Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

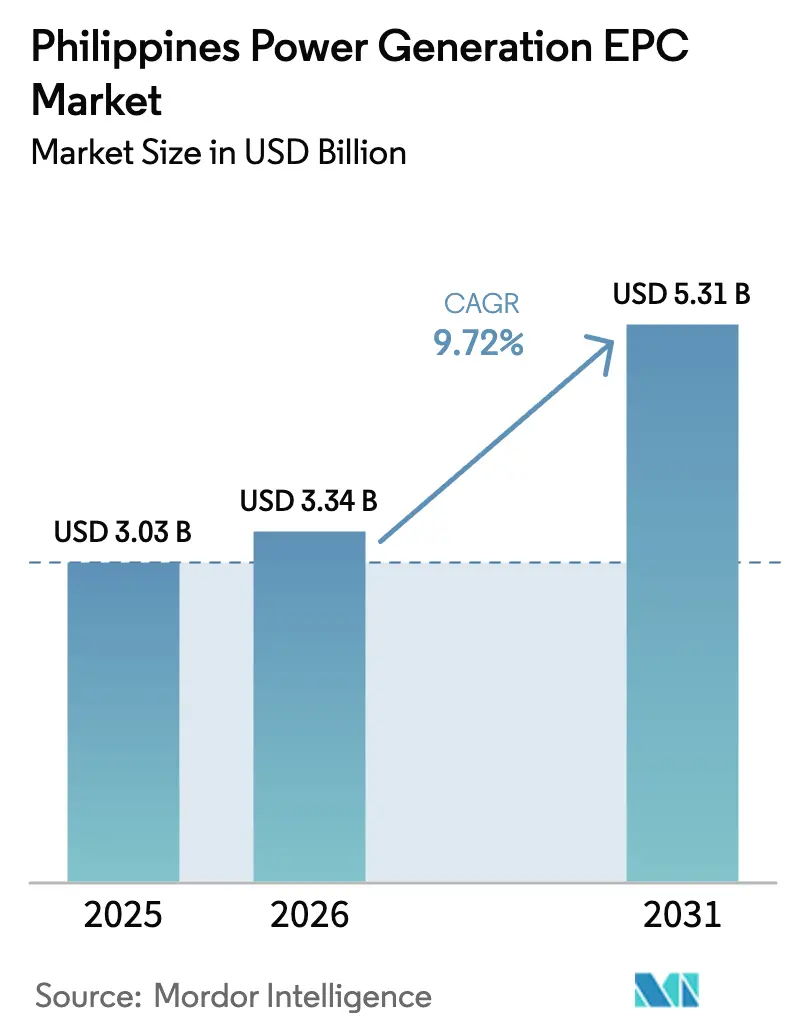

| Base Year Market Size (2025) | USD 3.03 Billion |

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 9.72% CAGR |

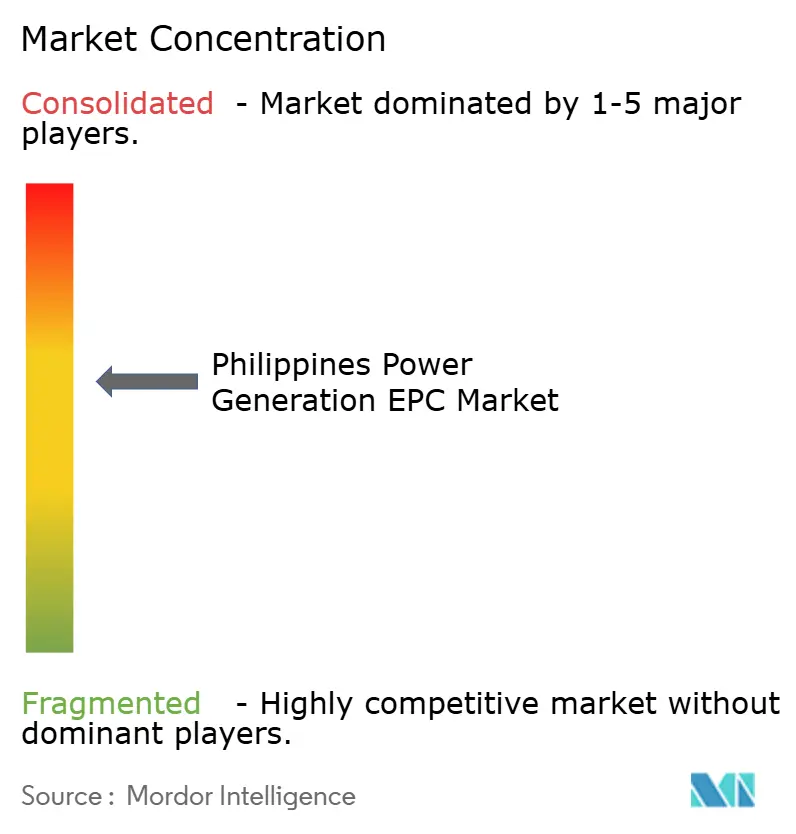

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Power Generation EPC Market Analysis by Mordor Intelligence

The Philippines Power Generation EPC Market size is projected to expand from USD 3.03 billion in 2025 and USD 3.34 billion in 2026 to USD 5.31 billion by 2031, registering a CAGR of 9.72% between 2026 to 2031.

Robust urban migration, the rollout of data-center campuses, and an aggressive renewable-energy policy pipeline exceeding 35 gigawatts are combining to accelerate contract awards. Renewables already absorb more than two-thirds of annual spending, and their share keeps rising as service-contract approvals fast-track solar, wind, and floating photovoltaic projects. At the same time, the Mindanao-Visayas interconnection is knitting the national grid together, allowing developers to pool offtake agreements across islands and unlock larger engineering scopes. Corporate power-purchase agreements from hyperscale data-center operators are redefining risk allocation by demanding performance guarantees that only well-capitalized EPC firms can provide. Lastly, liquefied-natural-gas-to-power hubs and hybrid floating solar on hydropower reservoirs are widening the technical canvas and creating premium-margin sub-segments inside the Philippines' power generation EPC market.

Key Report Takeaways

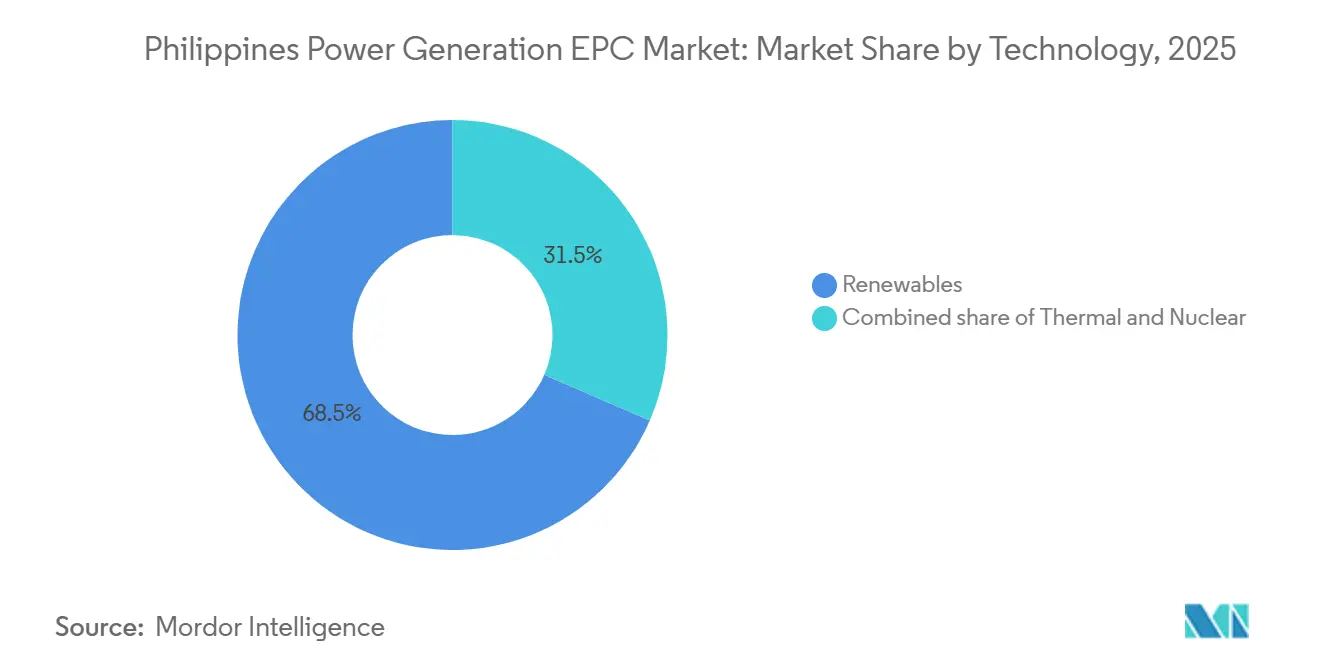

- By technology, renewables accounted for 68.5% of 2025 spending within the Philippines' power generation EPC market and are forecast to expand at a 14.9% CAGR through 2031.

- By capacity band, projects above 500 megawatts captured 72.3% of the Philippines' power generation EPC market share in 2025, while sub-100-megawatt distributed energy resources are advancing at a 13.5% CAGR to 2031.

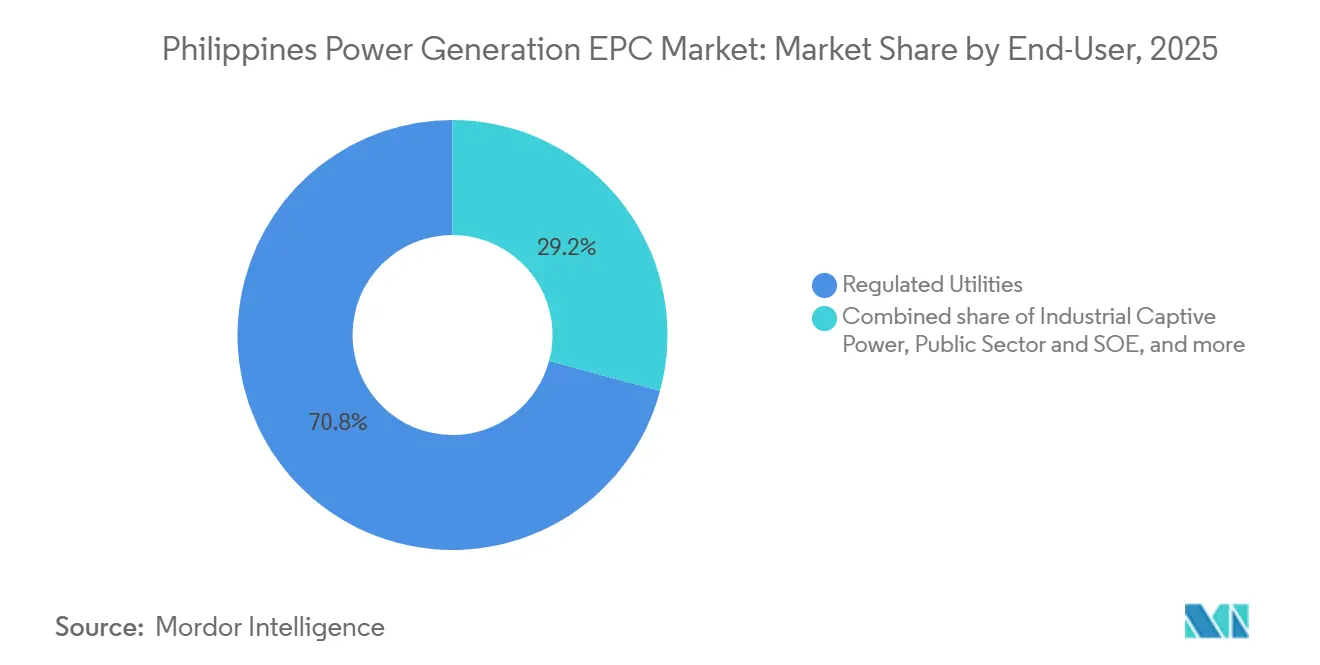

- By end-user, regulated utilities held 70.8% of demand in 2025; industrial captive-power buyers represent the fastest expansion, climbing at a 12.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Power Generation EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising electricity demand from rapid urbanisation and digital-economy growth | +3.2% | National, with concentration in Metro Manila, Calabarzon, Central Luzon, and Metro Cebu | Long term (≥ 4 years) |

| Fast-track approval of renewable-energy service contracts (2023-25) | +2.8% | National, with early gains in Luzon solar corridors, Visayas wind zones, and Mindanao hydro basins | Medium term (2-4 years) |

| Grid interconnection of Mindanao-Visayas corridors unlocking new EPC orders | +2.1% | Mindanao and Visayas, with spill-over to Luzon grid stability | Medium term (2-4 years) |

| Corporate PPAs by hyperscale data-centre entrants (Google, Amazon, Meta) | +1.5% | Metro Manila, Calabarzon, and emerging data-centre hubs in Clark and Cebu | Short term (≤ 2 years) |

| Novel LNG-to-power hubs enabling hybrid EPC scopes | +1.3% | Batangas, Subic Bay, and Davao LNG terminals | Medium term (2-4 years) |

| Modular floating solar projects on hydropower reservoirs | +0.9% | Luzon (Pantabangan, Magat reservoirs), Mindanao (Pulangi complex) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Demand From Rapid Urbanization And Digital-Economy Growth

Electricity consumption jumped 6.2% in 2024 to 108 terawatt-hours as Metro Manila extended into neighboring provinces and business-process outsourcing hubs ran round-the-clock cooling loads.[1]Department of Energy Philippines, “Power Development Plan 2023-2040,” doe.gov.ph Reserve margins are thinning; the Luzon grid logged only 1,850 megawatts of reserves in April 2025, near the yellow-alert threshold, which is pushing utilities to lock in new capacity faster.[2]National Grid Corporation of the Philippines, “Power Situation Outlook 2025,” ngcp.ph Hyperscale data centers in Cavite and Laguna already required 450 megawatts in 2025 and could double that by 2028, converting daily load curves and favoring solar EPC timelines that align with peak afternoon demand. Household air-conditioning penetration rose to 38% in 2024, adding to daytime peaks that battery-backed solar can manage efficiently.[3]Philippine Statistics Authority, “Household Energy Consumption Survey 2024,” psa.gov.ph The Power Development Plan targets 15 gigawatts of fresh capacity by 2030, translating into an annual engineering workload of 2.1 gigawatts that stretches local labor pools and benefits contractors with regional mobilization capability.

Grid Interconnection Of Mindanao-Visayas Corridors Unlocking New EPC Orders

The 450-megawatt Mindanao-Visayas submarine cable, energized in 2024, erased the discount that Mindanao projects once accepted, lifting project internal rates of return by 1.8 percentage points and resurrecting 1.2 gigawatts of shelved renewables. Luzon-based independent power producers can now aggregate offtake across islands, reducing counterparty risk and enabling bigger, more economical EPC scopes. Visayas can import hydro-rich power during rainy months, flattening seasonal price swings and improving the bankability of 15-year power-purchase agreements. A follow-on upgrade to 1,000 megawatts by 2027 is budgeted at PHP 35 billion and will further integrate the archipelago into a unified EPC bidding space. Contractors able to manage multi-island logistics gain a cost edge over rivals accustomed to single-site execution.

Corporate PPAs By Hyperscale Data-Center Entrants

Google’s 120-megawatt solar PPA in 2024, Amazon Web Services’ 200-megawatt wind agreement in 2025, and Meta’s 300-megawatt renewable commitment are redefining offtake profiles. These 15- to 20-year contracts shift construction risk onto EPC firms via stiff liquidated-damages clauses that can reach 15% of contract value, favoring balance-sheet-strong players. Hourly-matching requirements necessitate co-located batteries and advanced energy-management software, expanding EPC scopes beyond balance-of-plant work. Fiscal incentives clarified in a 2024 Department of Energy circular place corporate PPAs on par with utility deals, a change expected to lure additional hyperscalers by 2026. The model tightens timelines, pushing contractors toward modular approaches and digital twin deployment for schedule certainty.

Modular Floating Solar Projects On Hydropower Reservoirs

SN Aboitiz Power’s 6.63-megawatt floating pilot at Magat Dam, commissioned in December 2024, delivered capacity factors 8% higher than ground-mount arrays, validating the technology. The National Power Corporation controls 3,600 megawatts of hydropower across 18 reservoirs and seeks up to 500 megawatts of floating solar by 2028, a pipeline worth roughly USD 750 million in EPC fees. Modular pontoons enable 10-megawatt block commissioning, smoothing cash flow, and reducing foreign-exchange risk on imported panels. A University of the Philippines study confirmed that 5% surface coverage can cut reservoir evaporation by 30%, adding water-conservation co-benefits. New 2025 permitting guidelines cap reservoir coverage at 10% and remove earlier restrictions that limited projects to private ponds, setting the stage for steady EPC demand over the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission bottlenecks causing curtailment risk for new builds | -1.8% | Mindanao (isolated grid), Visayas inter-island links, Northern Luzon renewable zones | Short term (≤ 2 years) |

| Peso depreciation inflating imported EPC equipment costs | -1.4% | National, affecting all projects with imported turbines, inverters, and balance-of-plant equipment | Short term (≤ 2 years) |

| Local content rule ambiguities delaying contract awards | -0.9% | National, with heightened scrutiny on Chinese and Korean EPC contractors | Medium term (2-4 years) |

| Geothermal resource-rights disputes hindering brownfield repowering | -0.6% | Leyte, Negros, Albay geothermal fields | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transmission Bottlenecks Causing Curtailment Risk For New Builds

Grid operators curtailed 120 gigawatt-hours of renewable output in 2024, equal to 2.1% of total generation, because key corridors in Northern Luzon and the Panay-Negros link ran out of headroom.[4]Energy Regulatory Commission, “2025 Grid Curtailment Report,” erc.gov.ph Independent power producers receive no payment for lost energy, so EPC pro formas now assume a 3-5% deration, trimming internal rates of return. A PHP 17.09 billion 500-kilovolt backbone originally slated for 2024 slipped to 2026, stranding 1,200 megawatts in Ilocos Norte and Cagayan. The 230-kilovolt Panay-Negros interconnection operates at 95% utilization, forcing diesel dispatch that erodes the economics of fresh solar bids. A 2025 Energy Regulatory Commission directive orders a 10-year expansion roadmap with binding milestones, yet right-of-way disputes with local governments remain unresolved and continue to inflate project costs by up to 12%.

Peso Depreciation Inflating Imported EPC Equipment Costs

The peso slipped from PHP 55.2 per USD in 2023 to PHP 58.4 in 2025, raising the landed price of imported panels, turbines, and transformers that represent up to 70% of an EPC budget. Contractors locked into peso-denominated fixed-price contracts saw margins compress by as much as 300 basis points because suppliers invoice in dollars. Central-bank rate hikes to 6.5% in 2024, intended to stabilize the currency, also lifted local-currency construction loans by 150 basis points, straining working-capital lines. Mindanao projects suffer a further 50- to 75-basis-point premium on performance bonds due to regional credit risks, compounding cost pressure. A Department of Trade and Industry proposal to waive customs duties on renewable-energy equipment under a green-lane regime could offset part of the depreciation hit, but legislation is still pending as of mid-2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Renewables Dominate Amid Nuclear Discourse

Renewables commanded 68.5% of 2025 spending within the Philippines' power generation EPC market and are forecast to grow at a 14.9% CAGR through 2031. Solar comprised 55% of that total, led by the 3.5-gigawatt Terra Solar contract valued at USD 4 billion, while onshore wind held 30%, concentrated in Ilocos Norte and Guimaras. Floating solar captured 15% and is scaling rapidly as land access tightens, with capacity factors running 8% higher than ground-mount benchmarks.

Thermal plants accounted for 28% of the 2025 investment and are expanding modestly at 3.2% per year. Liquefied-natural-gas projects such as the 420-megawatt San Gabriel facility show how integrating regasification terminals with combined-cycle turbines secures premium margins. Coal additions are frozen under a government moratorium, and nuclear remains exploratory; a 2024 memorandum with Ultra Safe Nuclear Corporation keeps the topic alive but lacks a regulatory backbone. Absent swift policy progress, nuclear will not materially influence the Philippines' power generation EPC market size this decade.

By Capacity Band: Mega-Projects With Distributed Upsurge

Projects larger than 500 megawatts absorbed 72.3% of the 2025 contract value, underscoring the scale economics of utility-grade solar, wind, and hybrid battery complexes. Multi-gigawatt portfolios unlock double-digit supplier discounts and streamline civil works mobilization.

Mid-tier projects between 100 and 499 megawatts are growing as independent power producers mix technologies to match provincial demand without triggering enhanced environmental assessments. The sub-100-megawatt is rising fastest at 13.5% and is central to rural electrification and industrial self-generation strategies. Modular design allows phased commissioning that eases cash flow and reduces currency exposure, positioning the segment as a vital growth lever for the Philippines' power generation EPC market.

By End-User: Utilities Anchor, Captive Power Surges

Regulated utilities represented 70.8% of 2025 demand, leveraging access to multilateral financing and statutory reserve requirements that guarantee long-term offtake. Manila Electric Company alone procured 600 megawatts of renewable capacity in 2024-2025 using turnkey contracts that shift construction risk to EPC firms.

Industrial captive power, only 8.2% of spending in 2025, is rising at a 12.7% CAGR as semiconductor, nickel, and cement plants bypass 12% interruptible-service premiums and grid instability. Energy-intensive producers can now sell surplus into the wholesale market, improving project returns and stimulating fresh EPC orders. Independent power producers serve the balance, aggregating multi-utility PPAs that enable 1-gigawatt portfolios and allow equity syndication to strategic investors, further deepening the Philippines' power generation EPC market.

Geography Analysis

Luzon commands roughly 70% of installed capacity and spending in the Philippines' power generation EPC market, anchored by Metro Manila’s 18 terawatt-hours of consumption and industrial clusters in Cavite, Laguna, and Batangas. Deferred completion of the PHP 17.09 billion 500-kilovolt Bolo-Balaoan transmission line to 2026 keeps 1,200 megawatts of wind projects in Ilocos Norte on the drawing board. The Green Lane permitting scheme that halves approval timelines favors Luzon developers equipped to navigate detailed environmental reviews. Corporate PPAs concentrated near data-center campuses amplify demand for solar and battery installations that reach commercial operation within 24 months.

Visayas contributes about 15% of EPC activity and is accelerating following the 2024 Mindanao-Visayas interconnection that removed historic pricing discounts. Geothermal resources in Negros and Leyte still dominate generation, yet indigenous-rights disputes have stalled 200 megawatts of repowering, undercutting the pace of brownfield EPC work. Floating solar proposals on Panay and Negros reservoirs seek to leverage existing hydropower substations, reducing grid-tie costs by 20%. Transmission congestion on the Panay-Negros 230-kilovolt link, operating near saturation, forces curtailment and underscores the urgency of the PHP 8.5 billion upgrade mandated for completion by 2027.

Mindanao holds the remaining 15% share and is emerging as the renewable frontier. Hydropower supplies 60% of its 3,200 megawatts, offering shared interconnection points for hybrid floating solar. Lower credit ratings raise bonding costs, yet the new interconnection to Visayas improves offtake aggregation and bankability. Rotating blackouts during the 2024 dry season spurred 120 megawatts of industrial solar-plus-storage installations, illustrating captive power’s role in stabilizing plant operations. A Department of Energy directive lifting reserve requirements to 20% is forecast to spark 400 megawatts of additional EPC contracting by 2028, primarily solar and wind.

Regulatory Landscape

The Philippines power generation EPC market is governed by the Department of Energy (DOE) planning and endorsement process and the Energy Regulatory Commission (ERC) compliance framework. Proponents typically secure DOE endorsements, such as a Certificate of Endorsement (COE), and then obtain an ERC Certificate of Compliance (COC) ahead of commercial operation, which aligns EPC execution timelines with permitting and inspection milestones.

In February 2026, the DOE issued Department Circulars DC2026-02-0005 and DC2026-02-0006, introducing a load-based framework for generation resources (baseload, mid-merit, peaking) and requiring generation companies to file Annual Self-Assessment Forms to document technical performance and operational readiness. Alongside this, the DOE policy pipeline, anchored by the Power Development Plan 2023-2050 (including a 35% renewable energy target by 2030 and 50% by 2040) and the Green Energy Auction program with multiple 2026 auctions (including offshore wind and floating solar), is influencing bankability, contracting structures, and technology selection for EPC contractors.

Competitive Landscape

The Philippines' power generation EPC market remains moderately fragmented. The top five contractors, China Energy Engineering Corporation, Power Construction Corporation of China, Siemens Energy, Mitsubishi Power, and Hyundai Engineering, controlled about 45% of the 2025 contract value, leaving 55% to local conglomerates and mid-tier foreign entrants. Chinese state-owned enterprises undercut bids by up to 12% by bundling vendor-financed modules with EPC execution, as seen in the USD 4 billion Terra Solar award.

Local groups such as Aboitiz Power, San Miguel Global Power, and DMCI Power counter this pricing play by forming joint ventures with Japanese and South Korean partners to gain turbine technology and attract dollar-denominated project finance. DMCI Power's 2025 alliance with KEPCO Engineering & Construction on a 300-megawatt wind farm illustrates this hedging approach against peso weakness. White-space opportunities are growing in sub-100-megawatt distributed resources, where local logistics expertise and flexible commissioning trump scale, allowing smaller firms to build defensible niches inside the Philippines' power generation EPC industry.

Technology differentiation is sharpening around hybrid integration and digital controls. Siemens Energy's Omnivise T3000 platform marries combined-cycle gas turbines with grid-scale batteries, enabling synthetic inertia services that carry premium margins. Specialists in floating solar, such as Ocean Sun and Ciel & Terre, are teaming with local civil engineers to chase the 500-megawatt reservoir pipeline, an area legacy EPC providers have avoided due to marine risk. A 2025 Energy Regulatory Commission ruling allowing surplus captive power to trade on the spot market opens a pathway for EPC firms to shift toward energy-as-a-service models and capture recurring revenue streams.

Philippines Power Generation EPC Industry Leaders

Aboitiz Power Corporation

San Miguel Global Power

First Gen Corporation

ACEN Corporation

UPC Renewables

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procurement that combines auction-led and corporate-led demand is opening room for EPC firms to package grid-ready renewable capacity together with firming and compliance deliverables. The DOE accelerated 22 power projects totaling 1,471 MW of renewable energy and storage capacity by end-April 2026, pointing to a near-term execution queue where interconnection management and construction readiness tend to separate bidders. Developers are also increasing utility-scale solar with battery storage contracting, as reflected by Levanta Renewables awarding CEEC an EPC scope for a 166 MWp solar and 80 MWh BESS project in the Visayas (April 2026), which broadens EPC scope beyond balance-of-plant into controls, commissioning, and performance testing.

Opportunities extend into multi-package EPC, owner-engineer work, and balance-of-plant tenders around larger builds. TotalEnergies and Nextnorth reached financial close and began construction on a 440 MWp solar project in Ilagan, Isabela (April 2026). At the same time, the DOE revoked 84 renewable energy service contracts totaling 5,372.2 MW in 2025, reshaping the pipeline by reducing visibility for less execution-ready developers. With transmission constraints and tighter compliance oversight, EPC demand is increasingly for providers that can support bankable grid studies, plan dedicated interconnection facilities where required, and maintain schedule certainty against EVOSS and DOE endorsement timelines, rather than focusing on lowest-price, equipment-only offerings.

Recent Industry Developments

- July 2026: San Miguel Global Power received Energy Regulatory Commission approval to build a PHP 1.7 billion dedicated point-to-point transmission facility linked to its Masinloc complex. The approval highlights how interconnection works are becoming a critical enabling scope alongside generation EPC, especially where network headroom and right-of-way issues threaten commissioning timelines.

- October 2025: SP New Energy Corp. (SPNEC), via Terra Solar Philippines, finalized additional EPC agreements for the MTerra Solar Project, adding to the contracting momentum behind its large Luzon solar park buildout. The awards reinforce the scale of multi-package EPC demand for utility-scale solar and storage and sustain competitive pressure among major international contractors active in the Philippines.

- December 2024: SN Aboitiz Power (SNAP) tapped GEDI China Energy to deliver Phase 2 of the Magat battery energy storage system expansion in Isabela. The contract deepened the market shift toward storage-linked EPC scopes that require specialized commissioning, protection systems, and grid compliance capabilities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue earned from engineering, procurement, and construction (EPC) work delivered for power generation projects in the Philippines, covering both new-build and major expansion activities when a contractor is responsible for integrated project delivery.

Scope exclusions: We exclude routine operations and maintenance, minor repair jobs, and stand-alone equipment supply that is not part of an EPC contract.

Segmentation Overview

- By Technology

- Thermal

- Nuclear

- Renewables

- By Capacity Band

- Up to 100 MW (DER, micro-grid)

- 100 to 499 MW

- Above 500 MW

- By End-User

- Regulated Utilities

- Independent Power Producers

- Industrial Captive Power

- Public Sector and SOE

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the Philippines power project pipeline and the conditions that drive EPC awarding and execution timing. We relied on public sources such as Department of Energy publications, Energy Regulatory Commission releases, and national statistics and trade datasets to anchor inflation, currency timing, and construction activity. To avoid overstating opportunity, these signals were reviewed alongside development plan documents and permitting updates, which typically indicate whether projects are still active or have slipped.

For the market math, we also reviewed company filings and investor presentations to understand booked orders, project milestones, and typical contract structures for EPC delivery. Where needed, paid company financial and intelligence subscriptions were used to normalize contractor revenue references, and an import and export shipment-level database was used only as a sense check on large equipment movement patterns tied to power plant builds. The desk sources listed here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with EPC contractors, project developers, owners, and engineering consultants who track bid activity and execution realities in the Philippines. We used these discussions to confirm what is usually counted inside an EPC contract value versus supplied-by-owner items, and to test the reasonableness of cost per MW for different technologies and plant sizes. When desk signals were unclear, assumptions were tightened through repeat cross-checks across Luzon, Visayas, and Mindanao coverage and across regulated utilities, independent power producers, and captive industrial buyers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | |

| Mid tier: 45% | Functional/Unit leaders: 35% | |

| Smaller Players: 17% | Managers: 48% |

Market-Sizing & Forecasting

Sizing started with a top-down reconstruction of EPC demand using the country level capacity-addition outlook, project award timing, and typical EPC intensity by technology and plant size. We converted this into annual revenue flow based on build duration and milestone billing patterns. To keep totals grounded, we corroborated the output with selective bottom-up checks, such as sampled contract values from recent project announcements, sanity checks using cost per MW ranges, and a light roll-up of visible contractor exposure where disclosure allowed.

Key inputs used in the model included the scheduled MW pipeline, the split between thermal, nuclear, and renewables, capacity bands that affect engineering complexity, and end-user mix across utilities, IPPs, and industrial captive projects. We also tracked local cost inflation, imported equipment sensitivity, and PHP to USD conversion timing, since these can shift reported EPC value even when MW remains stable. For forecasting, we ran scenario analysis around award slippage and permitting pace, and we set scenario weights based on what interviewees expect for execution bottlenecks and financing comfort over the next few years. When a project value was not disclosed, the gap was filled using benchmark cost ranges adjusted for technology, size band, and likely balance-of-plant scope.

Data Validation & Update Cycle

Outputs were triangulated across multiple signals, including project lists, regulatory approvals, award announcements, and the implied revenue recognition profile from construction timelines. Large variances were flagged early, then the assumptions were reviewed again to ensure like-for-like scope treatment across technologies and end users.

Before sign-off, the model and final numbers go through multi-step analyst reviews, followed by targeted re-contacts when a major project shifts status or when a cost assumption looks out of line with current market quotes. Reports are refreshed annually, with interim updates triggered by material policy moves, large award wins, or cancellation headlines. Right before delivery, we do a fresh pass on the key inputs so clients receive the latest updated view.

Mordor Intelligence's Philippines Power Generation Epc Market Size Versus Other Published Estimates

Published market sizes for Philippines power generation EPC often do not match because the boundary of what counts as EPC is not treated the same way, and revenue recognition timing can also shift the number. Differences also show up when one source reports in local currency and later converts, or when it blends multi-year project values into a single year view.

In our checks, the largest gap drivers were refresh cadence and the conversion date used for PHP to USD, followed by how EPC price per MW is updated for inflation and imported equipment sensitivity, and then validated against what contractors say is actually being bid and executed in the current year. This is why the 2025 value used by Mordor Intelligence lands far from smaller estimates that appear to report only narrower contract types.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.03 B (2025) | |

| Global Consultancy A | USD 0.41 B (2025) | The estimate appears to stay closer to a narrow EPC contract value lens and may exclude sizable balance-of-plant work and larger capacity bands, which keeps the annual total lower. It also looks more sensitive to a single year award snapshot rather than recognizing multi year execution billing across ongoing projects. |

| Industry Publisher B | USD 0.38 B (2025) | This figure likely reflects a tighter definition of power EPC and may not fully carry through technology mix effects and end-user diversity that change EPC intensity. The number can also move if older FX conversion timing is used and if cost per MW updates are not refreshed in line with current inflation and equipment lead times. |

The spread in the table is mainly explained by what is counted inside EPC scope and when contract value is translated into annual revenue, rather than a disagreement on the direction of project activity. By keeping FX timing, price-per-MW updates, and project status validation consistent, the final market value stays traceable to clear inputs that can be repeated and rechecked.

Key Questions Answered in the Report

How large is the Philippines power generation EPC market today?

The Philippines power generation EPC market size reached USD 3.34 billion in 2026 and is set to rise to USD 5.31 billion by 2031.

Which segment is expanding fastest?

Renewable projects are advancing at a 14.9% CAGR, driven by strong policy support and corporate PPAs.

Why are floating solar projects gaining attention?

Floating arrays avoid land-use hurdles, deliver capacity factors 8% higher than ground-mount systems, and conserve reservoir water.

What role do corporate PPAs play?

Hyperscale data-center operators sign multi-year PPAs that demand strict performance guarantees and accelerate new project timelines.

How does currency risk affect EPC contractors?

A 5.8% peso depreciation between 2023 and 2025 raised imported equipment costs, squeezing margins on fixed-price contracts.

Which regions present the most EPC opportunity?

Luzon dominates spending today, but Visayas and Mindanao are accelerating as new interconnections integrate the national grid.

Page last updated on: