Philippines Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

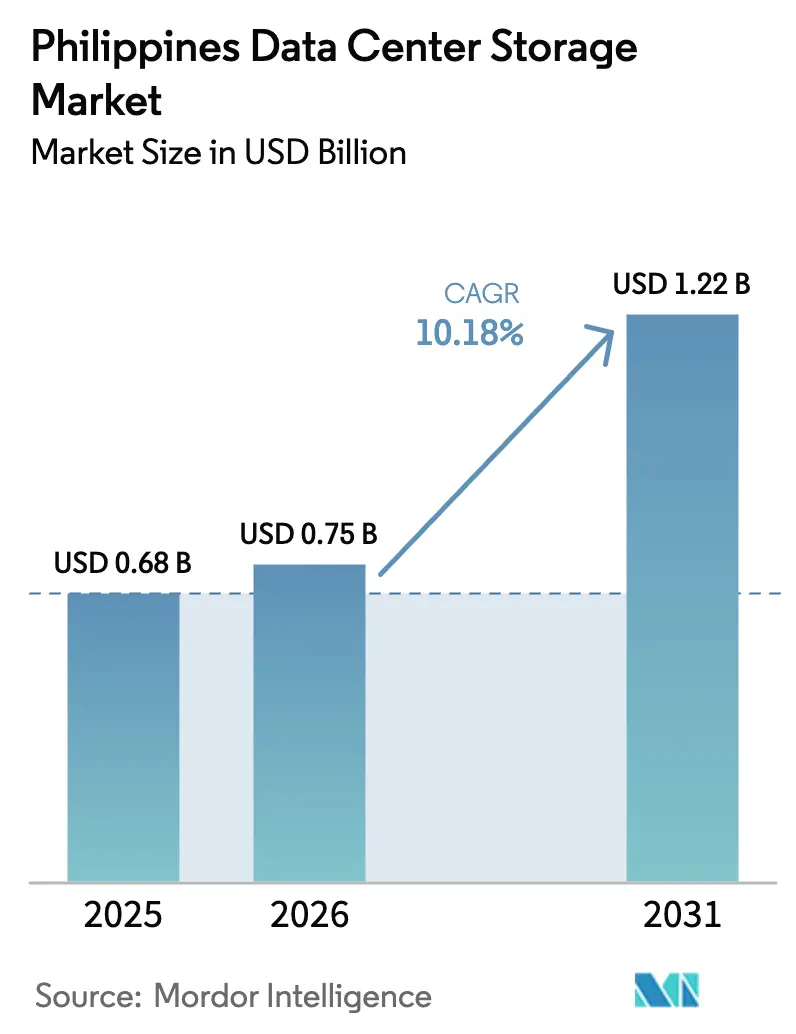

| Base Year Market Size (2025) | USD 0.68 Billion |

| Market Size (2026) | USD 0.75 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Data Center Storage Market Analysis by Mordor Intelligence

The Philippines data center storage market size was valued at USD 0.68 billion in 2025 and estimated to grow from USD 0.75 billion in 2026 to reach USD 1.22 billion by 2031, at a CAGR of 10.18% during the forecast period (2026-2031). Continued public-sector digitization, hyperscale build-outs, and strict data-localization rules are positioning the archipelago as a regional storage hub that meets rising AI and cloud workloads. Storage spending is also buoyed by the CREATE investment incentives and by the Department of Information and Communications Technology (DICT) target of expanding national data-center capacity to 300 MW by 2025 [1]U.S. Department of Commerce, “Philippines – ICT Infrastructure Overview,” trade.gov. Sustained currency weakness, a skills gap in certified professionals, and uneven inter-island fiber remain headwinds, yet submarine cable projects and the National Grid Corporation’s 2023-2040 plan are mitigating infrastructure risk [2]National Grid Corporation of the Philippines, “Transmission Development Plan 2023–2040,” ngcp.ph.

Key Report Takeaways

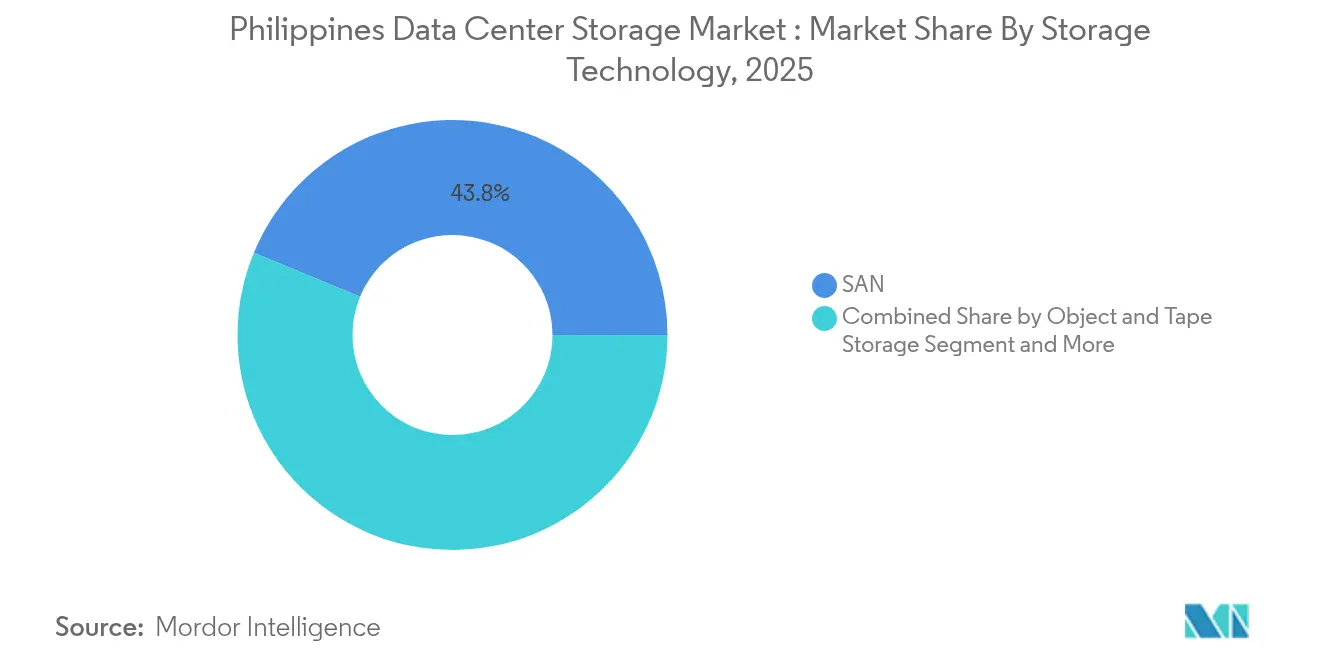

- By storage technology, Storage Area Network solutions led with 43.75% revenue share in 2025, whereas Object and Tape Storage is forecast to expand at a 12.02% CAGR through 2031.

- By storage type, traditional HDD arrays accounted for a 41.60% share of the Philippines data center storage market size in 2025, while all-flash arrays are advancing at a 12.85% CAGR through 2031.

- By data-center type, colocation facilities captured 52.55% of Philippines data center storage market share in 2025, while hyperscalers record the fastest 14.75% CAGR through 2031.

- By end user, IT and telecommunications held 38.65% revenue share in 2025; healthcare and life sciences is projected to expand at a 14.12% CAGR to 2031.

- Dell, NetApp, and Pure Storage collectively commanded 37.5% of external enterprise storage revenue in 2024, highlighting moderate market concentration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of IT infrastructure and digital transformation | +2.8% | National, concentrated in Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Surge in hyperscale and colocation investments | +2.1% | Metro Manila, expanding to Clark, Laguna | Short term (≤ 2 years) |

| Rapid cloud and hybrid-cloud adoption | +1.9% | National, with enterprise concentration in NCR | Medium term (2-4 years) |

| Government CREATE and DICT green-DC incentives | +1.4% | National, with focus on economic zones | Long term (≥ 4 years) |

| BSP Circular 1122 data-localization mandate | +1.2% | National, primarily affecting financial sector | Short term (≤ 2 years) |

| AI-driven analytics workload boom (NVMe flash uptake) | +1.0% | Metro Manila, expanding to secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of IT infrastructure and digital transformation

The digital economy reached USD 45 billion in 2024, equating to 8.5% of GDP, and could unlock PHP 5 trillion in value by 2030. This national pivot is overhauling storage architectures as enterprises move from siloed arrays to cloud-native platforms that scale elastically. Manila Water’s cloud-based water-management rollout illustrates mission-critical adoption, safeguarding service continuity for 27 million residents while minimizing data-loss risk. Government programs such as the Digital Philippines Campaign and the National Broadband Plan mean 85% of firms intend to migrate workloads to cloud by 2026, spurring uptake of hybrid storage that spans on-premises, edge, and hyperscale facilities. The Department of Trade and Industry’s Smart Industry Readiness Index across 400+ factories is further prompting demand for edge storage that enables real-time analytics.

Surge in hyperscale and colocation investments

Hyperscalers are allocating USD 4.7 billion to Philippine builds in 2024 alone, as AI racks require more than double traditional power density.[3]Telecom Review Asia, “Hyperscalers eye Philippines in 2024,” telecomreviewasia.com Equinix’s USD 100 million purchase of three Manila sites adds 1,000 carrier-neutral cabinets, demonstrating foreign confidence. PLDT opened a 50 MW hyperscale facility and is weighing a USD 1 billion REIT listing, while Globe Telecom has broken ground on a 124 MW campus . Narra Technology Park’s 300 MW green data-center build in New Clark City will be the country’s largest. These projects demand NVMe-based all-flash arrays that deliver low-latency throughput for AI inference workloads.

Rapid cloud and hybrid-cloud adoption

The BSP Digital Payments Transformation Roadmap digitized 50% of retail transactions by 2023 and is now pursuing cross-border payment interoperability through Project Nexus and Open Finance. UnionBank’s multiyear cloud and cybersecurity revamp relies on performant storage for real-time processing, supported by Palo Alto Networks NGFWs. As of November 2024, 1,277 government systems sit on cloud platforms through DICT’s eGovCloud, underscoring the state’s cloud-first posture DICT. Submarine routes such as Bifrost and TPU cables expand backhaul capacity, enabling hybrid architectures that blend local compliance with cross-border scale .

Government CREATE and DICT green-DC incentives

Executive Order 18 activates “green lanes” and a one-stop action center that cuts red tape for strategic facilities, fast-tracking builds like Narra’s 300 MW campus. The CREATE MORE Act and PEZA eco-zone rules offer tax holidays and duty exemptions, heightening ROI on storage infrastructure . Operators are trialing renewable power and liquid cooling, aligning with national 95% digital-TV coverage and Maharlika Fund financing that favor sustainable, large-scale deployments.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for enterprise-grade storage | -1.8% | National, particularly affecting SMEs | Medium term (2-4 years) |

| Shortage of certified storage engineers | -1.2% | National, acute in secondary cities | Long term (≥ 4 years) |

| Inter-island fibre and power reliability gaps | -0.9% | Visayas and Mindanao regions | Long term (≥ 4 years) |

| Peso depreciation inflating imported flash costs | -0.7% | National, affecting all import-dependent segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capex for enterprise-grade storage

Flash media retains a 5-7× price premium to HDD despite 15% annual declines and a projected 60% QLC price crash between 2022-2025. SMEs struggle to fund redundant arrays, backup appliances, and compliance controls mandated by the Data Privacy Act. Financing gaps are wider outside Metro Manila, where leasing and credit lines are limited. Subscription models are gaining ground—Pure Storage’s Evergreen portfolio drove 22% subscription revenue expansion in Q3 FY 2025—offering opex options that soften initial cash outlays.

Shortage of certified storage engineers

Only 564 Huawei-certified ICT graduates have entered the workforce since 2020, far below surging demand for NVMe-over-Fabrics, AI-optimized, and software-defined storage skill sets Huawei. Talent migration to Manila or overseas widens shortages in Cebu, Davao, and Clark. Red Hat and other vendors provide Kubernetes-storage training, yet supply lags the Philippines data center storage market growth trajectory. DICT’s 2023-2028 National Cybersecurity Plan highlights workforce development, but storage specialization remains underfunded.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN dominance meets object-storage surge

Storage Area Networks led revenue with 43.75% share in 2025, underscoring their reliability for mission-critical core-banking and telco OSS/BSS workloads. Object and Tape Storage is the fastest riser at 12.02% CAGR, propelled by AI, media streaming, and IoT data that scale better on flat-namespace architectures. Network-attached systems retain footholds among SMEs that favor file-level simplicity, while direct-attached setups cater to HPC clusters in research labs. The Philippines data center storage market size for object storage will expand swiftly as hyperscalers like Google deploy TPU cables delivering 260 Tbps capacity and flooding local nodes with unstructured content Vendors such as Dell have embedded S3-compatible services in PowerStore, aligning block, file, and object protocols inside a single appliance.

Operators increasingly apply AI-infused tiering to shuttle cold datasets into tape libraries or cloud buckets while reserving SAN flash for latency-sensitive analytics. This optimization preserves capital and aligns with BSP retention rules. In turn, the Philippines data center storage market benefits from widening hybrid adoption across BFSI and media enterprises pursuing cost-per-GB discipline without sacrificing performance.

By Storage Type: All-flash ascends amid HDD resiliency

HDD arrays still captured 41.60% revenue in 2025, servicing media archives and backup vaults that value USD/terabyte. Yet all-flash arrays will post a 12.85% CAGR through 2031 as AI inference workloads require microsecond response times. The Philippines data center storage market share of all-flash will thus rise sharply alongside NVMe penetration. Seagate’s 30 TB Heat-Assisted Magnetic Recording drives underscore HDD innovation, yet Western Digital’s corporate split indicates divergent futures for disk and flash. As flash price curves drop 15% yearly, hybrid arrays offer a compromise, combining SSD tiers with high-capacity spindles to serve transactional databases across telecom and fintech tenants.

Migration to flash accelerates under DICT’s cloud-first policy because SaaS and PaaS stacks expect IOPS densities unattainable on legacy HDD SANs. Data-localization rules also keep large datasets on-shore, lifting demand for efficient flash-based deduplication that stretches scarce floor space in Metro Manila. Consequently, the Philippines data center storage market continues to skew toward NVMe and QLC SSD deployments over the forecast horizon.

By Data-Center Type: Hyperscalers race ahead

Colocation remains dominant with 52.55% revenue in 2025, mirroring enterprises’ preference for neutral facilities that bundle carrier route diversity and lower latency. However, hyperscalers and CSPs post the highest 14.75% CAGR, pushed by data sovereignty requirements and gaming, fintech, and e-commerce traffic spikes. The Philippines data center storage market size generated by hyperscalers will surpass USD 0.64 billion by 2031. PLDT’s ambition to spin off its USD 1 billion portfolio and Equinix’s Manila entry confirm capital-market appetite for hyperscale platforms.

Government disaster-recovery mandates further elevate demand for resilient colocation suites outside Metro Manila, yet grid and fiber gaps in Visayas and Mindanao slow immediate uptake. Even so, New Clark City’s 300 MW hyperscale campus signals decentralization momentum, ensuring the Philippines data center storage market maintains balanced growth across tenancy models.

By End User: Healthcare outstrips telecom

IT and telecom generated 38.65% revenue in 2025 as 5G core rollouts and network-function virtualization soaked up capacity. Electronic medical record adoption, tele-radiology, and mHealth services will propel healthcare at a 14.12% CAGR, making it the fastest riser through 2031. Iron Mountain already safeguards 850 million patient files and 1 billion images, illustrating scale. Public-sector digitization via the eGovPH super-app similarly fuels secure storage needs for citizen data exchanges.

Media houses such as ABS-CBN stream 10 million daily YouTube users, boosting low-latency object storage demand to deliver HD content ABS-CBN. Under the Smart Industry Readiness Index, 400+ factories deploy edge nodes for predictive maintenance, further diversifying the Philippines data center storage market end-user tapestry.

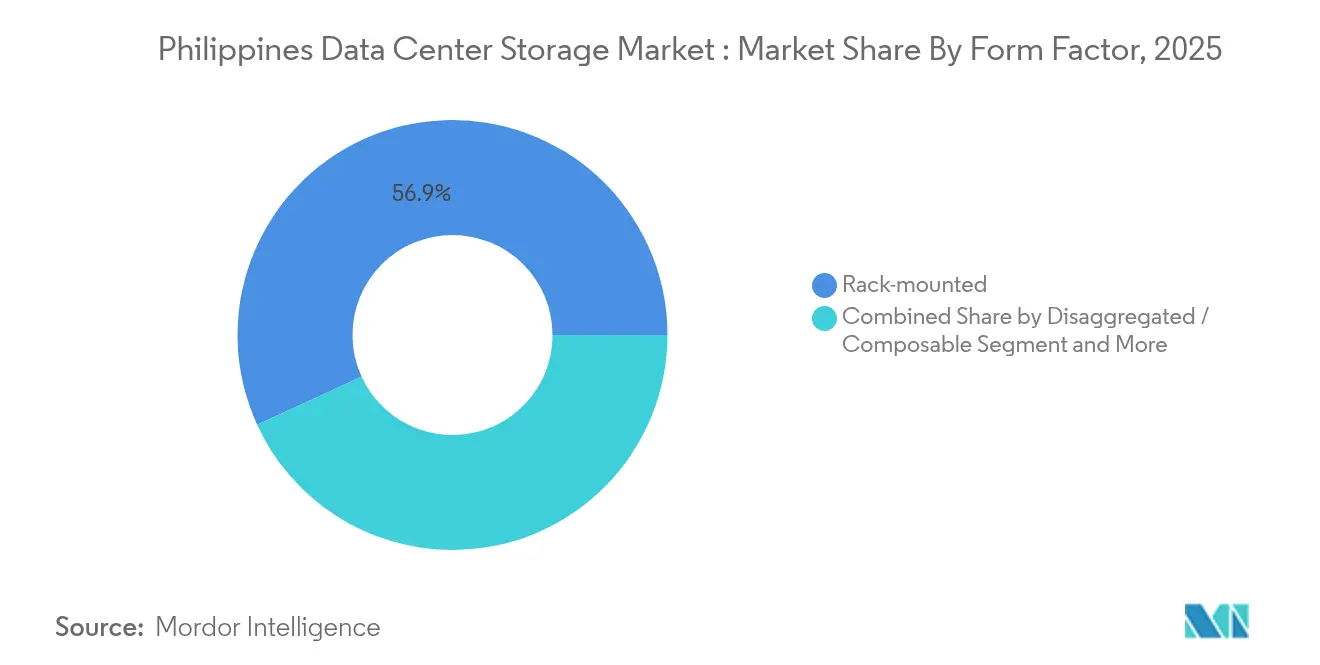

By Form Factor: Disaggregation gains ground

Rack servers still rule with 56.85% share in 2025 given standard 42U footprints and familiar operations. Yet disaggregated or composable infrastructure will expand at 13.2% CAGR, underpinned by software-defined control planes that reallocate compute, GPU, and storage resources on demand. The Philippines data center storage market size for composable gear will rise as AI labs seek pooled GPU farms decoupled from storage trays. Nutanix’s unified storage illustrates convergence of file, block, and object services, while CommScope forecasts 800G optical links that unlock east-west bandwidth essential for disaggregation.

Blade and modular chassis still serve space-constrained telco exchanges and finance trading floors, but next-generation workloads favor flexible PCIe-fabrics that minimize stranded capacity. Over time, rack incumbency will erode as enterprises modernize under DICT’s green-DC incentives.

By Interface: NVMe momentum builds

Legacy SAS/SATA commands 51.70% share due to large installed SAN bases, yet NVMe will post a 12.41% CAGR to 2031 as PCIe 5.0 and CXL reach production. The Philippines data center storage industry sees MiTAC’s Xeon 6 servers and Cisco-Lenovo DG arrays unleashing QLC all-flash optimized for generative AI Cisco. Fibre Channel persists in regulated banks, but NVMe-over-TCP and RoCE are eroding its grip with simpler fabric design and lower cost per port.

As hyperscalers land AI GPUs locally, NVMe becomes the default to eliminate I/O bottlenecks. Consequently the Philippines data center storage market is shifting toward end-to-end NVMe stacks that pair flash media with low-overhead protocol access for maximum throughput.

Geography Analysis

Metro Manila houses roughly 80% of live data-center capacity, a proportion expected to climb to 91% by 2028 given dense fiber routes, reliable power, and skilled labor. The Philippines data center storage market size concentrated in the capital therefore commands premium colocation rates and drives vendors to offer high-density rack options to conserve floor area. NGCP’s 2023-2040 Transmission Plan introduces battery energy storage and smart-grid controls to improve uptime, while the Bifrost, TPU, and CAP-1 cables add 370 Tbps aggregate capacity, reinforcing Manila as a subsea landing hub .

Government ambitions to diversify infrastructure underpin secondary clusters in Cebu, Davao, and Clark. PEZA incentives and lower land costs attract greenfield builds, though grid stability and certified-talent shortages temper immediate scaling. World Bank financing of USD 750 million for digital transformation strengthens provincial broadband backbones, supporting gradual expansion of the Philippines data center storage market outside Luzon.

New Clark City’s Narra Technology Park exemplifies deliberate decentralization: its 300 MW facility leverages renewable energy and proximity to an international airport, while DICT’s Very Small Aperture Terminal network supplies satellite backup connectivity for disaster resilience. Such projects broaden geographic reach, ensuring the Philippines data center storage market is not overly exposed to Metro Manila-centric risks yet continues to benefit from economies of scale.

Competitive Landscape

The market is moderately fragmented. Dell holds 29.2% of external enterprise storage revenue with PowerStore and PowerMax arrays, supported by data-reduction and NVMe roadmaps. NetApp maintains 8.3% share leveraging ONTAP, Keystone STaaS, and cloud-native integrations, while Pure Storage captures momentum in all-flash with Evergreen-based subscriptions that grew 22% in Q3 FY 2025 . Collectively, the top three account for roughly 37.5% of spend, leaving space for HPE, Huawei, Hitachi Vantara, and local system integrators.

Strategic differentiation now centers on AI-optimized architectures such as Seagate’s 3 TB-per-platter HAMR drives for cold data and Western Digital’s split that aligns business models to distinct flash and disk trajectories. Local partners bundle these global technologies with compliance consulting to navigate BSP localization rules. Edge-storage niches for manufacturing and robust DRaaS offerings for government agencies present open white-space opportunities.

Hyperscaler self-builds add a captive tier: PLDT, Globe, and Narra each integrate on-prem flash arrays with proprietary object stores, reducing available pie for traditional vendors yet creating pull-through for components and services. Consequently, partnerships rather than pure product sales are becoming the dominant go-to-market motion in the Philippines data center storage market.

Philippines Data Center Storage Industry Leaders

Dell Inc.

Huawei Technologies Co. Ltd.

Hewlett Packard Enterprise Company

Lenovo Group Limited

NetApp, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Equinix finalized the USD 100 million acquisition of three Manila facilities, adding 1,000 carrier-neutral cabinets to support the USD 45 billion digital economy

- February 2025: DICT launched the eGovPH app integrating 30 agency services, expanding demand for consolidated storage back-ends

- December 2024: Pure Storage logged USD 831.1 million revenue in Q3 FY 2025, up 9%, with 22% subscription growth via Evergreen//One and Evergreen//Flex

- December 2024: Seagate shipped the world’s first 30 TB HAMR HDDs, targeting energy-efficient petabyte-scale arrays

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Philippines data center storage market as all hardware, embedded software, and management tools that store, protect, and retrieve digital information inside purpose-built data-center facilities nationwide, spanning SAN, NAS, DAS, object, and tape subsystems. We track spend generated by colocation halls, hyperscale campuses, and captive enterprise sites, converted to end-user revenue.

Scope exclusion: Edge appliances installed in branch offices or street-level micro sites remain outside this count.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with facility operations chiefs, storage OEM channel heads, and cloud architects across Manila, Clark, Cebu, and Davao to verify utilization ratios, price dispersion, and flash penetration. Short web surveys with enterprise IT buyers fill any residual gaps on workload mix and refresh cycles.

Desk Research

We start by mapping the addressable pool through Department of Information and Communications Technology capacity bulletins, Bangko Sentral digital-economy reports, National Grid power statistics, and Asia Cloud Computing Association briefs. Volza shipment logs and Bureau of Customs codes reveal import volumes for disk drives and flash arrays, while Questel patent trends signal adoption of NVMe-over-Fabrics. Our analysts mine annual reports, investor decks, and Dow Jones Factiva news, then check vendor health in D&B Hoovers, ensuring the picture is current. These examples are illustrative; many other sources support collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down model anchors on installed IT-load megawatts, average storage density per rack, and import invoice values, which are then cross-checked through selective bottom-up supplier shipment roll-ups. Key variables like hyperscale build pipeline, SSD pricing, data-localization statutes, GDP-linked digital traffic, and 5G subscriber growth feed a multivariate regression that projects demand to 2030. Where shipment splits are missing, weighted regional benchmarks are tuned using local primary insight.

Data Validation & Update Cycle

Outputs pass automated anomaly flags, peer review, and lead-analyst sign-off. Figures refresh each year, with interim updates when events such as a >10 MW facility go live. A final sweep is run just before release.

Why Mordor's Philippines Data Center Storage Baseline Commands Confidence

Published estimates often diverge because firms disagree on what counts as storage spend and how fast flash displaces spinning media. Our disciplined scope and annual refresh keep us centered, whereas some publishers rely on one-off surveys or bundled infrastructure buckets.

Key gap drivers include inclusion of servers and networking gear, use of construction-investment proxies, or a focus purely on service revenue.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.68 B (2025) | Mordor Intelligence | |

| USD 0.63 B (2024) | Regional Consultancy A | Bundles all IT infrastructure, not storage alone |

| USD 4.73 B (2024) | Trade Journal B | Adds facilities, power, and real-estate spend |

| USD 0.15 B (2024) | Global Consultancy A | Captures only colocation service revenue |

The comparison shows our balanced, transparent baseline sits between narrow service-only views and broad infrastructure totals, giving decision-makers a dependable figure that traces back to clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the Philippines data center storage market in 2026?

The market stands at USD 0.75 billion in 2026 and is forecast to reach USD 1.22 billion by 2031, reflecting a 10.18% CAGR.

Which storage technology is growing fastest?

Object and Tape Storage leads growth with a 12.02% CAGR as unstructured data from AI, streaming, and IoT applications accelerates.

Why are hyperscalers investing heavily in the Philippines?

Data-localization rules, DICT incentives, and new submarine cables reduce latency and create favorable conditions for regional cloud nodes.

What is the main challenge faced by local enterprises adopting flash storage?

High upfront capex remains the biggest hurdle, though subscription-based Storage-as-a-Service models are easing this barrier.

Page last updated on: