Indonesia Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

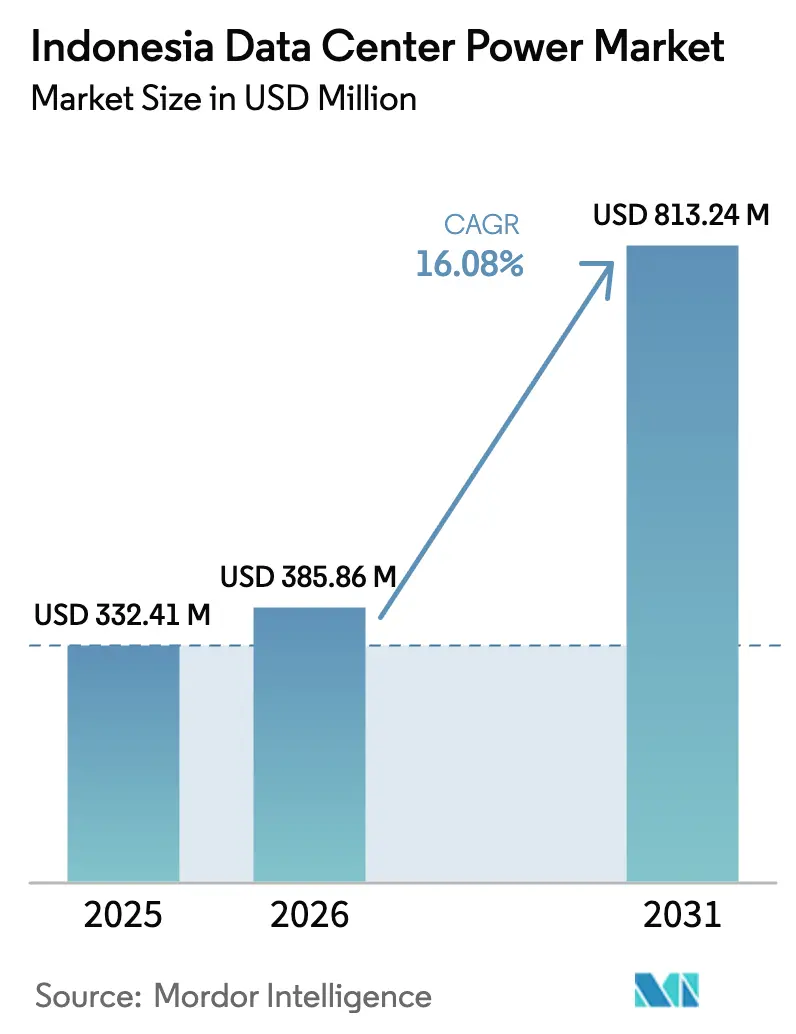

| Base Year Market Size (2025) | USD 332.41 Million |

| Market Size (2026) | USD 385.86 Million |

| Market Size (2031) | USD 813.24 Million |

| Growth Rate (2026 - 2031) | 16.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Data Center Power Market Analysis by Mordor Intelligence

The Indonesia data center power market size was valued at USD 332.41 million in 2025 and estimated to grow from USD 385.86 million in 2026 to reach USD 813.24 million by 2031, at a CAGR of 16.08% during the forecast period (2026-2031). Capacity additions led by hyperscale and colocation operators, a strengthening policy push for data sovereignty, and aggressive renewable-energy build-outs are combining to create one of the most dynamic power-infrastructure opportunities in Southeast Asia. Rapid deployment of 20-30 MW halls, a nationwide shift toward lower power-usage effectiveness (PUE), and new electricity procurements tied to sustainability metrics have already begun to reshape vendor strategies around high-efficiency uninterruptible power supplies (UPS), intelligent power distribution units (PDU), and next-generation backup systems. Operators capable of pairing modular designs with guaranteed renewable power now enjoy a clear competitive edge, especially in Java, Batam, and other coastal landing points where submarine-cable connectivity and grid headroom align. Lingering execution risks remain in the form of grid-stability gaps outside Java-Bali and the high upfront outlays demanded by Tier IV redundancy levels, yet the overall direction of spending remains decidedly expansionary.

Key Report Takeaways

- By component, UPS Systems accounted for 28.12% of the Indonesia data center power market share in 2025, while Power Distribution Units are projected to post the fastest 17.85% CAGR to 2031

- By data center type, colocation providers led with 52.63% revenue share in 2025; hyperscale/cloud service providers are expected to expand at a 19.02% CAGR through 2031

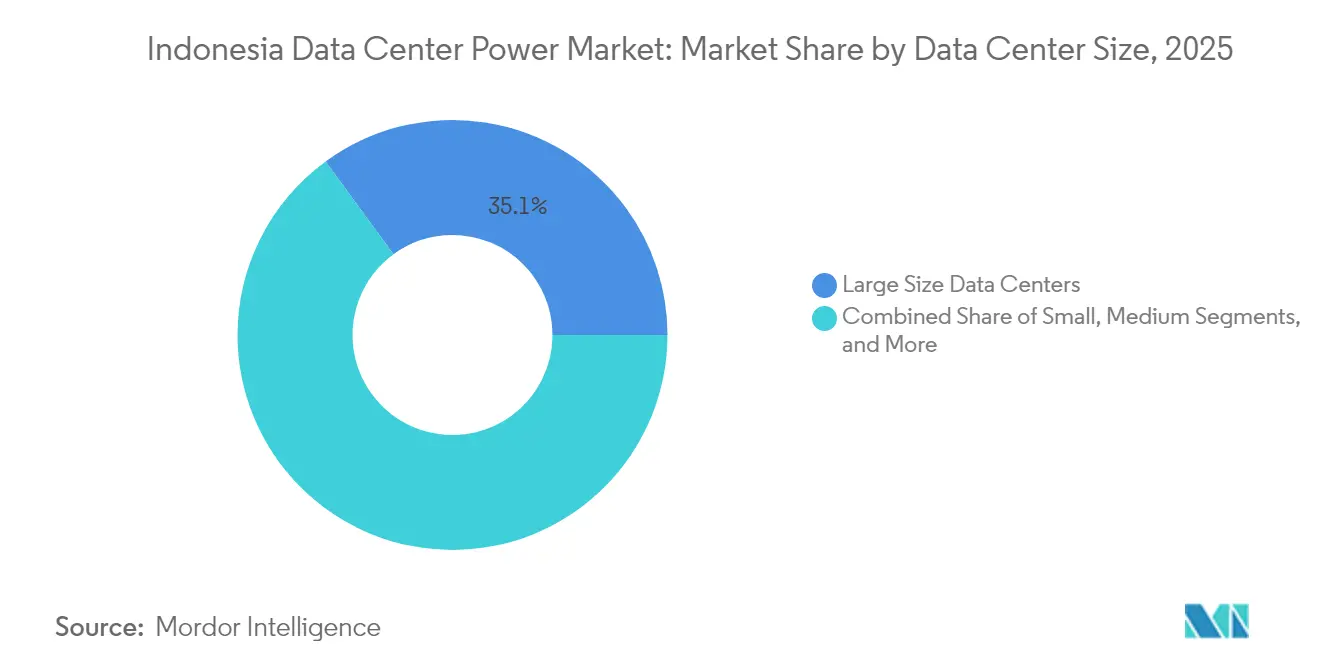

- By data center size, large facilities held 35.05% of the Indonesia data center power market size in 2025; mega facilities are forecast to grow at a 19.34% CAGR between 2026-2031

- By tier level, Tier III facilities commanded 49.88% of the market in 2025, while Tier IV deployments are set to accelerate at a 17.15% CAGR

- ABB, Schneider Electric, and Vertiv together served over 31.95% of installed UPS and PDU capacity in 2025, reflecting a moderate concentration pattern

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of hyperscale and cloud facilities | +4.2% | Java-Bali corridor, expanding to Batam and Surabaya | Medium term (2-4 years) |

| Government push for data-sovereignty regulations | +3.8% | National, with enforcement focus in Jakarta and major cities | Short term (≤ 2 years) |

| Need to lower PUE and power OPEX through efficient designs | +2.1% | National, with early adoption in Tier III+ facilities | Long term (≥ 4 years) |

| PLN "Green-Energy-as-a-Service" PPAs for DCs | +1.9% | National, prioritizing Java-Bali grid integration | Medium term (2-4 years) |

| New submarine-cable landings raising resiliency demand | +1.4% | Coastal regions, particularly Batam and Jakarta | Medium term (2-4 years) |

| AI/ML racks driving high-density battery upgrades | +2.1% | Major metropolitan areas with hyperscale presence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Hyperscale and Cloud Facilities

Hyperscale operators have set a radically higher baseline for capacity and density. Tencent’s USD 500 million multi-phase build, BDx’s 500 MW renewable-powered campus, and EdgeConneX’s 120 MW Jakarta project financed through a sustainability-linked loan all illustrate how individual campuses are now specified at 20-30 MW per hall rather than the earlier 5-10 MW format.[1]Data Center Dynamics Staff, “BDx Launches Renewable-Powered 500 MW AI Campus,” datacenterdynamics.com Larger footprints require sophisticated ring-bus switchgear, 2N UPS arrays, and high-voltage intake substations sized beyond 150 MVA, creating immediate pull-through demand for modular power trains, busway PDUs, and lithium-ion battery strings. Investment continues to concentrate in Java-Bali but is beginning to spill over to Batam as operators seek lower natural disaster risk and direct submarine-cable access

Government Push for Data-Sovereignty Regulations

Government Regulation No. 82 and successor decrees mandate in-country storage for strategic data, prompting global cloud incumbents to acquire land, secure long-term power purchase agreements (PPA), and commit to stringent uptime and security standards.[2]Digiserve Editorial Team, “Understanding GR 82/2012 on Electronic Systems Data Localization,” digiserve.co.id Four national data centers of up to 40 MW each are scheduled for commissioning by 2026, signalling direct public-sector demand for highly redundant electrical systems.[3]South China Morning Post, “Indonesia to Build Four State-Owned National Data Centers,” scmp.com PLN’s obligation to guarantee reliable, clean power for these facilities accelerates procurement of grid-interactive UPS and intelligent switchgear, while also creating additional incentives to co-locate with renewable-generation clusters.

Need to Lower PUE and Power OPEX Through Efficient Designs

Energy-efficiency targets have shifted from nice-to-have to board-level mandates. EDGE DC’s achievement of 100% Renewable Energy Certificates and its installation of StatePoint liquid cooling lowered PUE to sub-1.3 levels, proving that cutting OPEX can justify premium capex on higher-efficiency rectifiers and variable-speed drives. Delta Electronics’ air-assisted liquid cooling shelves delivering 2.5× traditional density demonstrate the direct link between thermal innovation and power-system design. Vendors that can guarantee measurable PUE gains while maintaining Tier III/IV redundancies now command pricing power in the Indonesia data center power market.

PLN “Green-Energy-as-a-Service” PPAs for DCs

PLN’s 8,786 MW renewable portfolio and launch of 21 green-hydrogen plants position the utility to offer bundled clean electricity, certificates, and potentially hydrogen backup solutions under multi-year contracts. Star Energy Geothermal’s planned 102.6 MW capacity illustrates the breadth of zero-carbon sources that data center operators can now tap. Designs must therefore accommodate variable renewable feeds, prompt tighter integration between UPS inverters and micro-grid controllers, and create a new aftermarket for energy-storage systems and fuel-cell gensets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for power infrastructure | -2.8% | National, particularly affecting smaller operators | Short term (≤ 2 years) |

| Grid-stability issues outside Jawa-Bali | -2.1% | Eastern Indonesia, Sumatra, Sulawesi | Medium term (2-4 years) |

| Volatile LNG prices limiting gas-gen adoption | -1.6% | Areas with limited pipeline gas access | Medium term (2-4 years) |

| Delay in RE policy execution and certificate supply | -1.3% | National renewable energy development zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Power Infrastructure

Expanding a hyperscale campus can demand USD 200-300 million in switchgear, UPS, and backup assets before a single server is racked. PT DCI’s recent campus expansion exemplifies the steep outlay curve, while Rolls-Royce Power Systems’ 2024 revenue surge underscores how premium redundancy commands higher prices. Sustainability-linked loans offer relief but only to operators able to evidence carbon-reduction pathways, effectively raising the bar for new entrants.

Grid-Stability Issues Outside Java-Bali

Outside the primary corridor, end-user surveys record outage frequencies 2.6-3.9× higher than utility reports, forcing operators to overspec reserve power and invest in extended-runtime gensets. Remote hubs such as Jayapura or Kupang still lack high-capacity interconnects, making battery-energy-storage systems and micro-grids essential but costly, a constraint that suppresses deployment pace in these regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Lead While PDUs Accelerate

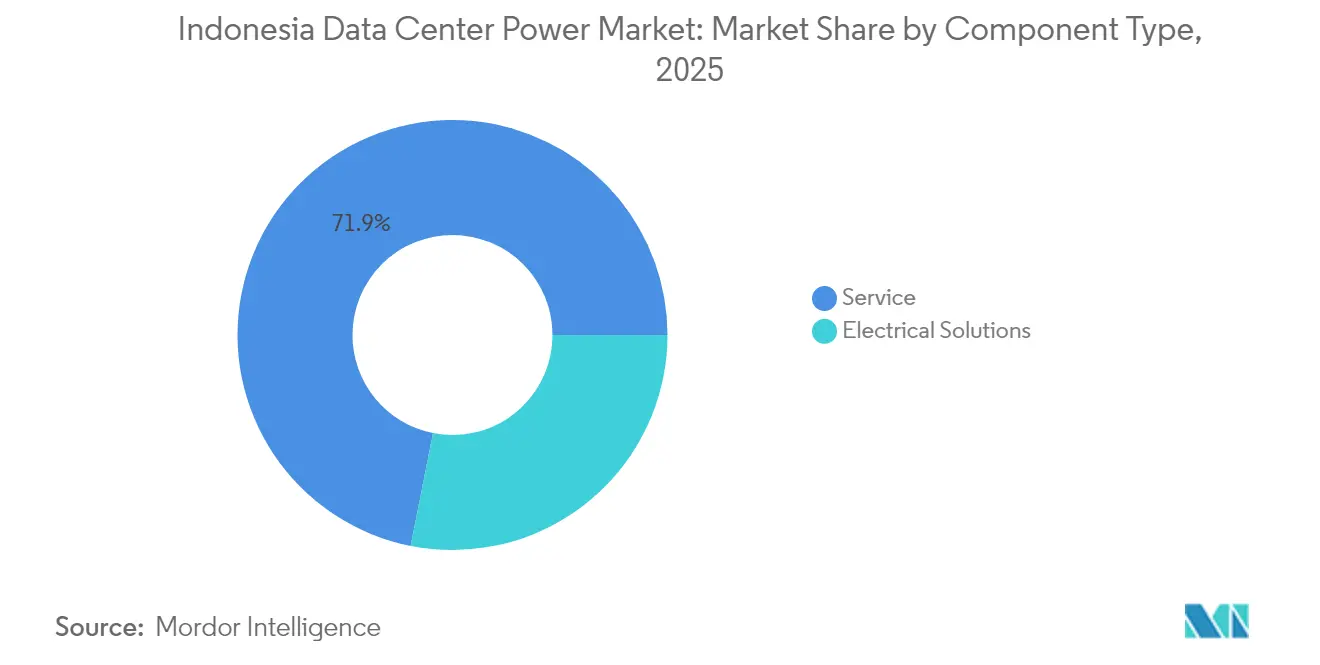

UPS Systems captured 28.12% of the Indonesia data center power market share in 2025 thanks to chronic grid volatility and the need for seamless fail-over. Lithium-ion adoption is rising rapidly, aided by declining cell prices and better thermal profiles. Power Distribution Units, though smaller in value today, are posting the fastest 17.85% CAGR as hyperscale users demand outlet-level metering and AI-driven load orchestration. The Indonesia data center power market size for PDUs is projected to exceed USD 208.6 million by 2031, growing in tandem with high-density rack deployments. Generator sets remain vital outside Java-Bali, but cleaner gas and emerging hydrogen fuels are already displacing diesel in new Tier IV blueprints. Energy-storage systems are evolving from short-duration UPS banks to multi-hour battery arrays supporting renewable integration, reflecting the country’s broader decarbonization agenda.

The service layer—installation, commissioning, and long-term maintenance—accounts for a rising share of total outlay as configurations grow more complex. Socomec’s DELPHYS XM launch demonstrates the pivot toward compact, high-power modules optimized for 2N architectures, reinforcing the premium placed on space-efficient redundancy

By Data Center Type: Colocation Dominance Faces Hyperscale Challenge

Colocation providers held 52.63% revenue share in 2025, benefiting from enterprises wishing to avoid capex and from multi-tenant architectures that squeeze more utilization out of each kW. Yet hyperscale/cloud service providers are on track for 19.02% CAGR, driven by AI and big-data workloads that justify dedicated campuses. The Indonesia data center power market size attached to hyperscale demand is expected to reach USD 583.7 million by 2031. EDGE2’s 23 MW renewable-powered hall in Jakarta typifies the specification leap: low-latency, high-density, and 100% green power. Enterprise and edge sites remain relevant for jurisdictional compliance and latency-sensitive applications, especially in secondary cities where broadband penetration is rising.

By Data Center Size: Mega Facilities Drive Infrastructure Evolution

Large data centers (10-40 MW) made up 35.05% of 2025 spend, delivering balanced economics for mixed enterprise and cloud demand. The mega category (>50 MW) is, however, expanding at a 19.34% CAGR toward 2031 as AI training clusters and regional cloud nodes co-locate in consolidated campuses. The Nongsa Digital Park’s planned 221 MW capacity illustrates how the Indonesia data center power market is pivoting to campus-scale builds that exploit economies of scale in substation interconnection and cooling. Prefabricated modules from suppliers such as Delta now allow incremental blocks of 1.7 MW to be deployed in 40-foot containers, reducing build time and de-risking capital staging

By Tier Level: Tier III Stability Meets Tier IV Innovation

Tier III still commands 49.88% share because it balances 99.982% uptime with manageable redundancy cost. Operators eyeing AI workloads, financial trading, or public-sector mandates are migrating to Tier IV, which is growing 17.15% annually. The Indonesia data center power market size for Tier IV halls is projected to top USD 301.2 million by 2031, driven by twin-path power architecture and fault-tolerant switchgear. Rolls-Royce mtu kinetic-power systems that provide dynamic UPS without batteries are finding early adopters among Tier IV builders needing ultra-clean power while shrinking floor space

Geography Analysis

Java-Bali remains the beating heart of the Indonesia data center power market. PLN data show 65.29% of the country’s 45,095.19 MW installed capacity located here, underpinning the bulk of hyperscale and colocation builds. Jakarta alone hosts more than 70% of current live racks, helped by its intersection of terrestrial fiber, multiple submarine cables, and a large enterprise client base. Batam has emerged as the secondary hot-spot: NeutraDC’s planned 51 MW campus and the 221 MW Nongsa Digital Park attest to its appeal as a low-seismic, Singapore-adjacent site with lower land cost and improving grid links.

Surabaya, Bandung, and Pekanbaru illustrate the nascent edge trend. Princeton Digital Group’s expansion into these cities proves that enterprise demand and government digital-service rollouts will push capacity outside Java-Bali in the coming years. Still, grid stability lags; operators often specify extended-autonomy UPS and on-site generation to offset local outage patterns. Eastern islands such as Sulawesi and Papua remain longer-term prospects, constrained by limited transmission infrastructure but rich in untapped renewable resources that could support micro-grid-centric data centers.

Renewable potential increasingly dictates siting decisions. Star Energy’s geothermal assets in West Java and Lampung and PLN’s green hydrogen pilots provide low-carbon electricity options that can help operators hit net-zero commitments without purchasing off-shore certificates. Regions able to combine such resources with dark-fiber availability and seismic stability are likely to attract the next wave of investment, broadening the geographic footprint of the Indonesia data center power market beyond its traditional core.

Competitive Landscape

The Indonesia data center power market is moderately concentrated. ABB, Schneider Electric, Vertiv, and Eaton supply a combined 32% of primary UPS, switchgear, and PDU shipments, leveraging global manufacturing scale and extensive service ecosystems. These incumbents routinely bundle design consultancy, remote monitoring, and lifecycle spares, erecting barriers for smaller entrants. Delta Electronics has carved share through modular, AI-optimized power shelves, while Rolls-Royce’s acquisition of Kinolt has reinforced its presence in dynamic UPS and gas gensets, segments where local competitors lack comparable reference sites.

Sustainability is now the critical differentiator. Vendors able to document measurable PUE reductions and embed renewable-readiness into product roadmaps secure preferred-supplier status for hyperscale RFPs. Schneider Electric’s EcoStruxure platform and Vertiv’s Trellis suite demonstrate how integrated software can optimize power-distribution efficiency, providing data that investors increasingly demand in environmental, social, and governance (ESG) audits. Local assemblers have responded by partnering with international brands for technology transfer, particularly around lithium-ion battery packs and intelligent breaker systems.

Innovation focus has shifted to hydrogen and long-duration storage. Rolls-Royce, Cummins, and Caterpillar have each launched pilot hydrogen-ready gensets, anticipating Indonesia’s green-hydrogen ramp-up. Smaller niche firms are targeting edge-specific micro-grid controllers that integrate solar and battery storage into a plug-and-play skid. Overall, competitive intensity is rising, but incumbents retain leverage through installed base, brand trust, and maintenance footprints that newcomers struggle to replicate.

Indonesia Data Center Power Industry Leaders

Schneider Electric SE

Vertiv Group Corp.

ABB Ltd

Eaton Corporation plc

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: PT PLN inaugurated 21 Green Hydrogen Plants across Indonesia, adding 199 tons of annual production capacity and opening a potential pathway for hydrogen backup in data centers.

- January 2025: President Prabowo Subianto opened 37 electricity projects totaling 3,222.75 MW, with Rp 72 trillion invested in renewables and transmission, directly benefiting future data-center siting.

- January 2025: PT PLN recorded a 500% spike in electricity sold to EV-charging stations over the holiday period, underlining grid elasticity for large incremental loads.

- December 2024: DCI Indonesia topped out a new Jakarta campus, extending capacity to keep pace with hyperscale demand and deploying next-gen liquid cooling.

- November 2024: Tencent earmarked USD 500 million for Indonesian data-center expansion, confirming sustained hyperscale appetite for local capacity.

- October 2025: Tencent earmarked USD 500 million for Indonesian data-center expansion, confirming sustained hyperscale appetite for local capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define Indonesia's data center power market as the annual value generated inside the country from electricity distribution and backup systems, namely UPS units, PDUs, generators (diesel, gas, and hydrogen fuel cell), switchgear, transfer switches, remote power panels, and on-site energy storage solutions that keep data halls online and within design redundancy. According to Mordor Intelligence, services tied to installation, commissioning, and periodic maintenance are also counted because customers procure them together with hardware.

Scope exclusion: Cooling equipment, IT compute racks, construction spend, and off-site utility sales are kept outside our baseline.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facility engineers at colocation plants in Jakarta and Batam, power equipment distributors, and government officials overseeing data localization policy. The discussions validated utilization rates, redundancy preferences, and likely commissioning timelines, filling gaps left by public statistics before final triangulation.

Desk Research

Our analysts began with open datasets from Badan Pusat Statistik, the Ministry of Energy and Mineral Resources, PLN's annual supply plans, and the Indonesian Internet Service Providers Association to size present grid capacity, data traffic, and power demand trends. We then triangulated those series with regional signals from the International Energy Agency, Ember's ASEAN data center electricity tracker, and customs shipment codes that isolate UPS and generator imports. Company filings, investor decks, and reputable press also added ASP and pipeline clues.

To enrich hard numbers, we tapped D&B Hoovers for supplier financials and Dow Jones Factiva for project news alerts, ensuring early capture of hyperscale campus announcements. This list is illustrative, not exhaustive; many additional sources supported data checks and clarification.

Market-Sizing & Forecasting

A top-down build starts with installed IT load (MW) and typical PUE to reconstruct annual electrical consumption, which is then priced using blended tariffs and average hardware cost curves. Supplier roll-ups of shipped UPS kVA and sampled generator ASP multiplied by volume act as bottom-up anchors that adjust totals. Key variables include new hyperscale MW additions, average redundancy (N+1 vs 2N), utility tariff progression, foreign direct investment in digital infrastructure, and renewable energy share commitments. A multivariate regression projects each driver to 2030, and scenario analysis brackets upside from AI workloads. Data gaps in supplier volumes are bridged with weighted averages from customs and primary interviews.

Data Validation & Update Cycle

Outputs pass variance checks against independent MW trackers, then a senior analyst reviews assumptions. Reports refresh annually, with interim revisions if policy or large project news triggers a re-run so clients receive the latest vetted view.

Why Mordor's Indonesia Data Center Power Baseline Commands Reliability

Published estimates diverge because firms mix different infrastructure buckets, apply unique pricing ladders, and refresh at varied cadences.

Key gap drivers include wider scope that folds in cooling or full construction spend, models built on headline investment cost rather than annual revenue, and aggressive or conservative hyperscale build-out assumptions not tested with on-ground respondents.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 332.4 M (2025) | Mordor Intelligence | - |

| USD 347.8 M (2024) | Regional Consultancy A | Excludes services, applies global ASP without local tariff adjustments |

| USD 2.39 B (2024) | Trade Journal B | Captures total data center investment, not just power equipment revenue |

| USD 1.45 B (2023) | Global Consultancy C | Blends power with cooling and facility construction, single-year survey with no update cycle |

These comparisons show that our disciplined scope selection, annually refreshed variables, and dual validation steps give decision makers a balanced, transparent baseline they can retrace and trust.

Key Questions Answered in the Report

What is the current size of the Indonesia data center power market?

The market is valued at USD 385.86 million in 2026 and is projected to expand to USD 813.24 million by 2031.

Which component segment is growing the fastest?

Power Distribution Units are forecast to grow at an 17.85% CAGR thanks to rising demand for intelligent, high-density power distribution in AI and hyperscale environments.

Why is Batam attracting new data-center investment?

Batam offers proximity to Singapore’s network hubs, lower seismic risk, and improving grid strength, making it an attractive secondary location for hyperscale builds.

How are sustainability targets influencing power-system choices?

Operators now favor UPS and generators that can integrate renewable energy and deliver measurable PUE improvements, with PLN’s green PPAs accelerating this shift.

What is the biggest restraint on market growth?

High upfront capital expenditure for Tier IV-grade power infrastructure remains the primary brake, especially for new entrants without proven ESG financing credentials.

Which tier level is expanding the fastest?

Tier IV facilities are projected to grow at a 17.15% CAGR as mission-critical AI and financial workloads demand 99.995% uptime and full fault tolerance.

Page last updated on: