Pharmacy Benefit Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

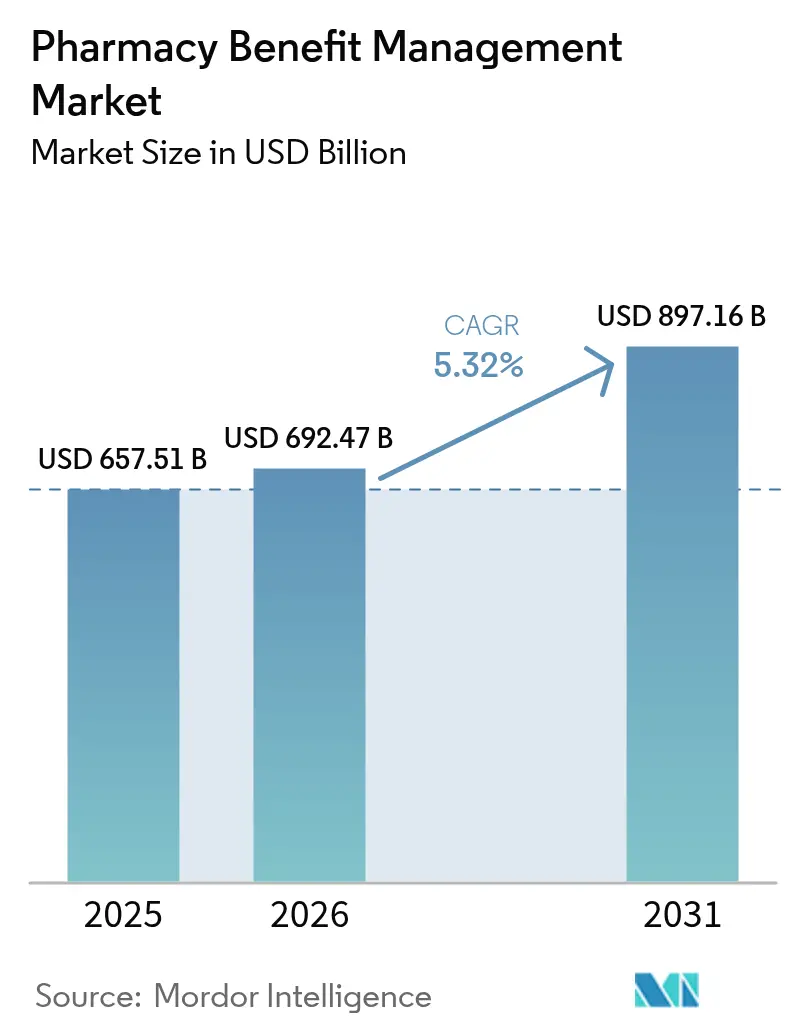

| Market Size (2026) | USD 692.47 Billion |

| Market Size (2031) | USD 897.16 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

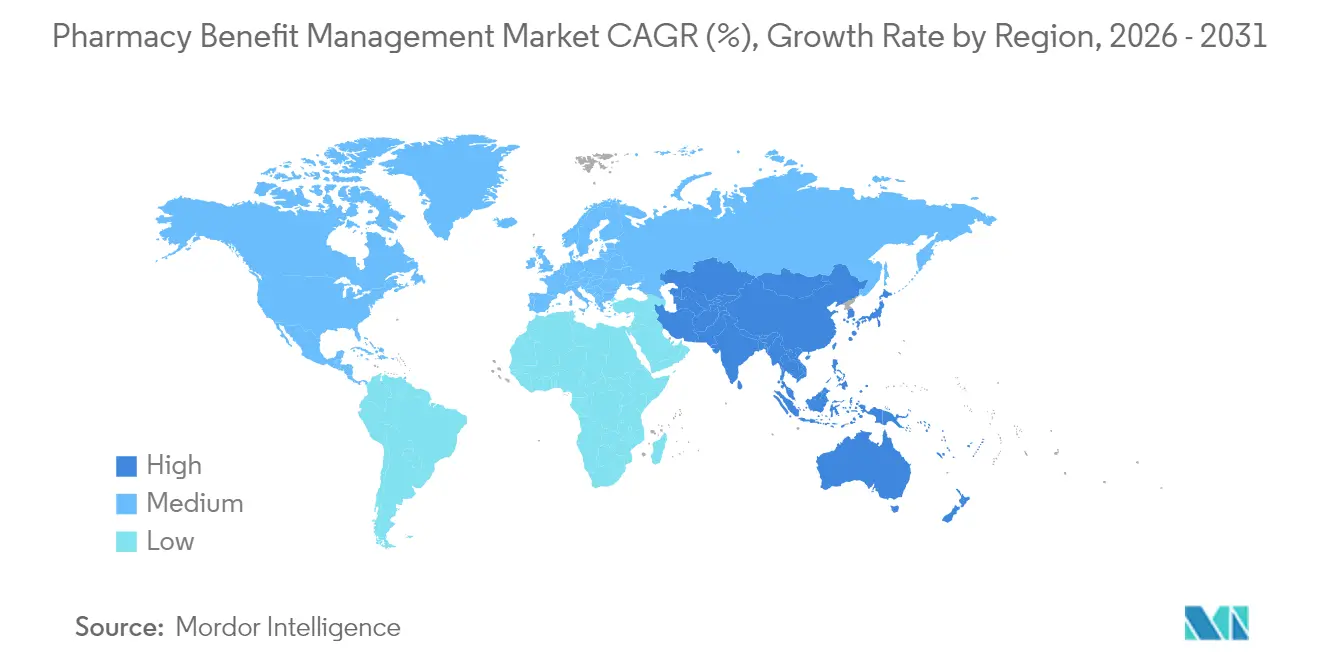

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmacy Benefit Management Market Analysis by Mordor Intelligence

The pharmacy benefit management market size is expected to grow from USD 657.51 billion in 2025 to USD 692.47 billion in 2026 and is forecast to reach USD 897.16 billion by 2031 at 5.32% CAGR over 2026-2031. Rising prescription-drug spending—now 27.0% of employer medical outlays—underscores the growing reliance on PBMs for cost control. The upswing also reflects surging specialty-drug utilization, accelerated employer scrutiny of benefit contracts, and technology investments that streamline claims and prior authorization workflows. North America leads the Pharmacy Benefit Management market with 46.3% revenue share, while Asia Pacific records the fastest growth as coverage expands in China and India. Competitive intensity remains high as vertically integrated PBMs consolidate buying power, even as transparent newcomers chip away at rebate-driven models.

Key Report Takeaways

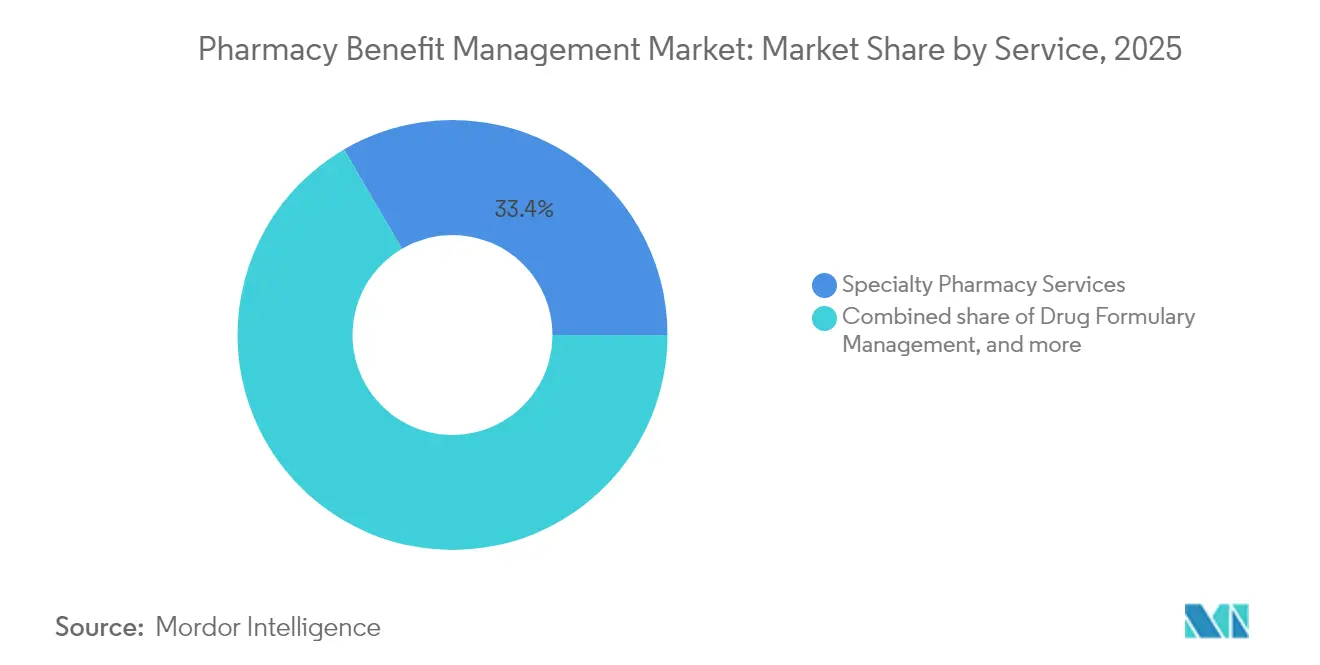

- By service, specialty pharmacy services led with 33.42% revenue share in 2025, whereas claims processing & adjudication is poised for a 7.12% CAGR through 2031.

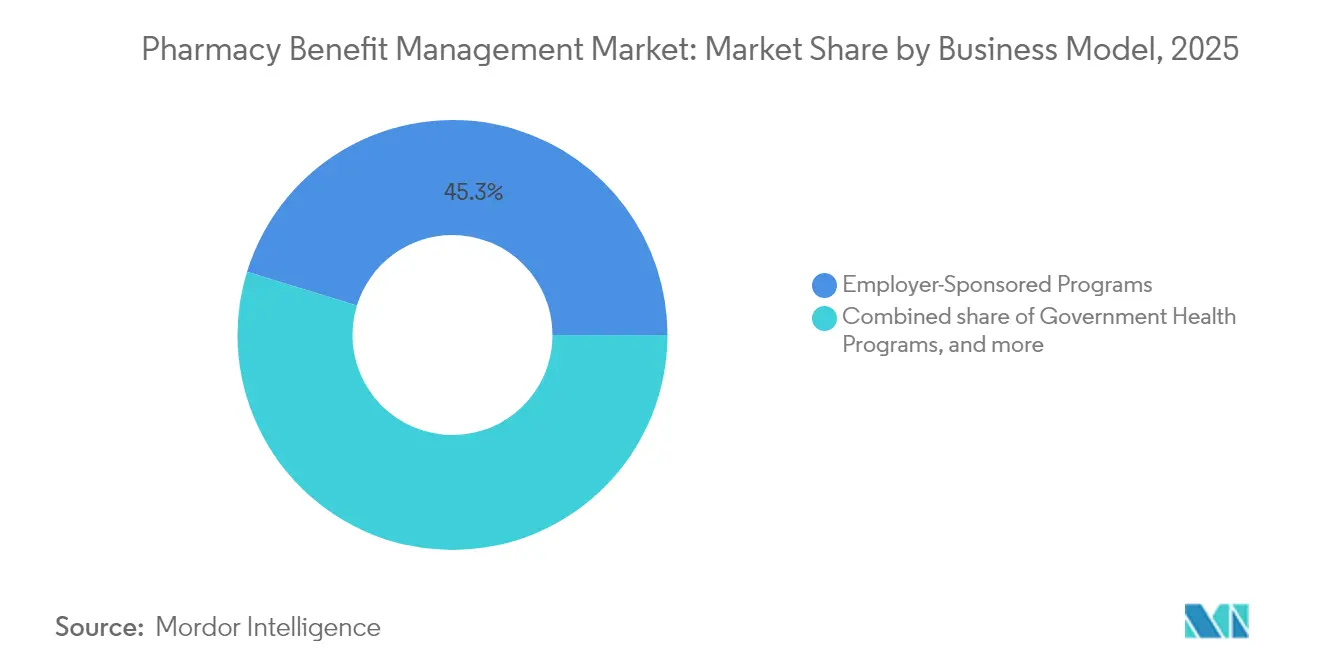

- By business model, employer-sponsored programs controlled 45.25% of the pharmacy benefit management market share in 2025; government health programs show the quickest rise at a 6.45% CAGR to 2031.

- By end user, PBM organizations and retail pharmacies jointly held 75.00% share in 2025; Mail-order pharmacies are projected to expand at an 7.78% CAGR through 2031.

- By region, North America dominated with 45.88% in 2025, whereas Asia Pacific is expected to log a 7.29% CAGR, lifting the region to USD 159.86 billion by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmacy Benefit Management Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating specialty-drug costs | +1.9% | Global | Long term (≥ 4 years) |

| Expansion of public & private coverage pools | +1.3% | North America, Asia Pacific | Medium term (2-4 years) |

| Shift to value-based pharmacy benefits | +1.1% | North America, Europe | Medium term (2-4 years) |

| Digital transformation & workflow automation | +0.9% | Global | Short term (≤ 2 years) |

| Rising demand for cost transparency & pass-through pricing models | +1.0% | North America, Europe | Short term (≤ 2 years) |

| Consolidation & vertical integration across the drug-supply chain | +0.8% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Prescription-Drug Expenditure & Therapeutic Complexity

Specialty medicines accounted for 54% of hospital drug spend in 2025, pressuring payers to adopt PBM models that integrate clinical expertise with utilization controls. The popularity of GLP-1 agonists for diabetes and obesity may lift that therapeutic class toward USD 100 billion within five years, requiring tighter formulary rules and step-therapy edits. Oncology pipelines and orphan drugs compound complexity, while multimorbidity drives polypharmacy across age cohorts. PBMs deploying advanced analytics can coordinate regimens, flag duplication, and negotiate indication-based contracting that balances outcomes with affordability. These pressures support sustained demand for Pharmacy Benefit Management market solutions through 2030.

Expansion of Public & Private Health-Coverage Pools

Medicare Part D is forecast to reach 36% of U.S. drug spending by 2032, up from 2024 levels. The Inflation Reduction Act caps out-of-pocket Part D costs at USD 2,000 for 18.7 million members beginning in 2025. Commercial employers are simultaneously re-bidding contracts, with 52% exploring new PBM partners within three years. As coverage pools widen, PBMs that master disparate formulary rules, vaccine mandates, and reporting obligations gain scale advantages. Ongoing enrollment growth in India’s Ayushman Bharat and China’s urban employee insurance adds regional tailwinds, enhancing the Pharmacy Benefit Management market outlook.

Shift Toward Value-Based & Outcome-Linked Pharmacy Benefits

Performance-based reimbursement models are moving beyond pilots, with 54% of executives expecting at least a 50% jump in outcome-based contracts by 2025. PBMs apply predictive analytics to risk-stratify members, trigger adherence interventions, and quantify avoided downstream costs. Real-world evidence supplements RCT data in drug evaluations, informing indication-based pricing and shared-savings mechanisms. Transparent metrics improve employer trust and may temper legislative calls for stricter PBM oversight. Value-based designs also encourage manufacturers to back clinical promises with refund or replacement guarantees, reinforcing Pharmacy Benefit Management market innovation.

Digital Transformation & Workflow Automation in PBM Operations

Seventy-seven percent of health leaders rank artificial intelligence as a top technology priority for 2025. Cloud-native claim engines speed prior authorization approvals, flag fraud, and cut average adjudication costs per script. Capital Rx’s Judi Health platform unites medical and pharmacy claims, breaking data silos that inflate total cost of care. Automation frees pharmacists for clinical counseling, raises throughput in mail facilities, and supplies employers near real-time spend dashboards. These advances support the 7.5% CAGR forecast for Claims Processing services and deepen the digital moat of the Pharmacy Benefit Management market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying legislative & regulatory scrutiny | −1.4% | North America, Europe | Short term (≤ 2 years) |

| Erosion of rebate economics from biosimilar & generic competition | −1.1% | Global | Long term (≥ 4 years) |

| Litigation & margin pressure from independent-pharmacy/DIR reform | −1.0% | North America | Short term (≤ 2 years) |

| Data-privacy & interoperability barriers limiting advanced analytics | −0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Legislative & Regulatory Scrutiny of PBM Practices

State legislatures introduced 34 targeted PBM bills for the 2025 session, covering spread pricing bans and audit rights. The FTC’s January 2025 interim report claimed the Big Three captured USD 7.3 billion in excess specialty generic markups between 2017 and 2022. Federal proposals, such as the Patients Before Monopolies Act, would separate PBMs from insurer and pharmacy affiliates, raising structural risk for vertically integrated firms. Compliance costs and contract renegotiations may trim margins and slow acquisition pipelines, tempering Pharmacy Benefit Management market expansion in the near term.

Erosion of Rebate Economics from Biosimilar & Generic Competition

Humira biosimilars flooded formularies in 2025, eroding rebate pools that underpinned PBM revenue streams. The gross-to-net gap for branded drugs hit USD 334 billion in 2023 but is narrowing as payers redirect rebates to premium relief. Medicare price-negotiation authority limits rebate leverage on high-spend therapies, while employers push for pass-through models like CVS Health’s CostVantage that surrender 100% of rebates by 2028. PBMs must cultivate alternative revenue—clinical programs, data analytics, and optional administrative fees—reducing reliance on rebates and reshaping long-term Pharmacy Benefit Management market economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Claims Processing Drives Digital Transformation

Specialty Pharmacy Services captured 33.42% of 2025 revenue as complex biologics proliferated in oncology and rare-disease care. Unified care teams, cold-chain logistics, and adherence coaching define this high-touch service line, anchoring the Pharmacy Benefit Management market size leadership among service categories. Claims Processing & Adjudication is projected to grow at 7.12% CAGR to 2031, powered by AI-enabled claim engines that curtail error rates and flag wasteful spending. Capital Rx’s February 2025 launch of Judi Health™ exemplifies the shift to integrated, cloud-native platforms that reconcile medical and pharmacy claims in real time.

Drug Formulary Management continues to pivot from price-tier grids to outcome-centric scorecards that weight real-world evidence and patient-reported metrics. Benefit Plan Design & Consultation helps employers evaluate copay maximizer programs and GLP-1 coverage carve-outs as that class gains weight-management indications. Together, these advisory services supplement transaction-based revenue and support wider adoption of transparent pass-through arrangements across the Pharmacy Benefit Management market.

By Business Model: Government Programs Reshape Market Dynamics

Employer-Sponsored Programs retained 45.25% market share in 2025, mirroring the central role of job-based insurance in U.S. healthcare. Heightened C-suite focus on drug inflation steers demand toward pass-through pricing, formulary exclusions, and value-based guarantees that limit budget surprises. The Pharmacy Benefit Management market size for Government Health Programs is forecast to advance at a 6.45% CAGR, aided by Medicaid expansion and the out-of-pocket cap in Medicare Part D.

Commercial Health-Insurance Management blends provider-sponsored plans and exchange products, requiring PBMs to synchronize benefit rules across metallic tiers. Direct-to-Consumer Discount-Card Programs proliferate through digital apps that post NADAC-based prices and offer mail-delivery perks. Mark Cuban’s Cost Plus movement underscores consumer appetite for transparent cash pricing, nudging incumbents to modernize benefit designs within the broader Pharmacy Benefit Management market.

By End User: Mail-Order Pharmacies Accelerate Growth

PBM Organizations and Retail Pharmacies together controlled 75.00% of dispensing revenue in 2025, reflecting durable store networks and vertically integrated ownership. The Pharmacy Benefit Management market share of Mail-Order Pharmacies is on track to expand fastest, at an 7.78% CAGR, as home delivery aligns with chronic-care adherence programs and Medicare’s 90-day supply incentives. FTC analysis shows PBM-owned mail pharmacies received reimbursements up to 200-times higher than independents for select oncology products, intensifying policy debate.

Hospital systems pursue specialty-pharmacy accreditation to capture infusion margins and coordinate value-based bundles. Telehealth entrants pair virtual prescribing with automated dispensing centers, widening access and reinforcing the omnichannel direction of the Pharmacy Benefit Management market.

Geography Analysis

North America led with 45.88% of 2025 revenue, anchored by U.S. drug-spend intensity and deep PBM penetration. The region’s oligopolistic PBM triad prompts policy activism, evident in 170 state bills introduced in 2024 to curb spread pricing and clawbacks Bloomberg Law. Inflation Reduction Act provisions that start in 2025 reshape formulary math, prompting contract rewrites and shifting rebate flows within the Pharmacy Benefit Management market.

Asia Pacific registers a 7.29% CAGR outlook, the fastest globally. China alone is projected to hit USD 159.86 billion by 2031 on rising chronic-disease prevalence and policy moves to centralize bulk-drug procurement. India’s growth stems from the Production-Linked Incentive scheme and expansion of Jan Aushadhi generic outlets to 10,500 by March 2025. Japan’s focus on biopharmaceutical R&D and value-based reimbursement may lift specialty-drug uptake, extending scope for PBM-like services despite demographic headwinds. Europe maintains sizable volume under reference-pricing rules and HTA frameworks. Germany’s AMNOG negotiations and the UK’s Voluntary Scheme for Branded Medicines Pricing push PBMs to demonstrate cost-offsets beyond list-price concessions. Middle East & Africa and South America contribute modest shares but display accelerating demand as mandatory health-insurance models roll out. Brazil’s unified procurement of high-cost drugs underscores the region’s appetite for centralized benefit management within the global Pharmacy Benefit Management market.

Competitive Landscape

The Pharmacy Benefit Management market remains highly concentrated: CVS Caremark, Express Scripts, and OptumRx processed about 80% of U.S. claims in 2024. Vertical integration binds these PBMs to insurers and retail or mail pharmacies, bolstering negotiating leverage yet raising conflict-of-interest concerns. The American Medical Association flagged potential anticompetitive risk in markets where the top two PBMs handle 80-90% of scripts[3]American Medical Association, “New AMA Analysis of Consolidation in PBM Markets,” ama-assn.org.

Strategic priorities emphasize scale economics, specialty-drug network control, and data lake investments that fuel predictive adherence interventions. CVS reported that 75% of commercial members adopted two or more features of its TrueCost suite by late 2024, signaling traction for fee-based, pass-through models. Express Scripts advances digital pharmacy channels, while OptumRx integrates behavioral-health datasets to improve medication safety.

Challenger PBMs—Capital Rx, SmithRx, Navitus—win share through transparent network pricing and low fixed fees. Capital Rx’s National Average Drug Acquisition Cost index feeds a clearinghouse model that aligns acquisition costs with client invoices, drawing interest from regional Blues plans. Start-ups test AI-driven prior-auth bots and consumer coupon engines, widening the innovation funnel for the Pharmacy Benefit Management market.

Regulatory scrutiny sharpens competitive risk. The FTC’s January 2025 report could spur structural remedies, while congressional hearings examine mail-pharmacy reimbursement disparities. Incumbents are diversifying into home-infusion, digital therapeutics, and primary-care alignment to offset margin compression, signaling an era of adaptive repositioning.

Pharmacy Benefit Management Industry Leaders

Optum Inc.

CVS Health (Caremark)

Express Scripts (Cigna Evernorth)

Humana Pharmacy Solutions

Prime Therapeutics LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Capital Rx launched Judi Health, a unified medical-and-pharmacy claims engine that delivers real-time benefit adjudication and integrated analytics.

- April 2025: Mobile-health Network Solutions agreed to acquire Lifepack, an Indonesian telehealth and pharmacy platform, for up to USD 7.2 million, expanding PBM-adjacent services in Southeast Asia

- March 2024: Prime Therapeutics and Capital Rx formed a strategic alliance to bolster claims-processing efficiency and transparency

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the pharmacy benefit management (PBM) market as the complete value generated by third-party administrators that design, negotiate, and manage prescription-drug plans for health insurers, employers, and public programs, including the claims adjudication platforms, rebate contracting, specialty-pharmacy fulfillment, and mail-order dispensing that sit inside a modern PBM operation.

Scope exclusion: stand-alone drug discount card vendors that do not underwrite or manage a full benefit design are not included.

Segmentation Overview

- By Service

- Specialty Pharmacy Services

- Drug Formulary Management

- Benefit Plan Design & Consultation

- Other Services

- By Business Model

- Government Health Programs

- Employer-Sponsored Programs

- Commercial Health-Insurance Management

- Direct-to-Consumer Discount-Card Programs

- By End User

- PBM Organizations (In-house & External)

- Mail-Order Pharmacies

- Retail Pharmacies

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured questionnaires with actuaries at health plans, large self-insured employers, retail pharmacists, specialty-drug distributors, and former PBM executives allowed us to validate rebate spreads, understand formulary steering tactics, and gauge likely changes under transparency legislation across North America, Europe, and selected Asia-Pacific markets.

Desk Research

We began with public datasets from agencies such as the Centers for Medicare & Medicaid Services, the U.S. Bureau of Labor Statistics, and the OECD that quantify prescription spending and plan enrollment. Trade associations, America's Health Insurance Plans, Pharmaceutical Care Management Association, and the National Community Pharmacists Association, provided utilization ratios, formulary tier shares, and mail-order penetration. Company 10-Ks, investor decks, and selected state pharmacy claims audits helped benchmark average script costs and rebate pass-through trends. Paid databases like D&B Hoovers and Dow Jones Factiva supplied revenue splits for vertically integrated PBMs. The sources noted illustrate, not exhaust, the wider pool we consulted.

Market-Sizing & Forecasting

A top-down build starts with national prescription spending, which is disaggregated by payer type and drug channel before applying PBM penetration rates that our analysts refine with primary-research inputs. We corroborate totals through selective bottom-up checks, mail-order script volumes multiplied by sampled average service fees and employer plan lives rolled up across Fortune 1000 cohorts, adjusting for double counting where integrated insurers report internal PBM revenue. Key variables tracked include specialty-drug share of spend, average rebate depth, mail-order utilization, public-program enrollment shifts, biosimilar uptake, and regulatory reimbursement caps. Multivariate regression, using GDP-per-capita growth and chronic-disease prevalence as leading indicators, frames the 2025-2030 forecast; scenario overlays address potential rebate reform shocks.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer-analyst cross-checks, and senior-review sign-off. Models refresh annually, with interim updates triggered by material events such as new federal rule makings or mega mergers, ensuring clients receive the latest vetted view.

Why Our Pharmacy Benefit Management Baseline Commands Reliability

Published PBM estimates often diverge because firms apply different benefit-scope boundaries, treat rebates inconsistently, or extrapolate U.S. data globally without enrollment adjustments.

Key gap drivers include: some publishers roll specialty-distribution revenue into PBM totals, others convert ex-manufacturer sales at list rather than net prices, and refresh cadences vary. Mordor revisits benchmarks each year, whereas a few peers update every three years, inflating numbers in high-inflation cycles.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 657.51 B (2025) | Mordor Intelligence | - |

| USD 609.13 B (2025) | Regional Consultancy A | Treats discount-card volume as PBM revenue and uses list-price drug spend |

| USD 810.50 B (2025) | Global Consultancy B | Adds specialty-distribution fees and projects global uptake from U.S. penetration rates |

The comparison shows that when scope is tightly defined around managed prescription benefits and net drug outlays, our approach, market sizing remains moderate and traceable. By grounding calculations in payer-level spend, verified rebate flows, and annually refreshed variables, Mordor Intelligence delivers a balanced baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the Pharmacy Benefit Management market?

The market reached USD 692.47 billion in 2026 and is projected to grow to USD 897.16 billion by 2031 at a 5.32% CAGR.

Why are specialty drugs so important to PBMs?

Specialty medicines represent 54.0% of hospital drug spend in 2025, so payers rely on PBMs for tailored clinical management and price negotiation .

How concentrated is the U.S. PBM sector?

CVS Caremark, Express Scripts, and OptumRx processed about 80% of U.S. prescription claims in 2024

What impact will the Inflation Reduction Act have on PBMs?

Beginning in 2025, Part D out-of-pocket costs are capped at USD 2,000, and price negotiations for selected drugs will alter rebate structures, reshaping PBM revenue models

Which service segment is expanding the fastest?

Claims Processing & Adjudication is forecast to grow 7.12% annually through 2031 as AI platforms streamline real-time decision making

Which region will see the quickest PBM growth?

Asia Pacific is projected to post a 7.29% CAGR, with China alone on track to reach USD 159.86 billion by 2031

Page last updated on: