Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

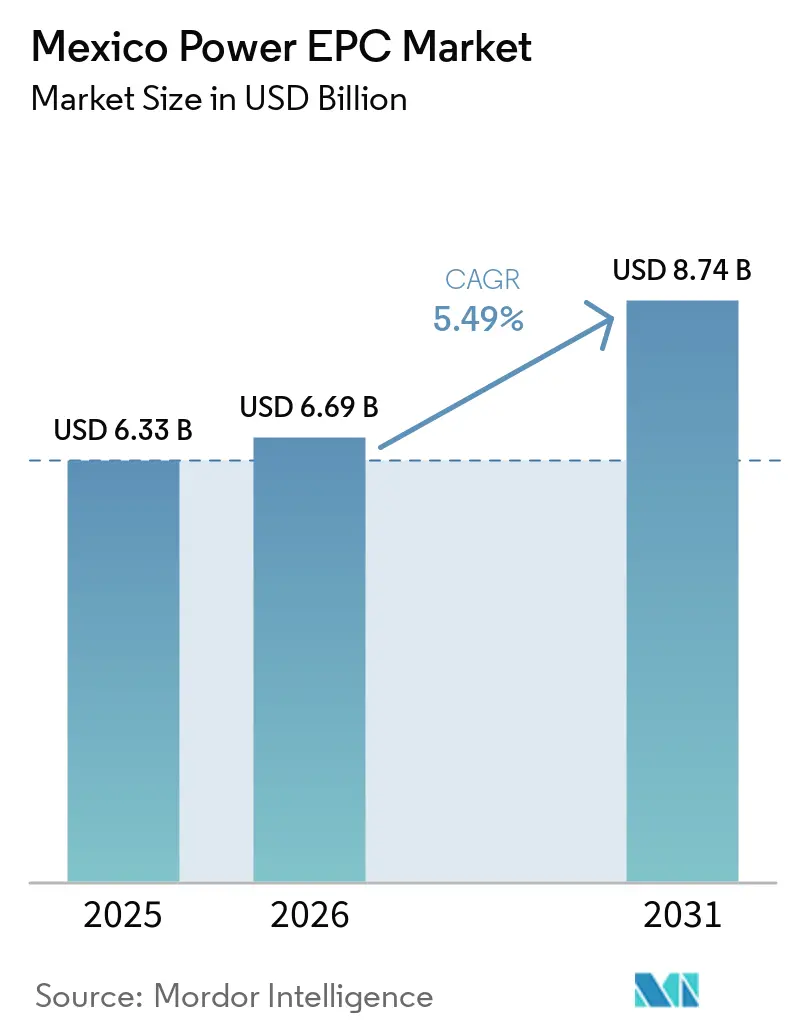

| Base Year Market Size (2025) | USD 6.33 Billion |

| Market Size (2026) | USD 6.69 Billion |

| Market Size (2031) | USD 8.74 Billion |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Power EPC Market Analysis by Mordor Intelligence

The Mexico Power EPC Market size is projected to expand from USD 6.33 billion in 2025 and USD 6.69 billion in 2026 to USD 8.74 billion by 2031, registering a CAGR of 5.49% between 2026 to 2031.

Transmission and distribution (T&D) work streams are gaining momentum because Comisión Federal de Electricidad (CFE) has committed USD 7.5 billion to 145 new lines and substations, a decision triggered by the May 2024 grid-stress event when more than 60% of Mexico’s transmission network operated at maximum load.[1]Comisión Federal de Electricidad, “CFE Announces USD 23.4 Billion Investment Plan Through 2030,” cfe.mx Generation EPC remains pivotal, yet its trajectory is reshaping: renewables already command three-quarters of generation value and are moving faster than thermal additions, while the March 2025 storage mandate has bundled solar and batteries into single turnkey packages. Nearshoring clusters in Nuevo León and Guanajuato are compressing the investment cycle by five to six years, lifting order volumes and revamping project sequencing. Global turbine OEMs, European EPC specialists, and local fabricators are forming joint platforms to meet tightening domestic-content rules that now require up to 60% local sourcing for transmission equipment.[2]Comisión Federal de Electricidad, “CFE Announces USD 23.4 Billion Investment Plan Through 2030,” cfe.mx

Key Report Takeaways

- The Mexico power EPC market is segmented into power generation EPC and power transmission and distribution (T&D) EPC. Power generation EPC accounted for 54.98% of the market in 2025, while power transmission and distribution (T&D) EPC is projected to grow at a 7.49% CAGR through 2031.

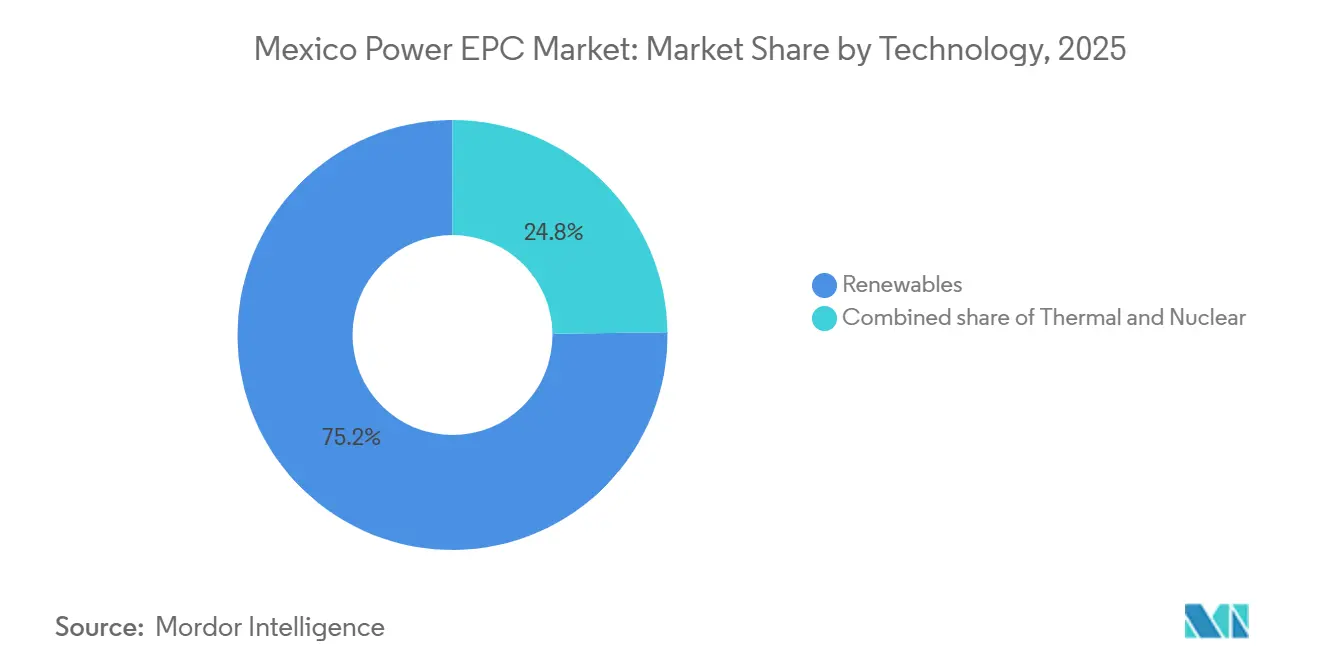

- By technology, renewables captured 75.2% of the Mexican power generation EPC market share in 2025, while the same segment is forecast to expand at a 9.8% CAGR through 2031.

- By capacity band, projects above 500 MW held 67.4% of the Mexico power generation EPC market size in 2025; the up-to-100 MW distributed segment is projected to grow at a 6.1% CAGR between 2026 and 2031.

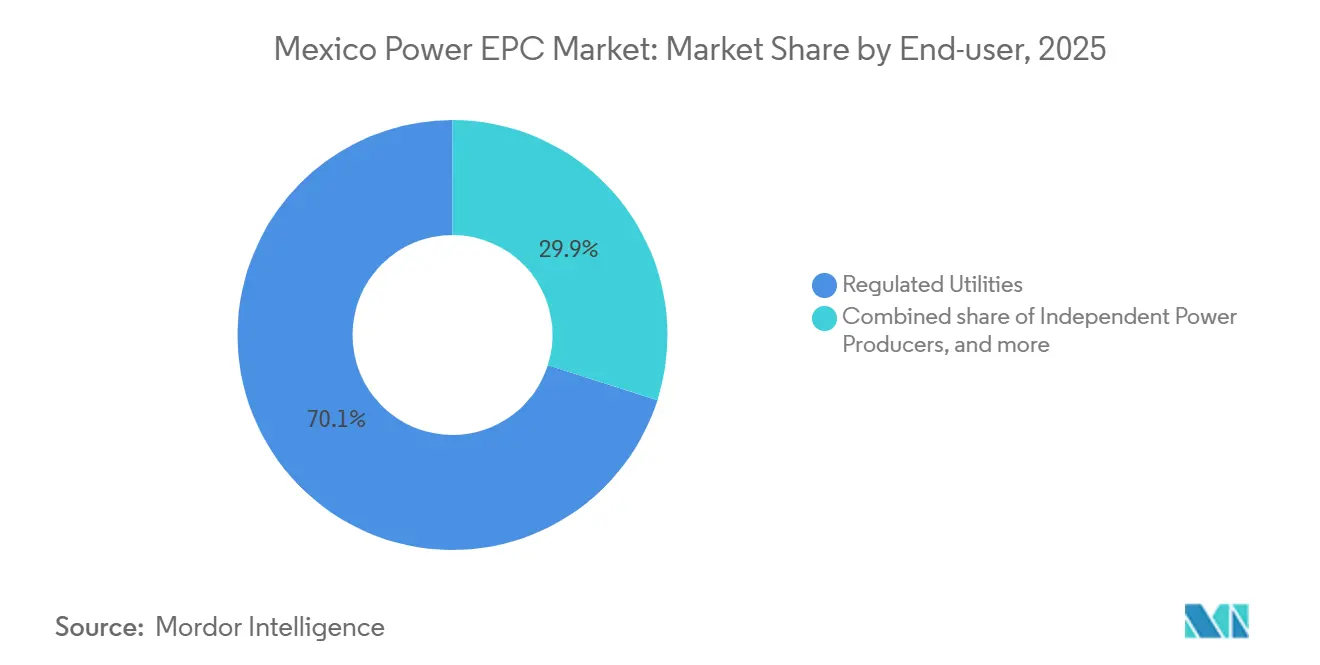

- By end user, regulated utilities controlled 70.1% of spending in 2025, yet independent power producers are expected to post the fastest 6.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Power EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated CFE-led grid modernization tenders | +1.8% | National, focus on Nuevo León, Guanajuato, Bajío | Medium term (2-4 years) |

| Nearshoring-driven industrial demand clusters | +1.2% | Northern states | Short term (≤ 2 years) |

| Fast-track permitting for ≥ 1 GW renewable parks | +0.9% | Nationwide, emphasis on Sonora, Coahuila, Baja California | Medium term (2-4 years) |

| Combined-cycle retrofits for CO₂ cuts | +0.5% | Existing thermal fleet nodes | Long term (≥ 4 years) |

| Digital EPC tool-chains (BIM-5D) | +0.7% | National, led by tier-1 contractors | Medium term (2-4 years) |

| Novel green-bond financing structures | +0.4% | National, with development-bank participation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated CFE-Led Grid Modernization Tenders

CFE’s August 2025 pledge of USD 23.4 billion for new capacity and network upgrades marks the largest single investment window in the utility’s history. The package includes 13,024 MW of new generation and 6,261 circuit-kilometers of high-voltage lines to be awarded from 2026 onward. Domestic-content thresholds climb to 60%, so foreign EPC firms are setting up fabrication joint ventures in Nuevo León and Estado de México to protect margins. The May 2024 grid-stress episode validated the urgency of these awards and has shifted bidding calendars forward by nearly two years. Faster award cycles are set to lock in higher volumes for the Mexico Power EPC market.

Nearshoring-Driven Industrial Demand Clusters

Mexico became the United States’ top trading partner in 2023, triggering a surge of manufacturing FDI that averaged 20% annual growth up to 2025.[3]Reuters, “Mexico Becomes Top U.S. Trade Partner,” reuters.com Automotive, electronics, and data-center facilities in Nuevo León, Guanajuato, and Baja California require captive power, prompting rapid upgrades to nearby substations and medium-voltage lines. Industrial tariffs near USD 0.18 per kilowatt-hour sharpen the business case for on-site solar-plus-storage plants that fall inside the new 0.7-20 MW self-generation bracket. As a result, distributed renewables and microgrids are emerging as a standalone opportunity set within the Mexico Power EPC market.

Fast-Track Permitting for ≥ 1 GW Renewable Parks

CFE invited 34 renewable parks totaling roughly 6 GW in October 2025 and offered a six-month environmental review for plants of at least 1 GW. The March 2025 rule that intermittent resources install storage equal to 30% of their nameplate output with a three-hour discharge duration has fused solar, wind, and batteries into single turnkey lots. Six solar plants scheduled for construction in 2027 will integrate 574 MW of batteries, illustrating how EPC scopes are expanding. By compressing permit timelines, CFE has brought a new tranche of mega-projects into the active pipeline, supporting growth in the Mexico Power EPC market.

Rediscovery of Combined-Cycle Retrofits for CO₂ Cuts

Siemens Energy’s four-plant package with CFE adds 4 GW of H-class turbines that cut carbon intensity 10-15% compared with legacy F-class units. GE Vernova’s Topolobampo III, completed in 2024, showed similar results using two 7HA.01 turbines. Blueprints now contemplate hydrogen blending and green-hydrogen auxiliary plants, such as the 210 MW electrolysis project in Sinaloa, awarded for front-end design in 2025. These projects preserve sunk assets while aligning with Mexico’s nationally determined contribution targets, keeping thermal EPC relevant in a renewables-heavy landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shifting political stance on private PPAs | -0.8% | National | Short term (≤ 2 years) |

| Persistent MXN-USD FX volatility | -1.1% | National | Short term (≤ 2 years) |

| Federal ROW clearance bottlenecks | -0.6% | Ejido and indigenous territories | Medium term (2-4 years) |

| Chronic Isthmus-Bajío transmission congestion | -0.9% | Southern export corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shifting Political Stance on Private PPAs Post-2024

The March 2025 energy reform requires CFE to hold at least 54% of generation, reducing room for pure merchant projects. Independent power producers must now co-invest with the utility under mixed-producer schemes, stretching contract negotiations and adding exposure to CFE’s credit metrics. Enel’s partial exit from Mexico in 2024 underscores how foreign utilities are reallocating risk. The regulatory shift weighs on the Mexico Power EPC market until new co-investment templates mature.

Persistent MXN-USD FX Volatility

Dollar-denominated turbine contracts and peso-based tariffs expose EPC margins to currency swings. Depreciations beyond 18.5 pesos per dollar can erode project EBITDA by 200-400 basis points, an acute issue for projects with more than 70% imported content. CFE’s local-content rules, rising to 60% for transmission kits, aim to cut exposure but will take several years to build domestic depth. Until then, hedging costs remain a drag on the Mexico Power EPC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Renewables Dominate While Gas Provides Flexibility

Renewables captured 75.2% of generation value and are poised for a 9.8% CAGR through 2031, propelled by CFE’s invitation to 34 solar and wind parks totaling about 6 GW. Storage rules compel developers to pair solar arrays with batteries, anchoring larger ticket sizes per award. The Mexico Power generation EPC market size for renewables is expected to reach USD 4.35 billion by 2031, equal to half of all generation outlays.

Thermal EPC stays relevant. Siemens Energy’s 4 GW program and Mitsubishi Power’s 1.5 GW duo illustrate continued appetite for gas as a balancing tool.[4]Siemens Energy, “Four-Plant Portfolio Totals 4 GW,” siemens-energy.com Hydrogen-ready turbines and small electrolyzer add-ons hint at future retrofits. Nuclear work remains limited, with no new announcements since Laguna Verde’s 1990s expansions. Hybrid portfolios combining solar, storage, and gas are emerging as the default reliability play, reinforcing volumes in the Mexico Power generation EPC market.

By Capacity Band: Utility-Scale Still Leads but Distributed Growth Accelerates

Plants above 500 MW secured 67.4% of generation spend in 2025, illustrating CFE’s bias toward scale economies. These mega-projects require long lead times yet command favorable tariffs. By contrast, the up-to-100 MW segment will post the fastest 6.1% CAGR as factories adopt on-site solar-plus-storage. That rise pushes smaller EPC contractors into the spotlight, broadening the Mexico Power generation EPC market.

Mid-range schemes between 100 MW and 499 MW include CFE’s González Ortega expansion and several regional combined-cycle add-ons. Water scarcity in northern states constrains thermal build-out in this band, nudging developers toward distributed renewables. The Mexico Power generation EPC market share for plants above 500 MW may edge down by 2031, even as absolute spending grows.

By End User: Utility Dominance Blends with IPP Momentum

CFE and other regulated utilities commanded 70.1% of 2025 spend, underpinned by the utility’s USD 23.4 billion program. Mixed-producer structures now invite minority private equity, allowing IPPs to grow at a 6.7% CAGR and widen the Mexico Power generation EPC market. Iberdrola’s plan to invest USD 1.9 billion after divesting select assets in 2023 signals continued foreign interest.

Industrial captive power is scaling quickly under the 0.7-20 MW rule, giving manufacturers more control over energy costs. Public-sector and state-owned enterprises, including Pemex cogeneration, round out demand by retrofitting aging plants. As co-investment norms solidify, IPPs are set to represent nearly a third of the Mexico Power generation EPC market size for generation by 2031.

Geography Analysis

The Mexico Power EPC market clusters along two axes. Northern industrial states, Nuevo León, Coahuila, and Guanajuato, attract the bulk of T&D upgrades because nearshoring has accelerated factory build-outs. CFE moved substation and line projects planned for the 2030s into the 2026-2028 window, injecting immediate value into regional backlogs. In Baja California, the cross-border CAISO link underpins battery-storage projects like Mexicali Volta, where IFC financing helped secure a 500 MW roadmap.

Southern resource hubs, Oaxaca, Veracruz, and Chiapas, boast rich wind and solar potential but suffer transmission congestion. Until new 400-kV corridors come online late in the decade, developers in these states accept curtailment or defer commercial start dates. Sonora and Sinaloa are emerging as hybrid zones: Acciona’s San Carlos Solar (220 MW) in Sonora and the Pacífico Mexinol electrolyzer in Sinaloa illustrate combined solar-hydrogen playbooks.

The Central Bajío states, Guanajuato, Querétaro, and Aguascalientes, form a manufacturing belt where distributed generation is blossoming. Water scarcity in the far north redirects some heavy industry southward, expanding the catchment for solar-plus-storage microgrids. Local-content rules entice EPC firms to site fabrication yards in Nuevo León and Jalisco, cutting logistics costs. In aggregate, regional variation embeds resilience in the Mexico Power EPC market by diversifying demand drivers.

Competitive Landscape

The Mexico Power EPC market shows moderate concentration. Siemens Energy, GE Vernova, and Mitsubishi Power collectively hold roughly 60% of combined-cycle packages thanks to multi-year master service agreements with CFE. European engineering groups, Acciona, Techint, and Iberdrola Ingeniería, lead renewable EPC bids by bundling storage to meet the 30% battery rule.

Technology is a differentiator. GE Vernova’s Toluca transmission-services hub applies digital-twin analytics that shorten commissioning by roughly 10-15%, positioning the firm favorably for CFE’s digitized tender packets. Techint’s green-hydrogen expertise wins design mandates for electrolysis add-ons, opening a niche that rivals lack. Meanwhile, Siemens Energy captures scale by integrating turbine supply, construction, and long-term service under a single wrap.

White-space potential sits in the distributed segment, where industrial owners need sub-100 MW solar-plus-storage plants and where smaller EPC houses with fabrication ties can win. Local firms aligned with Jalisco’s switchgear manufacturers or Nuevo León’s steel fabricators are stepping into these projects. Competition now hinges on localization, financing creativity, and the ability to deliver turnkey hybrids that satisfy new policy rules. These dynamics keep the Mexico Power EPC market competitive yet accessible for specialized entrants.

Mexico Power EPC Industry Leaders

ICA Fluor

Techint Ingeniería y Construcción

Abengoa México

Elecnor México

Sener Ingeniería y Sistemas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Revolve Renewable Power announced definitive agreements for a portfolio of 16 distributed-generation solar projects in Mexico. These projects aim to support commercial and industrial customers while creating additional demand for EPC (Engineering, Procurement, and Construction) and balance-of-plant contracting within the distributed energy sector.

- February 2026: Mexico also unveiled a new 25-year PPA-based framework under its “Mixed Development Structures” policy to unlock approximately 7.5 GW of renewable investments by 2030. The policy is designed to accelerate EPC deployment for utility-scale renewable and storage assets through partnerships between CFE and private developers.

- August 2025: Techint and Siemens Energy won front-end design for a 210 MW electrolysis plant tied to the Pacífico Mexinol methanol project.

- January 2024: GE Vernova completed the 766 MW Topolobampo III combined-cycle plant using Mexico’s first two 7HA.01 turbines.

Mexico Power EPC Market Report Scope

The power EPC market encompasses the global industry of companies that provide comprehensive execution of power generation, transmission, and distribution projects on a turnkey basis. EPC contractors handle engineering design, equipment procurement, construction, installation, testing, and commissioning of power infrastructure, ensuring project delivery aligns with agreed cost, time, and performance requirements.

The Mexico power EPC market is segmented into power generation EPC and power transmission & distribution EPC. By power generation EPC, the market is segmented into technology, capacity band, and end-user. These segments are further divided as technology- thermal, nuclear, and renewables; capacity band- Up to 100 MW, 100-499 MW, Above 500 MW; end-user- regulated utilities, IPPs, industrial captive power, and public sector/SOE. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion) for all the above segments.

Power Generation EPC

| By Technology | Thermal |

| Nuclear | |

| Renewables | |

| By Capacity Band | Up to 100 MW (DER, micro-grid) |

| 100 to 499 MW | |

| Above 500 MW | |

| By End-User | Regulated Utilities |

| Independent Power Producers | |

| Industrial Captive Power | |

| Public Sector and SOE |

| Power Generation EPC | By Technology | Thermal |

| Nuclear | ||

| Renewables | ||

| By Capacity Band | Up to 100 MW (DER, micro-grid) | |

| 100 to 499 MW | ||

| Above 500 MW | ||

| By End-User | Regulated Utilities | |

| Independent Power Producers | ||

| Industrial Captive Power | ||

| Public Sector and SOE | ||

Key Questions Answered in the Report

How large is the Mexico Power EPC market in 2026?

It stands at USD 6.69 billion and is tracking toward USD 8.74 billion by 2031, supported by a 5.49% CAGR.

Which segment holds the biggest Mexico Power EPC market share?

Renewables dominate generation EPC with 75.2% share in 2025 thanks to CFE's 6 GW solar-and-wind pipeline.

Where are most new T&D projects located?

Northern states such as Nuevo León and Guanajuato host the bulk of the 145 CFE transmission projects slated for 2026-2028.

What is the fastest growing capacity band?

Distributed plants up to 100 MW lead with a 6.1% CAGR as manufacturers install on-site solar-plus-storage systems.

How does the 30% storage mandate affect EPC scope?

Solar and wind developers must add batteries equal to 30% of nameplate output, turning single-technology jobs into turnkey hybrid awards.

Why are foreign EPC firms forming local joint ventures?

Domestic-content thresholds now reach 60% for many components, so foreign contractors partner with Mexican fabricators to secure bids and manage FX risk.

Page last updated on: