Pharmaceutical Analytical Testing Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

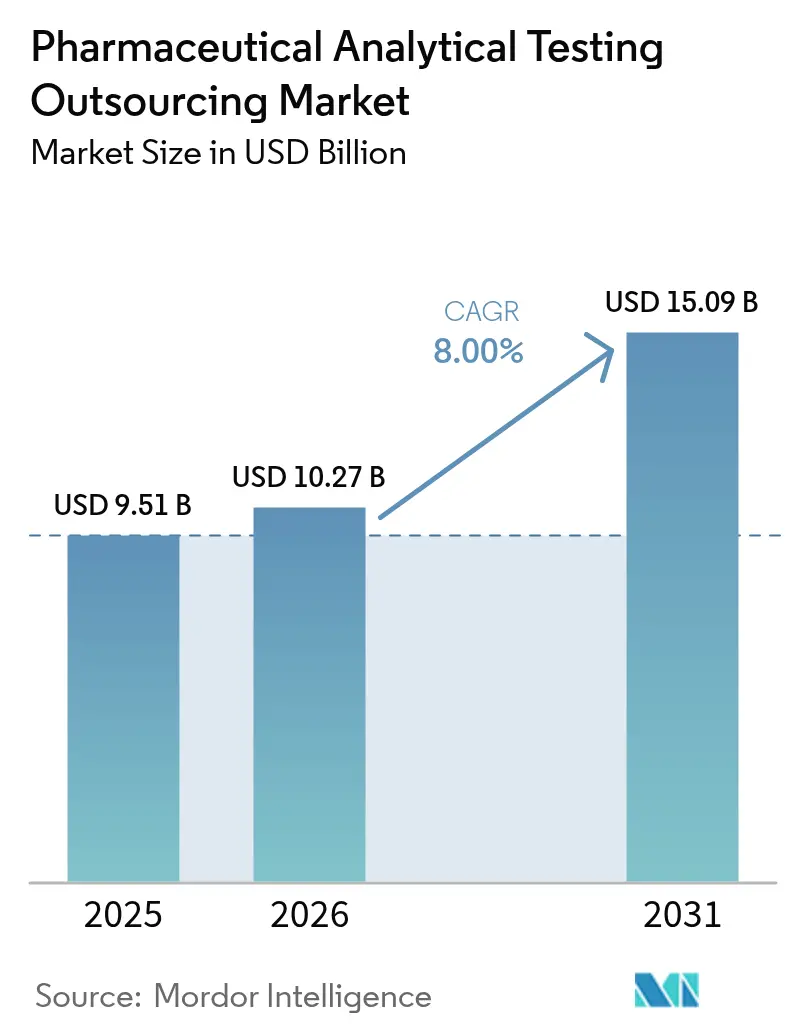

| Market Size (2026) | USD 10.27 Billion |

| Market Size (2031) | USD 15.09 Billion |

| Growth Rate (2026 - 2031) | 8.00% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Analytical Testing Outsourcing Market Analysis by Mordor Intelligence

The pharmaceutical analytical testing outsourcing market size is expected to grow from USD 9.51 billion in 2025 to USD 10.27 billion in 2026 and is forecast to reach USD 15.09 billion by 2031 at 8.00% CAGR over 2026-2031. This expansion is propelled by rigorous cGMP enforcement, a rapid pivot to biologics, and widening regulatory alignment that together elevate both the volume and complexity of outsourced analytical work. Large and mid-sized drug makers now regard external labs as strategic partners that de-risk compliance, inject specialized know-how, and deliver speed without heavy capital outlays. Continuous FDA audit pressure, exemplified by a 17% year-on-year rise in Form 483 observations during fiscal 2024, keeps quality management in sharp focus while simultaneously opening doors for advanced service offerings such as extractables-and-leachables and viral-vector assays. On the demand side, monoclonal antibodies, cell therapies, and gene therapies underpin accelerating bioanalytical workloads, whereas on the supply side, CROs scale capacity through new GMP sites, AI-enabled platforms, and targeted acquisitions that enhance geographic reach and technology depth.

Key Report Takeaways

- By services, bioanalytical testing led the market with 43.78% revenue share in 2025 and is projected to register the fastest 12.56% CAGR through 2031.

- By test type, chemistry testing held 30.80% share in 2025, while extractables & leachables is forecast to grow quickest at an 10.95% CAGR.

- By phase, commercial and QC release accounted for 32.05% of 2025 value; Phase I services are advancing at a 10.05% CAGR to 2031.

- By technology platform, chromatography-based methods dominated with 27.00% share in 2025, whereas cell-based bioassays are expanding at an 11.22% CAGR.

- By outsourcing model, full-service CRO arrangements captured 48.90% share in 2025, but functional service provider agreements are rising at a 9.73% CAGR.

- By end-user, pharmaceutical and biopharmaceutical companies generated 65.70% of 2025 revenue; CDMOs/CMOs represent the fastest-growing end-user group at 10.22% CAGR.

- By geography, North America contributed the largest 36.90% share in 2025, while Asia-Pacific is the fastest-growing region with a 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Analytical Testing Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened global cGMP enforcement | +1.8% | US, EU, India | Medium term (2-4 years) |

| Shift to biologics expands complex testing | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Cost-saving and CAPEX avoidance for small pharma | +1.4% | Global | Short term (≤ 2 years) |

| Rising use of Quality-by-Design protocols | +1.2% | US, EU, APAC | Medium term (2-4 years) |

| AI-enabled remote audits | +0.9% | Developed markets | Long term (≥ 4 years) |

| Regulatory convergence in ASEAN & LATAM | +1.1% | ASEAN core, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Global cGMP Enforcement & Audit Frequency

Heightened FDA scrutiny is reshaping compliance strategies, as the agency issued 561 Form 483s in fiscal 2024 with a notable spike in stability-program findings. Manufacturers, especially in India, increasingly funnel samples to external labs with impeccable inspection records—SGS Shanghai recorded a 2024 FDA inspection with zero observations, reinforcing the credibility advantage of specialized providers The trend deepens as the FDA’s Quality Management Maturity prototype, rolled out in 2024, nudges firms toward proactive quality validation.[1]Federal Register Staff, “Voluntary Quality Management Maturity Prototype Assessment Protocol,” Federal Register, federalregister.gov

Shift-To-Biologics Expanding Complex Testing Demand

Biologics now exceed 30% of prescription drug revenue, elevating demand for assays such as cell-based potency, immunogenicity, and viral clearance that conventional small-molecule labs cannot support economically. Eurofins and SGS have each opened new biologics centers in 2024 to catch this wave. As gene-editing and cell-therapy pipelines mature, end-to-end bioanalytical outsourcing becomes mission-critical for both large pharma and virtual biotech alike.

Cost-Savings & CAPEX Avoidance For Small Pharma

A single high-resolution mass spectrometer can cost USD 1 million, a daunting barrier for seed-stage biotech. Functional service provider (FSP) models, whose adoption rose from 28% in 2018 to nearly 50% in 2023, let lean teams plug into expert resources only when needed. Charles River’s 2025 restructuring, aimed at USD 150 million in savings, underlines how even major CROs must fine-tune delivery models to meet budget-sensitive client expectations.

Rising Adoption Of Quality-By-Design Protocols

Regulators on both sides of the Atlantic now insist that quality be designed into processes, not inspected at the end. EMA’s 2025 Q&A on ICH Q8-Q10 raises the bar for process understanding, which in turn drives demand for analytics that support design-space justification.[2]European Medicines Agency Staff, “ICH Q8, Q9 and Q10 – Questions and Answers – Scientific Guideline,” European Medicines Agency, ema.europa.eu Outsourced labs with PAT and statistical-modeling skills therefore enjoy an edge, especially after the FDA’s 2025 draft guidance on sampling and in-process controls highlighted real-time data collection.[3] Federal Register Staff, “Considerations for Complying With 21 CFR 211.110; Draft Guidance for Industry; Availability,” Federal Register, federalregister.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP-data-security & cyber-risk concerns | -0.8% | North America, EU | Short term (≤ 2 years) |

| Skills shortage inflating CRO wage bills | -1.1% | Global, acute in US & EU | Medium term (2-4 years) |

| US BIOSECURE Act may curb China-based labs | -0.9% | US-centric, global supply chain | Medium term (2-4 years) |

| Capacity crunch for viral-vector/biologics assays | -1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IP-Data-Security & Cyber-Risk Concerns

Drug developers rank cybersecurity alongside scientific capability when selecting new partners as cloud adoption widens the attack surface. China’s 2024 Anti-Espionage Law adds further uncertainty by broadening state oversight of data handling, prompting some European auditors to pause on-site inspections.

Skills Shortage Inflating CRO Wage Bills

Advanced analytics needs data scientists fluent in Python and R, yet such expertise is scarce. CROs therefore raise salaries and invest in internal academies, which inflates cost bases and ultimately pricing. Industry surveys show talent gaps are most acute in automation and cyber-security roles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services: Bioanalytical Testing Dominates Complex Therapeutics Surge

Bioanalytical testing generated 43.78% of 2025 revenue, confirming its status as the linchpin of the pharmaceutical analytical testing outsourcing market. The segment’s 12.56% CAGR through 2031 reflects skyrocketing demand for ligand-binding assays, cell-based functional tests, and viral-vector characterization that accompany monoclonal antibody and cell-therapy pipelines. Method development and validation continues to anchor early-phase programs, while stability testing stays indispensable for shelf-life decisions. USP 1663/1664 enforcement pushes extractables-and-leachables assignments toward double-digit growth, and consulting services flourish as sponsors seek integrated strategies rather than transactional sample runs.

Pharmaceutical sponsors acknowledge that building comparable in-house bioanalytical suites would consume years and capital they prefer to channel into clinical assets. Eurofins’ 2024 tie-ups with mid-tier biotechs illustrate how large CROs now package protocol design, assay transfer, and regulatory writing under one roof. As a result, bioanalytical workflows consistently rank among the first candidates for externalization under both FSP and project-based frameworks, preserving internal bandwidth for intellectual-property management and clinical strategy.

By Test Type: Chemistry Testing Leadership Faces E&L Disruption

Traditional chemistry assays—identity, purity, residual solvents—still held 30.80% share in 2025, but growth has plateaued. In contrast, extractables & leachables posted an 10.95% CAGR outlook, signaling how container-closure scrutiny has become mission-critical in biologics programs. Microbiology, raw-material qualification, and dissolution remain essential for tablets and generics, yet their expansion trails the overall pharmaceutical analytical testing outsourcing market.

Intertek’s thirty-year E&L track record, built around LC-MS/MS screens and toxicological risk assessments, typifies the specialization now prized by sponsors. Precise quantification of additives, oligomers, and silicone residues is no longer optional in parenteral launches, making chemistry labs diversify or risk commoditization. Consequently, several mid-sized providers are investing in hyphenated techniques, such as GC-MS/MS, to stay relevant amid higher-margin biologics tests.

By Phase: Commercial QC Release Dominance Challenged by Phase I Acceleration

Commercial/QC release accounted for 32.05% of the pharmaceutical analytical testing outsourcing market size in 2025, reflecting routine batch testing volumes. Yet Phase I services will expand fastest, at 10.05% CAGR, powered by biotech funding rounds and accelerated pathway programs. Discovery support and preclinical tox remain steady as sponsors realize that comprehensive analytics early on mitigate late-stage attrition.

The United Kingdom’s rise as a hub for human-challenge studies offers a glimpse of how high-tempo early-phase trials rely on nimble external labs that can deliver 24-hour turnaround for PK endpoints. At the other end, commercial testing remains rooted in multiyear master service agreements that favor providers with global footprint and redundant instrumentation, ensuring business continuity and regulatory confidence.

By Technology Platform: Chromatography Leadership Faces Cell-Based Innovation

Chromatography platforms held 27.00% of 2025 revenues, a testament to their versatility across APIs. However, cell-based bioassays will grow at 11.22% CAGR as regulators demand mechanism-of-action readouts for biologics. Mass spectrometry remains indispensable for structural elucidation, while immunoassays and PCR sustain biologics release and potency testing.

The introduction of AI-driven, fully automated cell-culture systems like CellXpress.ai cuts assay variability and boosts throughput, giving CROs fresh levers for differentiation. Parallel advances in microfluidics enable multiplexed assays that shorten development timelines and reduce sample consumption. Together these innovations intensify the race to bundle orthogonal technologies—chromatography for impurities, cell-assays for function—inside unified data packages.

By Outsourcing Model: Full-Service CRO Stability Meets FSP Innovation

Full-service contracts owned 48.90% share in 2025, favoured by big pharma seeking one-stop accountability. Even so, functional service provider structures will log a 9.73% CAGR as smaller sponsors cherry-pick expertise without overhead. FSP penetration already tops 45% among Phase II/III programs for emerging biotech, where budget discipline is paramount.

CROs remodel internal P&Ls to accommodate FSP’s thinner margins, often by leaning on automation and near-shore delivery hubs. Clinical Leader reports that many legacy providers now split operational units into agile pods dedicated to single functions—method validation, stability, or E&L—mirroring client demand for granularity.

By End-User: Pharmaceutical Companies Lead While CDMOs Accelerate

Pharmaceutical and biopharmaceutical firms generated 65.70% of 2025 revenue. Yet CDMOs/CMOs will outpace at 10.22% CAGR as manufacturing outsourcing rises and production-linked analytics migrate accordingly. Hybrid manufacturing-testing bundles appeal to sponsors looking for seamless tech-transfer and reduced supply-chain nodes.

The CMOs will command more than half of global biologics capacity by 2028, underscoring the mutualism between large-scale drug substance production and off-site QC. Virtual biotech and academic spin-outs rely almost entirely on external labs, turning small-batch precision into a commercial niche for regional CROs that offer premium service levels.

Geography Analysis

North America contributed 36.90% of 2025 value, anchored by stringent FDA oversight and a dense CRO ecosystem that stretches from Boston to San Diego. Ongoing BIOSECURE Act deliberations compel US-based sponsors to re-map supply lines away from China, driving near-term traffic toward domestic and Canadian labs even at higher unit costs. Canada’s Ontario-Quebec corridor benefits from proximity and aligned GMP rules, while Mexico’s Baja and Jalisco clusters absorb late-phase stability studies thanks to bilingual workforces and competitive pricing.

Europe remains the second-largest region. Germany and the United Kingdom sustain demand through high R&D intensity and extensive clinical pipelines. EMA’s 2025 update on ICH Q8-Q10 compliance spurs penetration of PAT-enabled analytics, which smaller continental providers race to adopt. Southern Europe gains ground via growing biosimilar output, with Italy’s Lombardy region expanding wet-lab headcount by mid-single digits. Switzerland and the Nordics retain high-value project work, particularly bespoke cell-therapy assays where regulatory expectations align with their advanced hospital networks.

Asia-Pacific is the clear growth engine, projected at 10.12% CAGR to 2031. China continues to house the largest installed lab base, yet geopolitical pressures encourage US and EU sponsors to second-source in India, Singapore, and Australia. India’s Hyderabad Genome Valley, home to new viral-vector labs, captures contracts vacated by clients exiting China. Meanwhile, ASEAN’s Regulatory Harmonization Steering Committee smooths dossier formats, trimming launch timelines in Malaysia, Singapore, and the Philippines. Japan and South Korea focus on high-complexity biologics, leveraging domestic automation and robotics leadership to secure premium projects.

Other regions—South America, Middle East & Africa—comprise a smaller yet rising slice as local manufacturing incentives swell. Ecuador’s 2025 GMP overhaul exemplifies how modernized rules can attract international inflows, provided labs can document global equivalence.

Competitive Landscape

The pharmaceutical analytical testing outsourcing market features a moderately consolidated structure. SGS, Eurofins, and Labcorp are key players, while more than 300 regional providers address niche or local demand. Thermo Fisher’s USD 4.1 billion takeover of Solventum’s purification and filtration unit in 2025 underscores a race to secure advanced bioprocess assets that dovetail with analytical services.

Strategic expansion focuses on biologics capacity and digital quality systems. Eurofins’ AI-ready, cloud-based audit platform shortens vendor-qualification cycles, a critical differentiator for time-pressed biotech. SGS is scaling viral-vector QC in Lincolnshire and Shanghai, addressing shortages flagged by cell-therapy sponsors. Labcorp’s oncology assay acquisition from BioReference Health in March 2025 further fortifies end-to-end cancer-drug analytics.

Mid-tier entrants gain traction by offering boutique expertise—complex carbohydrate analysis, oligonucleotide characterization, or inhalation device testing—often leveraging academic ties or regional grant funding. Still, cyber-resilience and talent attraction remain critical Achilles’ heels, prompting several European independents to form alliances for shared IT security services.

Pharmaceutical Analytical Testing Outsourcing Industry Leaders

SGS SA

Eurofins Scientific

Pace Analytical Services, Inc.

Labcorp

Intertek Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fortrea and Emery Pharma launch rapid MNP impurity testing for rifampin lots, aligning with FDA acceptable-intake limits.

- April 2025: DDL inaugurates a new GMP lab dedicated to drug-device combination product testing, expanding support for injectable delivery systems.

- March 2025: Labcorp closes the purchase of BioReference Health’s oncology testing assets, broadening its specialized cancer diagnostics portfolio.

Global Pharmaceutical Analytical Testing Outsourcing Market Report Scope

Pharmaceutical analytical testing outsourcing encompasses all aspects of the pharmaceutical and therapies manufacturing, testing, and validation processes. This includes verifying pharmaceutical ingredients, compounds, and manufacturing procedures needed for medication development. These outsourcing services are provided by outsourcing companies that are focused on such services.

The pharmaceutical analytical testing outsourcing market is segmented by services (bioanalytical testing, method development and validation, stability testing, and other services), end-user (pharmaceutical and biopharmaceutical companies, contract manufacturing organizations, and other end-users), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Bioanalytical Testing | Clinical |

| Non-clinical | |

| Method Development & Validation | Extractables & Leachables |

| Impurity Methods | |

| Technical Consulting | |

| Stability Testing | Drug Substance |

| Accelerated / Photostability | |

| Other Services |

| Chemistry Testing |

| Microbiological Testing |

| Extractables & Leachables |

| Raw-Material & Excipient Testing |

| Dissolution & Disintegration |

| Other Test Types |

| Discovery & Preclinical |

| Phase I |

| Phase II |

| Phase III |

| Commercial / QC Release |

| Chromatography-Based |

| Mass Spectrometry |

| Spectroscopy (UV/IR/NMR) |

| Cell-Based Bioassays |

| Molecular / Immunoassays (PCR, ELISA) |

| Full-Service CRO |

| Functional Service Provider (FSP) |

| Project-Based (à la carte) |

| Pharmaceutical & Biopharmaceutical Companies |

| Contract Development & Manufacturing Organizations (CDMOs/CMOs) |

| Virtual / Small Biotech |

| Academic & Research Institutes |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Services | Bioanalytical Testing | Clinical |

| Non-clinical | ||

| Method Development & Validation | Extractables & Leachables | |

| Impurity Methods | ||

| Technical Consulting | ||

| Stability Testing | Drug Substance | |

| Accelerated / Photostability | ||

| Other Services | ||

| By Test Type | Chemistry Testing | |

| Microbiological Testing | ||

| Extractables & Leachables | ||

| Raw-Material & Excipient Testing | ||

| Dissolution & Disintegration | ||

| Other Test Types | ||

| By Phase | Discovery & Preclinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Commercial / QC Release | ||

| By Technology Platform | Chromatography-Based | |

| Mass Spectrometry | ||

| Spectroscopy (UV/IR/NMR) | ||

| Cell-Based Bioassays | ||

| Molecular / Immunoassays (PCR, ELISA) | ||

| By Outsourcing Model | Full-Service CRO | |

| Functional Service Provider (FSP) | ||

| Project-Based (à la carte) | ||

| By End-User | Pharmaceutical & Biopharmaceutical Companies | |

| Contract Development & Manufacturing Organizations (CDMOs/CMOs) | ||

| Virtual / Small Biotech | ||

| Academic & Research Institutes | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the pharmaceutical analytical testing outsourcing market?

The market is valued at USD 10.27 billion in 2026 and is projected to reach USD 15.09 billion by 2031.

Which service segment generates the highest revenue?

Bioanalytical testing leads with 43.78% share in 2025 and is also the fastest-growing segment at a 12.56% CAGR.

Why are extractables & leachables tests gaining momentum?

Stricter USP 1663/1664 requirements and the surge in biologics packaging drive an 10.95% CAGR for this test type.

How will the US BIOSECURE Act affect outsourcing strategies?

US sponsors receiving federal funds must phase out Chinese lab partnerships by 2032, prompting diversification toward India, Southeast Asia, and domestic providers.

What advantages do functional service provider models offer sponsors?

FSP models give flexibility and cost control by letting sponsors outsource specific functions—such as method validation—without committing to full-service contracts.

Which region is growing fastest, and why?

Asia-Pacific is expanding at 10.12% CAGR, buoyed by regulatory convergence, expanding manufacturing capacity, and competitive cost structures.

Page last updated on: