Physical Identity And Access Management (PIAM) Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

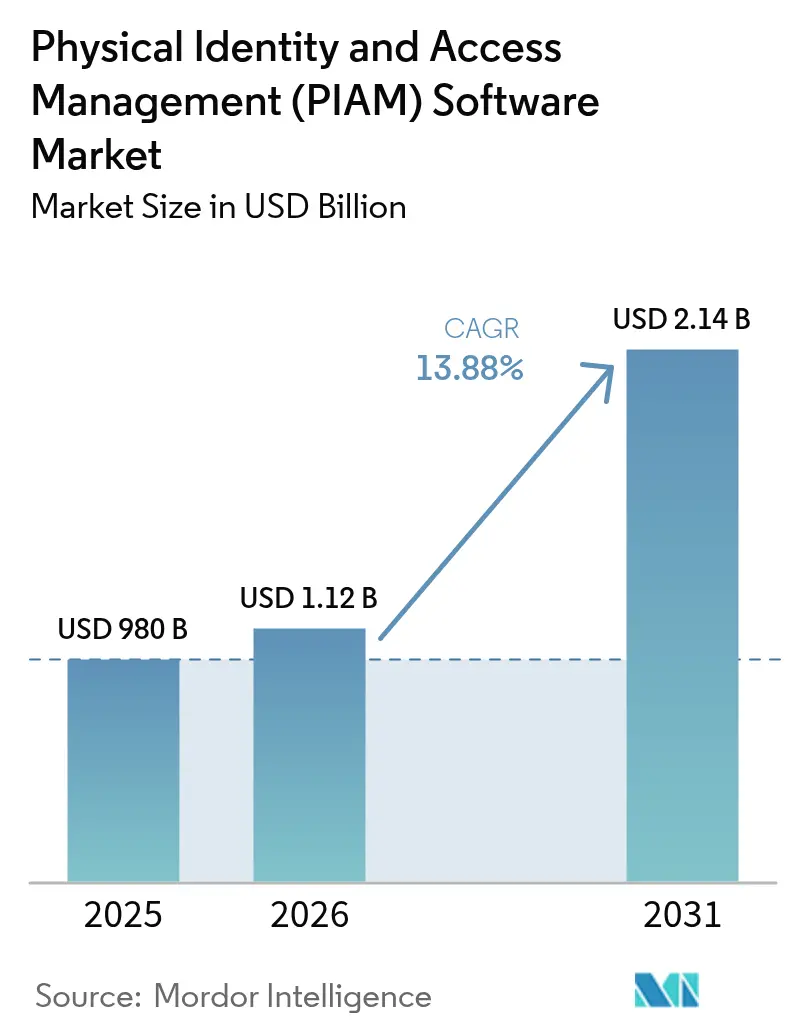

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 13.88% CAGR |

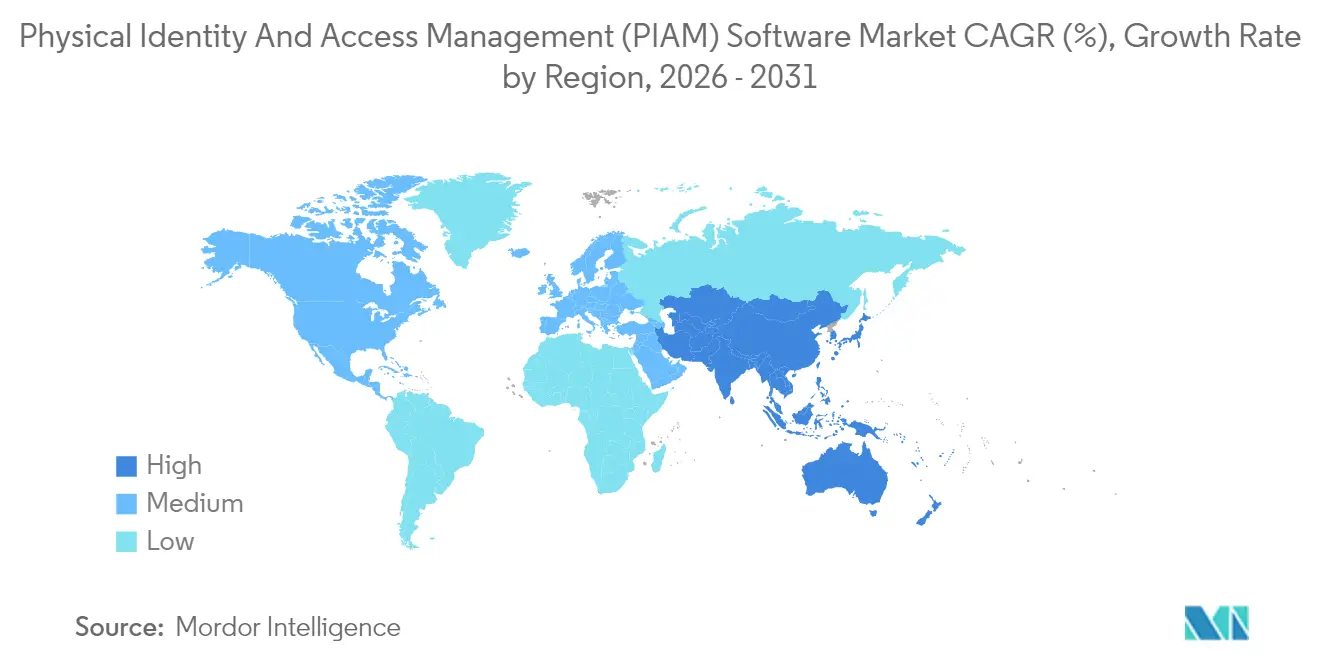

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Physical Identity And Access Management (PIAM) Software Market Analysis by Mordor Intelligence

Physical Identity And Access Management (PIAM) Software Market size in 2026 is estimated at USD 1.12 billion, growing from 2025 value of USD 980 million with 2031 projections showing USD 2.14 billion, growing at 13.88% CAGR over 2026-2031. North America remains as the largest revenue contributor in 2024, but policy moves, such as the European Union’s eIDAS 2.0 wallet mandate and the United States' National Institute of Standards and Technology’s SP 800-217, are accelerating spending in Europe and reshaping procurement criteria worldwide. The Asia-Pacific region is emerging as the fastest-growing region, driven by smart-city investments in Saudi Arabia, China, and India that incorporate biometric eGates and IoT-enabled access nodes from the design phase.[1]NEOM, “Smart Gates Project at NEOM Bay Airport,” neom.com Cloud-native vendors are lowering barriers for small and medium enterprises by eliminating hardware outlays, while large enterprises favor hybrid architectures that keep credential databases on-site yet offload analytics and disaster recovery to the cloud.

Key Report Takeaways

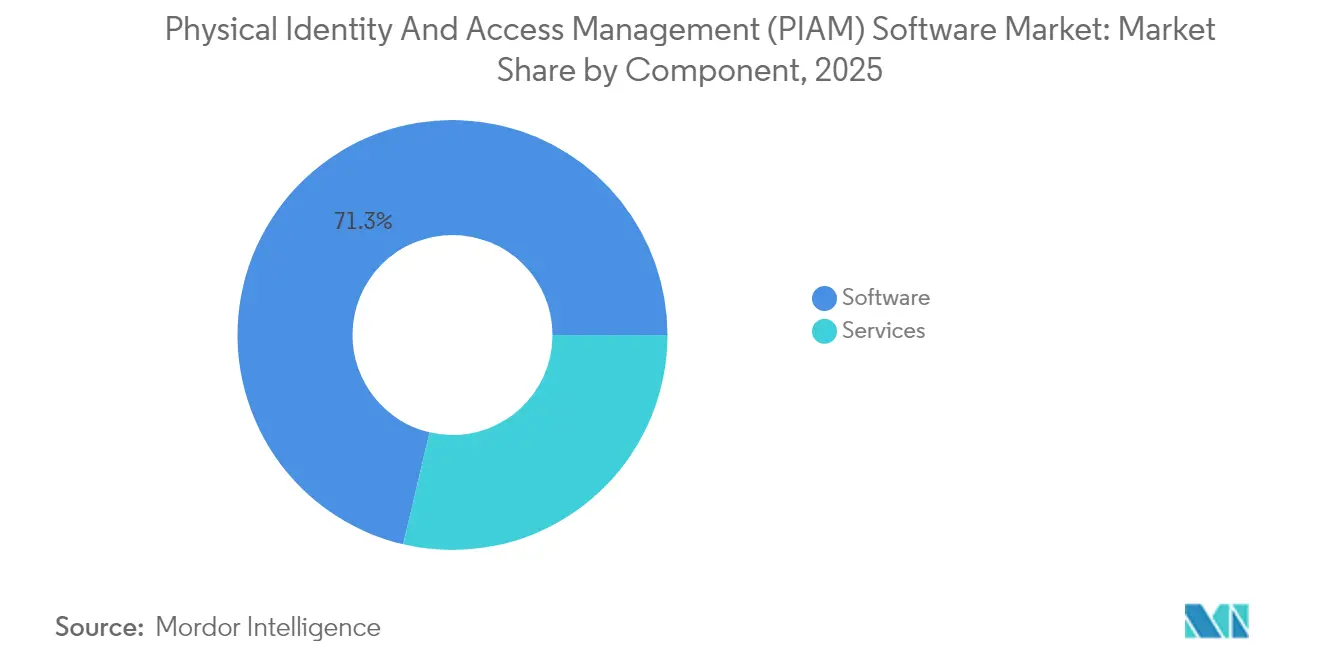

- By component, software led with 71.32% of physical identity and access management market share in 2025; services are forecast to advance at a 16.22% CAGR through 2031.

- By deployment mode, on-premises accounted for 56.75% of the physical identity and access management market size in 2025, while cloud solutions are projected to grow at a 15.05% CAGR to 2031.

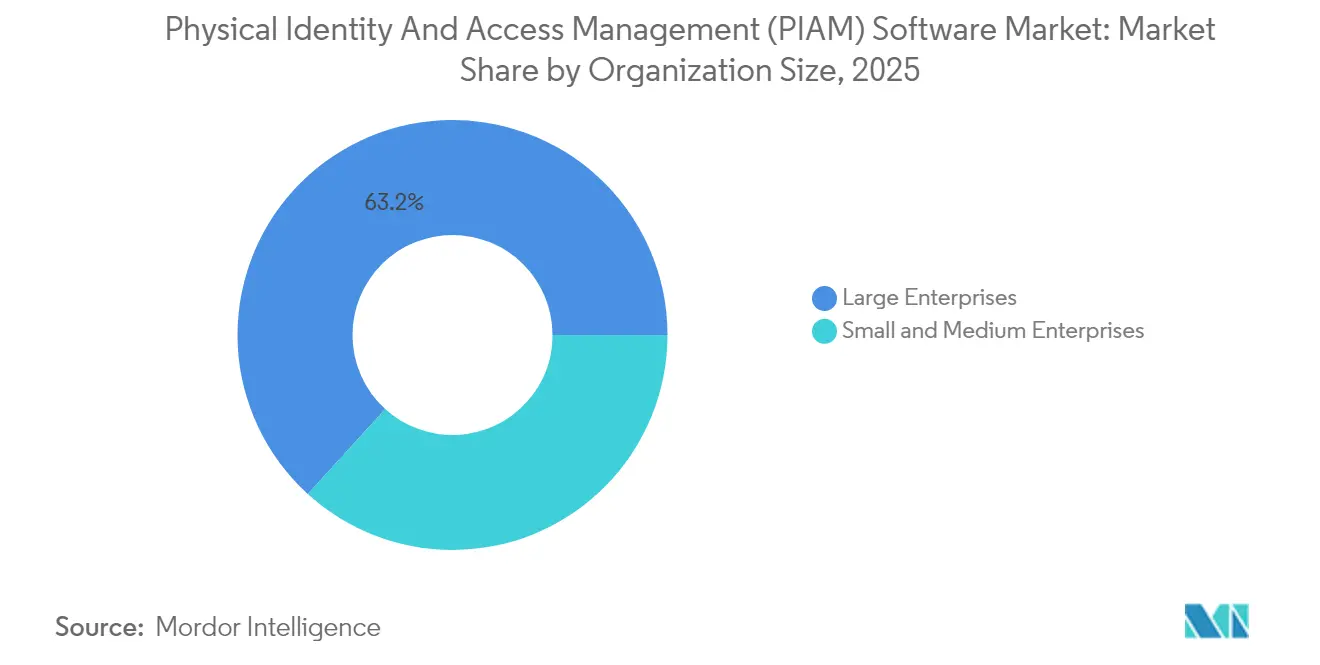

- By organization size, large enterprises contributed 63.25% of the physical identity and access management market size in 2025; small and medium enterprises are poised for a 15.29% CAGR between 2026-2031.

- By end-user industry, banking, financial services, and insurance held 26.05% of the physical identity and access management market size in 2025; healthcare is expanding at a 15.74% CAGR through 2031.

- By geography, North America commanded 36.02% of the physical identity and access management market size in 2025; Asia-Pacific is projected to post the fastest 15.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Physical Identity And Access Management (PIAM) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance mandates from governments | +3.2% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Increasing need to manage on-site visitors and contractors | +2.1% | Global, acute in healthcare and BFSI | Short term (≤ 2 years) |

| Rapid growth of smart buildings and IoT-enabled facilities | +2.8% | Asia-Pacific core, spill-over to Middle East | Long term (≥ 4 years) |

| Rising adoption of cloud-based PIAM platforms by SMEs | +2.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of PIAM with physical security information management | +1.9% | Global, led by critical-infrastructure sectors | Long term (≥ 4 years) |

| Convergence of cyber and physical identity governance | +2.4% | Global, concentrated in large enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compliance Mandates From Governments

Government regulations are shortening refresh cycles for identity systems. Australia’s Digital ID Act 2024 requires agencies to enable citizens to use a single credential for both digital and physical services, prompting the procurement of interoperable platforms that can issue mobile badges and bridge cyber and door-access policies. In the United States, the Cybersecurity and Infrastructure Security Agency’s Zero Trust Maturity Model requires continuous verification at the building entry point, moving agencies away from static swipe cards toward risk-scored decisions.[2]Cybersecurity and Infrastructure Security Agency, “Zero Trust Maturity Model,” cisa.gov ISO/IEC 27001:2022 now embeds physical controls in Annex A, nudging multinational firms to integrate building security into their enterprise governance programs. Collectively, these mandates elevate baseline functionality, such as audit-grade visitor logs and credential revocation, to “must-have” territory, driving the physical identity and access management market toward unified cyber-physical policy engines.

Rapid Growth of Smart Buildings and IoT-Enabled Facilities

Smart-city mega-projects are wiring thousands of sensors, from occupancy counters to HVAC valves, into converged operational networks. These endpoints require unique identities and least-privileged permissions, so owners should treat device onboarding similarly to human provisioning. In the Asia-Pacific region, NEOM’s biometric eGates process travelers without documents and sync credentials with building-management systems for frictionless movement. China’s Xiong’an planners embed PIAM hooks at the blueprint stage, enabling predictive maintenance based on real-time occupancy. Genetec reports that 77% of security leaders now collaborate with IT teams to manage this sensor sprawl, and 43% prefer hybrid cloud designs that ingest IoT telemetry while keeping door decisions at the edge. These practices place PIAM software at the heart of smart-building operating systems, expanding addressable spend beyond doors to every networked asset.

Rising Adoption of Cloud-Based PIAM Platforms by SMEs

Subscription pricing, zero hardware, and mobile onboarding are dismantling entry barriers for small firms. Brivo notes that 68% of its 2024 cohort were SMEs replacing keys and spreadsheets with SaaS consoles. RightCrowd’s tiered SmartAccess starts at USD 600 per year for estates with fewer than 50 doors, creating a clear cost curve for early adopters. Universities and school districts favor SaaS because campus staff can issue, change, or revoke badges from a phone without waiting for a technician. As insurance underwriters tighten requirements for visitor logs, the economics of compliance also tilt in favor of cloud subscription, accelerating penetration into professional-services offices, co-working hubs, and boutique hotels.

Convergence of Cyber and Physical Identity Governance

Chief information security officers now treat building entry as one more authentication vector. AlertEnterprise’s Guardian platform drives this shift by syncing with SAP’s HR modules so that a contract termination instantly deactivates IT credentials, OT permissions, and door badges in a single workflow. CyberArk found that 93% of firms experienced security incidents involving third-party identities in 2024, highlighting the risk of orphaned badges when contractors are off-boarded. NIST’s SP 800-207 formally recommends evaluating physical access under zero-trust tenets, triggering pilot projects where AI agents analyze badge-swipe, network login, and CCTV feeds to score session risk in real-time. This convergence expands seat counts for identity-governance software and positions PIAM as a mandatory extension of privileged-access programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns over security of third-party (cloud) data storage | -1.7% | Global, most acute in government and defense | Short term (≤ 2 years) |

| High up-front integration costs for legacy infrastructure | -2.3% | North America and Europe, older facility stock | Medium term (2-4 years) |

| Shortage of skilled PIAM implementation specialists | -1.1% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Fragmented global regulatory landscape | -0.9% | Global, cross-border operations most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns Over Security of Third-Party (Cloud) Data Storage

Defense agencies are hesitant to store biometric templates in multi-tenant clouds, citing data sovereignty rules and supply chain risks. The United States Department of Defense’s Cybersecurity Maturity Model Certification requires contractors to host PIAM either on FedRAMP-authorized environments or on-premises, effectively excluding many public clouds.[3]Department of Defense, “Cybersecurity Maturity Model Certification,” acq.osd.mil Europe’s GDPR labels biometric data as a “special category,” layering consent and encryption requirements that increase compliance costs for global rollouts. Although providers such as AWS offer customer-managed keys and regional instances, many agencies still view the cloud as an extra attack surface. This perception dampens near-term cloud share in government and classified projects, slowing the trajectory of the physical identity and access management market in those segments.

High Up-Front Integration Costs for Legacy Infrastructure

Facilities equipped with Wiegand readers and RS-485 controllers must either invest in modern IP devices or deploy middleware. The Security Industry Association estimates that converting a 500-door site can cost between USD 200,000 and USD 400,000 in hardware. Sectors like education and hospitality, already juggling thin margins, defer upgrades, which lengthens sales cycles. Systems integrators are increasingly selling phased programs, where cloud software is deployed first, followed by a hardware swap later. However, such hybrids limit analytics and complicate support, tempering adoption speeds in older buildings across North America and Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate as Integration Complexity Mounts

Services contributed a smaller portion of 2025 revenue but are expanding faster than software as projects grow multi-site and multi-vendor. The physical identity and access management market size for services is widening because enterprises face decades of technical debt from proprietary protocols. Convergint Technologies notes that 62% of engagements blend cloud consoles with on-premises door controllers, requiring engineers to be versed in both REST APIs and legacy wiring. Premium consultative packages now include policy template libraries, change management workshops, and managed administration, creating recurring revenue streams. HID Global’s Origo software, built on modular microservices, simplifies configuration while increasing the demand for professional tailoring to match workflows. As clients opt for outcome-based contracts that bundle licenses, upgrades, and monitoring, service providers capture a disproportionate share of incremental spending while reducing the time to value.

Cloud software still dominates the physical identity and access management market share because every deployment starts with a license. However, the mix will continue to tilt toward services through 2031 as subscription vendors embed implementation fees into multi-year commitments. Growth remains strongest where legacy estates require middleware bridges, such as hospitals running Wiegand readers or bank vaults protected by serial controllers. The shortage of certified PIAM specialists in emerging markets further boosts demand for services, positioning integrators with training academies and 24-hour remote support centers as key beneficiaries.

By Deployment Mode: Cloud Gains Ground Despite Sovereignty Headwinds

On-premises deployments retained 56.75% of revenue in 2025. Yet hybrid and cloud models are growing faster, propelled by mobile credential adoption and improved FedRAMP, ISO 27001, and SOC 2 attestations. The physical identity and access management market size associated with cloud is rising as SMEs choose SaaS to bypass server maintenance, and large enterprises leverage elastic compute for video analytics and behavioral risk scoring.

Edge gateways now cache decisions locally, allowing doors to continue functioning during internet loss, while logs are synced back once the links are restored. This architecture alleviates sovereignty concerns and encourages government agencies to offload non-classified workloads. Vendors respond with region-pinned data centers, customer-managed encryption keys, and role-based administration dashboards that audit every API call, chipping away at resistance. On-premises solutions will persist in air-gapped defense labs and ultra-secure data centers, but most green-field sites now default to hybrid topologies.

By Organization Size: SMEs Leapfrog With Subscription Models

Large enterprises still anchor revenue because they manage complex estates, but SMEs represent the fastest-growing segment. Cloud consoles, such as Soloinsight’s CloudGate, let property managers issue QR-code passes from a phone, streamlining onboarding for contractors and guests. Insurance carriers are increasingly requiring audited visitor logs at clinics, law offices, and co-working hubs, prompting small firms to adopt enterprise-grade controls.

The physical identity and access management market share held by large enterprises gradually narrows as SMEs’ proportional spend rises. Tiered licensing allows vendors to capture both segments: Gallagher’s Command Centre offers a starter SaaS edition for sites with fewer than 50 doors and a full-featured on-premises version for national campuses. As inflation pressures budgets, subscription alignment with headcount makes cost planning easier, further enticing small business owners.

By End-User Industry: Healthcare Emerges as Fastest Riser

Banking, financial services, and insurance lead revenue totals due to the stringent Payment Card Industry Data Security Standard (PCI DSS) and data center controls. Yet, hospitals, clinics, and research centers show the most rapid advances. Visitor-management modules tied to electronic medical records ensure only approved family members enter neonatal units, slashing infant-abduction risk. Johns Hopkins Medicine connects badge issuance to patient consent tables, so expired passes deactivate automatically. The physical identity and access management market size for healthcare benefits is driven by infection-control rules that favor touchless biometrics and mobile credentials.

The government and defense sector adopt PIAM to align with Personal Identity Verification (PIV) cards, while energy utilities integrate door events with supervisory control and data acquisition (SCADA) dashboards to meet NERC (North American Electric Reliability Corporation) Critical Infrastructure Protection audits. Education institutions balance open learning environments with emergency lockdown mandates, using PIAM to screen visitors and automate mass-notification messages.

Geography Analysis

North America generated 36.02% of 2025 revenue, buoyed by early SaaS adoption and mature integrator networks. Federal guidelines, such as NIST SP 800-217 and the Cybersecurity Maturity Model Certification, raised the baseline functionality, spurring spending in government, defense, and critical infrastructure. Canada mirrors the United States' patterns, with Crown corporations adopting zero-trust frameworks for both network and facility access.

The Asia-Pacific region is forecast to grow at a 15.98% CAGR, the fastest among regions, driven by national smart-city initiatives. Saudi Arabia’s NEOM airport eGates exemplify biometric ambitions, while India’s Smart Cities Mission channels municipal grants into IoT-ready access nodes embedded in traffic hubs and hospitals. China’s Xiong’an New Area hardwires PIAM APIs into building-management systems, ensuring real-time energy optimization based on occupancy. Local system integrators bundle PIAM with video surveillance and elevator control, offering turnkey packages to property developers.

Europe ranks second in revenue and third in growth. eIDAS 2.0 requires member states to standardize digital wallets that link to door credentials, thereby reducing demand for federated PIAM software. Germany’s automotive plants deploy contractor provisioning modules to support just-in-time manufacturing. The United Kingdom and France are accelerating cloud adoption in the public sector, leveraging local data centers operated by major hyperscalers. Strict GDPR biometric-data rules steer sensitive templates into region-pinned clusters or on-premises stores, shaping hybrid designs.

South America’s market centers on Brazil and Argentina. Banks and border authorities invest in facial-recognition kiosks, while oil refineries retrofit card readers with mobile badge upgrades to reduce administrative overhead. Middle East growth relies heavily on the United Arab Emirates and Saudi Arabia, where sovereign funds fund mega-projects that incorporate mobile access from the outset. Africa shows nascent traction: South African mines adopt ruggedized readers at shafts, and Nigerian banks deploy cloud consoles to monitor distributed branches. Although smaller today, these deployments lay the groundwork for future expansion as regulations modernize.

Competitive Landscape

The supplier field remains moderately fragmented. HID Global, Genetec, and Johnson Controls defend installed bases by layering AI anomaly detection and mobile credentialing on top of proprietary controllers. Cloud-native challengers such as Brivo and AlertEnterprise market open APIs and rapid onboarding to convert first-time buyers. Honeywell’s USD 4.95 billion purchase of Carrier’s Global Access Solutions signals that building-automation giants will bundle HVAC, lighting, fire, and access under unified dashboards, pressuring stand-alone PIAM vendors. SECOM’s USD 192 million investments in Eagle Eye Networks and Brivo indicate investor confidence in SaaS recurring revenue.

Vitaprotech’s USD 145 million acquisition of Identiv’s business adds more than 100 software engineers and a Hirsch brand recognized in government circles. Interoperability standards, such as the Security Industry Association’s Open Supervised Device Protocol, ratified in 2024, lower switching costs and encourage mixed estates, threatening vendors that rely on lock-in. Differentiation is shifting toward AI-powered liveness detection, edge gateways that cache permissions during outages, and privacy-by-design architectures certified to ISO 27001:2022. As consolidation continues, regional integrators that combine local expertise with global vendor ecosystems will exert greater control over channel influence.

Physical Identity And Access Management (PIAM) Software Industry Leaders

HID Global Corporation

AlertEnterprise Inc.

Genetec Inc.

Convergint Technologies LLC

IDCUBE Identification Systems Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SwiftConnect, a player in connected access networks, has officially joined the ServiceNow Build Partner Program. This announcement coincides with the launch of its ServiceNow Spoke integration on the ServiceNow Store. With this integration, SwiftConnect seamlessly links the AI capabilities of ServiceNow to physical access infrastructures. This ensures users enjoy a smooth access experience, eliminating the need to navigate a new interface or implement a specialized physical identity and access management (PIAM) platform.

- October 2025: Cohesion, a frontrunner in cloud-based smart building and IoT software, has proudly announced its attainment of Elite Partner status in the HID Technology Partner Program. This prestigious designation is awarded to only five companies globally. Through this partnership, HID's renowned Origo platform is now more seamlessly integrated with Cohesion's Cloud Access Portal. Notably, Cohesion's portal boasts certifications such as SOC 2 Type II and ISO 27001, and is recognized as a Platinum-certified Physical Identity and Access Management (PIAM) solution by UL Solutions.

- September 2024: RightCrowd, a global leader in physical identity and access management solutions, has formed a partnership with HID, the world's premier provider of trusted identity solutions. This alliance aims to equip enterprises with cutting-edge mobile credential technology, ensuring employees enjoy a seamless and secure digital access experience using their mobile devices.

- September 2024: Vitaprotech completed the acquisition of Identiv’s physical-security unit for USD 145 million, relaunching products under the Hirsch brand and generating USD 185 million in combined revenue.

Global Physical Identity And Access Management (PIAM) Software Market Report Scope

The Physical Identity and Access Management PIAM Software automates identity verification and credential issuance, determining who can access physical spaces like buildings and rooms, and when. By linking HR and IT data with Physical Access Control Systems (PACS), PIAM ensures secure and compliant management of physical entry. It also streamlines visitor management and oversees the entire identity lifecycle.

The Physical Identity and Access Management PIAM Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (On-Premises, and Cloud), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Banking Financial Services and Insurance, Government and Defense, Healthcare, Information Technology and Telecommunications, Energy and Utilities, Education, and Other End-user Industries), and Geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-Premises |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking Financial Services and Insurance (BFSI) |

| Government and Defense |

| Healthcare |

| Information Technology and Telecommunications |

| Energy and Utilities |

| Education |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | Banking Financial Services and Insurance (BFSI) | ||

| Government and Defense | |||

| Healthcare | |||

| Information Technology and Telecommunications | |||

| Energy and Utilities | |||

| Education | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the physical identity and access management market in 2031?

The market is forecast to reach USD 2.14 billion in 2031 on a 13.88% CAGR trajectory.

Which region is expected to record the fastest growth through 2031?

Asia-Pacific is projected to expand at a 15.98% CAGR due to smart-city programs and biometric infrastructure investment.

Why are services growing faster than software in physical identity and access management?

Integration complexity, hybrid cloud architectures, and a shortage of certified specialists are driving enterprises to outsource implementation and ongoing administration.

How do compliance mandates influence purchasing decisions?

Regulations such as eIDAS 2.0, ISO 27001:2022, and the United States Zero Trust Maturity Model require unified cyber-physical identity governance, raising baseline functionality and accelerating modernization projects.

What are the main obstacles to cloud adoption in government projects?

Data-sovereignty rules, FedRAMP requirements, and concerns over storing biometric templates in multi-tenant environments slow migration to public clouds.

Which end-user sector is growing the fastest?

Healthcare leads growth at a 15.74% CAGR as hospitals deploy visitor-management and infant-protection modules tied to electronic medical records.

Page last updated on: