PH Meters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 787.96 Million |

| Market Size (2031) | USD 992.84 Million |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

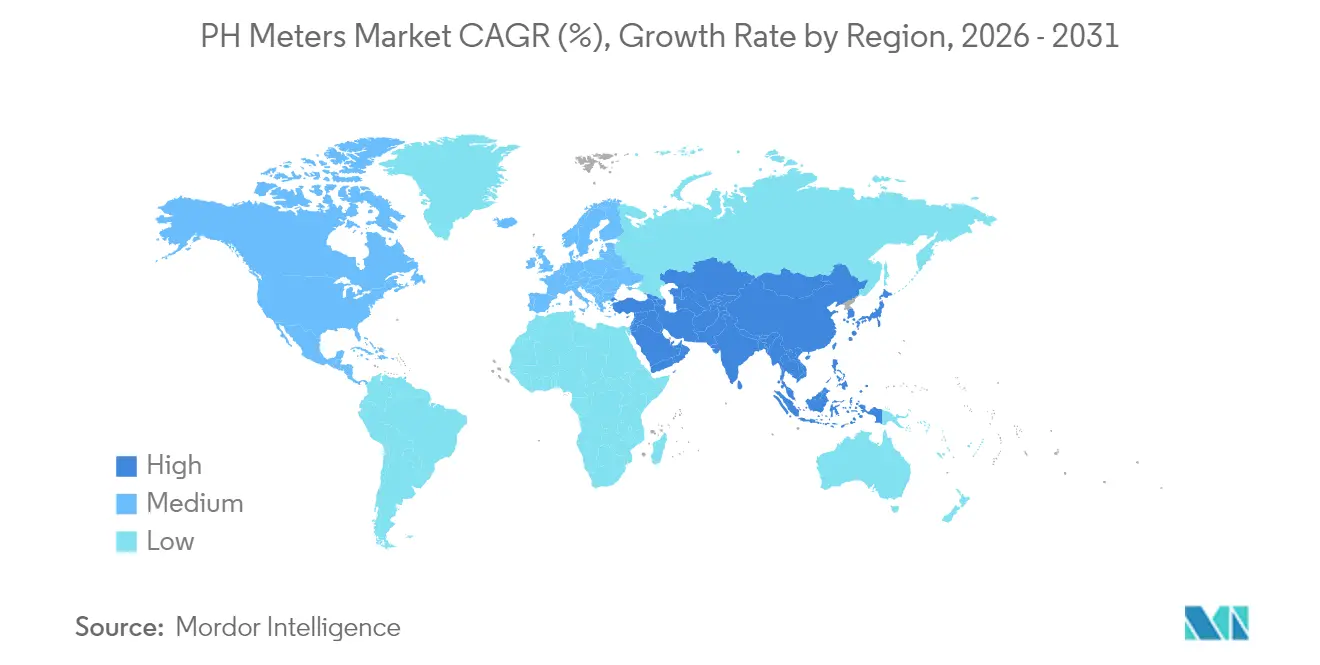

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PH Meters Market Analysis by Mordor Intelligence

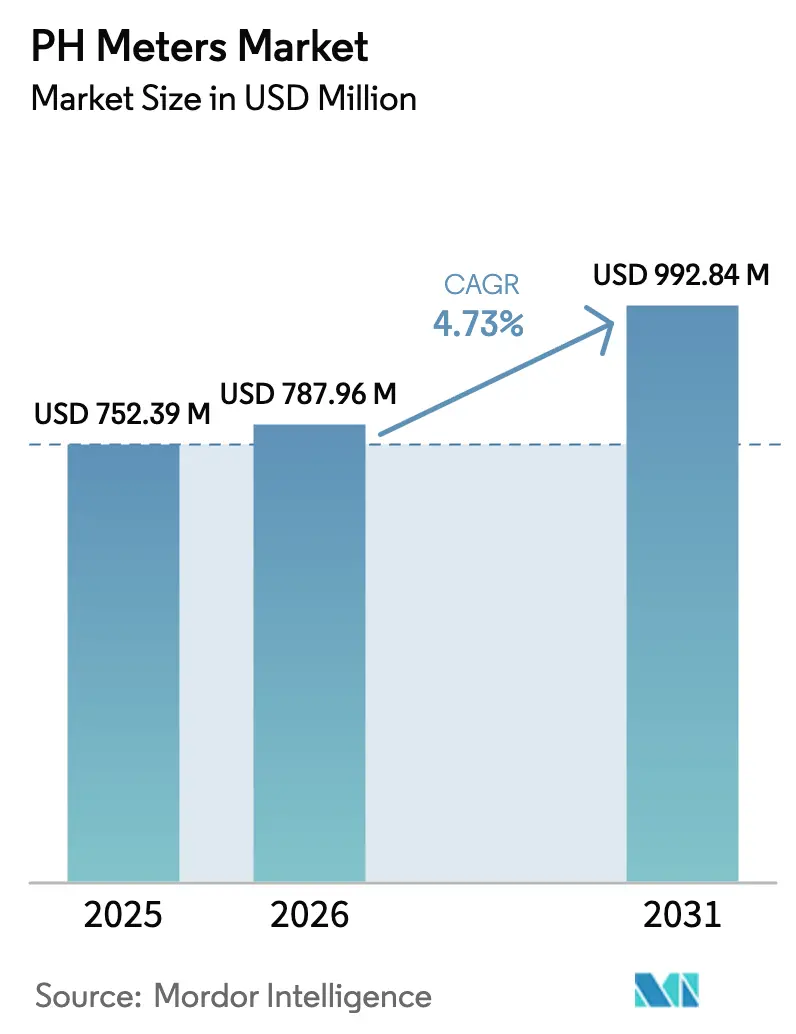

The pH meters market size was valued at USD 752.39 million in 2025 and estimated to grow from USD 787.96 million in 2026 to reach USD 992.84 million by 2031, at a CAGR of 4.73% during the forecast period (2026-2031). Rising regulatory stringency in food safety, expansion of precision agriculture, and industrial digitalization underpin this growth trajectory as users demand faster, more accurate, and connected pH measurement solutions. Smart sensor integration, exemplified by Bluetooth-enabled probes and cloud dashboards, supports real-time analytics and predictive maintenance, boosting operational efficiency across manufacturing and water treatment plants. The adoption of solid-state ISFET technology is accelerating because these sensors offer glass-free operation and better durability in clean-in-place cycles, challenging the entrenched position of glass electrodes. Asia-Pacific’s rapid industrialization and large-scale water infrastructure programs augment the global pH meters market by creating sizeable procurement pipelines for municipal utilities and private operators.

Key Report Takeaways

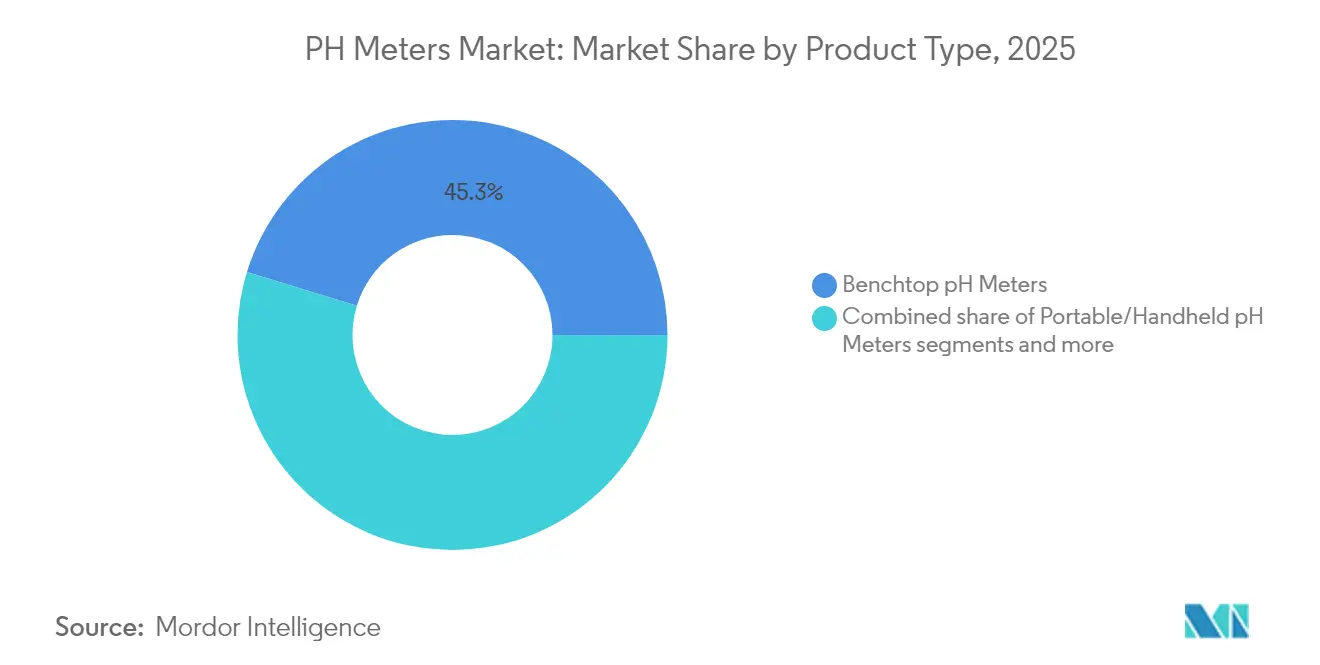

- By product type, benchtop instruments held 45.27% of the pH meters market share in 2025 while smart/IoT-enabled units, aided by Industry 4.0 adoption, expand at 5.07% CAGR through 2031.

- By form factor, glass electrodes accounted for 66.85% share of the pH meters market size in 2025 and solid-state ISFET sensors are forecast to progress at a 5.32% CAGR to 2031.

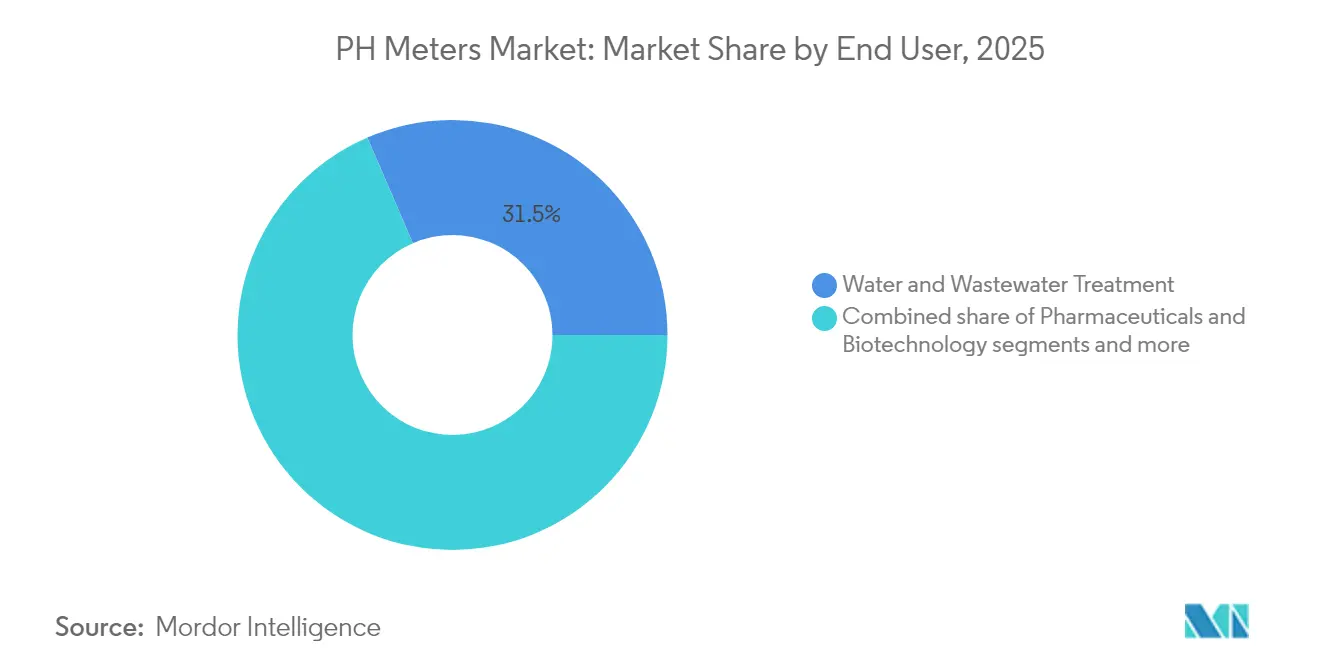

- By end-user industry, water and wastewater treatment commanded 31.48% of the pH meters market size in 2025 whereas agriculture is set to grow the fastest at 5.63% CAGR owing to precision-farming investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global PH Meters Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption in precision agriculture | +0.8% | APAC & North America | Medium term (2-4 years) |

| Expansion of water & wastewater treatment | +1.2% | APAC emerging markets | Long term (≥ 4 years) |

| Stringent food-safety pH regulations | +0.6% | North America & EU | Short term (≤ 2 years) |

| Rapid growth of at-home healthcare diagnostics | +0.4% | North America & EU | Medium term (2-4 years) |

| AI-enabled inline pH monitoring | +0.3% | Global | Long term (≥ 4 years) |

| Demand in battery-recycling leach processes | +0.2% | Battery hubs worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption in Precision Agriculture

Smart soil sensors relay real-time pH readings across vast fields, allowing variable-rate fertilizer dosing that improves nutrient uptake and lowers input costs . Cloud-based dashboards synthesize these data streams with weather and satellite imagery to guide agronomic decisions that raise yields and reduce environmental runoff . Agricultural service providers bundle pH analytics with crop-health alerts, converting raw data into actionable insights for growers. Governments in India, China, and the United States subsidize precision-farming equipment, thereby accelerating procurement of connected pH probes . As climate-resilient farming gains momentum, accurate pH control will remain pivotal to soil remediation and carbon-sequestration programs .

Expansion of Water & Wastewater Treatment Infrastructure

India’s water-treatment spend is forecast to top USD 18 billion by 2026, prompting sizable tenders for inline pH analyzers in desalination, industrial effluent, and municipal reuse projects. Utilities adopt AI-driven pH-control loops that lower chemical overfeed, cut energy use, and lengthen sensor life. Smart meters with built-in diagnostics reduce unplanned downtime, a key KPI for public-private partnership (PPP) operators. In North America, water districts report 31% reduced aeration costs after deploying machine-learning pH optimization, underscoring the financial case for digital upgrades. The shift from sulfuric acid to CO₂-based neutralization further raises demand for high-accuracy probes that can withstand rapid pH swings without recalibration

Stringent Food-Safety pH Regulations

U.S. regulations stipulate pH < 4.6 in acidified foods, making potentiometric measurement mandatory at critical control points. Plants integrate continuous pH monitoring with HACCP software to obtain real-time compliance dashboards for auditors. Modern probes auto-calibrate and run self-diagnostics, reducing labor and lowering the risk of product recalls. Global brands harmonize with EU and Codex standards, spreading advanced pH compliance tools from North America into APAC contract-manufacturing hubs. Markets for disposable food-contact electrodes rise as ready-to-eat categories proliferate and shelf-life targets extend.

AI-Enabled Inline pH Monitoring for Smart Factories

Digital pH sensors feed edge gateways that employ machine-learning models to forecast probe drift days in advance, trimming unscheduled process stoppages. Chemical plants gain up to 30% sensor-life improvements after switching to predictive maintenance protocols embedded in enterprise asset-management suites. Digital-twin replicas of batch reactors continuously ingest pH data to optimize reagent dosing and heat balance, raising throughput and lowering scrap. Multi-protocol transmitters (HART, Profibus DP, Ethernet-IP) facilitate seamless integration with distributed control systems, ensuring data liquidity across the factory floor. As sustainability metrics gain board-level visibility, inline pH control helps reduce chemical waste and improve ESG scores.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Calibration drift causing inaccuracy | -0.7% | Global | Short term (≤ 2 years) |

| Price pressure from low-cost Asian imports | -0.5% | Global | Medium term (2-4 years) |

| Scarcity of glass-electrode raw materials | -0.3% | Global | Long term (≥ 4 years) |

| Lack of skilled operators in emerging economies | -0.4% | APAC & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Calibration-Drift Causing Measurement Inaccuracy

Glass electrodes lose sensitivity as reference electrolyte depletes, triggering frequent recalibrations that raise operating costs and risk non-compliance. Temperature swings further distort readings, especially in high-purity water lines where low ionic strength amplifies error. Plants increasingly specify digital probes with built-in temperature compensation and calibration timers to mitigate drift. ISFET sensors reduce drift but may suffer from chemical fouling in aggressive media, necessitating dedicated cleaning cycles. Overall, predictive diagnostics that alert technicians before accuracy degrades offer a viable path to minimize downtime.

Price Pressure from Low-Cost Asian Imports

Handheld testers priced below USD 50 flood online marketplaces, eroding margins for premium brands in hobbyist and light-industrial segments. Although these devices often carry ±0.2 pH accuracy ratings, they remain unsuitable for pharmaceutical and food applications that require ±0.01 pH tolerance. Leading vendors counter by bundling calibration solutions, cloud analytics, and multiyear warranties to sustain a value-based premium. OEM partnerships with automation firms create integrated packages that low-cost suppliers struggle to replicate. Nevertheless, price-based competition will persist in resource-constrained regions where capital budgets remain tight [INSTRUMENTCHOICE.COM.AU]().

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Integration Drives Innovation

Smart/IoT-enabled instruments account for the fastest expansion at 5.07% CAGR as enterprises link edge analytics to MES and ERP platforms for end-to-end visibility of the pH meters market. Benchtop units continue to dominate laboratory workflows thanks to multi-parameter capabilities and high-resolution displays, retaining 45.27% share of the pH meters market size in 2025. Field inspectors leverage rugged handhelds for immediate water-quality assessments in environmental monitoring and aquaculture. Inline analyzers integrate with process control valves, allowing closed-loop pH adjustment that minimizes reagent use in chemical neutralization lines. As cloud-native firmware updates become standard, cybersecurity certifications (IEC 62443) gain importance in procurement criteria .

Laboratories increasingly demand units capable of simultaneous pH, conductivity, and ORP analysis, streamlining workflows and reducing bench-space utilization. In the pH meters market, subscription-based software that automates compliance logbooks offers recurring revenue to manufacturers . Portable kits with Bluetooth connectivity transmit GPS-tagged readings to centralized dashboards, enhancing audit trails for environmental agencies . Digital twin integrations help R&D chemists visualize titration curves in real time, accelerating formulation iterations. The wave of smart adoption underscores how connectivity reshapes the competitive dynamics of the pH meters industry.

By Form Factor: ISFET Technology Challenges Glass Dominance

Glass electrodes held 66.85% of the pH meters market share in 2025 due to their proven accuracy and wide chemical compatibility . ISFET solid-state probes, free of fragile glass, advance at 5.32% CAGR as contamination risks in food and biotech prompt demand for unbreakable alternatives . Alkali-stable gate materials now survive caustic CIP cycles, extending service life in dairy plants and vaccine fermenters . Hybrid probes merge an ISFET sensor with an integrated reference electrode, narrowing the accuracy gap while retaining robustness. Manufacturers deliver factory-calibrated ISFET cartridges that snap into transmitters without field wet-conditioning, slashing installation time .

Despite innovation, glass remains favored in ultrapure water (UPW) loops where legacy standards prescribe glass-based measurement. Anti-breakage coatings and reinforced bulb geometries improve durability without compromising response times. Hall-effect RFID chips embedded in new-generation glass probes track usage cycles and exposure to high-temperature sterilization, informing replacement schedules . Mass-production efficiencies continue to keep glass probe ASPs lower than ISFET, sustaining their prevalence in cost-sensitive verticals. A dual-portfolio approach emerges whereby suppliers offer both form factors to address diverse accuracy, robustness, and price points in the pH meters market.

By End-User Industry: Agriculture Accelerates Growth

Water and wastewater treatment captured 31.48% of the pH meters market size in 2025 as utilities mandated 24/7 inline monitoring for effluent compliance . Meanwhile, the agricultural sector is poised to post 5.63% CAGR given farmer adoption of soil mapping and variable-rate liming in high-value crops. Chemical and petrochemical operators embed pH probes in neutralization pits to prevent acid corrosion, anchoring steady replacement demand . Pharmaceutical manufacturers integrate digital pH analytics in single-use bioreactors to maintain narrow process windows during biologics production.

Food and beverage processors use continuous pH control to fine-tune fermentation, stabilize flavor profiles, and meet shelf-life targets dictated by regulators . Environmental agencies deploy multiparameter sondes that include pH, turbidity, and dissolved oxygen to automate river-health reporting. Point-of-care diagnostics leverage micro-pH sensors within disposable cartridges to assist clinical staff in rapid blood-gas analysis, broadening healthcare adoption. Battery recyclers monitor leachate pH to optimize lithium extraction, offering a new niche opportunity in the circular-economy supply chain . This breadth of applications stimulates continuous innovation across the pH meters industry.

Geography Analysis

North America commanded 41.78% share of the pH meters market in 2025, buoyed by stringent EPA and FDA mandates and a dense install base across chemical, biotech, and food sectors . Industrial retrofits in the United States and Canada increasingly favor digital probes with predictive diagnostics to reduce maintenance budgets . Public funding streams, including the Infrastructure Investment and Jobs Act, channel capital toward water-quality upgrades that stipulate high-accuracy pH monitoring.

Asia-Pacific exhibits the fastest 5.93% CAGR through 2031, fueled by India’s massive water-treatment build-out and China’s industrial modernization policies that elevate process-control standards . OEMs often tailor low-maintenance, splash-proof designs for Southeast Asian aquaculture, where brackish-water pH stability directly impacts shrimp yields . Japan and South Korea prioritize lab-grade accuracy in semiconductor fabs, generating orders for high-resolution benchtop meters with ±0.001 pH precision .

Europe presents a mature yet steady landscape, with REACH and Food Hygiene regulations preserving baseline demand for compliant probes in chemical and dairy plants . The continent’s Green Deal pushes circular-economy initiatives, sparking investments in battery-recycling facilities that require advanced leach-process pH control . Latin America and the Middle East & Africa remain nascent but attractive; desalination programs in Saudi Arabia and wastewater concessions in Brazil introduce new tenders for process pH analyzers . Distributed manufacturing and localized food processing bolster incremental demand across emerging geographies, ensuring that the pH meters market retains a truly global footprint .

Competitive Landscape

The pH meters market is moderately fragmented, with top players offering holistic suites that combine sensors, calibration services, and cloud analytics to maintain stickiness . Mettler-Toledo’s Intelligent Sensor Management embeds RFID chips and onboard memory to log calibration data, enabling true plug-and-measure capability . Thermo Fisher Scientific strengthens its value proposition via bundled reagents and global technical-support centers that expedite troubleshooting. Xylem touts an enhanced online selector for pH electrodes that simplifies decision-making and drives e-commerce sales, catering to small-volume buyers.

Regional brands such as HORIBA and Eutech Instrument push competitiveness through localized production and multilingual firmware tailored to Asian markets[2]Source: HORIBA, “HORIBA Report 2023-2024,” horiba.com . Endress+Hauser differentiates with Heartbeat Technology, offering continuous health checks and SIL-compliant documentation critical to pharmaceuticals and chemicals. Entry-level Chinese and Indian manufacturers intensify price competition in handheld categories, pressing incumbents to emphasize total cost of ownership over sticker price.

Strategic partnerships flourish between probe OEMs and industrial IoT platforms; for instance, pH data streams feed Rockwell Automation’s FactoryTalk Analytics for holistic process insights. M&A activity centers on complementary software assets that enhance AI-driven predictive maintenance, evidenced by recent acquisitions of data-analytics startups by top-tier instrumentation firms . Overall, competitive dynamics will hinge on digital-service depth and application-specific expertise rather than purely on hardware differentiation.

PH Meters Industry Leaders

Danaher Corporation

Hanna Instruments

Thermo Fisher Scientific Corporation

PerkinElmer Inc.

Metrohm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Virginia Cooperative Extension released guidance for calibrated pH measurements in farmers-market acidified foods .

- February 2024: HORIBA unveiled its MLMAP2028 plan targeting JPY 450 billion in sales and new pH sensor production lines by 2026

Global PH Meters Market Report Scope

As per the scope of the report, a pH meter is an electric device used to measure hydrogen-ion activity (acidity or alkalinity) in solution. Fundamentally, a pH meter consists of a voltmeter attached to a pH-responsive electrode and a reference electrode. The pH market is segmented into product type, application, and geography. By product type, the market is segmented into benchtop pH meters, portable pH meters, and continuous pH meters. By application, the market is segmented into the pharmaceutical industry, biopharmaceutical industry, diagnostic centers, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America). The report offers the value (in USD) for the above segments.

| Benchtop pH Meters |

| Portable/Handheld pH Meters |

| Inline/Process pH Analyzers |

| Smart/IoT-Enabled pH Meters |

| Glass-Electrode |

| ISFET (Solid-State) |

| Water & Wastewater Treatment Plants |

| Food & Beverage Processing |

| Chemical & Petrochemical |

| Pharmaceuticals & Biotechnology |

| Environmental Monitoring & Research Labs |

| Agriculture |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Benchtop pH Meters | |

| Portable/Handheld pH Meters | ||

| Inline/Process pH Analyzers | ||

| Smart/IoT-Enabled pH Meters | ||

| By Form Factor | Glass-Electrode | |

| ISFET (Solid-State) | ||

| By End-User Industry | Water & Wastewater Treatment Plants | |

| Food & Beverage Processing | ||

| Chemical & Petrochemical | ||

| Pharmaceuticals & Biotechnology | ||

| Environmental Monitoring & Research Labs | ||

| Agriculture | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the PH Meters Market?

The PH Meters Market size is expected to reach USD 787.96 million in 2026 and grow at a CAGR of 4.73% to reach USD 992.84 million by 2031.

What is the current PH Meters Market size?

In 2026, the PH Meters Market size is expected to reach USD 787.96 million.

Who are the key players in PH Meters Market?

Danaher Corporation, Hanna Instruments, Thermo Fisher Scientific Corporation, PerkinElmer Inc. and Metrohm are the major companies operating in the PH Meters Market.

Which is the fastest growing region in PH Meters Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031) at 5.93%.

Which region has the biggest share in PH Meters Market?

In 2025, the North America accounts for the largest market share in PH Meters Market at 41.78%.

What years does this PH Meters Market cover, and what was the market size in 2025?

In 2025, the PH Meters Market size was estimated at USD 787.96 million. The report covers the PH Meters Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the PH Meters Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: