Qatar Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

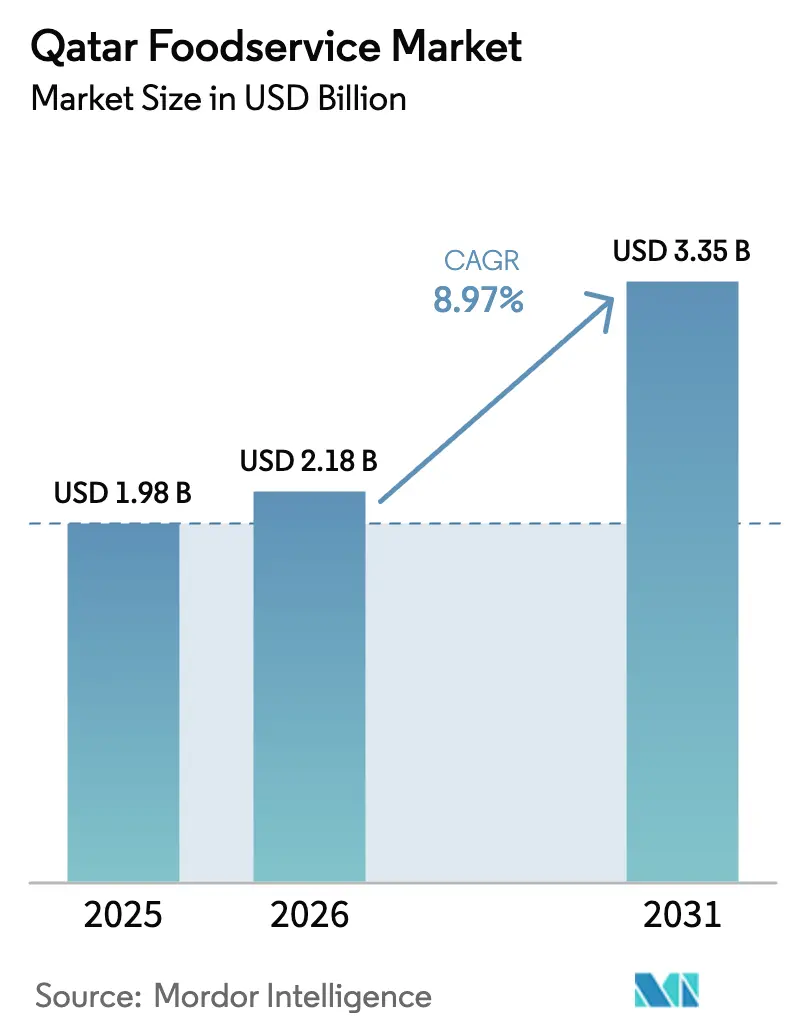

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 8.97% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Qatar Foodservice Market Analysis by Mordor Intelligence

The Qatar foodservice market size is projected to expand from USD 1.98 billion in 2025 and USD 2.18 billion in 2026 to USD 3.35 billion by 2031, registering a CAGR of 8.97% between 2026 to 2031. Owing to repurposed infrastructure from FIFA 2022, a steady influx of visitors, and a swift embrace of digital services, demand is surging across dine-in, takeaway, and delivery options. Hamad International Airport's annual handling of 65 million passengers underscores the area's vibrant travel traffic, making it a critical hub for foodservice businesses targeting transit and tourism-driven consumers. In 2024, consumer spending on delivery apps topped QAR 5.2 billion, reflecting a significant shift in consumer behavior toward convenience and technology. The Snoonu–Jahez partnership highlights a growing investor trust in tech-driven services, further accelerating innovation in the market. Government initiatives aimed at localizing food supplies and championing sustainability are transforming procurement practices, ensuring long-term resilience in the foodservice supply chain. However, rising water tariffs and rents in prime districts are squeezing operating margins, posing challenges for operators. With tourism on the rise, digital services gaining traction, and a focus on localizing supply chains, Qatar's foodservice market is poised for sustained growth through 2031.

Key Report Takeaways

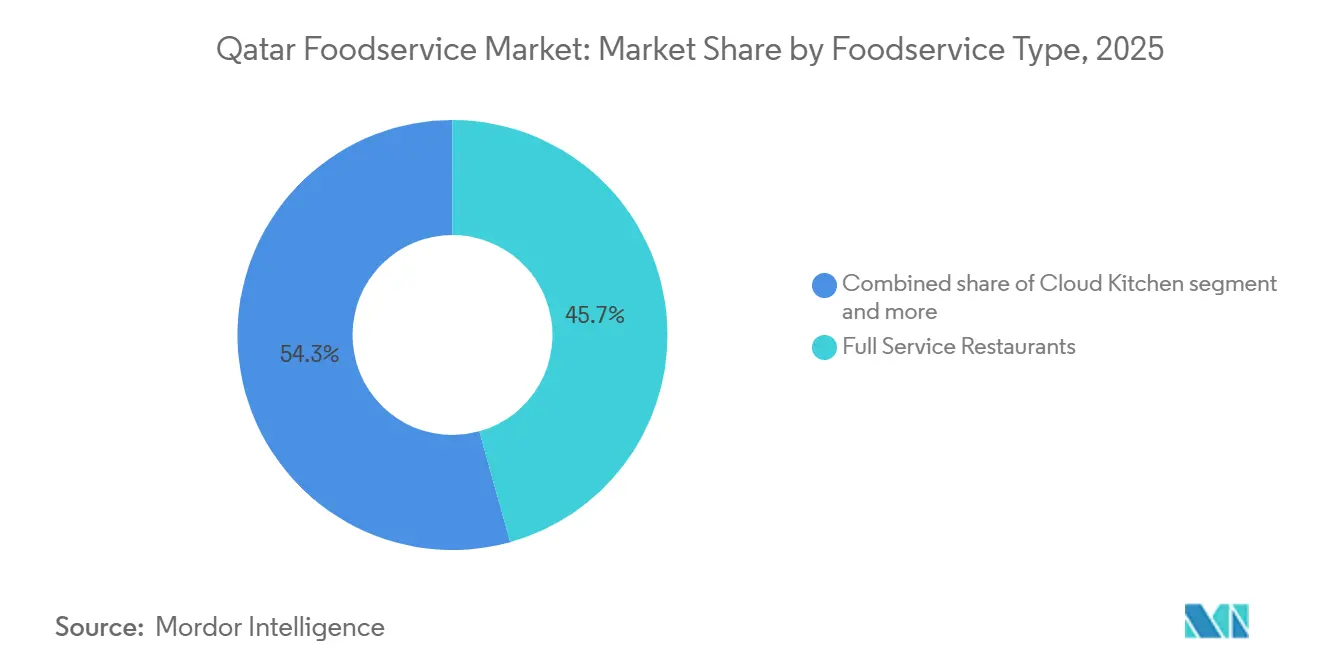

- By foodservice type, full-service restaurants held 45.68% share of 2025 revenue, while cloud kitchens are forecast to grow at a 17.10% CAGR through 2031.

- By outlet format, independents controlled 75.42% of the 2025 value, whereas chained outlets are advancing at an 8.98% CAGR on the back of master-franchise expansion.

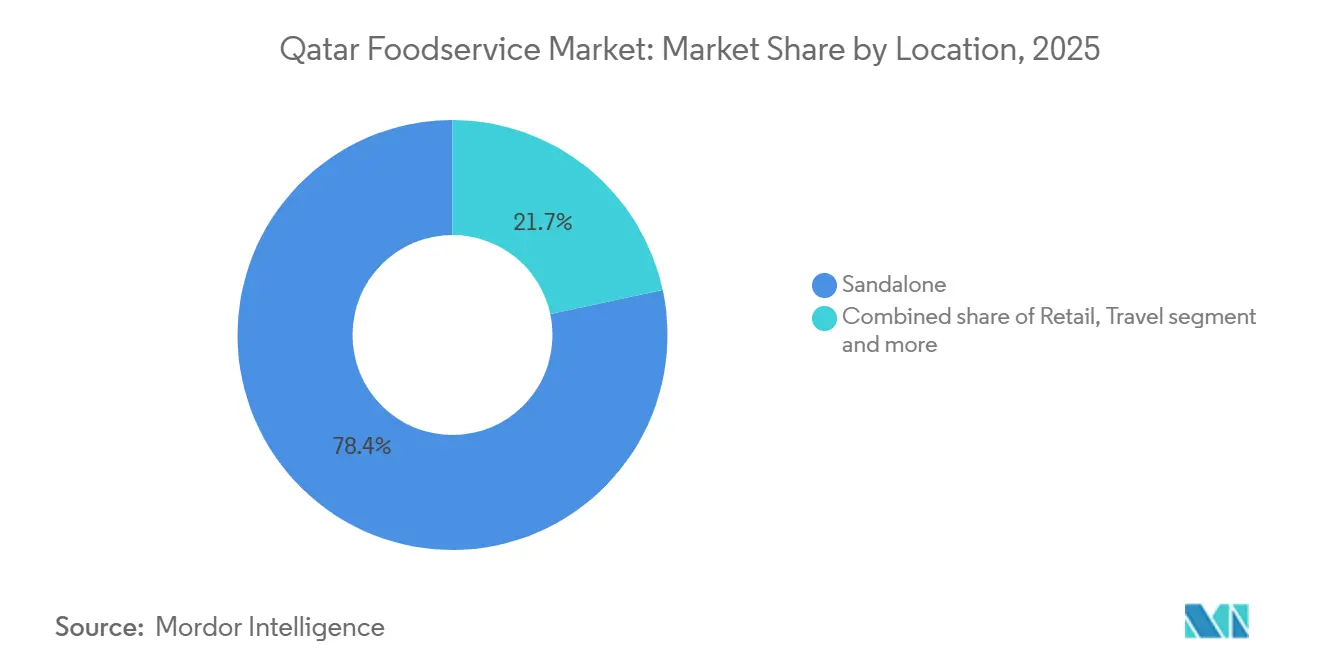

- By location, standalone stores captured 78.35% of 2025 spending; travel locations are on track for a 10.74% CAGR as airport capacity rises.

- By service, dine-in accounted for 64.72% of sales in 2025, yet delivery is projected to expand at an 11.88% CAGR due to aggregator consolidation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding tourism sector and influx of international visitors | +2.1% | National concentration in Doha, Lusail, West Bay | Medium term (2-4 years) |

| Widespread adoption of delivery apps and online ordering | +1.8% | Highest penetration in Doha metro | Short term (≤2 years) |

| Rising disposable incomes and large expatriate base | +1.5% | Nationwide, strongest in high-income districts | Long term (≥4 years) |

| Large, young demographic favoring frequent dining-out and fast service | +1.3% | Urban centers with youth clusters | Medium term (2-4 years) |

| FIFA 2022 legacy infrastructure accelerating concept roll-outs | +1.0% | Early gains in Lusail, West Bay, airport zones | Short term (≤2 years) |

| Government Tawteen program boosting domestic sourcing | +0.7% | Supply chain impact nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expanding tourism sector and influx of international visitors

In 2024, Qatar welcomed 5.08 million visitors, setting its sights on reaching 6 million by 2030, in line with its National Vision 2030, as highlighted by Qatar News Agency[1]Source: Qatar News Agency, "Ministry of Transport Finalizes Qatar Freight Master Plan," qna.org.qa. This growth aligns with the country's strategic efforts to position itself as a global tourism hub. In the first half of 2025, hotel occupancy averaged 71%, keeping visitor nights robust and reflecting the sustained demand for accommodation. Hamad International Airport, with its newly added gates, boosted its annual capacity to 65 million passengers, and notably, a quarter of these travelers opted for direct point-to-point journeys instead of transiting through. This expansion supports Qatar's aim to enhance connectivity and attract more international visitors. A diverse influx of visitors from the GCC, Europe, and Asia not only smoothens seasonal fluctuations but also expands the demand for various cuisines, catering to a wide range of cultural preferences. Venues once dedicated to FIFA events have been transformed, now hosting conferences and concerts, further driving repeat traffic to Qatar's foodservice sector and contributing to the country's broader economic diversification goals.

Widespread adoption of delivery apps and online ordering

Food delivery apps are significantly transforming dining habits in Qatar, driven by technological advancements and strategic initiatives. Talabat, a prominent player in the market, expanded from a modest team to a robust workforce of over 160 in 2024, cementing its market leadership, according to Invest Qatar[2]Source: Invest Qatar, “Investor spotlight: talabat Qatar,” invest.qa. This growth reflects the increasing demand for convenient food delivery services and the company's ability to adapt to evolving consumer preferences. Jahez's USD 245 million acquisition of Snoonu introduced AI-driven routing and dynamic pricing to the local platform, enhancing operational efficiency and customer experience. With commission rates ranging from 15% to 35%, restaurants are increasingly leaning towards first-party apps that prioritize data capture and profit margins, enabling them to maintain greater control over their operations. Americana launched its proprietary last-mile network across 109 domestic units, effectively sidestepping intermediaries and ensuring faster, more reliable deliveries. Meanwhile, the government, with its digital-economy initiatives, aims for a 3.2% GDP contribution by 2030, paving the way for deeper market penetration and fostering innovation in the food delivery ecosystem.

Rising disposable incomes and large expatriate base

Expatriates, making up over 85% of Qatar's residents, are fueling a rising demand for international cuisines and upscale dining, as noted by the IMF[3]Source: IMF Staff, “Artificial Intelligence in Qatar – Assessing the Potential Economic Impacts,” imf.org. This demographic's diverse cultural backgrounds contribute to the popularity of global food options, creating opportunities for restaurants to cater to varied tastes. While Qatari nationals shell out USD 112 monthly per capita on dining out, expatriates spend a more modest USD 51, bolstering the city's premium dining scene. The World Bank reported a robust 13.6% year-on-year surge in accommodation and food services in early 2025, driven by increased consumer spending and tourism activities. Thanks to low inflation, real incomes remained intact, allowing more room in budgets for fine dining experiences. With LNG expansions and a boom in service-sector hiring, wages are projected to rise through 2026, ensuring a steady influx of patrons to Qatar's foodservice market. This growth is expected to further enhance the market's competitiveness, encouraging innovation and investment in the sector.

Large, young demographic favoring fast service

With a median age below 35, many residents in Qatar are clocking in long shifts across the construction, retail, and hospitality sectors. This young and dynamic workforce drives demand for convenient and efficient dining options. Quick-service chains, prioritizing speed, halal certification, and digital ordering, are striking a chord with this demographic by catering to their fast-paced lifestyles. Jollibee, boasting 15 stores, has seamlessly integrated mobile ordering, appealing to both Filipino patrons and locals by offering familiar and accessible dining experiences. Cafés like Chac'Late and Blue Signature Café, known for their Instagram-worthy aesthetics and premium beverages, are magnetizing Gen Z, who value immersive interiors and high-quality offerings. Enhanced metro connectivity is not only shortening commutes but also amplifying grab-and-go trips, propelling growth in both takeaway and delivery segments of Qatar's foodservice market, as consumers increasingly seek convenience and speed in their dining choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food-safety and environmental compliance costs | −0.9% | Highest burden in Doha and prime districts | Short term (≤2 years) |

| High rents and outlet saturation in prime districts | −1.2% | West Bay, The Pearl, Lusail City | Medium term (2-4 years) |

| Water scarcity raising utility costs for full-service formats | −0.6% | Nationwide | Long term (≥4 years) |

| Sharia-compliant finance limiting leverage for independents | −0.8% | Disproportionate effect on SMEs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Water scarcity raising utility costs for water-intensive formats

Qatar, one of the most water-scarce countries, has only 58 cubic meters of renewable freshwater resources per capita annually. The nation depends on desalination for 99% of its water supply, making utility costs sensitive to energy prices and environmental regulations. In 2024, Kahramaa, Qatar's General Electricity and Water Corporation, raised commercial water tariffs by 15%. Full-service restaurants, requiring water for dishwashing, ice machines, and beverage preparation, face higher costs compared to quick-service outlets using disposable packaging and minimal water. The government's sustainability initiatives, such as GSAS green building standards promoting water-efficient fixtures, are increasing capital expenditures for new outlets and retrofitting costs for existing ones. Operators not investing in water-saving technologies risk margin compression as tariffs rise. Desalination capacity reached 710 million gallons per day in 2024, but population growth and economic expansion are straining supply. The government is exploring treated wastewater reuse for landscaping and cooling systems, offering operators opportunities to reduce potable water use by adopting greywater systems for non-food purposes.

Sharia-compliant finance limits leverage for independent operators

Islamic banking constitutes about 80% of Qatar's banking sector, one of the highest globally. Sharia-compliant financing methods, such as Murabaha (cost-plus financing) and Ijara (leasing), require asset-backed collateral and prohibit interest-based leverage, limiting debt capacity for independent operators and smaller chains. In 2024-2025, Qatar Islamic Bank (QIB), Masraf Al Rayan, and Qatar International Islamic Bank (QIIB) offer commercial financing at profit rates of 5-7%. However, operators without real estate or equipment collateral face difficulties in securing expansion capital, while chained outlets benefit from corporate guarantees and stronger parent company balance sheets. In 2025, independent outlets held 75.42% of the market value but grew at a slower 8.98% CAGR compared to chained outlets. Independents rely on retained earnings and family office equity injections, while chained outlets leverage growth. The challenge is more pronounced for cloud kitchens and delivery-only models, which lack physical storefronts for collateral. This constraint is driving consolidation, with well-capitalized regional players like Jahez acquiring local platforms such as Snoonu to expand market share and utilize their balance sheets for multi-market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Deliver Rapid Growth

In 2025, full-service restaurants led Qatar's foodservice market, claiming 45.68% of the total revenue. These establishments capitalize on experiential dining, an upscale ambiance, and the allure of Michelin-starred chefs, allowing them to command premium prices. Aesthetic cafés and dessert bars are rapidly emerging in malls and lifestyle hubs, leveraging their social media presence and visually appealing offerings. While Asian and Middle Eastern dining formats resonate with the expatriate community, North American steak and burger joints enjoy unwavering loyalty. Overall, full-service operators uphold their dominance through brand prestige and a broad cultural appeal.

Cloud kitchens are emerging as the fastest-growing segment, with a projected CAGR of 17.10% through the forecast period. A license fee cut to QAR 500 in July 2025 spurred a wave of registrations and streamlined operations catering to off-premise demand. These kitchens boast 30–50% cost savings over traditional outlets, thanks to reduced rent, labor, and overheads. Local brands like Go Crispy and Tea Time are on an aggressive expansion spree, eyeing 400 international branches with concepts ready for export. Meanwhile, quick-service outlets are enhancing efficiency, adopting AI scheduling and IoT upgrades that trim energy costs by about 10%.

By Outlet: Chained Concepts Narrow the Gap

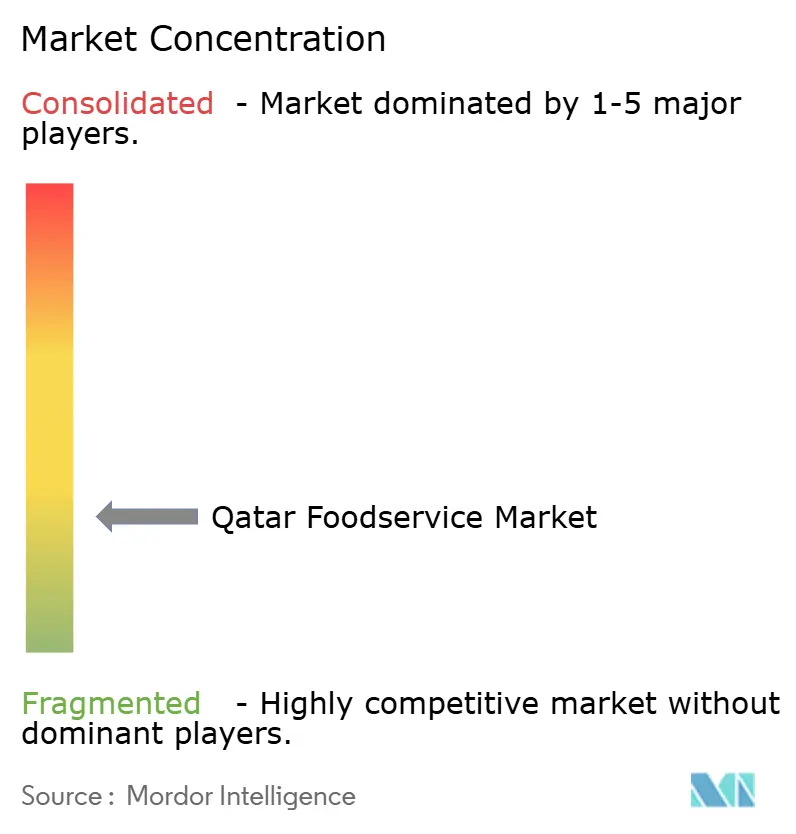

In 2025, independent operators captured 75% of Qatar's foodservice spending, capitalizing on their local adaptability and strong customer relationships. To counter challenges like rising rents and compliance costs, these smaller entities have relocated to more affordable areas like Lusail and Msheireb. They also experiment with new concepts through pop-ups and food trucks. Collaborating with partners like Al Meera, they utilize digital procurement platforms, which help in reducing working capital needs and enhancing profit margins. Yet, despite these strategic moves, independents grapple with pressures from consolidation trends, notably from private equity-backed multi-brand roll-ups. With a market concentration score of 3, there's significant potential for mergers without the looming threat of an oligopoly.

Chains are emerging as the fastest-growing segment, boasting an impressive 8.98% CAGR during the forecast period. Major players like Alshaya, adding 250 Starbucks outlets annually (with several in Doha), and Sterling Restaurants, securing rights for TCBY, highlight the lucrative opportunities in scalable financing and frozen desserts. Technological advancements, including self-ordering kiosks, integrated loyalty applications, and Sharia-compliant capital frameworks, enhance the competitiveness and omnichannel allure of these chains. Such investments not only facilitate localized menus but also expand their reach, gradually diminishing the stronghold of independent operators. As a result, the chains' aggressive expansion strategy is set to redefine the market landscape, emphasizing their scale and innovative edge.

By Location: Travel Hubs Gain Momentum

In 2025, standalone stores dominated Qatar's foodservice landscape, accounting for 78.35% of its total value. These stores, primarily located in malls and bustling street clusters, serve as anchors for daily consumer traffic. Leisure hotspots like Katara and The Pearl further bolster this traffic, drawing in a consistent stream of tourists. In response to challenges from e-commerce and escalating rents, mall-based outlets have turned to experiential strategies, incorporating live cooking demonstrations and collaborations with chefs. This adaptive approach has allowed them to retain their market dominance, even as they grapple with tighter margins due to rising operational costs. Ultimately, the widespread accessibility of standalone venues solidifies their foundational role in the market's scale.

Meanwhile, travel-related venues are outpacing others with a robust growth rate of 10.74% CAGR. This surge is largely attributed to a record 52.7 million passengers passing through airports in 2024. Operators such as HMSHost are seizing the opportunity, rolling out 24 branded concepts that leverage the extended dwell times of travelers for premium sales. The introduction of metro connectivity has further boosted sales, with cafés near stations benefiting from impulsive purchases, thanks to their strategic links to both residential and business areas. Additionally, mixed-use developments in Lusail are seen as a goldmine, promising sustained footfall and attracting investors who are willing to trade immediate traffic for the allure of lower rents. Given these trends, channels associated with travel and mobility are poised for significant growth.

By Service Type: Delivery Extends Reach

In 2025, dine-in channels held sway over Qatar's foodservice market, commanding a 64.72% share, thanks to their immersive ambiance and social allure. These establishments attract consumers who value experience over speed, especially in full-service and leisure contexts. Yet, as younger generations lean towards convenience in their fast-paced lives, the dominance of dine-ins is slowly waning. In response, restaurants are bolstering loyalty programs and enhancing ambiance to maintain foot traffic. Despite the mounting competition, the cultural significance and scale of dine-ins ensure their continued prominence. Furthermore, the integration of technology, such as digital menus and contactless payments, is helping dine-in venues stay relevant in a competitive market.

On the other hand, delivery platforms are making significant strides, boasting an 11.88% CAGR, and are now outpacing dine-ins, thanks to the expanding reach of aggregator networks. Notable consolidations, such as Jahez’s acquisition of Snoonu, are harnessing AI for load balancing and fine-tuning last-mile logistics, leading to reduced fulfillment costs per order. In a bid to reclaim margins and harness customer data, operators are rolling out first-party apps, incentivizing loyalty. Additionally, takeaways are amplifying this trend with curbside pickup lanes and specialized windows, effectively cutting down wait times. The growing adoption of eco-friendly packaging by delivery platforms is also appealing to environmentally conscious consumers, further driving their growth.

Geography Analysis

Population density, corporate offices, and tourist attractions significantly drive most spending in Doha and its satellite areas, making them key contributors to the region's foodservice market. West Bay and The Pearl, known for their numerous premium full-service units, continue to attract high-end consumers. However, these areas face challenges due to rising rent inflation, which impacts operational costs and profitability for foodservice operators. Lusail City is rapidly emerging as a prominent hotspot, owing to its pedestrian-friendly urban design and efficient Metro connectivity. These features not only enhance accessibility but also support the growth of food halls and casual dining establishments, making it an attractive destination for both residents and visitors. Secondary centers such as Al Wakrah and Al Khor are also witnessing significant developments, with outlet roll-outs targeting their growing residential populations. These expansions provide new opportunities for the Qatar foodservice market to cater to untapped demand and diversify its offerings.

Metro extensions are playing a pivotal role in transforming the foodservice landscape by reducing travel times and increasing footfall at stations. This surge in station activity is fueling the popularity of grab-and-go formats, which cater to the needs of commuters and busy urban dwellers. Additionally, the Tawteen program is driving a shift towards peri-urban farming, encouraging suppliers to focus on local production. This initiative not only enhances the potential for local sourcing but also strengthens the supply chain by reducing dependency on imports.

Operators are increasingly turning to geographic diversification as a strategy to counteract the challenges posed by rent volatility. By venturing into untapped demand corridors, businesses not only tap into fresh customer bases but also reduce their dependency on high-rent areas, thereby spreading financial risks. This approach enables operators to adapt to shifting market dynamics and strengthens their growth prospects in Qatar's fiercely competitive foodservice arena.

Competitive Landscape

In Qatar's foodservice market, fragmented competition presents significant opportunities for local entrepreneurs and international franchises alike. This market structure allows for varied strategies: independent operators focus on cultural authenticity and customized menus, while chain concepts benefit from brand recognition and standardized operations. The diversity in approaches caters to a wide range of consumer preferences, making the market dynamic and competitive.

While a select few master franchisees oversee global brands, independent operators continue to hold cultural significance and offer niche variety. Americana, with a debt-free balance sheet, operates 109 units of KFC, Pizza Hut, and Hardee’s, and is pioneering AI workforce software to enhance operational efficiency and reduce labor costs. Alshaya is rapidly expanding Starbucks, leveraging its strong brand equity and consumer loyalty. Al Mana oversees 75 McDonald’s locations, all of which embraced fully recyclable packaging in 2024, aligning with global sustainability trends and consumer demand for eco-friendly practices. As Qatar's coffee culture flourishes, the Apparel Group is expanding its Burger King and Tim Hortons presence, tapping into the growing demand for quick-service restaurants and premium coffee offerings.

Key strategies include optimizing last-mile logistics, refining menus through data insights, and prioritizing sustainable packaging. By vertically integrating into dairy and produce, chains bolster their defenses against import fluctuations, thanks to Tawteen, which supports local sourcing and reduces dependency on imports. Meanwhile, tech-forward disruptors and delivery platforms are urging traditional players to merge dine-in experiences with delivery services, reshaping the landscape of Qatar's foodservice market. This omnichannel approach ensures that businesses cater to evolving consumer preferences for convenience without compromising on the dining experience.

Qatar Foodservice Industry Leaders

-

Al Mana Restaurants & Food Company

-

Almuftah Group

-

Americana Restaurants International PLC

-

M.H. Alshaya Co. WLL

-

Teatime

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Alshaya Group has made its mark in Qatar by inaugurating the first-ever Chipotle Mexican Grill restaurant, heralding the brand's entry into the Qatari market. This launch not only diversifies Alshaya's already extensive portfolio of global foodservice brands but also introduces Qatari diners to Chipotle's renowned customizable Mexican dishes.

- July 2025: Americana Restaurants inked an exclusive franchise deal, introducing the upscale Greek café and retail brand, Carpo, to the Middle East. This pact bestows Americana with the sole rights to run Carpo outlets in both Kuwait and Qatar.

- June 2025: In a bid to enhance its culinary offerings, Qatar Airways has teamed up with renowned French chef Yannick Alléno. This collaboration has led to the inauguration of the Pavyllon restaurant, situated in the Qatar Airways Al Safwa First Lounge at Doha's Hamad International Airport.

- April 2025: MARZA Restaurant, Qatar's largest multi-cuisine dining destination, has officially opened its doors at the Midmac Roundabout on Salwa Road. The restaurant unveiled "Chai Story," a 24-hour tea counter that offers authentic South Indian delicacies, perfectly complemented by Samovar tea.

Qatar Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms