Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

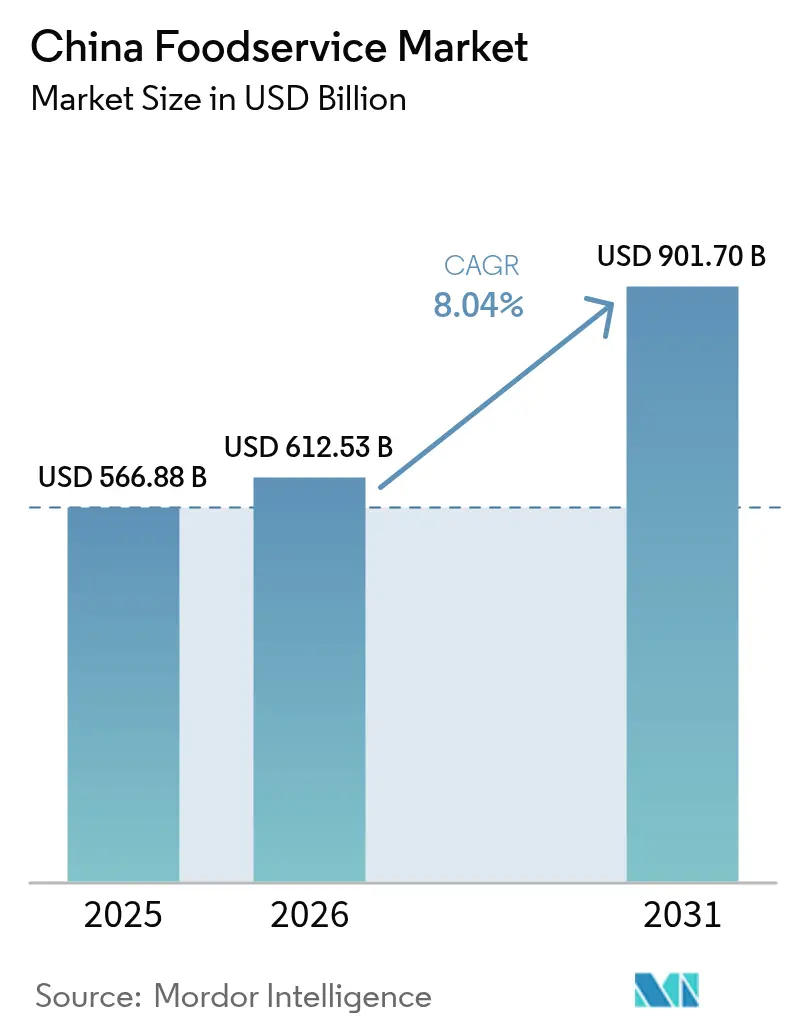

| Base Year Market Size (2025) | USD 566.88 Billion |

| Market Size (2026) | USD 612.53 Billion |

| Market Size (2031) | USD 901.70 Billion |

| Growth Rate (2026 - 2031) | 8.04% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Foodservice Market Analysis by Mordor Intelligence

The Chinese foodservice market size is recorded at USD 566.88 billion in 2025 and is projected to be USD 612.53 billion in 2026 and is expected to reach USD 901.70 billion by 2031 at 8.04% CAGR over 2026-2031. Strong pent-up demand for out-of-home dining, the rapid expansion of digitally native quick-service formats, and rising disposable incomes in middle-tier cities are reinforcing the growth trajectory of the Chinese foodservice market. Higher adoption of plant-based menus by global and domestic brands is widening consumer choice and nudging average spend upward. Operators are integrating kitchen robotics, AI-driven demand forecasting, and cashier-less ordering to lift throughput during peak periods while mitigating rising labor costs. In parallel, the boom in ghost kitchens is letting chains test new concepts at lower capital outlays and speed up delivery times. Competitive intensity remains moderate because independent eateries still dominate foot traffic in residential clusters, although branded chains continue to capture spend in malls and transit hubs.

Key Report Takeaways

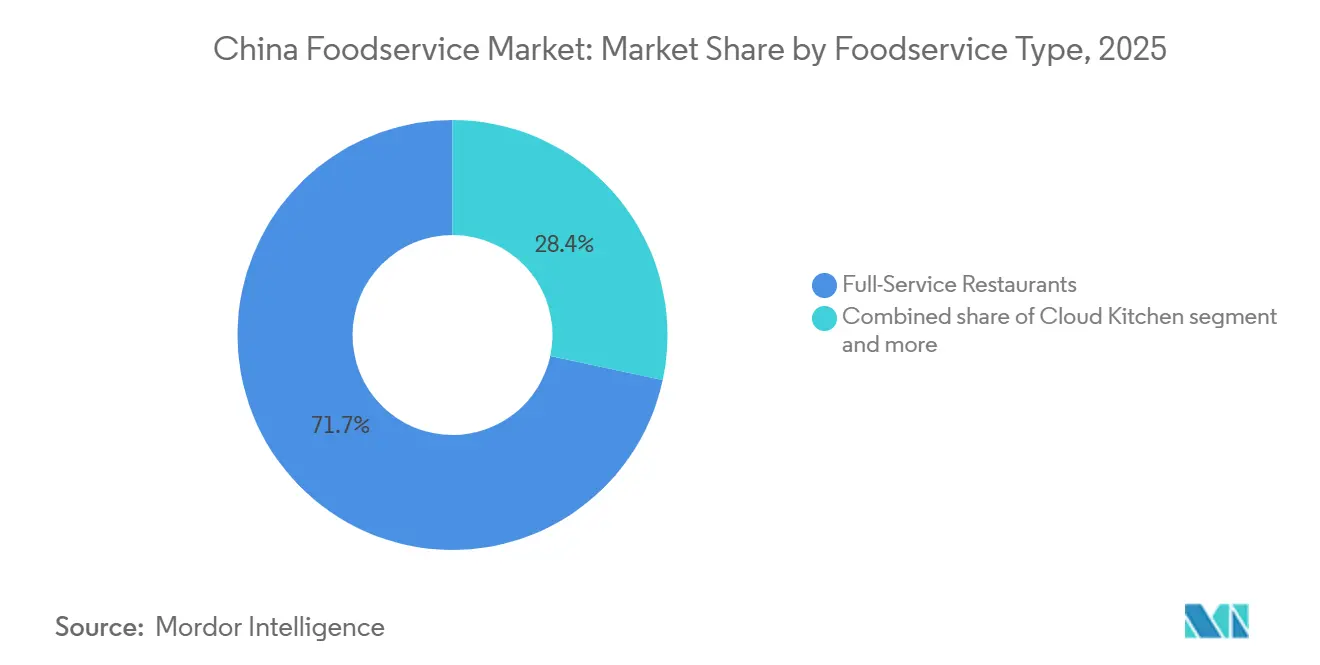

- By foodservice type, full-service restaurants led with a 71.65% share of the China foodservice market in 2025, while cloud kitchens are forecast to post the fastest 8.24% CAGR through 2031.

- By outlet, independent operators accounted for a commanding 92.40% slice of the China foodservice market size in 2025; chained outlets are projected to expand at an 8.57% CAGR between 2026 and 2031.

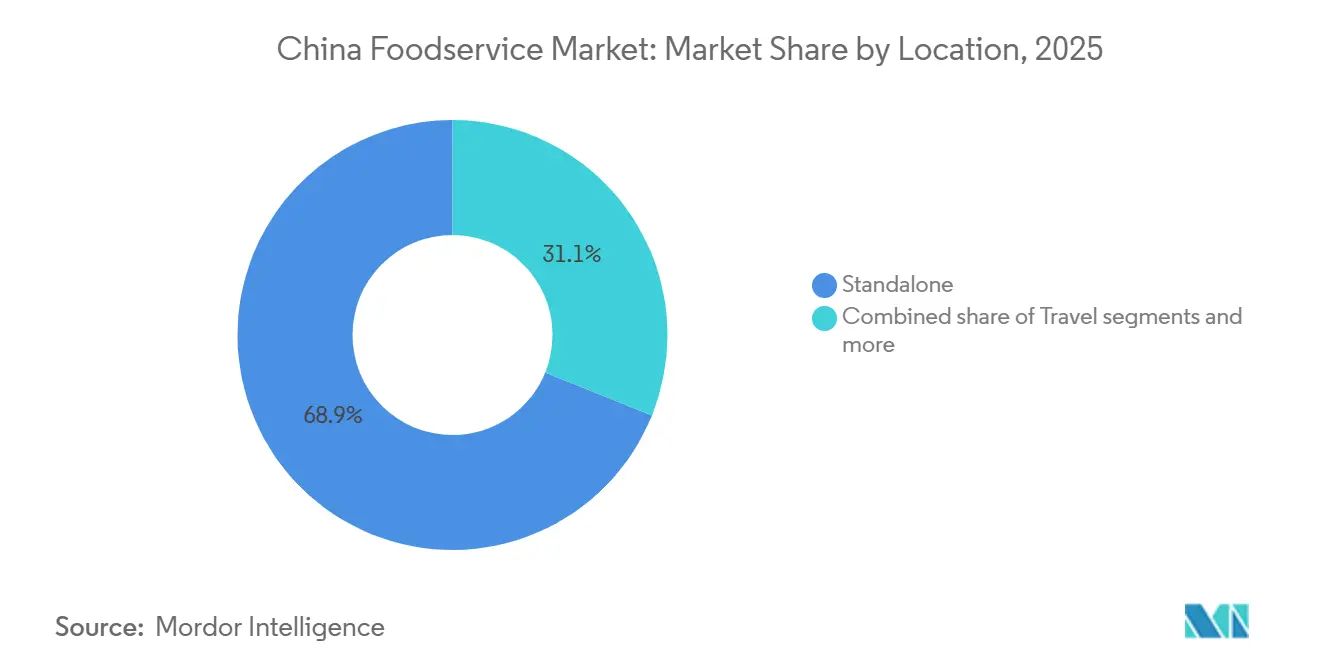

- By location, standalone venues represented 68.90% of 2025 revenue, whereas travel-based locations are on track to register the quickest 9.03% CAGR to 2031.

- By Cuisine type, Asian represented 41.32% of 2025 revenue, whereas specialty tea and coffee are on track to register the quickest 8.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for vegan and plant-based menus | +0.8% | Tier-1 cities; spillover to Tier-2 | Medium term (2-4 years) |

| Kitchen automation and robotics powered by AI | +1.2% | National; early urban gains | Short term (≤ 2 years) |

| Surge in quick-service and fast casual restaurants | +1.0% | National; lower-tier focus | Medium term (2-4 years) |

| Proliferation of ghost and cloud kitchens | +0.9% | Urban cores; suburban spread | Short term (≤ 2 years) |

| Urbanization and evolving lifestyles on the rise | +1.1% | Tier-2 and Tier-3 cities | Long term (≥ 4 years) |

| Shifting consumer preferences and dining habits | +0.7% | Tier-1; gradual Tier-2 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for vegan and plant-based menus

In China, as vegetarianism gains traction, a niche but expanding market for plant-based alternatives is emerging. ProVeg International reveals that 98% of Chinese consumers are inclined to eat more plant-based foods once they understand the health benefits [1]Source: ProVeg International Organization, "Most people in China will eat more plant-based food when told of the benefits, survey finds", proveg.org. This growing focus on health-conscious dining has led major chains to introduce plant-based options. International brands such as Burger King (China) introduced plant-based Whopper variants in 2025, lifting same-store traffic among young professionals in Shenzhen and Guangzhou. Domestic fast-casual players are pairing grain bowls with tofu-based toppings to target Gen-Z diners seeking novelty and sustainability cues. Ingredient suppliers are localizing pea isolate and heme-like flavor bases, lowering cost premiums against animal products. The resulting affordability is expected to keep demand momentum intact across mid-priced dining formats.

Shifting consumer preferences and dining habits

The post-pandemic dining landscape has fundamentally altered consumer behavior, with delivery orders now accounting for the majority of digital sales at major chains like Yum China in 2024. As consumers focus more on convenience and value, the pre-prepared food market is expected to exceed CNY 500 billion in 2024, according to the China Food Circulation Association [2]Source: Food Circulation Association, "China Food Industry Market Analysis Report", xinyingyang.com. Millennials value communal dining yet favor digitally mediated reservations that cut queueing. Tea-based beverages, low-sugar desserts, and functional botanicals gain traction as health consciousness rises. Experiential formats, such as pop-up regional street food counters within full-service venues, deliver novelty without heavy capital spending. Social media-led viral menu items, like soufflé pancakes or chili-oil ice cream, can lift transaction counts week-over-week during limited runs, reinforcing the dynamism of the Chinese foodservice market.

Surge in quick-service and fast casual restaurants

Local QSR chains are surpassing international competitors by aligning with local culture and employing aggressive pricing strategies. Chinese fast-food brands, such as Lao Xiang Ji and Micun Banfan, are rapidly gaining market share by offering traditional flavors in convenient formats and expanding across lower-tier cities. Value menus and combo deals resonate with price-sensitive students and office workers, while limited-time flavors keep churn low. Franchisors offer turnkey store kits that compress build-out cycles to 30 days, helping entrepreneurs tap into footfall clusters near metro stations. Digital ordering kiosks push average ticket values up by promoting add-on beverages and desserts. The format’s capital-light model strengthens its position as the steadiest growth pillar for the Chinese foodservice market over the forecast horizon.

Proliferation of ghost and cloud kitchens

Ghost kitchens address this demand by offering diverse menus and fast delivery, particularly in major cities like Shanghai and Beijing. By utilizing technology for order management, delivery coordination, and customer analytics, cloud kitchens are improving efficiency and adapting to market trends. In 2024, the penetration rate of online food delivery services in China increased, according to the China Internet Network Information Center, highlighting strong demand for delivery-only models [3]Source: China Internet Network Information Center, "55th Statistical Report on China's Internet Development", cnnic.com.cn. Third-party operators provide fully outfitted micro-kitchens within logistic hubs, letting brands enter new districts without street-front rent exposure. Aggregators bundle several virtual brands under one roof to maximize equipment utilization and cross-promote across apps. Data-driven menu localization trims underperforming SKUs within weeks, keeping ingredient inventory slim. Riders benefit from optimized pick-up corridors that shave three minutes off hand-off times versus standalone stores. Combined, these efficiencies translate into delivery fees that remain flat even as fuel costs rise, reinforcing consumer loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Full-service restaurants grapple with soaring operating and rental costs | -0.6% | National; stricter in Tier-1 | Short term (≤ 2 years) |

| Stringent food safety regulations and compliance costs | -0.8% | National; urban concentration | Medium term (2-4 years) |

| Supply chain disruptions that affect ingredient availability and costs | -0.4% | Tier-1 and Tier-2 | Medium term (2-4 years) |

| Rising labor costs and staffing challenges | -0.3% | National; urban focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety regulations and compliance costs

Regulatory compliance costs are escalating as China implements 50 new food safety standards and 9 amendments in 2025, including comprehensive updates to food labeling requirements under GB 7718-2025. The National Food Safety Standard for Food Additives (GB 2760-2024), which takes effect in February 2025, requires substantial reformulation and testing, driving up operational costs for foodservice operators. Moreover, school foodservice providers must comply with new guidelines for cleaning and disinfecting reusable dining utensils, necessitating specialized equipment and training. To address the complexity, the China National Center for Food Safety Risk Assessment has issued 98 FAQs on national food safety standards. While these measures aim to improve food safety, they present considerable challenges for smaller operators with limited resources for compliance.

Rising labor costs and staffing challenges

China's service sectors are experiencing a severe shortage of skilled workers, which is driving up wages. To address the mismatch between job openings and workforce skills, the government is promoting vocational training. The food delivery industry, a significant employer, is intensifying labor demand and contributing to wage increases. Restaurant operators in major cities report that fixed costs are rising faster than revenue, compressing profit margins and, in some cases, leading to closures. High-end restaurants promote profit-sharing and provide dormitory housing to improve retention, yet gains remain uneven. Automation offers respite but demands upfront capex that small players cannot always finance. Unless wage growth aligns with productivity gains through technology or workflow redesign, margin compression may persist across labor-intensive formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Full-Service Strength and Cloud Kitchen Momentum

Full-service restaurants captured 71.65% of the Chinese foodservice market share in 2025. Their dominance stems from entrenched cultural preferences for communal dining and banquet-style gatherings. Nevertheless, traffic shifts toward speed and convenience have elevated cloud kitchens, whose agile cost structures underpin the strongest 8.24% CAGR outlook. The Chinese foodservice market size for cloud kitchens is projected to widen steadily as aggregator platforms expand into lower-tier cities. In full-service, experiential menus and tableside cooking now supplement traditional white-tablecloth formats to maintain relevance among younger diners. Forward-looking chains blend dine-in theatre with integrated e-commerce, ensuring consistent brand touchpoints across channels.

Full-service operators are also redesigning menus for smaller plate options, encouraging repeat orders, and controlling waste. Cloud kitchens leverage centralized procurement and shared rider fleets to keep per-order logistics costs under USD 0.80, enabling aggressive promotional pricing that undercuts street-front rivals. Venture capital continues to favor virtual-brand incubators, signaling further innovation waves that can reconfigure competitive landscapes. As dining-in recovers, hybrid models, where dine-in kitchens backfill off-site dark facilities during off-peak hours, are emerging to optimize fixed asset utilization. Such synergies are expected to reinforce profitability across both ends of the format spectrum.

By Outlet: Chain Consolidation Drives Efficiency

Independent venues controlled 92.40% of 2025 revenue, validating the fragmentation characteristic of the Chinese foodservice market. Street-side noodle stalls, mom-and-pop Cantonese cafés, and family-run hotpot joints cater to hyper-local palates and price points. Yet franchised and corporate-run outlets exhibit sharper expansion velocity, leading the China foodservice market size for chained outlets to climb at an 8.57% CAGR. Chain operators tout standardized quality, loyalty apps, and nationwide marketing heft, attracting repeat customers in shopping malls and transit hubs. Their scale allows investment in traceable sourcing and ESG reporting, which institutional landlords increasingly demand. As the market evolves, the tug-of-war between independent charm and corporate efficiency intensifies, shaping the future of China's culinary landscape. Observers note that while independents hold sway today, the rapid ascent of chains could redefine dining norms in urban centers.

Independent restaurateurs deploy live-stream selling and short-video marketing to stay visible amid rising digital advertising costs. Community group buying complements dine-in with bulk meal box preorders that anchor weekday production volumes. Franchisors simplify compliance through turnkey packages covering POS, supply contracts, and hygiene protocols, thereby lowering barriers for first-time investors. Nonetheless, conversion of independents into branded networks may face cultural resistance in heritage cuisine segments where chefs prize artistic autonomy. As digital platforms become the new storefronts, restaurateurs are not just selling meals but crafting narratives that resonate with their audience. The challenge lies in balancing tradition with modern marketing, ensuring that the essence of their culinary art isn't lost in the digital shuffle.

By Location: Retail Venues Anchor Convenience Growth

Standalone locations generated 68.90% of 2025 sales, anchored by street-front sites in residential precincts that fulfill daily dining occasions. Households rely on neighborhood eateries for breakfast buns and late-night skewers, ensuring resilient baseline demand. However, travel nodes, airports, railway stations, and highway service areas represent the quickest 9.03% CAGR underpinned by surging domestic tourism and business mobility. The Chinese foodservice market size attached to transit corridors benefits from round-the-clock flight schedules and mandatory wait times, which lift average dwell periods. Brands with compact, speed-of-service-optimized footprints, such as kiosk-format coffee chains, are well-suited to capture this upside. Standalone operators are increasingly turning to community loyalty programs, rewarding their repeat patrons with enticing off-peak discounts.

This strategy not only smooths out day-part volatility but also deepens the bond between the operator and the community. Shopping mall eatery clusters, in a bid to enhance their appeal, supplement the standalone mix. They offer not just climate-controlled seating but also family entertainment options in close proximity, making them a preferred choice for families. Travel sites are evolving, with digital menus now available in multiple languages. Coupled with contactless QR ordering, these innovations significantly shorten queue times, a boon for passengers often juggling baggage. Furthermore, the convenience of these features can influence a traveler's choice of dining establishment. Security clearance zones, often bustling with travelers, also play a pivotal role in shaping pricing strategies. Here, the premium pricing power comes into play, as customers find themselves with limited alternative options, making them more willing to pay a premium for convenience.

By Cuisine Type: Asian Staples and Beverage Innovation

The Chinese foodservice market thrives on vast regional flavor diversity, from fiery Sichuan to delicate Jiangnan dishes. In full-service categories, Asian cuisine remains the anchor, while newer European and Middle Eastern themed outlets attract adventurous diners seeking global flavors. Burger and bakery quick-service sub-segments post consistent ticket growth as breakfast-on-the-go habits spread beyond tier 1 metros. Specialty coffee and tea cafés adopt single-origin beans and cold-brew infusions to stand out in a crowded beverage landscape. Ice cream chains experiment with durian, matcha, and spicy chili variants, showcasing how local tastes steer innovation cycles. Operators refine menu engineering by tracking flavor trends on social media, feeding near-real-time data into R&D cycles that last mere weeks.

This rapid adaptation allows them to stay ahead of competitors and cater to evolving consumer preferences. Virtual brands experiment with fusion formats, such as Peking duck tacos, testing reception without the constraints of dine-in ambience. By sidestepping traditional dining limitations, they can gauge market appetite more freely. Successful hits transition into physical menus, demonstrating the porous boundary between online and offline culinary ideation. This seamless integration underscores the changing dynamics of the food industry. As a result, operators are not only boosting their bottom line but also solidifying their brand presence in a competitive landscape.

Geography Analysis

Eastern China, comprising Shanghai, Jiangsu, and Zhejiang, accounts for the single largest slice of consumer spending due to its dense urban clusters and higher disposable incomes. The region's bustling cities, with their neon-lit streets and upscale malls, are a testament to the affluent lifestyle of their residents. As a result, international brands are increasingly setting their sights on these urban hubs, eager to tap into the lucrative market. Tier 1 cities host a critical mass of multinationals and high-income expatriates, which supports a vibrant premium casual scene. This dynamic not only fuels the growth of upscale dining establishments but also paves the way for innovative culinary concepts to flourish. Central provinces like Hubei and Henan, bolstered by manufacturing resurgence and rapid urbanization, represent rising middle-class demand for branded quick-service concepts, underpinning future volume gains. As these provinces continue to evolve, they are becoming hotspots for both domestic and international food brands seeking to establish a foothold.

Southern metros, spearheaded by Guangdong’s Pearl River Delta, register a robust breakfast and late-night snacking culture that benefits 24-hour eateries. This round-the-clock demand has led to a surge in establishments catering to these specific meal times, ensuring patrons are never left wanting. Regional street food traditions influence chain menu localization, from congee variants to cha chaan teng-style milk tea. Such adaptations not only resonate with local tastes but also enhance the authenticity of these chains in the eyes of consumers. Northern regions encounter colder climates, driving higher hotpot and lamb skewer consumption during extended winters, ensuring seasonal spikes for players that tailor inventories accordingly. These seasonal trends highlight the importance of adaptability for businesses aiming to thrive in the region.

Western provinces, long constrained by lower income levels, witness accelerated infrastructure rollout that bridges cold chain gaps for perishable goods. This development is pivotal, ensuring that fresh produce and other perishables reach consumers in prime condition, thereby reducing wastage. Government tourism initiatives in Sichuan and Yunnan attract domestic travelers, boosting demand for café and casual-dining venues near scenic spots. As these regions become more accessible and popular, the culinary scene is poised for a significant uplift. Collectively, these geographic contrasts create a patchwork of micro-markets, compelling operators to adopt region-specific pricing, marketing, and format strategies to secure share within the China foodservice market. Such tailored approaches are not just beneficial but essential for success in China's diverse and dynamic foodservice landscape.

Competitive Landscape

Global majors such as Yum! Brands, Restaurant Brands International, and McDonald’s are making significant inroads into tier 3 and tier 4 cities, employing multi-brand master franchise structures. Their strategic investment in localized R&D centers not only accelerates menu adaptation cycles but also tailors offerings to regional tastes; for instance, KFC has introduced mala chicken skewers, while Pizza Hut has rolled out durian cheese pies. Meanwhile, domestic champions Haidilao and Jiumaojiu are cautiously extending their store footprints. In a bid to diversify revenue streams, they're also introducing semi-finished retail packs in supermarkets, tapping into the omnichannel market.

Coffee specialists Starbucks and Luckin Coffee are diversifying their store formats. They're piloting drive-thru lanes on intercity expressways, catering to travelers, and compact booths in office lobbies, targeting the busy workforce. On the tea front, chains like HeyTea and Nayuki are scaling up the use of smart tea robots, which can whip up beverages in just 45 seconds, significantly cutting down on labor reliance. Quick-service pizza giants, Domino’s and Papa John’s, are capitalizing on their proprietary rider fleets, ensuring a swift 20-minute delivery promise in select megacities.

Operators are increasingly aligning with delivery aggregators like Meituan and Ali’s Ele.me. By negotiating preferential home-page banner placements, they secure exclusive combo deals, leading to a surge in order volumes, especially during national holiday peaks. In the realm of corporate responsibility, ESG disclosures are emphasizing sustainable packaging and carbon-neutral commitments, a direct response to heightened consumer activism and investor scrutiny. While independent eateries hold a numerical advantage, the landscape is shifting. Scale economics and tech investments are driving a consolidation trend, favoring branded chains in China's foodservice market.

China Foodservice Industry Leaders

-

Starbucks Corporation

-

Yum! Brands Inc.

-

McDonald's Corporation

-

Luckin Coffee Inc.

-

Haidilao International Holding Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Starbucks has initiated its first store expansion plan in China, introducing a variety of products such as injection-molded cups, in-mold labeled cups, and mini freeze-dried coffee powder cups.

- April 2025: Domino's Pizza China launched 97 new stores in Q1 2025, strengthening its community presence. The brand's growth strategy is centered on its 4D approach: Development, Delicious Pizza at Value, Delivery, and Digital.

- October 2024: McDonald's has taken a major step towards sustainability by opening its first "Four Zeros" restaurant in Shenzhen, China, at Meisha Vanke. The "Four Zeros" designation indicates that the restaurant is certified in all four LEED categories: Zero Carbon, Zero Energy, Zero Water, and Zero Waste.

- July 2024: Luckin Coffee Inc. has opened its 20,000th store in Beijing. The company prioritizes product innovation, makes significant investments in its supply chain, and consistently enhances its digital capabilities to raise customer satisfaction in China’s coffee industry.

China Foodservice Market Report Scope

Foodservice refers to the preparation, distribution, and sale of food and beverages in various settings such as restaurants, cafeterias, and other establishments. The China Foodservice Market is Segmented by Foodservice Type (Cafes and Bars, Cloud Kitchen, Full-Service Restaurants, Quick-Service Restaurants), Outlet (Chained Outlet, Independent Outlet), Location (Leisure, Lodging, Retail, Standalone, Travel), Cuisine Type (Asian, European, Latin American, Middle Eastern, North American, Other Cuisines), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Foodservice Type

| Cafes and Bars |

| Cloud Kitchen |

| Full-Service Restaurants |

| Quick-Service Restaurants |

By Outlet

| Chained Outlet |

| Independent Outlet |

By Location

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

By Cuisine Type

| Full Service Restaurants | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other Full-Service Restaurant Cuisine | |

| Quick Service Cuisine | Bakeries |

| Burger | |

| Ice Cream | |

| Meat-Based Cuisine | |

| Other Quick Service Cuisine | |

| Cafes and Bars | Bars and Pubs |

| Cafes | |

| Juices/Smoothies/Desserts | |

| Specialty Coffee and Tea | |

| Cloud Kitchen |

| By Foodservice Type | Cafes and Bars | |

| Cloud Kitchen | ||

| Full-Service Restaurants | ||

| Quick-Service Restaurants | ||

| By Outlet | Chained Outlet | |

| Independent Outlet | ||

| By Location | Leisure | |

| Lodging | ||

| Retail | ||

| Standalone | ||

| Travel | ||

| By Cuisine Type | Full Service Restaurants | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other Full-Service Restaurant Cuisine | ||

| Quick Service Cuisine | Bakeries | |

| Burger | ||

| Ice Cream | ||

| Meat-Based Cuisine | ||

| Other Quick Service Cuisine | ||

| Cafes and Bars | Bars and Pubs | |

| Cafes | ||

| Juices/Smoothies/Desserts | ||

| Specialty Coffee and Tea | ||

| Cloud Kitchen | ||

Key Questions Answered in the Report

How large will the China foodservice market be by 2031?

It is projected to reach USD 901.70 billion by 2031, expanding at an 8.04% CAGR from 2026.

Which format is growing fastest within China’s dining landscape?

Cloud kitchens lead with a forecast 8.24% CAGR through 2031 as delivery demand deepens in urban corridors.

Are independent restaurants still dominant across China?

Yes, they held 92.40% of 2025 revenue, though chained outlets are scaling faster at an 8.57% CAGR.

What is the main operational challenge facing full-service operators?

Rising rental and operating costs in tier 1 central business districts are compressing margins.

Page last updated on: