Plant Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

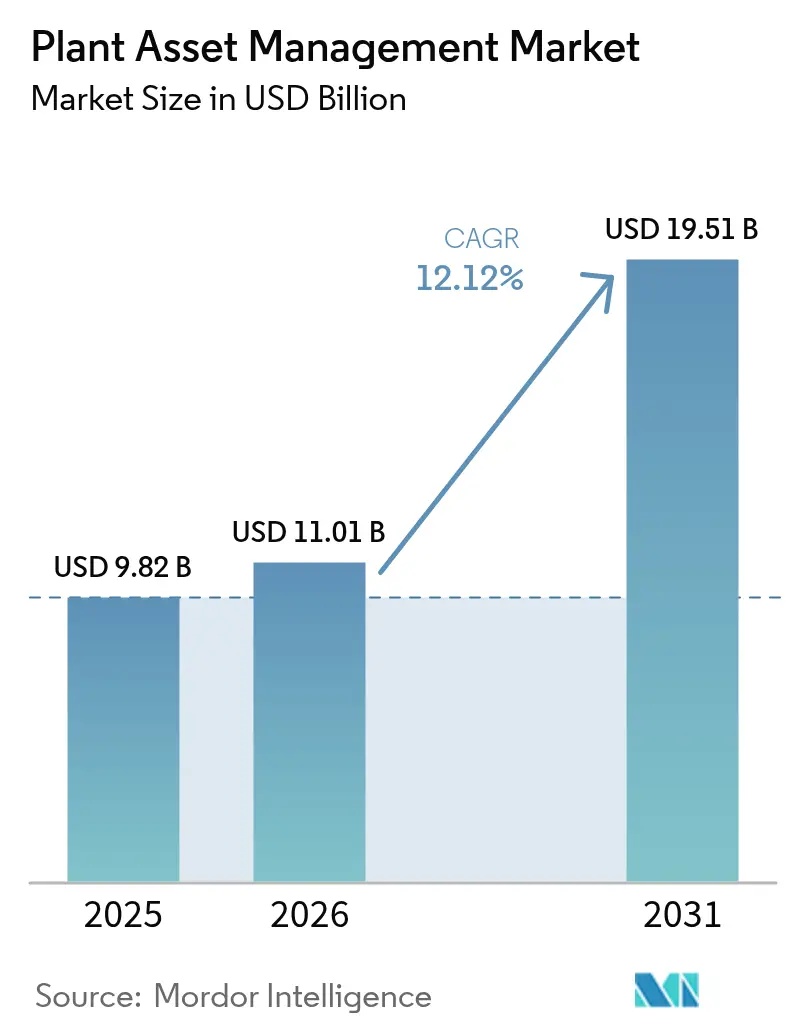

| Market Size (2026) | USD 11.01 Billion |

| Market Size (2031) | USD 19.51 Billion |

| Growth Rate (2026 - 2031) | 12.12% CAGR |

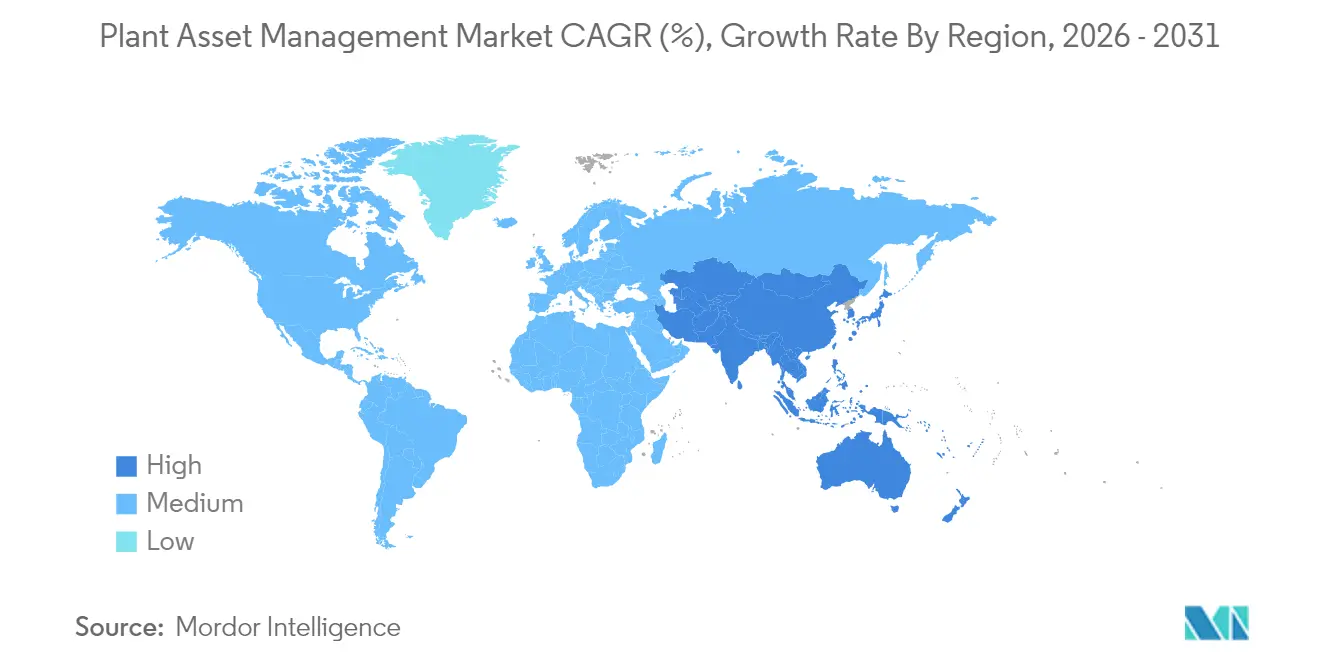

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

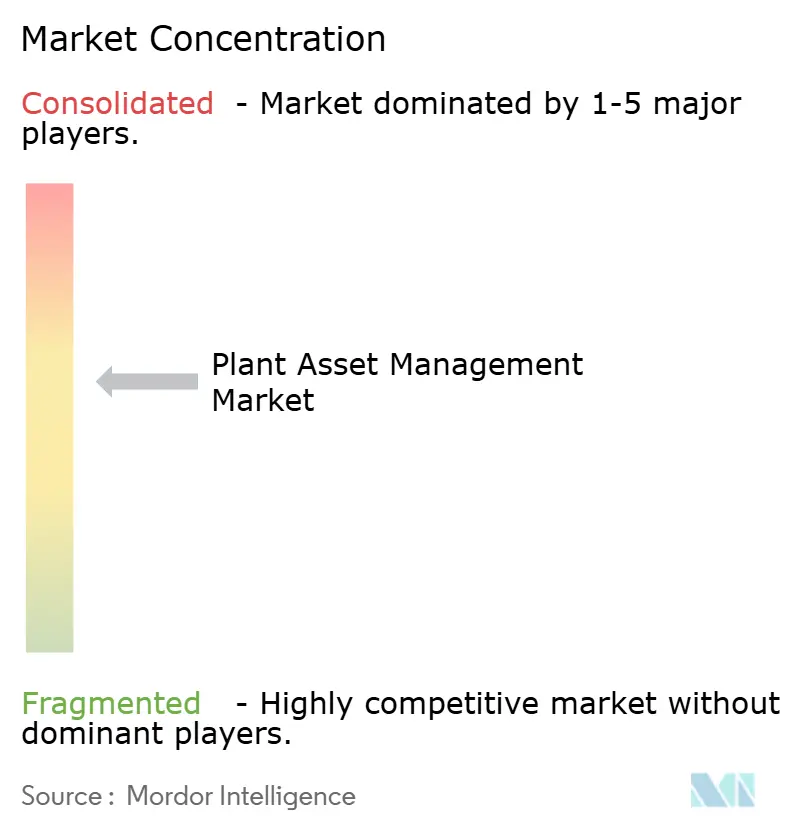

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plant Asset Management Market Analysis by Mordor Intelligence

The plant asset management market size is expected to grow from USD 9.82 billion in 2025 to USD 11.01 billion in 2026 and is forecast to reach USD 19.51 billion by 2031 at 12.12% CAGR over 2026-2031. Expanding demand stems from industrial digitalization programs, stricter safety and sustainability rules, and the urgent need to improve aging electrical and mechanical infrastructure. Private 5G pilots, such as Korea Electric Power Corporation’s wireless IoT network for real-time substation monitoring, illustrate how ultra-low-latency connectivity is broadening asset visibility and shortening intervention cycles[1]Korea Electric Power Corporation, “Substation IoT and Robot Monitoring Trial,” kepco.co.kr. Software platforms hold sway as firms shift from reactive to predictive maintenance, while hybrid cloud designs alleviate data-sovereignty fears and speed analytics deployment. Rapid growth in services mirrors the scarcity of skilled reliability engineers and the complexity of integrating decades-old operational technology with new analytics layers. Regionally, North America keeps the lead thanks to mature infrastructure and tight environmental enforcement, but Asia-Pacific is scaling fastest as renewables, manufacturing expansion, and government-backed digital factories converge.

Key Report Takeaways

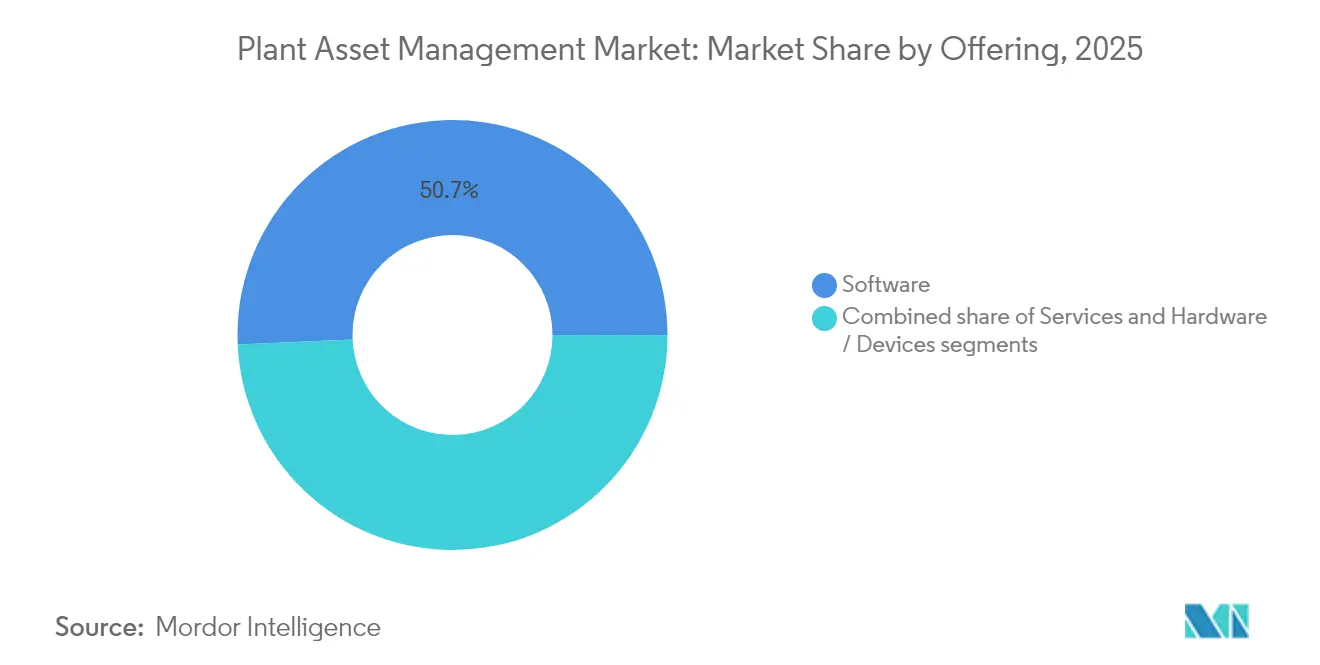

- By offering, software retained 50.70% revenue share in 2025; services are advancing at a 12.74% CAGR to 2031.

- By deployment, on-premise models held 53.20% of the plant asset management market in 2025, whereas cloud platforms are growing at 13.05% CAGR to 2031.

- By asset type, electrical assets captured 43.10% of plant asset management market share in 2025; rotating equipment is forecast to expand at 12.58% CAGR through 2031.

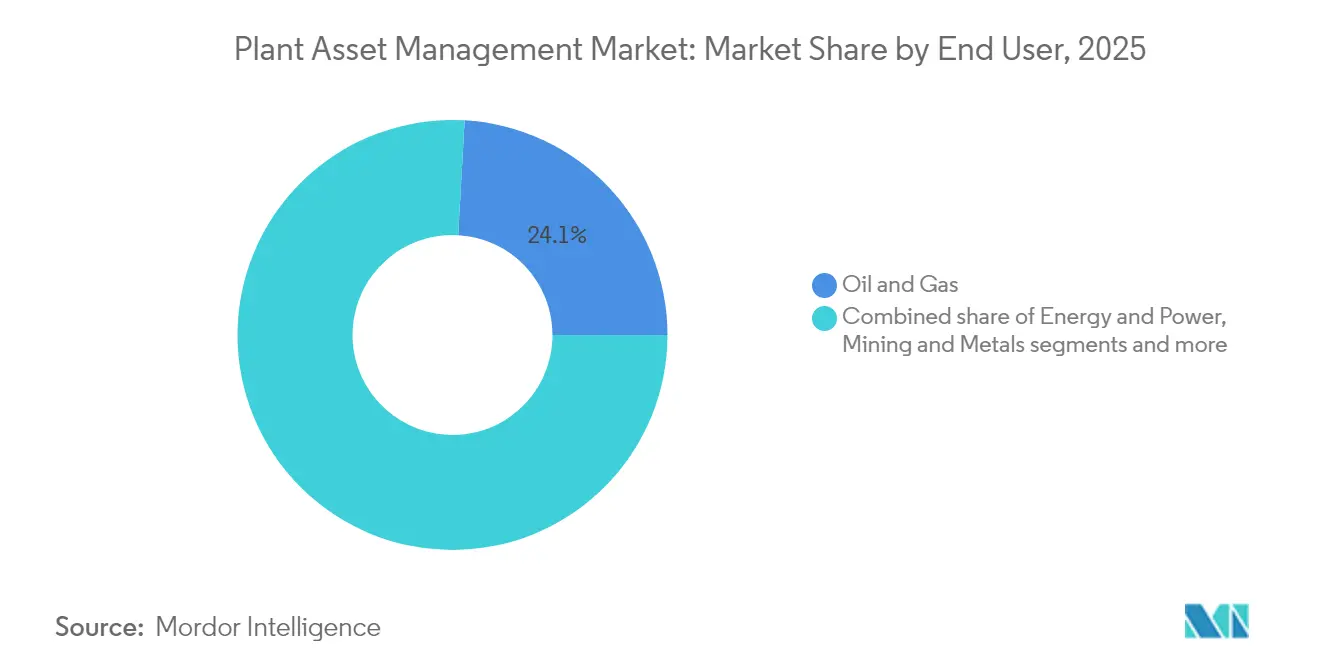

- By end user, oil and gas led with 24.10% plant asset management market share in 2025; mining and metals is the fastest riser at 12.34% CAGR to 2031.

- By organization size, large enterprises owned 71.80% of 2025 revenues, yet SMEs are growing at 13.02% CAGR to 2031.

- By region, North America accounted for 40.80% of 2025 sales; Asia-Pacific is on track for 12.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Plant Asset Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IIoT-enabled real-time analytics adoption | +2.8% | Global, APAC leadership | Medium term (2-4 years) |

| Growth in predictive and prescriptive maintenance programs | +2.5% | North America and EU, spreading to APAC | Short term (≤ 2 years) |

| Digital-twin integration across brownfield plants | +2.1% | Global, energy‐sector focus | Long term (≥ 4 years) |

| Stringent safety and environmental compliance mandates | +1.8% | North America and EU | Medium term (2-4 years) |

| Private 5G networks for asset data | +1.6% | APAC core | Long term (≥ 4 years) |

| Edge-AI sensors lowering monitoring cost | +1.5% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IIoT-enabled Real-time Analytics Adoption

Continuous sensor streams lift overall equipment effectiveness by 30% in plants that marry IIoT devices with edge computing, enabling millisecond-level anomaly detection and swift operator response[2]Siemens AG, “Senseye Predictive Maintenance Success Stories,” siemens.com. Large manufacturers record 15% cost savings by removing manual inspections and triggering predictive tasks automatically. Pairing AI with IIoT yields self-diagnosing assets that schedule repairs without human input, a pivotal shift for facilities facing an aging asset base. These benefits are tempered by data-interoperability gaps and fresh cybersecurity risks when operational networks connect to IT domains. Standardized protocols and zero-trust architectures are therefore gaining board-level attention to support wider IIoT rollout.

Growth in Predictive and Prescriptive Maintenance Programs

Early adopters tally 5:1 to 10:1 returns on predictive projects as unplanned downtime plummets and maintenance windows shrink. Transitioning from time-based to condition-based routines extends asset lifespans by up to 40% and cuts maintenance spend by 18-25%. Prescriptive analytics now takes the baton by suggesting optimal fixes and scheduling them for minimal disruption. Accuracy gains reduce false alarms that once eroded technician trust, while falling sensor prices and pay-per-use cloud models lower barriers for newcomers. Plants achieving holistic programs report 50% fewer breakdowns and double-digit gains in asset availability.

Digital-twin Integration Across Brownfield Plants

Ninety-six percent of surveyed executives see significant value from digital twins that replicate equipment behaviour and stress-test scenarios in software rather than on the factory floor. Firms document 19% cost cuts and comparable revenue boosts by optimizing capacity and supply-chain flows within the twin. Aerospace leaders employ the concept for design validation and flight scenario simulation, and the energy sector uses twins to balance throughput, safety, and emissions in aging refineries. Adoption hurdles arise around data continuity and high-speed connectivity, especially where decades-old control systems lack digital interfaces. Standard frameworks and modular component libraries are being forged to streamline future rollouts.

Stringent Safety and Environmental Compliance Mandates

The US Environmental Protection Agency’s FY 2025 plan accelerates enforcement actions that hinge on continuous emissions data and predictive risk models. Parallel requirements under the EU Corporate Sustainability Reporting Directive demand granular asset-level monitoring that feeds verified sustainability metrics. Firms now integrate safety and environmental parameters directly into plant asset management market platforms, avoiding fines that can reach seven figures. Unified dashboards consolidate condition, energy, and compliance data, letting operators demonstrate adherence in real time. These mandates are motivating investments that also yield productivity benefits, aligning operational excellence with regulatory duty.

Private 5G Networks for Ultra-low-latency Asset Data

Industrial 5G trials deliver sub-10 millisecond round-trip times, supporting mobile robots and high-frequency sensor arrays in harsh environments[3]NTT DATA, “Private 5G Managed Security Service Launch,” ntt-data.com. Energy utilities and semiconductor fabs deploy local spectrum to guarantee deterministic connectivity where Wi-Fi falters. Vendors bundle 5G with edge computing nodes, letting mission-critical analytics run on-site while archiving reports to the cloud. Spectrum costs and specialized radio skills initially confined uptake to large enterprises, yet managed-service models are now targeting SMEs. As regulation clarifies local licensing and device certification, private 5G is expected to become a backbone for next-generation asset orchestration.

Edge-AI Sensors Driving Cost-effective Monitoring

Custom silicon and energy-efficient neural networks enable sensors that both measure and analyse vibration, temperature, or acoustics locally, flagging abnormal patterns in real time. Such devices eliminate bandwidth overload by transmitting only exception data, lowering the total cost of ownership by up to 40% compared with streaming raw waveforms. Battery-powered nodes simplify retrofits on rotating machines where cabling is prohibitive. Wider use hinges on secure firmware updates and cross-vendor data models that ensure compatibility with broader analytics stacks. As standards mature, edge-AI sensing is set to permeate every level of the plant asset management market.

Restraints Impact Analysis of Plant Asset Management Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and ROI uncertainty | –1.9% | Global, notably SMEs | Short term (≤ 2 years) |

| Shortage of domain-skilled reliability engineers | –1.4% | North America and EU | Medium term (2-4 years) |

| Cyber-security and data-sovereignty concerns | –1.1% | Global | Medium term (2-4 years) |

| Legacy OT protocol fragmentation | –0.8% | Mature industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and ROI Uncertainty

Full-featured systems can surpass USD 1 million per site when sensors, gateways, licences, and training are bundled, a daunting outlay for many SMEs. Although documented ROI ranges from 5:1 to 10:1, payback can straddle several budget cycles, complicating approvals. Outcome-based services that shift expenditure to operating budgets are gaining traction, with vendors guaranteeing uptime or energy-savings thresholds. Phased pilot-to-scale strategies also soften risk, enabling proof points before enterprise rollouts. Growing availability of rental sensors and subscription analytics is therefore pivotal for widening participation in the plant asset management market.

Shortage of Domain-skilled Reliability Engineers

Manufacturing had more than 600,000 vacancies in 2025, and maintenance roles are especially pressured because they demand both mechanical acumen and data literacy. Retirements outstrip new entrants, forcing 22% of firms to outsource maintenance or rely on OEM service contracts. Training academies, digital twins for virtual upskilling, and augmented-reality work instructions are partial salves. Vendors that bundle consulting and 24/7 monitoring fill the competency gap, but wage pressure heightens cost structures for all players.

Cyber-security and Data-sovereignty Concerns

Asset data is converging with enterprise IT, widening the attack surface. Industrial ransomware events rose 50% year-on-year in 2024, pushing insurers to demand proof of zero-trust architectures and real-time threat monitoring. Jurisdictions such as the EU apply strict rules on exporting operational data, prompting hybrid deployments where raw telemetry stays on-site. Certification schemes like IEC 62443 are becoming procurement prerequisites, and platforms now integrate anomaly-detection engines fine-tuned for OT traffic patterns.

Legacy OT Protocol Fragmentation Inflating Integration Cost

Plants often host dozens of field-bus and proprietary protocols that pre-date Ethernet. Mapping this heterogeneity into a unified data model drives up project hours and middleware licence fees. Edge gateways with protocol conversion help, yet vendor lock-in risks persist. Open-source data brokers and OPC UA adoption are slowly improving interoperability, but brownfield refits still consume the lion’s share of integration budgets. Standardisation roadmaps featured prominently in recent industry consortium charters, a promising step toward lower integration barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Plant Asset Management Market Segment Analysis

By Offering:

Services Accelerate Despite Software DominanceSoftware commanded 50.70% of revenue in 2025 as enterprises anchored reliability programs around condition monitoring dashboards, asset performance management suites, and analytics engines. Implementation complexity and skill shortages are propelling services at 12.74% CAGR, the fastest growth in the plant asset management market. Consulting, integration, and training projects remain prime revenue streams because each brownfield site brings distinct control architectures that demand bespoke data pipelines. SME clients prefer outcome-based contracts that tie fees to uptime or energy-savings milestones, lowering risk and securing internal buy-in. Vendors increasingly package hardware, software, and advisory expertise to differentiate in crowded bids. AI-infused sensors that perform on-board analytics are nudging hardware revenues upward, yet the largest profit pools still derive from recurring software licences and long-term service agreements that cement customer stickiness.

Integrated solutions catalyse OEM strategies: Emerson noted 48% annual expansion in software and control solutions in FY 2024, lifting those lines to 30.5% of its total turnover. Such traction underscores the shift toward converged stacks that shave integration time and ease security assurance. As domain-specific AI models mature, software teams are embedding cause-analysis libraries that let technicians troubleshoot failures faster, reinforcing the software segment’s primacy within the plant asset management market.

By Deployment:

Cloud Gains Ground Despite On-premise LeadershipOn-premise deployments retain 53.20% market share because many industrial clients insist on local governance for operational data and require deterministic response times unattainable over wide-area links. Yet cloud subscriptions are clocking 13.05% CAGR as policymakers clarify data-residency rules and hyperscalers roll out regional zones with industry-specific controls. Hybrid designs lead the plant asset management market size calculations for new projects; companies stream raw telemetry to edge nodes for instant processing, then batch insights to cloud repositories for fleet-level optimisation. This pattern pairs latency-critical control with elastic analytics that would otherwise overwhelm on-site infrastructure budgets.

Private 5G networks deepen the attraction of distributed architectures by connecting thousands of mobile or hard-to-reach assets without the interference and roaming issues that hobble Wi-Fi. Energy, oil, and gas players still lean toward air-gapped or DMZ-secured systems due to stringent safety audits, whereas discrete manufacturers gravitate to SaaS suites that minimise capex. Over the forecast horizon, multisite enterprises are expected to refactor legacy installs into cloud-connected nodes, unlocking benchmarking insights across geographies and boosting vendor opportunities for advanced analytics modules.

By Asset Type:

Rotating Equipment Momentum BuildsElectrical assets attracted 43.10% of 2025 revenues because power failures can cascade across entire plants, jeopardising safety and production quotas. Rotating equipment, however, is scaling fastest at 12.58% CAGR, propelling a notable slice of the plant asset management market size toward vibration, acoustic, and thermographic sensing. Edge-AI chips analyse waveform signatures on the motor casing, spotting misalignment or lubrication faults hours earlier than human rounds. These early warnings let operators plan repairs during scheduled stops instead of halting production, a boon for continuous-process industries.

Fixed equipment such as pressure vessels and heat exchangers remains vital; digital twins simulate fatigue and corrosion rates, guiding maintenance capital over long horizons. Instrumentation health monitoring also gains momentum as smart valves, flowmeters, and pressure transmitters periodically self-diagnose, guarding against measurement drift that could skew control loops. Vendors that unify rotating and electrical analytics in one pane of glass win preference because plant teams favour holistic dashboards over siloed point solutions.

By End User:

Mining Accelerates Beyond Oil and Gas LeadershipOil and gas captured 24.10% of revenue in 2025, testament to offshore platforms and refineries where a single hour of downtime can erase millions of USD. Digital twins forecast equipment stress under varying feedstock mixes, fine-tuning run rates for both output and emissions. Mining and metals, however, will post 12.34% CAGR, the steepest in the plant asset management industry, as haul-truck fleets, crushers, and conveyers embed sensors that curtail unscheduled stoppages in remote pits. Sibanye-Stillwater documented median ROIs above 200% from process-optimization twins that trimmed energy costs and upped throughput.

Power and utilities exploit asset analytics to balance renewables and ageing thermal plants, while chemicals face severe compliance scrutiny, spurring investments in leak detection and predictive relief-valve maintenance. Aerospace and defence push the envelope on digital twins for design validation, whereas food, beverage, and pharmaceuticals focus on hygienic maintenance and traceability. Water utilities, spurred by AMP8 in the UK, are earmarking billions toward smart pumping, digitised pipe networks, and net-zero targets that dovetail with advanced asset management.

By Organization Size:

SME Growth Outpaces Enterprise AdoptionLarge enterprises controlled 71.80% of spending in 2025, reflecting multi-site asset inventories and dedicated transformation budgets. Yet SMEs are expanding at 13.02% CAGR, broadening the addressable base of the plant asset management market. Cloud subscriptions eliminate the need for in-house servers, while plug-and-play wireless sensors slash installation labour. SMEs report the fastest wins in energy savings and reduced scrap rather than broad digital overhauls. Financing models such as Equipment-as-a-Service transfer capex to opex, aligning with SME cash-flow cycles.

Workforce constraints loom larger for smaller firms, prompting demand for turnkey managed services. Vendors courting SMEs emphasize rapid ROI dashboards that display avoided downtime in monetary terms, easing internal justification. As frontline technicians gain confidence in data-guided interventions, adoption accelerates and referrals ripple across local industry clusters, multiplying growth prospects.

Geography Analysis

North America Plant Asset Management Market

North America owned 40.80% of 2025 revenue owing to legacy infrastructure, mature 5G rollouts, and strict environmental oversight that encourages real-time emissions tracking. Federal incentives for grid modernization and tax credits for energy-efficiency upgrades underpin high adoption across utilities and heavy manufacturing. Regional universities and OEMs collaborate on pilot labs that showcase AI-enabled maintenance, further anchoring leadership in the plant asset management market.

APAC Plant Asset Management Market

Asia-Pacific is accelerating at a 12.76% CAGR to 2031, propelled by China’s expansive renewable installations and India’s Production-Linked Incentive scheme that prioritises smart factories. Governments in Japan and South Korea sponsor 5G and robotics testbeds, reducing perceived risk for private firms. Low median asset ages combine with aggressive capacity expansion, letting many plants leapfrog directly to predictive maintenance rather than incremental upgrades. Local vendors bundle affordable sensors with cloud back ends hosted in-region to satisfy data residency mandates, catalyzing uptake among SMEs.

EMEA and South America Plant Asset Management Market

Europe shows steady growth under the European Green Deal and Corporate Sustainability Reporting Directive, both of which necessitate granular asset-level data for energy and climate disclosures. Digital twin pilots in Germany’s process industries streamline ESG reporting while trimming maintenance spend. Eastern Europe’s emerging manufacturing hubs view asset analytics as a route to competitiveness against higher-wage Western peers. South America and the Middle East, and Africa remain smaller today but post solid mid-single-digit growth as mining, water, and energy diversification agendas unlock investments, especially where sovereign funds prioritise digital infrastructure.

Competitive Landscape

The plant asset management market hosts a mix of automation incumbents and analytics newcomers. ABB, Siemens, Honeywell, and Emerson rely on vast installed bases and decades-deep process know-how to cross-sell software, while nimble software specialists differentiate through domain-specific AI and intuitive dashboards. Market fragmentation is moderate; the top five command a sizeable but not dominant portion, leaving room for regional champions to flourish.

Acquisition activity intensified in 2024-2025 as vendors sought portfolio breadth. ABB’s purchase of Aurora Motors added high-efficiency motors that feed richer data to its Ability analytics platform, while Emerson’s buyout of flow-meter expert Flexim bolstered non-invasive sensing capabilities. Cybersecurity specialists such as Nozomi Networks attract strategic stakes from automation vendors eager to embed threat detection natively, reflecting converged OT-IT risk priorities. Managed-service tie-ups, exemplified by NTT DATA and Palo Alto Networks’ 5G-secure offering, underscore customer appetite for turnkey packages that bundle connectivity, security, and analytics.

Competitive success hinges on quantifiable ROI demonstrations and talent support. Vendors that train customer maintenance crews on failure-mode diagnostics and root-cause analysis gain trust and long-term renewals. As standards harmonise and open APIs proliferate, buyers become less tolerant of vendor lock-in, rewarding suppliers that interoperate gracefully with mixed control stacks. The march toward outcome-based contracts is reshaping pricing models, transferring performance risk to solution providers, and tightening alignment between vendor and operator objectives.

Plant Asset Management Industry Leaders

ABB Group

Emerson Electric Co.

Honeywell International Inc.

Rockwell Automation, Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Plant Asset Management Market Companies Covered in this Report

- ABB

- Emerson Electric

- Honeywell International

- Siemens

- Rockwell Automation

- SKF

- Schneider Electric

- General Electric

- Endress+Hauser

- Yokogawa Electric

- AVEVA

- IBM

- AspenTech

- Bentley Systems

- Dassault Systèmes

- Bosch Rexroth

- SAP

- Oracle

- Ramco Systems

Recent Industry Developments in Plant Asset Management Market

- June 2025: Siemens and Sachsenmilch deployed AI-powered predictive maintenance for a dairy plant processing 4.7 million liters daily.

- May 2025: Honeywell acquired Johnson Matthey’s Catalyst Technologies for GBP 1.8 billion (USD 2.3 billion), deepening process-technology coverage across refining, petrochemicals, and renewable fuels sectors.

- May 2025: Engineering Industries eXcellence partnered with Augury to blend Machine Health analytics with SAP solutions.

- April 2025: The UK water sector started AMP8 with GBP 88 billion for digital asset upgrades aimed at net-zero goals by 2030.

- March 2025: NTT DATA and Palo Alto Networks launched a managed security service safeguarding private 5G networks in manufacturing and healthcare.

- March 2025: Nozomi Networks raised USD 100 million in Series E financing to speed OT/IoT security platform development.

- February 2025: Schneider Electric reported EUR 38.2 billion (USD 41.2 billion) 2024 revenue and assisted clients in avoiding 679 million tonnes of CO₂ emissions.

- January 2025: Verdantix released its Green Quadrant ranking of industrial data management platforms, citing ABB, AVEVA, and Cognite as leaders.

Plant Asset Management Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the plant asset management market as the integrated suite of on-premise or cloud software, intelligent field devices, and professional services that inspect, monitor, and optimize physical production and support assets inside one plant's boundary through their full life cycle. We include condition monitoring platforms, asset performance management modules, vibration and corrosion sensors, and related integration or training work.

Scope exclusion: Enterprise-wide EAM packages that merely aggregate plant data without directly collecting asset-health signals are kept outside this definition.

Segments Covered in This Report

- By Offering

- Software

- Asset Performance Management (APM)

- Condition and Vibration Monitoring

- Predictive Analytics Platform

- Services

- Implementation and Integration

- Training and Support

- Hardware / Devices

- Software

- By Deployment

- On-Premise

- Cloud

- Hybrid / Edge

- By Asset Type

- Rotating Equipment

- Fixed Equipment

- Instrumentation and Control Devices

- Electrical Assets

- By End User

- Energy and Power

- Oil and Gas

- Chemicals and Petrochemicals

- Mining and Metals

- Aerospace and Defense

- Automotive and Transportation

- Food and Beverage

- Pharmaceuticals and Life Sciences

- Water and Wastewater

- Others

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We validate desk findings through semi-structured interviews with plant maintenance heads, control-system integrators, and regional distributors across North America, Europe, and Asia Pacific. Their inputs on average sensor refresh cycles, project backlogs, and software subscription rates refine assumptions and spotlight fast-shifting cost drivers.

Desk Research

Mordor analysts first compile baseline data from freely accessible tier-1 repositories such as the US Bureau of Labor Statistics for maintenance labor trends, Eurostat PRODCOM for industrial equipment output, and UN Comtrade for trade flows of sensors and actuators. Guidelines from bodies such as ISA-95, OMAC, and IEC 61511 clarify technology adoption norms, while patent counts pulled via Questel signal future innovation pipelines. We also parse annual reports and 10-Ks of major automation vendors, plus North American Electric Reliability Corporation advisories that shape spending on predictive tools. Numerous other public and paid resources inform the desk stage; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down build starts by reconciling the global installed base of process-industry plants with capex-to-opex conversion ratios; that demand pool is then tempered with sensor penetration and cloud-migration multipliers. Select bottom-up checks, sampled supplier revenues and channel ASP x unit estimates, calibrate the totals. Key variables feeding the model include new greenfield capacity additions, average maintenance spend per asset, share of assets under predictive monitoring, cloud subscription price decay, and region-wise labor cost inflation. Forward curves are projected with multivariate regression blended with ARIMA smoothing, and our expert panel reviews every coefficient before lock-in. Data gaps in bottom-up rolls are bridged using weighted regional proxies rather than simple extrapolation.

Data Validation & Update Cycle

Outputs pass three-layer variance checks, after which senior reviewers vet anomalies. Models refresh annually, with interim revisions triggered by material events such as cyber-security mandates or abrupt sensor price swings. Just before release, an analyst reruns the latest quarter's data to keep clients current.

How Mordor Intelligence's Plant Asset Management Market Size Compares to Other Published Estimates

Published values often diverge because firms slice the market by unlike asset lists, apply divergent subscription price curves, or freeze exchange rates at different quarters.

Key gap drivers include whether installation-only services are counted, if software upgrades are amortized or expensed, the cadence at which aging plants exit the universe, and the refresh frequency of underlying trade data. Mordor's scope centers on in-plant hardware plus directly linked software and services, and our annual refresh yields better currency realism, which peers sometimes skip.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.82 B (2025) | Mordor Intelligence | - |

| USD 9.4 B (2024) | Global Consultancy A | Includes corporate-wide EAM and omits hardware retrofits |

| USD 7.29 B (2024) | Industry Publication B | Uses subscription ASPs from 2022 and applies a single regional uplift factor |

Taken together, the comparison shows estimates sway when scope or variable refresh lags. Mordor's disciplined plant-level focus, double-sourced inputs, and yearly model tune-ups give decision-makers a stable yet realistic baseline.

Key Questions Answered in the Report

What is the current size of the plant asset management market?

The market stands at USD 11.01 billion in 2026 and is projected to climb to USD 19.51 billion by 2031, growing at a 12.12% CAGR.

Which segment is expanding fastest within the plant asset management market?

Services are registering the quickest growth at 12.74% CAGR, driven by system-integration complexity and the shortage of skilled reliability engineers.

How fast is cloud deployment growing compared with on-premise solutions?

Cloud-based implementations are expanding at 13.05% CAGR, more than double the pace of on-premise installations, as hybrid architectures ease data sovereignty concerns.

Why is Asia-Pacific the fastest-growing region?

Strong government support for smart manufacturing, rapid renewable-energy deployment, and widespread adoption of private 5G are propelling Asia-Pacific at a 12.76% CAGR.

What return on investment can predictive maintenance deliver?

Industry case studies report ROI ratios between 5:1 and 10:1 due to lower unplanned downtime, extended asset lifespans, and reduced maintenance spending.

How are private 5G networks impacting plant asset management?

They provide deterministic, ultra-low-latency connectivity that supports mobile robots and high-frequency sensors, enabling real-time analytics inside secure industrial campuses.

Page last updated on: