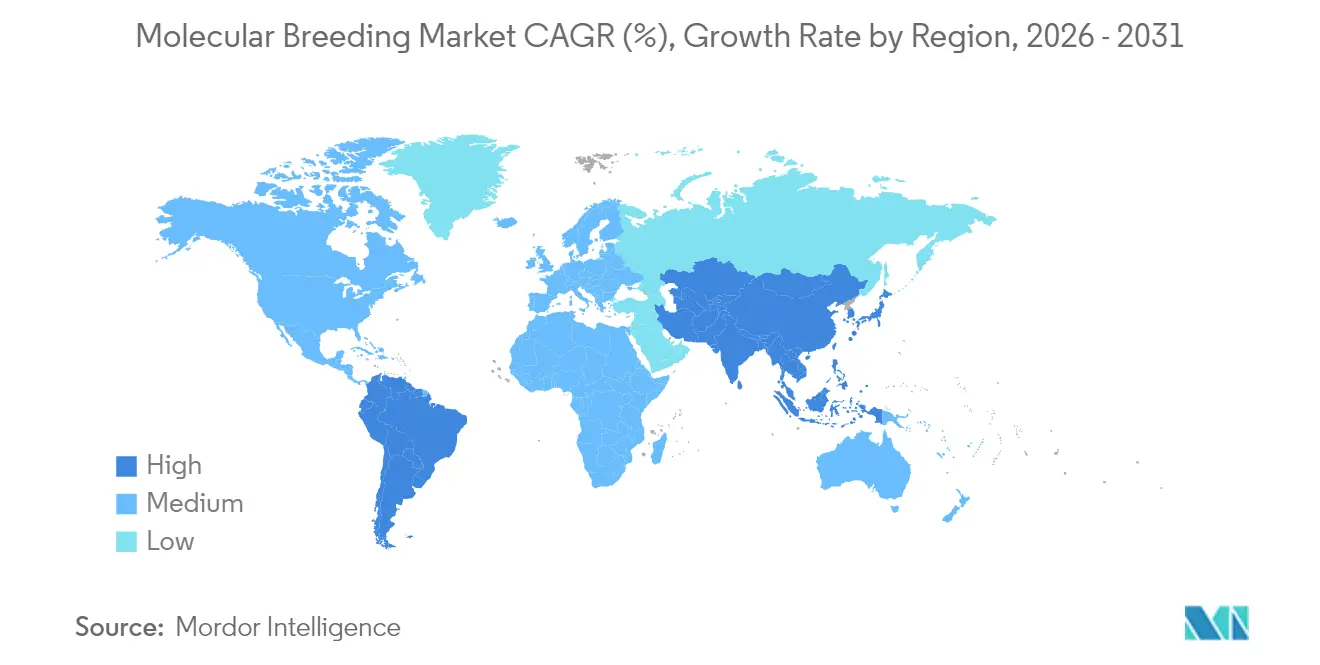

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molecular Breeding Market Analysis by Mordor Intelligence

The molecular breeding market size was valued at USD 5.5 billion in 2025 and estimated to grow from USD 6.04 billion in 2026 to reach USD 9.62 billion by 2031, at a CAGR of 9.78% during the forecast period (2026-2031). The incorporation of artificial intelligence with genomic selection has reduced breeding cycles from years to months, enhancing product development efficiency. Government initiatives, including the U.S. Vision for Adapted Crops and Soils and India's National Action Plan on Food Security, are driving demand for climate-resilient crop varieties. Market expansion is facilitated by high-throughput phenotyping, decreased sequencing costs, and accessible genotyping services. While North America retains its advantage in research infrastructure, the Asia-Pacific region demonstrates substantial growth potential due to regulatory reforms and food security requirements.

Key Report Takeaways

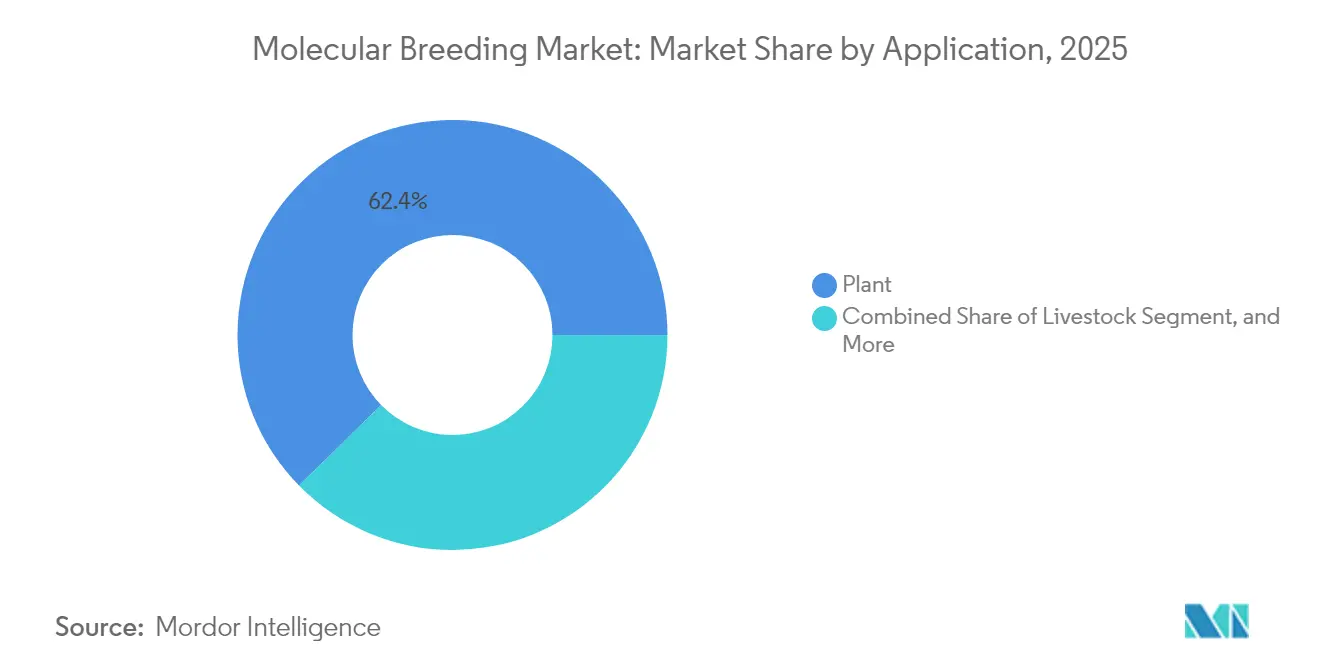

- By application, plant breeding dominated with 62.35% of the molecular breeding market share in 2025; livestock breeding is projected to grow at a 12.64% CAGR through 2031.

- By marker type, SNP technology represented 41.55% of the molecular breeding market size in 2025 and is anticipated to grow at a 12.85% CAGR.

- By breeding process, marker-assisted selection comprised 50.35% of the molecular breeding market size in 2025, while genomic selection is growing at a 15.35% CAGR.

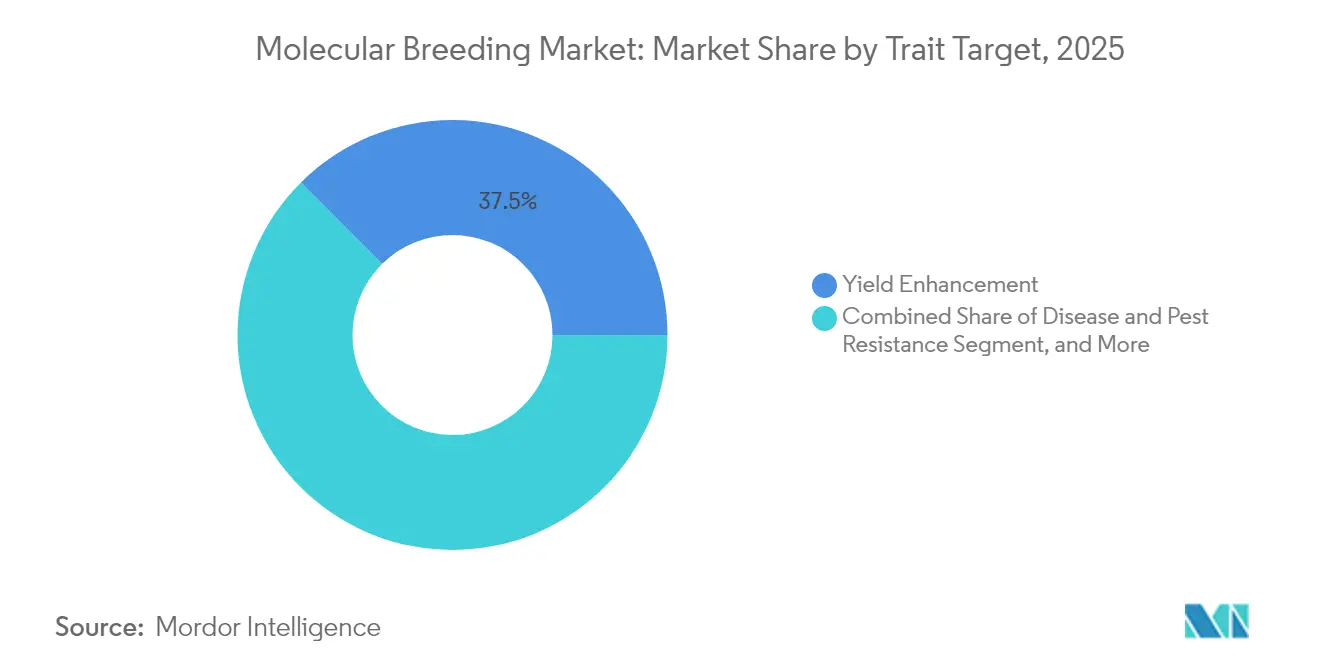

- By trait target, yield enhancement led with 37.45% revenue share in 2025; abiotic stress tolerance is projected to grow at a 11.72% CAGR through 2031.

- By end-user, seed and crop-protection companies held 51.25% revenue share in 2025; independent breeding service providers grew at a 12.58% CAGR through 2031.

- By geography, North America held a 35.55% share of the molecular breeding market in 2025, while Asia-Pacific will grow at a 11.45% CAGR through 2031.

- Major Players, Illumina Inc., Thermo Fisher Scientific, and LGC Limited (Cinven) together held 39.70% of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Molecular Breeding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding biotechnology research and development funding | +2.8% | North America and Europe | Medium term (2-4 years) |

| Growing demand for high-yield, climate-resilient crops | +2.5% | Asia-Pacific and Africa | Long term (≥ 4 years) |

| Rapid adoption of precision breeding and phenotyping platforms | +2.2% | North America and Europe | Short term (≤ 2 years) |

| Government-backed food-security initiatives | +1.8% | Developing economies | Medium term (2-4 years) |

| Convergence of AI and genomic selection | +1.4% | North America, Europe, China | Short term (≤ 2 years) |

| Carbon-credit incentives for low-input cultivars | +0.9% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Biotechnology Research and Development Funding

Private and public spending in the market is increasing rapidly. Thermo Fisher invested USD 1.3 billion in research and development in 2023 to advance next-generation sequencing and reagent innovation, reducing entry costs for midsized breeders. The U.S. Department of Agriculture's data-standards programs are harmonizing genomic datasets, preventing redundant trials, and reducing time-to-market. These capital investments have decreased compliance barriers for smaller firms, enabling novel trait developers to navigate regulatory requirements. Additionally, multilateral initiatives, such as CGIAR's USD 400 million nutrition-focused portfolio, are attracting donor funds and accelerating biofortification outcomes.

Growing Demand for High-Yield, Climate-Resilient Crops

India's release of 100-day wheat varieties capable of withstanding record temperatures has enabled heat- and drought-tolerant genotypes to advance from pilot to commercial scale. Japanese research centers are developing quinoa and soybean varieties adapted to saline and water-stress conditions to maintain production levels in climate-vulnerable countries. Plant breeding priorities now extend beyond yield optimization to include multistress tolerance, necessitating the use of multiplexed molecular markers that integrate productivity with environmental resilience. The financial implications are significant, as extreme weather events currently cause crop losses worth billions of USD per season, increasing the return on investment for climate-resilient seed portfolios.

Rapid Adoption of Precision Breeding and Phenotyping Platforms

High-throughput imaging and sensor systems enable non-destructive trait measurement and, combined with machine learning, allow breeders to conduct multiple crop generations annually in controlled environments. Syngenta laboratories integrates AI to optimize molecular design and bioassay cycles for seeds and crop-protection molecules, reducing development timelines significantly. The emergence of phenomics-as-a-service models provides regional breeders with limited capital access to these technologies, driving market adoption.

Government-Backed Food Security Initiatives

Programs such as India's National Food Security Mission provide substantial grants for breeder seed multiplication, ensuring rapid adoption of molecular-bred cultivars.[1]National Food Security Mission, “Allocations 2024-25,” nfsm.gov.in Australia's regional partnerships offer grants and technical training on climate-ready varieties across the Indo-Pacific, converting policy commitments into commercial demand. USDA grants for sweet-potato research in Pacific Island nations demonstrate how dedicated budgets reduce local research and development risks while addressing nutrition gaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent, slow-moving regulatory approvals | −1.8% | Europe | Long term (≥ 4 years) |

| High capital cost of sequencing and genotyping infrastructure | −1.2% | Developing economies | Medium term (2-4 years) |

| Limited breeder access to interoperable data platforms | −0.9% | Global | Medium term (2-4 years) |

| Public perception concerns over “molecular‐modified” seeds | −0.7% | Europe and parts of Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent, Slow-Moving Regulatory Approvals

The compliance cost per new trait can reach USD 15 million, consuming approximately half of the total development budgets and deterring smaller innovators. The European Union's regulation of gene-edited crops under GMO legislation drives companies to focus on markets with favorable regulations, such as the United States and Brazil. While Argentina, Uruguay, and Thailand updated their regulations in 2024 to simplify approvals, regulatory uncertainty continues to extend timelines and increase financing costs.

High Capital Cost of Sequencing and Genotyping Infrastructure

Sequencers and high-density SNP arrays remain cost-prohibitive for many public institutes. In several low-income economies, biosafety compliance costs exceed national breeding-program budgets, reinforcing reliance on imported germplasm. Shared facilities and contract-genotyping models are emerging, but their availability remains limited outside major research hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Livestock Segment Accelerates Despite Plant Dominance

Plant applications accounted for 62.35% of the molecular breeding market in 2025, primarily through genomic selection implementation in maize, wheat, and soybean breeding programs. The livestock segment is experiencing growth at a 12.64% CAGR, driven by genomic breeding values that demonstrate superior performance compared to traditional estimates in dairy cattle and CRISPR-based disease-resistant pig development. Tools such as Angus SteerSELECT have demonstrated prediction accuracies exceeding 0.72 for critical carcass traits, enhancing feedlot profitability and attracting investment.

The poultry sector is implementing precision editing of fertility and growth genes to reduce generation intervals. Furthermore, integrated metabolomic and genomic models in swine breeding demonstrate potential for improving average daily gain, despite current modest outcomes. These developments indicate that the livestock segment may substantially increase its contribution to the molecular breeding market by 2031.

By Marker Type: SNP Technology Dominates Through Superior Precision

Single nucleotide polymorphisms (SNPs) accounted for 41.55% of the molecular breeding market size in 2025 and maintain a 12.85% CAGR due to their compatibility with high-throughput platforms and enhanced genome-wide association outputs. The reduction in unit costs has diminished the price advantage previously held by simple sequence repeats, prompting developing-country programs to adopt SNP solutions directly. The implementation of functional-variant panels from RNA-seq and ATAC-seq data has improved breeding accuracies by 3 percentage points in dairy-protein traits, demonstrating the technology's reliability.

The standardization of SNP workflows has positioned express sequence tags and other traditional markers primarily in specialized applications such as expression profiling. The increased adoption of SNPs enhances data interoperability, which is fundamental for developing AI-enabled breeding systems.

By Breeding Process: Genomic Selection Revolutionizes Traditional Methods

Marker-assisted selection maintains a 50.35% revenue share in 2025, demonstrating its established effectiveness for single-gene traits. Genomic selection exhibits robust growth with a 15.35% CAGR, attributed to its capabilities in managing complex traits such as drought tolerance and nutrient-use efficiency. Companies such as Benson Hill integrate genomic selection with speed-breeding protocols to generate multiple soybean generations annually, reducing product development timelines.

Quantitative trait-loci mapping and marker-assisted back-crossing maintain their significance where trait architecture is well-defined, although their growth rate is moderating. The integration of machine learning with genomic selection is projected to enhance performance differentials, establishing it as the primary methodology in commercial breeding programs.

By Trait Target: Abiotic Stress Tolerance Gains Prominence

Yield enhancement maintained its dominant position at 37.45% market share in 2025, while abiotic-stress tolerance emerged as the fastest-growing segment with a 11.72% CAGR. The development of extreme-weather resilience and soil salinity tolerance has become a strategic priority in breeding programs, as evidenced by India's development of heat-resistant wheat varieties and China's salt-tolerant rice prototypes. Disease and pest resistance continues to generate sustained demand, driven by the transition toward biological control methods to reduce chemical inputs. Furthermore, micronutrient biofortification is experiencing increased consumer interest.

Modern breeding programs are integrating multiple traits - combining yield enhancement, stress tolerance, and nutritional improvements within single varieties. This integration utilizes advanced techniques such as multiplexed CRISPR editing and polygenic scoring to minimize trait trade-offs, establishing new standards for product differentiation.

By End-User: Independent Providers Challenge Traditional Dominance

Seed and crop-protection companies maintain 51.25% of spending in 2025 through established distribution networks and comprehensive IP portfolios. Independent breeding service providers demonstrate growth at 12.58% CAGR, delivering contract genotyping, AI analytics, and trait-discovery services to regional seed firms. Livestock genetics companies increase investments as genomic evaluation systems advance.

Academic and government institutes maintain their essential role in pre-competitive research, though commercial limitations affect their direct revenue share. Market consolidation persists as agribusinesses acquire biotech firms to obtain proprietary algorithms and marker panels, reflecting the strategic importance of data-driven capabilities.

Geography Analysis

North America holds 35.55% of the molecular breeding market share in 2025, supported by advanced research infrastructure and efficient regulatory frameworks. Illumina reported USD 4.33 billion revenue in 2024 and has partnered with LGC Biosearch Technologies to increase targeted genotyping-by-sequencing capabilities for row-crop and livestock segments. The USDA's SECURE rule streamlines the approval process for gene-edited products, maintaining the region's market leadership.

Asia-Pacific demonstrates the highest growth potential with a projected 11.45% CAGR through 2031. China approved disease-resistant gene-edited wheat in 2024, while India's regulatory updates streamline approvals for specific genome edits, accelerating private breeding initiatives. Japan's tiered regulatory system and focus on crop-stress research establishes it as a key regional hub. The combination of government funding and private venture capital is strengthening the region's breeding infrastructure to address food security needs.

Europe maintains significant market presence despite regulatory constraints. The EU Environment Committee's approval of new genomic technology legislation in late 2024 indicates movement toward risk-based assessment. The UK implemented the Precision Breeding Act, establishing a two-tier safety review system to expedite gene-edited crop trials. Switzerland is implementing similar regulatory changes. Market growth depends on policy developments, with substantial demand for varieties meeting European Green Deal sustainability requirements.

Regulatory Landscape

Regulation remains shaped by divergent national approaches to gene editing and other new genomic techniques, which affects where molecular breeding programs commercialize and how they substantiate marker and trait claims. In the European Union, the regulatory environment shifted in 2026 with a tiered framework for plants obtained by certain New Genomic Techniques (NGTs): the Council of the European Union adopted its position at first reading in April 2026, and the European Parliament provided final legislative approval in June 2026. The framework separates NGT plants into Category 1 (treated as equivalent to conventional) and Category 2 (subject to a more flexible authorization and monitoring pathway than traditional GMO rules), while North America continues to rely on comparatively streamlined pathways for certain gene-edited products, including the USDA SECURE rule referenced in the report context, reinforcing regional differences in time-to-market.

At the international level, Codex Alimentarius continues to function as an important reference point for food safety and trade alignment as molecular-bred products enter cross-border supply chains. The Codex Alimentarius Commission held its 49th session in July 2026, where biotechnology and food safety assessment topics remained part of the global standards agenda. For companies and breeding programs operating across multiple markets, the combination of evolving EU NGT rules and ongoing Codex work increases the need for region-specific compliance strategies, traceability-ready documentation, and data packages that support safety assessments, given how market access requirements vary across jurisdictions.

Competitive Landscape

The molecular breeding market demonstrates moderate concentration, with the top five sequencing providers - Illumina Inc., Thermo Fisher Scientific, LGC Limited (Cinven), Eurofins Scientific, and SGS SA - accounting for 40.1% of revenue share in 2024. Research and development investments function as a primary strategic tool, as evidenced by Thermo Fisher's USD 1.3 billion budget in 2023 for platform innovations to reduce the cost per datapoint.

Strategic partnerships are expanding in the market. Illumina's collaboration with LGC integrates Amp-Seq protocols with high-throughput sequencing for cost-efficient marker panels. Bayer maintains an innovation pipeline valued at USD 37.1 billion (EUR 32 billion) in peak sales, incorporating artificial intelligence, gene editing, and herbicide-tolerance stacks. Syngenta implements machine learning across its processes, from molecular design to greenhouse validation, to optimize efficiency.

Specialized companies such as Pairwise and MolBreeding Biotech concentrate on specific innovations, such as CRISPR berries and Genotyping-by-Targeted-Sequencing, establishing market niches despite the presence of large companies. The increasing requirement for data in AI applications has established proprietary multi-omics datasets as a competitive advantage, leading to an increase in data-focused acquisitions.

Molecular Breeding Industry Leaders

Illumina, Inc.

Thermo Fisher Scientific Inc.

LGC Limited (Cinven )

Eurofins Scientific

SGS SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The convergence of AI, high-throughput phenotyping, and genomic selection is expanding opportunities to shorten breeding cycles and improve selection accuracy, especially for complex traits tied to climate resilience and architecture-driven yield. Evidence from 2026 also points to measurable performance gains from molecular approaches: a Nature Genetics study (March 2026) reported pyramiding of validated architecture-regulating alleles in parental lines of the maize hybrid Yufeng303, delivering 4.1% to 9.2% higher plot yields across eight environments. This supports ongoing demand for scalable marker workflows, including SNP panels and targeted genotyping-by-sequencing, as well as for service providers that can combine genotyping throughput with robust analytics.

A second opportunity sits in multi-trait stacking and improved trait deployment workflows that reduce iteration cycles between design and validation. Research reported in 2026 points to more integrated development loops, including frameworks that connect AI models with genome editing datasets (Molecular Plant, April 2026), and newer genome engineering approaches for site-specific, large-fragment integration that support multigene stacking (Nature Biotechnology, June 2026). Because regulatory requirements differ by geography, commercial whitespace is more visible for programs and vendors that can produce compliant, audit-ready data and interoperable datasets across environments, particularly where phenomics-enviromics integration helps address genotype-by-environment effects using satellite and vehicle-based sensing with AI-assisted modeling (Nature Communications, June 2026).

Recent Industry Developments

- June 2026: The European Parliament granted final legislative approval for the European Union framework on plants obtained by certain New Genomic Techniques (NGTs), introducing a tiered approach that differentiates Category 1 NGT plants from more complex Category 2 cases. This clarification improves the practical alignment between breeding innovation and market authorization pathways in Europe, where regulatory timelines have been a key bottleneck for commercial deployment of molecular-led trait pipelines.

- September 2025: LGC Limited partnered with Genolution to accelerate high-throughput nucleic acid purification for agrigenomics applications. Scaling automated sample prep helps reduce turnaround times and per-sample costs for breeding programs that depend on routine, large-volume genotyping to run marker-assisted selection and genomic selection cycles.

- September 2024: Illumina and LGC Biosearch Technologies announced a strategic partnership to advance agricultural genotyping-by-sequencing, combining LGC's Amp-Seq methodology with Illumina sequencing platforms, with emphasis on Asia-Pacific and Latin America. The collaboration broadened access to targeted GBS workflows that support cost-efficient marker panels, strengthening service capacity for crop and livestock breeding users outside the largest research hubs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from tools, consumables, instruments, and service support used to apply DNA-level information in breeding decisions for plants and livestock, where molecular markers and genomic data guide selection and trait improvement.

Scope exclusions: We exclude standalone gene-editing inputs, generic sequencing sold outside breeding programs, and broad discovery-only bioinformatics platforms.

Segmentation Overview

- By Application

- Plant

- Livestock

- Other Application

- By Marker Type

- Simple Sequence Repeats (SSR)

- Single Nucleotide Polymorphisms (SNP)

- Expressed Sequence Tags (EST)

- Other Markers

- By Breeding Process

- Marker-Assisted Selection (MAS)

- Quantitative Trait Loci (QTL) Mapping

- Marker-Assisted Back-Crossing

- Genomic Selection

- By Trait Target

- Yield Enhancement

- Disease and Pest Resistance

- Abiotic Stress Tolerance

- Quality and Nutritional Traits

- By End-User

- Seed and Crop-Protection Companies

- Livestock Breeding Firms

- Academic and Government Research Institutes

- Independent Breeding Service Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping what is actually purchased in molecular breeding workflows, then linking those activities to observable demand signals. Public sources such as USDA and Economic Research Service releases, FAOSTAT crop and livestock series, OECD agriculture indicators, and UPOV variety and plant breeder rights references helped us anchor adoption and crop mix assumptions. Where relevant, we also checked peer-reviewed genetics and breeding journals to confirm how quickly marker types and genomic selection are being used in mainstream programs.

To keep revenues realistic, we reviewed company annual reports, investor decks, and product catalogs to understand how offerings are packaged (kits, reagents, platforms, and service contracts), and to identify typical customer groups. We also used paid subscriptions for company financials and intelligence, patent databases, and import-export shipment-level checks where trade flows were informative for instruments and consumables. These desk sources are illustrative only, and many other public references and documents were also used to collect, verify, and clarify data points.

Primary Interviews and Surveys

Primary discussions were run with a mix of breeding program heads, lab managers, product specialists, and commercial leaders to clarify what is being bought, how often it is replenished, and which steps are kept in-house versus outsourced. For a global view, input was balanced across major breeding geographies so pricing, adoption pace, and procurement cycles could be checked against local crop priorities and research funding patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 38% |

| Mid tier: 55% | Functional/Unit leaders: 24% | EMEA: 36% |

| Smaller Players: 16% | Managers: 60% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built mainly from a top-down demand pool, where crop area and breeding intensity indicators are used to reconstruct the likely volume of genotyping and marker workflows that translate into spend. The model then applies practical spend factors across the workflow, including marker type mix (for example SNP versus SSR usage), sample throughput per program, instrument installed-base replacement cycles, and the share of outsourced versus internal lab work.

Once the first cut is built, selective bottom-up checks are used to keep totals grounded, such as roll-ups from a sample of supplier revenues, channel feedback on consumables pull-through, and simple ASP times volume logic for common assays. Forecasting uses scenario analysis supported by expert consensus on the pace of genomic selection adoption, public and private breeding budgets, regulatory stance on breeding technologies, and expected improvements in turnaround times that influence testing frequency. When revenue is hard to see directly for smaller or mixed business units, gaps are handled with proportional allocation based on product mix cues, regional presence, and interview-validated usage rates.

Data Validation & Update Cycle

Outputs are checked against independent signals such as agriculture R&D funding direction, breeding pipeline activity, and equipment and consumables demand patterns that should move with genotyping intensity. If a region or application shows a jump that cannot be explained by area, budget, or adoption logic, the inputs are re-checked and the assumptions are reviewed again before sign-off.

A multi-step internal review is used so definitions, math, and year-over-year movements stay consistent across the model. The report is refreshed annually, and interim updates are triggered when material events occur (for example major policy shifts, sharp currency moves, or step-changes in technology adoption). Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Molecular Breeding Market Size Versus Other Published Estimates

Published market values for molecular breeding can differ even when the topic name looks the same, because the counted revenue lines are not always consistent and the time window is set differently. In our review, the largest swings usually came from how far upstream or downstream the definition goes, and whether the estimate is tied to breeding program spend or to broader genomics activity.

By tracking assay and marker workflow demand drivers and refreshing currency timing and scope boundaries each update, Mordor Intelligence keeps the number focused on molecular breeding enablement spend rather than pulling in unrelated discovery genomics or standalone gene-editing inputs. Another common gap driver is how services are treated, since some estimates bundle wide bioinformatics services or grant-funded activity into the same pot, and then growth rates get pushed higher by aggressive adoption assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.04 B (2026) | |

| Global Consultancy A | USD 4.02 B (2025) | Uses a different base year and a wider growth arc to 2034, and the scope appears to lean more toward broader genomics and breeding technology activity, which can understate or overstate the breeding-specific spend depending on what is bundled. |

| Industry Publisher B | USD 4.85 B (2025) | Includes genotyping plus broader bioinformatics services and counts some non-commercial funding flows, which can shift the market boundary versus a purchase-led view of instruments, reagents, consumables, and service contracts tied to breeding decisions. |

Across the table, the spread is mainly explained by what gets counted as molecular breeding spend and which year is treated as the starting point. When the boundary is kept close to breeding workflows and checked with practical usage and pricing inputs, the estimate becomes easier to replicate and to audit over time.

Key Questions Answered in the Report

What is the current size of the molecular breeding market?

The molecular breeding market was valued at USD 6.04 billion in 2026 and is forecast to reach USD 9.62 billion by 2031.

Which region is growing the fastest?

Asia-Pacific is anticipated to post a 11.45% CAGR through 2031, propelled by regulatory reforms in China and India that speed up gene-edited crop approvals.

Why are SNP markers so dominant?

SNPs combine high precision with compatibility for high-throughput sequencing, giving them 41.55% share of 2025 revenues and a 12.85% growth trajectory.

How is AI impacting breeding timelines?

AI-enabled genomic selection has shortened breeding cycles from five years to as little as four months, significantly accelerating product launches.

What restrains wider technology adoption?

High regulatory compliance costs and capital-intensive sequencing infrastructure remain key barriers, particularly for smaller firms and developing-country programs.

Which traits are attracting the most investment?

Yield enhancement remains lucrative, but abiotic stress tolerance is the fastest-growing trait focus as climate resilience becomes a commercial imperative.

Page last updated on: