Pipeline Monitoring System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.20 Billion |

| Market Size (2031) | USD 22.40 Billion |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pipeline Monitoring System Market Analysis by Mordor Intelligence

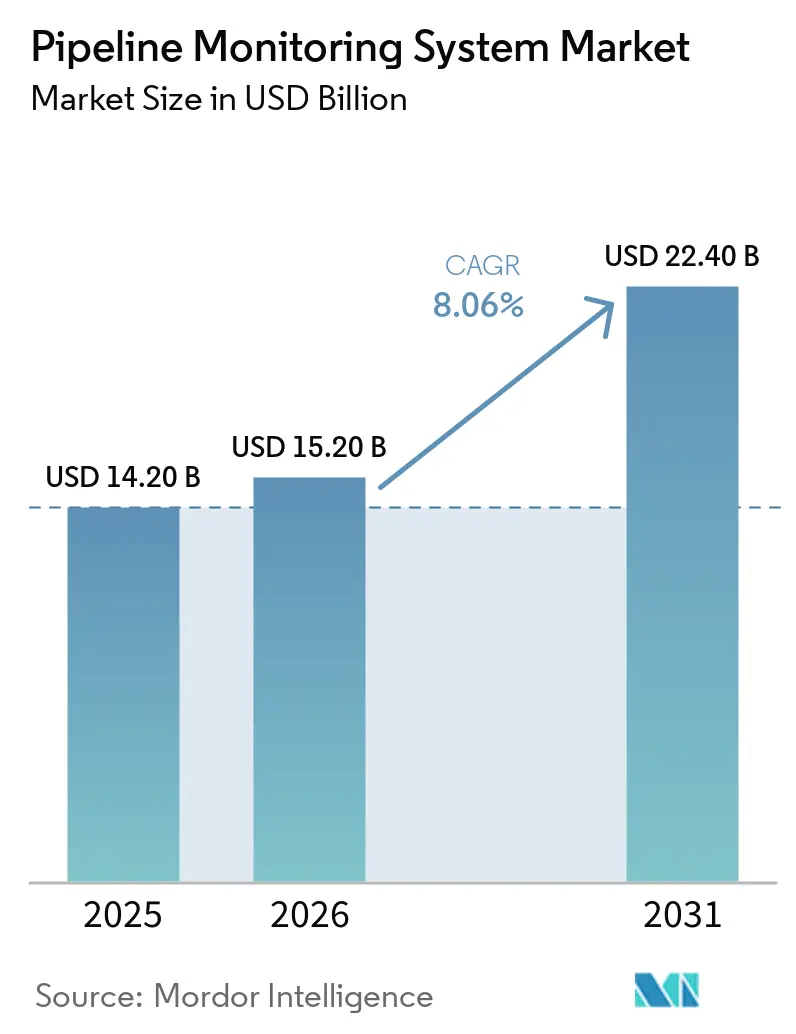

The Pipeline Monitoring System Market size is projected to be USD 14.20 billion in 2025, USD 15.20 billion in 2026, and reach USD 22.40 billion by 2031, growing at a CAGR of 8.06% from 2026 to 2031.

The pipeline monitoring system market is growing, supported by regulatory compliance and infrastructure investment, as operator spending is now more closely tied to enforceable safety and leak-detection requirements than to discretionary inspection timing. In the United States, the January 2025 PHMSA leak detection rule introduced an Advanced Leak Detection Program under 49 CFR § 192.763, raising the minimum performance standard for gas pipeline monitoring programs. At the same time, the International Energy Agency reported that global natural gas investment rose by more than 10% year over year to USD 330 billion in 2026, supporting increased transmission line construction and new monitoring demand during initial commissioning. The pipeline monitoring system market is also benefiting from the wider use of AI, IIoT sensor networks, and real-time analytics, which are changing how operators balance inspection costs, uptime, and regulatory exposure. Competitive pressure is rising because large automation firms retain installed-base advantages, while specialist sensing and inspection vendors are gaining share where distributed sensing, smart pigging, and predictive analytics matter most.

Key Report Takeaways

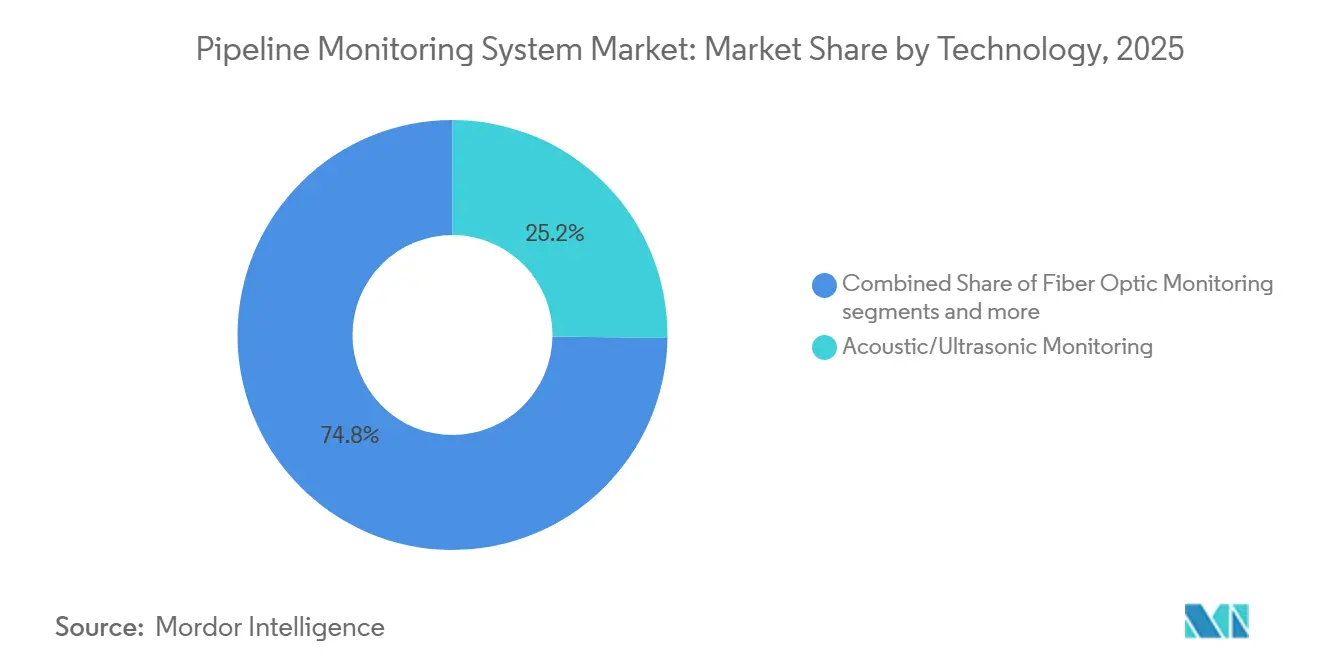

- By technology, acoustic and ultrasonic monitoring technologies led with 25.2% share of the pipeline monitoring system market size in 2025, while Smart PIG monitoring was the fastest-growing technology segment through 2031.

- By component, hardware accounted for 52.3% share in 2025, while software is projected to expand at a 10.3% CAGR through 2031.

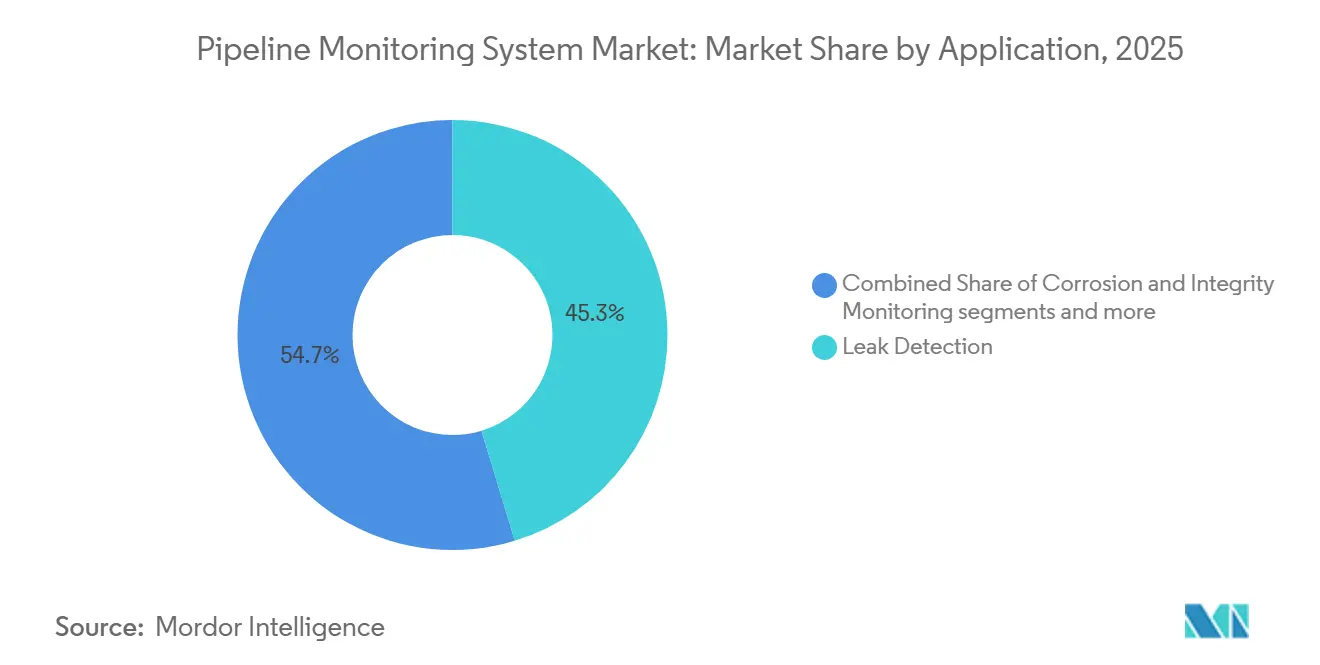

- By application, leak detection accounted for 45.3% of pipeline monitoring system market share in 2025, while real-time data analytics was the fastest-growing application over the forecast period.

- By pipeline type, oil pipelines accounted for the largest revenue share in 2025, while gas pipelines are projected to grow at a 9.5% CAGR through 2031.

- By deployment, onshore accounted for 72.3% of revenue in 2025, while offshore was the faster-growing deployment segment through 2031.

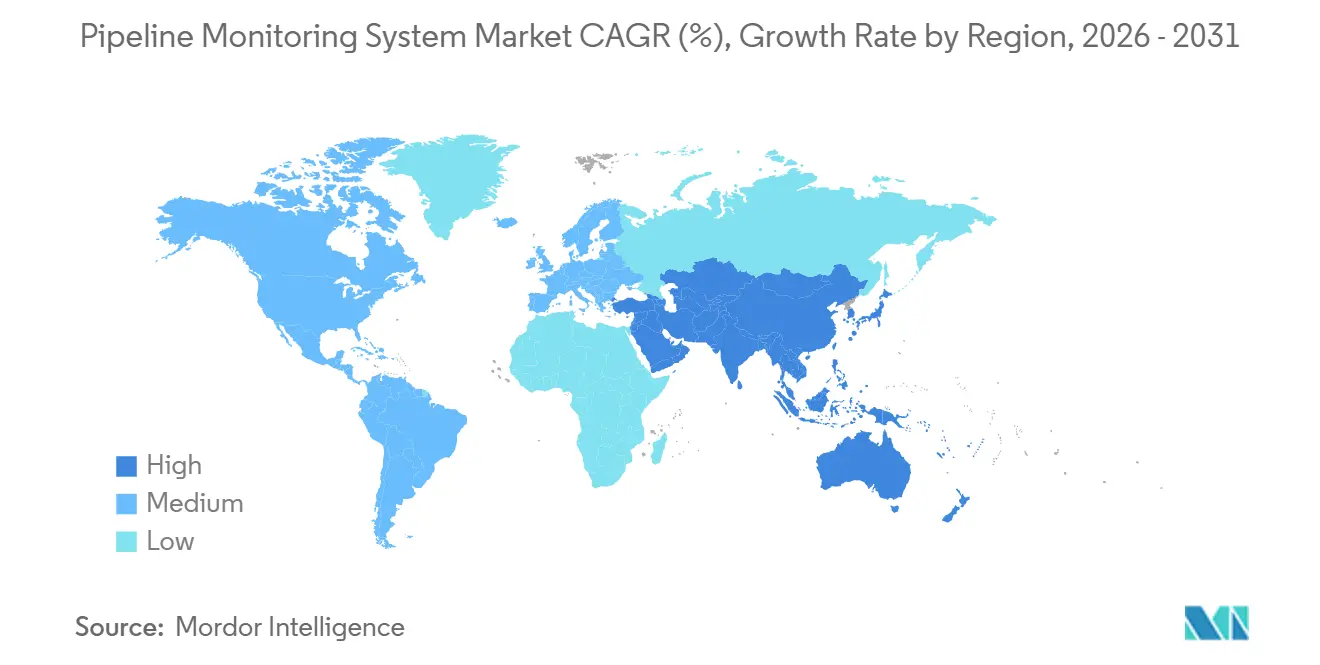

- By geography, North America held a 28.3% share in 2025, while Asia-Pacific is forecast to expand at a 10.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pipeline Monitoring System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Crude Oil and Natural Gas Pipeline Expansion Projects | +2.1% | Global, concentrated in North America, Asia-Pacific, and the Middle East | Short term (≤ 2 years) |

| Increasing Integration of AI, IoT, and Predictive Analytics in Pipeline Operations | +1.8% | Global, early leaders in North America and Europe, with spillover to the Asia-Pacific | Medium term (2-4 years) |

| Rising Incidents of Pipeline Leaks and Corrosion Failures | +1.5% | Global, concentrated in North America, and aging infrastructure markets | Short term (≤ 2 years) |

| Stringent Environmental and Pipeline Safety Regulations | +1.2% | North America and Europe are core markets, with growing relevance in Asia-Pacific, the Middle East, and Africa. | Medium term (2-4 years) |

| Growing Adoption of Fiber Optic Monitoring in Long-Distance Pipelines | +0.8% | Global, led by North America and Asia-Pacific long-haul networks | Medium term (2-4 years) |

| Rising Offshore Pipeline Installations and Deepwater Energy Projects | +0.6% | Asia-Pacific, South America, the Middle East, Africa, and the offshore Gulf of America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Crude Oil and Natural Gas Pipeline Expansion Projects Globally

Pipeline expansion is the clearest near-term demand driver for the pipeline monitoring system market because every new line requires instrumentation from commissioning onward. The United States Energy Information Administration stated in 2026 that 12 new or expanded United States natural gas pipeline projects were scheduled for completion this year, adding close to 18 Bcf/d of capacity, the largest annual addition since 2008.[1]U.S. Energy Information Administration, “Most Natural Gas Pipelines Built in 2025 Connect the South Central United States to Supply,” U.S. Energy Information Administration, eia.gov The INGAA Foundation also projected in its 2025 midstream infrastructure report that more than USD 1 trillion in total midstream capital investment will be required through 2052, including at least 37,000 additional miles of United States gas transmission pipelines.[2]INGAA Foundation, “2025 North American Midstream Infrastructure Report,” INGAA Foundation, ingaa.org In Canada, Enbridge received federal approval in April 2026 for the USD 4 billion Sunrise Expansion Program on the West Coast pipeline system, with construction set to begin in July 2026. The pipeline monitoring system market is also gaining a broader demand base because intrastate pipeline additions accounted for close to 65% of United States capacity added in 2025, indicating that monitoring choices are shaped by a mix of federal rules, state oversight, and operator judgment rather than a single regulatory path.

Increasing Integration of AI, IoT, and Predictive Analytics in Pipeline Operations

The main technology-led growth path in the pipeline monitoring system market is the shift from periodic inspection toward condition-based maintenance supported by AI and connected sensors. A 2026 peer-reviewed study in npj materials degradation described machine learning applied to multi-sensor in-line inspection data as a key step in turning high data volumes into predictive maintenance actions and noted that signal complexity, rather than hardware limitations, is now the main challenge. The Society of Petroleum Engineers also highlighted in 2025 that AI applications for offshore pipeline integrity are enabling real-time condition monitoring in locations where operators once relied mainly on periodic inspection runs.[3]Society of Petroleum Engineers, “A Practical Distributed Acoustic Sensing Approach for Gas-Pipeline-Leak Detection,” SPE Journal, jpt.spe.org In the pipeline monitoring system market, this is shifting value toward software layers that can score anomalies, support digital twins, and shorten the detection gap between inspections. It is also changing procurement behavior because vendors with stronger data models and longer operating histories are in a better position than firms that sell hardware alone. As a result, the pipeline monitoring system market is seeing a gradual shift toward recurring software and analytics revenue.

Rising Incidents of Pipeline Leaks and Corrosion Failures

Failure events continue to support non-discretionary spending in the pipeline monitoring system market across both new and aging assets. AMPP reported in March 2026 that corrosion accounted for more than 25% of PHMSA-reported incidents in 2024, compared with a longer-term average of about 18%, and that it remained one of the largest contributors to the 600 to 700 incidents PHMSA tracks each year across the United States network. PHMSA data cited in the submitted draft also showed that internal corrosion was the leading cause of hazardous liquid incidents between 2010 and 2024, which supports demand for continuous ultrasonic and magnetic flux leakage-based monitoring. The demand pattern is uneven, as Texas alone accounted for nearly 37% of 2024 United States pipeline incidents, creating concentrated regional demand for terrain-specific monitoring solutions. Under 49 CFR Part 195, corrosion-related failures in high-consequence areas trigger mandatory integrity assessments, so in the pipeline monitoring system market, corrosion monitoring is becoming the minimum compliance layer rather than an optional optimization tool.

Stringent Environmental and Pipeline Safety Regulations

The regulatory base supporting the pipeline monitoring system market has strengthened as requirements shift away from fixed inspection schedules toward performance-based risk management. In January 2025, PHMSA finalized the Gas Pipeline Leak Detection and Repair Rule, which introduced the Advanced Leak Detection Program standard under 49 CFR § 192.763 and broadened the need for credible leak detection capability beyond the most sensitive segments. In Europe, the EU Methane Regulation 2024/1787 entered into force in August 2024 and established binding leak detection and repair obligations for oil and gas infrastructure across member states. API RP 1173 and ISO 13623 reinforce the broader move toward formalized safety management and risk-based integrity programs, which raise specification requirements for monitoring systems even in markets that do not yet have equally detailed national rules. The pipeline monitoring system market is therefore expanding not only because more pipelines are being built, but also because the compliance threshold per pipeline is getting higher. That combination increases both addressable volume and system complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Installation and Integration Costs of Advanced Monitoring Systems | -1.8% | Global, especially pronounced in South America, the Middle East, and Africa, and cost-constrained operators | Short term (≤ 2 years) |

| Cybersecurity Risks Associated with Connected Pipeline Monitoring Networks | -0.9% | North America, Europe, and any operator with SCADA or ICS connectivity | Medium term (2-4 years) |

| Operational Challenges in Retrofitting Aging Pipeline Infrastructure | -0.7% | North America and Europe, where the infrastructure is mature and aging | Medium term (2-4 years) |

| Limited Monitoring Efficiency in Remote and Harsh Environments | -0.5% | Asia-Pacific remote regions, the Middle East and Africa desert environments, the Arctic, and deep offshore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Installation and Integration Costs of Advanced Monitoring Systems

Capital intensity remains the clearest adoption barrier for the pipeline monitoring system market, especially where operators work under tight budgets. Distributed fiber-optic monitoring for long-haul pipelines requires high-grade cable, interrogation units, and integration with existing SCADA systems, and costs rise further in difficult terrain or subsea routes. For mid-sized operators and many state-owned entities in South America and Sub-Saharan Africa, that cost burden still favors legacy periodic inspection over fully digital monitoring. The challenge is greater on live networks because upgrades often require replacing remote terminal units, software licensing, validation work, and long commissioning cycles. The pipeline monitoring system market is gaining some relief as sensor prices fall and cloud analytics reduce the need for on-premises infrastructure. Still, that improvement is uneven across regions and does not remove the near-term funding hurdle. As a result, lifecycle savings are often acknowledged before purchase, but not always enough to accelerate final approvals.

Cybersecurity Risks Associated with Connected Pipeline Monitoring Networks

Cyber risk is now an embedded constraint on the pipeline monitoring system market because more monitoring value depends on connected architectures. In November 2024, TSA published a proposed rule to make cyber risk management programs permanent for critical pipeline operators, and it directly recognized that connected SCADA and industrial control systems present systemic vulnerabilities across the pipeline network. TSA Security Directive Pipeline-2021-02F, effective in May 2025, requires designated critical operators to implement continuous monitoring, stronger access controls, and annual cybersecurity assessments. ISA/IEC 62443 also pushes operators toward tighter segmentation of critical control systems, but many older networks still lack that architecture because retrofits are costly and complex. In the pipeline monitoring system market, this creates a trade-off: some operators delay digital upgrades to limit cyber exposure, even though that delay also limits real-time visibility. That hesitation slows adoption most in the very systems where analytics and remote supervision could add the most value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Acoustic and Ultrasonic Methods Anchor Share While Smart PIGs Lead Growth

Acoustic and ultrasonic methods accounted for 25.2% of the pipeline monitoring system market share in 2025, maintaining this technology group in the leading position. That leadership reflects broad use across leak detection and corrosion assessment, as well as compatibility across onshore and offshore pipeline configurations. Acoustic emission systems capture stress-wave signals from crack growth and localized leaks, making them useful for passive, continuous surveillance. Ultrasonic testing, including through-wall and guided-wave variants, remains important because it can quantify wall loss with very high resolution on liquid-filled lines.

The pipeline monitoring system market is now seeing faster growth from Smart PIG solutions, as operators need more frequent and more detailed inline inspection on high-consequence transmission lines. Smart PIG platforms are becoming more capable as vendors combine magnetic flux leakage, ultrasonic caliper tools, and inertial measurement systems into a single inspection run. A 2026 peer-reviewed review in npj Materials Degradation stated that machine learning-assisted signal processing is helping convert dense in-line inspection data into predictive maintenance actions, thereby increasing the practical value of these tools. Fiber-optic monitoring is also gaining ground in the pipeline monitoring system market, especially on long-haul gas networks, where distributed acoustic sensing can improve detectability in sections that are difficult to monitor with external installation methods alone. Magnetic flux leakage remains the most widely deployed in-line inspection method in many operating environments, while lower-field variants are attracting attention for defects that conventional high-field tools do not isolate as well. International framework standards such as ISO 13623 and DNV-ST-F101 continue to shape technology selection, especially where domestic rules are still evolving.

By Component: Hardware Anchors Revenue, While Software Expands the Fastest

Hardware accounted for the largest share of the pipeline monitoring system market in 2025, as every monitored pipeline still requires physical field devices. That includes control systems, remote terminal units, flow computers, pressure transducers, and acoustic or ultrasonic sensor arrays deployed over long distances. New-build pipelines continue to drive incremental hardware demand because instrumentation is required from the first day of operation. Replacement demand is also rising as legacy devices no longer meet updated leak-detection and performance standards.

Software is the fastest-growing component in the pipeline monitoring system market and is projected to grow at a 10.3% CAGR from 2026 to 2031. This growth is tied to cloud-hosted SCADA environments, analytics subscriptions, and digital twin tools that process multi-sensor data in near real time. As sensor hardware becomes more standardized, commercial value is shifting toward interpretation layers that convert field data into alarms, maintenance priorities, and operational decisions. That change is also compressing hardware pricing power in parts of the pipeline monitoring system industry where basic field instrumentation is becoming less differentiated. Services remain an important revenue layer because commissioning, calibration, managed inspection, and long-term maintenance support are still difficult for many operators to manage internally. Vendors with stronger software libraries and longer data histories, therefore, have a clear edge over hardware-only challengers.

By Application: Leak Detection Holds the Largest Base While Analytics Delivers the Fastest Momentum

Leak detection accounted for 45.3% of the pipeline monitoring system market in 2025, making it the largest application area. That position reflects both regulatory requirements and the direct costs of undetected releases across oil and gas transmission systems. Computational pipeline monitoring, pressure-point analysis, and negative-pressure-wave methods still form the base of many existing systems. At the same time, acoustic and fiber-optic methods are gaining greater prominence, as pressure-only approaches no longer meet the required detection performance.

Real-time data analytics is the fastest-growing application in the pipeline monitoring system market because operators need more than raw sensor outputs to make faster decisions. Acoustic, ultrasonic, and fiber-optic arrays generate large data volumes, and without AI-based classification, these systems can cause operational overload rather than produce usable action. Corrosion and integrity monitoring remains the second-largest application block because aging carbon-steel infrastructure continues to face external corrosion, internal erosion, and stress corrosion cracking across many networks. Operational monitoring is also attracting renewed spending as operators try to optimize throughput and defer new construction amid elevated project costs. A less visible change in the pipeline monitoring system market is that analytics buying decisions are moving beyond field engineering teams toward IT and data functions. That shift increases the importance of interoperability, cybersecurity, and API compatibility during procurement.

By Pipeline Type: Oil Pipelines Lead Revenue While Gas Pipelines Drive Growth

Oil pipelines accounted for the largest share of revenue in the pipeline monitoring system market by pipeline type in 2025. Hazardous liquid systems operate under stringent monitoring and integrity requirements, especially under 49 CFR Part 195, and rely on multiple monitoring layers for leak detection, corrosion control, cathodic protection assessment, and smart pig inspection. That broad compliance burden supports higher per-line spending than in many other pipeline categories. Oil pipeline monitoring demand also remains relatively stable because hazardous liquid operators cannot delay safety-critical programs for long.

Gas pipelines are the fastest-growing pipeline type in the pipeline monitoring system market and are forecast to grow at 9.5% CAGR from 2026 to 2031. The strongest demand support comes from the United States buildout cycle, where the EIA tracks 44.9 Bcf/d of new natural gas pipeline capacity expected in 2026 and 2027, following another 6.3 Bcf/d added in 2025. India is advancing this growth path through major gas infrastructure development, including the 3,306 km Jagdishpur-Haldia-Bokaro-Dhamra line, scheduled for completion by September 2026. Water and wastewater pipelines are also opening a secondary demand stream in the pipeline monitoring system market, as aging municipal networks and smart infrastructure programs require acoustic leak detection and pressure monitoring. Chemical pipelines are shorter overall, but spending per kilometer is often higher because the hazard profile is more severe. India’s proposed LPG pipeline expansion program, valued at INR 12,500 crore (USD 1.5 billion), also points to broader demand for non-road transport monitoring as network coverage expands.

By Deployment: Onshore Dominates Volume While Offshore Requires Higher Monitoring Intensity

Onshore deployment accounted for 72.3% of the pipeline monitoring system market in 2025, as global onshore networks are longer and more established than offshore systems. Installation practices are better standardized on land, per-unit sensor costs are lower, and vendor availability is broader. New onshore demand continues to closely track North American expansion and the Asian gas network buildout. The INGAA Foundation’s 2025 report, which projected at least 37,000 additional miles of United States gas transmission lines through 2052, supports a durable base for future onshore instrumentation demand.

Offshore is the fastest-growing deployment segment in the pipeline monitoring system market because deepwater and remote projects require more intensive surveillance and often face higher-consequence exposure. In subsea environments, in-line inspection campaigns require specialist vessels, higher day rates, and supporting infrastructure that older assets do not always have. That cost structure favors fixed alternatives such as subsea distributed acoustic sensing and acoustic monitoring arrays. Europe adds one visible example with Romania’s Neptun Deep gas development, which involves EUR 4 billion (USD 4.3 billion) in total investment and active pipelaying in 2026. DNV-ST-F101 and API RP 1160 remain important reference frameworks for offshore monitoring intervals, data requirements, and risk-based inspection logic. The result is that the pipeline monitoring system market grows faster offshore, even though the route length is much smaller than onshore.

Geography Analysis

North America held a 28.3% share of the pipeline monitoring system market in 2025, maintaining its leading regional position. The region benefits from a very large regulated pipeline base, strong federal oversight, and a new gas capacity buildout cycle. In the United States, the EIA said 12 natural gas pipeline projects were scheduled for completion in 2026, adding close to 18 Bcf/d of capacity, making this the largest annual buildout since 2008. The PHMSA leak detection rule, finalized in January 2025, and the TSA Security Directive Pipeline-2021-02F, effective in May 2025, have also tightened compliance expectations for gas and hazardous liquid operators. Canada adds to this base through Enbridge’s Sunrise Expansion approval in April 2026, while Mexico’s growing import pipeline network broadens the regional opportunity beyond long-established operators.

Asia-Pacific is the fastest-growing regional market for pipeline monitoring systems, with a 10.2% CAGR forecast through 2031. India remains central to that growth because the Jagdishpur-Haldia-Bokaro-Dhamra pipeline is targeting completion in September 2026, while other large crude and gas corridor projects are also moving toward commissioning. China is expanding transmission capacity through a new fourth-line contract on the Central Asia-China system in 2026, while domestic gas networks continue to scale to meet industrial and residential demand. Southeast Asia is also becoming a more visible source of monitoring demand as Indonesia, Vietnam, and Malaysia expand offshore gas infrastructure for domestic power and industrial use. The pipeline monitoring system market in this region, therefore, benefits from both onshore transmission growth and offshore surveillance needs.

Europe remains a strategically important market for pipeline monitoring systems, supported by an increasingly stringent regulatory framework and ongoing offshore infrastructure development. The EU Methane Regulation 2024/1787 has strengthened demand for advanced leak detection and repair solutions by establishing mandatory compliance requirements across oil and gas infrastructure, while Romania's Neptun Deep project is expected to generate additional demand for high-specification monitoring systems during pipeline construction and subsequent operations. In the Middle East and Africa, large pipeline networks, expanding energy infrastructure, and high consequence exposure are driving greater adoption of continuous digital corrosion monitoring and integrity management solutions. The region also offers long-term growth potential as increasing upstream oil and gas investment is expected to support new onshore and offshore pipeline developments, creating sustained demand for monitoring technologies throughout the asset lifecycle.

Competitive Landscape

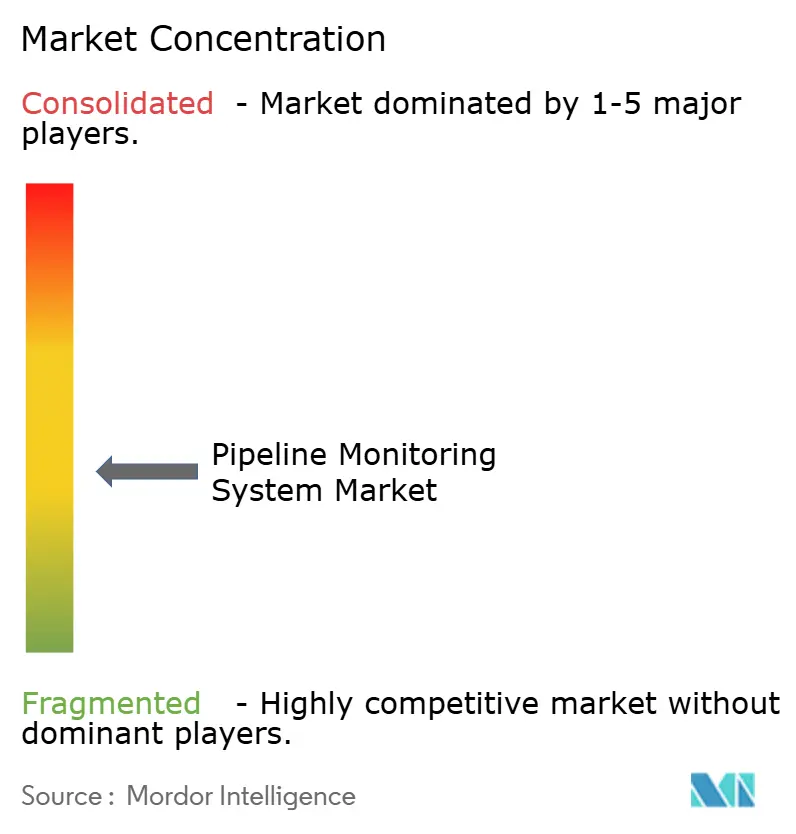

The pipeline monitoring system market was moderately fragmented in 2025. These firms benefit from long service histories, broad product portfolios, and the ability to bundle controls, software, and maintenance into long-term contracts. The next competitive tier is much more fragmented because specialty vendors focus on narrower capabilities, such as fiber-optic sensing, acoustic emission monitoring, in-line inspection, or regional SCADA integration. No single competitive model dominates the market for pipeline monitoring systems. It is shaped by whether an operator values scale, integration depth, field service reach, or specialist technical performance.

Large vendors in the pipeline monitoring system market are increasingly trying to lock in recurring revenue through managed services and software subscription models. Specialist firms are responding by emphasizing proprietary inspection methods, AI-assisted analytics, and non-intrusive assessment tools that can solve problems in unpiggable or high-risk segments. One clear example is ROSEN Group’s Non-Intrusive Pipeline Assessment service, which combines large stand-off magnetometry, AI analytics, and drone-enabled data capture and was recognized with the Business Innovation Award at the Gas Industry Awards 2026 after deployment across more than 700 km of pipelines in 2025. This kind of field-proven specialization is important because it gives mid-tier vendors a way to disrupt incumbent relationships without needing the same installed base. Competitive white space also persists in water and wastewater pipelines, in unpiggable sections, and in newer hydrogen and carbon dioxide pipeline applications where standards are still evolving.

Intellectual property is also becoming increasingly relevant in the pipeline monitoring system market, as vendors differentiate through defect classification models, distributed acoustic sensing signal processing, and low-field magnetic flux leakage refinement. Procurement expectations are rising at the same time, as compliance with ISA/IEC 62443 cybersecurity requirements and API RP 1173 safety management principles is increasingly difficult to avoid in regulated contracts. That raises entry barriers for smaller firms that do not yet have a mature cybersecurity architecture or certification support. The result is a pipeline monitoring system market where growth opportunities are real, but competitive participation is becoming more technically demanding with each new compliance cycle.

Pipeline Monitoring System Industry Leaders

Honeywell International Inc.

Siemens AG

ABB Ltd.

Emerson Electric Co.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ROSEN Group received the Business Innovation Award at the Gas Industry Awards 2026, organized by IGEM and the Energy & Utilities Alliance, for its Non-Intrusive Pipeline Assessment service combining Large Stand-off Magnetometry with AI analytics and drone-enabled data capture. NIPA was deployed across more than 700 km of pipelines in 2025, detecting previously unrecognized metal-loss features requiring repair on operational assets.

- April 2026: Enbridge received Canadian federal government approval for the USD 4 billion Sunrise Expansion Program, adding approximately 300 million cubic feet per day of natural gas transportation capacity to the Westcoast pipeline system in British Columbia. Construction is scheduled to begin in July 2026, with a targeted in-service date in late 2028, requiring integrated monitoring systems across the expanded network.

- January 2025: PHMSA issued the Gas Pipeline Leak Detection and Repair Final Rule, introducing an Advanced Leak Detection Program performance standard under 49 CFR § 192.763 and reducing permissible fugitive and vented emissions from gas transmission operators. The rule creates a compliance-driven demand signal for advanced gas monitoring systems across the United States gas pipeline network.

Global Pipeline Monitoring System Market Report Scope

The Pipeline Monitoring System Report is segmented by technology (Fiber Optic, Acoustic, and more), by Component (Hardware, Software, Services), by Application (Leak Detection, Operational Monitoring, and more), by Pipeline Type (Oil, Gas, and more), by Deployment (Onshore, Offshore), by Geography (North America, South America, and more). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| Fiber Optic Monitoring |

| Acoustic Monitoring |

| Ultrasonic Monitoring |

| Magnetic Flux Leakage (MFL) |

| Smart PIG Monitoring |

| Others |

| Hardware |

| Software |

| Services |

| Leak Detection |

| Corrosion & Integrity Monitoring |

| Operational Monitoring |

| Real-Time Data Analytics |

| Oil Pipelines |

| Gas Pipelines |

| Water & Wastewater Pipelines |

| Chemical Pipelines |

| Onshore |

| Offshore |

| By Technology | Fiber Optic Monitoring |

| Acoustic Monitoring | |

| Ultrasonic Monitoring | |

| Magnetic Flux Leakage (MFL) | |

| Smart PIG Monitoring | |

| Others | |

| By Component | Hardware |

| Software | |

| Services | |

| By Application | Leak Detection |

| Corrosion & Integrity Monitoring | |

| Operational Monitoring | |

| Real-Time Data Analytics | |

| By Pipeline Type | Oil Pipelines |

| Gas Pipelines | |

| Water & Wastewater Pipelines | |

| Chemical Pipelines | |

| By Deployment | Onshore |

| Offshore |

Key Questions Answered in the Report

What is the current size of the pipeline monitoring system space and how fast is it growing?

It stood at USD 14.2 billion in 2025 and is forecast to reach USD 22.4 billion by 2031 at an 8.1% CAGR during 2026-2031.

Why is spending on pipeline monitoring becoming less discretionary?

Newer rules such as the PHMSA leak detection final rule and the EU Methane Regulation have pushed operators toward performance-based monitoring rather than optional inspection timing.

Which region leads today and which one is expanding the fastest?

North America led with 28.3% share in 2025, while Asia-Pacific is projected to grow the fastest at 10.2% CAGR through 2031.

Which application accounts for the largest revenue base?

Leak detection led with 45.3% of revenue in 2025 because it sits at the center of both compliance programs and loss prevention economics.

Why are Smart PIG and analytics solutions gaining traction?

Operators are shifting toward predictive maintenance, and Smart PIG tools plus analytics platforms help convert dense inspection data into earlier and more practical maintenance action.

What is the main barrier to wider adoption of advanced systems?

High installation and integration costs remain the biggest hurdle, especially for operators retrofitting older networks or working in cost-constrained regions.

Page last updated on: