Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

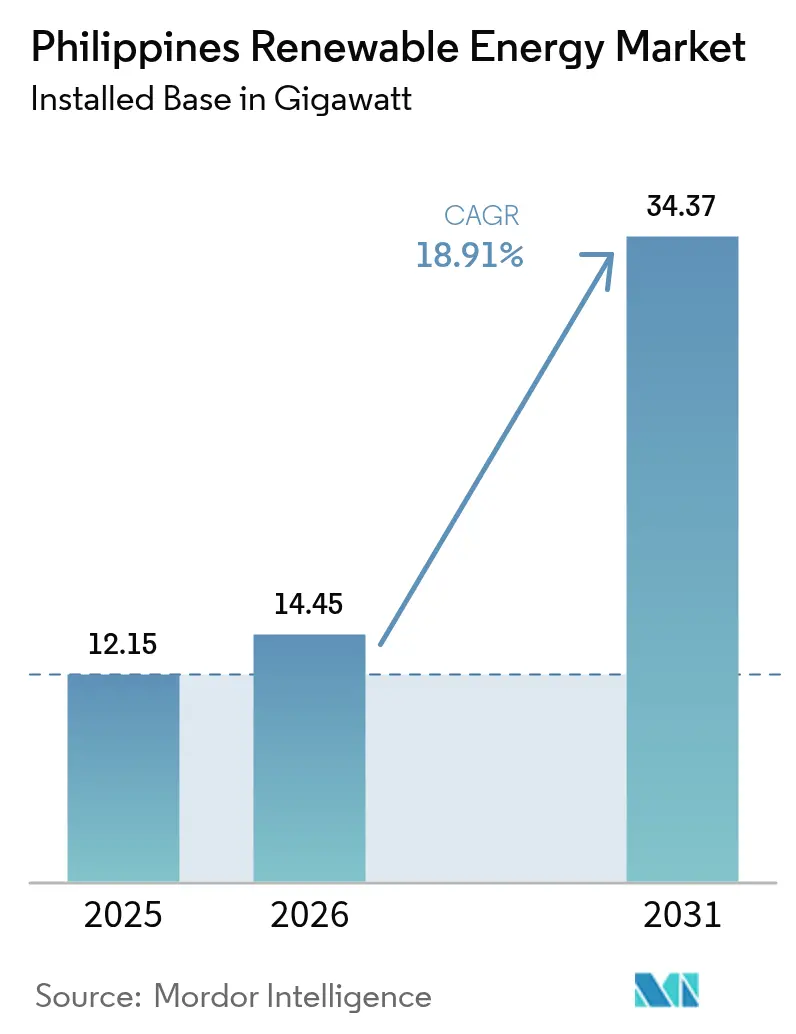

| Base Year Market Size (2025) | 12.15 gigawatt |

| Market Volume (2026) | 14.45 gigawatt |

| Market Volume (2031) | 34.37 gigawatt |

| Growth Rate (2026 - 2031) | 18.91% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Philippines Renewable Energy Market Analysis by Mordor Intelligence

The Philippines Renewable Energy Market size was valued at 12.15 gigawatt in 2025 and estimated to grow from 14.45 gigawatt in 2026 to reach 34.37 gigawatt by 2031, at a CAGR of 18.91% during the forecast period (2026-2031).

Policy-mandated portfolio standards, falling solar and wind equipment costs, rising retail tariffs, and a moratorium on new coal plants are collectively accelerating the shift away from thermal generation. Coal still supplied 60% of electricity in 2022; yet, imminent retirements backed by USD 500 million of concessional capital from the Climate Investment Funds will displace 900 MW of aging capacity, creating headroom for new green projects.[1]Climate Investment Funds, "Philippines Just Energy Transition Program," cif.org Grid-ready assets, notably ACEN’s 600 MW Bataan solar farm and Solar Philippines’ 3.5 GW Terra Solar complex, are capturing first-mover scale advantages and attracting institutional capital. At the same time, the corporate power-purchase market is booming as data centers and 24/7 business-process outsourcing campuses sign long-term offtake contracts to hedge against the country’s region-leading retail tariffs.

Key Report Takeaways

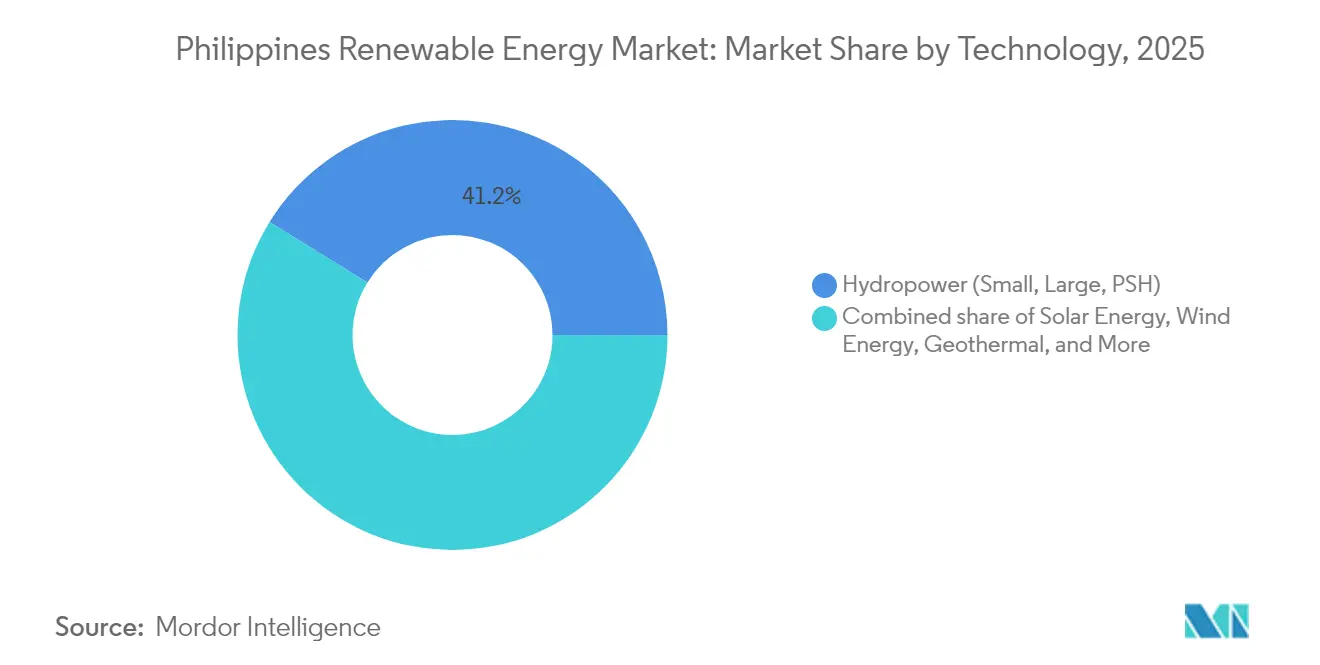

- By technology, hydropower led the Philippines' renewable energy market share with 41.20% in 2025, while ocean energy is projected to post the fastest expansion at a 114.2% CAGR from 2026 to 2031.

- By end-user, utilities held 63.45% of the Philippines' renewable energy market share in 2025, and the commercial and industrial segment is forecast to record the highest growth at a 22.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable Portfolio Standards & Feed-in Tariffs | +3.2% | National, Luzon concentration | Medium term (2-4 years) |

| Declining Solar-PV & Wind Turbine Capex | +4.1% | National, strongest in Luzon and Visayas | Short term (≤ 2 years) |

| Rising Electricity Demand & High Retail Tariffs | +3.8% | Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Corporate PPAs from BPO/IT Hubs | +2.9% | NCR, Cebu IT parks | Short term (≤ 2 years) |

| Grid Upgrades via JICA-funded Projects | +2.5% | Luzon backbone, Visayas links | Long term (≥ 4 years) |

| Disaster-resilient Island & Micro-grid Programs | +1.8% | Mindanao, Palawan, Eastern Visayas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renewable Portfolio Standards & Feed-in Tariffs

The Renewable Portfolio Standard was reset to 11% in 2024 and is expected to increase to 35% by 2030, forcing distribution utilities to contract a third of their supply from clean generators. Feed-in tariffs helped seed initial projects; however, the latest Green Energy Auction Program rounds are now the principal procurement channel, with 3.4 GW awarded in 2024, and storage-linked bids are scheduled for 2025. The Energy Regulatory Commission’s June 2024 circular removed most foreign-ownership caps, simplifying partnership structures. Seven-year income-tax holidays followed by a 10% rate under the CREATE Act sharpen fiscal competitiveness, placing the Philippines among Southeast Asia’s most favorable jurisdictions for greenfield renewables.[2]Energy Regulatory Commission, “DC2024-06-0018,” erc.gov.ph

Declining Solar-PV & Wind Turbine Capex

Global module prices have fallen by 89% since 2010, pushing utility-scale solar levelized costs below PHP 2.50/kWh in Ilocos Norte and Pangasinan. ACEN’s Bataan plant commissioned in 4Q 2024 at under USD 0.60 per watt, 25% under the prior domestic benchmark, while NREL projects offshore-wind costs sliding to USD 34 /MWh by 2050 as floating-platform learning curves mature.[3]National Renewable Energy Laboratory, “Philippines Offshore Wind Roadmap 2025,” nrel.gov Manufacturers Trina Solar and Vestas are integrating bifacial modules and turbines exceeding 5 MW into the Philippine supply chain, accelerating efficiency gains.

Rising Electricity Demand & High Retail Tariffs

Electricity consumption is projected to grow by approximately 5.4% annually to mid-century, increasing the peak load from 16.6 GW in 2022 to 68.5 GW. Meralco’s PHP 11.55–11.64/kWh residential tariff in early 2025 ranks among the region’s highest and incentivizes direct renewable energy sourcing. Evolution Gaming locked in a 100 MW solar PPA at a tariff reportedly 30% below the utility rate, a template many service-sector multinationals now seek.

Corporate PPAs from BPO/IT Hubs

Metro Manila, Cebu, and Clark Freeport host 1.3 million BPO workers drawing 24/7 power. The Green Energy Option Program allows customers above 100 kW to bypass distributors and purchase electricity directly from generators, enabling firms such as Accenture and Concentrix to pursue 100% renewable electricity by 2030. Solar Philippines capitalized by signing 10–15-year PPAs that de-risked financing for its 500 MW Nueva Ecija array.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Congestion & Limited Transmission Capacity | −2.7% | Luzon grid, Visayas | Short term (≤ 2 years) |

| Regulatory Uncertainty around CREZ Auctions | −1.5% | Nationwide, offshore wind | Medium term (2-4 years) |

| Typhoon-driven Insurance Cost Escalation | −1.2% | Eastern seaboard, offshore | Long term (≥ 4 years) |

| Land-use Conflicts with Agrarian Reform Lands | −0.9% | Central Luzon, Negros, Mindanao | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid congestion & limited transmission capacity

Only 75 of 258 planned transmission projects were completed by 2024, leaving 58 schemes delayed up to nine years.[4]House of Representatives, “Committee Hearing on NGCP Project Status,” house.gov.ph TransCo estimates that congestion adds PHP 0.80/kWh to end-user bills, nullifying much of the cost advantage of renewables. ERC’s deferral of Group 3 capex frozen interconnection for 2 GW of solar and wind contracts, and curtailment in the Ilocos Norte corridor reached 12% during off-peak hours in 2024.

Regulatory Uncertainty around CREZ Auctions

Competitive Renewable Energy Zones are intended to pre-build transmission for high-resource areas, yet cost-allocation rules remain vague. NREL identified seven offshore wind zones with 42.86 GW of technical potential, but feed-in tariffs and priority dispatch for floating platforms are still under review. Copenhagen Infrastructure Partners and Equinor publicly stated they will wait for clearer guidance before investing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hydropower Dominates as Ocean Energy Accelerates

Hydropower accounted for 41.20% of the installed capacity in 2025 and remains the cornerstone of electricity generation in mountainous regions. The Philippines' renewable energy market size for hydropower is expected to expand as retrofits upgrade existing dams, although growth is moderate compared to solar and wind additions. Ocean energy, while starting from a negligible baseline, is projected to compound at a rate of 114.2% per year through 2031, thanks to tidal and wave pilot plants in San Bernardino and Eastern Visayas. This niche could transform coastal supply if floating platforms prove commercially viable. The National Renewable Energy Laboratory maps 42.86 GW of offshore wind technical potential, 93% of which is suited for floating turbines, indicating long-term marine dominance once costs converge with onshore benchmarks.

The expansion of solar energy in the Philippines is relentless; ACEN's Solar Philippines' Terra Solar projects alone will surpass 4 GW when Luzon's power grid is reinforced, thereby solidifying Luzon's dominance. Wind farms cluster along the Ilocos and Panay corridors where monsoon speeds average 7.5 m/s. Geothermal output remains steady at about 1.5 GW, with binary-cycle upgrades at Bacman leveraging existing wells. Bioenergy plays a modest role, and pumped storage, exemplified by the 360 MW Kalayaan plant, supplies vital balancing; however, no new schemes have reached financial close since 2010. Overall, diversified additions underpin the new renewable industry's resilience against fluctuations in energy supply and fluctuations in fuel prices.

By End-User: Utilities Lead but C&I Demand Surges

Utilities controlled 63.45% of installed renewables in 2025 as auction-winning developers tied projects to distribution companies and the wholesale spot market. The Philippines' renewable energy market size attributable to utilities is expected to continue rising, albeit at a slower pace, as corporate buyers claim a growing share. The commercial-and-industrial (C&I) segment is forecast to expand at a rate of 22.95% per year through 2031, driven by direct supply rules under the Green Energy Option Program and aggressive net-zero targets among multinationals.

Meralco PowerGen's 1.2 GW pipeline dedicated to hyperscale data centers illustrates how round-the-clock digital loads reshape offtake structures. Evolution Gaming's 100 MW solar PPA, signed in 2024, secured a tariff 30% below prevailing retail prices, underscoring the economic pull factors. Residential uptake is smaller in volume yet brisk; 12,000 rooftop net-metering applications were filed in 2024, thanks in part to zero-down financing from integrators such as Solaric and Solenergy. Altogether, the Philippines' renewable energy market is transitioning from purely utility-driven build-outs to a balanced mix, where commercial and industrial (C&I) buyers supply bankable credit profiles for greenfield development.

Geography Analysis

Luzon hosts roughly 59% of electricity demand and the lion's share of commissioned projects. Hydropower from Benguet, Ilocos wind arrays, and mega-solar in Bataan and Nueva Ecija anchor the region's dominance. Right-of-way disputes under agrarian law, especially across Central Luzon farmlands, are delaying several 500 kV lines, even as JICA-funded upgrades increase backbone capacity. Visayas contributes nearly 21% of installed renewables, led by Energy Development Corporation's 1.48 GW geothermal fleet in Leyte and Negros. Completion of the Central Negros–Panay submarine link in 2024 unlocks stranded baseload, and prospective offshore wind leases in the Guimaras and Tañon straits could pivot the resource mix toward marine generation once policy clarity arrives.

Mindanao accounts for approximately 16% of the country's capacity, dominated by hydropower that supplies loads for mineral processing and the agro-industry. The Mindanao–Visayas connection, scheduled for 2026, will allow seasonal hydropower surpluses to flow northward, thereby improving system balancing. Palawan remains off-grid until a planned submarine cable energizes in 2027; meanwhile, solar-diesel hybrids reduce costly fuel subsidies. The Eastern Visayas coastline, squarely in the typhoon corridor, serves as a test bed for disaster-resilient microgrids, with USAID's Siargao project demonstrating the advantages of rapid restoration. Collectively, these regional dynamics reveal that the Philippines' renewable energy market gains hinge not only on resource endowment but equally on transmission rollout and climate-resilience strategies.

Competitive Landscape

Eleven family-controlled conglomerates held 74% of generation in 2024, yielding a moderately concentrated structure where incumbents can mobilize capital quickly, yet rivalry is intensifying. ACEN and Aboitiz chart contrasting growth paths: ACEN acquires pipelines, Gigawatt1, BIM Energy, and Bronzeoak, while Aboitiz invests organically and pairs new plants with battery storage. Solar Philippines, though outside the conglomerate club, raised USD 150 million in 2024 to finance the world's largest integrated solar-plus-battery complex, proving independent power producers can still scale if offtake and grid access align.

Technology suppliers shape cost curves: Trina Solar's bifacial modules and Vestas' turbines exceeding 5 MW are now standard in recent bids, lowering installed-cost benchmarks. Energy Development Corporation's geothermal expertise forms a competitive moat as it pilots binary-cycle upgrades. Offshore wind is the next frontier; Copenhagen Infrastructure Partners and Equinor await firmer auction rules, giving domestic developers a narrow window to secure seabed leases. Regulatory liberalization, as outlined in the ERC's June 2024 circular, eliminated most nationality caps, inviting foreign joint ventures and sharpening competition for prime interconnection slots.

Corporate PPAs add a new layer of rivalry. Meralco PowerGen's data-center-focused 1.2 GW pipeline and Evolution Gaming's solar contract illustrate how load aggregation outside the utility franchise reshapes deal origination. Market share battles now span not only auctions but also private bilateral channels, suggesting that the Philippines' renewable energy market will see accelerating competition across financing, site control, and advanced storage integration.

Philippines Renewable Energy Industry Leaders

-

Aboitiz Power Corporation

-

ACEN Corporation

-

First Gen Corporation (incl. EDC)

-

Solar Philippines Power Project Holdings Inc.

-

Vena Energy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Copenhagen Infrastructure Partners obtained the first DENR environmental clearance for its 1 GW San Miguel Bay offshore wind project.

- March 2025: DOE released the Green Energy Auction 4 terms referencing 10,478 MW of capacity, including 1,100 MW integrated with storage.

- March 2024: wpd GmbH pledged PHP 392.4 billion for 3,260 MW of offshore wind across Cavite, Negros Occidental, and Guimaras.

- January 2024: Copenhagen Infrastructure Partners announced a PHP 108 billion investment for a 650 MW offshore wind facility in Northern Samar. The project is planned to be located off the coast of six towns in the province: Bobon, Catarman, Mondragón, San Roque, Pambujan, and Laoang.

Philippines Renewable Energy Market Report Scope

Renewable energy refers to energy sources that are naturally replenished and will not be depleted over time, such as solar, wind, hydro, geothermal, and biomass energy. Unlike fossil fuels like coal, oil, and natural gas, which are finite resources and will eventually be depleted, renewable energy is sustainable and can be continuously harnessed without depleting the Earth's resources.

The Philippines' renewable energy market report includes:

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How fast is renewable capacity expanding in the Philippines?

Aggregate capacity is growing at a 18.91% CAGR, rising from 14.45 GW in 2026 to an expected 34.37 GW by 2031.

Which technology currently leads installed capacity?

Hydropower tops the mix with a 41.20% share in 2025, though solar plants are catching up quickly.

What segment is seeing the quickest demand growth?

Commercial-and-industrial buyers, especially data centers and BPO hubs, are forecast to expand renewable uptake at 22.95% annually through 2031.

Why are corporate PPAs important in the Philippines?

They let large power users bypass high retail tariffs and lock in cheaper renewable supply, de-risking project finance for generators.

What is the main infrastructure bottleneck today?

Delayed transmission lines, only 29% of planned projects were finished by 2024, limit grid access for new solar and wind plants.

How exposed are projects to climate risks?

The country lies in a typhoon corridor, so premium costs for insurance are rising, though parametric products are gaining adoption to speed post-storm payouts.

Page last updated on: