Philippines Data Center Physical Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

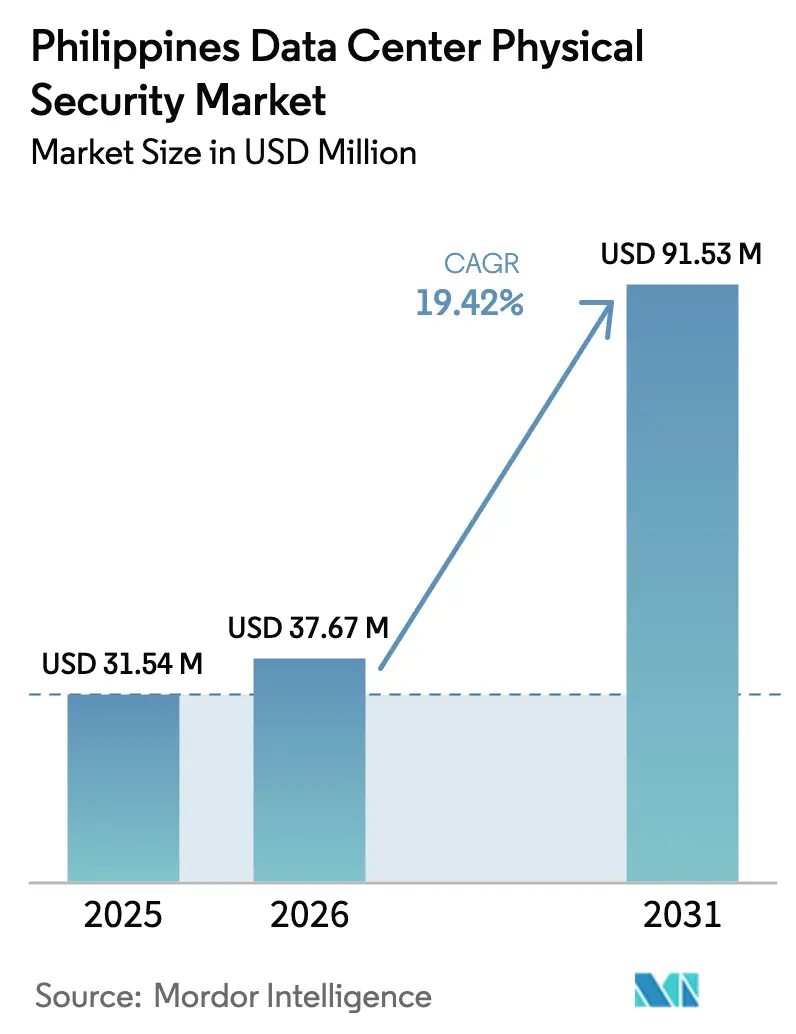

| Base Year Market Size (2025) | USD 31.54 Million |

| Market Size (2026) | USD 37.67 Million |

| Market Size (2031) | USD 91.53 Million |

| Growth Rate (2026 - 2031) | 19.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Data Center Physical Security Market Analysis by Mordor Intelligence

The Philippines data center physical security market size is expected to grow from USD 31.54 million in 2025 to USD 37.67 million in 2026 and is forecast to reach USD 91.53 million by 2031 at 19.42% CAGR over 2026-2031. Rapid hyperscale construction, stricter national cybersecurity mandates, and rising AI workloads are collectively amplifying demand for multilayered perimeters, access controls, and environmental safeguards. Strong capital inflows—over USD 18 billion earmarked for 1 gigawatt of capacity by 2029—directly translate into higher spending on cameras, biometrics, and intrusion-detection technologies. Operators view advanced physical security as a business enabler that lowers cyber-insurance premiums, supports international compliance audits, and sharpens competitive positioning when courting cloud and fintech tenants. Global suppliers such as Honeywell, Johnson Controls, and Schneider Electric are expanding local project teams, while specialist integrators offer modular, AI-powered analytics to offset the national skills gap.

Key Report Takeaways

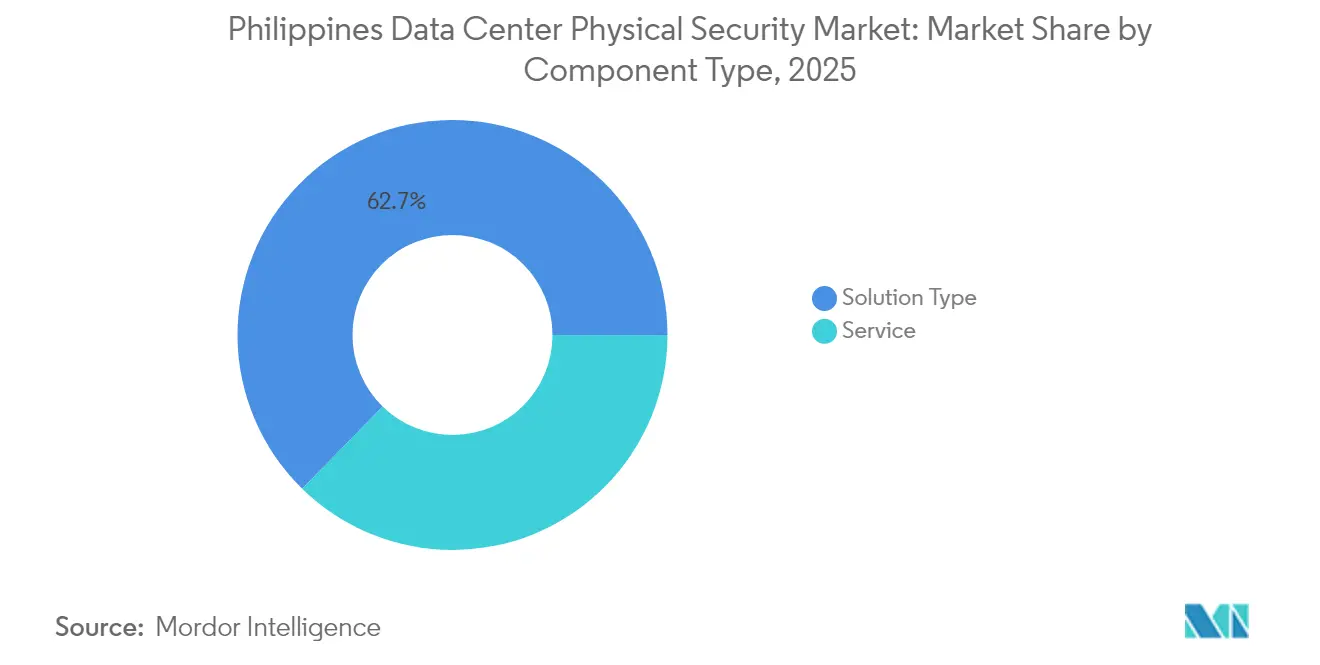

- By component, Solution Type held 62.68% of the Philippines data center physical security market share in 2025, whereas Service revenues are projected to expand at a 21.63% CAGR to 2031 STT GDC.

- By tier classification, Tier III facilities commanded 56.74% share of the Philippines data center physical security market size in 2025; Tier IV is poised for the fastest 20.96% CAGR through 2031 EPI Certification.

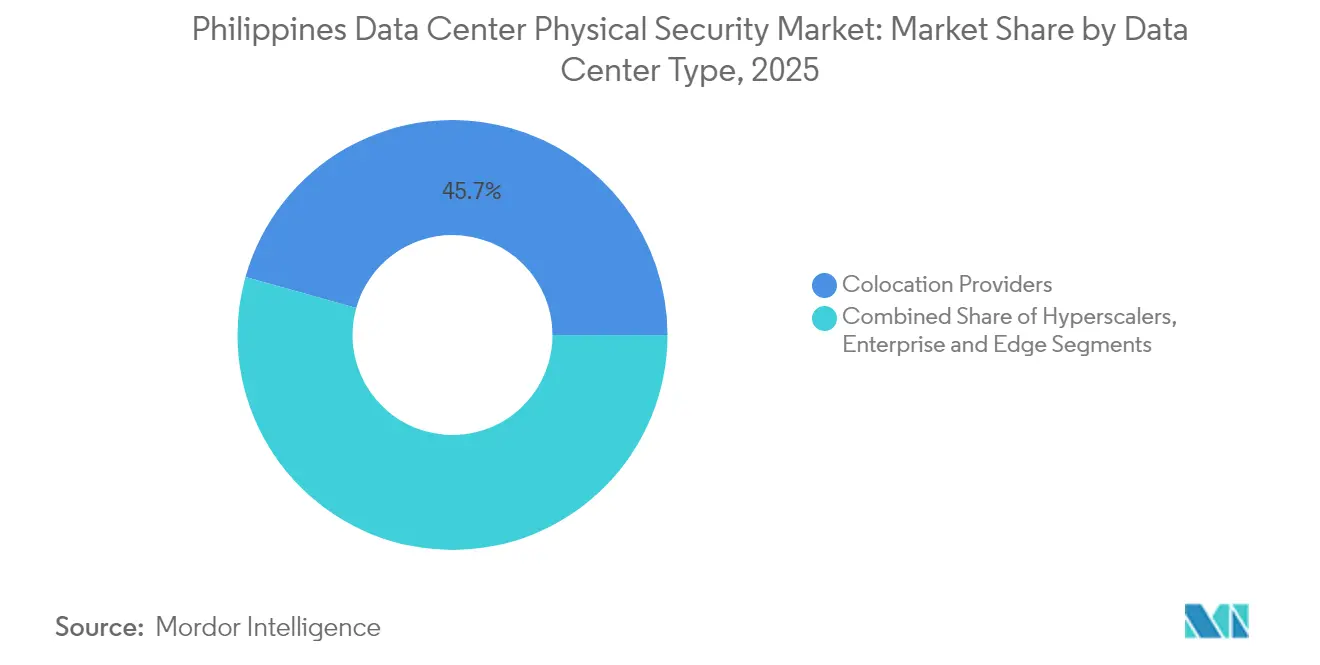

- By data center type, Colocation providers led with 45.65% revenue share in 2025, while the hyperscaler/cloud segment is forecast to rise at a 22.58% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The data center physical security market size of Mordor Intelligence integrates these into one global valuation.

Philippines Data Center Physical Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale and colocation build-outs across Luzon | 6.2% | Luzon region, with spillover to Visayas and Mindanao | Medium term (2-4 years) |

| Escalating cyber-crime driving multilayer security mandates | 4.8% | National, with concentration in Metro Manila | Short term (≤ 2 years) |

| Stricter compliance (Data Privacy Act 2012, NCSP 2023-28) | 3.9% | National, with early enforcement in financial and telecom sectors | Medium term (2-4 years) |

| AI-ready facilities require higher CCTV density and analytics | 2.7% | Metro Manila, Clark, and emerging hyperscale zones | Long term (≥ 4 years) |

| Insurance premium discounts for certified security designs | 1.8% | National, with higher adoption in Tier III-IV facilities | Medium term (2-4 years) |

| ESG-linked finance favouring low-power security hardware | 1.4% | National, driven by international financing requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in hyperscale and colocation build-outs across Luzon

A cluster of large projects in Luzon is redefining design baselines. STT GDC’s 124 MW Fairview campus became operational in Q2 2025 with 8-layer fencing, mantraps, AI-enabled video analytics, and redundant guardhouses that exceed TIA-942 Rated-3 norms.[1]STT GDC, “STT GDC Fairview Campus Launch Announcement,” sttelemedia-globaldata.com ENDECGROUP’s USD 2.7 billion, 300 MW hyperscale estate in Tarlac allocates more than 15% of its capital budget to physical protection infrastructure, illustrating how scale magnifies security line-items. The density of builds around Metro Manila and Clark allows operators to share threat-intelligence feeds, leverage joint response teams, and negotiate better insurance terms, cutting unit security expenditure by 8-10% without diluting safeguards. PLDT’s USD 29 million Clark build and Digital Halo’s USD 400 million regional platform further validate investor confidence in the corridor’s security ecosystem

Escalating cyber-crime driving multilayer security mandates

The Philippines ranked fourth globally for web threats in 2024, prompting regulators to impose end-to-end physical-cyber frameworks under the National Cybersecurity Plan 2023-2028 Philippine News Agency.[2]Philippine News Agency, “National Cybersecurity Plan 2023-2028 signed,” pna.gov.phEighty-five percent of firms now acknowledge potential operational disruptions from cyberattacks, spurring adoption of biometric portals, AI-driven video alarms, and compartmentalized zoning that isolates suspicious activity within seconds. Beeinfotech PH’s 3,600-rack HIVE facility, launched March 2025, integrates iris scanners and predictive surveillance that automate incident triage, addressing the 71% talent shortage in cybersecurity roles. Insurers have responded by linking premium rebates to third-party certification, generating a 23% annual rise in policy pricing for facilities lacking documented multilayer controls

Stricter compliance requirements under Data Privacy Act and NCSP 2023-28

Enhanced enforcement since January 2023 obliges every registered Personal Information Controller to install “reasonable organizational, physical, and technical security measures,” making TIA-942 or ISO 27001 audits prerequisites for many enterprise contracts. Digital Edge’s NARRA1 and ePLDT’s VITRO Sta. Rosa both secured ANSI/TIA-942-C Rated-3 attestations in 2024, showcasing biometric vaults, segmented corridors, and real-time environmental analytics that meet national audit checklist. The Department of Information and Communications Technology coordinates annual self-assessments, shrinking gaps between metropolitan and secondary-city facilities while lifting the overall floor on acceptable safeguards.

AI-ready facilities require higher CCTV density and analytics

AI racks increase power and heat loads, creating new failure modes that physical security teams must monitor. CCTV point counts in AI-enabled halls are up 40–60% over legacy rooms, often combining visual, thermal, and LiDAR feeds. STT GDC deploys real-time behavior analytics that cut false alerts by 90% and trigger automatic lockdowns in abnormal situations. Converge ICT’s forthcoming Metro Manila and Pampanga sites employ liquid cooling, necessitating additional leak-detection sensors that integrate with video dashboards for unified alerting.[3]InsiderPH, “Converge ICT unveils liquid-cooling data centers,” insiderph.com Cisco’s Hypershield architecture, adopted by early Philippine hyperscalers in 2025, embeds exploit mitigation logic into the network fabric, allowing physical controls to synchronize with micro-segmentation policies

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited IT budgets at legacy enterprise sites | -3.2% | National, concentrated in SME and traditional enterprise segments | Short term (≤ 2 years) |

| Availability of low-cost, non-certified substitutes | -2.8% | National, with higher penetration in cost-sensitive segments | Medium term (2-4 years) |

| High CAPEX of Tier III-IV physical security compliance | -2.1% | Metro Manila and major urban centers | Medium term (2-4 years) |

| Shortage of skilled security-system integrators | -1.9% | National, with acute shortages in specialized AI and biometric systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited IT budgets at legacy enterprise sites

Many SME-operated data rooms run on basic locks and standalone DVRs despite the Philippines’ high cyber-risk profile. Upgrading to Tier III compliance costs USD 7-12 million per megawatt, equal to 15–20% of build budgets, placing modern CCTV, biometrics, and fire suppression beyond reach for cash-constrained operators. Managed Security Service Providers are filling the gap with subscription-based monitoring, yet integration complexity and recurring fees have slowed conversion outside Metro Manila.

Shortage of skilled security-system integrators

A 2.1 million-person cybersecurity talent gap across Southeast Asia is most acute in biometric enrollment, AI video analytics, and converged OT-IT monitoring. Seventy-one percent of Philippine firms report hiring challenges, pushing wages upward and elongating deployment timelines Business Inquirer. Global vendors now host local academies, but project teams still import niche expertise for iris recognition or liquid-cooling camera alignments, adding cost premiums that restrain aggressive roll-outs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Market Foundation

Solutions captured 62.68% of 2025 spending as operators rushed to install cameras, biometric gates, and sensor-rich perimeter arrays. Video surveillance dominates, buoyed by AI-ready builds that require analytics-capable edge cameras enabling real-time object detection and anomaly spotting. Access control is the fastest-rising sub-segment, with iris and multi-factor biometrics standardizing across Tier III-IV estates. Perimeter barriers, fiber fences, and active infrared grids protect sprawling hyperscale grounds, while next-generation fire and environmental systems guard against hot-aisle flashovers linked to high-density AI racks. The Philippines data center physical security market size for Service-based offerings is set to expand at 21.63% CAGR, as integrators, managed-service units, and audit consultants monetize skills that offset local talent shortages, reduce downtimes, and align facilities with Data Privacy Act compliance checks.

Services growth is strongest in integration and deployment, which account for multi-month builds that combine CCTV orchestration, network segmentation, and SOC-as-a-service. Managed services appeal to colocation customers that cannot justify on-premise security staff. Consulting remains niche but high-margin, guiding clients through ANSI/TIA-942 and ISO 27001 evidence gathering. As hyperscale expansions accelerate, out-tasking of preventive maintenance for cameras, biometric scanners, and smart PDUs is rising, supporting recurring revenue streams that stabilise the Philippines data center physical security industry amid discrete project cycles.

By Data-center Tier: Tier III Dominance with Tier IV Acceleration

Tier III facilities held 56.74% of the Philippines data center physical security market size in 2025. Carrier-neutral colocation halls plus fintech and telecom cloud zones view Tier III’s 99.982% uptime and fault-tolerant power paths as cost-optimal. Physical safeguards include redundant biometric portals, dual-feed camera networks, and SOC suites with hot-standby power. Digital Edge’s NARRA1 exemplifies this architecture, offering enterprise tenants compartmentalised racks guarded by continuous facial-recognition patrols.

Tier IV footprints are expanding at a 20.96% CAGR as regional hyperscalers and critical banking workloads demand 2N+1 redundancy and no single points of failure. Military-grade perimeter fences, multi-credential gates, and distributed camera clusters ensure uninterrupted security even during maintenance windows. Emerging edge and Tier II micro-sites fill latency niches but face mounting pressure to elevate controls as NCSP enforcement extends to provincial cities.

By Data Center Type: Colocation Leadership with Hyperscaler Momentum

Colocation providers retained 45.65% share in 2025 by pooling premium security across diverse tenants. Shared investments justify AI analytics engines, SOC dashboards, and integrated visitor management. STT GDC and Digital Edge attract SMEs needing Tier III protections without capex burden. Policies enforce tenant segregation via biometric-controlled cages and per-suite CCTV, supporting compliance for fintech and healthcare users.

Hyperscaler/cloud campuses, though smaller in count, are the fastest-growing at 22.58% CAGR through 2031. Vast land parcels allow concentric security rings with armed patrols and anti-ram barriers. ENDECGROUP’s 300 MW Tarlac estate implements drone surveillance and AI-triggered flood-lighting that activates on suspicious perimeter activity. Enterprise and edge facilities grow steadily, but many adopt cloud-native security dashboards inspired by hyperscale playbooks to stay relevant.

Geography Analysis

Luzon dominates deployment with Metro Manila hosting the densest concentration of large campuses, proximity to submarine cables, and the highest pool of security technicians. STT GDC’s Fairview hub and PLDT’s VITRO series have raised the bar for integrated SOCs, layered biometrics, and AI-based perimeter analytics. The Clark Special Economic Zone is an emerging cluster offering cost incentives, robust grid redundancy, and government support that collectively lower TCO for advanced security roll-outs.

Visayas and Mindanao are early-stage markets where government broadband projects and the National Fiber Backbone spur edge builds. As secondary cities gain fibre, regional financial institutions and BPO operators require micro-data centers that meet baseline NCSP controls. Limited local integrator capacity and higher logistics costs mean most installations source pre-fabricated surveillance pods and remote monitoring, delaying parity with Luzon but securing a multiyear growth runway.

International connectivity boosts the archipelago’s appeal to foreign investors seeking diversification within ASEAN. Alignment with ISO 27001 and PCI-DSS eases cross-border data flow, while geographic fragmentation across 7,641 islands provides natural disaster-recovery dispersion for regional cloud nodes. Digital Halo’s USD 400 million platform illustrates rising cross-border capital eager to leverage Philippine tax holidays and English-speaking technical labour, provided that security designs pass both domestic and overseas audits

Mordor Intelligence tracks the global data center physical security market across other major regions such as Africa, South America, and Europe, with additional country-level coverage spanning Japan, New Zealand, South Africa, Brazil, Germany, and South Korea, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Philippines data center physical security market features moderate fragmentation with growing consolidation as global majors extend local footprints. Honeywell integrates Pro-Watch access control with AI cameras tailored for hot and humid environments. Johnson Controls promotes its C-CURE platform alongside aspirating smoke detection that protects dense GPU racks. Schneider Electric’s EcoStruxure solution marries smart breakers with central dashboards, cutting incident response times for power-related alarms Manila Standard.

Specialist integrators differentiate through AI analytics or green hardware. Start-ups deploy solar-powered CCTV towers and battery-less sensor grids that align with ESG-linked financing metrics, while cloud-native SOC providers deliver dashboards that unify physical and network events. Patent filings on iris-facial fusion identification demonstrate the innovation drive to reduce false rejects and expedite high-volume personnel throughput Patents Encyclopedia. A scarcity of in-country experts encourages joint ventures—multinationals fund local academies while smaller players form consortiums to win Tier IV bids.

Philippines Data Center Physical Security Industry Leaders

Axis Communications AB

ABB Ltd

Bosch Sicherheitssysteme GmbH

Honeywell International Inc.

Johnson Controls.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: STT GDC Philippines opened a next-generation data hall in Makati City with 5 MW IT load and eight-layer physical protection.

- May 2025: ARCH Capital and Partners Group injected USD 400 million into Digital Halo to develop 500 MW regional capacity.

- May 2025: Meralco Energy won the electrical package for STT GDC Fairview, installing high-voltage GIS that powers redundant security systems .

- April 2025: PLDT launched the Sta. Rosa VITRO data center, featuring AI-assisted surveillance and biometric dual-factor portals

Philippines Data Center Physical Security Market Report Scope

The data center physical security market refers to the industry focused on providing products and services to safeguard the physical infrastructure and assets of data centers. This includes measures to protect data centers from unauthorized access to premises, hardware theft, vandalism, sabotage, terrorist acts, and other physical threats. Key components of data center physical security may include video surveillance and monitoring, access control systems, physical barriers, biometric authentication, and environmental controls designed to ensure the safety and integrity of the data center environment.

The Philippine data center physical security market is segmented by solution type, service type, and end-user industry. By type, the market is segmented into video surveillance and access control solutions. By service type, the market is segmented into consulting services and professional services. By end-user industry, the market is segmented into IT & telecommunication, BFSI, government, media & entertainment, and other end users. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Solution Type | Video Surveillance |

| Access Control | |

| Perimeter Security (Mantraps, Fences, Bollards) | |

| Intrusion Detection and Monitoring | |

| Environmental and Fire Safety Systems | |

| By Service Type | Consulting |

| Integration and Deployment | |

| Maintenance and Managed Services |

| Tier I and II |

| Tier III |

| Tier IV |

| Hyperscaler/Cloud Service Providers |

| Colocation Providers |

| Enterprise and Edge Data Center |

| By Component | By Solution Type | Video Surveillance |

| Access Control | ||

| Perimeter Security (Mantraps, Fences, Bollards) | ||

| Intrusion Detection and Monitoring | ||

| Environmental and Fire Safety Systems | ||

| By Service Type | Consulting | |

| Integration and Deployment | ||

| Maintenance and Managed Services | ||

| By Data-center Tier | Tier I and II | |

| Tier III | ||

| Tier IV | ||

| By Data Center Type | Hyperscaler/Cloud Service Providers | |

| Colocation Providers | ||

| Enterprise and Edge Data Center | ||

Key Questions Answered in the Report

How big is the Philippines Data Center Physical Security Market?

The Philippines Data Center Physical Security Market size is expected to reach USD 37.67 million in 2026 and grow at a CAGR of 19.42% to reach USD 91.53 million by 2031.

What is the current Philippines Data Center Physical Security Market size?

In 2026, the Philippines Data Center Physical Security Market size is expected to reach USD 37.67 million.

Who are the key players in Philippines Data Center Physical Security Market?

Axis Communications AB, ABB Ltd, Bosch Sicherheitssysteme GmbH, Honeywell International Inc. and Johnson Controls. are the major companies operating in the Philippines Data Center Physical Security Market.

What years does this Philippines Data Center Physical Security Market cover, and what was the market size in 2025?

In 2025, the Philippines Data Center Physical Security Market size was estimated at USD 37.67 million. The report covers the Philippines Data Center Physical Security Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Philippines Data Center Physical Security Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: