Contract Development and Manufacturing Organization (CDMO) Market Size

| Study Period | 2019 - 2029 |

| Market Size (2024) | USD 238.47 Billion |

| Market Size (2029) | USD 330.36 Billion |

| CAGR (2024 - 2029) | 6.74 % |

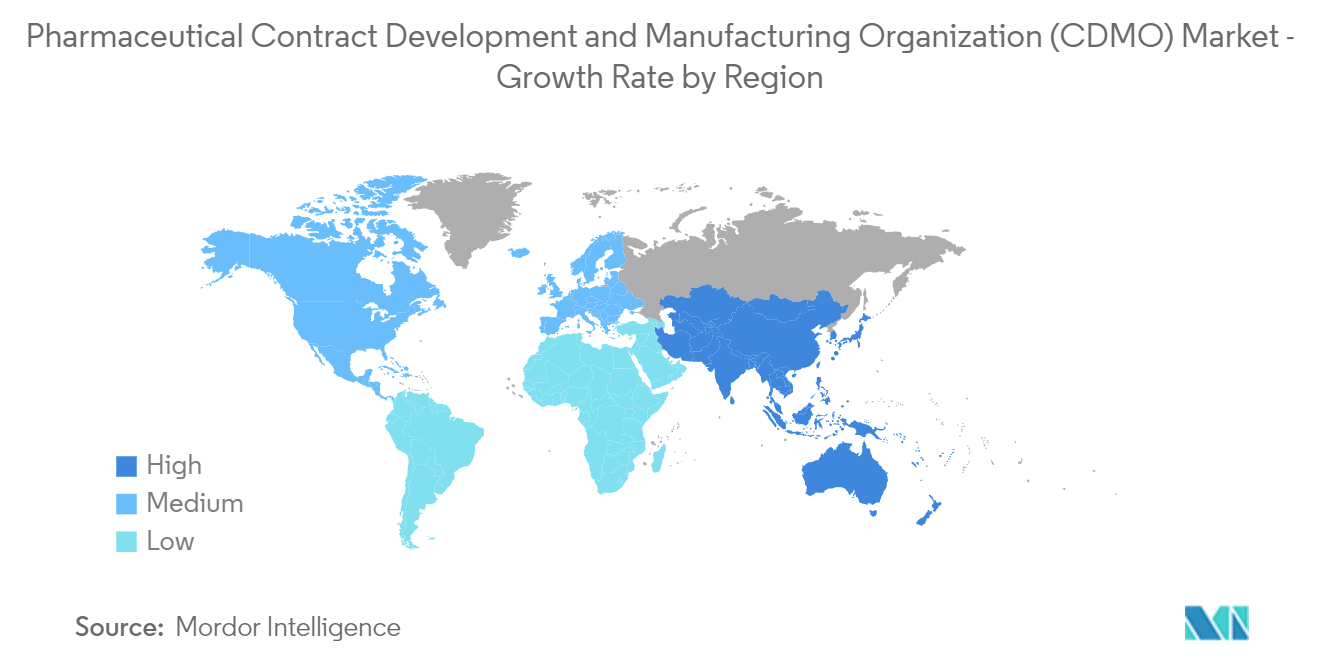

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Contract Development and Manufacturing Organization (CDMO) Market Analysis

The Pharmaceutical Contract Development and Manufacturing Organization Market size is estimated at USD 238.47 billion in 2024, and is expected to reach USD 330.36 billion by 2029, growing at a CAGR of 6.74% during the forecast period (2024-2029).

- Advanced manufacturing techniques and processes are projected to help the CMO market grow. CMOs are expected to improve the efficiency of their manufacturing processes, minimizing waste and lowering costs, owing to new operational strategies, such as continuous manufacturing. The growth of small and mid-sized pharmaceutical firms, which are in charge of an expanding portion of new drug approvals and frequently lack manufacturing capacity, is anticipated to be a driving force behind CMOs adopting new manufacturing technologies.

- A growing number of pharmaceutical companies recognized the potential profitability of working with a CMO for clinical and commercial-stage manufacturing due to the increasing demand for generic drugs and biologics, the capital-intensive nature of the industry, and the complex manufacturing requirements. Pharmaceutical innovator companies must fill their pipelines with fresh medications in light of the pharmaceutical industry's continued expansion, particularly from the onset of the COVID-19 pandemic. They lack the funding to research, create, and produce goods. Therefore, the need for CMOs is crucial.

- Growth of the generic drugs market, high uptake of small molecule drugs across a wide range of diseases, patent expiration of various drugs, advanced manufacturing techniques for active pharmaceutical ingredients (API), finished dosage formulations (FDF), growing requirements for advanced processes and production technologies to meet regulatory requirements, rising deals, such as mergers, acquisitions, and other investments, increased demand for generic injectables, growing pipeline of COVID-19 vaccines and biologics production, and increasing geriatric population are contributing drivers of CMO market.

- With the rise of personalized medicine, the one-size-fits-all model is rendered obsolete. Since the industry is trying to make clinical trials more accessible and patient-friendly, technology has become a key element in contract research organizations. To maintain a competitive edge and ensure they can provide customers with the full range of solutions, CROs are at the forefront of implementing the newest technologies and tools. Adopting these new technologies has been helping CROs to be more effective and increase the speed of research, thereby driving CRO market growth.

- The costs invested in R&D are continuously increasing, yet the valuable results from these processes are becoming rarer. Many pharmaceutical companies have invested in AP biologics and injectable capabilities projects. Also, pharmaceutical companies have been seeking vendors who provide contract manufacturing, contract packaging, and quality testing services. In addition, third-party logistic providers, like DHL, have been extending their service capabilities to include contract packaging services. Furthermore, as the turnaround in formulations and technology increases, CMOs will need to invest more significant amounts to achieve agility and accommodate quicker changes in the manufacturing setup. All these factors may restrict the growth of the studied market.

- The CMO/CDMO service industry is in a unique position to help drug developers overcome some of the difficulties brought on by the COVID-19 pandemic. The pharma and biopharma industries were impacted in many ways by this pandemic, including supply chain logistics, drug development, clinical trials, supplies, and manufacturing. The COVID-19 pandemic spurred digital transformation initiatives across the pharmaceutical industry, particularly in clinical development. The need for quicker clinical development increased as COVID-19, non-COVID-19 drugs, and treatments continued to develop during that period.

Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Statistics

Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market growth is not evenly distributed across regions. The US, China, India, and Germany are the largest country markets for Pharmaceuticals CDMO Market, however, many smaller country market segments are expected to register much higher growth compared to these giants. For example, the United States is one of the top three Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market but lags behind emerging economies such as India, Germany, and South Africa in terms of future growth.

United States Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in the United States was valued at USD 54.21 billion in 2023. It is expected to reach USD 68.32 billion by 2028, growing at a CAGR of 4.74% during the forecast period (2023-2028). United States contract manufacturing organizations (CMOs) have evolved from an initial offering of essential manufacturing services to a wide range of services to meet market and outsourcer demand. Steady growth in the U.S. pharmaceutical industry and increasing outsourcing by major pharmaceutical companies focusing on their core competencies to improve profit margins are driving the country's market.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| United States Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 54.21 billion | USD 68.32 billion | 4.74% |

Canada Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in Canada was valued at USD 5.67 billion in 2023. It is expected to reach USD 7.88 billion by 2028, growing at a CAGR of 6.79% during the forecast period (2023-2028). The pharmaceutical industry of Canada is one of the most innovative in terms of products. Pharmaceuticals, a key sector of the Canadian economy, is supported by the Canadian government, which provides a business-friendly environment for pharmaceutical companies and can leverage assets for short- and long-term business strategies.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| Canada Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 5.67 billion | USD 7.88 billion | 6.79% |

United Kingdom Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in United Kingdom was valued at USD 6.02 billion in 2023. It is expected to reach USD 7.07 billion by 2028, growing at a CAGR of 3.24% during the forecast period (2023-2028). The UK’s pharmaceutical and life sciences sector has pitched up well in the face of the covid crisis, with robust capitalization providing the structure for continued momentum despite the downturn. It was due to the backdrop of innovation, aided by a complex and wide-ranging network of government support, financial incentives, and other collaboration with research institutions and the National Health Service (NHS).

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| United Kingdom Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 6.02 billion | USD 7.07 billion | 3.24% |

Germany Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in Germany was valued at USD 13.63 billion in 2023. It is expected to reach USD 17.41 billion by 2028, growing at a CAGR of 5.02% during the forecast period (2023-2028). Germany is likely to remain the largest contract manufacturing market in Western Europe, both in capacity and market share. One of the factors attracting pharmaceutical manufacturers to outsource production to this region is highly skilled and specialized employees, which is vital for manufacturing highly potent APIs (HPAPIs).

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| Germany Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 13.63 billion | USD 17.41 billion | 5.02% |

France Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in France was valued at USD 11.18 billion in 2023. It is expected to reach USD 13.75 billion by 2028, growing at a CAGR of 4.22 % during the forecast period (2023-2028). Drug prices in France are lower than in other European countries as the French government bears most of the drug costs. Due to favorable reimbursement policies and high margins, the injectable segment is expected to experience a higher growth rate than other segments of its FDF manufacturing.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| France Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 11.18 billion | USD 13.75 billion | 4.22% |

China Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in China was valued at USD 27.12 billion in 2023. It is expected to reach USD 42.94 billion by 2028, growing at a CAGR of 9.63% during the forecast period (2023-2028). China is rapidly growing as the most attractive outsourcing country. Most CMOs operating in China mainly offer API and bulk drug product manufacturing for approved generic and branded drugs. Asymchem Laboratories, Beijing Second Pharmaceutical, Chongqing Huapont Pharmaceutical, Shandong Xinhua Pharmaceutical, Venturepharm Laboratories, Porton Fine Chemicals, and Tianjin Pharmaceutical are some of the top API and chemical intermediate CMOs in the nation.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| China Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 27.12 billion | USD 42.94 billion | 9.63% |

India Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in India was valued at USD 15.63 billion in 2023. It is expected to reach USD 26.73 billion by 2028, growing at a CAGR of 11.34% during the forecast period (2023-2028). The pharmaceutical sector in India produces a variety of bulk pharmaceuticals, which are active pharmaceutical ingredients that serve as the basic raw materials for formulations. Formulations comprise the remaining four-fifths of the industry's output, with bulk pharmaceuticals making up about one-fifth.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| India Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 15.63 billion | USD 26.73 billion | 11.34% |

Japan Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in Japan was valued at USD 4.59 billion in 2023. It is expected to reach USD 5.47 billion by 2028, growing at a CAGR of 3.57% during the forecast period (2023-2028). Japan has a significant position in the pharmaceutical world globally, where the country stands as the third-largest pharmaceutical market in the world. Many multinational corporations have found it difficult to enter the industry despite this. High entrance obstacles with a historically closed domestic market have limited options. The trend is beginning to change.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| Japan Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 4.59 billion | USD 5.47 billion | 3.57% |

Australia Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in Australia was valued at USD 3.52 billion in 2023. It is expected to reach USD 4.45 billion by 2028, growing at a CAGR of 4.82% during the forecast period (2023-2028). Numerous pharmaceutical companies in Australia are struggling due to major regulatory reforms in drug pricing, structural adjustments, unpredictable reimbursement decisions, and pricing decisions. However, the nation is geographically well-positioned for pharmaceutical exports because of its proximity to South Asia's growing markets.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| Australia Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 3.52 billion | USD 4.45 billion | 4.82% |

United Arab Emirates Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in the United Arab Emirates was valued at USD 0.79 billion in 2023. It is expected to reach USD 0.88 billion by 2028, growing at a CAGR of 2.33% during the forecast period (2023-2028). The UAE pharmaceutical industry is one of the most developed markets in the Middle Eastern region, armed with a robust healthcare infrastructure and the highest per capita medical spending. There has been a spurt in drug manufacturing activities by domestic producers in the United Arab Emirates.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| United Arab Emirates Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 0.79 billion | USD 0.88 billion | 2.33% |

South Africa Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market revenue in South Africa was valued at USD 0.52 billion in 2023. It is expected to reach USD 0.67 billion by 2028, growing at a CAGR of 5.08% during the forecast period (2023-2028). South Africa is the largest CMO market in Africa. Some of the major factors responsible for South Africa’s attractive pharmaceutical contract manufacturing are its well-established and stable markets and high turnover to investments.

-Market-Revenue-in-USD-Billion.png)

| 2023 Market Size | 2028 Market Size | CAGR (2023-2028) | |

| South Africa Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market | USD 0.52 billion | USD 0.67 billion | 5.08% |

Get 10-year market size data by segments and in-depth analysis on specific countries. Contact us now.

Contract Development and Manufacturing Organization (CDMO) Market Trends

Increasing Investment in R&D Drives the Market

- The United States is one of the largest pharmaceutical markets, accounting for about half of the R&D spending in the pharmaceutical and biotech markets. CMOs play a vital role in this market, investing in new facilities and technology to serve a wide range of outsourcing entities. Also, companies are not only reaping the benefits of their Asian footprint through in-house investments but also looking to research-based partnerships to acquire high-end sourcing expertise, build drug discovery, and invest in Asia.

- In January 2022, Aragen Life Sciences (formerly GVK Biosciences) stated that it anticipated demand for outsourced research, development, and manufacturing services to continue to gain momentum. With the increasing demand for end-to-end integrated services, the CRO and CDMO industry is likely to consolidate in India and globally. The company added that it expects CROs and CDMOs to invest in new capabilities, build additional infrastructure, and increase their geographic footprint organically or inorganically.

- In addition, the need for proper infrastructure for the safe handling and containment of high-potency drugs, especially the need for appropriate analytical skills for high-potency drugs and adequate project management (including proper launch, execution, and completion) is needed to stand out in the market for research and development. In January 2022, Aragen Life Sciences (formerly GVK Biosciences) stated the demand for outsourced research, development, and manufacturing services might continue to gain momentum. With the increasing demand for end-to-end integrated services, the CRO and CDMO industry is likely to consolidate in India and globally. The company added that it expects CROs and CDMOs to invest in new capabilities, build additional infrastructure, and increase their geographic footprint organically or inorganically.

- As pharmaceutical companies shift their target toward scientific research and pharmaceutical marketing, CDMOs can further establish themselves as vital partners and build strategic, integrated partnerships with their customers. Given the rising number of complex and high-potency compounds, CDMOs can stand out through advanced technology and specialized expertise.

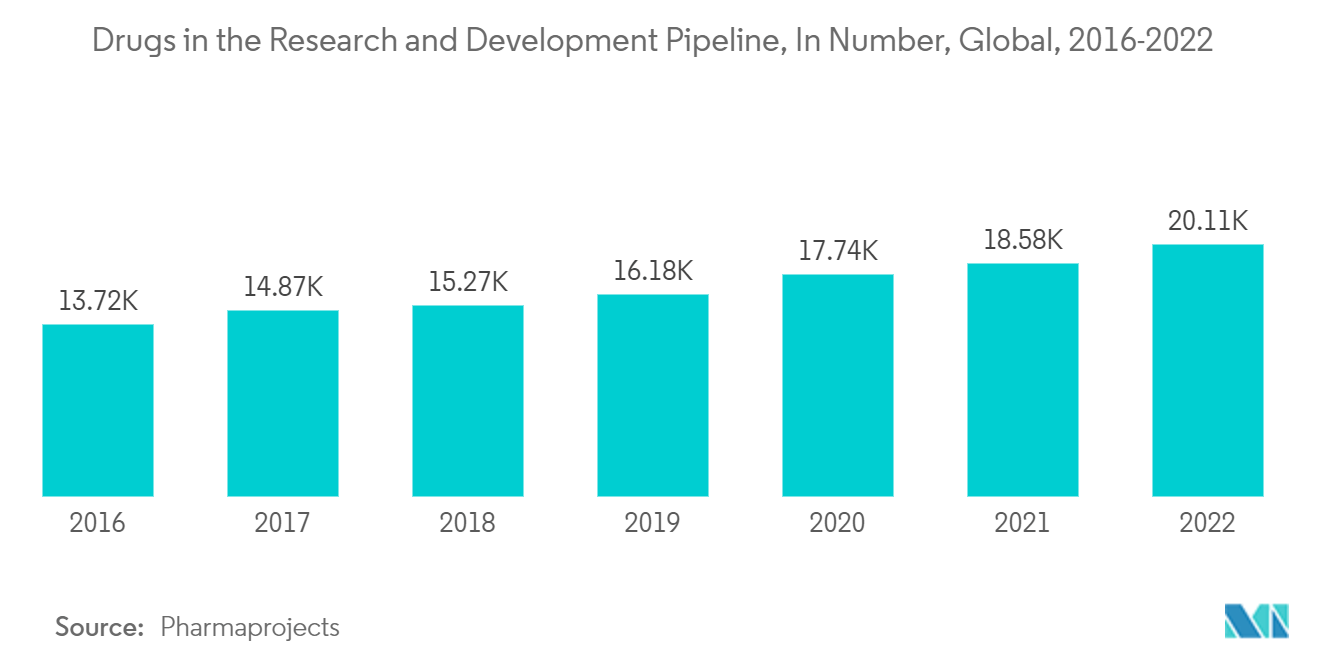

- In addition, new operational approaches such as continuous manufacturing are expected to allow CDMOs to improve the efficiency of their manufacturing processes, reducing costs and wastage. CDMOs are anticipated to discover new opportunities with an increasing number of small & medium-sized pharma firms. Such small & medium-sized pharma companies are mainly accountable for the growing share of new drug approvals and often have no manufacturing capacity. According to Pharmaprojects, globally, there will be 20,109 drugs in the R&D pipeline in 2022.

Asia-Pacific is Expected to be the Fastest-growing Region for the CRO Segment

- Asia-Pacific is anticipated to witness the highest growth in the CRO market over the forecast period due to the region's low cost compared to the United States and other developed economies. Additionally, growing incidences of chronic and lifestyle diseases, such as diabetes and heart disease, along with ease of patient recruitment and availability of expertise for clinical trials, are major driving factors boosting growth in the region.

- For instance, China has over 180 million elderly citizens suffering from chronic diseases, of whom 75% have more than one, according to the National Health Commission (NHC). Furthermore, by 2030, cardiovascular disease will cost USD 1,044 billion to the Chinese government. Similar trends for the high prevalence of diabetes are present around Asia-Pacific geographies, including China, South Korea, and Australia.

- With the increasing privatization of clinical trials, there has been an increase in research process outsourcing in developing countries such as China and India. For example, large pharmaceutical companies are increasingly outsourcing research services such as Clinical Data Management, Pharmacovigilance, Biostatistics, etc.

- There are numerous reasons why certain regions attract organizations conducting clinical trials. Some include cost, patient recruitment, required testing, and shorter timelines. The overall number of clinical trials is increasing in China, India, and Japan, making Asia-Pacific one of the potential regions. India provides preclinical services at lower costs than developed nations. Initiatives taken by the Indian government to expand the CRO potential have offered an attractive market opportunity in recent years.

- Additionally, the availability of scientific expertise in the country may boost business growth over the next few years. Clinical trials in the country are about 50% less costly than in the United States. India is one of the largest drug producers and has the most FDA-approved manufacturing plants outside the United States, giving it a competitive edge over China.

- Over the past few months, Novotechannounced numerous collaborations to facilitate the project management of clinical trials and boost biotech drug development. For instance, in July 2022, Medidata announced its renewed partnership with Novotechto continues scaling clinical studies in various therapeutic areas from 2022. With this renewed partnership, Novotechis equipped with flexible, configurable tools to address clinical research needs at scale and facilitate accelerated drug and device development in Asia Pacific and the United States.

Contract Development and Manufacturing Organization (CDMO) Industry Overview

The Pharmaceutical CDMO market is fragmented since several vendors contribute to the market share. The existence of numerous competitors in the market has an impact on service pricing, making it a direct source of competition, particularly for small-scale providers. The vendors in the market are anticipated to concentrate on offering one-stop-shop services to gain a competitive edge. The CMO, with access to significant capital, would be able to engage in these activities, thus making entry difficult for new players and enhancing competition. Players in the market are adopting strategies such as partnerships, company expansions, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- June 2023 - Catalent announced that it has broadened the scope of its One Bio Suite solution, comprising development, manufacturing, and supply for a range of biotechnological modalities including antibody and recombinant proteins, cellular and gene therapy as well as mRNA.

- January 2023 - Catalent announced that it signed a development and license agreement with Ethicann Pharmaceuticals Inc., a Canadian/American specialty pharmaceutical company specializing in creating high-value cannabinoid drug therapies, using Zydis orally disintegrating tablet (ODT) technology to advance Ethicann's clinical drug pipeline. Per the agreement, Catalent would use its Zydis technology to create pharmaceutical products containing cannabidiol (CBD) and tetrahydrocannabinol (THC) for Ethicann's use in clinical trials for a variety of conditions.

- January 2023 - Thermo Fisher Scientific Inc. acquired the global provider of specialty diagnostics, Binding Site Group, for USD 2.8 billion. With the addition of ground-breaking innovation in multiple myeloma diagnosis and monitoring, the Binding Site broadens Thermo Fisher's already expanded specialized diagnostics range. Patient outcomes can be significantly impacted by early diagnosis and well-informed treatment choices.

Contract Development and Manufacturing Organization (CDMO) Market Leaders

Catalent Inc.

Recipharm AB

Jubilant Pharmova Ltd

Patheon Inc. (Thermo Fisher Scientific Inc.)

Boehringer Ingelheim Group

*Disclaimer: Major Players sorted in no particular order

_Market_Concentration.webp)

Contract Development and Manufacturing Organization (CDMO) Market News

- June 2023 - Lifera, a commercial scale CDMO for the development of Saudi Arabia's local Biopharmaceutical Industry, has been launched by the Public Investment Fund of the Kingdom of Saudi Arabia. The PIF is the Kingdom of Saudi Arabia's sovereign wealth fund, with a mandate to undertake targeted investments and forge partnerships that will strengthen its supply chain, skills, resource development, pharmaceuticals, employment opportunities as well as technological transfer from global private sector partners.

- February 2023 - Catalent, the global provider and distributor of superior medicines, disclosed the completion of a USD 2.2 million expansion to its clinical supply facility in Singapore, resulting in a 31,000 square-foot increase in the site's footprint, allowing for the installation of 35 extra new freezers for ultra-low temperature (ULT) storage. As a result of the investment, the facility is now better equipped to handle biopharmaceuticals and advanced modalities, such as mRNA-based vaccines, cell and gene therapies, and larger packaging campaigns.

- December 2022 - Thermo Fisher Scientific, a global leader in providing scientific services, recently inaugurated a new facility in Hangzhou, China, as part of its global initiative to assist businesses more quickly in delivering treatments to patients. The manufacturing facility may cater to Chinese and international organizations' demands for manufacturing and researching biologics and sterile in the Asia-Pacific area.

Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Porter's Five Forces Analysis for CMO

4.2.2 Porter's Five Forces Analysis for CRO

4.3 Industry Value Chain Analysis

4.4 Industry Policies

4.5 Impact of COVID-19 on the Pharmaceutical Industry

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Outsourcing Volume by Big Pharmaceutical Companies

5.1.2 Advent of CDMO Model into the Market

5.1.3 Increasing Investment in R&D

5.2 Market Restraints

5.2.1 Increasing Lead Time and Logistics Costs

5.2.2 Stringent Regulatory Requirements

5.2.3 Capacity Utilization Issues Affecting the Profitability of CMOs

5.3 Emphasis on Solid-based Oral Dosage Formulations

5.4 Qualitative Coverage on the 3D Printing Developments in the OSD Segment

5.4.1 Evolution of 3D Printing in Fabrication Processes and the Key Advantages Over Conventional Processes

5.4.2 Analysis of Major Drugs Manufactured Using 3D Printing-based Process

5.4.3 Analysis of Key Techniques Deployed (SLS & FDM), Along with their Relative Advantages

5.4.4 Key Developments on Stakeholders

5.4.5 Market Outlook

6. TECHNOLOGY SNAPSHOT

6.1 Dosage Formulation Technologies

6.2 Dosage Forms by Route of Administration

6.3 Key Considerations for Outsourcing of Pharmaceutical R&D

6.4 Major Segments in CRO Bio Analytical Testing, Central Laboratory Testing, and cGMP Testing

7. MARKET SEGMENTATION

7.1 By Service Type CMO Segment

7.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

7.1.1.1 Small Molecule

7.1.1.2 Large Molecule

7.1.1.3 High Potency (HPAPI)

7.1.2 Finished Dosage Formulation (FDF) Development and Manufacturing

7.1.2.1 Solid Dose Formulation

7.1.2.1.1 Tablets

7.1.2.1.2 Others(Capsules, Powders, Etc.)

7.1.2.2 Liquid Dose Formulation

7.1.2.3 Injectable Dose Formulation

7.1.3 Secondary Packaging

7.2 By Research Phase CRO Segment

7.2.1 Pre-clinical

7.2.2 Phase I

7.2.3 Phase II

7.2.4 Phase III

7.2.5 Phase IV

7.3 By Geography - Pharmaceutical CMO***

7.3.1 North America

7.3.1.1 United States

7.3.1.2 Canada

7.3.2 Europe

7.3.2.1 United Kingdom

7.3.2.2 Germany

7.3.2.3 France

7.3.2.4 Italy

7.3.2.5 Rest of Europe

7.3.3 Asia-Pacific

7.3.3.1 China

7.3.3.2 India

7.3.3.3 Japan

7.3.3.4 Australia

7.3.3.5 Rest of Asia-Pacific

7.3.4 Latin America

7.3.4.1 Brazil

7.3.4.2 Mexico

7.3.4.3 Argentina

7.3.4.4 Rest of Latin America

7.3.5 Middle East and Africa

7.3.5.1 United Arab Emirates

7.3.5.2 Saudi Arabia

7.3.5.3 South Africa

7.3.5.4 Rest of Middle East and Africa

7.4 By Geography - Pharmaceutical CRO

7.4.1 North America

7.4.2 Europe

7.4.3 Asia-Pacific

7.4.4 Latin America

7.4.5 Middle East and Africa

8. VENDOR MARKET SHARE

9. COMPETITIVE LANDSCAPE

9.1 Company Profiles

9.1.1 Catalent Inc.

9.1.2 Recipharm AB

9.1.3 Jubilant Pharmova Ltd

9.1.4 Patheon Inc. (Thermo Fisher Scientific Inc.)

9.1.5 Boehringer Ingelheim Group

9.1.6 Pfizer CentreSource

9.1.7 Aenova Holding GmbH

9.1.8 Famar SA

9.1.9 Baxter Biopharma Solutions (Baxter International Inc.)

9.1.10 Lonza Group

9.1.11 Tesa Labtec GmbH (TESA SE)

9.1.12 Tapemark

9.1.13 ARX LLC

9.1.14 CMIC Holdings Co. Ltd

9.1.15 LabCorp Drug Development

9.1.16 Syneos Health Inc.

9.1.17 LSK Global Pharma Service Co. Ltd

9.1.18 Novotech Pty Ltd

9.1.19 PAREXEL International Corporation

9.1.20 Pharmaceutical Product Development LLC (Thermo Fisher Scientific Inc.)

9.1.21 PRA Health Sciences Inc. (Icon PLC)

9.1.22 Quanticate Ltd

9.1.23 IQVIA Holdings Inc.

9.1.24 SGS Life Science Services SA

9.1.25 Hangzhou Tigermed Consulting Co. Ltd

9.1.26 Samsung Bioepis Co. Ltd

9.1.27 WuXi AppTec Inc.

9.1.28 Sagimet Biosciences (3V Biosciences Inc.)

- *List Not Exhaustive

10. INVESTMENT SCENARIO

11. FUTURE OUTLOOK OF THE GLOBAL PHARMACEUTICAL CDMO MARKET

Contract Development and Manufacturing Organization (CDMO) Industry Segmentation

The Pharmaceutical CDMO Market study provides a detailed breakdown of the CRO (Contract Research Organization) and CMO (Contract Manufacturing Organization) market, as the term CDMO represents organizations that provide both development and manufacturing of drugs, encompassing the overall market trends and growth projections. The market size reflects the revenue generated by CDMO companies. Revenue from both types of organizations has been considered for the total market size. In their capacity as adaptable third-party service providers, CDMOs assist pharmaceutical firms at all stages of the production of medicines, including research and development, manufacturing, and formulating and finishing processes.

The Pharmaceutical Contract Development and Manufacturing Organization Market is segmented by Service Type CMO Segment (Active Pharmaceutical Ingredient (API) Manufacturing (Small Molecule, Large Molecule, High Potency (HPAPI)), Finished Dosage Formulation (FDF) Development and Manufacturing (Solid Dose Formulation (Tablets), Liquid Dose Formulation, Injectable Dose Formulation), Secondary Packaging), Research Phase CRO Segment (Pre-clinical, Phase I, Phase II, Phase III, Phase IV), and Pharmaceutical CMO Geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, Italy, Rest of Europe), Asia-Pacific (China, India, Japan, Australia, Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, Rest of Latin America), Middle-East and Africa (United Arab Emirates, Saudi Arabia, South Africa, Rest of Middle-East and Africa)), Pharmaceutical CRO Geography (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa). The market sizes and forecasts are provided in terms of value USD for all the above segments.

| By Service Type CMO Segment | ||||||||

| ||||||||

| ||||||||

| Secondary Packaging |

| By Research Phase CRO Segment | |

| Pre-clinical | |

| Phase I | |

| Phase II | |

| Phase III | |

| Phase IV |

| By Geography - Pharmaceutical CMO*** | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

| By Geography - Pharmaceutical CRO | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Research Faqs

How big is the Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market?

The Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market size is expected to reach USD 238.47 billion in 2024 and grow at a CAGR of 6.74% to reach USD 330.36 billion by 2029.

What is the current Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market size?

In 2024, the Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market size is expected to reach USD 238.47 billion.

Who are the key players in Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market?

Catalent Inc., Recipharm AB, Jubilant Pharmova Ltd, Patheon Inc. (Thermo Fisher Scientific Inc.) and Boehringer Ingelheim Group are the major companies operating in the Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market.

Which is the fastest growing region in Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market?

In 2024, the North America accounts for the largest market share in Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market.

What years does this Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market cover, and what was the market size in 2023?

In 2023, the Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market size was estimated at USD 223.41 billion. The report covers the Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

CDMO Industry Report

Statistics for the 2024 Pharmaceutical Contract Development and Manufacturing Organization (CDMO) market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Pharmaceutical Contract Development and Manufacturing Organization (CDMO) analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Report Snapshots

- Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Size

- Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Share

- Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Market Trends

- Pharmaceutical Contract Development and Manufacturing Organization (CDMO) Companies