Philippines Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 462.90 Million |

| Market Size (2026) | USD 519.75 Million |

| Market Size (2031) | USD 927.23 Million |

| Growth Rate (2026 - 2031) | 12.28% CAGR |

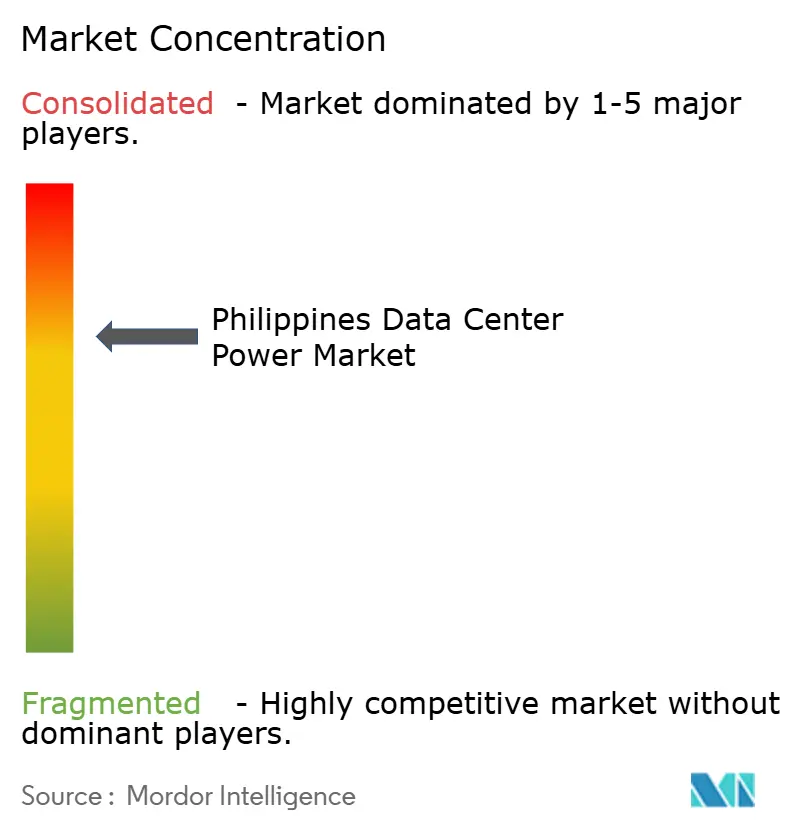

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Data Center Power Market Analysis by Mordor Intelligence

The Philippines data center power market size is expected to grow from USD 462.90 million in 2025 to USD 519.75 million in 2026 and is forecast to reach USD 927.23 million by 2031 at 12.28% CAGR over 2026-2031. The expansion is supported by faster cloud adoption, a surge of hyperscale projects and government plans to add 1 gigawatt of data-center capacity by 2029. Eased permitting for renewable energy, a PHP 639 billion green-lane pipeline and the Energy Virtual One-Stop Shop are reducing lead times for new power assets. March 2025 power-price volatility—from PHP 2.73 to PHP 5.34 per kWh—highlighted the need for stable backup capacity. As hyperscale operators insist on energy-efficient designs, demand for advanced UPS, PDUs and hybrid micro-grid solutions is gaining momentum. Competitive pressure stays moderate: Schneider Electric, Vertiv and Eaton hold strong brand recognition, yet local alliances and service quality often decide contract wins.

Key Report Takeaways

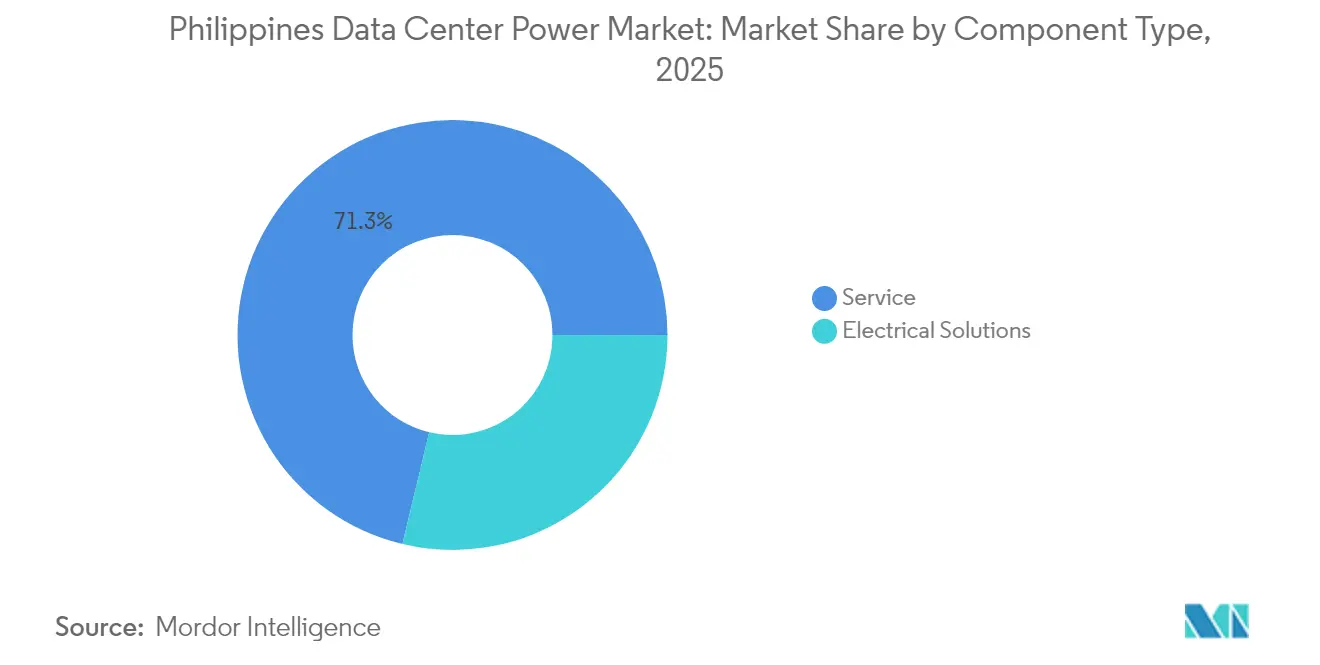

- By component, UPS Systems led with 28.74% of the Philippines data center power market share in 2025, whereas Power Distribution Units are predicted to post a 16.07% CAGR to 2031.

- By data-center type, Colocation Providers held 53.60% revenue share in 2025; Hyperscale/Cloud Service Providers are set to accelerate at 16.84% CAGR through 2031.

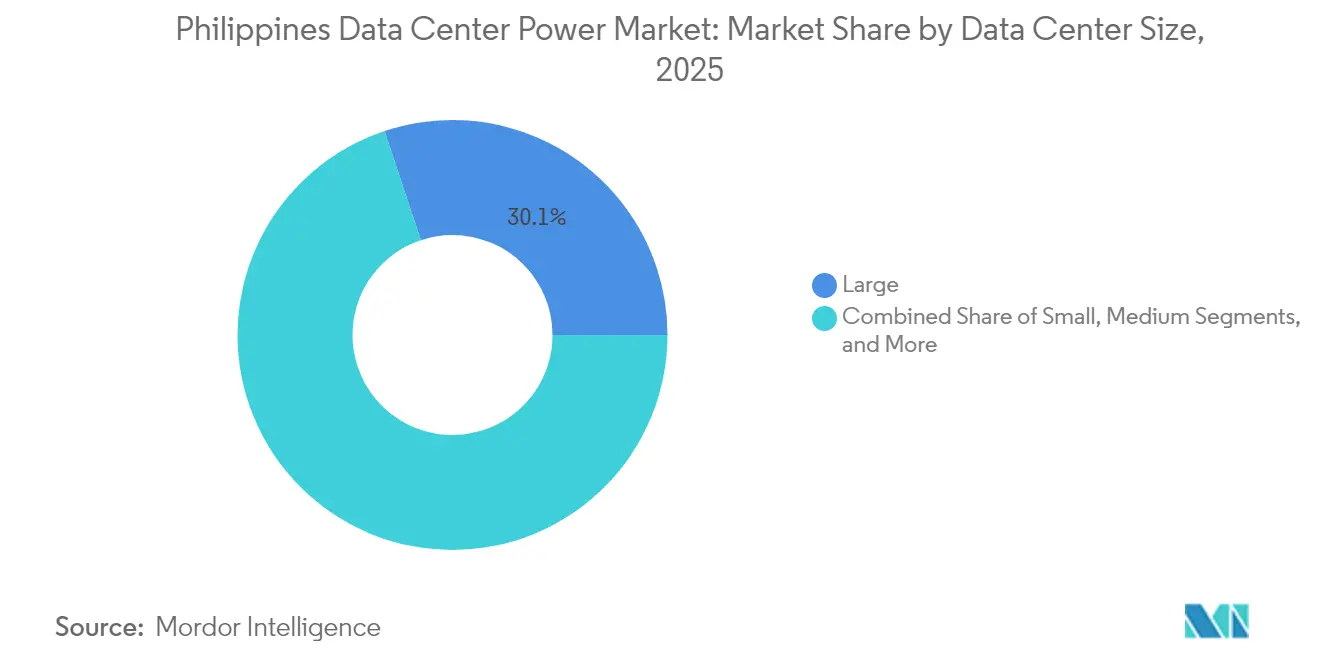

- By size, Large facilities accounted for 30.12% of the Philippines data center power market size in 2025, while the Mega category is forecast to expand at an 17.82% CAGR.

- By tier, Tier III captured 53.55% share of the Philippines data center power market size in 2025; Tier IV facilities are projected to grow at 15.96% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-service hyperscale build-out | +2.8% | National, concentrated in Metro Manila and Central Luzon | Medium term (2-4 years) |

| Cost-driven UPS retrofits in metro Manila | +1.9% | Metro Manila and surrounding provinces | Short term (≤ 2 years) |

| Rapid fibre network densification | +1.5% | National, with priority in urban centers | Medium term (2-4 years) |

| Renewable-hybrid micro-grids for edge DCs | +1.2% | Provincial areas and island communities | Long term (≥ 4 years) |

| Green-tax incentives for high-efficiency gensets | +0.8% | National, with focus on industrial zones | Medium term (2-4 years) |

| Modular DC-in-a-box roll-out by telecom towers | +0.6% | National, prioritizing underserved regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-service hyperscale build-out

ST Telemedia’s USD 1 billion, 124 MW STT Fairview 1 facility that opened in 2025 set a new local record for single-site investment.[1]STT GDC confirmed Q2 2025 opening of its 124 MW Fairview site STT GDC ENDECGROUP’s 300 MW Narra Technology Park, planned for late 2026, shows that hyperscalers now view the archipelago as an alternative to crowded hubs like Singapore. Alibaba Cloud launched its first site in 2024 and five US providers are evaluating land banks for future builds. Each added megawatt of hyperscale space triggers USD 7-12 million in power gear spending, creating steady pull for high-efficiency UPS and PDUs. These projects raise average rack density and push suppliers to deliver solutions ready for AI workloads that often exceed 30 kW per rack.

Cost-driven UPS retrofits in Metro Manila

The March 2025 tariff spike forced many legacy colocation operators to advance replacement cycles for 2010-era UPS fleets. Socomec’s DELPHYS XM, with 99% efficiency and 0.8 m² footprint, illustrates how vendors target space- and energy-constrained sites.[2]Socomec Editorial Team, “DELPHYS XM: 99 Percent Efficient UPS,” socomec.com Vertiv’s advisory on UPS tuning during record heat events in 2024 also pushed upgrades that cut power losses and cooling loads. Retrofit demand is strongest in Metro Manila, where 20 facilities house over 60% of national rack capacity and operators seek lower PUE to defend margins. Replacement activity supports a rising service market for commissioning and remote monitoring contracts.

Rapid fibre network densification

PLDT’s newest Clark data center added 1,200 racks and brings its rack estate above 8,000, a direct outcome of densifying backbones. Converge ICT’s two Tier III builds, totaling 1,500 racks, underline the integration of last-mile fibre and data-center services. Government spending of 5-6% of GDP on connectivity until 2028 pushes carriers to expand into secondary cities.[3]Asian Development Bank Authors, “Public Infrastructure Spending Outlook 2025-2028,” adb.org Edge computing at 5G towers raises demand for compact power blocks; Vertiv’s SmartAisle 3 supports 120 kW loads in a single enclosure. Fibre penetration in provincial centers is therefore translating into dispersed need for resilient, quickly deployable power systems.

Renewable-hybrid micro-grids for edge DCs

DOE has awarded eight micro-grid franchises across Cebu, Quezon and Palawan that combine solar, batteries and diesel to serve remote clusters. Sabang Renewable Energy’s 1.4 MW solar plus 2.3 MWh storage plant in Palawan shows an early commercial template. Studies on the Polillo Islands suggest hybrid mixes cut generation cost 42.01% while lifting renewable share to 80% Energies. The Microgrid Systems Act grants 20-year tariff support, reducing payback risk for investors. Such schemes align with telco tower operators that install edge nodes needing off-grid power independence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and OPEX of Tier III/IV compliance | -2.1% | National, with higher impact in provincial areas | Medium term (2-4 years) |

| Grid instability and diesel price volatility | -1.8% | National, with acute impact in Visayas and Mindanao | Short term (≤ 2 years) |

| Delays in DOE clearance for >1 MW generators | -1.3% | National, affecting large-scale projects | Medium term (2-4 years) |

| Scarcity of Level 3 electrical contractors outside NCR | -0.9% | Provincial areas outside Metro Manila | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and OPEX of Tier III/IV compliance

Converge ICT’s Tier III push in Metro Manila and Pampanga highlights the 40% CAPEX premium attached to redundant power paths and dual utility feeds. PLDT’s TIA-942 Rated 3 estate of 26.5 MW needed roughly USD 8-10 million per added megawatt of power infrastructure. Smaller provincial operators face a steeper hurdle because revenue density is lower than in the capital. Ongoing costs mount as redundant generators, UPS strings and switchgear demand skilled maintenance teams that remain scarce outside Luzon. As a result, many second-tier cities still rely on Tier II halls that limit uptake from financial and cloud tenants.

Grid instability and diesel price volatility

The Luzon grid issued its first yellow alert of 2025 when only 659 MW of reserve margin stood between supply and blackouts. Forced outages affecting 3,362.3 MW capacity, plus 19 end-of-life plants retired in 2024, exacerbate the risk South China Morning Post. Peak-hour spot prices spiked to PHP 12.15 per kWh in March 2025, making genset operation the lesser evil despite high fuel bills. Visayas facilities are most vulnerable because they import power from Mindanao, yet still face undersupply. Operators, therefore, maintain large diesel inventories, exposing them to commodity price swings that tighten profit margins and complicate long-term planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems anchor modernization

UPS Systems held 28.74% of the Philippines' data center power market share in 2025 due to their vital role in shielding IT loads from frequent grid events, Manila Standard. A single 124 MW hyperscale launch can lift UPS demand by USD 350-400 million, pushing global vendors to localize inventories. PDUs are tracking a 16.07% CAGR thanks to hyperscale designs that need refined branch monitoring and load balancing. Switchgear, transfer switches, and remote power panels remain standard fixtures, but their growth trails the advanced monitoring segment. Generators stay relevant, although gas and hydrogen pilots are inching forward in Luzon industrial parks.

Energy-storage systems record faster take-up where hybrid micro-grids combine solar and batteries to limit genset run-time. Socomec’s 0.8 m² DELPHYS XM shows how suppliers tackle space and sustainability goals simultaneously. Service revenue—installation, commissioning, preventive care—scales in parallel as operators pivot toward outcome-based support contracts. The Philippines data center power market, therefore, rewards vendors that can bundle hardware with lifecycle services.

By Data Center Type: Colocation still leads, hyperscale rising

Colocation providers controlled 53.60% of the Philippines data center power market in 2025, a share built on carrier neutrality and tenant diversity. Digital Edge’s NARRA1 in Manila is rated as the nation’s most energy-efficient carrier-neutral site, underscoring scale economics in shared models. Enterprise and edge facilities complete the mix, serving banks and telcos that need local latency.

Hyperscale builds are moving faster, showing a 16.84% forecast CAGR and driving mega-project pipelines in Central Luzon. STT Fairview 1 at 124 MW and PLDT’s 50 MW VITRO Sta. Rosa illustrates how telecom incumbents pivot toward GPU-as-a-Service aligned with AI demand,. These capital-heavy sites compress construction cycles to under 24 months, raising the bar for coordinated power, cooling and fibre delivery. Hybrid models, where a colocation wing co-exists with dedicated halls for one hyperscale tenant, are emerging to balance utilization risk.

By Data Center Size: Large sites hold ground, mega sites scale up

Large facilities held a 30.12% share of the Philippines data center power market size in 2025, as early builds generally topped out at 50 MW. They still capture steady refresh spending from telecom and enterprise tenants. Mega facilities, however, are projected to post an 17.82% CAGR through 2031, reflecting the strategic decision by global operators to secure contiguous land and grid connections years in advance. ENDECGROUP’s 300 MW Narra Technology Park redefines local capacity limits and is likely to spur a similar scale in adjacent provinces.

Massive and medium footprints remain relevant where zoning, grid access or demand profiles cannot justify mega outlays. Small edge nodes flourish at 5 GWh towers across islands, leaning on modular DC-in-a-box formats that integrate UPS, thermal and security in a single skid. The Philippines data center power industry thus exhibits a dual track: urban mega campuses on one side, and agile micro sites on the other.

By Tier Level: Tier III dominates, Tier IV gains traction

Tier III designs captured 53.55% of the Philippines data center power market size in 2025 because they deliver 99.982% uptime at a manageable cost, a sweet spot for colocation and banking tenants, PLDT Enterprise. Operators optimize for concurrent maintainability rather than full fault tolerance, trimming both build and run expenses. Tier I and II halls still serve DR and non-mission-critical loads in provincial zones.

Tier IV demand is rising with AI, fintech and international cloud mandates, bringing a 15.96% CAGR outlook. The added reliability requires dual independent power feeds, mirrored UPS strings and active-active switchgear, all of which lift per-MW cost. ST Telemedia incorporates energy-efficient chillers and renewable PPAs to offset the premium STT GDC. As long as uptime penalties stay severe, top-end clients will tolerate the extra spend, keeping Tier IV on an upward trajectory.

Geography Analysis

Metro Manila hosts roughly 20 active data centers run by seven operators, making it the anchor of the Philippines' data center power market. Its proximity to seven submarine cable landings and the largest skilled workforce base sustains steady investment inflows, Baxtel. Central Luzon, notably Clark and Tarlac, is the fastest-growing corridor because of land availability, renewable-energy zones, and incentives that cut build time by up to six months, Philippine News Agency. STT Fairview 1 and Narra Technology Park alone add nearly 450 MW combined committed capacity, underscoring the shift north of the capital.

Visayas and Mindanao show budding interest despite grid constraints. Meralco PowerGen’s planned 20-40 MWh battery storage in Cebu aims to stabilize local frequency events and could unlock colocation builds near Tech Hubs in South Manila, Standard. DOE-backed micro-grids in Palawan and Quezon will provide reliable electrons for small edge nodes serving tourism and agri-tech clusters, according.

Policy tailwinds matter. The Board of Investments green-lane pipeline funnels PHP 639 billion to clean-energy assets, favoring provinces that can guarantee renewable supply guarantees to new data centers Philippine News Agency. Government infrastructure spends equal 5-6% of GDP, with a sizable share for digital highways that connect Cebu, Davao and Baguio through new fibre spurs Asian Development Bank. These factors help spread the Philippines data center power market beyond traditional Metro hub status.

Competitive Landscape

Schneider Electric, Vertiv, and Eaton retain leadership by leveraging global product depth, local warehousing, and certified service teams. Schneider’s MasterPacT MTZ Active breaker with built-in sensors positions the firm for Industry 4.0 and data-center retrofits, Manila Standard. Vertiv differentiates through SmartAisle micro-modular kits that compress deployment time for banks and healthcare, Manila Standard. Eaton focuses on lithium-ion UPS modules that slash footprint and maintenance intervals.

Local alliances are equally decisive. STT GDC Philippines bundles Schneider switchgear with Meralco power contracts to fast-track grid interconnections, Philippine News Agency. PLDT taps First Gen for at least 180 MW of renewable supply, linking brownfield sites to a cleaner grid profile Philippine News Agency. These tie-ups allow both sides to navigate licensing, talent, and logistics hurdles swiftly.

White-space opportunity lies in provincial edge builds where few incumbents have a strong presence. New entrants that arrive with turnkey solar-battery-diesel hybrids or AI-ready modular blocks can win share without directly confronting entrenched players in Metro Manila. The Philippines data center power market will therefore reward flexible service models, not sheer product breadth.

Philippines Data Center Power Industry Leaders

ABB Ltd.

Schneider Electric SE

Vertiv Group Corp.

Eaton Corporation plc

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: PLDT inaugurated the Vitro Sta. Rosa hyperscale center with 50 MW initial capacity and GPU-as-a-Service features

- April 2025: President Marcos opened the StB Giga Factory, the first Philippine LFP battery plant with 300 MWh output and PHP 10 billion future investment plan

- March 2025: Beeinfotech launched the PH HIVE hybrid facility in Manila, housing 3,600 racks under Tier 3+ rating

- March 2025: ABB pledged USD 120 million to widen low-voltage breaker capacity in the US, enhancing supply for Asia data-center customers

- February 2025: Schneider Electric reported strong 2024 earnings tied to global data-center demand.

- January 2025: SolX Technologies and YCO Cloud unveiled the Malvar One hyperscale build in Batangas.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Philippines data center power market as all revenue earned from electrical infrastructure that guarantees clean, continuous electricity inside local data centers. This covers factory-built uninterruptible power supply systems, diesel or gas generators, power distribution units, switchgear, transfer switches, remote power panels, and energy-storage add-ons sold for new builds as well as refreshes.

Scope exclusion. Cooling equipment, IT servers, mechanical construction, and retail electricity tariffs lie outside this market.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Desk Research

Our analysts first map the country's data-center footprint using open information from the Department of Information and Communications Technology, the Philippine Statistics Authority, and the Energy Regulatory Commission. They then relate it to import statistics, building permits, and tariff filings. Annual reports, investor decks, and Luzon grid expansion plans supply installed-base clues, while D&B Hoovers and Dow Jones Factiva help us follow vendor revenue trends. Trade association briefs from the Asia Cloud Computing Association and IEEE journals clarify efficiency norms and conversion factors. The sources mentioned illustrate the breadth consulted; many additional public and subscription assets were reviewed as well.

Primary Research

We spoke with facility operators in Metro Manila and Cebu, regional engineering consultants, UPS and generator suppliers, and utility regulators. Their insight sharpened unit price bands, typical power density, and commissioning schedules, filling gaps left by public data.

Market-Sizing & Forecasting

Mordor Intelligence builds a top-down model that starts with megawatts of live and planned capacity, multiplies by standard power gear cost per megawatt, and is then cross-checked with a bottom-up roll-up of vendor shipments collected during interviews. Key variables include new data-center floor area, average power density, import value of UPS equipment, diesel price outlook, renewable-energy targets, and announced hyperscale projects. A multivariate regression linking these drivers to historical spend provides the base year, after which scenario analysis and exponential smoothing guide the 2025-2030 forecast. Where supplier data are partial, interpolation uses median price benchmarks agreed with experts.

Data Validation & Update Cycle

Before release, senior analysts test the model against customs records, grid connection approvals, and reported vendor bookings. Outliers trigger a re-survey. Reports refresh each year, with interim updates when material capacity announcements occur.

Why Mordor's Philippines Data Center Power Baseline Commands Reliability

Published estimates often vary because each firm selects its own market boundary, escalation factors, and refresh cadence.

Differences in whether services revenue, partial equipment categories, or currency adjustments are included drive most gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 462.9 million (2025) | Mordor Intelligence | - |

| 462.9 million (2024) | Global Consultancy A | Keeps base-year values, omits services revenue uplift |

| 411.5 million (2025) | Industry Newsletter B | Relies on limited supplier survey, excludes after-sales services |

| 633 million (2024) | Regional Consultancy C | Captures total construction and IT hardware, not isolated power gear |

The comparison shows that while others either broaden the scope or skip key revenue pockets, our disciplined definition, multi-source validation, and yearly refresh give decision-makers a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

How large is the Philippines data center power market in 2026?

The market is valued at USD 519.75 million in 2026 and is projected to reach USD 927.23 million by 2031 on a 12.28% CAGR over 2026-2031.

Which component leads spending?

UPS Systems hold the top spot with 28.74% market share on account of widespread grid reliability issues.

Where are most new hyperscale sites being built?

Metro Manila remains dominant, but Central Luzon provinces such as Tarlac and Pampanga are now attracting the largest green-field projects.

What is the key restraint facing operators?

High capital and operating costs to meet Tier III and IV standards, especially outside major urban centers, curb new entrants.

How does fibre expansion influence power demand?

Rapid fibre densification drives edge facilities that require compact, high-efficiency power blocks, lifting demand for modular UPS, PDUs and micro-grids.

Which firms are market leaders in power equipment?

Schneider Electric, Vertiv and Eaton command significant share, complemented by local alliances that expedite project delivery.

Page last updated on: